For Sellers

The Secret To Selling This Spring: Start the Prep Work Now

Spring is the busiest season in the housing market. It’s the time of year when buyers are most active – that means it’s when homes sell faster and for top dollar. If you’ve already got a move on your mind, why not list this spring and take advantage of the added buyer demand?

Since spring is just around the corner, now’s the time to start getting your house market-ready. You’ve got just over a month to do the prep work. And while that may sound like a decent amount of time, it’s going to go by quickly. And you won’t want to rush through this important task – especially this year.

The Right Repairs Will Matter More This Spring

Right now, two things are true. There are more homes on the market than there have been in years. And buyers are being extra selective. That combination means you need to invest some time and effort in making strategic repairs. And many homeowners already have a jump on this work.

In the 2025 Outlook for Home Remodeling, Carlos Martin, Director of the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University, explains:

“. . . homeowners are slowly but surely expanding the pace and scope of projects compared to the last couple years.”

And the most common projects they’re tackling are replacing water heaters, HVAC units, and flooring. Energy efficiency is a key consideration too, based on home improvement data from the Census.

What To Prioritize as You Plan Ahead

But just because that’s what other homeowners are doing, it doesn’t mean that’s what you have to tackle. Think about what you’d want to see if you were a buyer. Focus on quick wins that are easy to knock out with the time you have – but, don’t ignore key repairs, especially ones you think could turn off buyers.

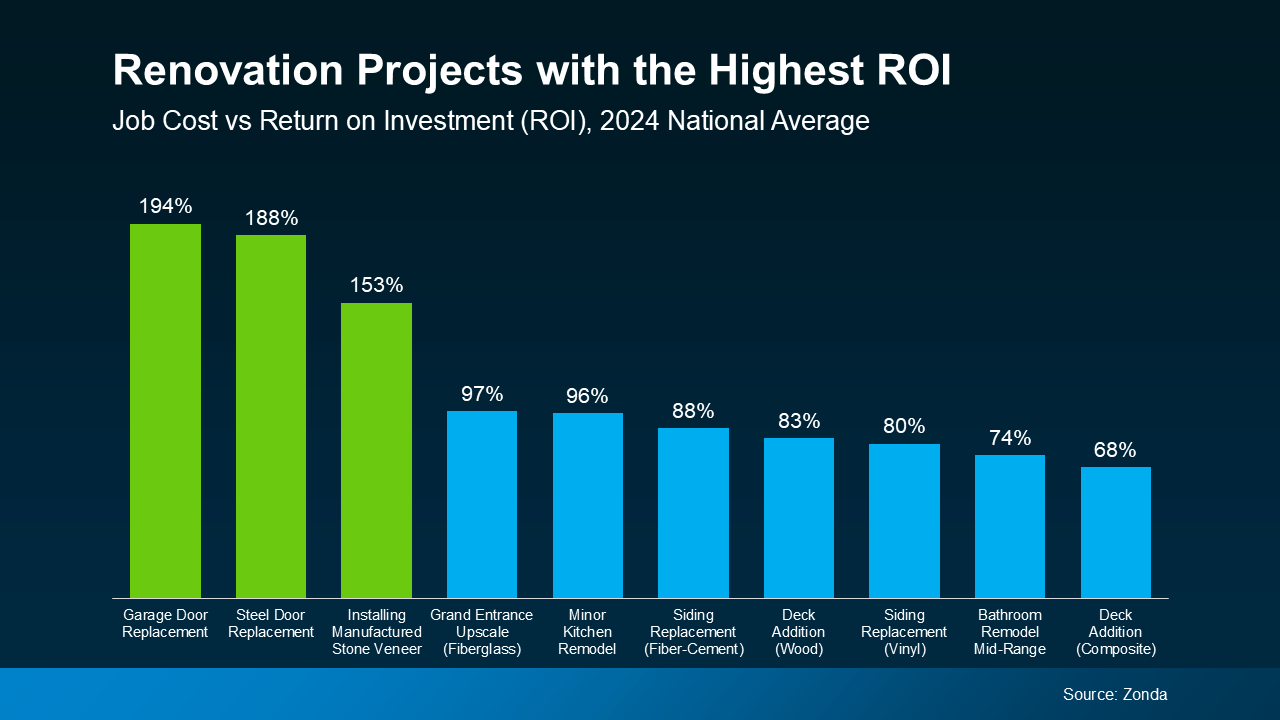

While big-ticket items like replacing an old roof or outdated flooring may seem daunting, they can pay off – especially if you focus on projects with the best return on investment (ROI).

An agent’s expertise is key in narrowing down your list to what’s actually worth it. They know what buyers in your area want and they also have data like this report from Zonda to guide you on which updates have the best ROI (see green in the graph below):

That’s why it’s so important to talk to a local real estate agent before you dive into any repairs. Bankrate puts it best:

That’s why it’s so important to talk to a local real estate agent before you dive into any repairs. Bankrate puts it best:

“As a seller, it’s smart to be prepared and control whatever factors you’re able to. Things like hiring a great real estate agent and maximizing your home’s online appeal can translate into a smoother sale — and more money in the bank.”

It’s not too early to partner with an agent. By starting now, you’ve still got time to space out the work and find any contractors you need to get the job done. If you wait until spring to roll up your sleeves, you risk running out of time – and that means your house may be overshadowed by others who are more buyer-ready.

Bottom Line

If you’re planning to sell this spring, it’s time to start tackling your to-do list. But, before you get started, connect with an agent. That way you can make sure you’re spending your time and budget on projects that’ll pay off in the long run.

Send an agent a list of what’s on your to-do list, so you can prioritize them together.

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

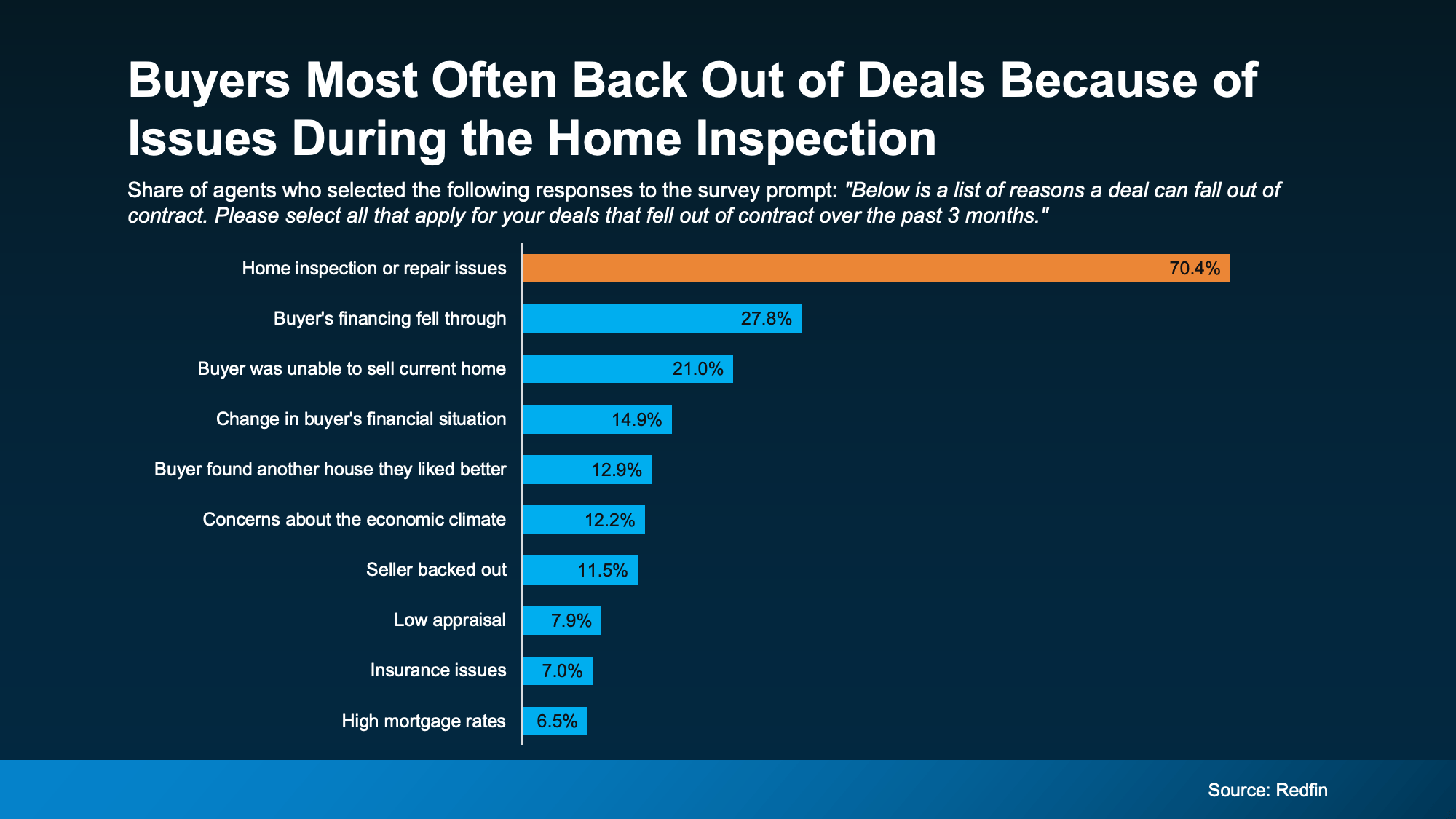

The Top Dealbreaker: Issues That Pop Up During the Inspection

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

Why Fixing Things Before You List Matters More Today

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

How Your Agent Can Help Give You the Edge

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They’ll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

- Roof leaks or damage: sagging, leaking, etc.

- Plumbing problems: standing water, leaks, water damage, etc.

- Electrical concerns: outdated or exposed wiring, missing GFCI outlets, etc.

- HVAC issues: non-functioning units

- Pest or insect damage: termite colonies, etc.

- Hazardous materials: lead, mold, asbestos, etc.

- Safety/code violations: missing smoke detectors, windows stuck closed, etc.

- Structural problems: cracks in the foundation, sagging floors, etc.

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

The Benefits of a Pre-Listing Inspection

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

- Fix concerns before you list, or disclosue issues upfront

- Avoid having to respond or negotiate under pressure

- Stop scrambling to find contractors with availability before your closing date

But remember, you don’t have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

- Decide if a pre-listing inspection is worth it where you live

- Recommend a trusted inspector (if you decide to get one)

- Look at the results with you to identify true dealbreakers in your market

- Help you decide what to fix or what to credit

- Make sure you avoid over-spending or under-preparing

Bottom Line

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, connect with an agent.

Foreclosures are ticking up. And that may make your mind jump straight to thoughts of 2008 – specifically to what happened to the market during the housing crash. So, let’s do exactly what your brain already wants to do, and see if there’s any connection there.

The simple truth is foreclosure filings are rising. But they’re nowhere near crisis levels. And that’s not where they’re headed either. Here’s why.

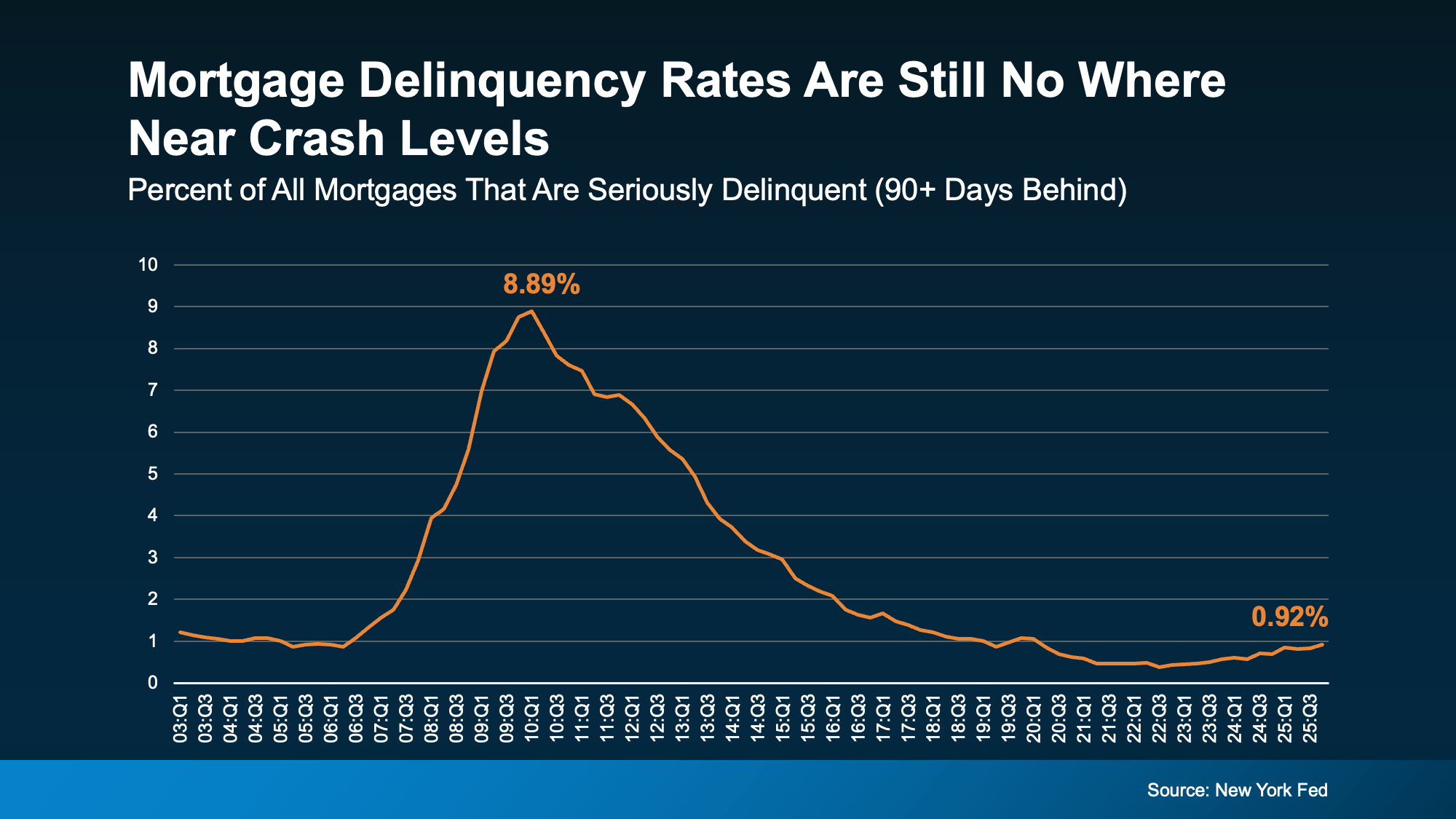

Take a look at serious delinquencies – loans where the homeowner is more than 90 days late on their mortgage payments.

While those have increased slightly, data from the New York Fed shows they still remain low. And they aren’t anywhere close to levels seen when the market crashed (see graph below):

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

In the years around the crash, they were up around 9%. That’s 1 in 11.

That’s a big difference.

And it’s important to remember not all delinquencies even become foreclosure filings. Some homeowners who are falling behind will work out repayment plans with their banks and lenders because banks don’t want to see a wave of foreclosures either.

That’s why foreclosure numbers are even lower than delinquencies. ATTOM shows only 0.3% of all homes are currently going through a foreclosure filing. And those won’t even all go to a full foreclosure. That’s not a wave. That’s a ripple at most.

If People Are Falling Behind on Payments, Why Aren’t There Even More Foreclosures?

And maybe you’re wondering, if people are struggling financially, why aren’t there more foreclosures? Here’s the easiest way to answer that.

When households feel financial pressure, they tend to prioritize their mortgage payment above almost everything else. Because the last thing they want to lose is their home.

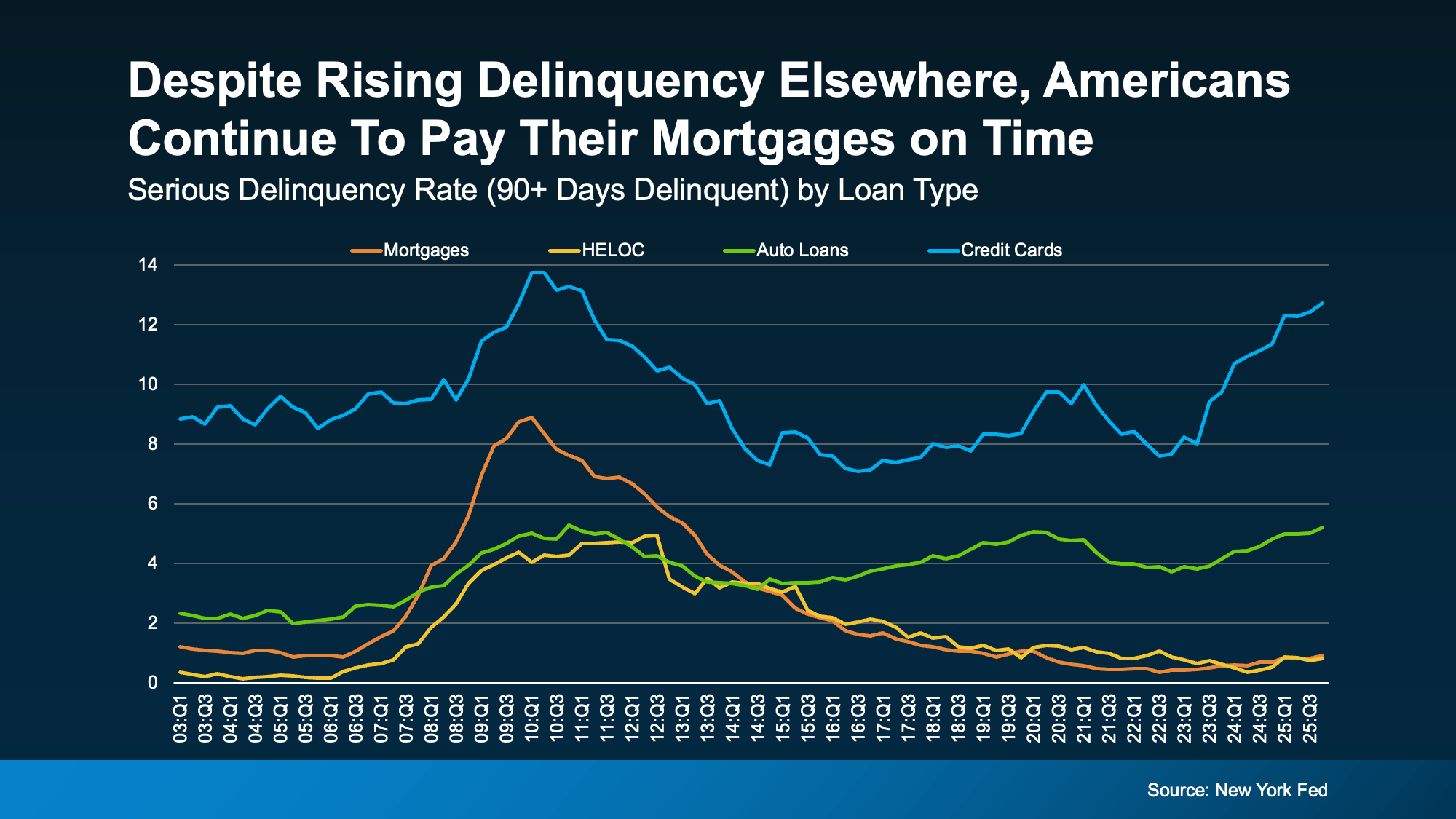

Data from the New York Fed shows serious delinquencies have risen more for credit cards and auto loans (the blue and green lines). But mortgage delinquencies and home equity lines of credit (borrowing against the value of your home) aren’t seeing the same big uptick (the yellow and orange lines). They’re a lot more stable overall.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

Home Equity Changes Everything

Many people have built significant equity over the past several years. And that creates options. As Daren Blomquist, VP of Market Economics at Auction.com, explains:

“Distressed homeowners… many times they still have equity in their homes. There’s an opportunity for them to sell that home, avoid foreclosure, and walk away with equity.”

That’s a major difference from 2008. Back then, many homeowners owed more than their homes were worth. And selling wasn’t an easy solution. Today, for many people, it is. And even in situations where equity isn’t enough, homeowners are encouraged to contact their loan servicer early to explore alternatives to foreclosure.

Bottom Line

Are foreclosure filings rising slightly? Yes. Are they anywhere near crash territory? No. And homeowners today have far more equity and flexibility than they did during the crash.

If you’re concerned about what you’re seeing in the headlines, the best move isn’t panic, it’s perspective. And the data right now says this isn’t 2008 all over again.

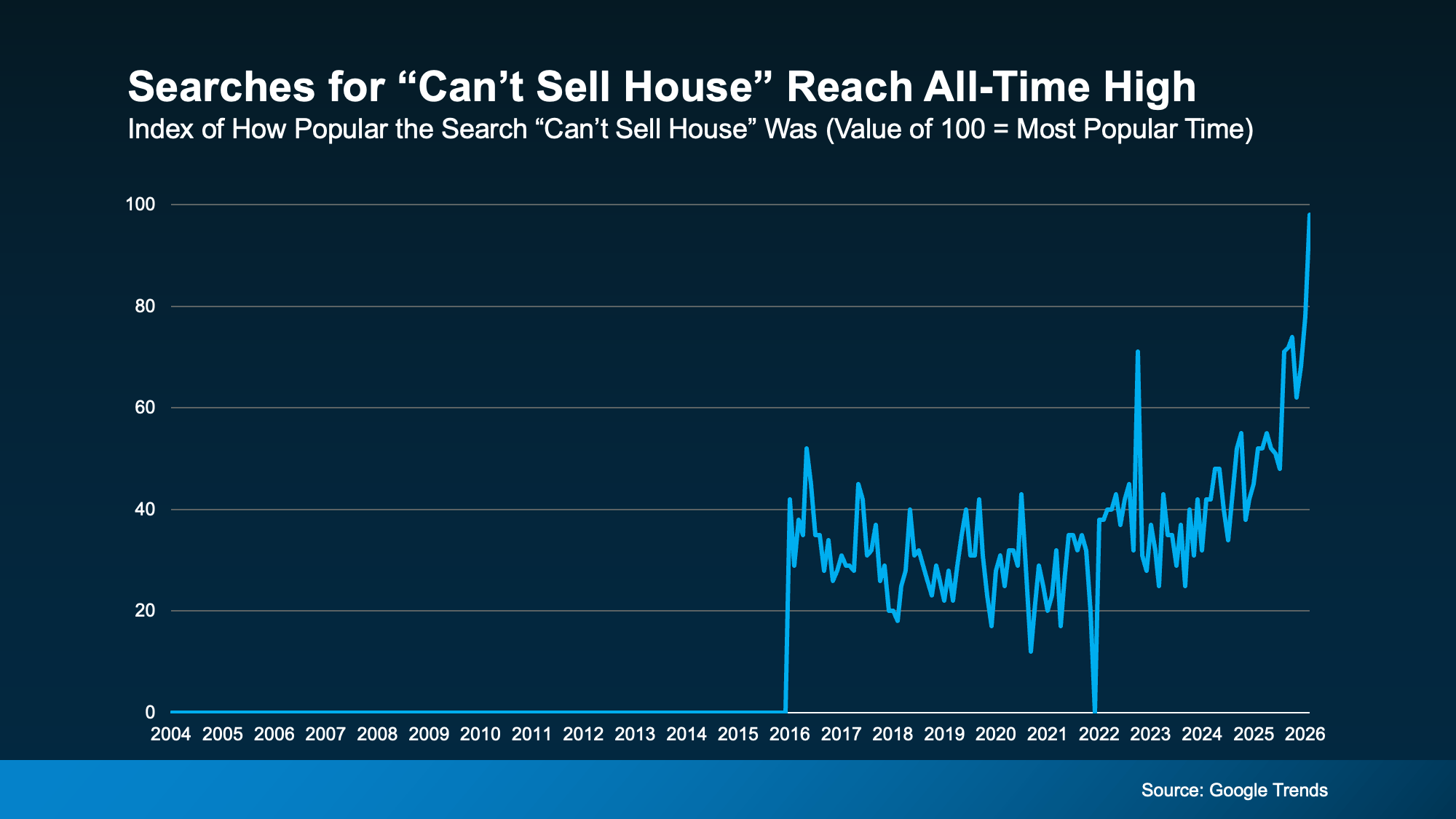

Online searches for “can’t sell house” just hit an all-time high according to Google Trends. So, if your house has been sitting on the market without any bites, you’re not the only one. But it’s also not the end of the road.

Homes are selling every day, so you can turn this around. You just need to take another look at your approach.

If you’re feeling this pain, know this: an online search engine isn’t where you should go for your answers. It’s much better to talk to your agent. Because a search engine doesn’t know your market or your house. But your agent does.

If you’re feeling this pain, know this: an online search engine isn’t where you should go for your answers. It’s much better to talk to your agent. Because a search engine doesn’t know your market or your house. But your agent does.

While a quick search or an AI platform may give you some tips on what to try, only an expert agent can actually diagnosis what’s going on – and how to fix it.

For example, your agent knows most homes that struggle to sell today are usually being held back by one (or more) of these three things.

1. Presentation: Buyers Will Compare Everything

When inventory was tight a few years ago, buyers overlooked imperfections because they had to, or they’d lose out to another bidder. Now? That’s no longer the case.

Today’s buyers scroll through dozens of listings in just minutes. They compare condition, updates, lighting, finishes, layout, and more – all side by side. If your home feels dated, cluttered, or in need of repairs, buyers will notice and it’ll knock your house right off their list of contenders.

This doesn’t mean you need a full renovation. But it does mean first impressions matter again. To compete today, you need curb appeal. Clean spaces. Neutral colors. Professional photos. If there are scuffs on the walls, obvious repairs, or too many outdated features, it could be what’s holding you back.

2. Pricing: If the Price Isn’t Compelling, It’s Not Selling

This is maybe the hardest one to hear, but what your neighbor sold their house for a few years ago isn’t necessarily the same price you’ll get today. As Selma Hepp, Chief Economist at Cotality, says:

“For sellers, the days of pricing aggressively and expecting instant offers are largely over. Homes that are well-priced and well-presented will still sell, but pricing discipline matters more than it did during boom years.”

Buyers are budget-conscious right now. If your home is priced based on outdated expectations instead of current demand, buyers may still look at your house online… but they likely won’t write an offer. Or, they’ll make an offer that you think is too low.

Pricing too high for this market is one of the top things sellers miss the mark on today. And those who aren’t willing to meet the market where it is or entertain offers may feel stuck.

3. Access: If Buyers Can’t See It, They Can’t Buy It

It sounds obvious but limited showing availability can kill your momentum. If your house isn’t easy to see because you’re restricting showings to evenings only, no weekends, or requiring a 24-hour notice, you’re cutting your buyer pool down by more than you may realize.

And the more friction you create, the fewer buyers walk through the door.

In a market where buyers have more options, the last thing you want to do is give them a reason to skip your house. Availability matters because if no one sees it, no one buys it.

Don’t Let Search Results Decide Your Next Step

When your house isn’t selling, it’s tempting to spiral and wonder if it’s the market or if something’s wrong with your house. But instead of searching for answers online, here’s what to do.

Sit down with your agent and ask three honest questions:

- What are buyers looking for in today’s market?

- What feedback are we getting from showings?

- Why do you think my house hasn’t sold yet?

That conversation will bring a lot more clarity than any search engine results.

Bottom Line

If your listing feels stuck, it’s not a sign you shouldn’t sell. It’s the market giving you feedback. And feedback is powerful when you use it.

Start with a real conversation with a real agent about what’s working and what’s not. Your agent will be able to tell you which small adjustments could totally change the momentum. Because in this market, the sellers who adapt are the ones who move.

The #1 Reason Buyers Walk Away (And How To Get Ahead of It)

One Key Sign We’re Not Headed for a Wave of Foreclosures

If Your House Isn’t Getting Offers, Read This.

-

Affordability3 weeks ago

Affordability3 weeks agoRenting vs. Buying: The Numbers Might Surprise You

-

For Sellers4 weeks ago

For Sellers4 weeks agoThe Real Reason Home Sales Slowed in January. And It’s Not What You Think.

-

For Sellers3 weeks ago

For Sellers3 weeks agoTop Mistakes Homeowners Are Making in 2026 (And How To Avoid Them)

-

Equity3 weeks ago

Equity3 weeks agoHow Your Equity Could Help Younger Generations Buy a Home

-

For Buyers4 weeks ago

For Buyers4 weeks agoMove-Up Buyers Are Choosing New Construction

-

Agent Value4 weeks ago

Agent Value4 weeks agoThe Price You Set Can Make (or Break) Your Sale

-

Downsize2 weeks ago

Downsize2 weeks agoThe Hidden Advantage Repeat Buyers Have Right Now

-

For Sellers2 weeks ago

For Sellers2 weeks agoSpring Sellers Have an Edge. Here’s Why.

You must be logged in to post a comment Login