Housing Market Updates

Exploring the Future of Mortgage Rates: What Homebuyers Need to Know

For those embarking on the journey to buy a home this year, mortgage rates are likely a top-of-mind concern. It’s no surprise since these rates have a significant impact on what you can afford when securing a home loan. In a housing market where affordability is a pressing issue, it’s a good time to take a step back and analyze the broader historical context of mortgage rates in comparison to their present state. Furthermore, delving into their connection with inflation can provide valuable insights into the potential trajectory of mortgage rates in the near future.

Putting Sticker Shock into Perspective

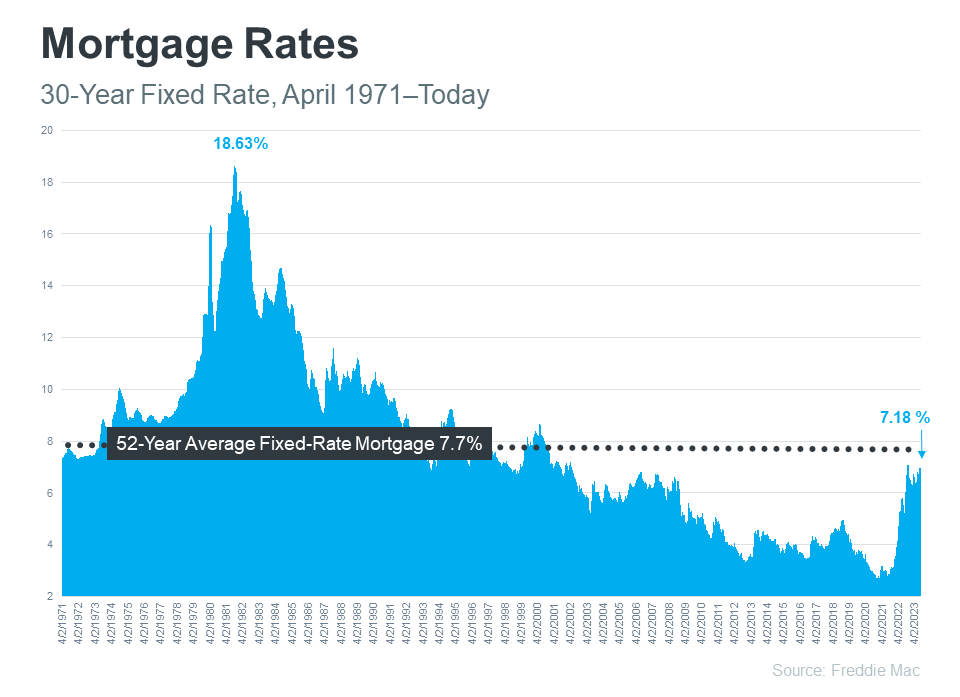

Freddie Mac has been diligently tracking the 30-year fixed mortgage rate since April of 1971. On a weekly basis, they publish the results of their Primary Mortgage Market Survey, which amalgamates mortgage application data from lenders across the nation (refer to the graph below):

Examining the right side of the graph, it becomes apparent that mortgage rates have seen a notable increase since the onset of the previous year. However, even with this upswing, today’s rates still linger below the 52-year average. While this historical context is informative, most homebuyers have grown accustomed to mortgage rates hovering between 3% and 5%—a range that has prevailed for the past 15 years.

This familiarity with lower rates elucidates why the recent surge might be causing sticker shock, even though rates are, by historical standards, near their long-term average. While many buyers have adapted to the higher rates that have persisted over the past year, a slight dip in rates would certainly be a welcome development. To ascertain the feasibility of this, it is crucial to factor in the variable of inflation.

Where Might Mortgage Rates Head in the Future?

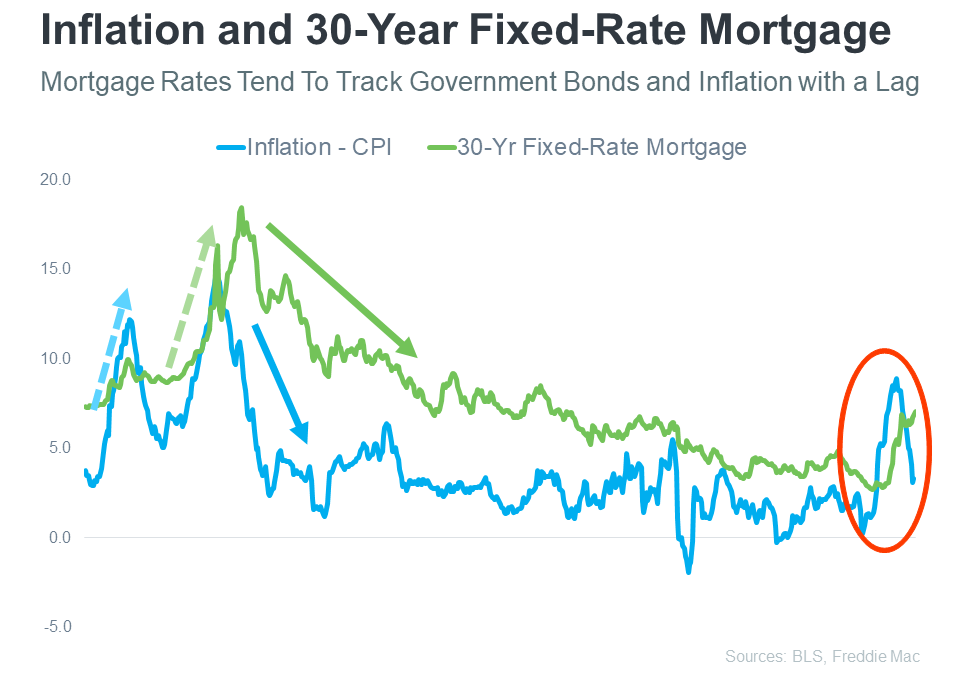

The Federal Reserve has been diligently engaged in efforts to quell inflation since the early part of 2022. This holds significance because, historically, there has been a discernible link between inflation and mortgage rates (refer to the graph below):

The graph vividly illustrates a fairly consistent relationship between inflation and mortgage rates. On the left side of the graph, each significant shift in inflation (highlighted in blue) is closely followed by a corresponding adjustment in mortgage rates (depicted in green).

The circled segment of the graph draws attention to the recent inflation surge, with mortgage rates showing a concurrent response. While inflation has shown signs of moderating somewhat this year, mortgage rates have not mirrored the same pattern.

Consequently, if history offers any guidance, it implies that the market is awaiting a scenario in which mortgage rates align with the trajectory of inflation and begin to recede. While it’s impossible to make precise predictions regarding mortgage rates, the evidence suggests that moderating inflation could portend a forthcoming dip in mortgage rates, consistent with a well-established trend.

In Conclusion

In order to gauge the potential path of mortgage rates, it is instructive to examine their historical journey. There exists a clear, proven correlation between inflation and mortgage rates, and if this historical link remains valid, the recent moderation in inflation might bode well for the future of mortgage rates and your aspirations of homeownership.

You must be logged in to post a comment Login