Demographics

Homeownership Rate on the Rise to a 6-Year High

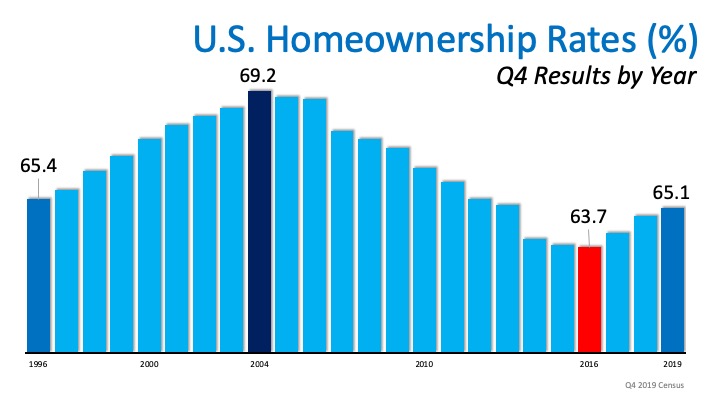

Regardless of the lack of inventory on the market, the U.S. homeownership rate has climbed to a 6-year high. The United States Census Bureau reported that it increased to 65.1% in the fourth quarter of 2019, representing the highest level in the past six years. See the graph below: This increase does not come as a surprise. According to realtor.com,

This increase does not come as a surprise. According to realtor.com,

“The largest cohort of the millennial generation turns 30-years-old in 2020 and they are hitting the housing market in full force. At the end of the fourth quarter of 2019, millennials made up the largest generational segment of homebuyers, growing their share of home purchase mortgages to 48 percent.”

With so many Millennials entering a homebuying phase of life and getting into the market, the Millennial Report also explains,

“Homeownership is an even bigger goal for younger generations. Of those with savings, 41 percent of Gen Z and 40 percent of younger millennials are saving to buy a home.”

Today’s low interest rates are providing a break to new homeowners too, regardless of generation, making homeownership more desirable and achievable at the same time. Freddie Mac explains,

“The combination of very low mortgage rates, a strong economy and more positive financial market sentiment all point to home purchase demand continuing to rise over the next few months.”

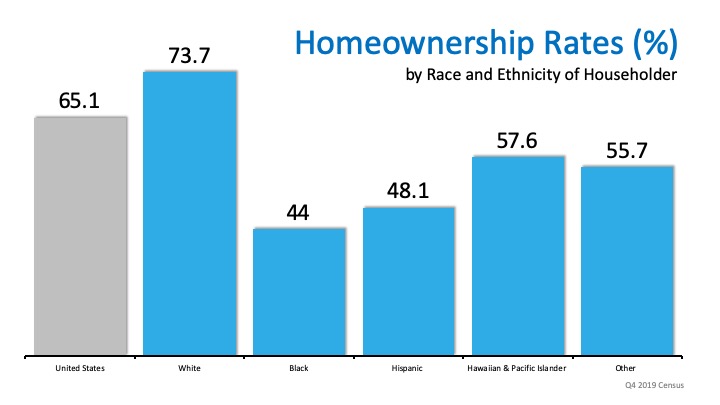

The increase in homeownership rate was also represented by race and ethnicity of the householders. HousingWire explains,

“The homeownership rate for black Americans in 2019’s fourth quarter rose to 44%, a seven-year high, increasing from the record low it reached in 2019’s second quarter. The rate for Hispanic Americans was 48.1%, a two-year high, the Census data showed…The rate for white Americans was 73.7%, an eight-year high.”

See the graph below:

Bottom Line

If you’re considering buying a home this year, let’s get together to set a plan that will help you get one step closer to achieving your dream.

Have you heard the term “Silver Tsunami” getting tossed around recently? If so, here’s what you really need to know. That phrase refers to the idea that a lot of baby boomers are going to move or downsize all at once. And the fear is that a sudden influx of homes for sale would have a big impact on housing. That’s because it would create a whole lot more competition for smaller homes and would throw off the balance of supply and demand, which ultimately would impact home prices.

But here’s the thing. There are a couple of faults in that logic. Let’s break them down and put your mind at ease.

Not All Baby Boomers Plan To Move

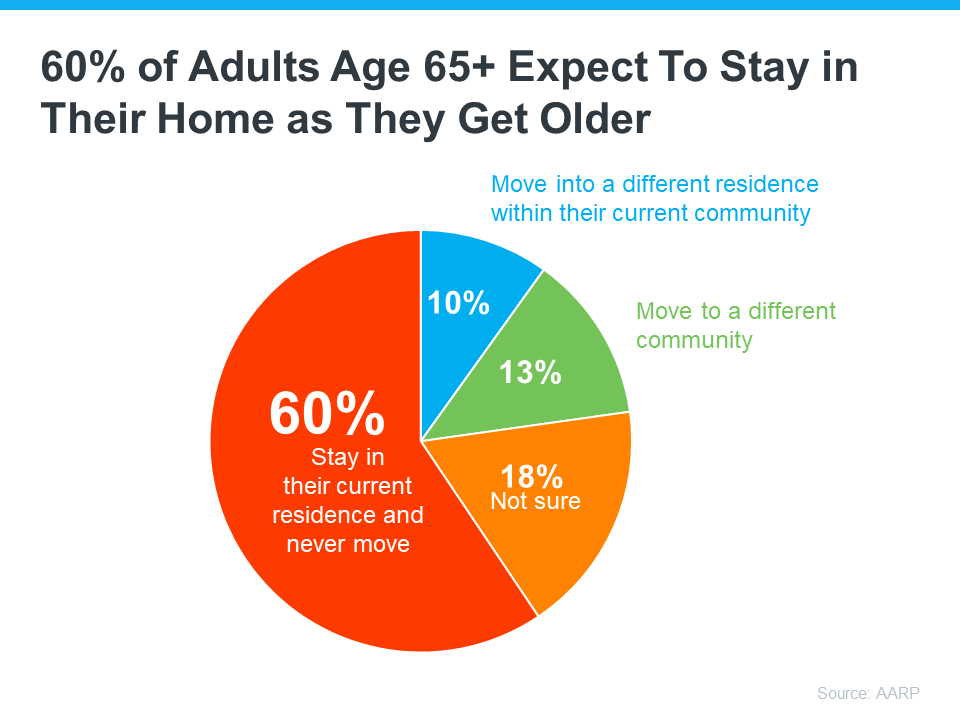

For starters, plenty of baby boomers don’t plan on moving at all. A study from the AARP says more than half of adults aged 65 and older want to stay in their homes and not move as they age (see graph below):

While it’s true circumstances may change and some people who don’t plan to move (the red in the chart above) may realize they need to down the road, the vast majority are counting on aging in place.

As for those who stay put, they’ll likely modify their homes as their needs change over time. And when updating their existing home won’t work, some will buy a second home and keep their original one as an investment to fuel generational wealth for their loved ones. As an article from Inman explains:

“Many boomers have no desire to retire fully and take up less space . . . Many will modify their current home, and the wealthiest will opt to have multiple homes.”

Even Those Who Do Move Won’t Do It All at Once

While not all baby boomers are looking to sell their homes and move – the ones who do won’t all do it at the same time. Instead, it’ll happen slowly over many years. As Freddie Mac says:

“We forecast the ‘tsunami’ will be more like a tide, bringing a gradual exit of 9.2 million Boomers by 2035 . . .”

As Mark Fleming, Chief Economist at First American, says:

“Demographics are never a tsunami. The baby boomer generation is almost two decades of births. That means they’re going to take about two decades to work their way through.”

Bottom Line

If you’re stressed about a Silver Tsunami shaking the housing market overnight, don’t be. Baby boomers will move slowly over a much longer period of time.

Have you ever heard the term “Silver Tsunami” and wondered what it’s all about? If so, that might be because there’s been lot of talk about it online recently. Let’s dive into what it is and why it won’t drastically impact the housing market.

What Does Silver Tsunami Mean?

A recent article from HousingWire calls it:

“. . . a colloquialism referring to aging Americans changing their housing arrangements to accommodate aging . . .”

The thought is that as baby boomers grow older, a significant number will start downsizing their homes. Considering how large that generation is, if these moves happened in a big wave, it would affect the housing market by causing a significant uptick in the number of larger homes for sale. That influx of homes coming onto the market would impact the balance of supply and demand and more.

The concept makes sense in theory, but will it happen? And if so, when?

Why It Won’t Have a Huge Impact on the Housing Market in 2024

Experts say, so far, a silver tsunami hasn’t happened – and it probably won’t anytime soon. According to that same article from HousingWire:

“. . . the silver tsunami’s transformative potential for the U.S. housing market has not yet materialized in any meaningful way, and few expect it to anytime soon.”

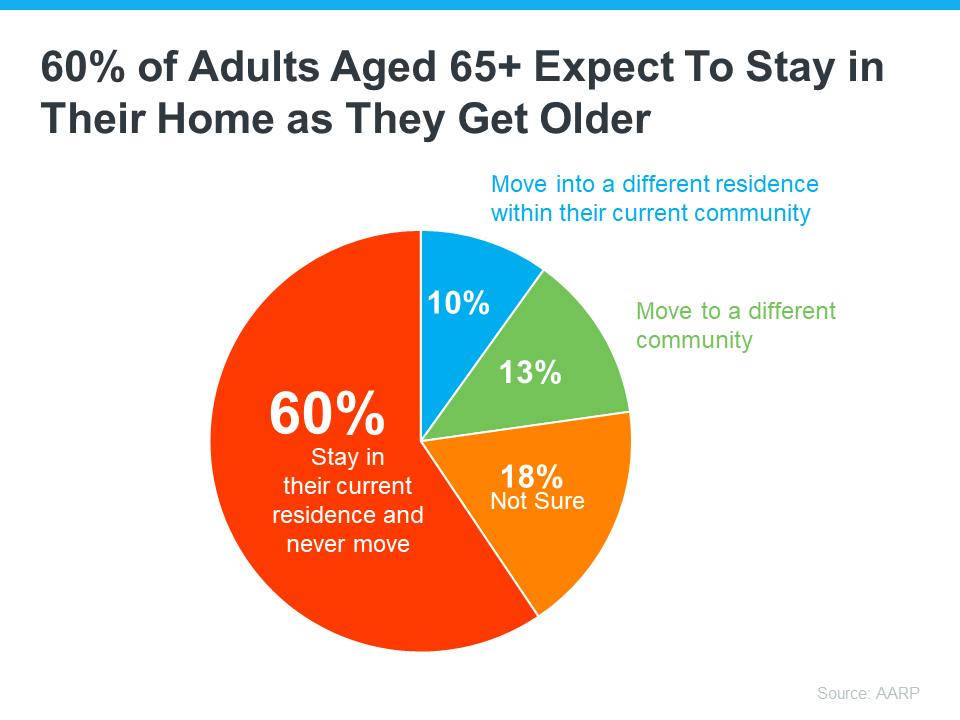

Here’s just one reason why. Many baby boomers don’t want to move. Data from the AARP shows over half of the surveyed adults ages 65 and up plan to stay put and age in place in their current home rather than move (see chart below):

Clearly, not every baby boomer is planning to sell or move – and even those who do won’t do it all at once. Instead, it will be more gradual, happening slowly over time. As Mark Fleming, Chief Economist at First American, says:

“Demographics are never a tsunami. The baby boomer generation is almost two decades of births. That means they’re going to take about two decades to work their way through.”

Bottom Line

If you’re worried about a Silver Tsunami shaking up the housing market, don’t be. Any impact from baby boomers moving will be gradual over many years. Fleming sums it up best:

“Demographic trends, they don’t tsunami. They trickle.”

The House That Started It All Could Kickstart What’s Next

Priced Out? A Condo or Townhome Could Be Your Way In.

More Homes, Better Prices: A Buyer’s Summer

-

Economy4 weeks ago

Economy4 weeks agoMore Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Agent Value4 weeks ago

Agent Value4 weeks agoYour House Didn’t Sell. Here’s How To Turn It Around.

-

Equity3 weeks ago

Equity3 weeks agoThe Housing Market Is Stronger Than You Think

-

Economy2 weeks ago

Economy2 weeks agoWhat Buying or Selling a Home Gives Back to Your Community

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoThe 1 Factor That Explains Everything Happening with Home Prices Right Now

-

Affordability3 weeks ago

Affordability3 weeks agoDown Payments Are Smaller Than They’ve Been Since 2021

-

Affordability2 weeks ago

Affordability2 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoStudent Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

You must be logged in to post a comment Login