For Buyers

Some Buyers Prefer Smaller Homes

If you’ve been looking for a home lately, you’ve probably felt how tough affordability still is. And that’s exactly why more buyers are opting for adjustable-rate mortgages, or ARMs.

Here’s what you need to understand about how they work, and whether they make sense for you.

What Is an Adjustable-Rate Mortgage?

Since a lot of people aren’t familiar with this type of loan, let’s start with a definition. This is how Business Insider explains the main difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Basically, one doesn’t change much over the life of your loan.

And one could change… either by a little, or a lot.

Of course, things like taxes or homeowner’s insurance can still have an impact on a fixed-rate loan, but the baseline of your mortgage payment is fairly steady. But the big difference is that with an ARM, your monthly payment could change over time.

Why Adjustable-Rate Mortgages Are Getting More Attention

So, why do some buyers choose this option? It’s simple. It’s because of the upfront savings. Business Insider explains it like this:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

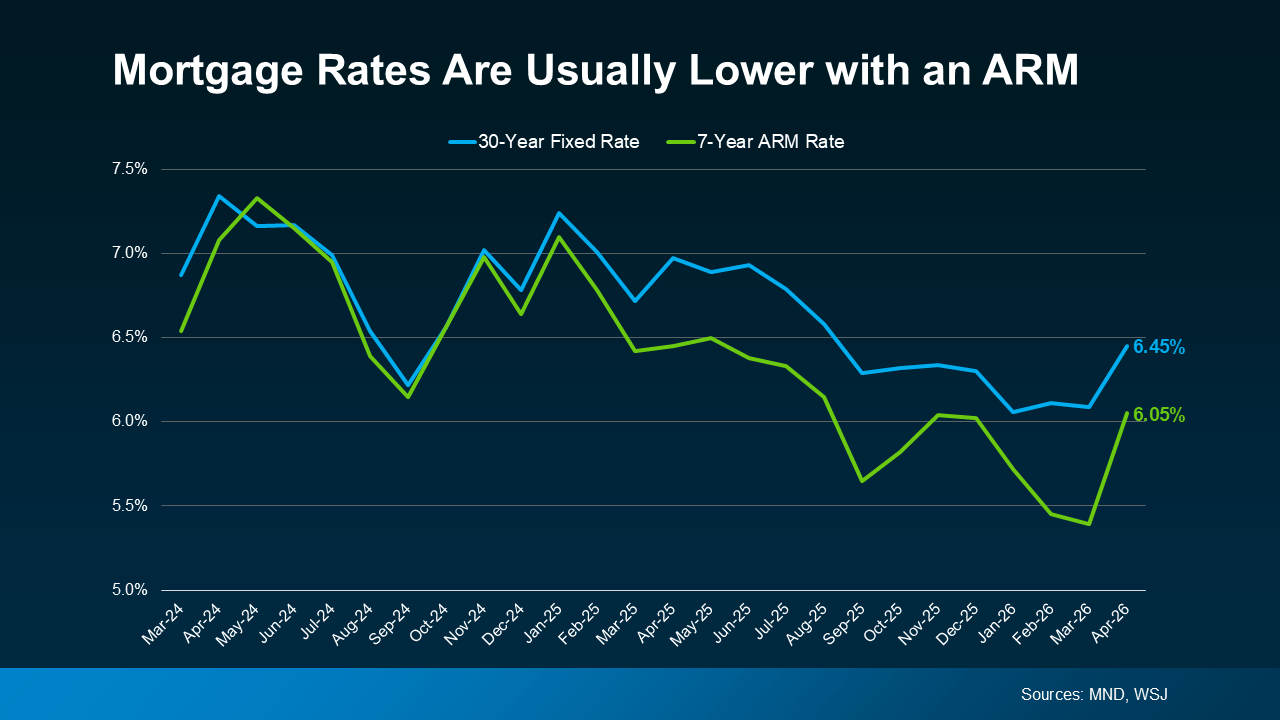

And right now, according to Mortgage News Daily and the Wall Street Journal, the upfront rate on an ARM is lower than a 30-year fixed mortgage (see graph below):

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

For some people, that’s enough to make a difference.

More Buyers Are Choosing Adjustable-Rate Mortgages Today

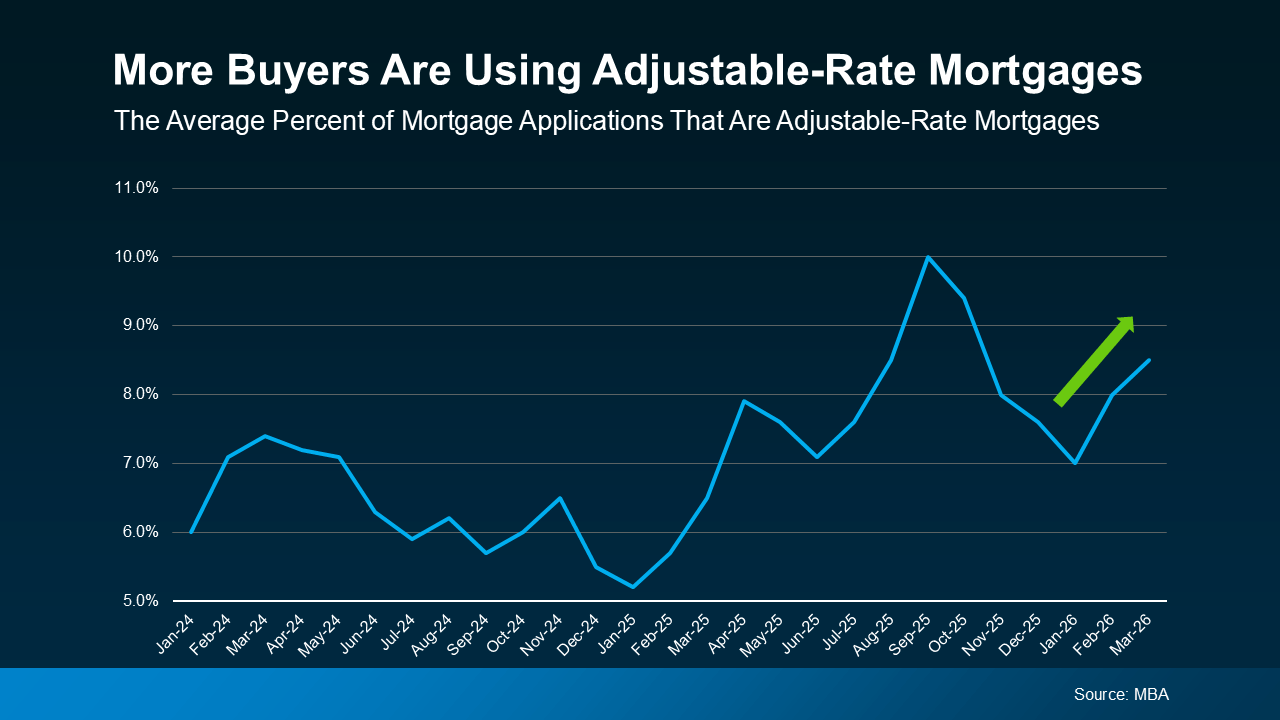

A growing number of buyers are willing to trade the uncertainty later for a lower payment now. Data from the Mortgage Bankers Association (MBA) shows the share of buyers choosing ARMs has increased, especially over the last few years (see graph below).

This doesn’t mean ARMs are becoming the go-to option for everyone. It only means some buyers are opting for this type of mortgage, so they can still buy today.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

Back then, some buyers were given loans they couldn’t afford once rates adjusted.

Today, lending standards are stricter, and lenders evaluate whether borrowers could still handle the payment if rates rise. So, the return of ARMs doesn’t signal another widespread crash. It just reflects how some buyers are adapting to today’s affordability challenges.

The Trade-Off – What You Need To Consider

If you’re considering an adjustable-rate mortgage yourself, just remember it really all depends on your situation and your risk tolerance.

An ARM may make sense if you plan to move before your rate would adjust or if you expect you’ll make a higher income in the future. But there are trade-offs you need to think through.

For example, once the fixed period ends, your rate can adjust, and your payment could increase, potentially by a meaningful amount depending on where rates are at that time.

And keep in mind, there’s also no guarantee mortgage rates will come down in the future, which means refinancing later isn’t always an option. That’s why it’s important to think through your plan, understand your long-term earning potential, and work closely with a trusted lender before you choose an ARM.

Bottom Line

ARMs are getting more attention again because they can make buying a home more affordable in the short term. But they’re not right for everyone.

The key is understanding how they work, what the risks are, and whether they fit your plan. And that’s why you need to talk to a trusted lender and financial advisor before you make any decisions.

Spend about 5 minutes online searching for news about the housing market, and odds are you’ll see something pop up about home prices. You may even stumble onto social media influencers saying we’re headed for a crash. Let’s get you the context you need.

The truth is prices are going to vary depending on where you live. But they’re not crashing.

Here’s what you need to know.

The Local Perspective: Home Price Trends by Area

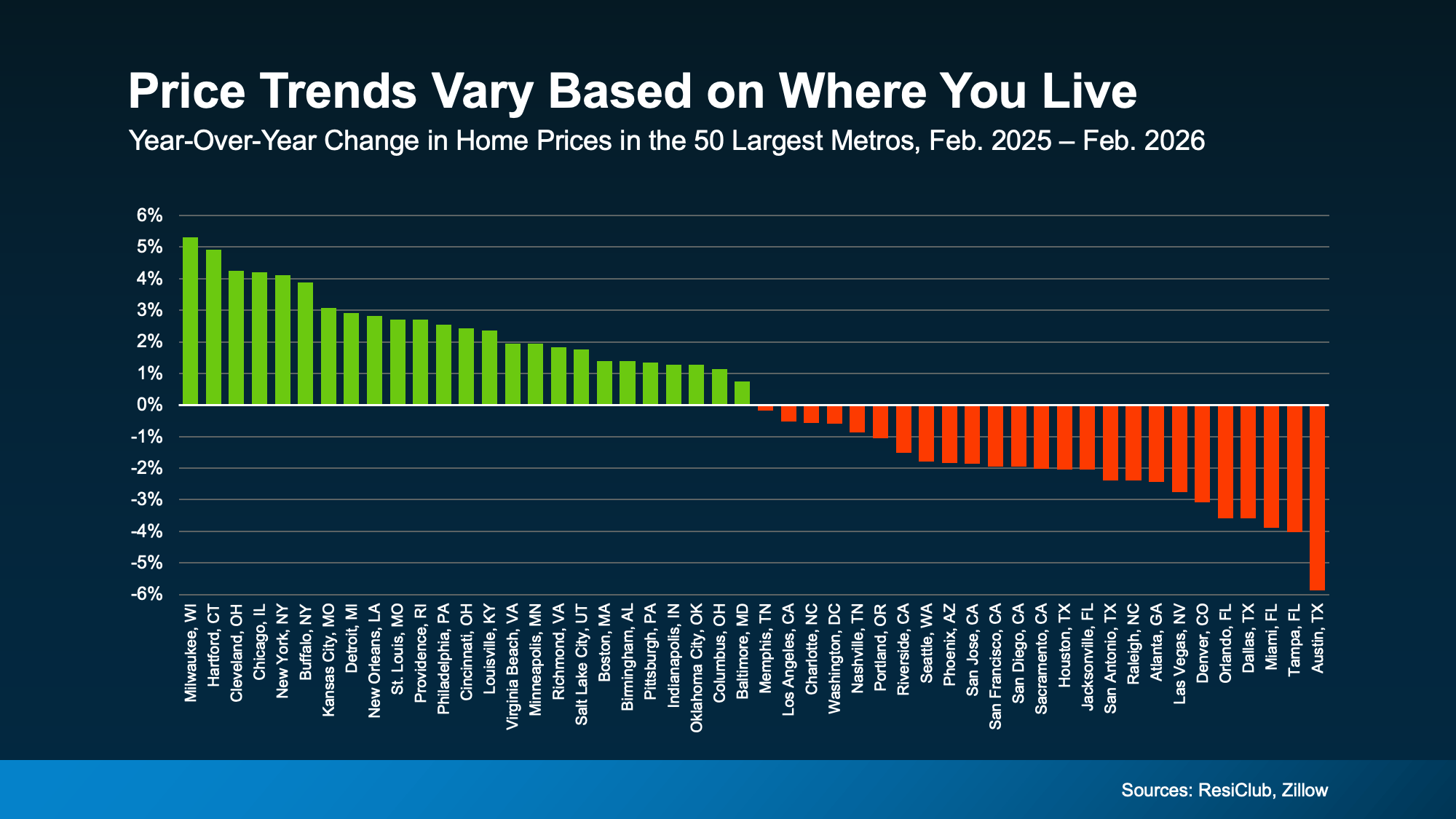

The biggest thing feeding into the confusion online is how different home price trends are by area right now. Take a look at this data from ResiClub and Zillow (see graph below).

About half of the largest metros are seeing prices go up.

The other half are seeing some declines.

Unfortunately, the online chatter only focuses on the markets where prices are down – and that makes it sound like something bigger is happening.

Unfortunately, the online chatter only focuses on the markets where prices are down – and that makes it sound like something bigger is happening.

But, as you can see in this graph, that’s only one side of the story. The full picture is different.

The National Perspective: Moderate Price Growth

As a country, when you average it all together to get a true baseline, one thing becomes clear, home prices are still net positive at the national level.

According to the Redfin, national home prices were up about 1% year-over-year in February. So, what we’re seeing right now isn’t a collapse. It’s a market that’s normalizing after a period of unusually fast growth. And that impacts some local markets more than others – particularly those where prices rose too far, too fast during the pandemic.

A true crash, like what happened in 2008, would mean prices dropping sharply across the entire country. That’s just not what the data shows today. And it’s not where things are going either.

Experts Agree This Isn’t 2008

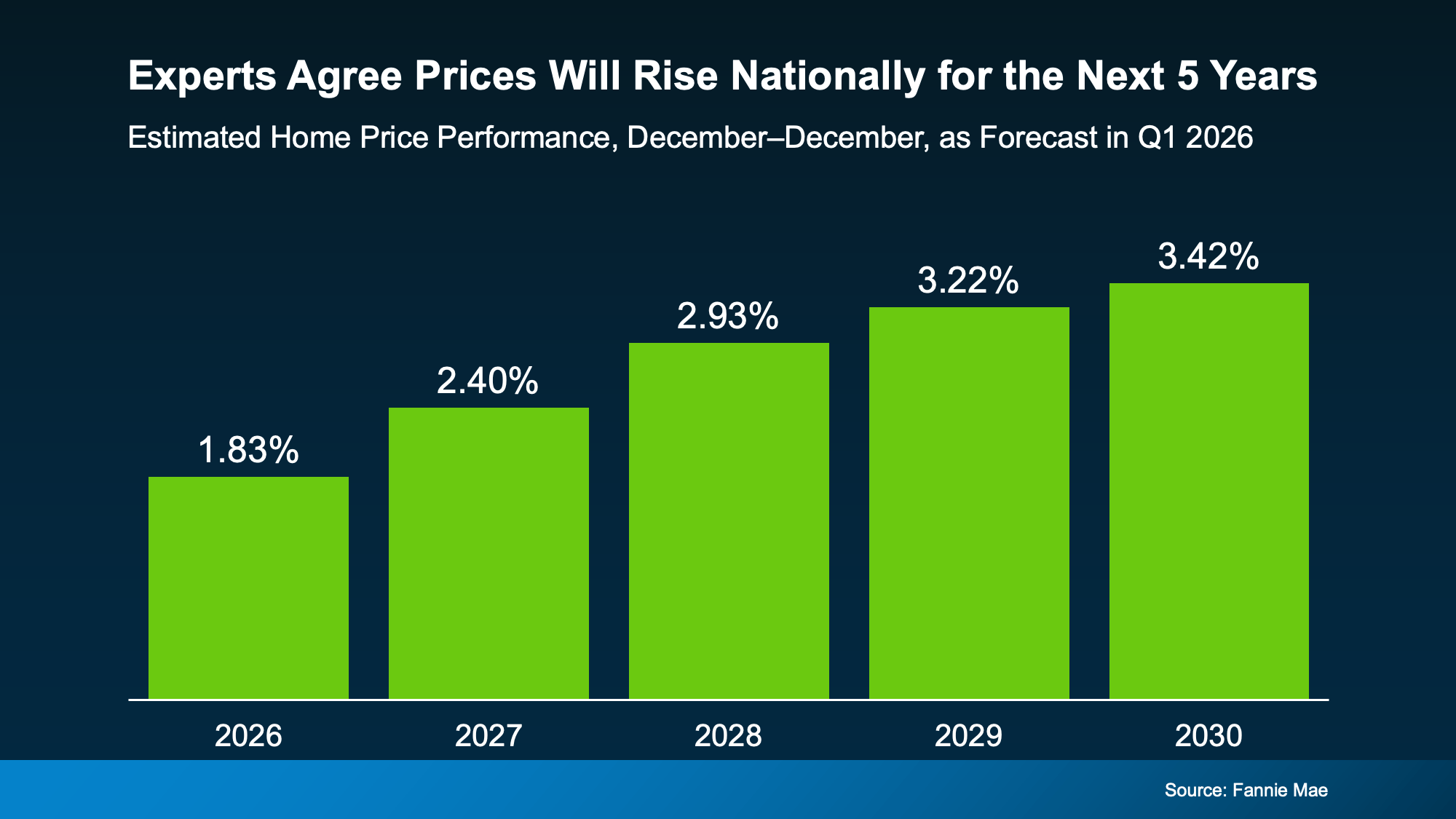

In fact, Fannie Mae surveyed over 100 housing market experts to ask their opinions on where prices are headed from here. And the experts agree, nationally, prices are expected to keep rising over the next five years:

That rise will be moderate, particularly this year, but the trend is clear. Nationally, prices are forecast to grow every year now through at least 2030 – and that’s normal. Daryl Fairweather, Chief Economist, at Redfin explains:

That rise will be moderate, particularly this year, but the trend is clear. Nationally, prices are forecast to grow every year now through at least 2030 – and that’s normal. Daryl Fairweather, Chief Economist, at Redfin explains:

“House prices aren’t going to fall on a national scale any time soon—and that’s actually a good thing. It’s normal for house prices to rise gradually over time . . .”

That’s why even in the select areas where prices have dropped slightly this year, the decline is expected to be temporary. According to that same quarterly Fannie Mae survey mentioned above, 85% of the experts say the markets that are seeing mild declines right now will return to positive price growth before the end of 2027.

The main takeaway? This isn’t a crash. And prices aren’t expected to fall nationally. If anything, the few areas experiencing declines are expected to rebound in the next year or so.

Bottom Line

It’s easy to get caught up in headlines that make it sound like something big is about to happen. But don’t be fooled. The housing market isn’t crashing. It’s just shifting.

The key is understanding what’s actually happening in your market, so you can make the right move for you. Connect with a real estate agent if you want the local perspective.

Thinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

Your House Hasn’t Sold Yet. Should You Rent It Out Instead?

Before You Fall in Love with a House, Do This First.

-

Agent Value4 weeks ago

Agent Value4 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

For Buyers4 weeks ago

For Buyers4 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

-

Agent Value3 weeks ago

Agent Value3 weeks agoThe #1 Reason Buyers Walk Away (And How To Get Ahead of It)

-

For Buyers1 week ago

For Buyers1 week agoDon’t Let Home Prices Headlines Fool You

-

Affordability3 weeks ago

Affordability3 weeks agoAffordability Has Improved in All 50 States

-

Agent Value3 weeks ago

Agent Value3 weeks ago3 Must-Do’s for First-Time Home Buyers

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoYou Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

-

Equity2 weeks ago

Equity2 weeks agoThe Remodel You’ve Been Dreaming About May Be Closer Than You Think

You must be logged in to post a comment Login