For Buyers

The New Spring Real Estate Market is Here. Are You Ready?

Mortgage rates have been volatile lately. And if you’re thinking about buying a home, that can make it harder to plan. But there are still things you can do to get the best rate possible in today’s market. It starts with having the right information.

So, what’s causing the bumps in rates? And what can you do about it? Let’s break it down.

Mortgage Rate Volatility Is Normal

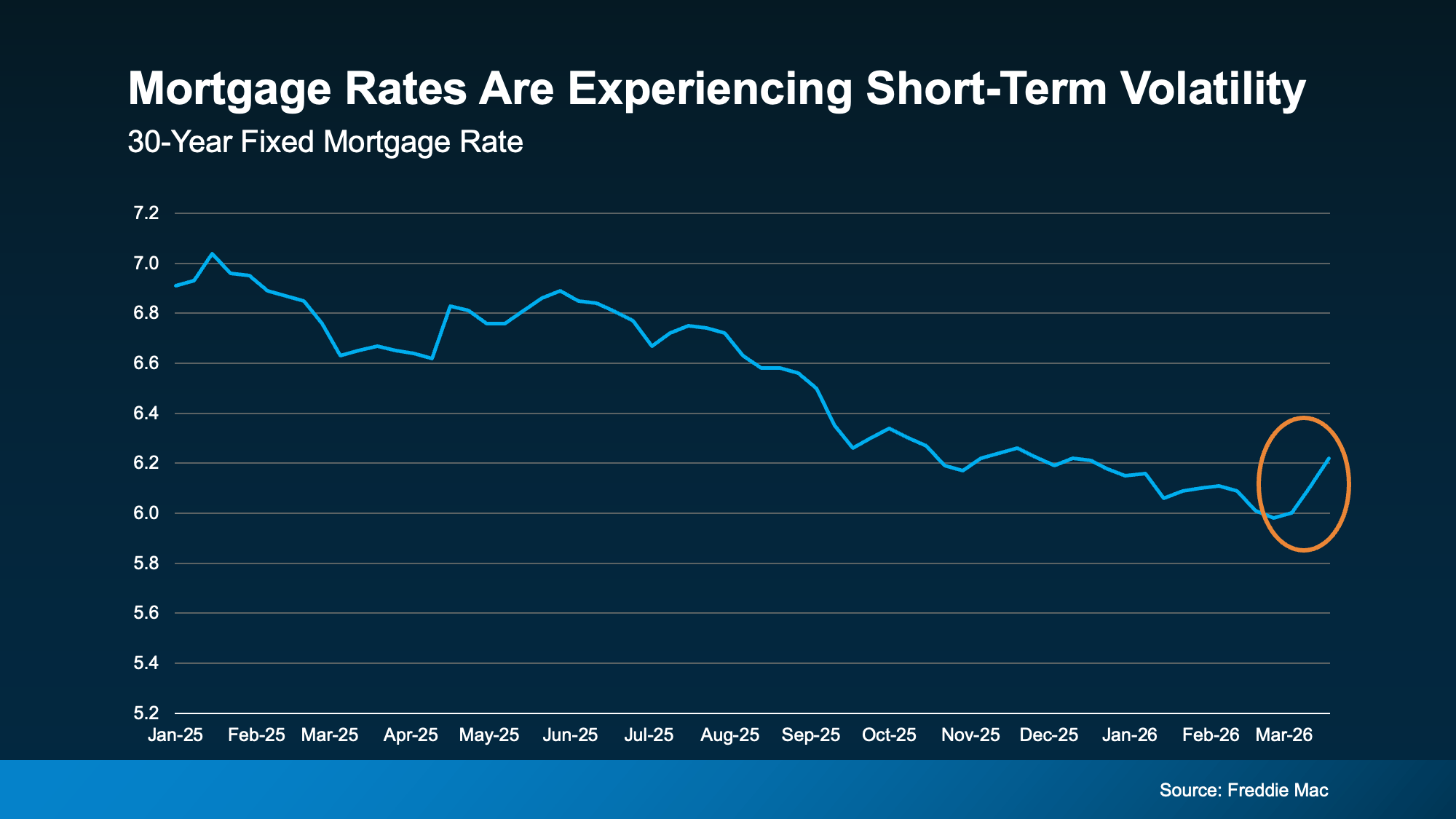

Data from Freddie Mac shows the recent volatility. After trending down for well over a year, there was a rise this month (see graph below):

While it’s easy to be distracted by the changes, here’s what you need to remember.

It’s normal for rates to bounce around a bit here and there. For example, if you look back at the graph, you’ll see that even within the past year there have been times like this when rates inched up. We’re in one of those moments right now and you need to be aware of that.

Especially when there’s economic uncertainty or big global events happening, volatility like this is expected. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

And that’s one of the reasons why trying to time the market isn’t a wise move.

You can’t control what happens with mortgage rates. But there are still things you can do to help you get the best rate possible in today’s market. And here’s where to focus your effort.

Your Credit Score

Your credit score plays a big role in the rate you qualify for. Even a small improvement can make a noticeable difference in your monthly payment. As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

So, make sure you do what you can to keep your credit score up. If you’re not sure what your score is or how you can improve it, talk to a trusted loan officer.

Your Loan Type

There are also different types of home loans – and each one can have unique requirements, benefits, and rates for qualified buyers. The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

That’s why it’s so important to explore your options with a lender. You may even want to talk to multiple lenders to see how the options vary.

Your Loan Term

The length of your loan matters too. Most lenders typically offer 15, 20, or 30-year loans. Freddie Mac offers this advice:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Again, to figure out what makes the most sense for your budget and long-term goals, have a lender walk you through all your options.

Bottom Line

Thinking about buying right now? The best advice is to accept that you can’t control where rates are going to go from here.

What you can do is work with a trusted lender and take steps that’ll help you get the best rate possible.

So, if you want to move today, talk to an agent and a lender to make it happen. You just need to control the controllables and focus where it counts.

For the past few years, affordability has been what’s stopped a lot of buyers in their tracks. Maybe it stopped you, too.

At some point you probably did the math, looked at the monthly payment, and decided to pause your search and wait for things to get better. But here’s something you may have missed while you’ve been sitting on the sidelines.

Over the last year, housing affordability has improved in all 50 states. Yes, you read that right. It’s gotten better in every single state.

That’s based on new research coming out of First American. And while housing is still fairly expensive compared to historical standards, the pressure buyers felt over the last few years is finally starting to ease.

Some Areas Are Seeing Bigger Improvements

The first thing you need to know is that this isn’t just happening in one region or in a small handful of cities. The trend is happening almost everywhere.

Sure, individual states, cities, and even neighborhoods are going to vary – sometimes by a lot. But overall, more buyers are able to buy again. And in 48 of the top 50 metros, affordability has improved over the past year.

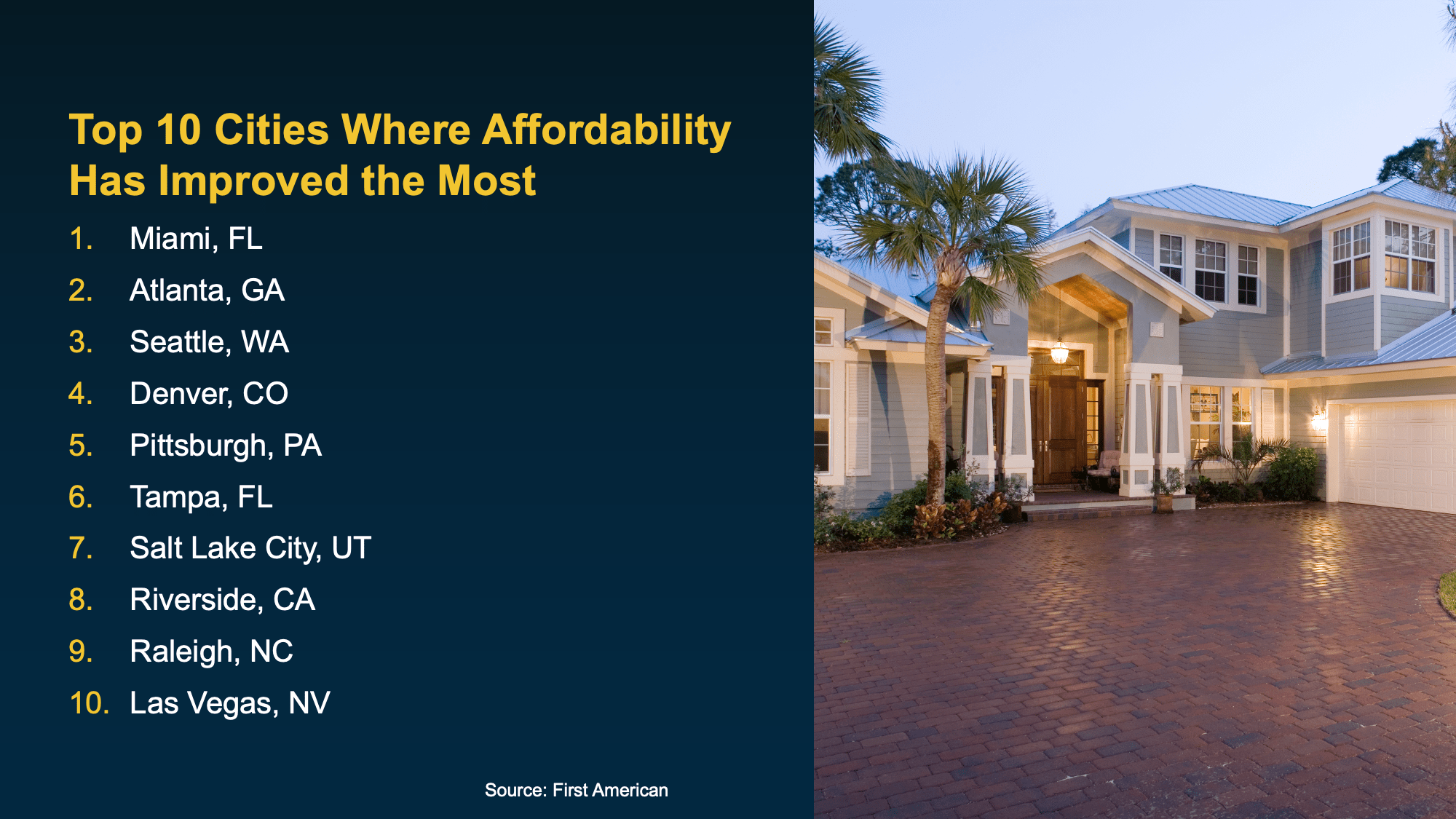

That same research breaks down which cities are seeing the biggest gains:

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

When buyers have more choices, it creates a healthier balance in the market and that can help bring affordability back within reach. With homes up for grabs, it opens the door a bit wider for buyers to negotiate with sellers for credits, price cuts, and more. And it gives you more chances to find a house that works for your needs and budget.

It may make more of a difference than you think.

None of this means affordability challenges have completely disappeared. Buying a home is still a big financial decision. But the trend is moving in a direction many buyers have been waiting for.

As Chen Zhao, Head of Economic Research at Redfin, puts it:

“The housing affordability crisis is showing signs of easing . . . opening the door for more Americans to make the jump to homeownership.”

Bottom Line

If you were holding off on buying, this could be exactly the signal you’ve been waiting so long for. To find out how much affordability’s improved in your area, connect with a local real estate agent.

Foreclosures are ticking up. And that may make your mind jump straight to thoughts of 2008 – specifically to what happened to the market during the housing crash. So, let’s do exactly what your brain already wants to do, and see if there’s any connection there.

The simple truth is foreclosure filings are rising. But they’re nowhere near crisis levels. And that’s not where they’re headed either. Here’s why.

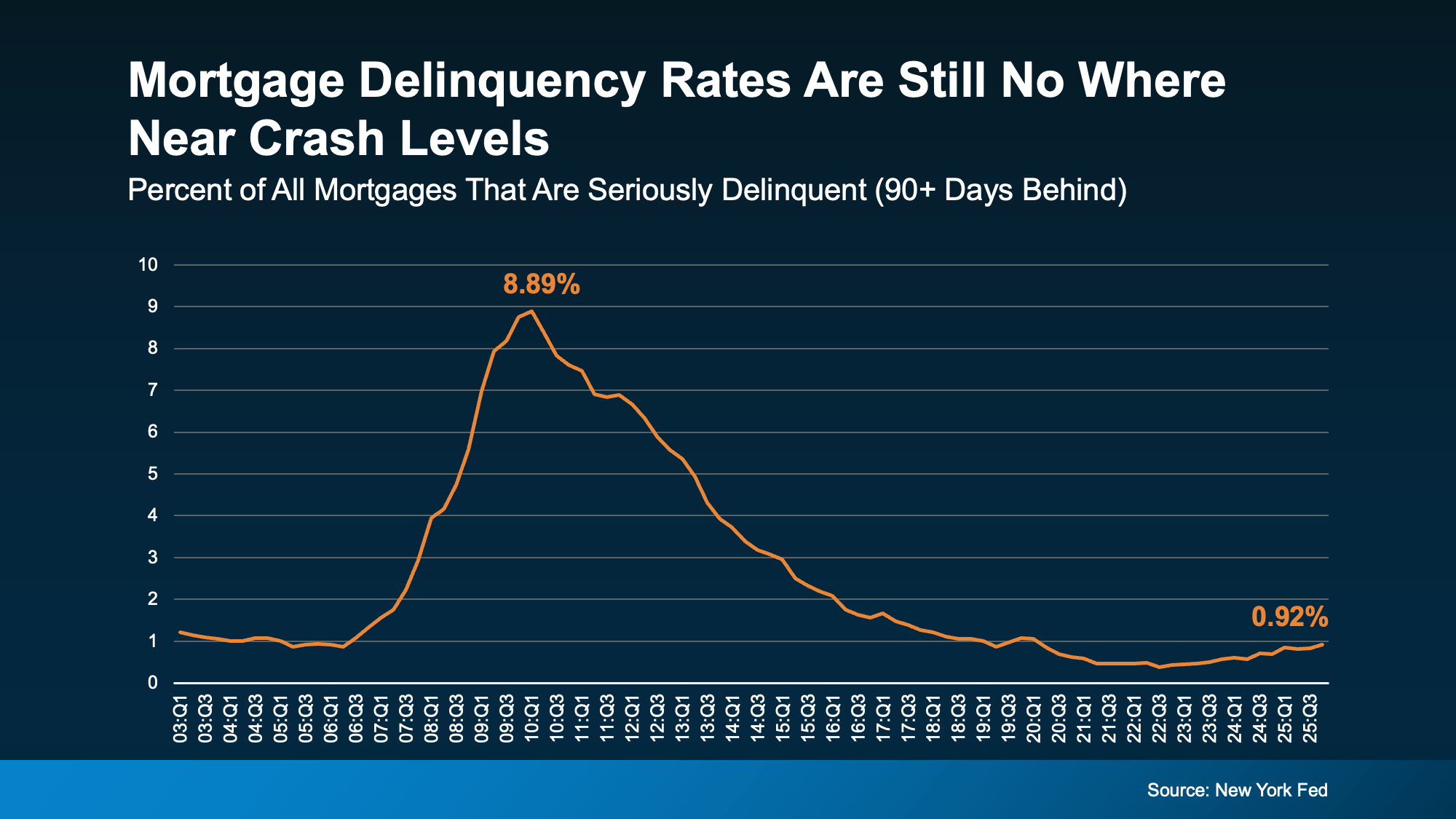

Take a look at serious delinquencies – loans where the homeowner is more than 90 days late on their mortgage payments.

While those have increased slightly, data from the New York Fed shows they still remain low. And they aren’t anywhere close to levels seen when the market crashed (see graph below):

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

In the years around the crash, they were up around 9%. That’s 1 in 11.

That’s a big difference.

And it’s important to remember not all delinquencies even become foreclosure filings. Some homeowners who are falling behind will work out repayment plans with their banks and lenders because banks don’t want to see a wave of foreclosures either.

That’s why foreclosure numbers are even lower than delinquencies. ATTOM shows only 0.3% of all homes are currently going through a foreclosure filing. And those won’t even all go to a full foreclosure. That’s not a wave. That’s a ripple at most.

If People Are Falling Behind on Payments, Why Aren’t There Even More Foreclosures?

And maybe you’re wondering, if people are struggling financially, why aren’t there more foreclosures? Here’s the easiest way to answer that.

When households feel financial pressure, they tend to prioritize their mortgage payment above almost everything else. Because the last thing they want to lose is their home.

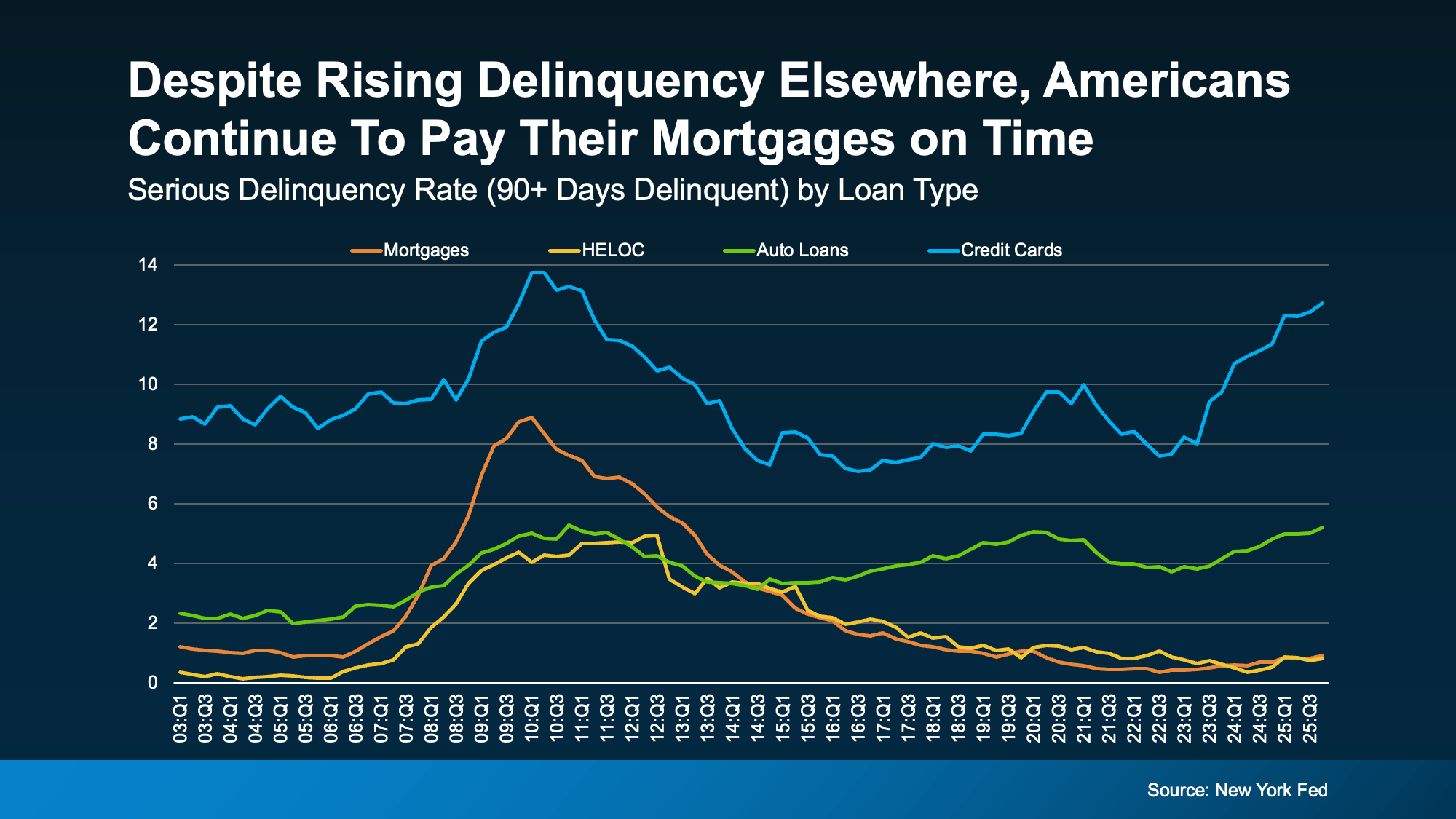

Data from the New York Fed shows serious delinquencies have risen more for credit cards and auto loans (the blue and green lines). But mortgage delinquencies and home equity lines of credit (borrowing against the value of your home) aren’t seeing the same big uptick (the yellow and orange lines). They’re a lot more stable overall.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

Home Equity Changes Everything

Many people have built significant equity over the past several years. And that creates options. As Daren Blomquist, VP of Market Economics at Auction.com, explains:

“Distressed homeowners… many times they still have equity in their homes. There’s an opportunity for them to sell that home, avoid foreclosure, and walk away with equity.”

That’s a major difference from 2008. Back then, many homeowners owed more than their homes were worth. And selling wasn’t an easy solution. Today, for many people, it is. And even in situations where equity isn’t enough, homeowners are encouraged to contact their loan servicer early to explore alternatives to foreclosure.

Bottom Line

Are foreclosure filings rising slightly? Yes. Are they anywhere near crash territory? No. And homeowners today have far more equity and flexibility than they did during the crash.

If you’re concerned about what you’re seeing in the headlines, the best move isn’t panic, it’s perspective. And the data right now says this isn’t 2008 all over again.

The Best Week To List Your House Is Just Around the Corner

You Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

The Remodel You’ve Been Dreaming About May Be Closer Than You Think

-

For Sellers4 weeks ago

For Sellers4 weeks agoSpring Sellers Have an Edge. Here’s Why.

-

Downsize4 weeks ago

Downsize4 weeks agoThe Hidden Advantage Repeat Buyers Have Right Now

-

Equity4 weeks ago

Equity4 weeks agoAre Home Prices Dropping? Here’s the Real Story.

-

Agent Value3 weeks ago

Agent Value3 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability3 weeks ago

Affordability3 weeks agoShould You Wait for Lower Rates?

-

For Buyers3 weeks ago

For Buyers3 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

-

Agent Value2 weeks ago

Agent Value2 weeks agoThe #1 Reason Buyers Walk Away (And How To Get Ahead of It)

-

Affordability2 weeks ago

Affordability2 weeks agoAffordability Has Improved in All 50 States

You must be logged in to post a comment Login