Buying Tips

Pre-Approval Isn’t Commitment – It’s Clarity

Mortgage rates have been volatile lately. And if you’re thinking about buying a home, that can make it harder to plan. But there are still things you can do to get the best rate possible in today’s market. It starts with having the right information.

So, what’s causing the bumps in rates? And what can you do about it? Let’s break it down.

Mortgage Rate Volatility Is Normal

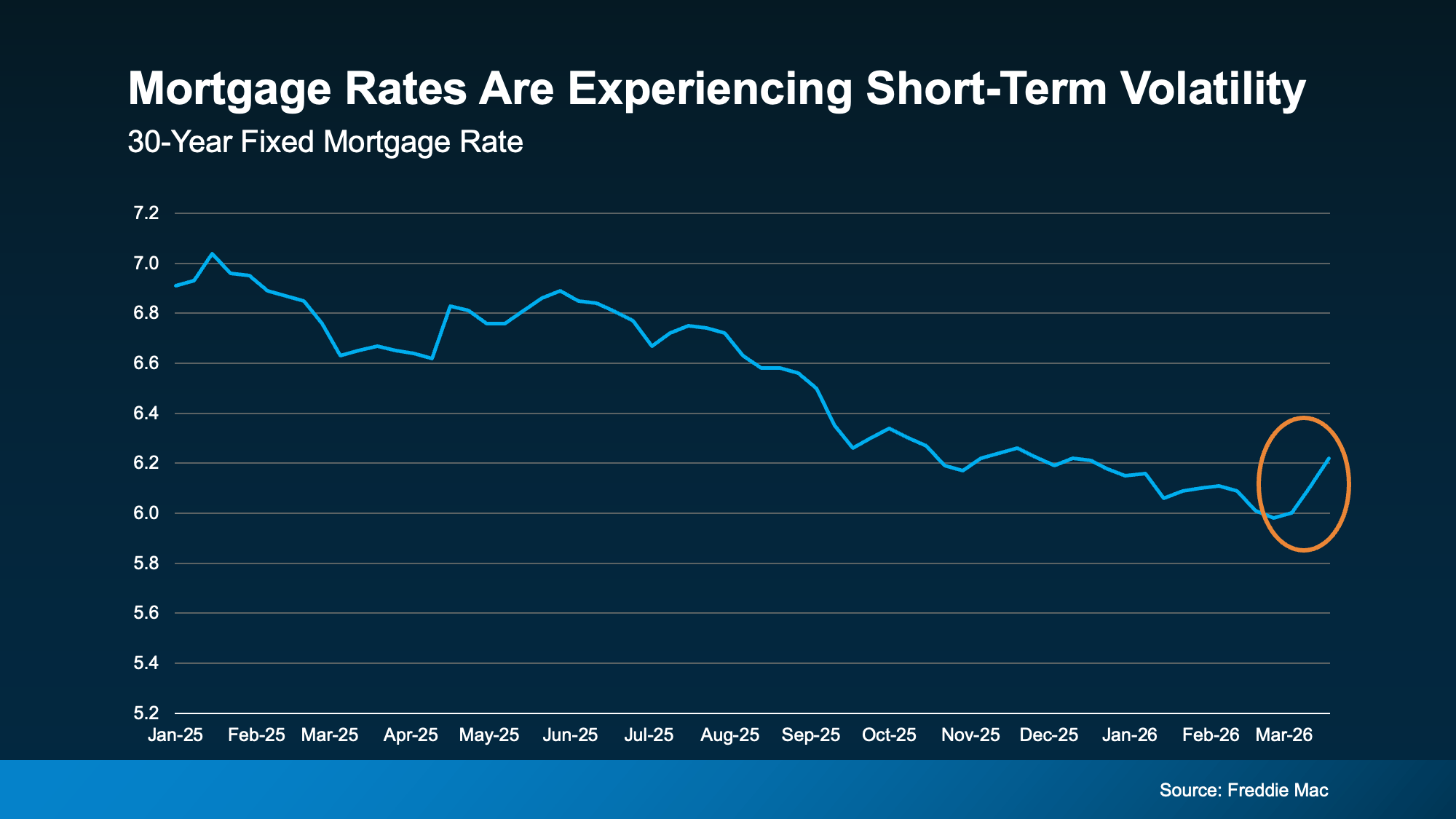

Data from Freddie Mac shows the recent volatility. After trending down for well over a year, there was a rise this month (see graph below):

While it’s easy to be distracted by the changes, here’s what you need to remember.

It’s normal for rates to bounce around a bit here and there. For example, if you look back at the graph, you’ll see that even within the past year there have been times like this when rates inched up. We’re in one of those moments right now and you need to be aware of that.

Especially when there’s economic uncertainty or big global events happening, volatility like this is expected. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

And that’s one of the reasons why trying to time the market isn’t a wise move.

You can’t control what happens with mortgage rates. But there are still things you can do to help you get the best rate possible in today’s market. And here’s where to focus your effort.

Your Credit Score

Your credit score plays a big role in the rate you qualify for. Even a small improvement can make a noticeable difference in your monthly payment. As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

So, make sure you do what you can to keep your credit score up. If you’re not sure what your score is or how you can improve it, talk to a trusted loan officer.

Your Loan Type

There are also different types of home loans – and each one can have unique requirements, benefits, and rates for qualified buyers. The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

That’s why it’s so important to explore your options with a lender. You may even want to talk to multiple lenders to see how the options vary.

Your Loan Term

The length of your loan matters too. Most lenders typically offer 15, 20, or 30-year loans. Freddie Mac offers this advice:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Again, to figure out what makes the most sense for your budget and long-term goals, have a lender walk you through all your options.

Bottom Line

Thinking about buying right now? The best advice is to accept that you can’t control where rates are going to go from here.

What you can do is work with a trusted lender and take steps that’ll help you get the best rate possible.

So, if you want to move today, talk to an agent and a lender to make it happen. You just need to control the controllables and focus where it counts.

If you’re planning to buy a home this year, you may be focused on the spring market. And hoping that when spring does hit, you’ll see:

- Mortgage rates drop a little more.

- More homes hit the market.

But here’s what most buyers don’t realize. Buying just a few weeks earlier could mean paying less, dealing with less stress, and feeling less rushed.

Here are three reasons why accelerating your timeline over the next few weeks could actually be a better play.

1. Holding Out for Lower Rates May Pay Off

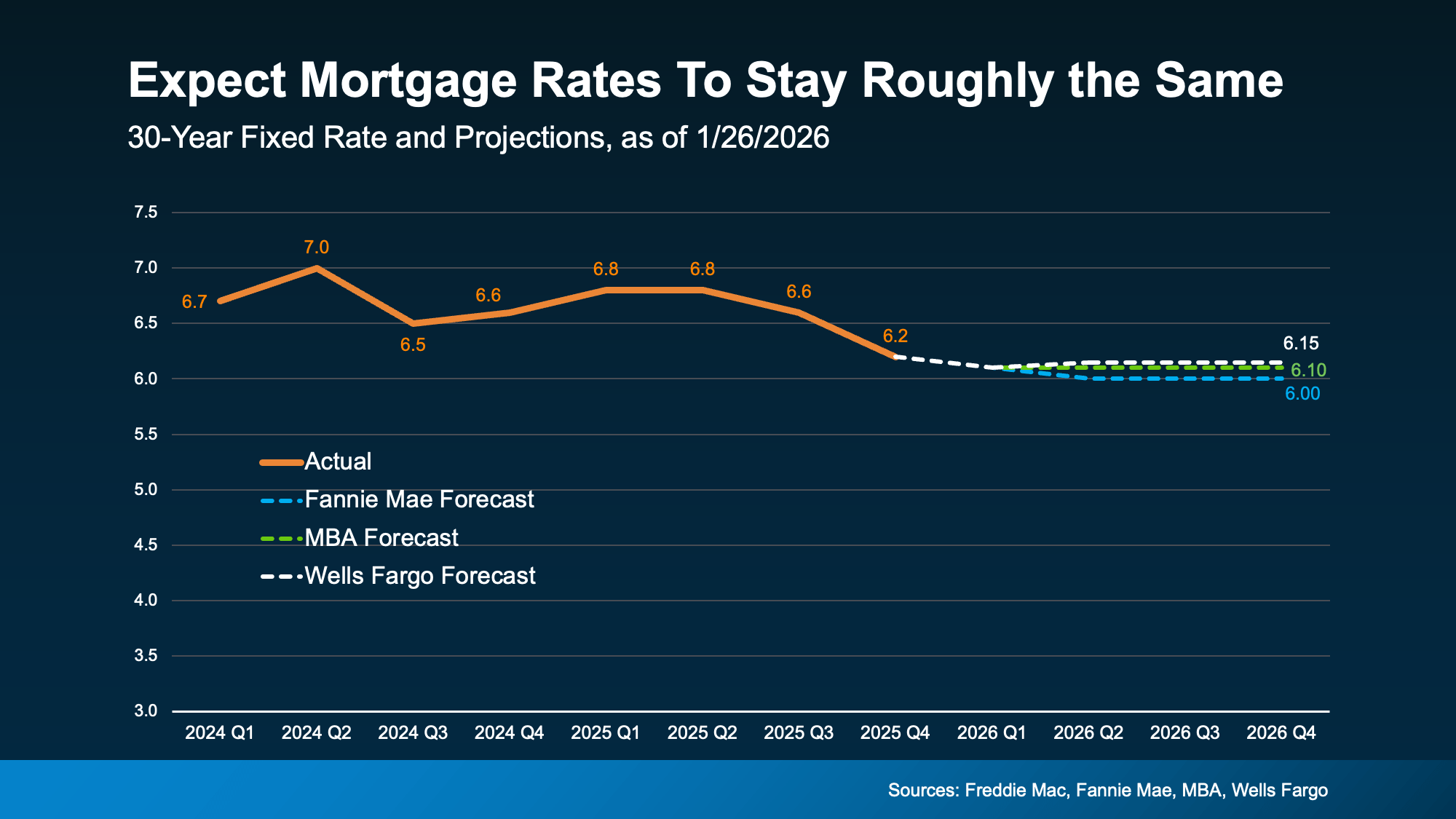

A lot of buyers are hoping mortgage rates will fall even further. But that’s not the best strategy. Here’s why. Experts are pretty aligned on this: rates are expected to stay roughly where they are.

Forecasts throughout the industry all point to the same thing: rates are projected to be in the low-6% range this year (see graph below):

That’s not a bad thing, especially if you consider how much rates have already come down. Over the past 12 months, they’ve dropped roughly a full percentage point. And for many buyers, that means affordability has already improved more than they may realize.

That’s not a bad thing, especially if you consider how much rates have already come down. Over the past 12 months, they’ve dropped roughly a full percentage point. And for many buyers, that means affordability has already improved more than they may realize.

So why wait a few more weeks just for more buyers to jump in and act as your competition? You already have a window right now. As Chen Zhao, Head of Economics Research at Redfin, explains:

“House hunters should know that this may be near the lowest mortgage rates fall for the foreseeable future.”

2. Spring Means More Competition + More Stress

Speaking of competition, the spring market is popular for a reason, but with popularity comes pressure. With more buyers active at that time of year, you’ll have to move faster once you find a home you like. And no one likes feeling rushed.

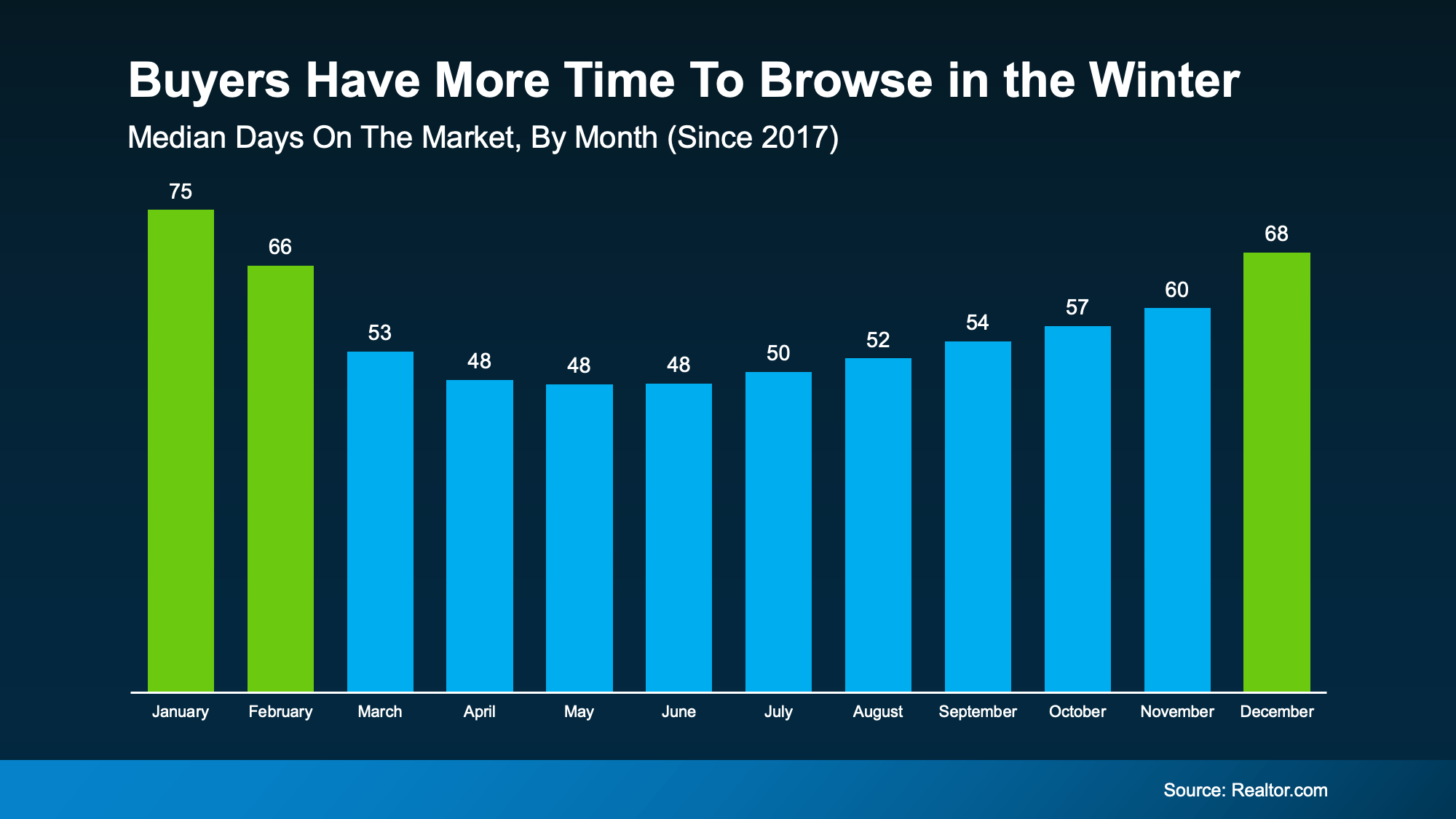

But buy now and you have more time to browse. Fewer people are looking, so homes sit longer.

You can see this play out in the data from Realtor.com (see graph below). In winter months, it takes an average of about 70 days for a home to sell. In spring? That drops to about 50 days. That’s a 20-day swing – and that pace is going to be more stressful.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

3. Prices Tend To Rise When Competition Heats Up

And here’s something most buyers forget to factor in. Prices usually respond to demand. So, when demand is higher, prices are too. Bankrate explains:

“Spring and early summer are the busiest and most competitive time of year for the real estate market . . . home prices tend to be steeper to reflect the increased demand.”

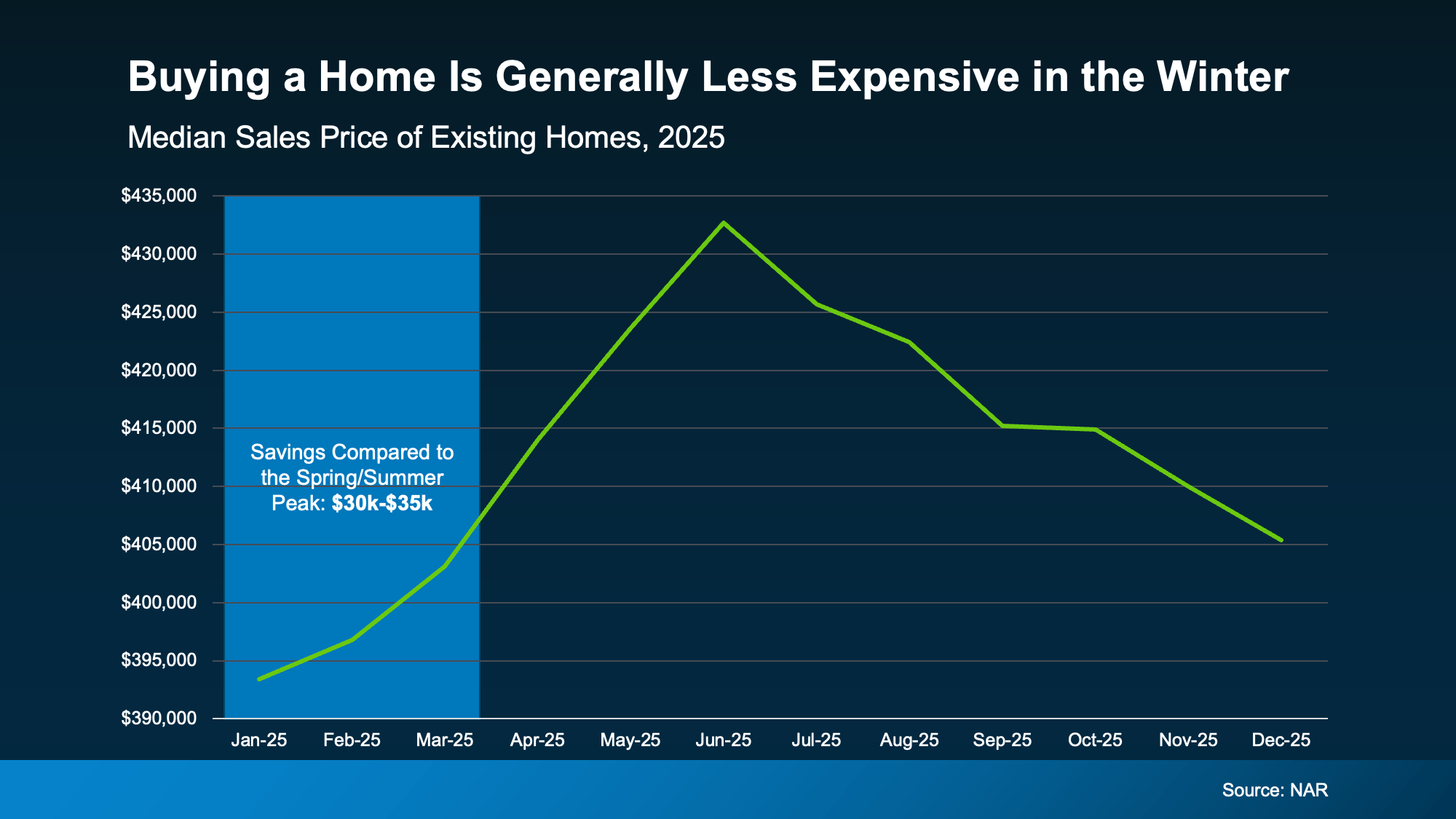

In fact, data from the National Association of Realtors (NAR) shows that in 2025, buyers who purchased in the beginning of the year saved roughly $30,000–$35,000 compared to those who bought when prices peaked in the spring or early summer.

And let’s be honest, for a lot of buyers today, every little bit of savings helps. That’s why buying just a few weeks earlier, before prices ramp up, will be better for you and your wallet.

And let’s be honest, for a lot of buyers today, every little bit of savings helps. That’s why buying just a few weeks earlier, before prices ramp up, will be better for you and your wallet.

Bottom Line

Buying a few weeks before spring isn’t about rushing. It’s about choosing to be ahead of the curve and knowing you want more leverage, less stress, and meaningful savings.

If you’re ready and able to buy now and want to get the ball rolling, connect with a local agent.

You Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

The Remodel You’ve Been Dreaming About May Be Closer Than You Think

Affordability Has Improved in All 50 States

-

Affordability4 weeks ago

Affordability4 weeks agoRenting vs. Buying: The Numbers Might Surprise You

-

For Sellers4 weeks ago

For Sellers4 weeks agoTop Mistakes Homeowners Are Making in 2026 (And How To Avoid Them)

-

For Sellers3 weeks ago

For Sellers3 weeks agoSpring Sellers Have an Edge. Here’s Why.

-

Downsize3 weeks ago

Downsize3 weeks agoThe Hidden Advantage Repeat Buyers Have Right Now

-

Equity3 weeks ago

Equity3 weeks agoAre Home Prices Dropping? Here’s the Real Story.

-

Agent Value2 weeks ago

Agent Value2 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability2 weeks ago

Affordability2 weeks agoShould You Wait for Lower Rates?

-

For Buyers2 weeks ago

For Buyers2 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

You must be logged in to post a comment Login