For Buyers

4 Things To Expect from the Spring Housing Market

Spring is in full swing, and the housing market is picking up along with it. And if you’ve been wondering whether now is the right time to buy or sell, here’s the inside scoop on why this spring may be a great time to make your move.

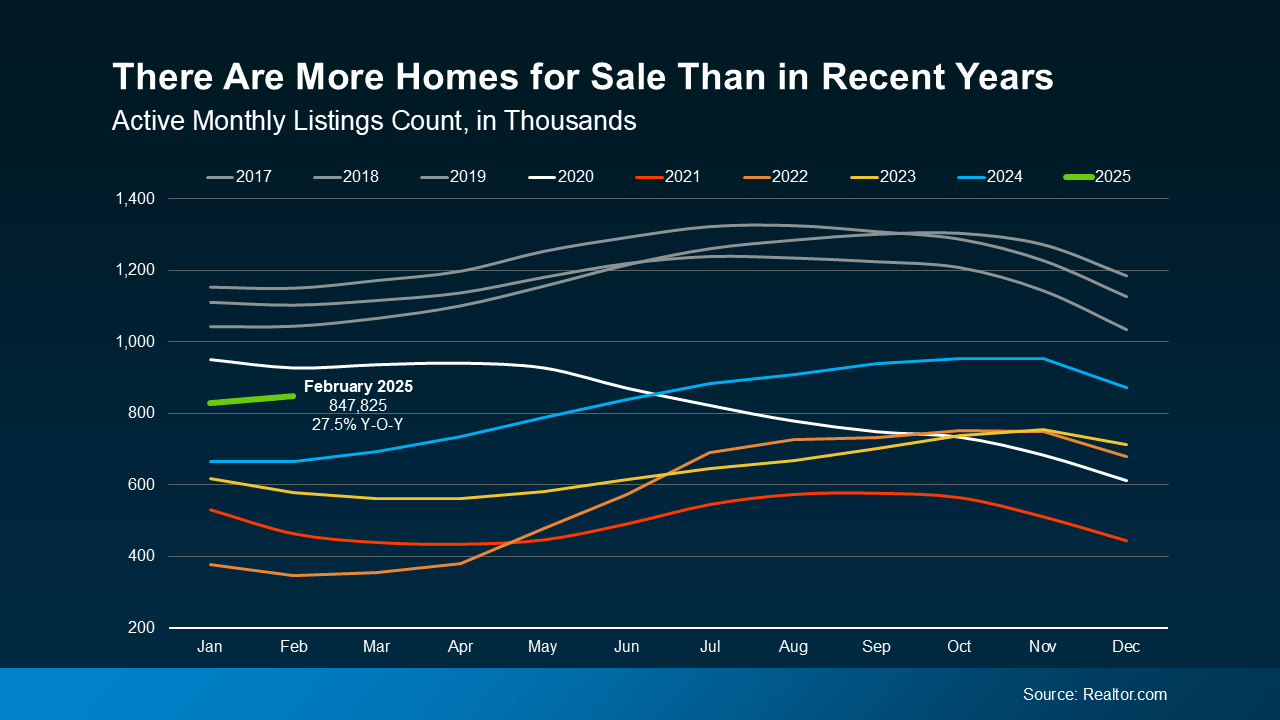

1. There Are More Homes for Sale

After a long stretch of tight inventory, the number of homes for sale is finally improving. According to recent national data from Realtor.com, active listings are up 27.5% compared to this time last year.

Look at the graph below and follow the green line for 2025. You can see, even though inventory levels still haven’t returned to pre-pandemic norms (shown in gray), that number is higher than it has been going into the spring market over the past few years (see graph below):

Buyers: This means you have more choices, and you can be more selective.

Buyers: This means you have more choices, and you can be more selective.

Sellers: With more homes available than in recent years, you’re more likely to find what you’re looking for when you move. And knowing that inventory is still below more normal levels means there will be demand for your home when you sell it, too.

2. Home Price Growth Is Moderating

As inventory grows, the pace of home price growth is slowing down – and that will continue into the spring market. This is because prices are driven by supply and demand. When there are more homes for sale, buyers have more options, so there’s less competition for each house. Rising supply and less buyer competition causes price growth to slow, but it should still remain positive in most markets. As Freddie Mac says:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

And while prices aren’t dropping at the national level, every market is different. Some areas are seeing stronger price growth, while others are cooling off or even seeing some price declines.

Buyers: The slower pace of growth means prices aren’t rising as quickly as before – and that’s a relief. Any home you buy now is likely to appreciate in value over time, helping you build equity.

Sellers: While prices are still rising, you might need to adjust your expectations. Overpricing your house in a more balanced market could mean it takes longer to sell. Pricing your house competitively is going to be key to attracting offers.

3. Mortgage Rates Are Stabilizing

One of the biggest hurdles for buyers over the past couple of years has been high, volatile mortgage rates. But there’s some good news – overall, they’ve stabilized in recent weeks – and have even declined a bit since the beginning of this year. And while that decrease hasn’t been a big drop, stabilizing mortgage rates has helped make buying a home a bit more predictable. According to Selma Hepp, Chief Economist at CoreLogic:

“With the spring homebuying season upon us, the recent improvements in mortgage rates may help invite homebuyers back into the market.”

Buyers: When mortgage rates are more stable, it’s easier to plan ahead because you have a better idea of what your future payment might be. But remember, rates will continue to be volatile. So, lean on your agent and your lender to make sure you know what the latest mortgage rate means for you.

Sellers: Slightly lower rates that are starting to stabilize are encouraging more buyers to move forward with their plans. That’s good for demand when you’re planning to sell your house.

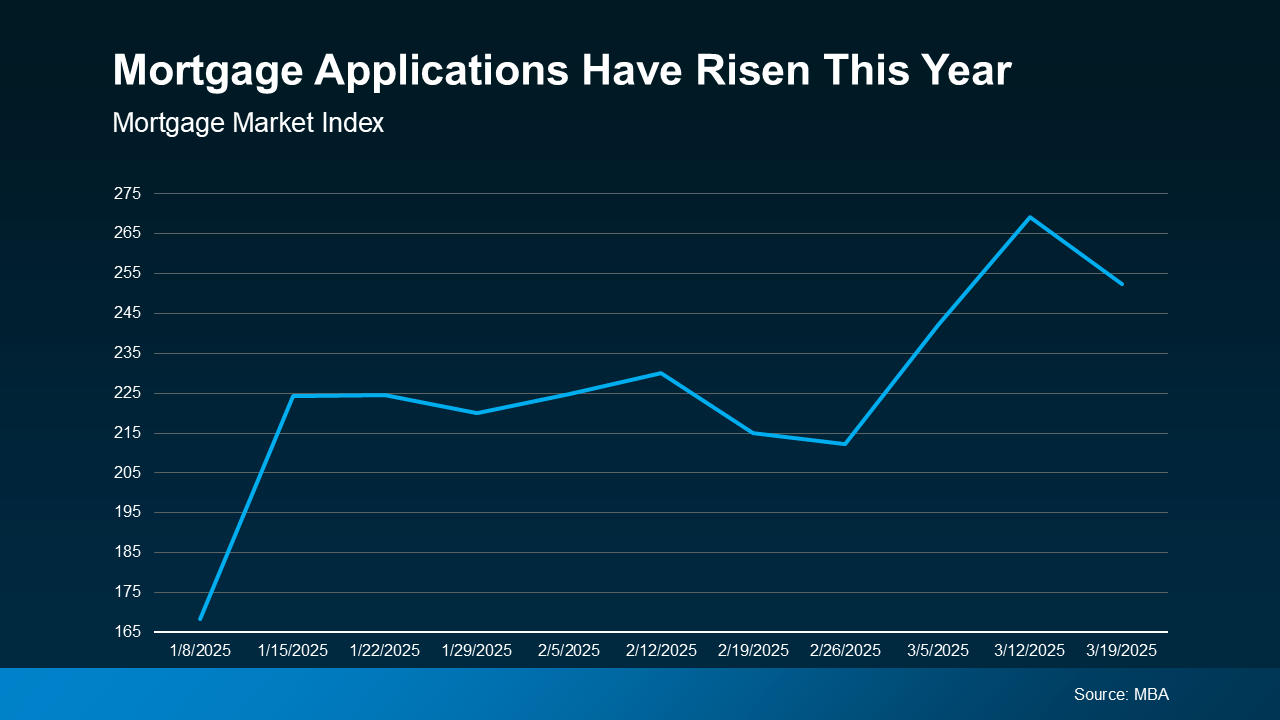

4. More Buyers Are Returning

With more inventory, slowing price growth, and stabilizing mortgage rates, buyers are gaining confidence and coming back into the market. Demand is picking up, and data from the Mortgage Bankers Association (MBA) shows an increase in mortgage applications compared to the start of the year (see graph below):

Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.

Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.

Sellers: This is great news for you – more buyers mean a better chance of selling your house quickly.

Bottom Line

Do you have questions about what the spring market means for you? Connect with a local real estate agent and talk about how to craft your plan this season.

With more homes for sale, slowing price growth, and stabilizing mortgage rates, how will this impact your decision to buy or sell this spring?

If you’ve thought about buying a home in the past few years, you may have run into two frustrations: asking prices that kept climbing and too few homes to choose from.

In many places, both sticking points are letting up this summer, with lower asking prices and more homes for sale. Let’s look at the trends, and what they mean for your search.

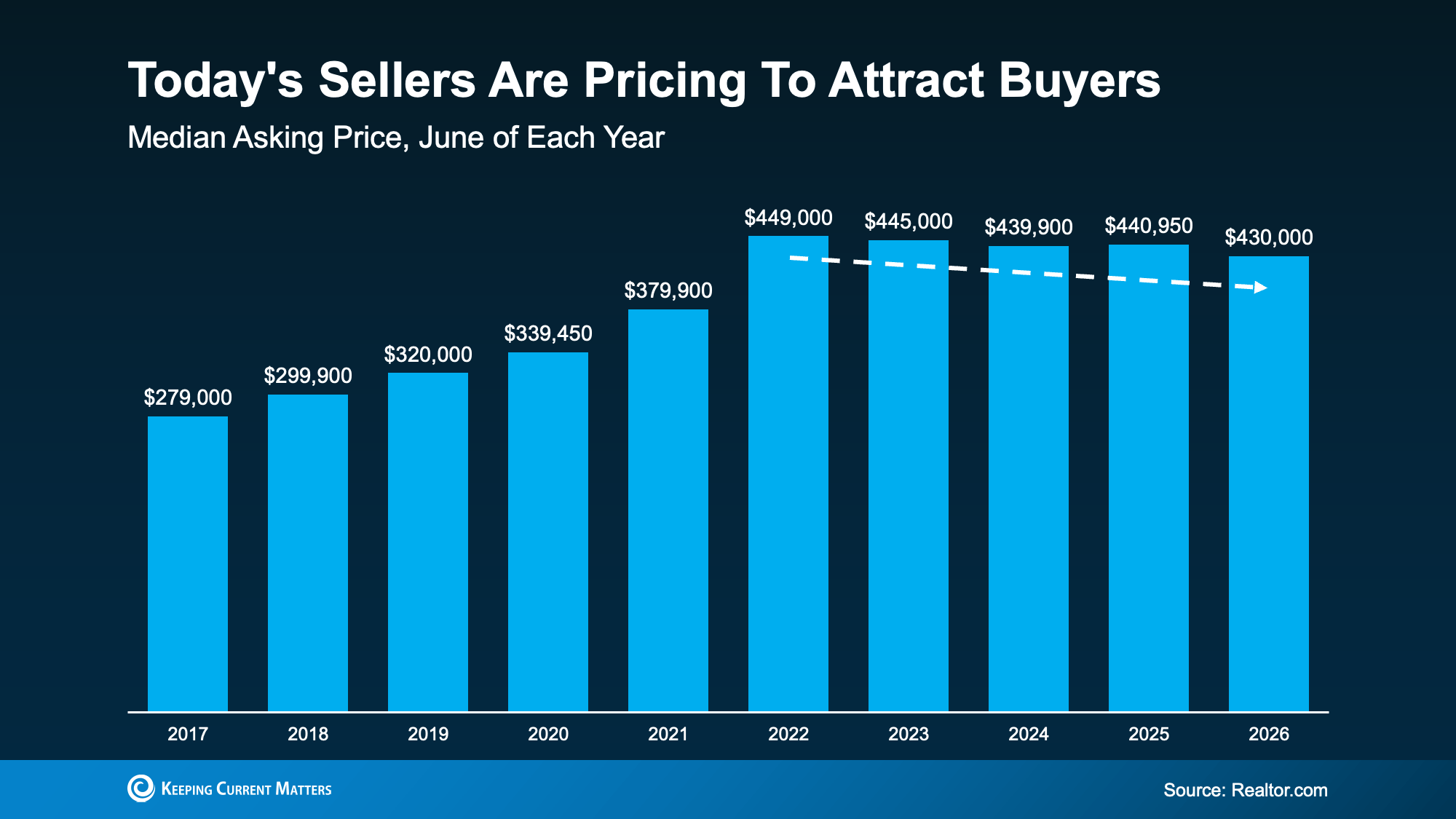

Sellers Are Pricing To Attract Buyers

According to Realtor.com, the national median asking price was $430,000 in June, nearly $11,000 under what it was the year before (see graph below):

That’s the eighth month in a row that the typical asking price has dipped below where they were the previous year, according to the same Realtor.com report.

And while falling prices can sound worrying, this isn’t a sign of an impending crash. We’re talking about asking prices, not sold prices. This is a sign that today’s sellers are meeting the market where it is and pricing to draw buyers. And that’s actually something normal we’d expect from the market. As Danielle Hale, Chief Economist at Realtor.com, puts it:

“Sellers are reading market conditions and are pricing accordingly from the start rather than listing high and cutting later, and buyers are taking note and making bids. This is a welcome sign that we are in a functioning market.”

Asking prices were never going to climb forever – now they’re just settling closer to what buyers can actually pay. That signals a healthier market, and sellers re-adjusting their expectations.

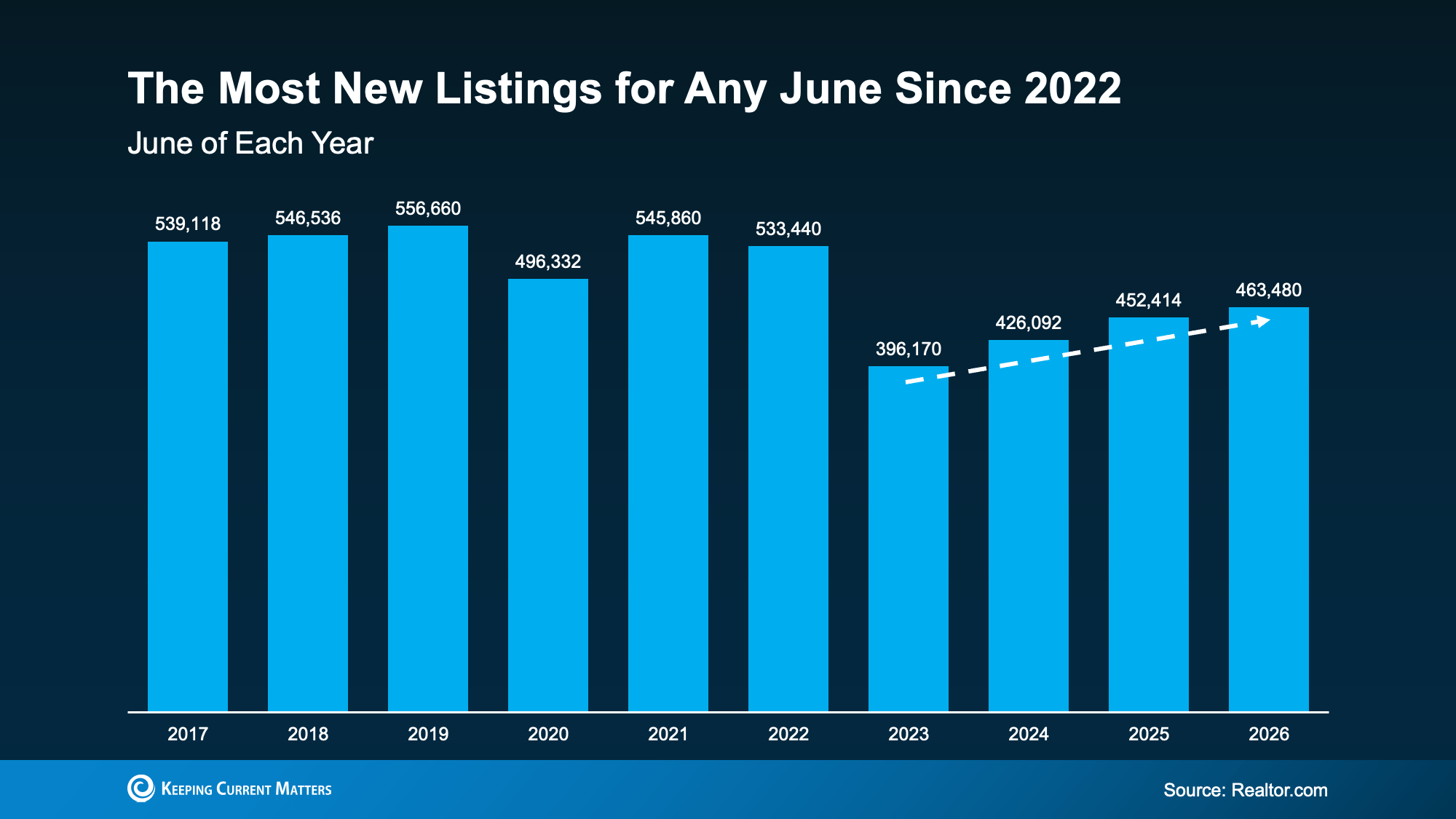

More Homes Are Available Now

If you’ve spent the past few years watching homes disappear before you could even schedule a tour, this is for you.

Supply is starting to catch up. According to Realtor.com, the number of homes listed for sale in June was the highest June number we’ve seen in three years (see graph below):

This means more options for you and less competition for each one.

Now, supply is not back to normal everywhere. As you can see, we’re still down from where we were back in 2017-2019. But in many places, it’s better than it’s been in a while. Here’s how that helps you.

You don’t have to rush an offer just to stay in the running, and you have better odds of finding and landing the right home, not just the one that’s available. Plus, you’ll have more room to negotiate, so you’re searching from a stronger position than buyers had even a year ago.

Why This Is Encouraging if You’re Buying Your First Home

For first-time buyers looking for lower-priced homes, these trends line up especially well. Mischa Fisher, Chief Economist at Zillow, explains:

“The lowest price tiers are exhibiting some softness in terms of price, they also had the most listing-activity growth, the first time since 2022 that’s been the case.”

So, if you’re searching for your first place or your next house, there’s a little more to choose from and a little more give on price.

Bottom Line

If a tight budget or a thin selection has kept you from buying a home, now might be the time to restart your search.

Connect with a local real estate agent to see what’s available where you’re looking.

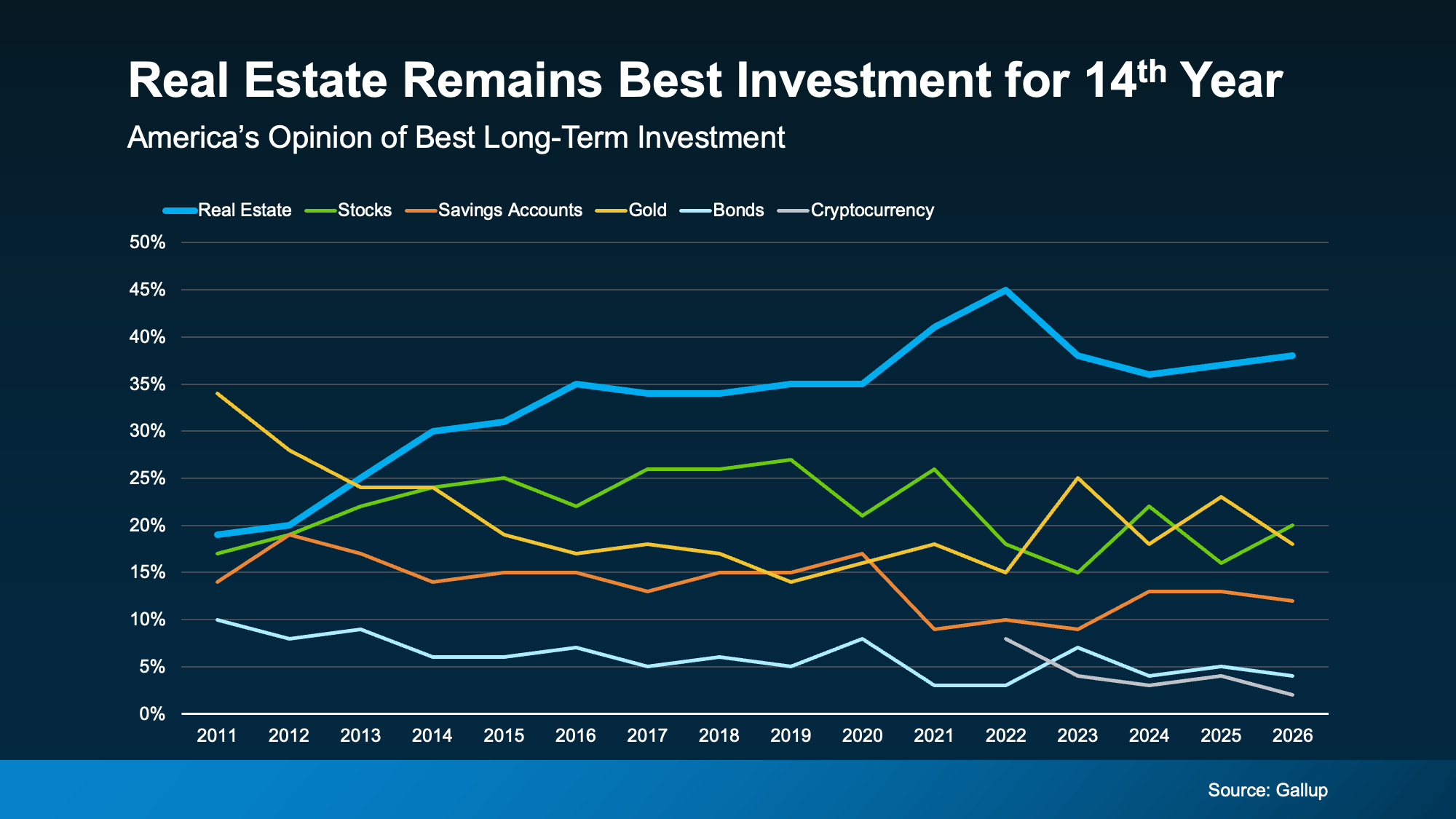

Quick gut reaction. Which investment do Americans trust more than stocks, gold, savings accounts, and bonds? The answer hasn’t changed in 14 years.

It’s real estate. And this year, that answer comes with even more conviction behind it. New data shows people aren’t just saying homeownership is a smart move, they’re feeling better about it than they have in years. Let’s dig into why.

Real Estate Takes the Top Spot – Again

Every year, Gallup asks Americans to name the best long-term investment. And for the 14th year in a row, real estate came out on top (see graph below):

That’s not a fluke or a hot streak. That’s 14 straight years of beating out stocks, gold, and everything else.

Think about everything that’s happened in that stretch – rising rates, market swings, election years, you name it. Through all of it, Americans kept picking real estate. That kind of staying power says something about how people view homeownership – and it makes sense. Historically, it’s one of the best ways to build wealth in this country.

As Michelle Egan, Head of Credit Solutions, Impact Finance at JPMorgan Chase, explains:

“Owning a home has long been considered one of the most reliable ways to build wealth. Beyond providing shelter, a home is a valuable asset that can appreciate over time, build equity, and serve as a financial resource for generations.”

Now, you may have seen chatter online saying home prices are falling and wondered if that changes the math. It really shouldn’t. Nationally, home prices are still rising – just at a slower pace than a few years ago.

Yes, some local markets are seeing slight dips, but those dips are small compared to how much home values have grown over the past 5 years. Generally speaking, home prices almost always rise. As long as you plan to live there for a good length of time, you should still have the chance to build equity.

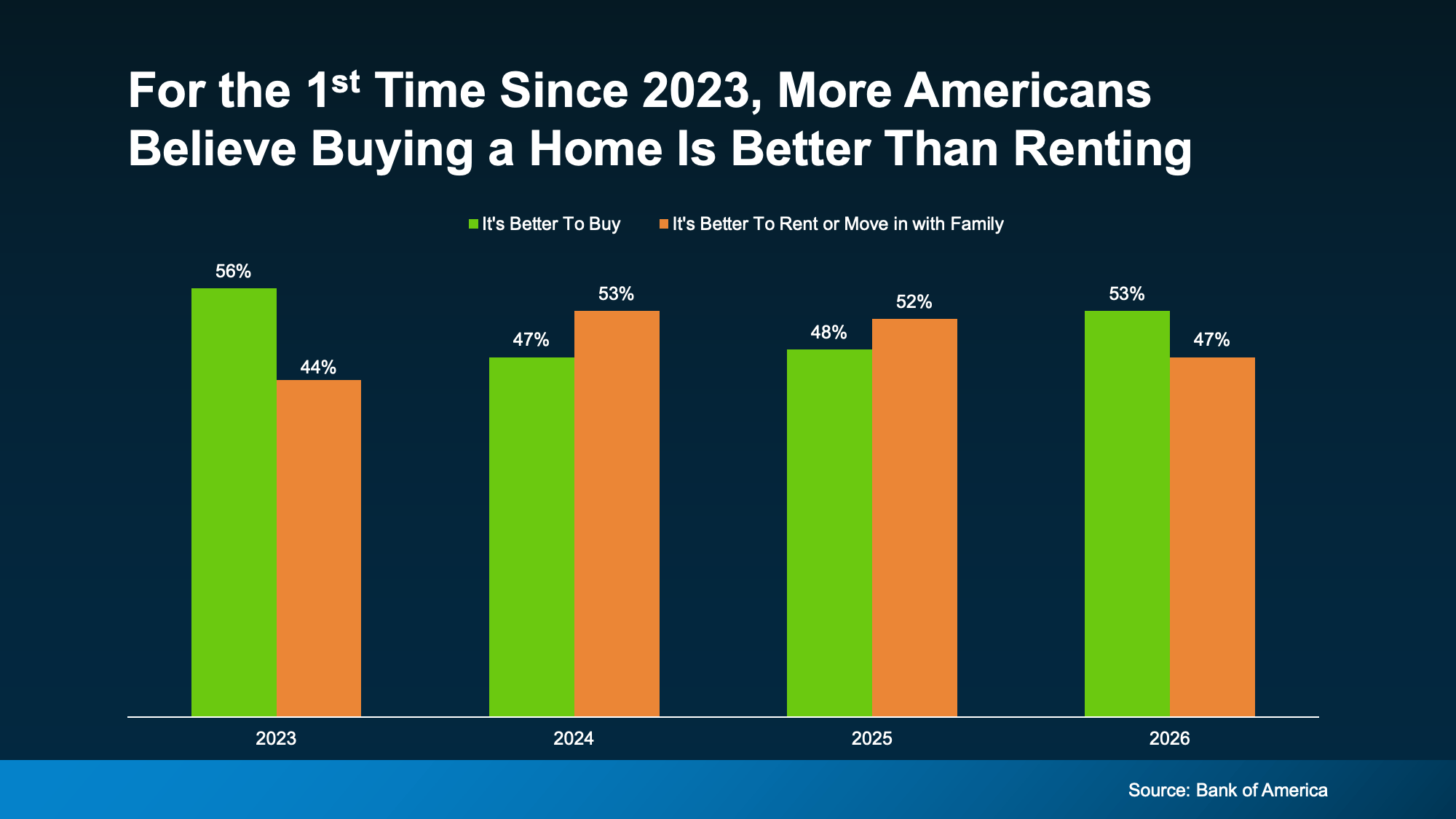

More People Say Buying Beats Renting

And while it’s true homeownership has been seen as a worthwhile pursuit for years now, something interesting is happening. It may actually be gaining a bit more popularity again.

According to Bank of America‘s latest Homebuyer Insights Report, 53% of people now say it’s better to buy a home than to rent or move in with family. That’s the first time buying has taken the lead since 2023 (see graph below):

In that same report, here are a few other signals that confidence in homeownership is on the rise:

-

90% of people say a home is a valuable investment, up from 79% just last year.

-

And 94% say owning a home provides stability, up from 83% the year prior.

Those are relatively big jumps in a short amount of time. And here’s what may be driving it.

It’s About More Than Money

Sure, affordability is still tight and some markets are still hard to break into, but that hasn’t changed what people feel about homeownership as a goal. And the reason why is simple – it’s not just a financial decision. It’s a lifestyle choice.

A home pays you back in ways stocks never could. As Sheharyar Bokhari, Principal Economist at Redfin, says:

“For many homeowners, a home is more than a place to sleep and store belongings—it’s a reflection of who they are. Homeownership can help people put down roots, build relationships and create a space that feels uniquely their own.”

You can’t get that from a brokerage account. A home is the one investment that grows your wealth and gives you a place to build your life. And that means something.

Bottom Line

For 14 years straight, Americans have called real estate the best long-term investment, and confidence in owning a home is on the rise. If you’ve been weighing whether buying is worth it, connect with a local real estate agent and talk through what that first step could look like for you.

Negotiations are back. More buyers are asking for better deals, and more sellers are giving them. Builders are throwing in extras, too.

That’s why whether you’re buying or selling today, there are two terms you’ll hear a lot: concession and incentive.

-

A concession is something a seller agrees to during negotiations to get a deal done.

-

An incentive is a perk a builder (or a seller) advertises upfront to attract buyers.

Let’s run through what you need to know about both and how they could play a role in your move.

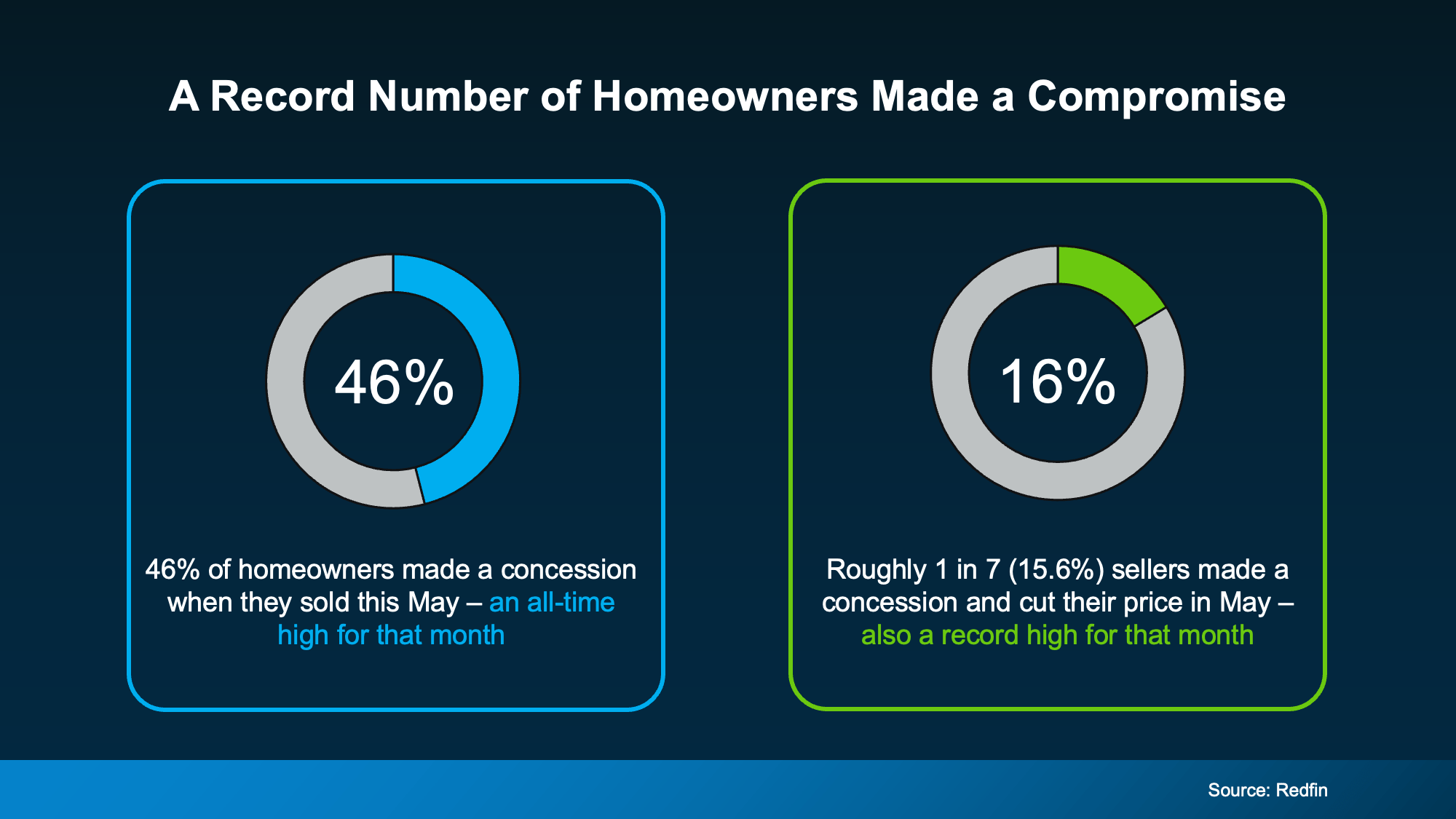

More Sellers Are Agreeing to Concessions

Almost half (46%) of homeowners who sold recently gave the buyer a concession, according to Redfin. That’s the highest share on record for this time of year. And roughly 1 in 7 (16%) sellers went a step further, cutting their asking price and offering a concession on top (see chart below):

So, what kind of concessions are we talking about?

A seller might cover part of your closing costs, take care of a repair, or offer a credit that trims your upfront costs. It’s how they keep a deal on track when buyers have more options to choose from – and homeowners aren’t the only ones compromising.

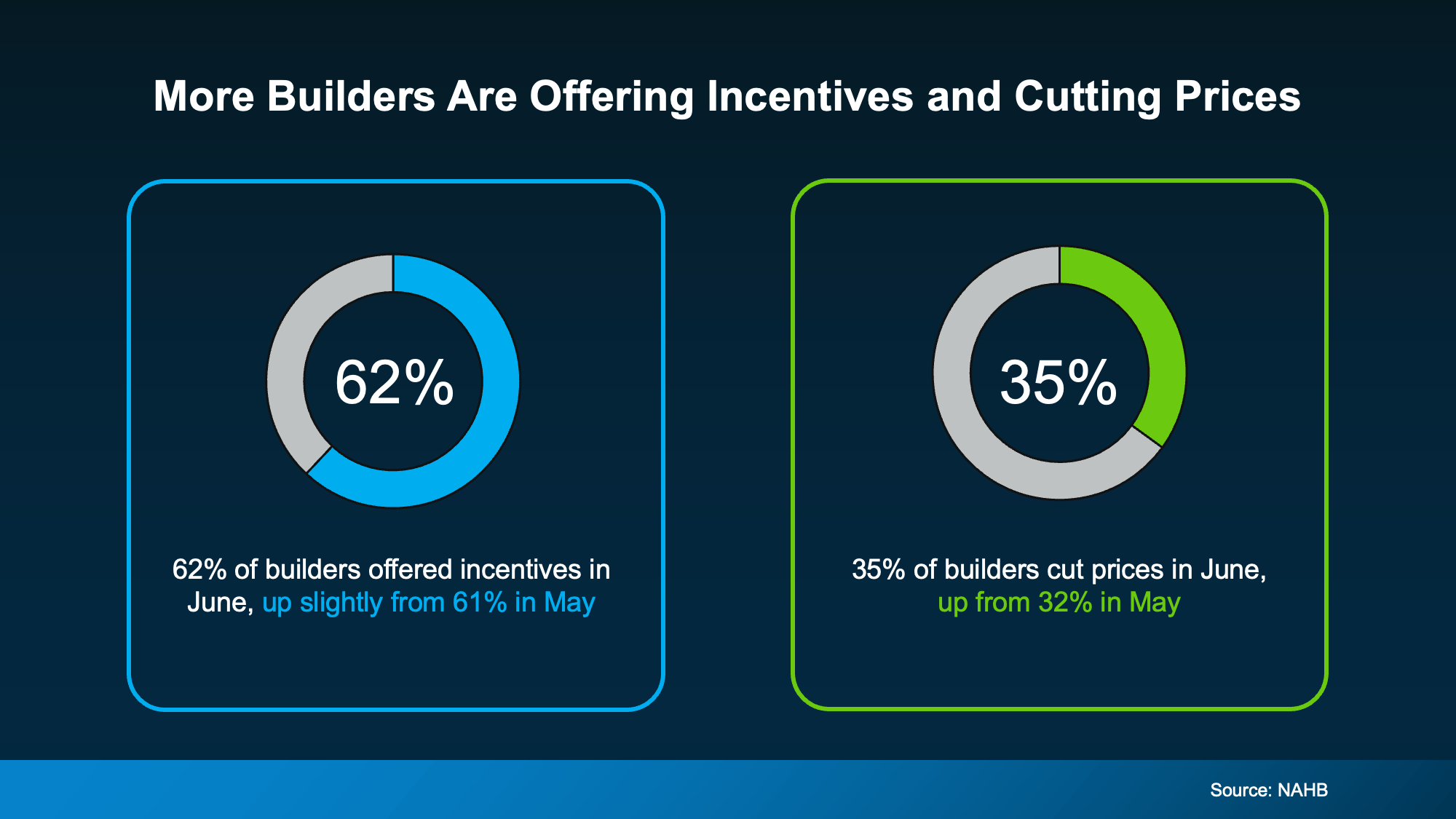

Builders Are Cutting Prices, Too

Newly built homes are seeing the same push and pull. According to the National Association of Home Builders (NAHB), 62% of builders are offering incentives right now. And about 35% are cutting prices outright (see chart below):

Those incentives often look like:

-

Mortgage rate buydowns

-

Free upgrades, like nicer finishes or appliances

Danielle Hale, Chief Economist at Realtor.com, explains why:

“New construction has been one of the steadiest parts of the housing market over the past few years, but builders are clearly responding to today’s affordability pressures and higher levels of existing-home inventory.”

Even builders, who many people think rarely negotiate, are competing on price and perks. They have been for over a year now. The same data shows this is the 15th straight month where more than 60% of builders have offered incentives to sweeten the deal. And that’s significant.

What This Means for Your Move

If you’re buying, this is a good time to ask. Whether you have your eye on an existing house or a newly built home, there’s a chance the seller or builder will meet you partway on price, terms, or both.

If you’re selling, expect buyers to ask. Even builders of brand-new homes are making concessions more often than not right now. Holding firm on every term could mean more time on the market, or a lost sale altogether.

Bottom Line

Sellers and builders are both giving buyers more to work with this year. A local agent can tell you what to expect in concessions and incentives based on inventory and competition in your local market.

More Homes, Better Prices: A Buyer’s Summer

14 Years Running: Why Real Estate Is Still America’s Favorite Investment

Think Nobody’s Buying Homes Right Now? Think Again.

-

Economy4 weeks ago

Economy4 weeks agoMore Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Agent Value4 weeks ago

Agent Value4 weeks agoYour House Didn’t Sell. Here’s How To Turn It Around.

-

Affordability4 weeks ago

Affordability4 weeks agoThat House That’s Been Sitting Could Be Your Best Shot at a Deal

-

Equity3 weeks ago

Equity3 weeks agoThe Housing Market Is Stronger Than You Think

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoThe 1 Factor That Explains Everything Happening with Home Prices Right Now

-

Economy2 weeks ago

Economy2 weeks agoWhat Buying or Selling a Home Gives Back to Your Community

-

Affordability3 weeks ago

Affordability3 weeks agoDown Payments Are Smaller Than They’ve Been Since 2021

-

Affordability2 weeks ago

Affordability2 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

You must be logged in to post a comment Login