Equity

You Could Use Some of Your Equity To Give Your Children the Gift of Home

If you’re a homeowner, chances are you’ve built up a lot of wealth – just by living in your house and watching its value grow over time. And that equity? It’s something that could help change your child’s life.

Since affordability is still a challenge, a lot of first-time buyers are struggling to buy a home in today’s market. Even if they have a stable job and a solid plan, buying can still feel out of reach. But that’s where your equity could make all the difference.

To give you an idea, the average homeowner with a mortgage has $311,000 worth of equity, according to Cotality (formerly CoreLogic). That’s significant. And some parents are using a portion of their equity to help their children become homeowners, too.

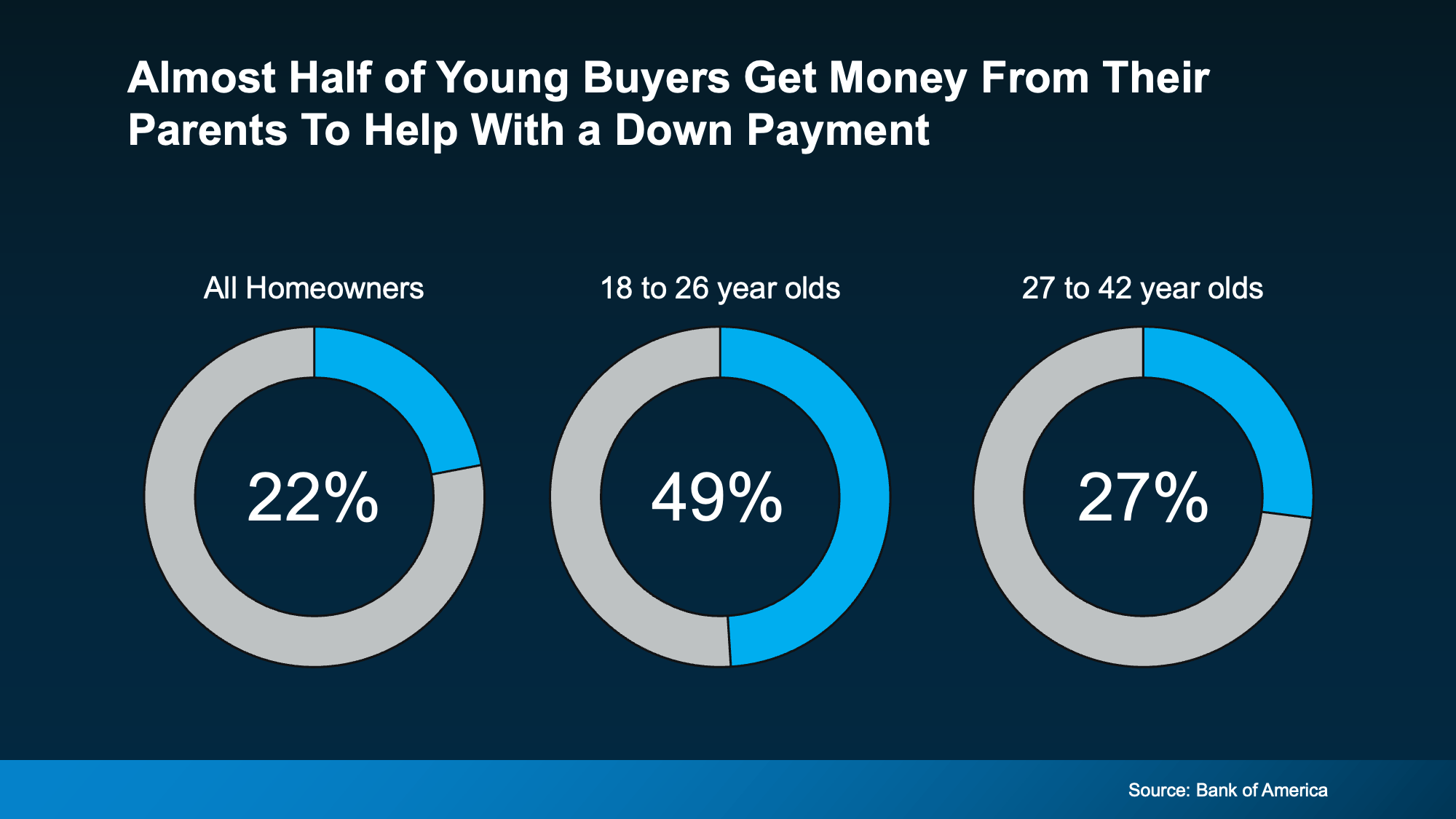

According to Bank of America, 49% of buyers between 18 and 26 got money from their parents to use toward their down payment (see chart below):

Even though the data doesn’t specify how many parents used their equity, the wealth they’ve built through homeownership may have helped make it possible – especially given how much equity the average homeowner has today.

Even though the data doesn’t specify how many parents used their equity, the wealth they’ve built through homeownership may have helped make it possible – especially given how much equity the average homeowner has today.

While what’s right for each person’s specific situation will vary on a case-by-case basis, that’s a powerful legacy to pass on. It helps those younger people buy a home, build equity of their own, and begin the next chapter of their life with a little less financial stress and a lot more stability. And for those parents? It’s a way to turn what they’ve built into something deeply meaningful.

This isn’t just about money. For many homeowners, it’s about being the reason their child gets to say, “we got the house.” And giving them the kind of head start they might’ve only dreamed of at their age. And here’s the part that really sticks. Compare the Market says:

“Of those who did receive monetary aid from parents and grandparents to buy a house, 45% of Americans said they would not have been able to purchase a house without financial support from parents and grandparents.”

Bottom Line

Your equity could be the thing that makes homeownership possible for your children when they might not be able to do it on their own. So, here’s the question.

If helping your kids buy a home was more feasible than you thought, would you want to explore that option?

If you want to learn more or find out the best way to make it happen, talk to your lender and a financial advisor you trust.

You may have seen the headlines lately about mortgage debt in America hitting a record high. And maybe your brother-in-law brought it up at the dinner table like he’s been waiting all week to spark a debate.

Here’s the thing. He’s not wrong. But he only has half the story. And the half he’s missing? It changes everything.

Spoiler: homeowners are on stronger footing than the headlines suggest, and the housing market has more going for it than most people realize.

The Headline Number Is Real, But It’s Missing Context

Yes, according to the Federal Reserve, there is currently about $14 trillion in mortgage debt in the United States. That is an all-time high. And when you hear that alongside stories about people struggling to pay their bills, it’s easy to assume the worst.

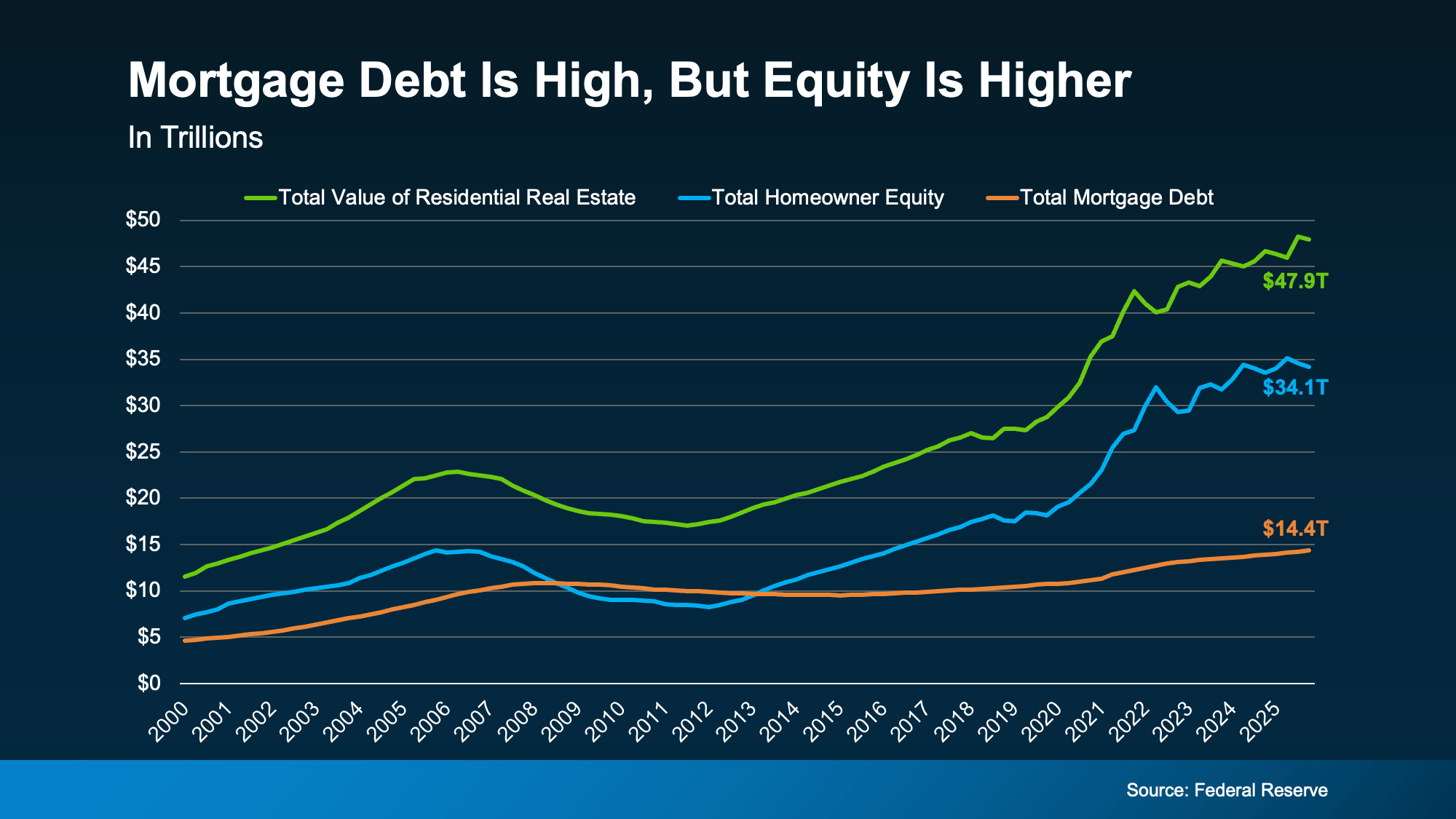

But here’s what the data actually shows (see graph below):

This chart from the Federal Reserve tracks three things from 2000 to today: the total value of all U.S. homes (the green line), the equity homeowners hold in those homes (the blue line), and the total mortgage debt owed on them (the orange line).

This chart from the Federal Reserve tracks three things from 2000 to today: the total value of all U.S. homes (the green line), the equity homeowners hold in those homes (the blue line), and the total mortgage debt owed on them (the orange line).

Right now, home values sit at $47.9 trillion. Homeowner equity is at $34.1 trillion. And the mortgage debt everyone’s worried about? It’s $14.4 trillion.

Debt is at a record high, sure. But the equity homeowners have built up is more than double that number, and it’s also near a record high.

Here’s the part worth pausing on. See the years between 2008 and 2013 where the orange line was higher than the blue one? That’s when the housing market was in genuine trouble. When debt exceeds equity like it did back then, homeowners have no cushion.

So, when prices dropped in 2008, millions of people owed more than their homes were worth and had nowhere to go. That’s what a housing crisis actually looks like. That’s not what’s happening today. Right now, it’s just the opposite.

The gap between what people owe and what they own has never been wider – in a good way. Today, they have far more equity than debt.

Most Homeowners Are in a Rock-Solid Position

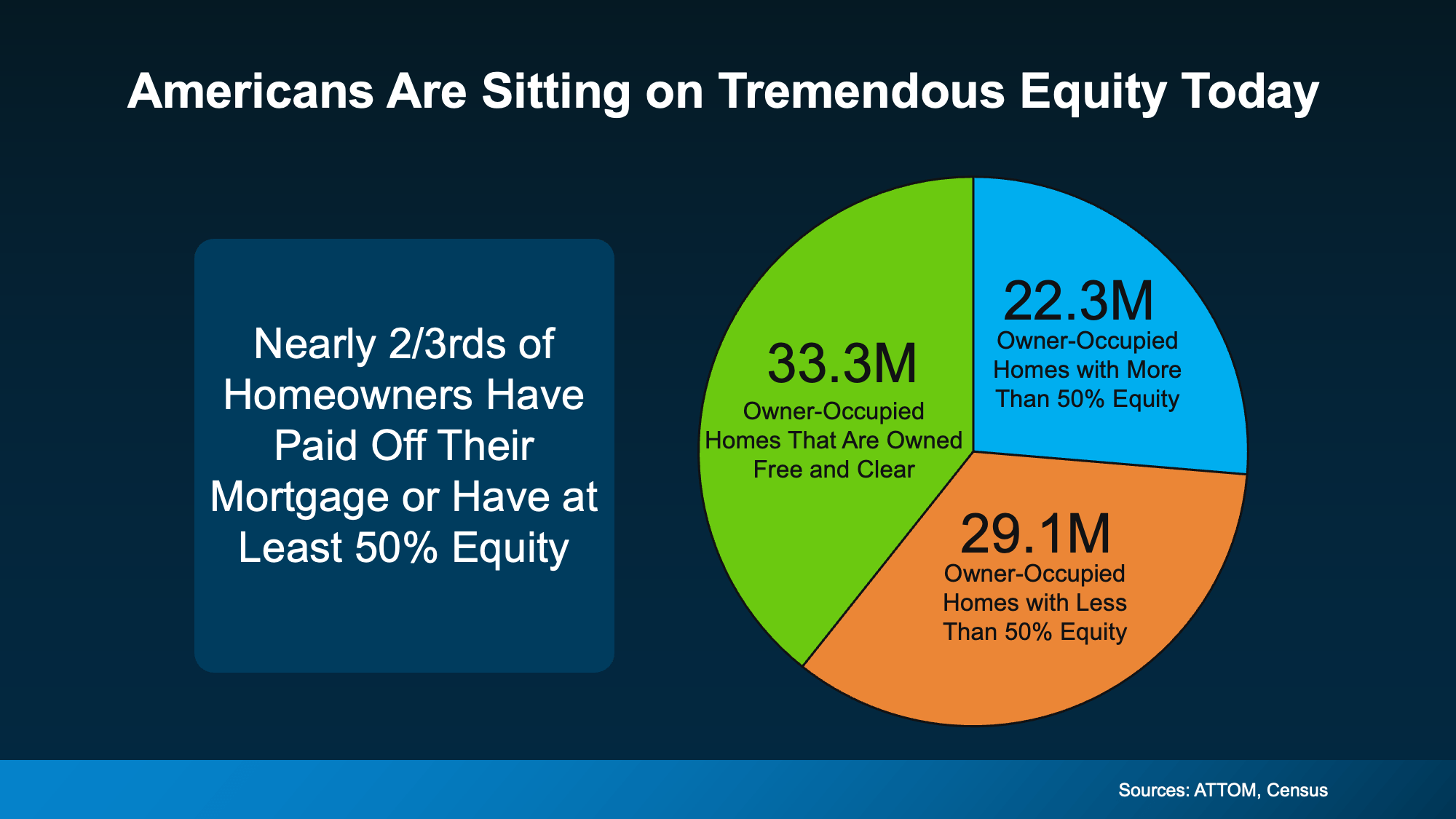

So, we know equity is high nationally. But what does that actually look like at the individual homeowner level? This next chart uses data from ATTOM and the Census to put it in perspective:

Out of all owner-occupied homes in the country, 33.3 million are owned completely free and clear – no mortgage, no lender, no risk of foreclosure. Another 22.3 million homeowners have more than 50% equity in their homes.

Out of all owner-occupied homes in the country, 33.3 million are owned completely free and clear – no mortgage, no lender, no risk of foreclosure. Another 22.3 million homeowners have more than 50% equity in their homes.

Add those together, and you’re looking at nearly two-thirds of all homeowners who have either paid off their mortgage entirely or have such a substantial equity stake that they’re in an extremely stable position.

The remaining slice – 29.1 million homes with less than 50% equity – isn’t a sign of distress, either. That includes plenty of people who recently bought, are building equity over time, and are doing just fine.

The point is this isn’t a market teetering on the edge. It’s a market built on an unusually strong foundation.

Bottom Line

Record mortgage debt makes for a scary headline. But context matters.

Equity is near an all-time high, home values have surged, and the vast majority of homeowners are in a position of real financial strength. The conditions that made 2008 a crisis simply don’t exist right now.

If you’re wondering what all of this means for your situation, whether you’re thinking about buying, selling, or just trying to make sense of the market, a local real estate agent would love to talk it through with you. Reach out anytime. No pressure, just answers.

It’s one of the biggest hold ups some buyers have right now: “What if I buy, and home prices go down?”

With everything in the news, that concern makes some sense. No one wants to make a big financial decision at the wrong time. But here’s what’s important to know. You don’t want to get hung up on the few places seeing slight declines right now.

When you zoom out and look at the full picture, home prices usually rise over time.

What the Data Really Shows

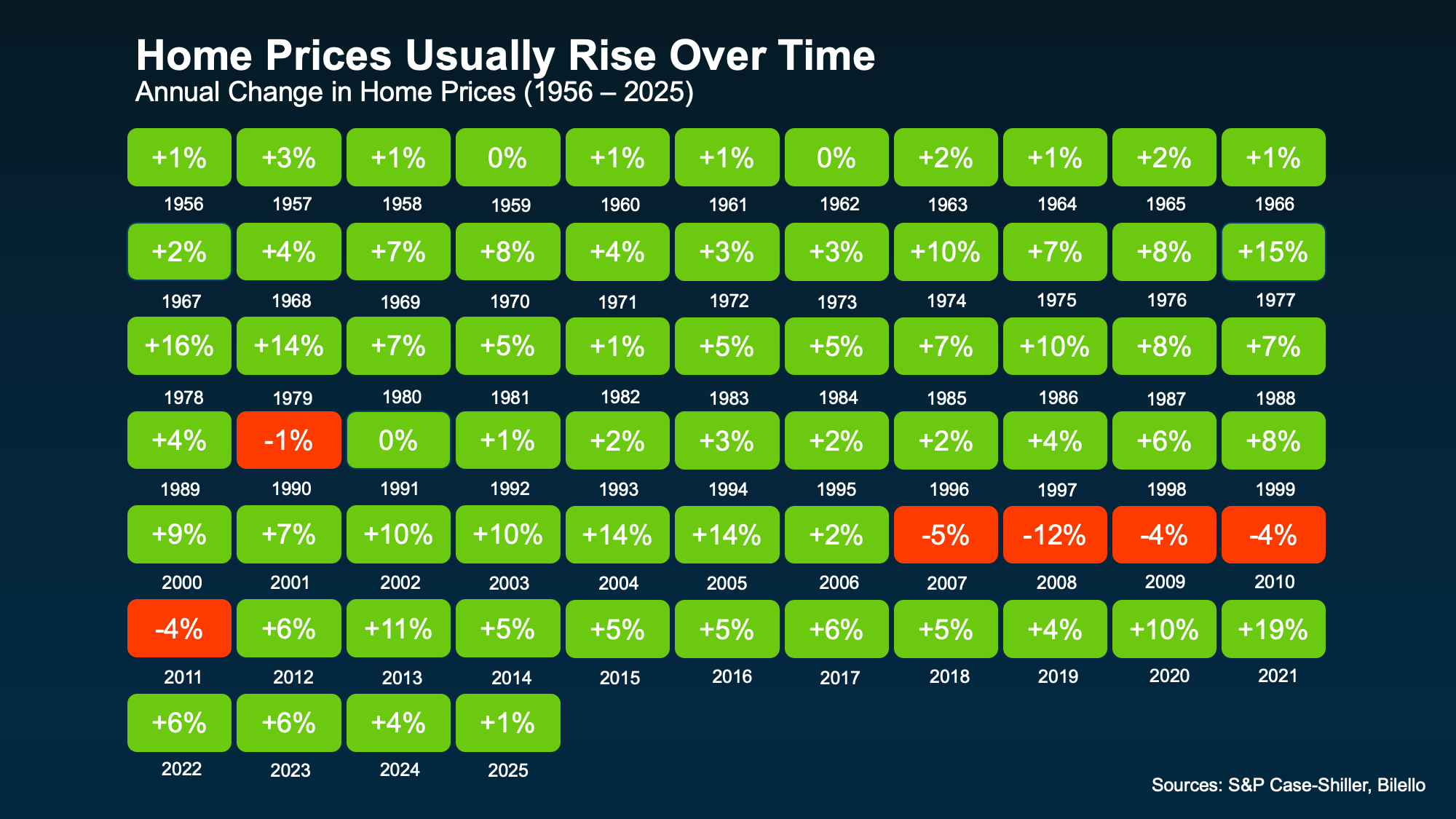

Take a look at the visual below. It uses data from Case-Shiller and Bilello to show how home prices have changed year by year going all the way back to the 1950s.

Here’s the key takeaway.

Outside of the housing crash, home prices have either held steady or increased in just about every year for decades (see visual below):

That’s a remarkably consistent track record. And it shows something a lot of headlines miss.

That’s a remarkably consistent track record. And it shows something a lot of headlines miss.

While short-term shifts can happen, it’s the long-term gains that really matter.

Why Prices Tend To Rise Over Time

There are a few core reasons prices usually go up each year:

- There are always people who need to move. People need a place to live, and that demand will never fully go away. It may ebb and flow, but someone will always have to move as big changes happen in their life. So, homes stay in demand.

- There still aren’t enough homes for sale. While the number of homes for sale has grown, nationally there’s still an undersupply based on how many people want a home. That keeps upward pressure on prices.

- Inflation has an impact. Over time, the cost of goods (including homes) naturally increases. That pushes home values higher.

What That Means for You as a Buyer

It’s easy to get caught up in what might happen with home prices next month or next year, especially if you’re a first-time buyer and you’re feeling a little anxious about making such a big financial commitment. But the big picture is clear. Prices usually rise.

That doesn’t mean prices will go up every single year in every market. Real estate is local, and there can be short-term ups and downs. We’re seeing that in some places right now. You can even see it in the few annual dips in the visual above.

But historically, the declines have been temporary.

That’s why it’s generally recommended to buy a home only if you plan to stay for a while – typically at least five years. That’s normally enough time to see your house grow in value. And, it’s enough so you can ride out any short-term changes in the market.

Because when you can do that, something powerful happens. Those rising home values grow your net worth, and by extension, help you build wealth.

The right decision isn’t about timing the market perfectly. It’s about making a move that works for your life and staying in it long enough to benefit from the bigger trend.

Bottom Line

Home prices have a long track record of going up over time. And that’s why buying a home is generally considered a safe long-term investment.

That certainly doesn’t mean you have to buy now. You should only move when it makes sense, and you plan to live there for a while.

But if you’re interested, let this reassure you. If you want to talk about what home prices are doing in our market, your goals, or your timelines, reach out to a local agent.

You’ve probably seen the headlines saying, “foreclosures are on the rise,” and maybe your mind jumped straight to 2008. That’s understandable. A lot of people remember that crash and all the foreclosures that happened during that window, and they’re hoping something like that never happens again.

But this isn’t a repeat of what happened back then. Here’s the context to prove it.

Foreclosures Are Rising, But They’re Still Historically Low

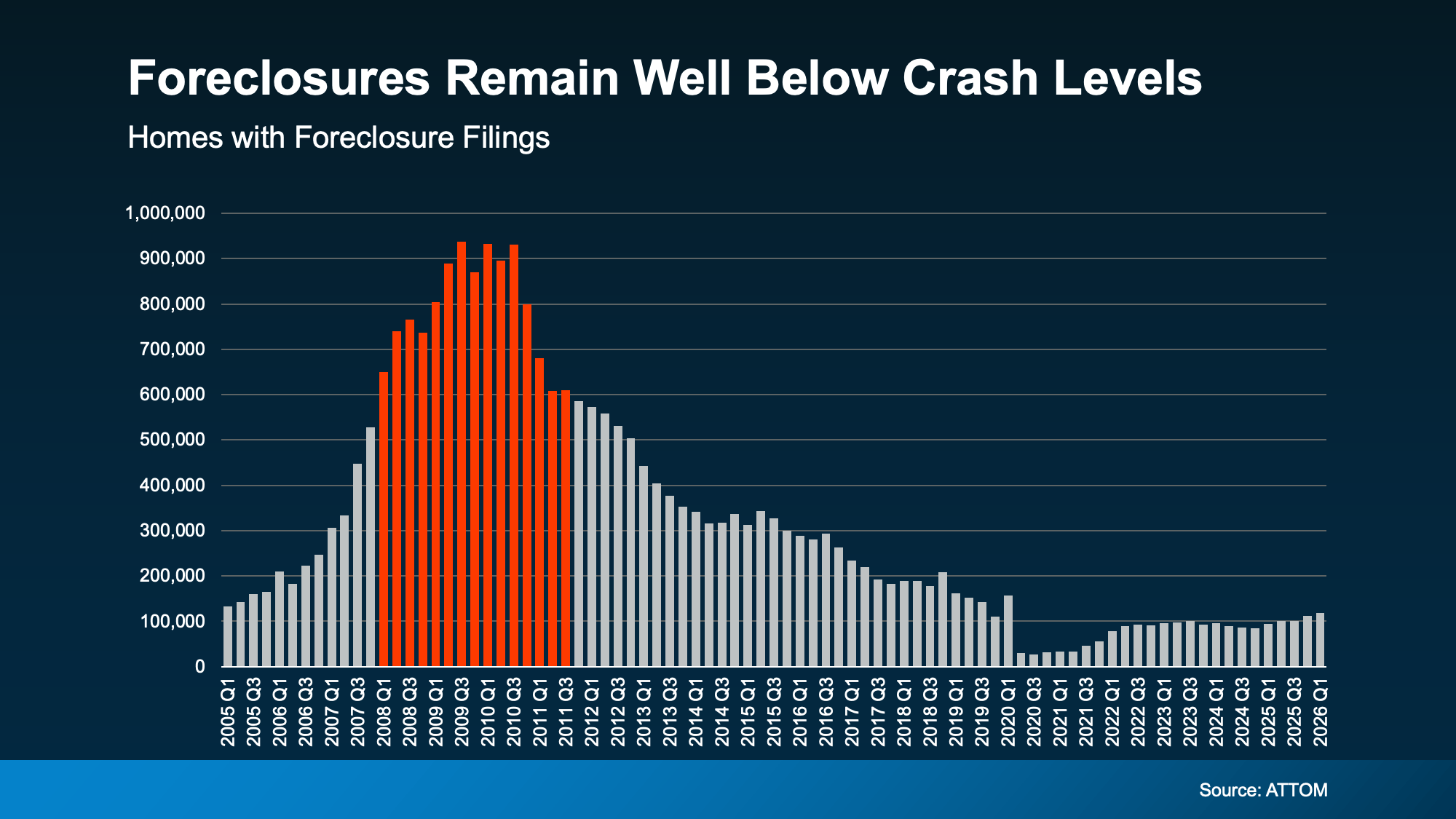

Yes, foreclosure filings are up 26% from a year ago, according to ATTOM. And they’ve been rising for 5 straight quarters. That’s a real trend worth paying attention to. But the full picture isn’t scary like the headlines suggest.

The reality is the increase we’re seeing is a sign of the market normalizing.

Here’s an important thing to know about this chart. The extremely low numbers you see in 2020 and 2021 don’t represent what’s “normal.” That’s when the government put a moratorium on foreclosures to help homeowners get through the pandemic. Those years were an exception, not the baseline.

Instead, compare where we are today to 2017, 2018, and 2019 – the last years the market was running normally. Today’s numbers are still lower. So, we’re not even back to what’s typical, yet. That means this can’t be a crash. (see graph below):

While today’s numbers are getting closer to pre-pandemic levels, they’re still below historical norms. And just look at what was happening around 2008. Even with the recent increase, we’re nowhere near those levels. This is a market returning to normal, not heading toward a crisis.

While today’s numbers are getting closer to pre-pandemic levels, they’re still below historical norms. And just look at what was happening around 2008. Even with the recent increase, we’re nowhere near those levels. This is a market returning to normal, not heading toward a crisis.

Why Today’s Equity Picture Changes Everything

Most of those filings won’t even end in a completed foreclosure. That’s because today’s homeowners have something most people in 2008 simply didn’t have. And that’s equity.

The average homeowner today is sitting on roughly $295,000 in home equity right now, according to Cotality. Back in 2008, many people owed more than their homes were worth. Selling wasn’t an option. And foreclosure was often the only door available.

Today, that’s not the case. If you have enough equity to cover what you owe and the cost of selling, you could sell your home, pay off your debt, protect your credit, and potentially walk away with money in your pocket.

That’s a completely different situation than what homeowners faced during the last crash, and it’s a big reason we’re unlikely to see foreclosures spiral the way they did back then.

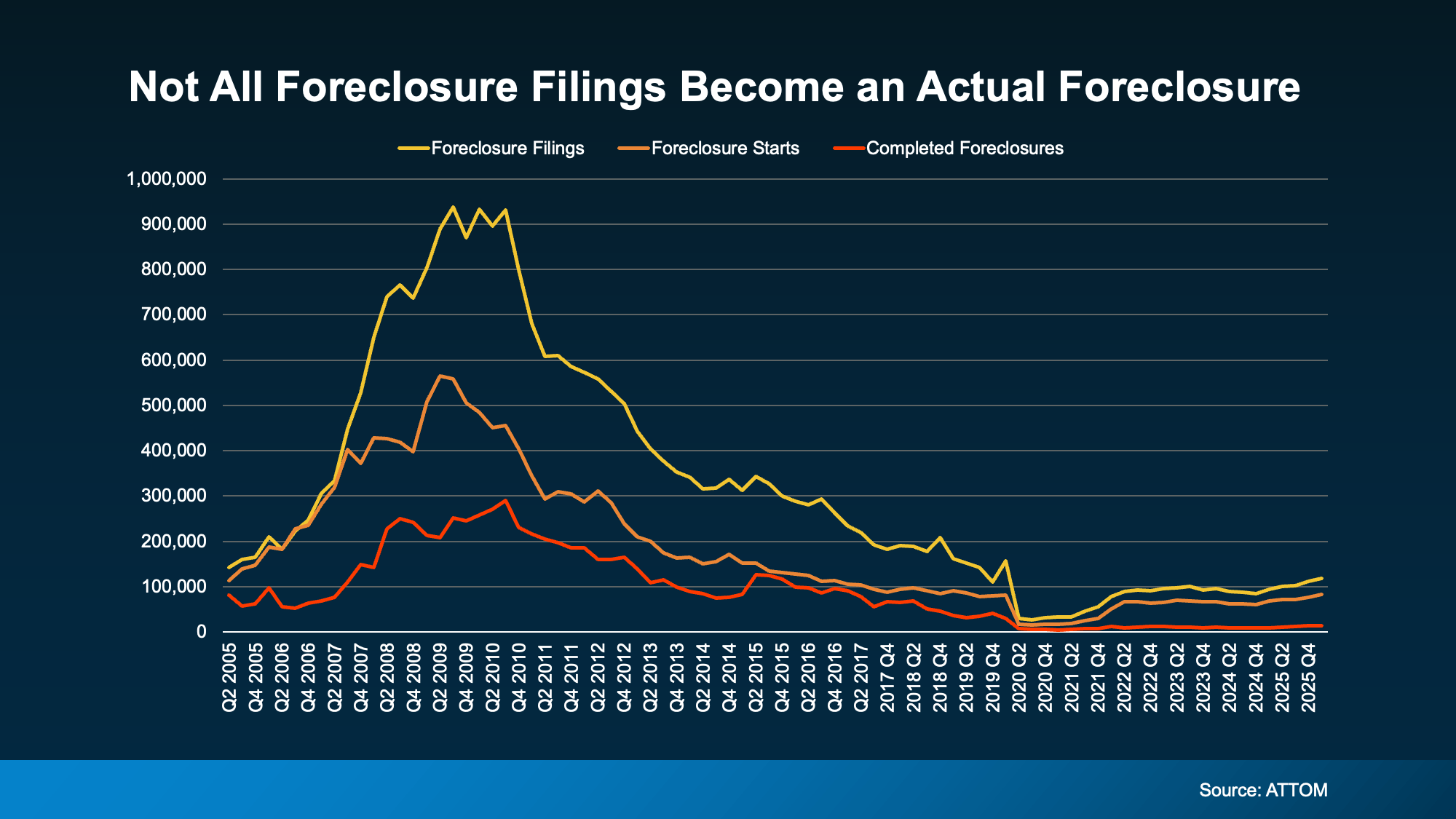

Check out the graph below. It shows foreclosure data from ATTOM going back to 2005. Here’s how to read it:

- The yellow line tracks all foreclosure filings.

- The orange line tracks foreclosure starts, meaning the process has officially begun.

- And the red line at the bottom tracks completed foreclosures (the ones where a homeowner actually lost their home).

See how the red line stays well below the other two? That gap tells the real story. A lot of homeowners who enter the foreclosure process never end up losing their home because they find another way forward first.

See how the red line stays well below the other two? That gap tells the real story. A lot of homeowners who enter the foreclosure process never end up losing their home because they find another way forward first.

Today’s equity is a big reason for that. So, even the filings we are seeing now won’t all end in foreclosure.

If You’re Struggling, You Have More Options Than You Think

Maybe you’re behind on payments. Maybe you’re stressed about what comes next. That’s an incredibly hard place to be, but it’s important to know that missing a payment or two doesn’t automatically mean you’ll lose your home.

Banks would much rather work with you than foreclose. It’s a complicated, costly process for them, too. They’re often willing to set up a repayment plan, offer forbearance (a temporary pause or reduction in your payments), or modify your loan to make things more manageable long-term.

Just know the sooner you reach out to your lender, the more options you’ll have. In some states (ones that don’t require the foreclosure process to go through a court) things can move faster than people expect. Getting ahead of it early gives you and your lender the most room to find a solution.

And if selling makes more sense for your situation, a real estate agent can help you understand what your home is worth and whether that’s a path worth exploring.

Bottom Line

Foreclosure filings may be rising, but they’re still low. And the equity most homeowners are sitting on today is a key reason this looks nothing like 2008.

The 1 Factor That Explains Everything Happening with Home Prices Right Now

Your House Didn’t Sell. Here’s How To Turn It Around.

More Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Affordability4 weeks ago

Affordability4 weeks agoWhat Rising Inflation Means for Your Move

-

Economy4 weeks ago

Economy4 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability4 weeks ago

Affordability4 weeks agoLess House, More Home: Why Smaller Homes Are Paying Off for Today’s Buyers

-

Affordability3 weeks ago

Affordability3 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoTwo Big Reasons To Move This Summer

-

Affordability3 weeks ago

Affordability3 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers2 weeks ago

For Sellers2 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers2 weeks ago

For Buyers2 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

You must be logged in to post a comment Login