Housing Market Updates

Why the Economy Won’t Tank the Housing Market

If you’re worried about a coming recession, you’re not alone. Over the past couple of years, there’s been a lot of recession talk. And many people worry, if we do have one, it would cause the unemployment rate to skyrocket. Some even fear that a spike in unemployment would lead to a rash of foreclosures similar to what happened 15 years ago.

However, the latest Economic Forecasting Survey from the Wall Street Journal (WSJ) reveals that, for the first time in over a year, less than half (48%) of economists believe a recession will actually occur within the next year:

“Economists are turning optimistic on the U.S. economy . . . economists lowered the probability of a recession within the next year, from 54% on average in July to a more optimistic 48%. That is the first time they have put the probability below 50% since the middle of last year.”

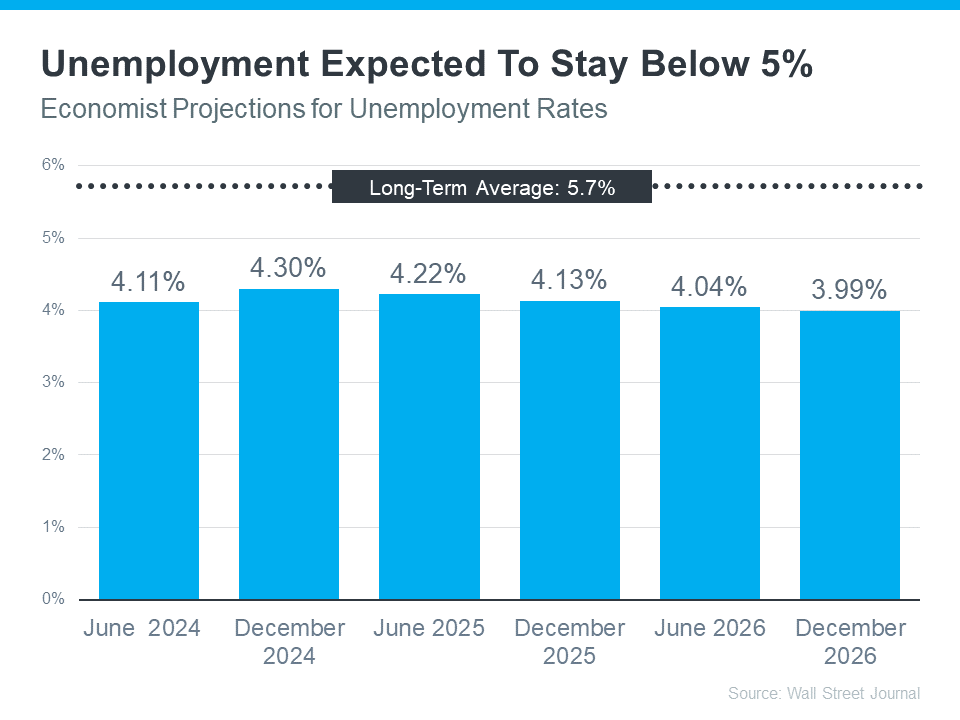

If over half of the experts no longer expect a recession within the next year, you might naturally think those same experts also don’t expect the unemployment rate to jump way up – and you’d be right. The graph below uses data from that same WSJ survey to show exactly what the economists project for the unemployment rate over the next three years (see graph below):

If those expert projections are correct, more people will lose their jobs in the upcoming year. And job losses of any kind are devastating for those people and their loved ones.

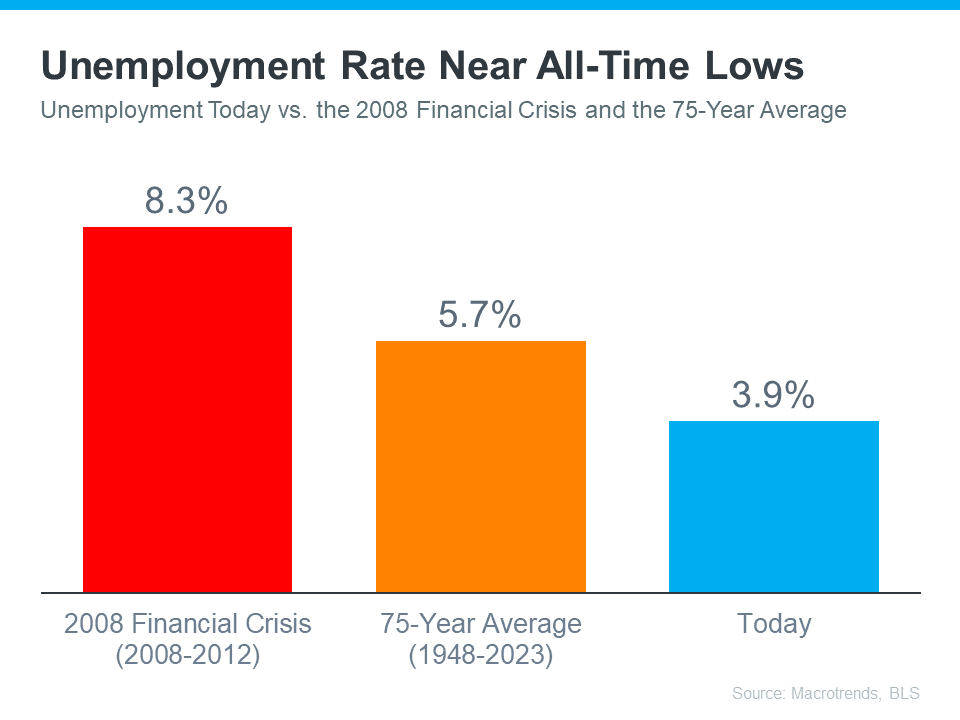

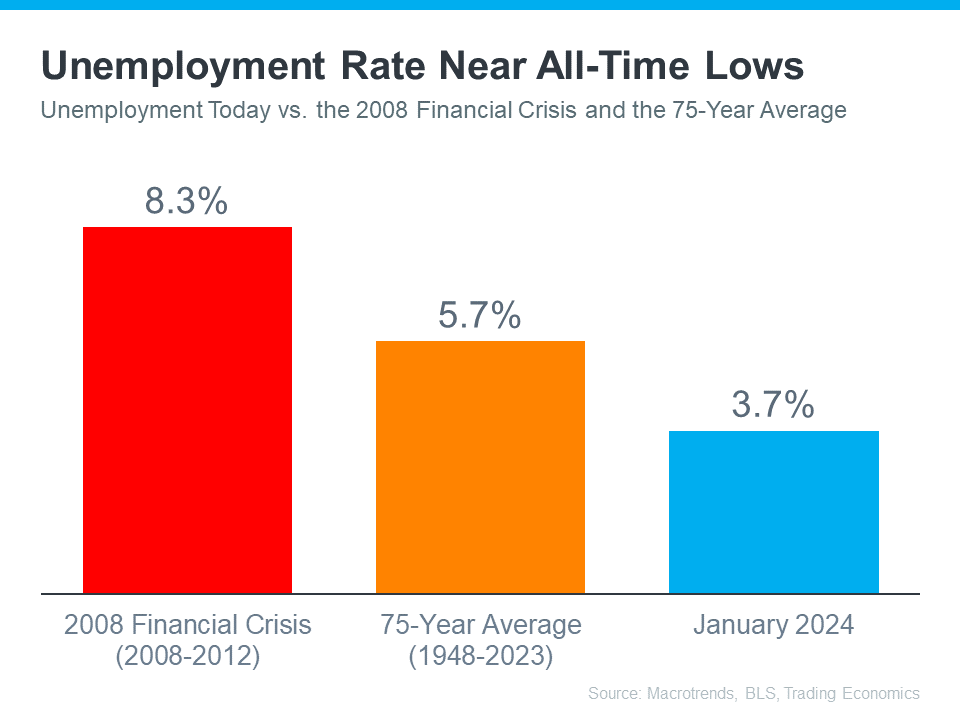

However, the question here is: will there be enough job losses to cause a wave of foreclosures that will crash the housing market? Based on historical context from Macrotrends and the Bureau of Labor Statistics (BLS), the answer is no. That’s because the unemployment rate is currently near all-time lows (see graph below):

As the orange bar in the graph shows, the average unemployment rate dating back to 1948 is 5.7%. The red bar shows, the last time the housing market crashed, in the immediate aftermath of the 2008 financial crisis, the average unemployment rate was up to 8.3%. Both of those bars are much higher than the unemployment rate today (shown in the blue bar).

Moving forward, projections show the unemployment rate is likely to stay beneath the 75-year average. And that means we won’t see a wave of foreclosures that would severely impact the housing market.

Bottom Line

Most economists no longer expect a recession to occur in the next 12 months. That’s why they also don’t expect a dramatic rise in the unemployment rate that would lead to a rash of foreclosures and another housing market crash. If you have questions about unemployment and its impact on the housing market, connect with a real estate professional.

Have you heard the term “Silver Tsunami” getting tossed around recently? If so, here’s what you really need to know. That phrase refers to the idea that a lot of baby boomers are going to move or downsize all at once. And the fear is that a sudden influx of homes for sale would have a big impact on housing. That’s because it would create a whole lot more competition for smaller homes and would throw off the balance of supply and demand, which ultimately would impact home prices.

But here’s the thing. There are a couple of faults in that logic. Let’s break them down and put your mind at ease.

Not All Baby Boomers Plan To Move

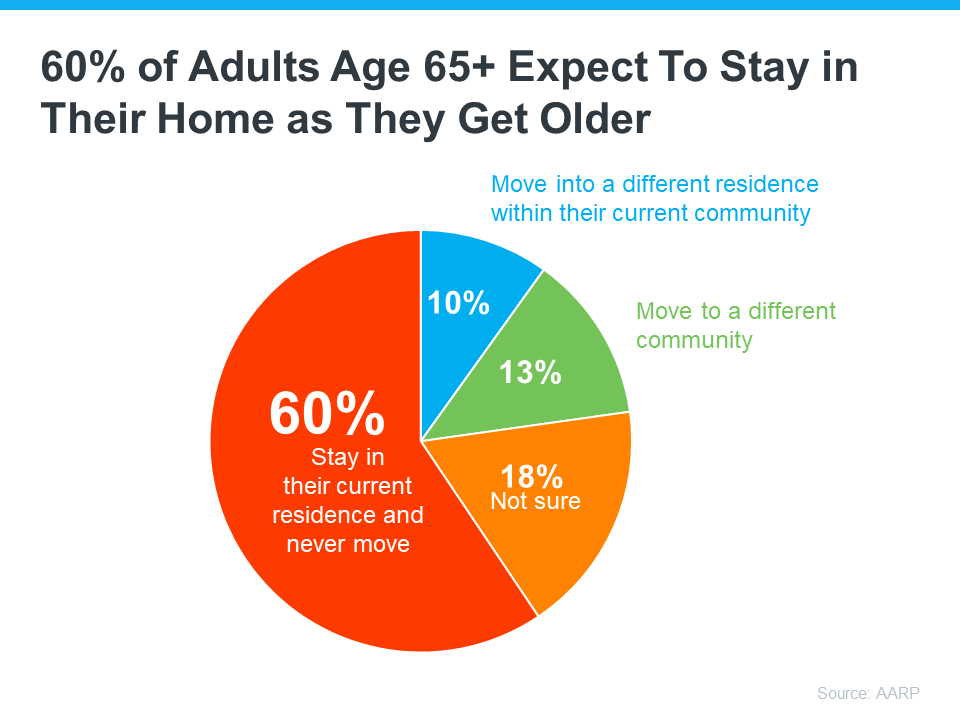

For starters, plenty of baby boomers don’t plan on moving at all. A study from the AARP says more than half of adults aged 65 and older want to stay in their homes and not move as they age (see graph below):

While it’s true circumstances may change and some people who don’t plan to move (the red in the chart above) may realize they need to down the road, the vast majority are counting on aging in place.

As for those who stay put, they’ll likely modify their homes as their needs change over time. And when updating their existing home won’t work, some will buy a second home and keep their original one as an investment to fuel generational wealth for their loved ones. As an article from Inman explains:

“Many boomers have no desire to retire fully and take up less space . . . Many will modify their current home, and the wealthiest will opt to have multiple homes.”

Even Those Who Do Move Won’t Do It All at Once

While not all baby boomers are looking to sell their homes and move – the ones who do won’t all do it at the same time. Instead, it’ll happen slowly over many years. As Freddie Mac says:

“We forecast the ‘tsunami’ will be more like a tide, bringing a gradual exit of 9.2 million Boomers by 2035 . . .”

As Mark Fleming, Chief Economist at First American, says:

“Demographics are never a tsunami. The baby boomer generation is almost two decades of births. That means they’re going to take about two decades to work their way through.”

Bottom Line

If you’re stressed about a Silver Tsunami shaking the housing market overnight, don’t be. Baby boomers will move slowly over a much longer period of time.

Some Highlights

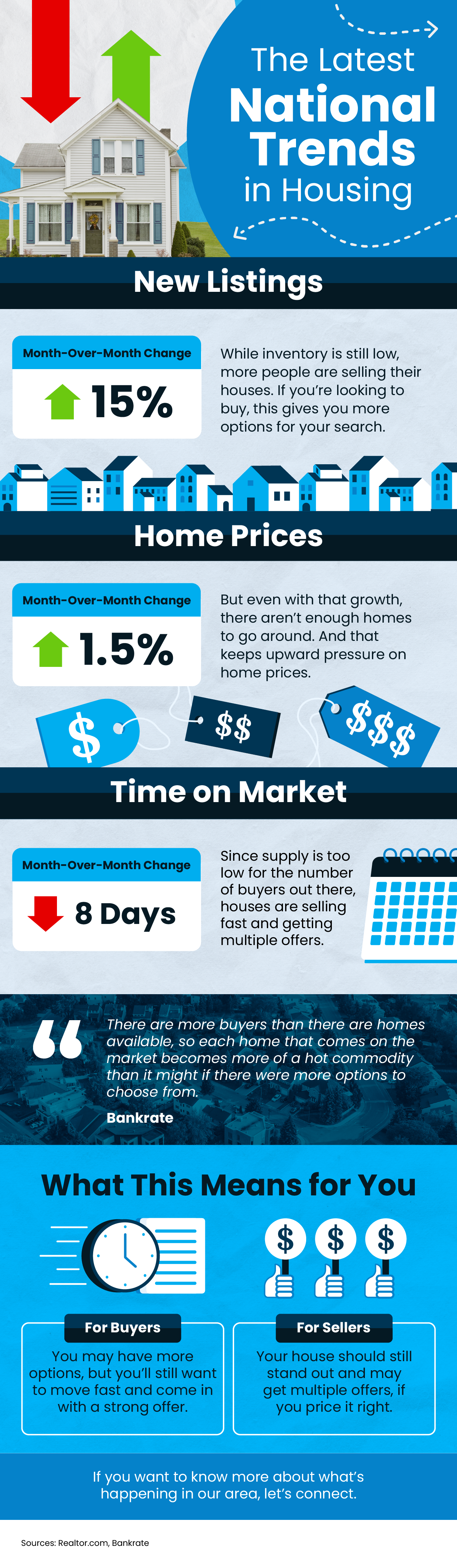

- With the number of new listings going up and average days on market going down, buyers may have more options, but will still want to move fast.

- For sellers, inventory is still low and houses are selling fast, meaning your house should stand out and may get multiple offers if you price it right.

- If you want to know more about what’s happening in your area, connect with a local real estate agent.

There’s been a lot of recession talk over the past couple of years. And that may leave you worried we’re headed for a repeat of what we saw back in 2008. Here’s a look at the latest expert projections to show you why that isn’t going to happen.

According to Jacob Channel, Senior Economist at LendingTree, the economy’s pretty strong:

“At least right now, the fundamentals of the economy, despite some hiccups, are doing pretty good. While things are far from perfect, the economy is probably doing better than people want to give it credit for.”

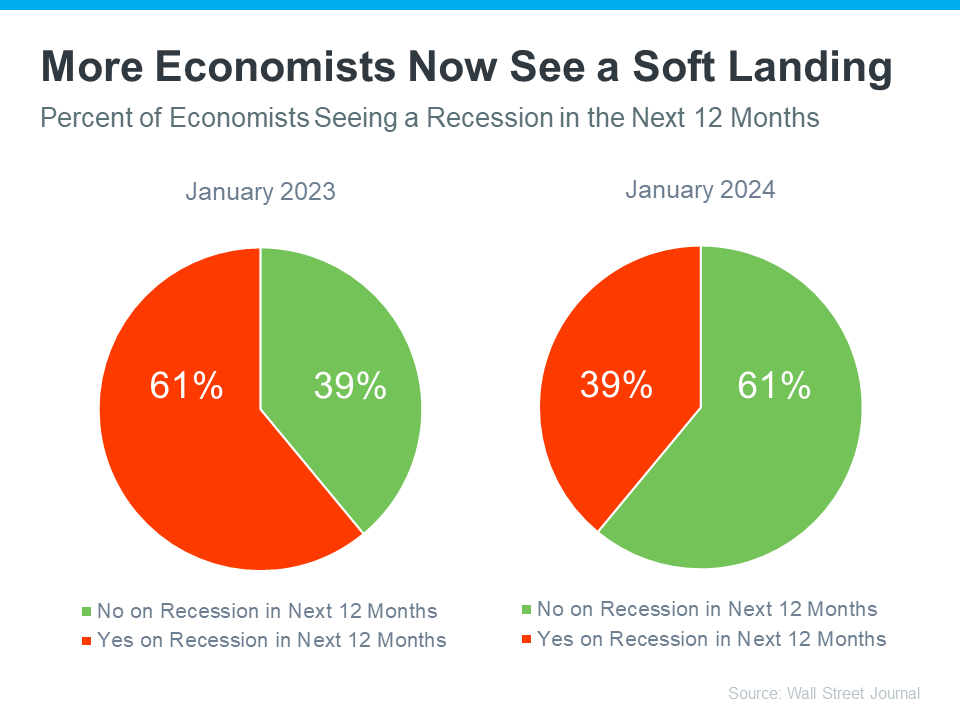

That might be why a recent survey from the Wall Street Journal shows only 39% of economists think there’ll be a recession in the next year. That’s way down from 61% projecting a recession just one year ago (see graph below):

Most experts believe there won’t be a recession in the next 12 months. One reason why is the current unemployment rate. Let’s compare where we are now with historical data from Macrotrends, the Bureau of Labor Statistics (BLS), and Trading Economics. When we do, it’s clear the unemployment rate today is still very low (see graph below):

The orange bar shows the average unemployment rate since 1948 is about 5.7%. The red bar shows that right after the financial crisis in 2008, when the housing market crashed, the unemployment rate was up to 8.3%. Both of those numbers are much larger than the unemployment rate this January (shown in blue).

But will the unemployment rate go up? To answer that, look at the graph below. It uses data from that same Wall Street Journal survey to show what the experts are projecting for unemployment over the next three years compared to the long-term average (see graph below):

As you can see, economists don’t expect the unemployment rate to even come close to the long-term average over the next three years – much less the 8.3% we saw when the market last crashed.

Still, if these projections are correct, there will be people who lose their jobs next year. Anytime someone’s out of work, that’s a tough situation, not just for the individual, but also for their friends and loved ones. But the big question is: will enough people lose their jobs to create a flood of foreclosures that could crash the housing market?

Looking ahead, projections show the unemployment rate will likely stay below the 75-year average. That means you shouldn’t expect a wave of foreclosures that would impact the housing market in a big way.

Bottom Line

Most experts now think we won’t have a recession in the next year. They also don’t expect a big jump in the unemployment rate. That means you don’t need to fear a flood of foreclosures that would cause the housing market to crash.

The Case for Putting 20% Down on Your Next Home

Thinking About Waiting for Lower Mortgage Rates? Read This First.

Big Investors Are Backing Off and That’s Your Opening

-

For Sellers4 weeks ago

For Sellers4 weeks agoThink Nobody’s Buying Homes Right Now? Think Again.

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

-

First-Time Buyers4 weeks ago

First-Time Buyers4 weeks ago14 Years Running: Why Real Estate Is Still America’s Favorite Investment

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoMore Homes, Better Prices: A Buyer’s Summer

-

Equity3 weeks ago

Equity3 weeks agoThe House That Started It All Could Kickstart What’s Next

-

Affordability3 weeks ago

Affordability3 weeks agoPriced Out? A Condo or Townhome Could Be Your Way In.

-

For Sellers2 weeks ago

For Sellers2 weeks agoSelling a Luxury House? Here’s Why Now Is a Good Time

-

Affordability2 weeks ago

Affordability2 weeks agoBuying a Home? Here’s What You Should Know About Home Insurance Costs.

You must be logged in to post a comment Login