First Time Home Buyers

Thinking About Buying a Home? Ask Yourself These Questions

If you’re thinking of buying a home this year, you’re probably paying closer attention than normal to the housing market. And you’re getting your information from a variety of channels: the news, social media, your real estate agent, conversations with friends and loved ones, the list goes on and on. Most likely, home prices and mortgage rates are coming up a lot.

Here are the top two questions you need to ask yourself as you make your decision, including the data that helps cut through the noise.

1. Where Do I Think Home Prices Are Heading?

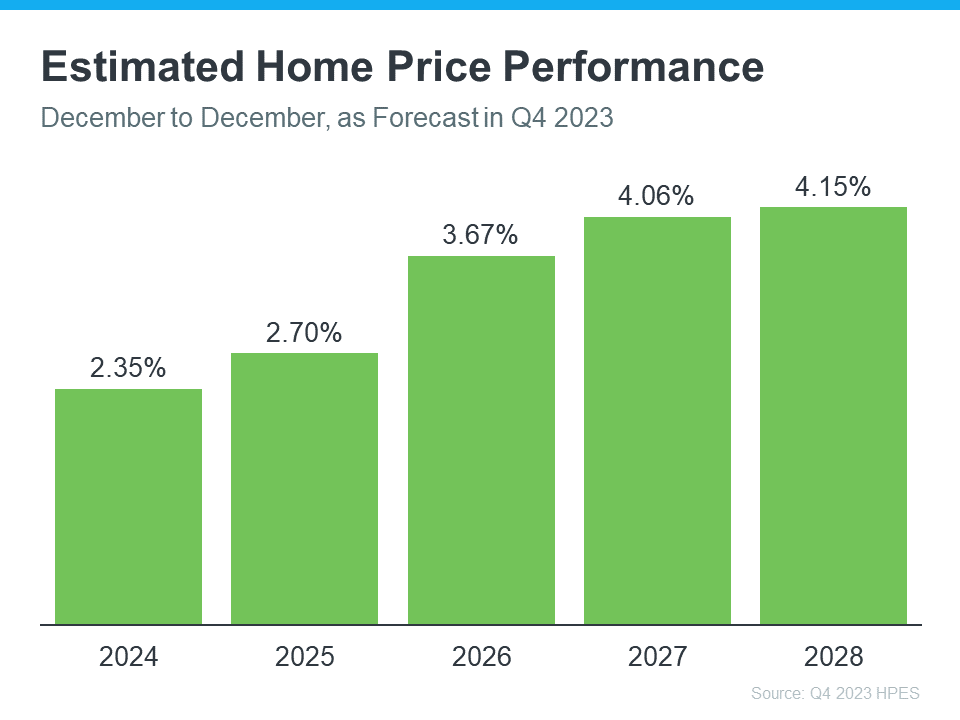

One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts, and investment and market strategists.

According to the most recent release, the experts are projecting home prices will continue to rise at least through 2028 (see the graph below):

So, why does this matter to you? While the percent of appreciation may not be as high as it was in recent years, what’s important to focus on is that this survey says we’ll see prices rise, not fall, for at least the next 5 years.

And home prices rising, even at a more moderate pace, is good news not just for the market, but for you too. It means, by buying now, your home will likely grow in value, and you should gain home equity in the years ahead. But, if you wait, based on these forecasts, the home will only cost you more later on.

2. Where Do I Think Mortgage Rates Are Heading?

Over the past year, mortgage rates spiked up in response to economic uncertainty, inflation, and more. But there’s an encouraging sign for the market and mortgage rates. Inflation is moderating, and here’s why this is such a big deal if you’re looking to buy a home.

When inflation cools, mortgage rates generally fall in response. That’s exactly what we’ve seen in recent weeks. And, now that the Federal Reserve has signaled they’re pausing their Federal Funds Rate increases and may even cut rates in 2024, experts are even more confident we’ll see mortgage rates come down.

Danielle Hale, Chief Economist at Realtor.com, explains:

“. . . mortgage rates will continue to ease in 2024 as inflation improves and Fed rate cuts get closer. . . . a key factor in starting to provide affordability relief to homebuyers.”

As an article from the National Association of Realtors (NAR) says:

“Mortgage rates likely have peaked and are now falling from their recent high of nearly 8%. . . . This likely will improve housing affordability and entice more home buyers to return to the market . . .”

No one can say with absolute certainty where mortgage rates will go from here. But the recent decline and the latest decision from the Federal Reserve to stop their rate increases, signals there’s hope on the horizon. While we may see some volatility here and there, affordability should improve as rates continue to ease.

Bottom Line

If you’re thinking about buying a home, you need to know what’s expected with home prices and mortgage rates. While no one can say for certain where they’ll go, making sure you have the latest information can help you make an informed decision. Connect with a trusted local real estate agent so you can stay up to date on what’s happening and why this is such good news for you.

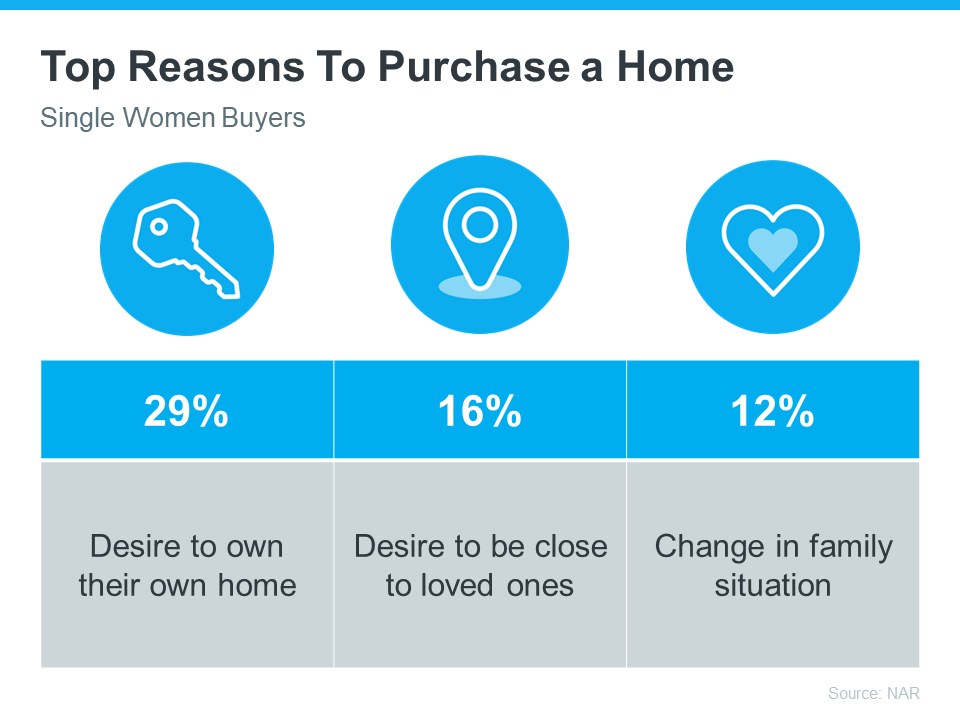

In today’s housing market, more and more single women are becoming homeowners. According to data from the National Association of Realtors (NAR), 19% of all homebuyers are single women, while only 10% are single men.

If you’re a single woman trying to buy your first home, this should be encouraging. It means other people are making their dreams a reality – so you can too.

Why Homeownership Matters to So Many Women

For many single women, buying a home isn’t just about having a place to live—it’s also a smart way to invest for the future. Homes usually increase in value over time, so they’re a great way to build equity and overall net worth. Ksenia Potapov, Economist at First American, says:

“. . . single women are increasingly pursuing homeownership and reaping its wealth creation benefits.”

The financial security and independence homeownership provides can be life-changing. And when you factor in the personal motivations behind buying a home, that impact becomes even clearer.

The same report from NAR shares the top reasons single women are buying a home right now, and the reality is, they’re not all financial (see chart below):

If any of these reasons resonate with you, maybe it’s time for you to buy too.

Work with a Trusted Real Estate Agent

If you’re a single woman looking to buy a home, it is possible, even in today’s housing market. You’ll just want to be sure you have a great real estate agent by your side.

Talk about what your goals are and why homeownership is so important to you. That way your agent can keep what’s critical for you up front as they guide you through the buying process. They’ll help you find the right home for your needs and advocate for you during negotiations. Together, you can make your dream of homeownership a reality.

Bottom Line

Homeownership is life-changing no matter who you are. Connect with a local real estate agent to talk about your goals in the housing market.

Some Highlights

- Trying to buy your first home? If you’re worried about affordability today or the limited number of homes for sale, these tips can help.

- Look into homebuyer programs, expand your search area, and consider a multi-generational home.

- Connect with a local real estate agent so you have an expert on your side to help you make your dream a reality.

The 1 Factor That Explains Everything Happening with Home Prices Right Now

Your House Didn’t Sell. Here’s How To Turn It Around.

More Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Affordability4 weeks ago

Affordability4 weeks agoWhat Rising Inflation Means for Your Move

-

Economy4 weeks ago

Economy4 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability4 weeks ago

Affordability4 weeks agoLess House, More Home: Why Smaller Homes Are Paying Off for Today’s Buyers

-

Affordability3 weeks ago

Affordability3 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoTwo Big Reasons To Move This Summer

-

Affordability3 weeks ago

Affordability3 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers2 weeks ago

For Sellers2 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers2 weeks ago

For Buyers2 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

You must be logged in to post a comment Login