For Buyers

Builders & Realtors Agree: Real Estate Is Back

Buying or selling a home is a big financial decision. And right now, it feels even bigger. Inflation is high, costs are high, and you want to be sure the timing is right before you make your move.

But if you do decide to go for it, whether you’re buying or selling, here’s something reassuring to hold onto. Not only does your move change your own life, but it also gives your whole community a boost.

Real estate is a huge part of the economy. In 2025, it added up to about $5.6 trillion, according to the National Association of Realtors (NAR). A good share of that comes from everyday people buying and selling homes, just like you.

Your Move Puts Real Money Into the Local Economy

Every sale sends money flowing through your area. NAR data shows that buying an existing home (one that’s already been lived in) adds about $64,000 to the local economy. Buy a newly built home, and that number climbs to more than $134,000 (see graph below):

Over half of that comes from the work of building the home itself. The rest flows to real estate services, like agent and lender fees, plus what you spend settling in afterward, on things like furniture and remodeling.

And the money doesn’t stop there. As local businesses earn it, they spend it again in your area, so a single sale ripples further than the sale price alone.

One Sale Keeps a Lot of People Working

Behind every sale is a whole network of people doing their jobs. Contractors, lenders, inspectors, movers, and more. When you buy or sell, you help keep them busy. Lawrence Yun, Chief Economist at NAR, puts it this way:

“Increased home sales mean more economic activity — lawn care, furniture purchases, moving services, mortgage originations and other related business activities all get a boost.“

So, your move supports your neighbors’ livelihoods, too. The deal that gets you into your next home also helps a local crew make payroll. In a year when every paycheck counts, that’s no small thing.

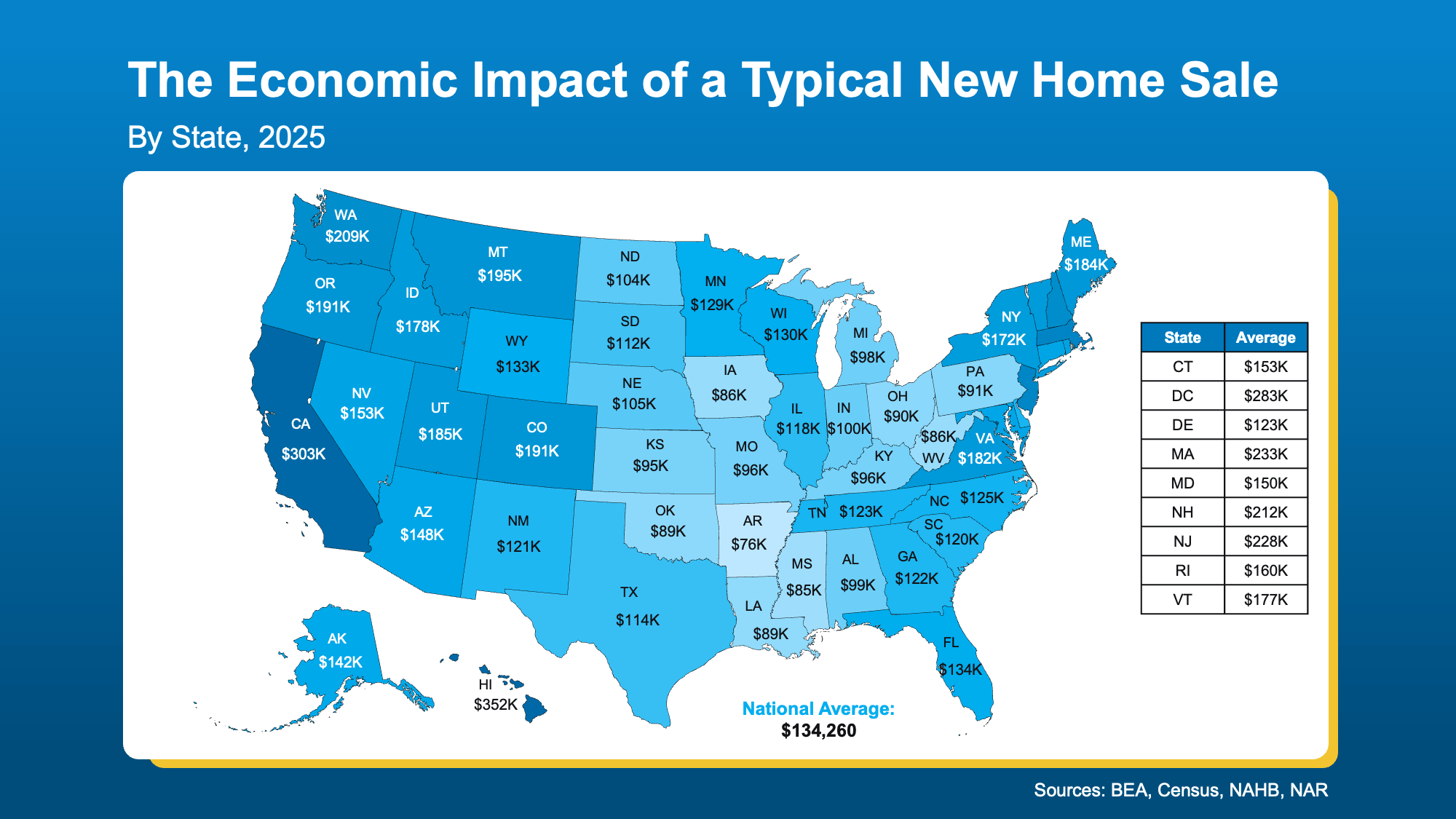

Your Local Impact May Be Even Bigger

What your move financially adds to your community depends a lot on where you live. To help you see how it can vary, here’s a look at the impact of a typical newly built home sale by state.

The national average for a newly built home is about $134,000, but some states see far more (see map below):

In California, a single sale adds more than $300,000 to the local economy. In Hawaii, it’s over $350,000. Even in the most affordable states, the number lands in the tens of thousands.

Want to know what a move would mean where you live? A local agent can show you the figure close to home.

Bottom Line

Moving is both a personal milestone and an investment in your community. So, if the time is right for you, connect with a local agent. You’ll make a difference for more people than you know.

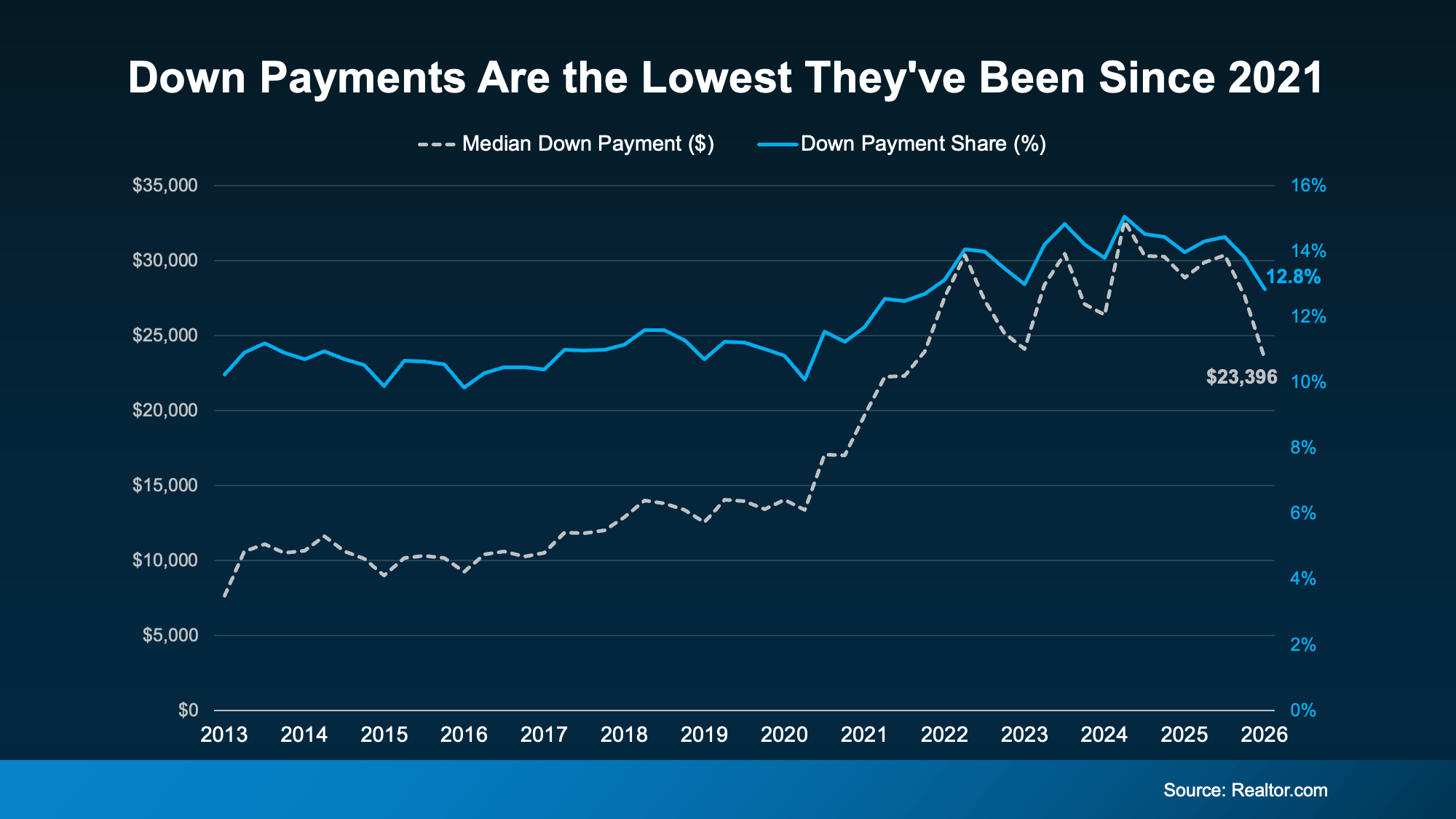

Saving for a down payment can feel like the hardest part of buying a home. And with affordability as tight as it’s been lately, it’s fair to wonder how anyone manages it right now. Here’s something you may not have seen coming.

Some people are getting their foot in the door with a smaller down payment.

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that’s around $5,000 below what was typical the year before (a 19% drop year over year). That’s the lowest down payments have been since 2021 (see graph below):

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

There are a few things driving the trend:

-

Less competition between buyers. Part of it comes down to a more balanced market. With buyers facing less competition than they did a few years ago, there’s less pressure to put a big sum down just to stand out.

-

More moderate home prices. Your down payment is a percentage of the purchase price. So, as price growth cools, the amount you need to put down may change too. In a lot of markets, prices have slowed or leveled off, and some areas are even seeing slight dips. That can translate into smaller down payments.

-

Buyers opting for loans with lower down payments. More buyers are also turning to government-backed loans, like FHA and VA, which often need little or no money down. FHA loans have made up more than 24% of purchase mortgages for five straight quarters, and VA loans recently hit their highest share in over a decade, according to Mortgage Professional America.

But even a smaller down payment is still a significant chunk of cash, and saving it can be hard. So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

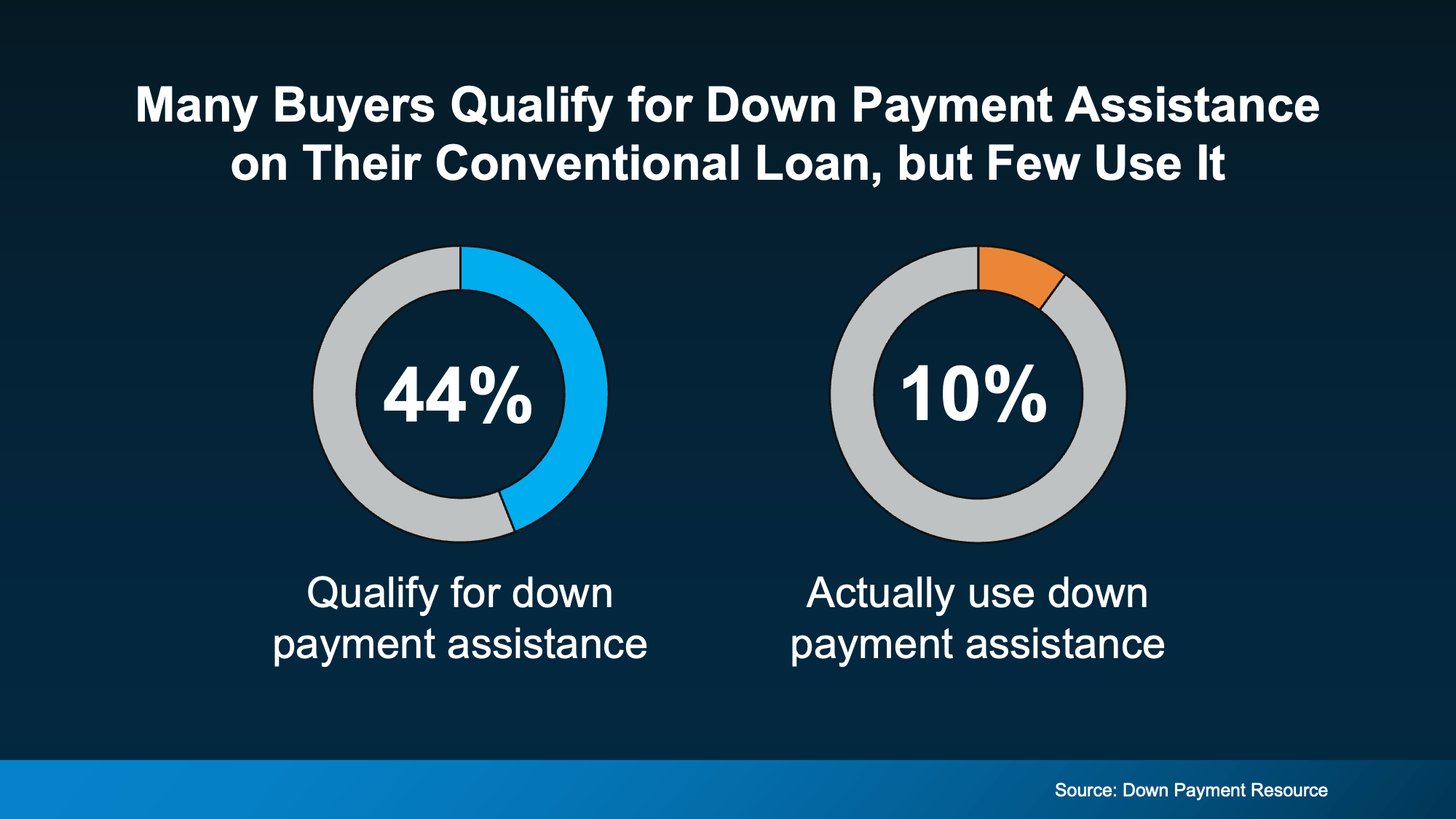

Help You May Not Know You Qualify For

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

-

There are more than 2,600 down payment assistance programs available

-

More than half (62%) are designed to help first-time buyers

-

38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

-

62% are open to buyers earning $100,000 or more

A Boost from Loved Ones

For a growing number of buyers, help comes from closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support most often goes toward the down payment, followed by help qualifying for a mortgage and covering closing costs. Chris Birk, VP of Mortgage Insight at Veterans United, puts it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, it can make a real difference in how soon you can buy.

Bottom Line

Down payments are smaller than they’ve been in years, and that opens the door for more buyers.

And with added help from assistance programs and a little help from loved ones, you may have more ways forward than you realized. Connect with a trusted lender to talk through your options.

You’ve probably heard plenty of doom and gloom about the housing market lately. High rates. Stretched budgets. Headlines that make buying or selling sound like a terrible idea. But the data tells a very different story.

This isn’t 2020 or 2021. It was never going to be. Those were the “unicorn years” – historic low mortgage rates, bidding wars on everything, homes flying off the market in days. That kind of market was a once-in-a-generation anomaly, not a baseline. So, when people compare today to that, of course it looks rough.

But compared to almost any other housing market in modern history? This one is holding up remarkably well.

Homeowners Are Sitting on a Mountain of Equity

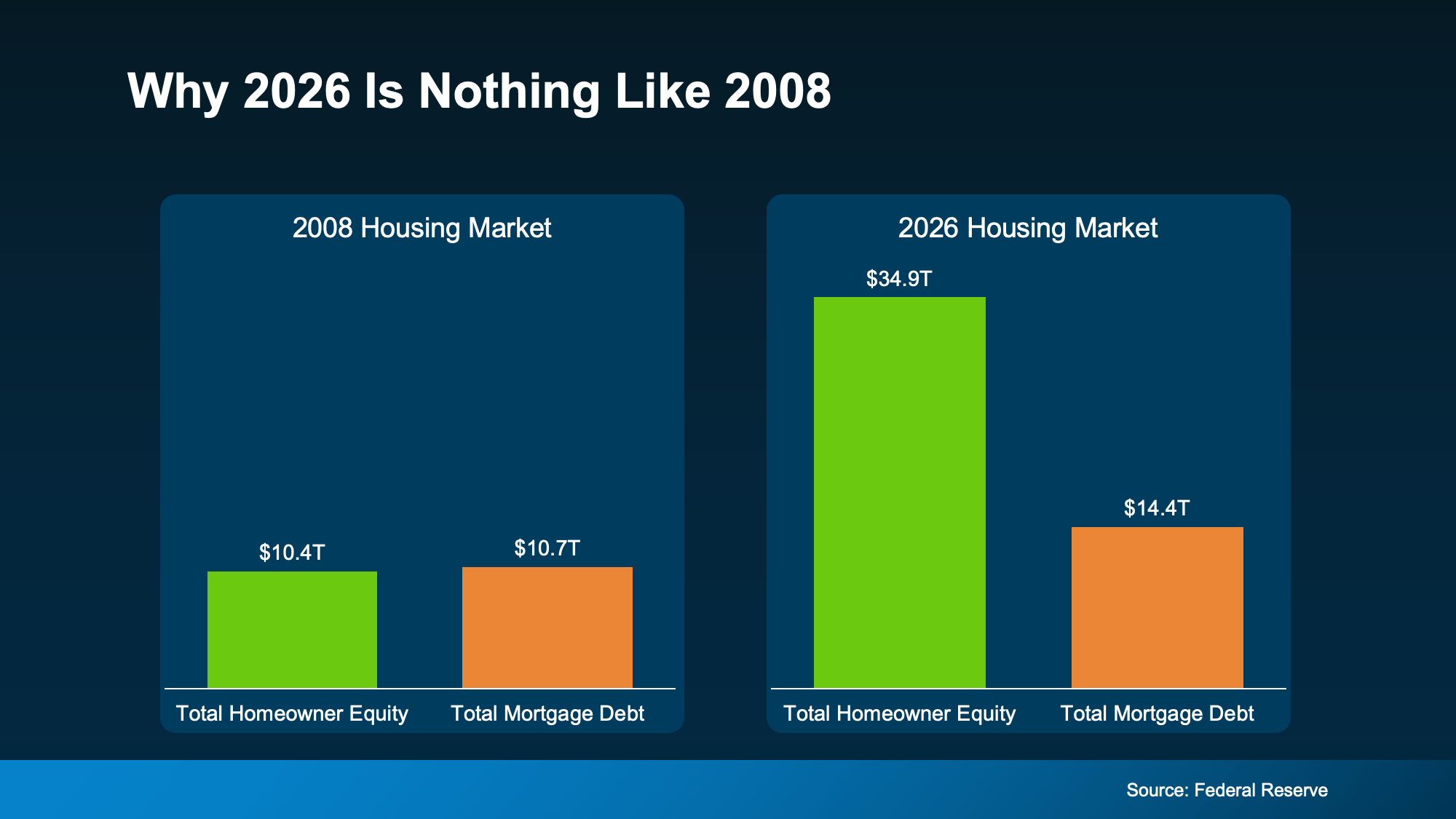

One of the biggest reasons this market hasn’t cracked is the financial strength of the American homeowner. According to Federal Reserve data, homeowner equity and mortgage debt were nearly identical in 2008. That means, if someone hit a rough patch, they had almost nothing to fall back on. That’s what made that crash so bad.

Today? Total homeowner equity across the country sits at $35 trillion – dwarfing total mortgage debt (see graph below):

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

-

Realtor.com found that homeowners who’ve been in their home just 5 years have built up around $180,000 in equity on average. Stick around 6-10 years, and that jumps to over $340,000.

-

Data from ATTOM and the Census shows two-thirds of homeowners either own their home outright or have more than 50% equity.

That’s not a fragile market. That’s a population of homeowners who are financially positioned to sell, to stay, or to make their next move from a place of strength rather than pressure.

Low Rates and Low Foreclosures

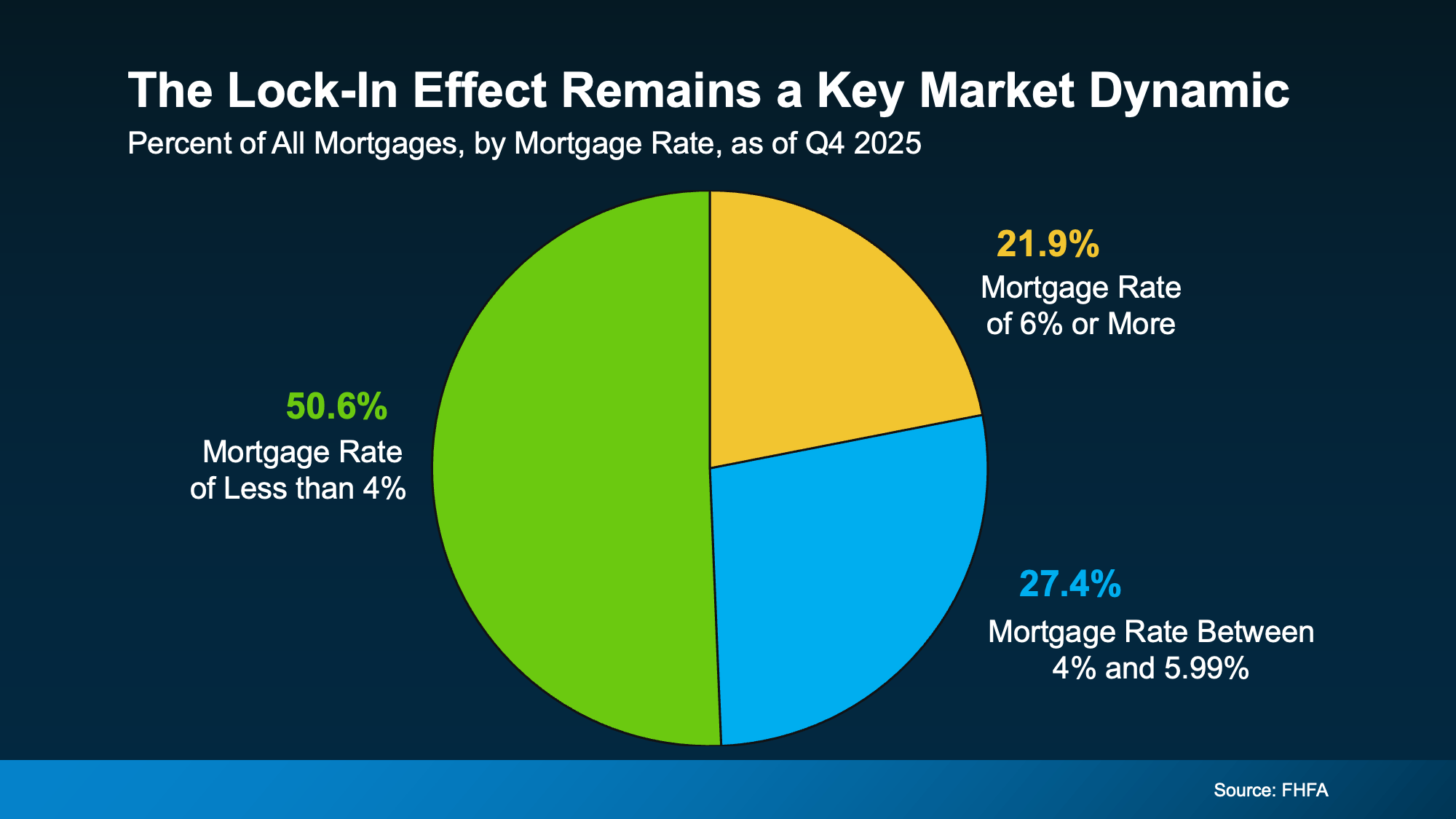

At the same time, Federal Housing Finance Agency (FHFA) data shows more than half of all active mortgages still carry a rate below 4% (see graph below):

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That comfort shows up in the foreclosure numbers, too. Despite a slight recent uptick, foreclosure volumes remain dramatically below historical norms, according to ATTOM. Homeowners aren’t losing their homes in droves. They have equity, they have breathing room, and most have options that keep them out of financial distress.

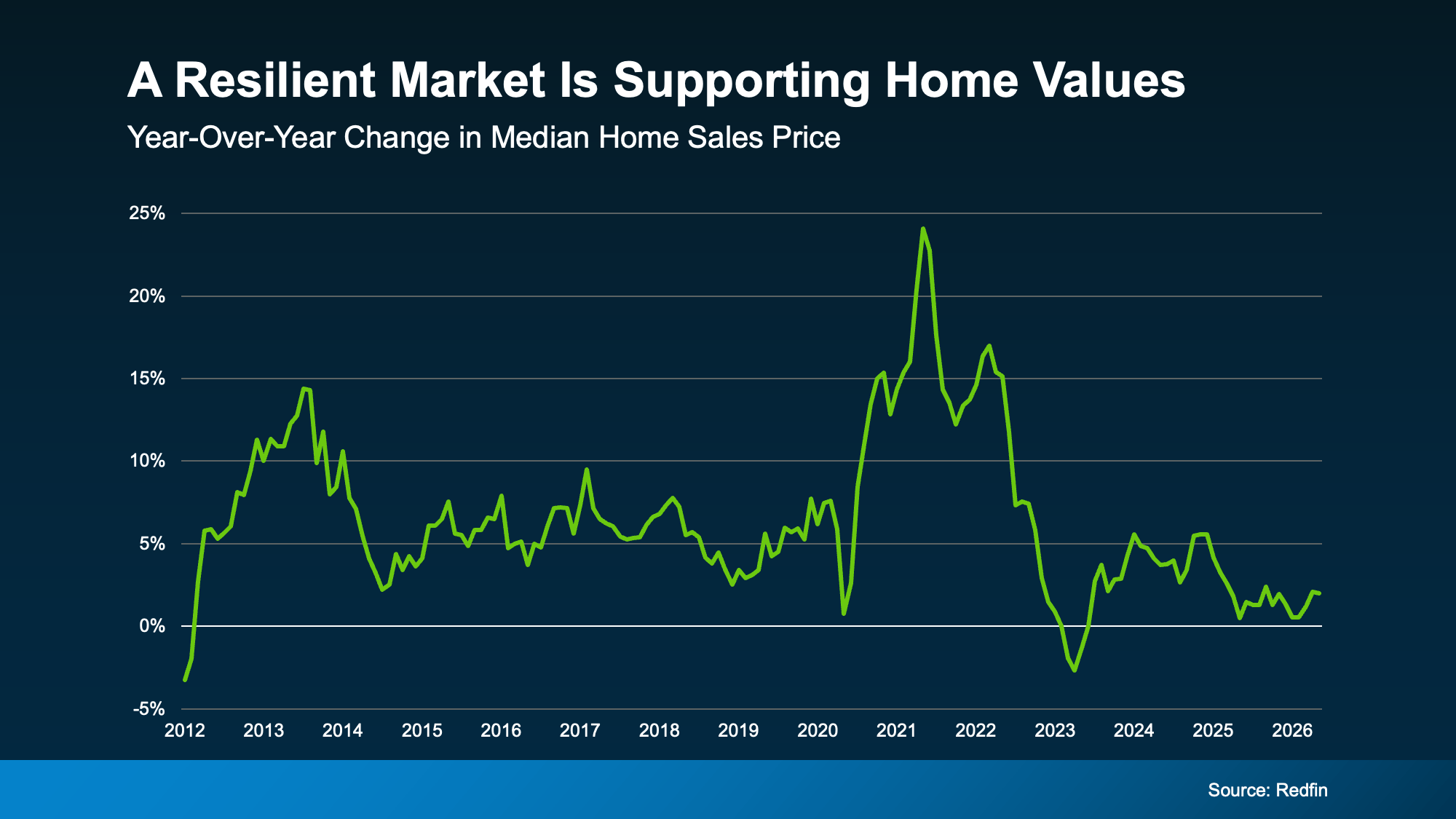

Prices Are Stabilizing, Not Crashing

Here’s another point on the resilience of the market. Redfin research shows home prices are still rising, but the pace has slowed, now closer to 2% year-over-year nationally (see graph below):

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

“We’re in the middle of a long-term housing market correction, not a housing market crash. After the pandemic-era frenzy sent prices soaring and inventory to historic lows, the market needed a reset.”

Bottom Line

This market isn’t broken, and waiting for a crash that isn’t coming has a cost. Every month spent on the sidelines is a month someone else is building equity, locking in a price, or getting ahead of what most experts expect to be a housing surge once broader economic conditions settle.

Whether you’re thinking about buying or selling, a local real estate agent can help you figure out what this market means for your specific situation and what your next move could look like.

What Buying or Selling a Home Gives Back to Your Community

Down Payments Are Smaller Than They’ve Been Since 2021

The Housing Market Is Stronger Than You Think

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoTwo Big Reasons To Move This Summer

-

Affordability4 weeks ago

Affordability4 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Affordability4 weeks ago

Affordability4 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers3 weeks ago

For Sellers3 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers3 weeks ago

For Buyers3 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

-

Affordability2 weeks ago

Affordability2 weeks agoThat House That’s Been Sitting Could Be Your Best Shot at a Deal

-

Agent Value3 weeks ago

Agent Value3 weeks agoIs It Still a Seller’s Market? Here’s What the Data Says.

-

Economy2 weeks ago

Economy2 weeks agoMore Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

You must be logged in to post a comment Login