Buying Tips

Why Pre-Approval Is More Important Than Ever This Spring

If you’re planning to buy a home this year, you may be focused on the spring market. And hoping that when spring does hit, you’ll see:

- Mortgage rates drop a little more.

- More homes hit the market.

But here’s what most buyers don’t realize. Buying just a few weeks earlier could mean paying less, dealing with less stress, and feeling less rushed.

Here are three reasons why accelerating your timeline over the next few weeks could actually be a better play.

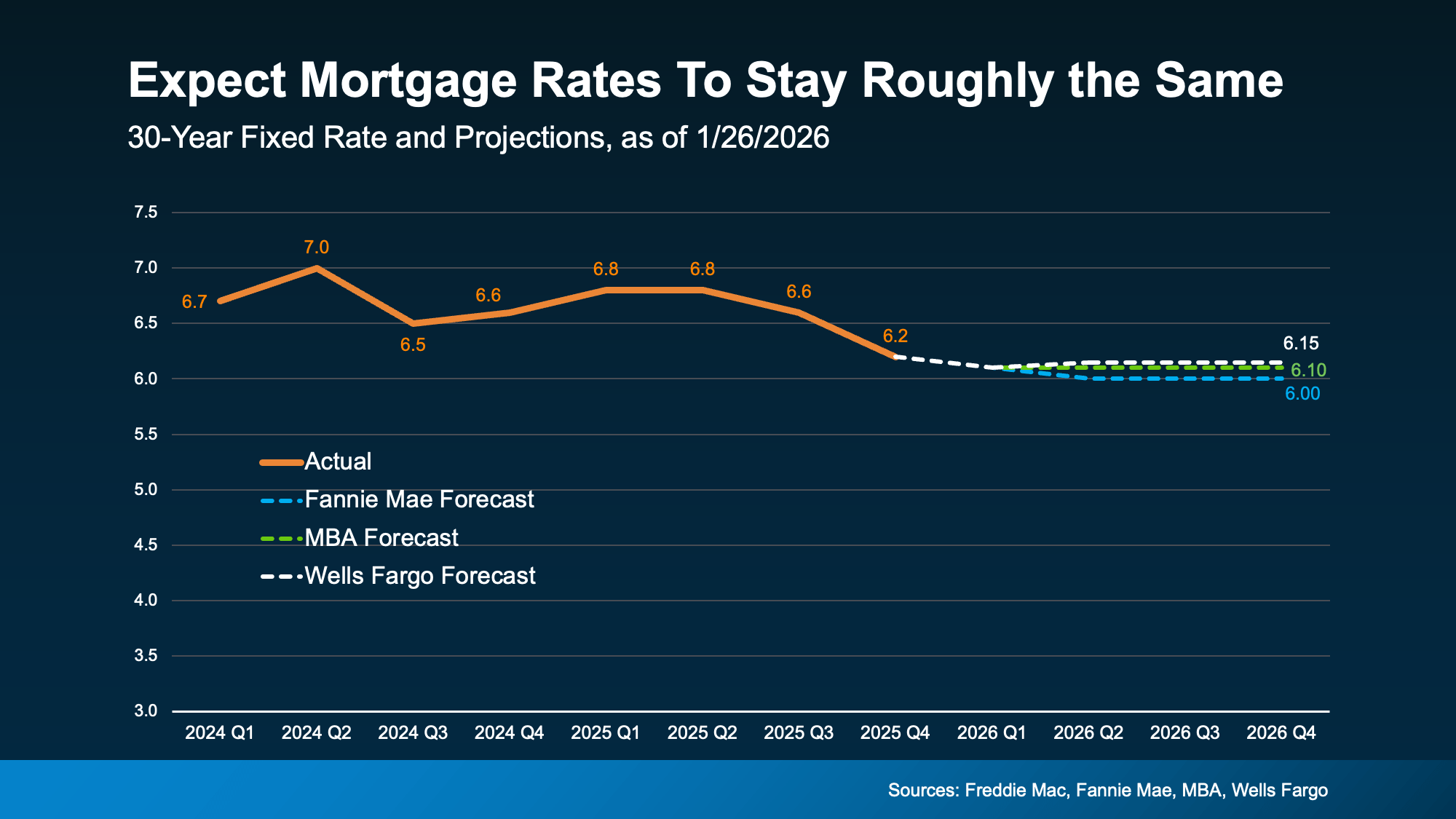

1. Holding Out for Lower Rates May Pay Off

A lot of buyers are hoping mortgage rates will fall even further. But that’s not the best strategy. Here’s why. Experts are pretty aligned on this: rates are expected to stay roughly where they are.

Forecasts throughout the industry all point to the same thing: rates are projected to be in the low-6% range this year (see graph below):

That’s not a bad thing, especially if you consider how much rates have already come down. Over the past 12 months, they’ve dropped roughly a full percentage point. And for many buyers, that means affordability has already improved more than they may realize.

That’s not a bad thing, especially if you consider how much rates have already come down. Over the past 12 months, they’ve dropped roughly a full percentage point. And for many buyers, that means affordability has already improved more than they may realize.

So why wait a few more weeks just for more buyers to jump in and act as your competition? You already have a window right now. As Chen Zhao, Head of Economics Research at Redfin, explains:

“House hunters should know that this may be near the lowest mortgage rates fall for the foreseeable future.”

2. Spring Means More Competition + More Stress

Speaking of competition, the spring market is popular for a reason, but with popularity comes pressure. With more buyers active at that time of year, you’ll have to move faster once you find a home you like. And no one likes feeling rushed.

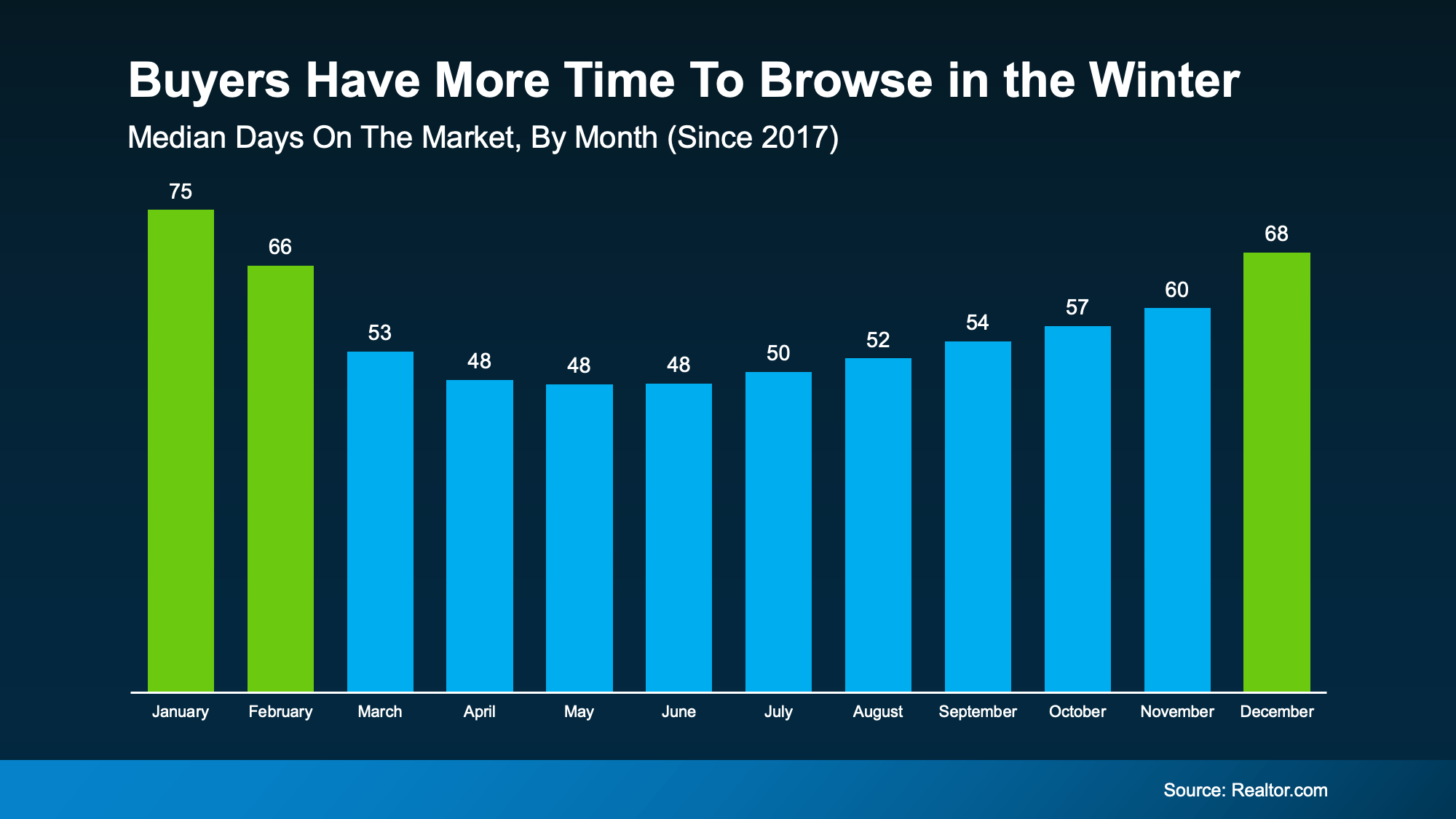

But buy now and you have more time to browse. Fewer people are looking, so homes sit longer.

You can see this play out in the data from Realtor.com (see graph below). In winter months, it takes an average of about 70 days for a home to sell. In spring? That drops to about 50 days. That’s a 20-day swing – and that pace is going to be more stressful.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

3. Prices Tend To Rise When Competition Heats Up

And here’s something most buyers forget to factor in. Prices usually respond to demand. So, when demand is higher, prices are too. Bankrate explains:

“Spring and early summer are the busiest and most competitive time of year for the real estate market . . . home prices tend to be steeper to reflect the increased demand.”

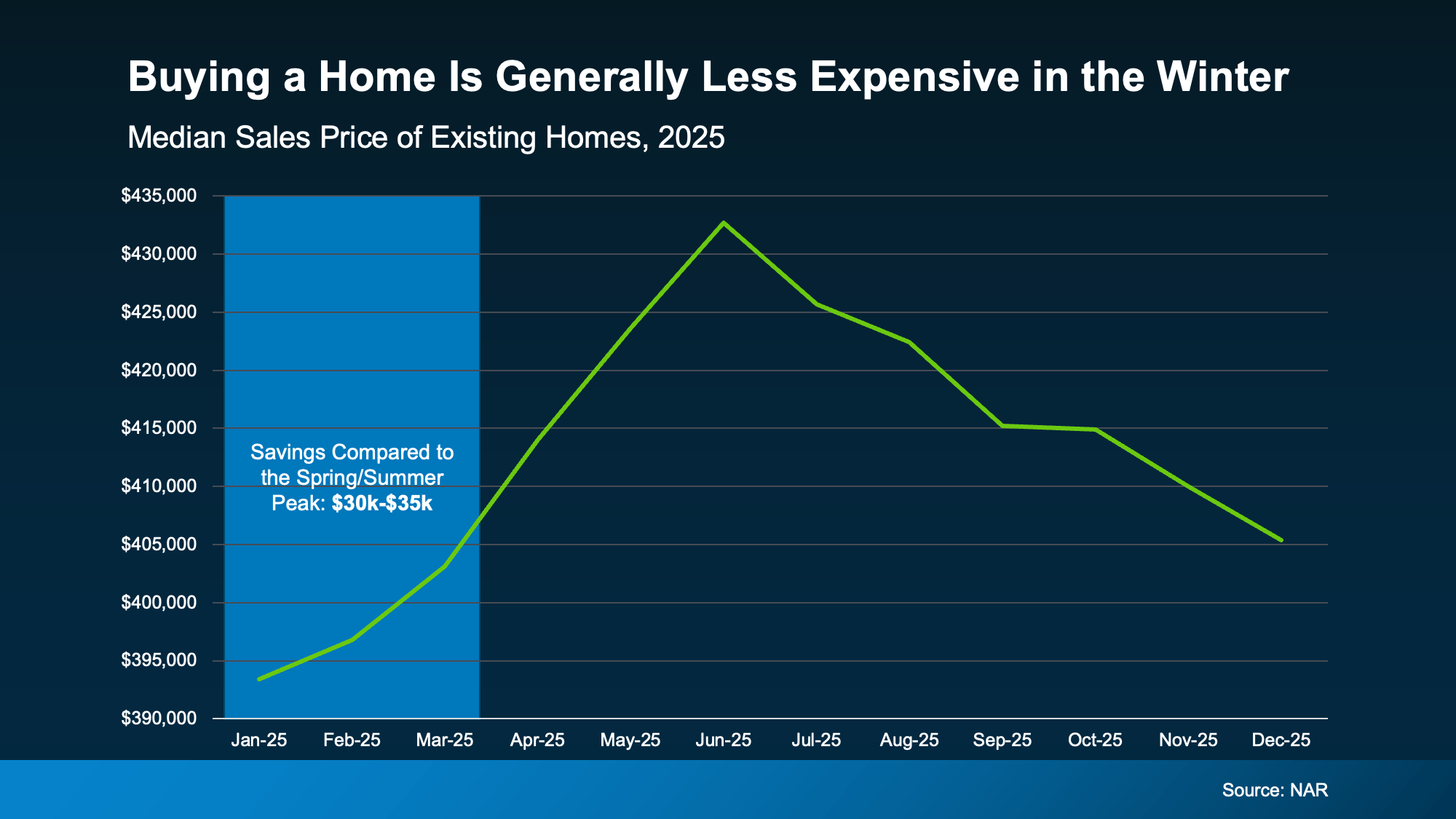

In fact, data from the National Association of Realtors (NAR) shows that in 2025, buyers who purchased in the beginning of the year saved roughly $30,000–$35,000 compared to those who bought when prices peaked in the spring or early summer.

And let’s be honest, for a lot of buyers today, every little bit of savings helps. That’s why buying just a few weeks earlier, before prices ramp up, will be better for you and your wallet.

And let’s be honest, for a lot of buyers today, every little bit of savings helps. That’s why buying just a few weeks earlier, before prices ramp up, will be better for you and your wallet.

Bottom Line

Buying a few weeks before spring isn’t about rushing. It’s about choosing to be ahead of the curve and knowing you want more leverage, less stress, and meaningful savings.

If you’re ready and able to buy now and want to get the ball rolling, connect with a local agent.

Buying a home is one of the biggest purchases you’ll ever make. And homeowner’s insurance is what protects that investment. Think of it as your safety net. NerdWallet explains it:

- Covers Repairs and Rebuilding Costs: If your home is damaged by fire, storms, or other covered events, it helps pay for repairs and possibly even a full rebuild, if that’s deemed necessary.

- Protects Your Belongings: It can also cover personal items like furniture, electronics, jewelry, and clothing if they’re stolen or damaged.

- Provides Liability Coverage: And, if someone gets injured on your property, your policy can help cover medical bills or legal expenses.

But that peace of mind does come with a cost, and lately those costs have been rising.

Why Home Insurance Premiums Are Going Up

There are a number of factors causing insurance premiums to rise today. But, in the simplest sense, here’s what’s driving prices up according to the Insurance Research Council (IRC).

Severe weather events and natural disasters are happening increasingly often, leading to more claims. At the same time, homebuilding materials and labor are more expensive. So, when it comes time to work on those claims, insurers have to manage higher costs to repair or rebuild the affected homes.

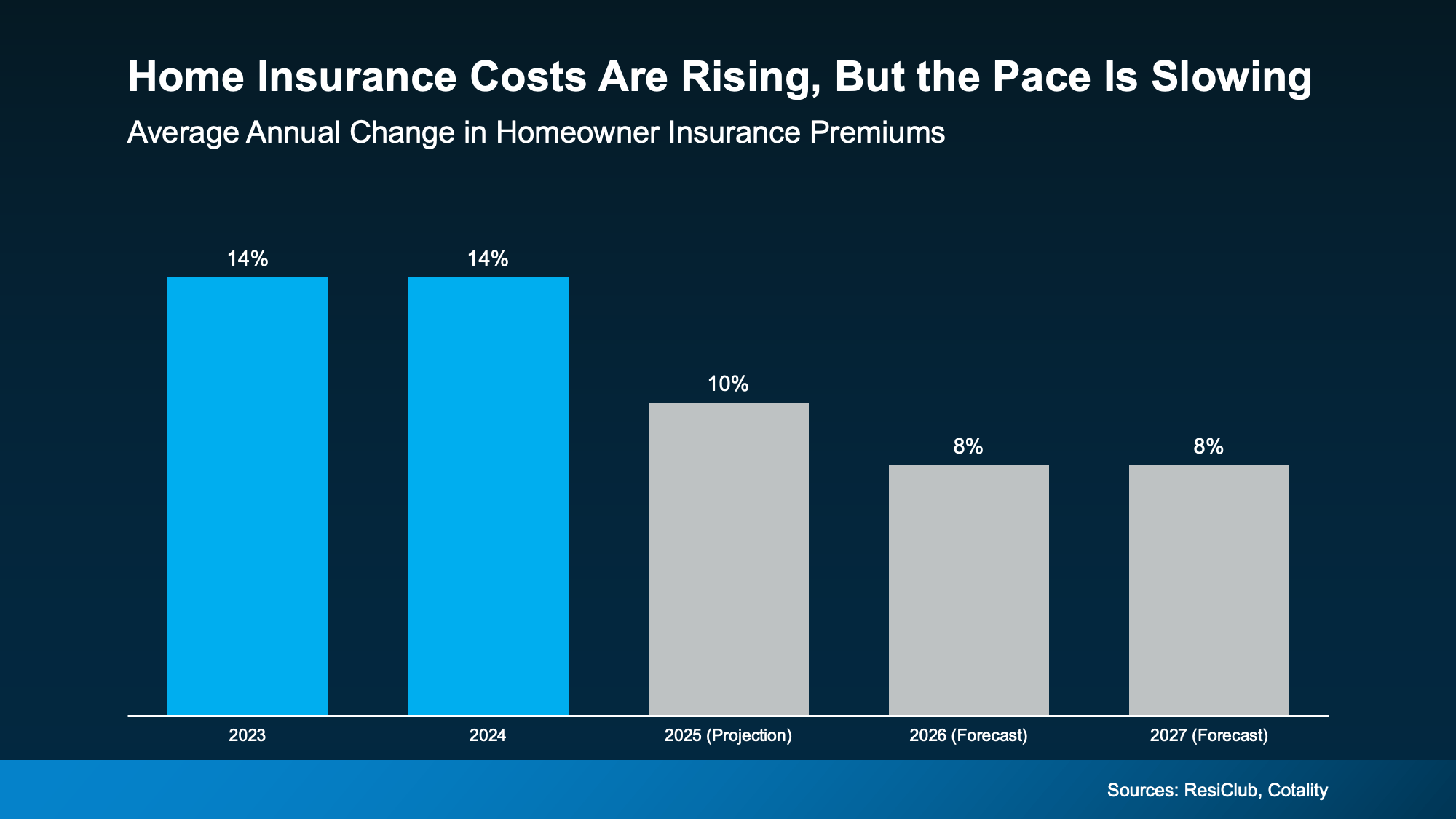

That combination adds up to higher premiums. You can see how it’s climbed recently in the graph below. Each bar marks the percentage increase in insurance costs for that calendar year.

The good news is, the annual pace of the increase may be starting to ease according to ResiClub and Cotality. By their count:

The good news is, the annual pace of the increase may be starting to ease according to ResiClub and Cotality. By their count:

- In 2023 and 2024, insurance costs went up 14% a year.

- In 2025, they rose about 10%.

- And in 2026 and 2027, it’s expected to go up about 8% each year.

That’s still an increase, but at least the pace is slowing down. And here’s another silver lining.

While insurance costs are rising, mortgage rates are falling. And that can help offset some of this expense. As Michael Gaines, Senior VP of Capital Markets, Cardinal Financial, explains:

“Rising taxes and insurance do create pressure, but they don’t erase the benefits of a lower rate . . . A small rate improvement, paired with the right loan program and smart planning, can still make homeownership possible . . . It’s less about one factor canceling another out, and more about helping buyers layer the right solutions together.”

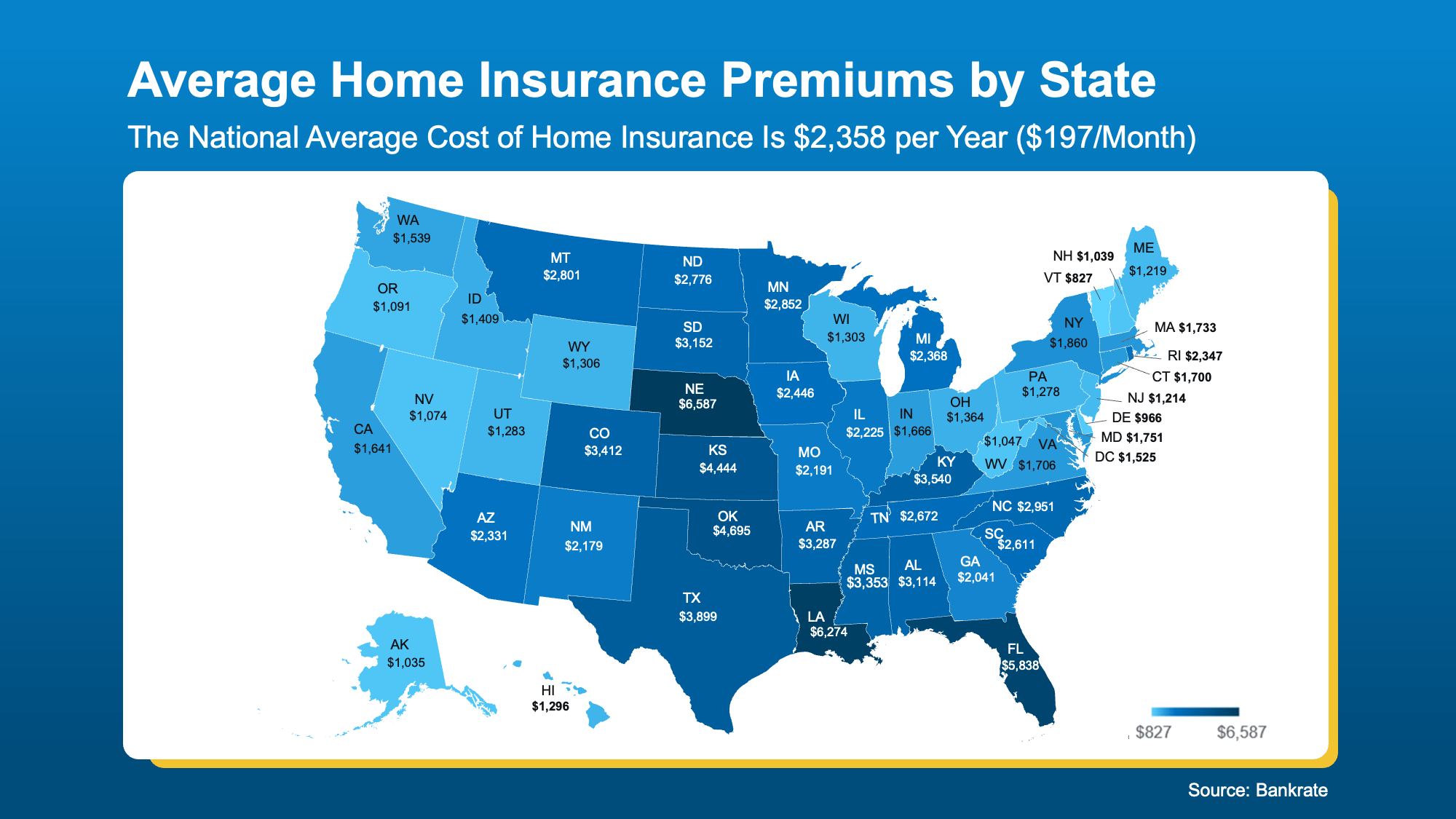

Costs Are Going To Be Different Depending on Where You Buy

So how much do you need to budget for this? It depends on the price point and location of house, the coverage you need, and more. And just like with everything else in real estate, costs vary by area.

You can get a rough idea of your state’s typical premiums in the map below:

So, What Can You Do About It?

So, What Can You Do About It?

Generally speaking, your first insurance payment will be wrapped into your closing costs. But after that, it’ll become a recurring expense. That’s why knowing these premiums are rising is so important. It helps you factor that into your budget, so you go in with a full picture of what you can comfortably afford.

If you’re crunching the numbers and trying to find other ways to save, here are a few tips from Insurify and NerdWallet that can help you get the best insurance price possible:

- Shop Around – Compare quotes from multiple companies.

- Bundle Policies – Combine home and auto for discounts.

- Ask About Discounts – Don’t miss out on savings you may qualify for.

- Highlight Upgrades – Features like a new roof or storm windows can cut costs.

- Improve Your Credit – A stronger credit score can mean better premiums.

Bottom Line

If you’re thinking about buying a home, don’t forget to plan ahead for your homeowner’s insurance.

While costs are rising, knowing what to expect and how to shop around can make a big difference as you’re budgeting for your purchase. Because this isn’t coverage you’ll want to skimp on. It’s your best protection for what’s likely your biggest investment.

When you see a house that’s been sitting on the market for a while, the reaction is almost automatic. You start thinking:

-

What’s wrong with it?

-

Why hasn’t anyone bought it yet?

-

Am I missing something?

That mindset made sense a few years ago. But in today’s market, you may actually miss out.

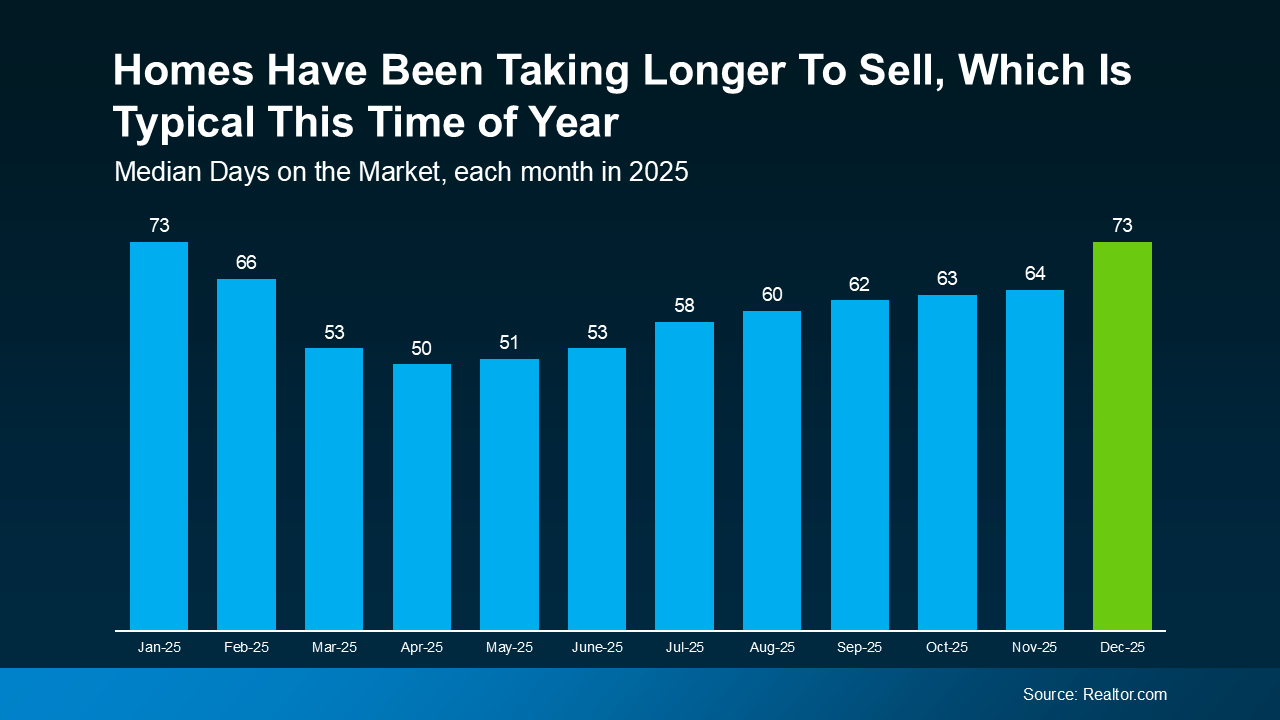

More Time on Market Isn’t Automatically a Concern Anymore

A few years ago, homes sold in just a matter of days. Sometimes, hours. Anything that lingered longer than that raised concerns. But that’s no longer the baseline.

Inventory has grown. Buyers have more choices. And homes are taking longer to sell across the board. Those are some of the reasons why the typical time it takes a home to sell has climbed this year:

And it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

And it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

That shift alone explains a lot of what you’re seeing. It’s not necessarily that there’s anything wrong with the house itself. Although, let’s be honest, sometimes that is the case.

Most of the time today, a house that’s taking longer to sell simply means:

-

There are a lot of homes for sale in that area

-

The seller priced a little too high at first

-

The home didn’t photograph as well online

-

Buyers passed it over for flashier listings nearby

-

The timing just wasn’t right when it first hit the market

None of those are necessarily deal-breakers.

What Buyers Often Get Wrong About These Listings

Because even though you may assume a house that hasn’t sold must have hidden issues, the reality is, that’s not always the case. And, if the house does have issues, it’ll show up quickly in your inspection.

That’s information you can use to negotiate. Not a reason to walk away automatically. And in many cases, that’s where buyers find the best deals.

The key is knowing which homes that have been sitting for a while are worth a second look – and which ones aren’t. That’s why working with a local agent makes a real difference. They’ll be able to look at disclosures and more to help you uncover hidden gems other buyers may overlook.

Bottom Line

A home sitting on the market isn’t always a warning sign. Sometimes it’s an overlooked opportunity.

If you want help identifying which homes are worth a second look (and which ones to skip), talk to a local agent.

One Key Sign We’re Not Headed for a Wave of Foreclosures

If Your House Isn’t Getting Offers, Read This.

Should You Wait for Lower Rates?

-

Affordability3 weeks ago

Affordability3 weeks agoRenting vs. Buying: The Numbers Might Surprise You

-

For Sellers4 weeks ago

For Sellers4 weeks agoThe Real Reason Home Sales Slowed in January. And It’s Not What You Think.

-

For Sellers3 weeks ago

For Sellers3 weeks agoTop Mistakes Homeowners Are Making in 2026 (And How To Avoid Them)

-

Equity3 weeks ago

Equity3 weeks agoHow Your Equity Could Help Younger Generations Buy a Home

-

For Buyers4 weeks ago

For Buyers4 weeks agoMove-Up Buyers Are Choosing New Construction

-

Agent Value4 weeks ago

Agent Value4 weeks agoThe Price You Set Can Make (or Break) Your Sale

-

Downsize2 weeks ago

Downsize2 weeks agoThe Hidden Advantage Repeat Buyers Have Right Now

-

For Sellers2 weeks ago

For Sellers2 weeks agoSpring Sellers Have an Edge. Here’s Why.

You must be logged in to post a comment Login