For Buyers

Where Have All the Houses Gone?

In today’s housing market, it seems harder than ever to find a home to buy. Before the health crisis hit us a year ago, there was already a shortage of homes for sale. When many homeowners delayed their plans to sell at the same time that more buyers aimed to take advantage of record-low mortgage rates and purchase a home, housing inventory dropped even further. Experts consider this to be the biggest challenge facing an otherwise hot market while buyers continue to compete for homes. As Danielle Hale, Chief Economist at realtor.com, explains:

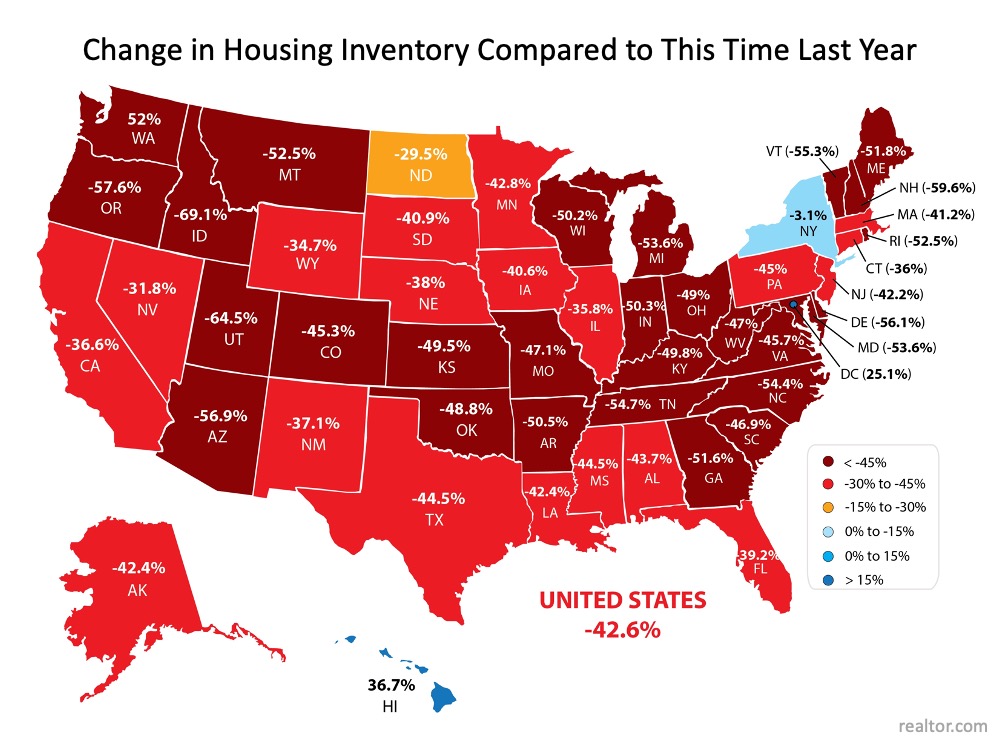

“With buyers active in the market and seller participation lagging, homes are selling quickly and the total number available for sale at any point in time continues to drop lower. In January as a whole, the number of for sale homes dropped below 600,000.”

Every month, realtor.com releases new data showing the year-over-year change in inventory of existing homes for sale. As you can see in the map below, nationwide, inventory is 42.6% lower than it was at this time last year:

Does this mean houses aren’t being put on the market for sale?

Not exactly. While there are fewer existing homes being listed right now, many homes are simply selling faster than they’re being counted as current inventory. The market is that competitive! It’s like when everyone was trying to find toilet paper to buy last spring and it was flying off the shelves faster than it could be stocked in the stores. That’s what’s happening in the housing market: homes are being listed for sale, but not at a rate that can keep up with heavy demand from competitive buyers.

In the same realtor.com report, Hale explains:

“Time on the market was 10 days faster than last year meaning that buyers still have to make decisions quickly in order to be successful. Today’s buyers have many tools to help them do that, including the ability to be notified as soon as homes meeting their search criteria hit the market. By tailoring search and notifications to the homes that are a solid match, buyers can act quickly and compete successfully in this faster-paced housing market.”

The Good News for Homeowners

The health crisis has been a major reason why potential sellers have held off this long, but as vaccines become more widely available, homeowners will start making their moves. Ali Wolf, Chief Economist at Zonda, confirms:

“Some people will feel comfortable listing their home during the first half of 2021. Others will want to wait until the vaccines are widely distributed.”

With more homeowners getting ready to sell later this year, putting your house on the market sooner rather than later is the best way to make sure your listing shines brighter than the rest.

When you’re ready to sell your house, you’ll likely want it to sell as quickly as possible, for the best price, and with little to no hassle. If you’re looking for these selling conditions, you’ll find them in today’s market. When demand is high and inventory is low, sellers have the ability to create optimal terms and timelines for the sale, making now an exceptional time to move.

Bottom Line

Today’s housing market is a big win for sellers, but these conditions won’t last forever. If you’re in a position to sell your house now, you may not want to wait for your neighbors to do the same. Let’s connect to discuss how to sell your house safely so you’re able to benefit from today’s high demand and low inventory.

You’ve probably asked yourself lately: Is it even worth trying to buy a home right now? It’s a question a lot of people are asking.

With today’s home prices and mortgage rates, renting can feel like the easier path. In some cases, it might even seem like the only realistic option right now. And if that’s where you are, there’s nothing wrong with that.

But if you’re weighing the decision, there’s one part of the conversation that doesn’t get talked about enough.

It’s what each choice does for your future.

What Renting Really Gets You (And What It Doesn’t)

Depending on your situation, renting does have some advantages:

- Lower upfront costs.

- Less responsibility.

- More flexibility to move when you want.

But even with those benefits, a Bank of America survey found 70% of aspiring homeowners worry about what long-term renting means for their future. And that concern comes down to one thing: you’re not building anything for your future. As Yahoo Finance explains:

“Paying rent doesn’t build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

So, while renting may feel easier, the flexibility you get comes at a cost.

How Homeownership Builds Your Wealth Over Time

On the other hand, owning a home is one of the most consistent ways people build wealth over time. Why? When you’re a homeowner, you gain something called equity. That’s the difference between what your home is worth and what you owe.

That equity grows with every monthly payment you make. It also gets a boost as home values go up through the years – and it adds up quicker than you may think.

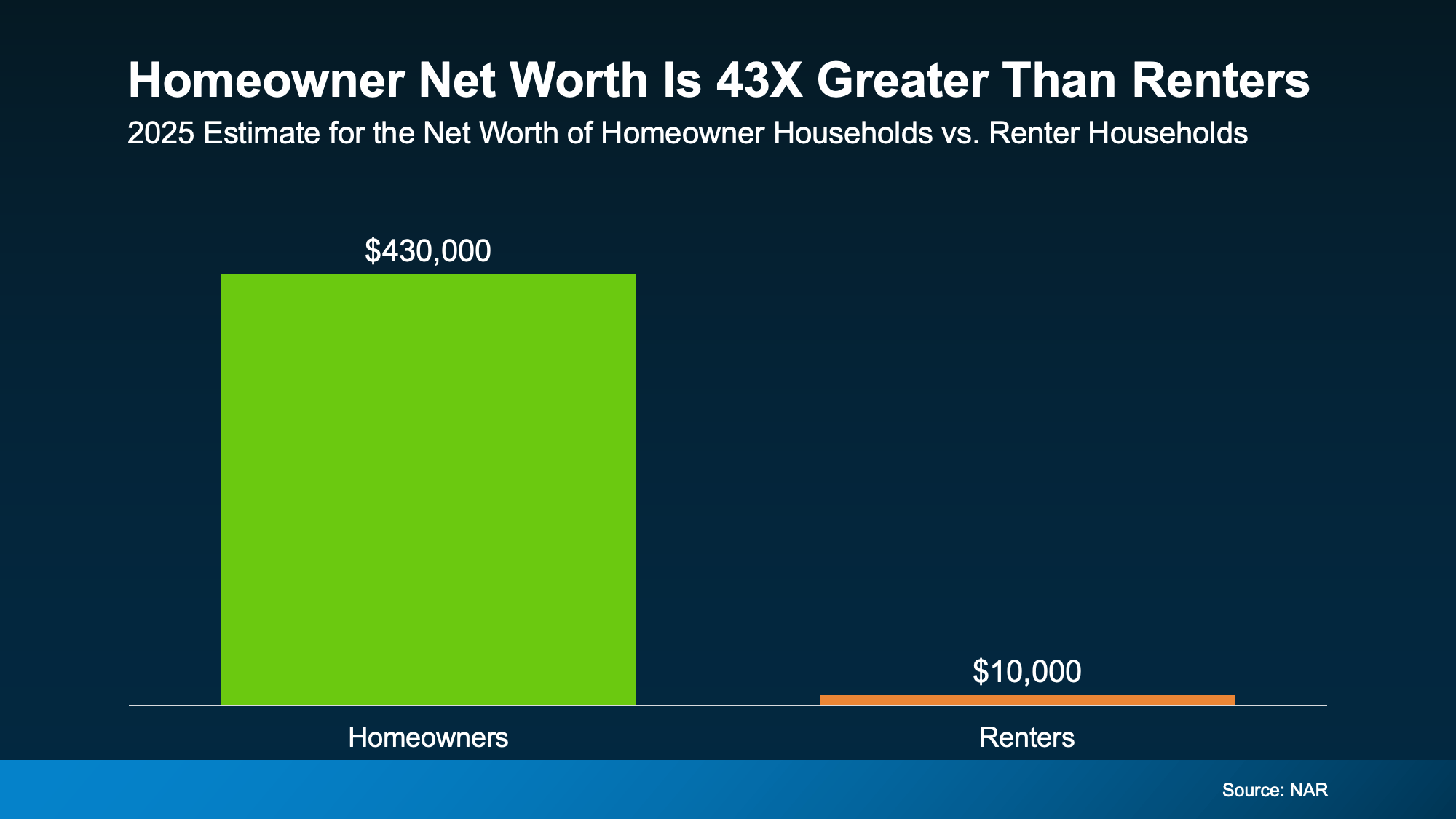

Today, the National Association of Realtors (NAR) says the average homeowner’s net worth is 43X greater than that of a renter:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

- Homeowners: $430k

- Renters: $10k

And it’s not because homeowners make wildly different decisions day to day. It’s because over time, one path builds something, and the other doesn’t.

So sure, buying comes with some upfront costs and more responsibility. But it’s basically a savings account you can live in.

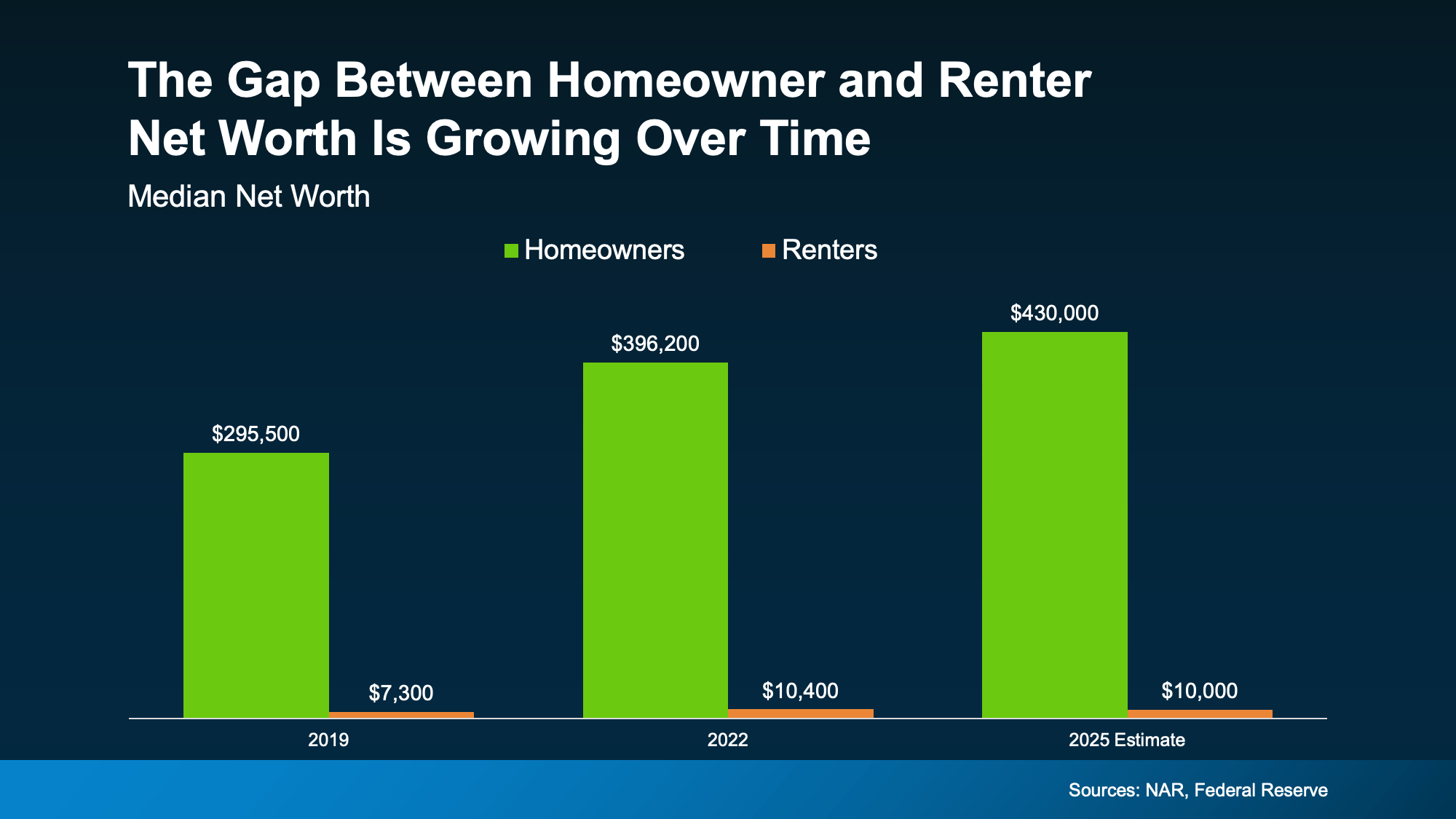

The Gap Is Growing Over Time

And here’s something else interesting. That net worth gap between renters and homeowners has been widening over time, not shrinking.

If you look back at the reports on net worth through the years, you can see the gap is growing as homeowners gain wealth and renters stay stuck in the rental trap (see graph below):

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

When you can afford it and you’re ready for the responsibility, history shows buying is usually worth it in the long run. Because either way, you’re paying for someone’s mortgage and building someone’s net worth.

When you rent, it’s your landlord’s mortgage – not yours. But when you buy? Your monthly payments help build equity.

The question is: whose do you want to pay? Yours or theirs?

So, Should You Buy a Home Now?

The short answer is, it depends on your situation.

While the long-term benefits of buying are clear, that doesn’t mean the timing is right for everyone right now. And that’s okay. You should only buy a home once you’re ready and the numbers work for you.

But whether you’re looking to buy now or planning for the future, the first step is the same. You should have a quick conversation with a local real estate agent about your goals, timeline, and budget.

They can help you run the numbers and see what’s realistic. You may find buying is closer than you thought. And if not, you’ll at least know exactly what it will take to get there.

Because the sooner you have a plan, the sooner you can decide when it makes sense, instead of wondering if it ever will.

Bottom Line

Renting may feel more do-able today. But over time, it could cost you.

If you want to ditch renting and start building something for your future, it starts with a simple conversation. Connect with a real estate agent to talk about your specific goals, and explore your options – so you’re ready when the time is right for you.

If you’re getting a tax refund this year, here’s something worth thinking about. That money could actually help you get closer to buying a home.

It may not be something you’ve factored into your plan yet, but it can give your savings a nice boost right when you need it most. And whether your refund is a few thousand dollars or more, there are some smart ways to put that money to work as you get ready to buy.

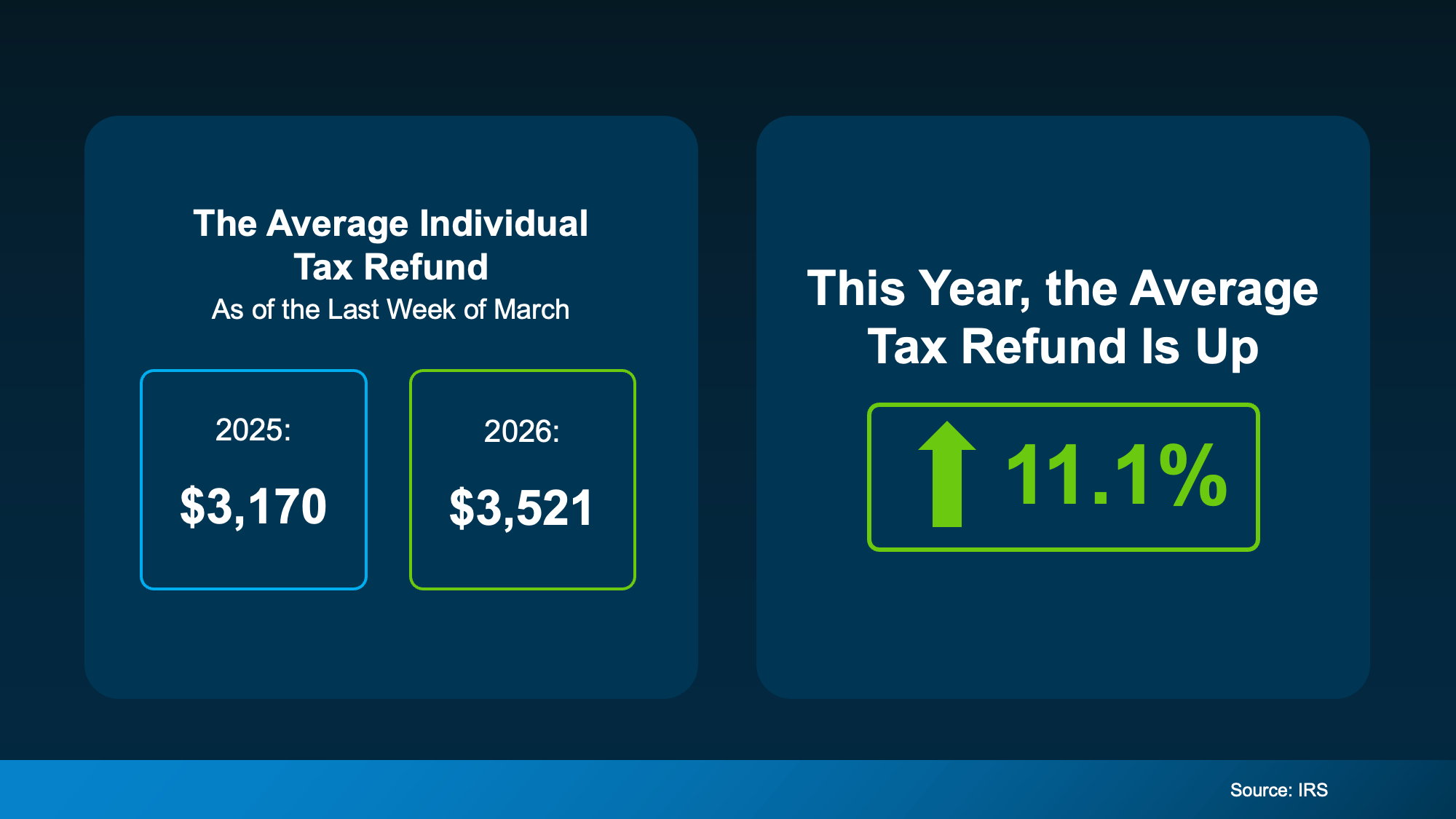

Your Refund May Be Even Bigger This Year

Let’s start with the good news. People are getting even more money back in their refunds than they did last year. The visual below uses data from the Internal Revenue Service (IRS) to show the average individual’s refund is 11.1% higher this year:

Of course, your exact refund will vary. But any extra money you get is a good thing, especially when affordability is still tight.

Of course, your exact refund will vary. But any extra money you get is a good thing, especially when affordability is still tight.

How You Can Use Your Tax Refund

So, how can you put that money to work? Here are a few smart ways to use your refund when buying a home, according to Freddie Mac:

- Put it toward your down payment. Data shows saving for a down payment is one of the biggest hurdles for first-time homebuyers. Using your refund can help you build that up faster. And the good news? You may not need to put as much down as you think.

- Use it for your closing costs. Closing costs usually range from about 2% to 5% of the home’s purchase price. Using your refund here can make things feel a lot more manageable on closing day.

- Lower your mortgage rate. You may have the option to buy down your mortgage rate. That means paying a little more upfront to get a lower monthly payment. If you’re looking for ways to make the numbers work a little better, this is something that could be worth asking about.

You Don’t Have To Figure This Out Alone

If you have a tax refund coming, it’s a great time to take another look at your homebuying savings. Maybe you’re almost at your goal and you can buy sooner than you expected.

A trusted real estate agent and lender can help you map out what you need, what your options are, and how to make the most of what you already have, including your tax refund.

Bottom Line

If buying a home is on your radar this year, don’t overlook your tax refund. It could be the extra push that helps you go from almost there to actually ready.

Want to see how far your savings could take you right now? Talk with a local real estate agent and build a plan that fits your situation.

With economic headlines, global events, and near constant talk about affordability, you may be wondering if this is the right time to move. But here’s what you need to remember.

While recent events do have some impact on the housing market, they don’t take buying off the table. You just have to use a different strategy.

Mortgage Rates Have Been Up Slightly – Here’s Why

After trending down for most of 2025, mortgage rates have been higher again for over roughly a month now. And experts say it’s a result of what’s happening overseas and in the broader economy. As Mark Fleming, Chief Economist at First American, explains:

“Mortgage rates have recently moved higher, driven by geopolitical uncertainty and rising energy costs that are contributing to inflation concerns.”

But what does that really mean for you? Should you wait for everything to settle back down before you buy a home?

The short answer is no. You don’t have to wait.

Your Window To Buy Didn’t Close

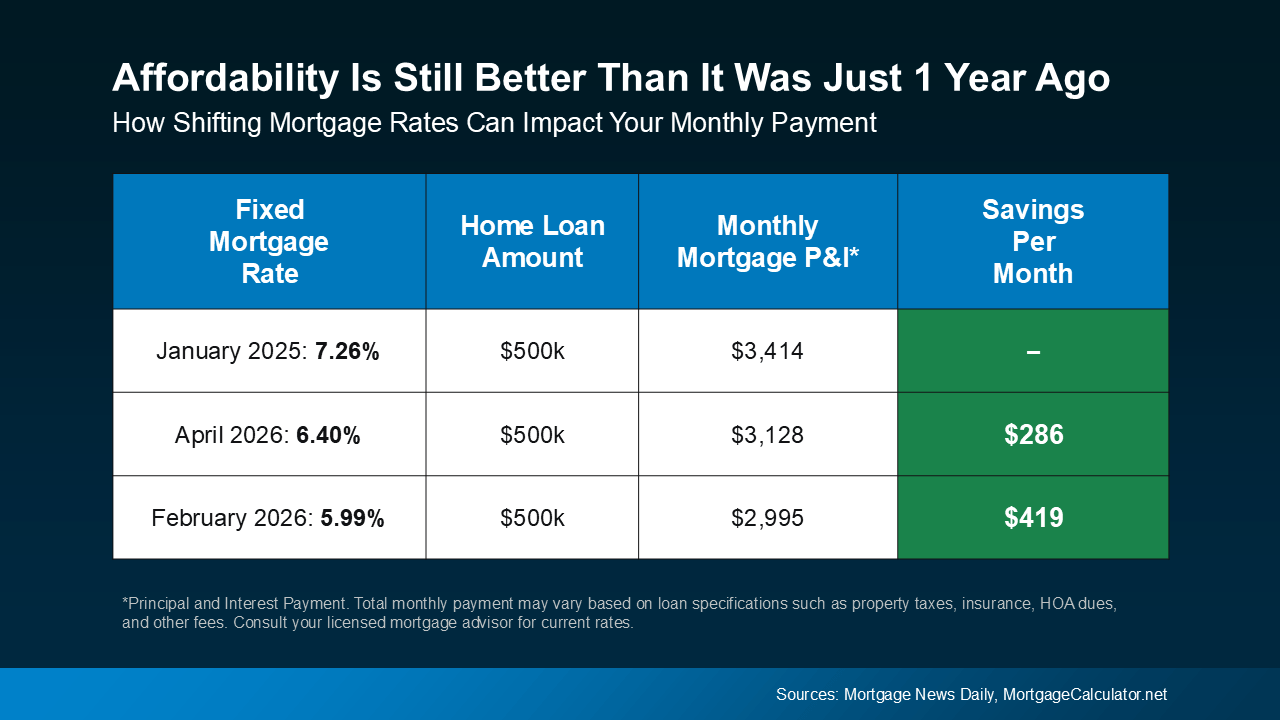

It’s true that a month or so ago, when rates were just shy of 6%, buying felt a bit more affordable. And now that rates are hovering around the mid-6s, monthly payment costs are higher.

But zoom out for a second.

Let’s say you’re taking out a loan for $500k. Even with rates in the mid 6s, you’re still saving roughly $300 on your monthly payment compared to buyers who made their purchase early last year.

That means this recent increase in rates hasn’t erased the progress we’ve seen. Buying is still more affordable than it was just one year ago (see below):

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

The goal moving forward shouldn’t be to perfectly time the market. Things change too quickly for that. Instead, the real goal is to make the best decision you can based on where things are today. And the best advice anyone can give is: brace for volatility.

When It Comes To Rates, Expect the Unexpected

Mortgage rates are going to continue to be move around in the weeks or months ahead as new information and economic reports come out.

Try to remember, you can’t control global events or where rates go next week (or even next month). But you can control how you prepare. If you do that, it becomes less about the headlines, and more about your situation.

If You Want or Need To Move, You Still Can

The simple truth is, if you want or need to move, you still can.

Some buyers are choosing to move forward right now because their needs haven’t changed. A growing family, a job relocation, a lifestyle shift – those things still matter.

And for buyers who do decide to move forward, there are ways to make it work.

For example, you could explore options like adjustable-rate mortgages (ARMs) to get a lower rate upfront. That may or may not be the right fit for you, but it highlights an important point: there are strategies that can help you move, even now.

What matters most is having a plan.

And working with the right agent and lender is a big part of that. With expert help, you’ll:

-

Understand your budget and what the math looks like at today’s rates.

-

Explore your financing options, including ARMs and assistance programs.

-

Have trusted guidance from experts who’ll keep you up to date throughout the process.

Bottom Line

Even though there’s some uncertainty, that doesn’t mean you’re out of options.

If you need to move, you still can. Connect with a trusted agent and lender so you can explore all your options and make your move happen.

The 10 Best Markets for First-Time Buyers This Spring

Rent or Buy? The Real Tradeoff Most People Don’t Talk About

Getting a Tax Refund? Here’s How It Can Help You Buy a Home

-

For Buyers3 weeks ago

For Buyers3 weeks agoDon’t Let Home Prices Headlines Fool You

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoYou Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

-

Equity4 weeks ago

Equity4 weeks agoThe Remodel You’ve Been Dreaming About May Be Closer Than You Think

-

For Buyers3 weeks ago

For Buyers3 weeks agoThis’ll Change What You Think About Investors in Today’s Housing Market

-

For Sellers4 weeks ago

For Sellers4 weeks agoThe Best Week To List Your House Is Just Around the Corner

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoBefore You Fall in Love with a House, Do This First.

-

Affordability2 weeks ago

Affordability2 weeks agoWhen Buying a Home Feels Out of Reach, Some Families Do This Instead

-

For Sellers2 weeks ago

For Sellers2 weeks agoYour House Hasn’t Sold Yet. Should You Rent It Out Instead?

You must be logged in to post a comment Login