For Buyers

Is It Better To Buy Now or Wait for Lower Mortgage Rates? Here’s the Tradeoff

Mortgage rates are still a hot topic – and for good reason. After the most recent jobs report came out weaker than expected, the bond market reacted almost instantly. And, as a result, in early August mortgage rates dropped to their lowest point so far this year (6.55%).

While that may not sound like a big deal, pretty much every buyer has been waiting for rates to fall. And even a seemingly small drop like this reignites the hope we’re finally going to see rates trending down. But what’s realistic to expect?

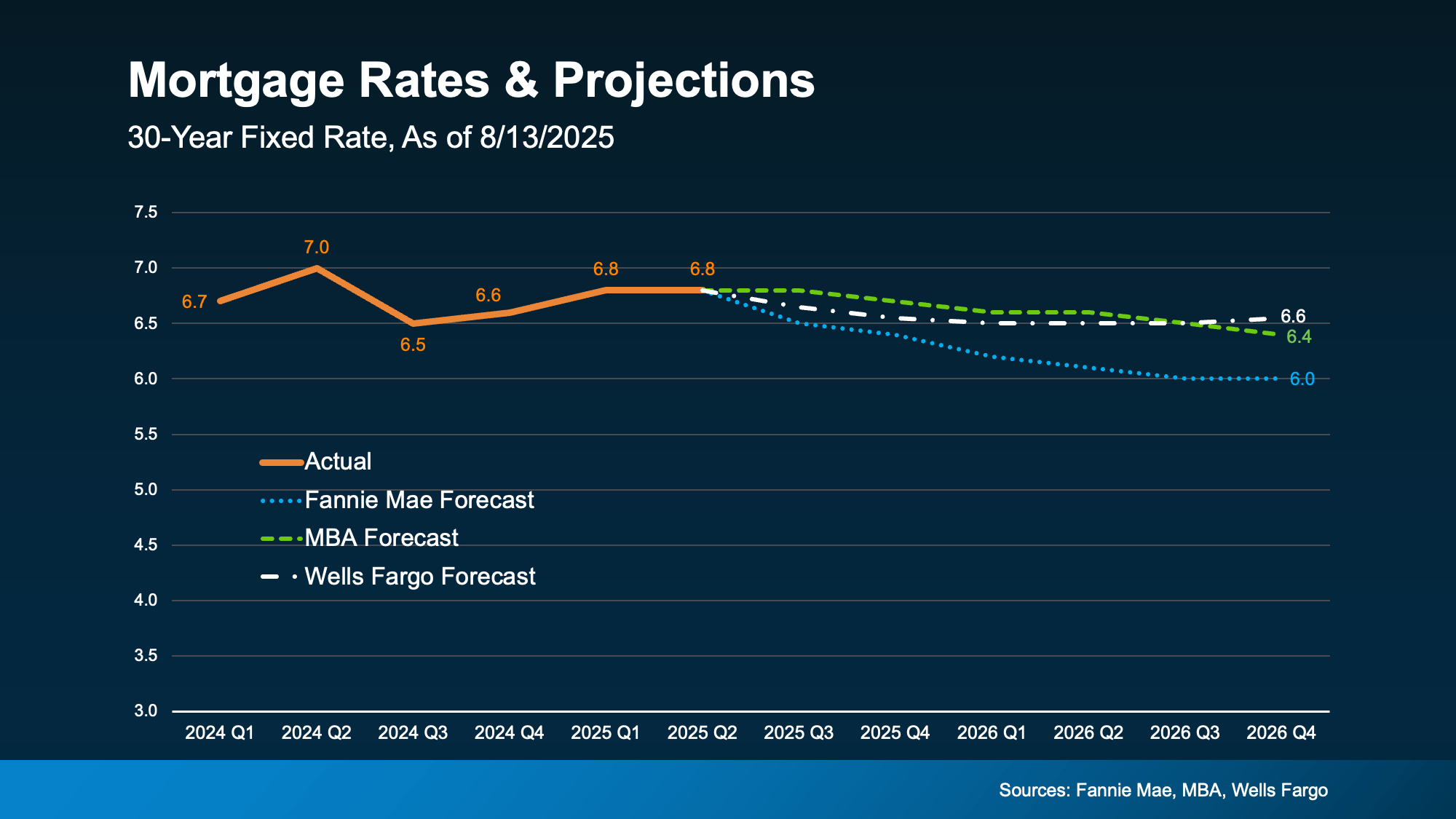

According to the latest forecasts, rates aren’t expected to fall dramatically anytime soon. Most experts project they’ll stay somewhere in the mid-to-low 6% range through 2026 (see graph below):

In other words, no big changes are expected. But small shifts, like the one we just saw, are still likely.

In other words, no big changes are expected. But small shifts, like the one we just saw, are still likely.

Each time there’s changing economic news, there’s a chance mortgage rates will react. And with so many reports coming out this week, we’ll get a better feeling of where the economy and inflation are headed – and how rates will respond.

What Rate Would Get Buyers Moving Again?

The magic number most buyers seem to be watching for is 6%. And it’s not just a psychological benchmark; it has real impact. A recent report from the National Association of Realtors (NAR) says if rates reach 6%:

- 5.5 million more households could afford the median-priced home

- And roughly 550,000 people would buy a home within 12 to 18 months

That’s a lot of pent-up demand just waiting for the green light. And if you look back at the graph above, you’ll see Fannie Mae thinks we’ll hit that threshold next year. That raises an important question: Does it really make sense to wait for lower rates?

Because here’s the tradeoff. If you’re waiting for 6%, you need to realize a lot of other people are too. And when rates do continue to inch down and more buyers jump into the market all at once, you could face more competition, fewer choices, and higher home prices. NAR explains it like this:

“Home buyers wishing for lower mortgage interest rates may eventually get their wish, but for now, they’ll have to decide whether it’s better to wait or jump into the market.”

Consider the unique window that exists right now:

- Inventory is up = more choices

- Price growth has slowed down = more realistic pricing

- You may have more room to negotiate = you could get a better deal

These are all opportunities that will go away if rates fall and demand surges. That’s why NAR says:

“Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.”

Bottom Line

Rates aren’t expected to hit 6% this year. But when they do, you’ll have to deal with more competition as other buyers jump back in. If you want less pressure and more negotiating power, that opportunity is already here – and it might not last for long. It all depends on what happens in the economy next.

Talk to a local agent about what’s happening in your area and whether it makes sense to make your move now, before everyone else does.

For a lot of people, the math on buying a home just doesn’t really work right now. Maybe that’s how it feels for you too. You look at the cost of buying. Then you look at the cost of childcare. And it starts to feel like you have to choose one or the other.

But some families are finding a way to make both work by doing something a little different: teaming up to purchase a multi-generational home.

One Reason This Is Becoming More Common

It’s no secret that affordability has been a challenge in recent years. But for families with young kids, there’s an added layer that can make it feel even harder: childcare.

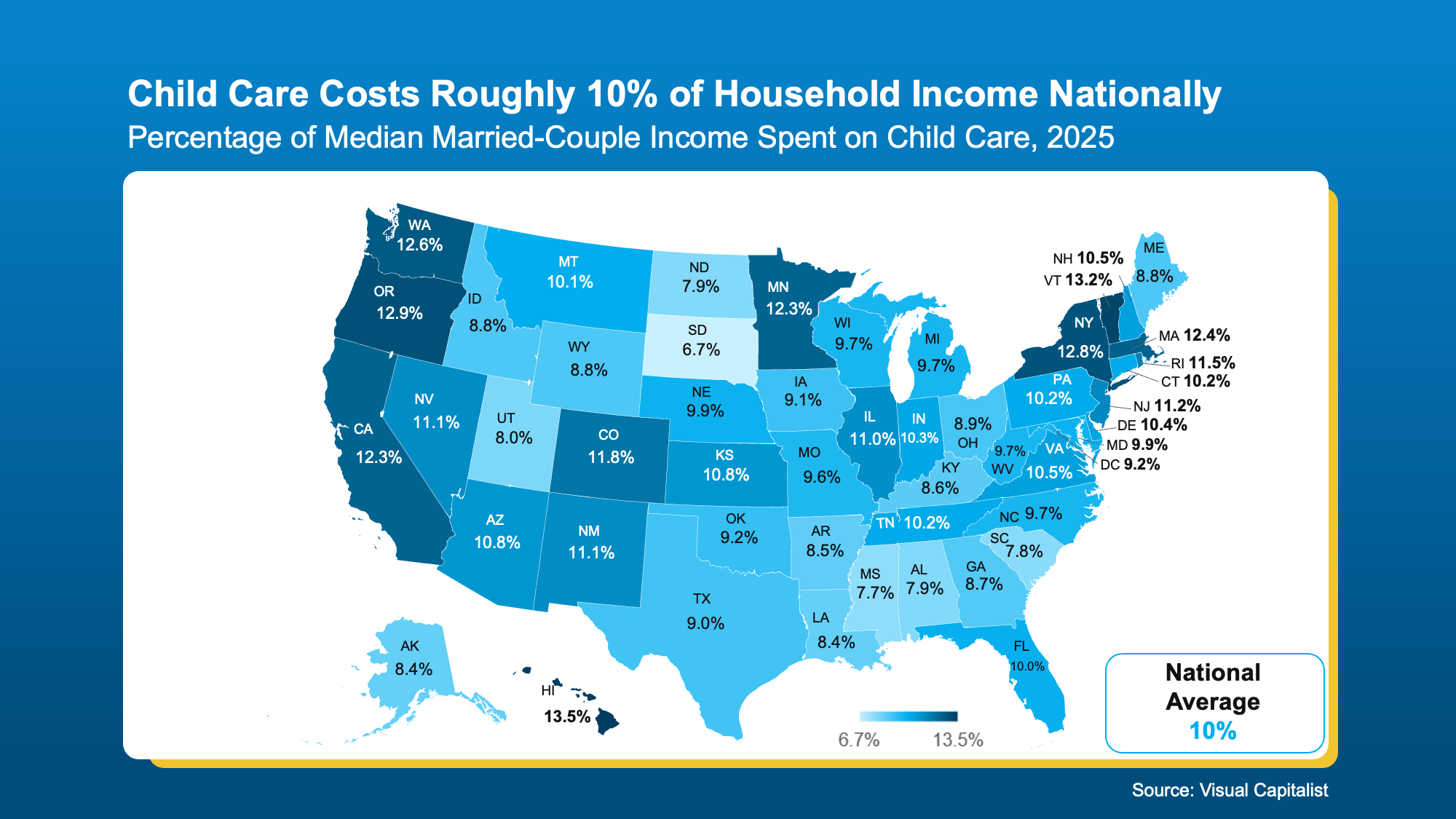

According to the Department of Health and Human Services, childcare should take up no more than 7% of your monthly income. But in reality, the average married couple spends closer to 10% (see map below):

When you combine that with the cost of buying a home, it’s easy to see why things can feel stretched. That’s exactly why more families are starting to rethink how they approach both.

When you combine that with the cost of buying a home, it’s easy to see why things can feel stretched. That’s exactly why more families are starting to rethink how they approach both.

The Solution More People Are Turning To: Multi-Generational Living

One option gaining traction? Multi-generational living. That’s when parents, grandparents, or other relatives buy a house together and live under the same roof. And it’s not just about convenience anymore. It’s becoming a go-to strategy.

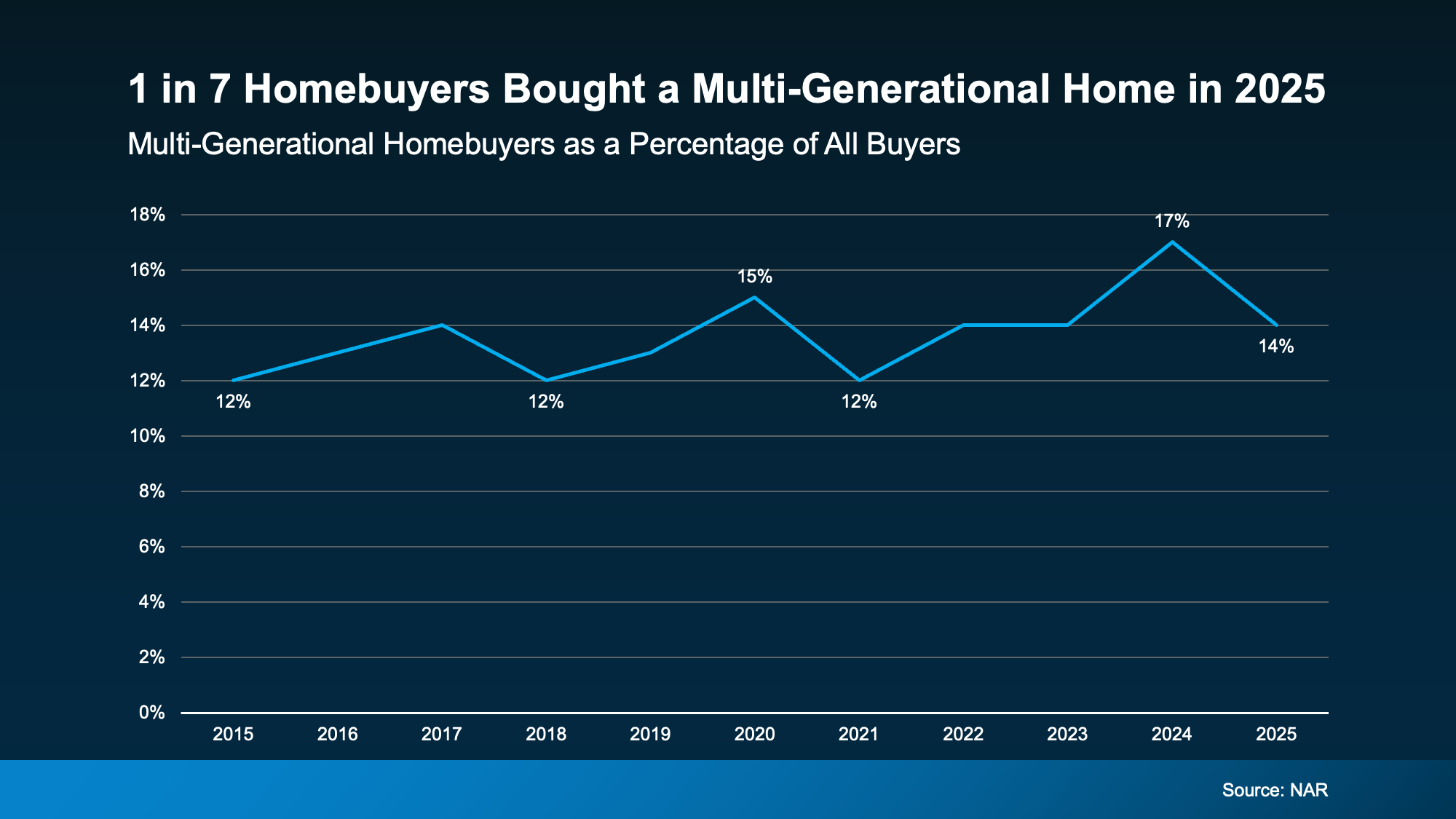

You can see it in the data. According to the National Association of Realtors (NAR), almost 1 in 7 homebuyers (14%) bought a multi-generational home in 2025 (see graph below):

And for the first time, childcare is showing up as a key reason why they chose this option. As NAR explains:

And for the first time, childcare is showing up as a key reason why they chose this option. As NAR explains:

“This year’s report features two new primary reasons for purchasing a multi-generational home: grandchildren living in the home (12%) and to help reduce the cost of childcare (6%).”

Why It Works

Buying a multi-generational home solves two big challenges at the same time.

- First, it shares the financial responsibility. If you pool multiple incomes together, you may be able to afford a home you couldn’t have on your own.

- Second, it can also solve the childcare puzzle. When grandparents or other relatives live in the home, they may be able to help with daily care – which can significantly reduce or even eliminate daycare costs.

And for many people, that combination is what finally makes their move possible.

If the costs of childcare and housing together have made buying feel out of reach right now, it may be worth exploring creative options like buying a home with your loved ones.

Bottom Line

If you want more information on multi-generational homes, talk to a local agent about what’s available in your area.

Sometimes the path to homeownership isn’t doing it alone. It’s doing it together.

If you’ve been looking for a home lately, you’ve probably felt how tough affordability still is. And that’s exactly why more buyers are opting for adjustable-rate mortgages, or ARMs.

Here’s what you need to understand about how they work, and whether they make sense for you.

What Is an Adjustable-Rate Mortgage?

Since a lot of people aren’t familiar with this type of loan, let’s start with a definition. This is how Business Insider explains the main difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Basically, one doesn’t change much over the life of your loan.

And one could change… either by a little, or a lot.

Of course, things like taxes or homeowner’s insurance can still have an impact on a fixed-rate loan, but the baseline of your mortgage payment is fairly steady. But the big difference is that with an ARM, your monthly payment could change over time.

Why Adjustable-Rate Mortgages Are Getting More Attention

So, why do some buyers choose this option? It’s simple. It’s because of the upfront savings. Business Insider explains it like this:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

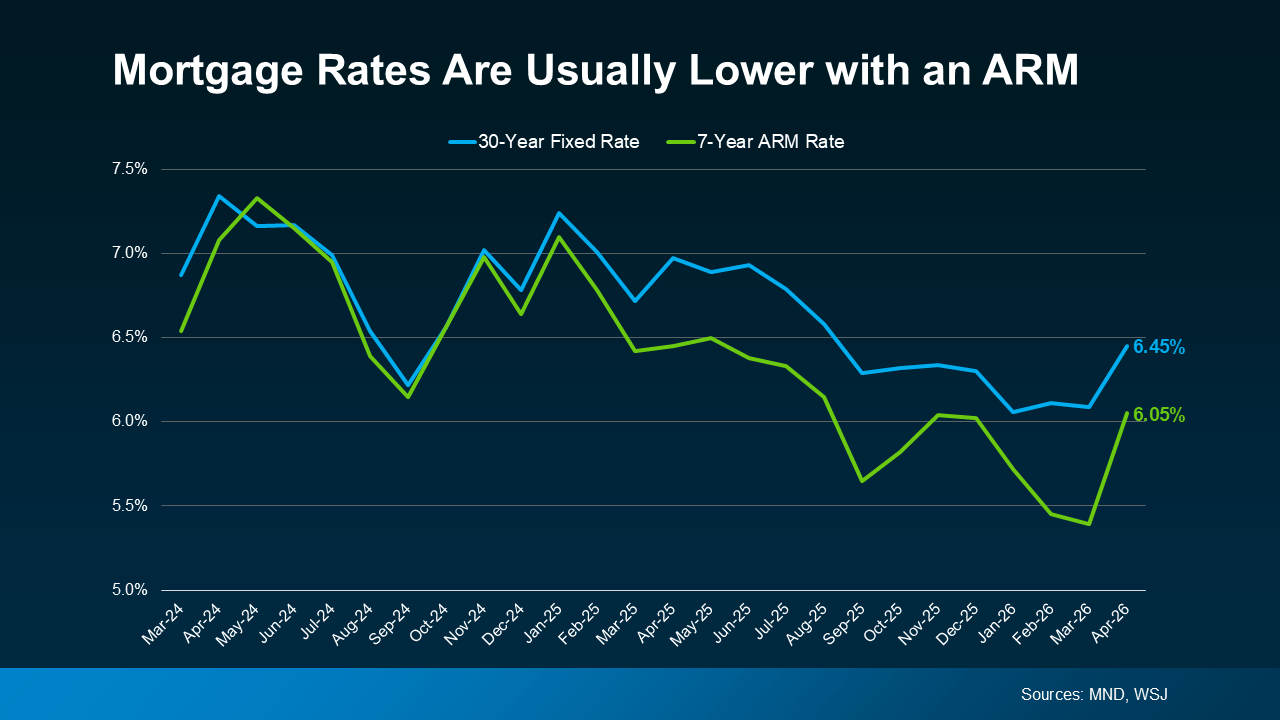

And right now, according to Mortgage News Daily and the Wall Street Journal, the upfront rate on an ARM is lower than a 30-year fixed mortgage (see graph below):

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

For some people, that’s enough to make a difference.

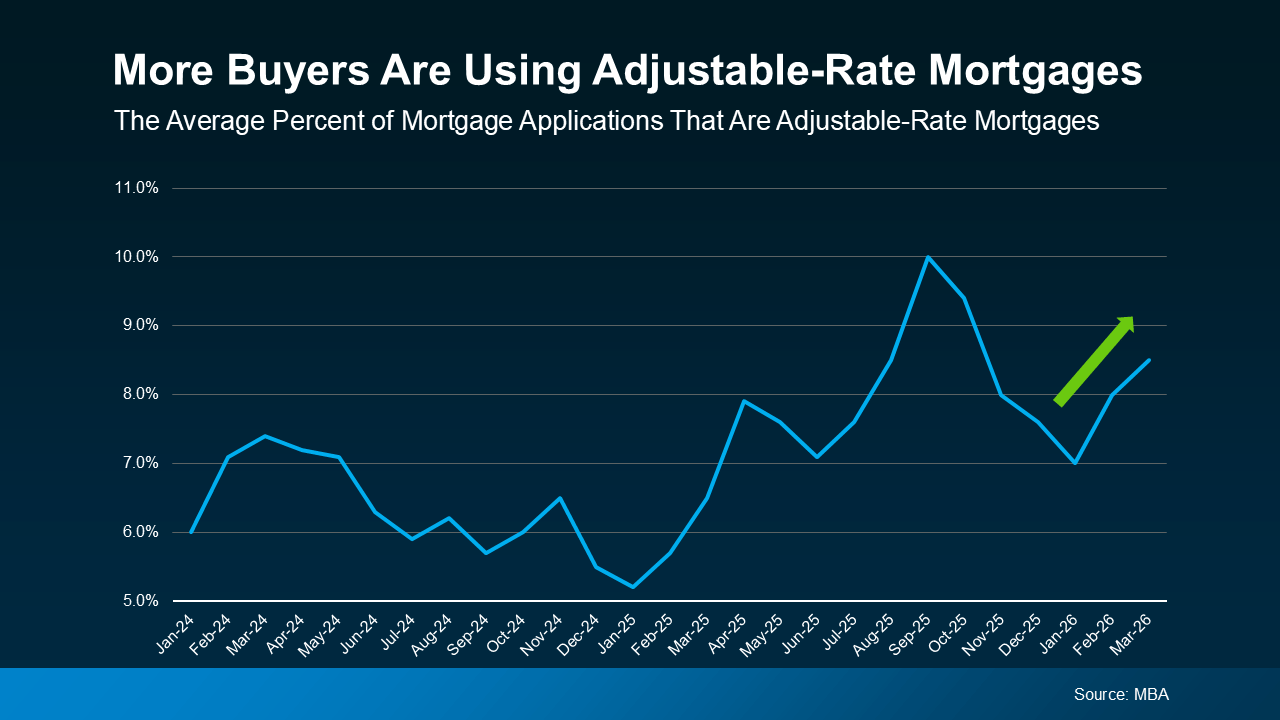

More Buyers Are Choosing Adjustable-Rate Mortgages Today

A growing number of buyers are willing to trade the uncertainty later for a lower payment now. Data from the Mortgage Bankers Association (MBA) shows the share of buyers choosing ARMs has increased, especially over the last few years (see graph below).

This doesn’t mean ARMs are becoming the go-to option for everyone. It only means some buyers are opting for this type of mortgage, so they can still buy today.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

Back then, some buyers were given loans they couldn’t afford once rates adjusted.

Today, lending standards are stricter, and lenders evaluate whether borrowers could still handle the payment if rates rise. So, the return of ARMs doesn’t signal another widespread crash. It just reflects how some buyers are adapting to today’s affordability challenges.

The Trade-Off – What You Need To Consider

If you’re considering an adjustable-rate mortgage yourself, just remember it really all depends on your situation and your risk tolerance.

An ARM may make sense if you plan to move before your rate would adjust or if you expect you’ll make a higher income in the future. But there are trade-offs you need to think through.

For example, once the fixed period ends, your rate can adjust, and your payment could increase, potentially by a meaningful amount depending on where rates are at that time.

And keep in mind, there’s also no guarantee mortgage rates will come down in the future, which means refinancing later isn’t always an option. That’s why it’s important to think through your plan, understand your long-term earning potential, and work closely with a trusted lender before you choose an ARM.

Bottom Line

ARMs are getting more attention again because they can make buying a home more affordable in the short term. But they’re not right for everyone.

The key is understanding how they work, what the risks are, and whether they fit your plan. And that’s why you need to talk to a trusted lender and financial advisor before you make any decisions.

When Buying a Home Feels Out of Reach, Some Families Do This Instead

Thinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

Your House Hasn’t Sold Yet. Should You Rent It Out Instead?

-

For Buyers2 weeks ago

For Buyers2 weeks agoDon’t Let Home Prices Headlines Fool You

-

Agent Value4 weeks ago

Agent Value4 weeks agoThe #1 Reason Buyers Walk Away (And How To Get Ahead of It)

-

Affordability3 weeks ago

Affordability3 weeks agoAffordability Has Improved in All 50 States

-

Agent Value4 weeks ago

Agent Value4 weeks ago3 Must-Do’s for First-Time Home Buyers

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoYou Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

-

Equity3 weeks ago

Equity3 weeks agoThe Remodel You’ve Been Dreaming About May Be Closer Than You Think

-

For Sellers2 weeks ago

For Sellers2 weeks agoThe Best Week To List Your House Is Just Around the Corner

-

For Buyers2 weeks ago

For Buyers2 weeks agoThis’ll Change What You Think About Investors in Today’s Housing Market

You must be logged in to post a comment Login