Affordability

Why Experts Say Mortgage Rates Should Ease Over the Next Year

You want mortgage rates to fall – and they’ve started to. But is it going to last? And how low will they go?

Experts say there’s room for rates to come down even more over the next year. And one of the leading indicators to watch is the 10-year treasury yield. Here’s why.

The Link Between Mortgage Rates and the 10-Year Treasury Yield

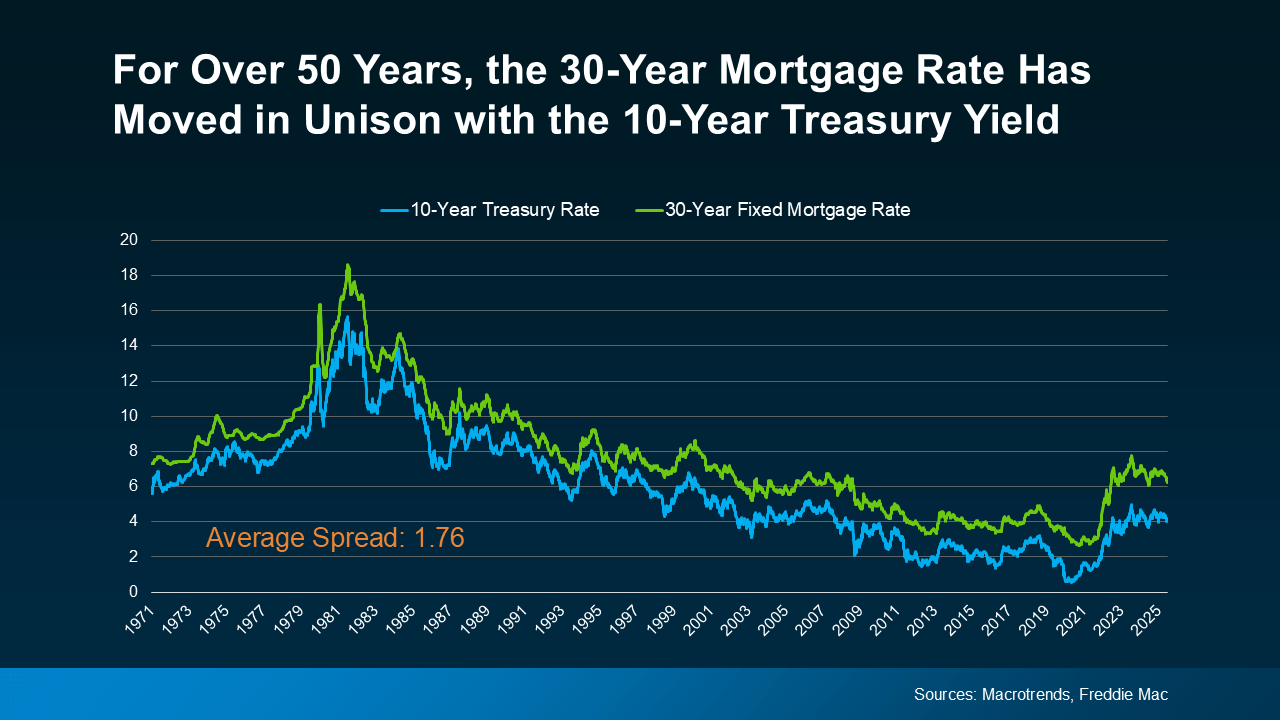

For over 50 years, the 30-year fixed mortgage rate has closely followed the movement of the 10-year treasury yield, which is a widely watched benchmark for long-term interest rates (see graph below):

When the treasury yield climbs, mortgage rates tend to follow. And when the yield falls, mortgage rates typically come down.

When the treasury yield climbs, mortgage rates tend to follow. And when the yield falls, mortgage rates typically come down.

It’s been a predictable pattern for over 50 years. So predictable, that there’s a number experts consider normal for the gap between the two. It’s known as the spread, and it usually averages about 1.76 percentage points, or what you sometimes hear as 176 basis points.

The Spread Is Shrinking

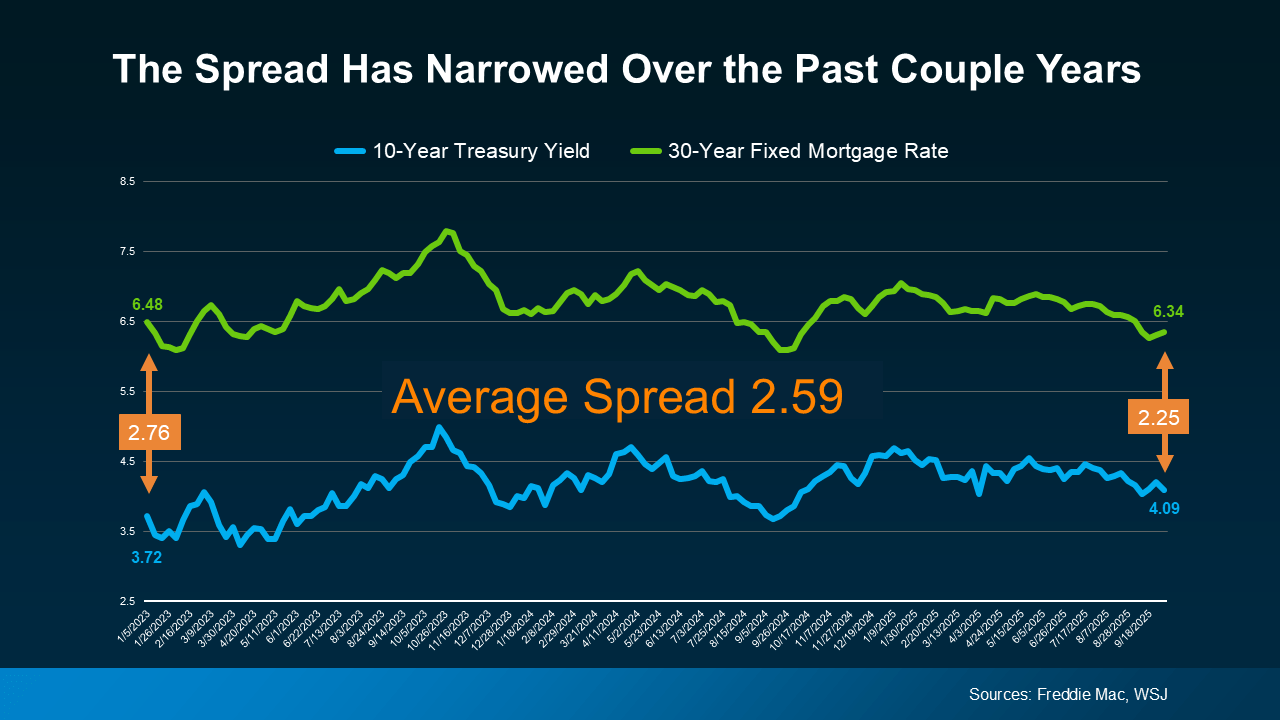

Over the past couple of years, though, that spread has been much wider than normal. Why? Think of the spread as a measure of fear in the market. When there’s lingering uncertainty in the economy, the gap widens beyond its usual norm. That’s one of the reasons why mortgage rates have been unusually high over the past few years.

But here’s a sign for optimism. Even though there’s still some lingering uncertainty related to the economy, that spread is starting to shrink as the path forward is becoming clearer (see graph below):

And that opens the door for mortgage rates to come down even more. As a recent article from Redfin explains:

And that opens the door for mortgage rates to come down even more. As a recent article from Redfin explains:

“A lower mortgage spread equals lower mortgage rates. If the spread continues to decline, mortgage rates could fall more than they already have.”

The 10-Year Treasury Yield Is Expected To Decline

It’s not just the spread, though. The 10-year treasury yield itself is also forecast to come down in the months ahead. So, when you combine a lower yield with a narrowing spread, you have two key forces potentially pushing mortgage rates down going into next year.

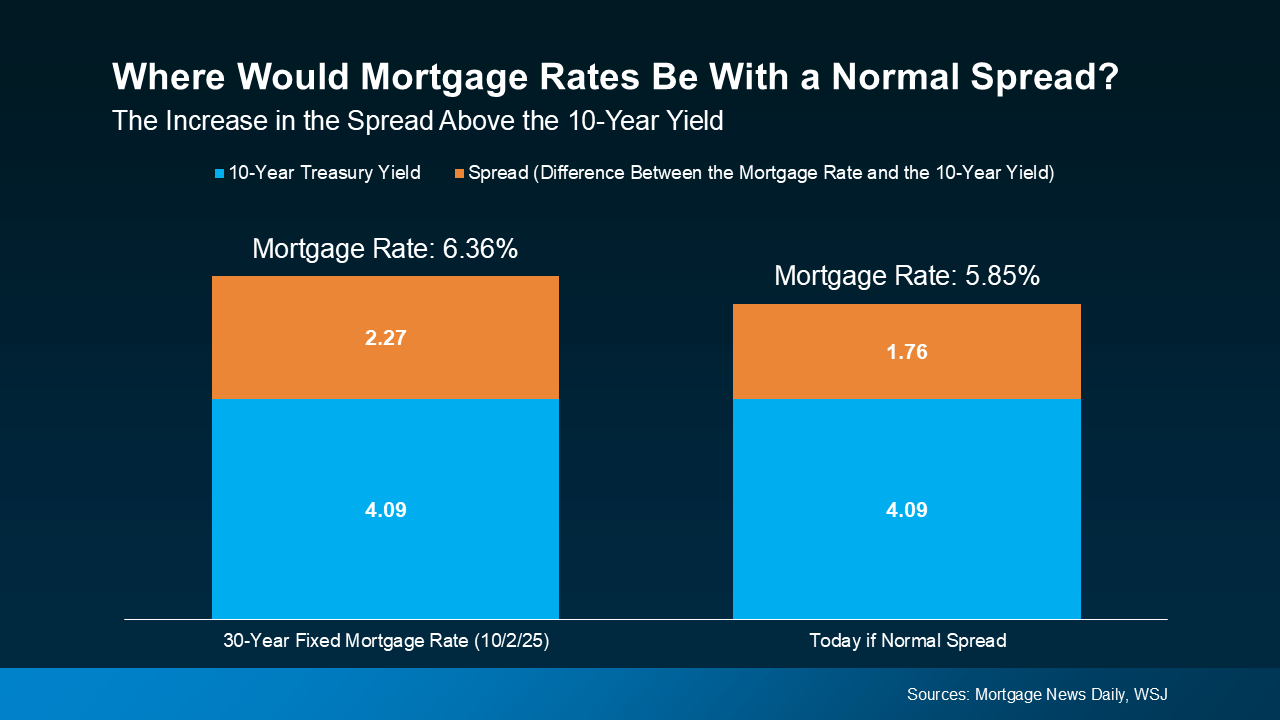

This long-term relationship is a big reason why you see experts currently projecting mortgage rates will ease, with a fringe possibility they’ll hit the upper 5s toward the end of next year.

Here’s how it works. Take the 10-year treasury yield, which is sitting at about 4.09% at the time this article is being written, and then add the average spread of 1.76%. From there, you’d expect mortgage rates to be around 5.85% (see graph below):

But remember, all of that can change as the economy shifts. And know for certain that there will be ups and downs along the way.

But remember, all of that can change as the economy shifts. And know for certain that there will be ups and downs along the way.

How these dynamics play out will depend on where the economy, the job market, inflation, and more go from here. But the 2026 outlook is currently expected to be a gradual mortgage rate decline. And as of now, things are starting to move in the right direction.

Bottom Line

Keeping up with all of these shifts can feel overwhelming. That’s why having an experienced agent or lender on your side matters. They’ll do the heavy lifting for you.

If you want real-time updates on mortgage rates, reach out to a trusted agent or lender who can keep you in the loop and help you plan your next move.

Open up a home search and you’ll see them. Listings that have been on the market for two months. Three. Some longer.

Most buyers scroll right past them, assuming something’s wrong with the house. But that instinct could be costing you, since the longer a home sits, the more motivated the seller usually gets.

Where Some Buyers Are Finding Better Deals

If affordability has been your #1 hurdle to buying, here’s a surprisingly simple strategy that could help you finally get your foot in the door. Start with the homes that have been sitting the longest. That’s often where the best deals are.

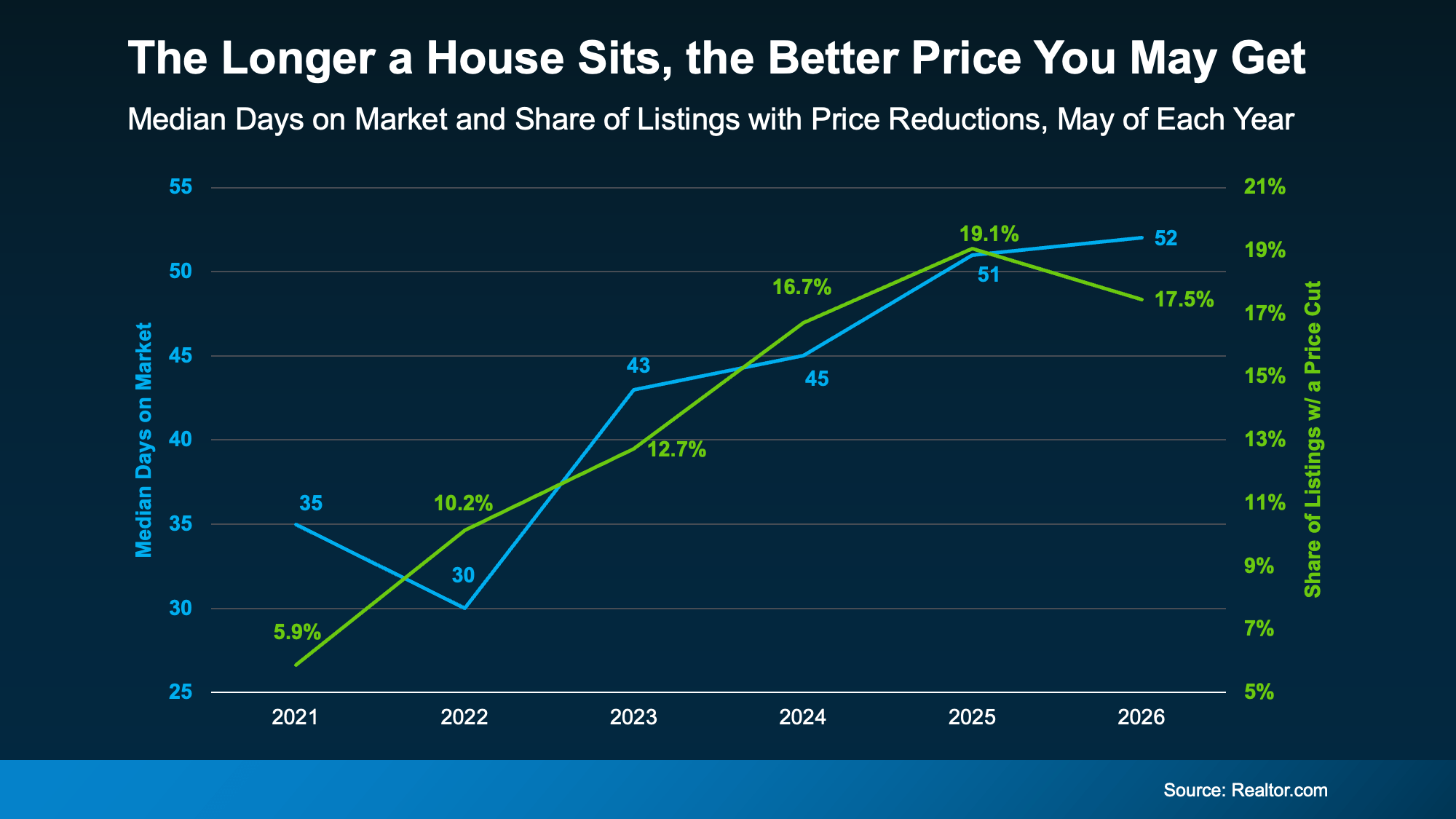

Here’s why. Data from Realtor.com shows there’s a connection between longer time on the market and lower sales prices. Basically, the longer a house sits, the more likely it is that the seller will reduce the price (see graph below):

The blue line tracks how long homes stay on the market, while the green line tracks the share of homes getting a price reduction. As one climbs, so does the other.

And if you focus on these homes that are just sitting and waiting, the opportunity for you is bigger than you may think right now.

Redfin data shows there’s $347 billion worth of stale listings on the market right now – more than ever before for this time of year. So, ask your agent to filter listings for you from oldest to newest. The home that fits your budget might already be there. Just further down the list than you thought.

Lingering Doesn’t Always Mean Something’s Wrong

Let’s say you do that and something catches your eye. Still, you might be questioning why the home has been sitting in the first place. Just remember, sometimes it has nothing to do with the home itself.

According to Redfin, common causes are:

-

The asking price was set too high to start

-

The home didn’t show well online

-

There are a lot of homes for sale in the area, so it just got buried

So, nothing that’s necessarily a dealbreaker, or even anything that’s wrong with the home itself. If there’s a real issue, a thorough inspection will surface it. And that’s information you can use to negotiate. Not a reason to assume it’s a house worth skipping over.

How To Turn a Lingering Listing into a Win

So how do you capitalize on a lingering listing? According to USA Today, you have two main levers to pull.

The first is price. Work with your agent to study what comparable homes recently sold for, then build an offer around that. Coming in below asking price is fair game when a home has been sitting.

The second is concessions. If a seller won’t budge much on price, they may still help in other ways, like covering some closing costs, repair credits, or even a mortgage rate buydown that lowers your monthly payment.

A local agent has the context to tell which homes are the real opportunities and which are skippable.

Bottom Line

A house sitting on the market isn’t always a glaring red flag. In today’s market, it may be your best opportunity yet.

For help deciding which lingering listings are actually worth a second look, connect with a local real estate agent.

If affordability has been the biggest thing standing between you and a home, there’s a little good news.

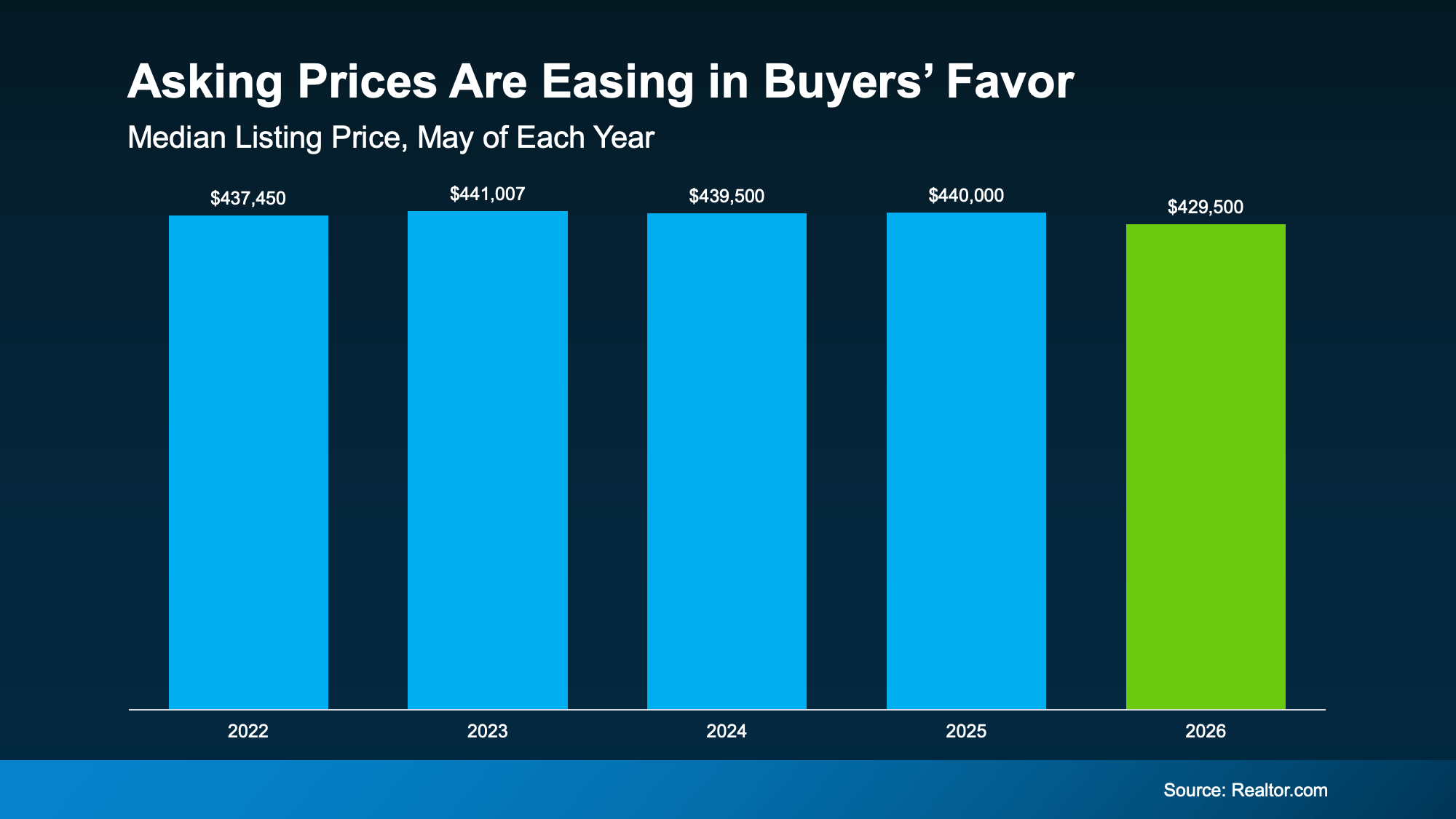

Asking prices have started to come down.

The typical seller listed their house for a median of $429,500 in May. That’s 2.4% lower than a year ago, according to Realtor.com. On its own, that won’t transform what you can afford, but in today’s market every little bit helps and it signals a broader shift taking place.

Buyers Are Finally Catching a Break

Check out this data from Realtor.com and you can see this is the first May in years where buyers have caught any sort of break price-wise.

Each May from 2022-2025, things held pretty steady. But this year? You can see that more noticeable shift in your favor (see graph below):

While the dip from $440,000 to $429,500 isn’t a big one, it gives you more breathing room. And that’s not a small thing when affordability has been this tough.

Now, lower asking prices don’t mean every home is suddenly within your range. But they do show buyers are gaining a little ground.

And in today’s market, a little ground can go a long way.

What That Means for the Housing Market

And just in case this crossed your mind, this is good news for your move, not bad news for the market as a whole.

The subtle dip from last May to this one shows prices are easing, but they’re not dropping off a cliff. What this is actually a sign of is that the market’s rebalancing now that the number of homes for sale has grown.

Buyers have a bit more power again, and sellers know they can’t name just any price and expect their house to sell. They either meet the market where it is, or face a price cut later. And in general, sellers would rather avoid a price cut. As the New York Post explains:

“Rather than swinging for the fences with pandemic-era price tags, sellers are increasingly coming to terms with a new reality. The share of listings featuring price cuts actually fell to 17.5% in May, suggesting homeowners are doing their homework before putting up a “For Sale” sign instead of chasing unrealistic numbers and cutting later.“

This signals a broader change in the market.

Seller expectations have been skewed a little high since the pandemic buying frenzy – you’ve probably felt that firsthand. But now, things are starting to normalize. It could mean less back-and-forth to land on a fair number. And homes should be priced a bit more realistically from the start.

Bottom Line

If affordability has been your top concern, the recent dip in prices is an opening. Connect with a local real estate agent to see what that looks like in your area.

Whether you’re dreaming about buying your first home or wondering if it’s time to move on from the one you’re in, affordability is probably weighing on your mind. Home prices are still high in many markets, and even though things have improved a bit over the past year, making the numbers work can still feel like a stretch.

But the people finding ways to move right now usually have one thing in common. They didn’t wait for affordability to come to them. They went looking for it.

According to PODS, 61% of people across all generations say affordability is the biggest factor when deciding where to move. And it’s led a growing number of people to do one thing – broaden their search to include more affordable areas they hadn’t seriously considered before. As PODS, put it:

“. . . moving is increasingly driven by affordability, connection, and quality of life. As economic pressures persist, Americans are taking a more intentional, values-driven approach to where they choose to live.”

It’s Not Just the Home Price – It’s the Whole Cost of Living

Here’s where it gets really interesting. When people talk about moving for affordability, they’re not just talking about finding a cheaper house. They’re thinking about the full picture. What does it actually cost to live somewhere?

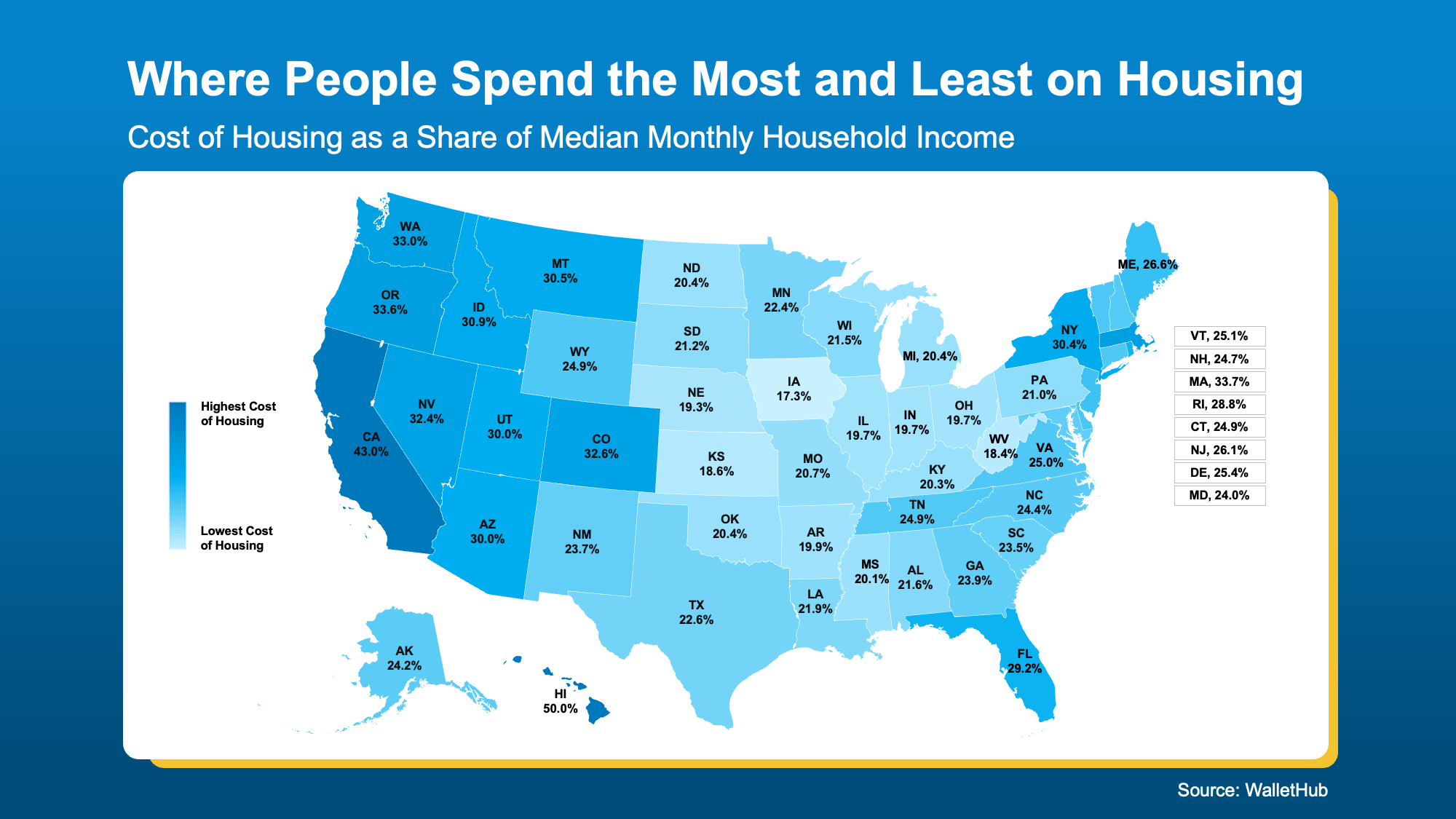

WalletHub looked at exactly this, measuring housing costs as a share of median monthly household income across every state (see map below).

Take a look at where you live on that map. The lighter the blue, the more affordable it generally is to live there. The darker the blue? Just the opposite.

If your state is showing up on the darker blue end of the scale, the cost of living may be putting a real pinch on your wallet, and it may be worth exploring what a lighter-blue area could mean for your finances.

Because if you’re less financially stretched, imagine how that could change things. Less stress. Less worry. More freedom and peace of mind.

You Don’t Have To Move to Another State To Find a Better Deal

But finding more affordable homeownership doesn’t have to mean a cross-country move. It doesn’t even have to mean leaving your state, your family, or your favorite coffee shop behind.

Every market has more affordable pockets that most buyers never think to explore – neighborhoods, towns, and communities where home prices are lower, property taxes are more manageable, and the overall cost of living just works better.

A great local real estate agent knows exactly where those places are.

And if you work remotely, or have any flexibility in where you’re based, your options open up even further. Remote work has already changed the way millions of people think about where to live, and that trend isn’t going away.

When location stops being tied to a daily commute, a more affordable area that’s a bit farther out suddenly becomes a very real option.

Bottom Line

Affordability is a real challenge, but it’s not an unsolvable one. The key is being open to places you might not have considered before. A local real estate agent can help you find them.

Ready to find out which areas have the best affordability right now? Reach out today.

The 1 Factor That Explains Everything Happening with Home Prices Right Now

Your House Didn’t Sell. Here’s How To Turn It Around.

More Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Affordability4 weeks ago

Affordability4 weeks agoWhat Rising Inflation Means for Your Move

-

Economy4 weeks ago

Economy4 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability4 weeks ago

Affordability4 weeks agoLess House, More Home: Why Smaller Homes Are Paying Off for Today’s Buyers

-

Affordability3 weeks ago

Affordability3 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoTwo Big Reasons To Move This Summer

-

Affordability3 weeks ago

Affordability3 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers2 weeks ago

For Sellers2 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers2 weeks ago

For Buyers2 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

You must be logged in to post a comment Login