For Sellers

Why You May Want To Cash in on Your Second Home

For a lot of parents or grandparents, watching a family member struggle to buy their first home right now is hard. That’s because you saw firsthand how homeownership gave your life more stability and helped grow your net worth – and you want your loved ones to have those same opportunities.

But with all the affordability challenges in recent years, that can feel like an uphill battle – even though it’s slowly improving lately. Here’s what you may not realize. You may be in a unique position to help (thanks to the equity in your current house).

The Equity Advantage You May Not Be Thinking About

You’ve likely owned your home for years, maybe even decades. And during that time, two things happened:

- Home values rose

- Your mortgage balance shrank (or you paid it off entirely)

That combination has created substantial equity for many homeowners like you.

And while you may think of that equity as something you want to have in your pocket for retirement, it can also serve another purpose: helping the next generation clear the biggest hurdle in their way.

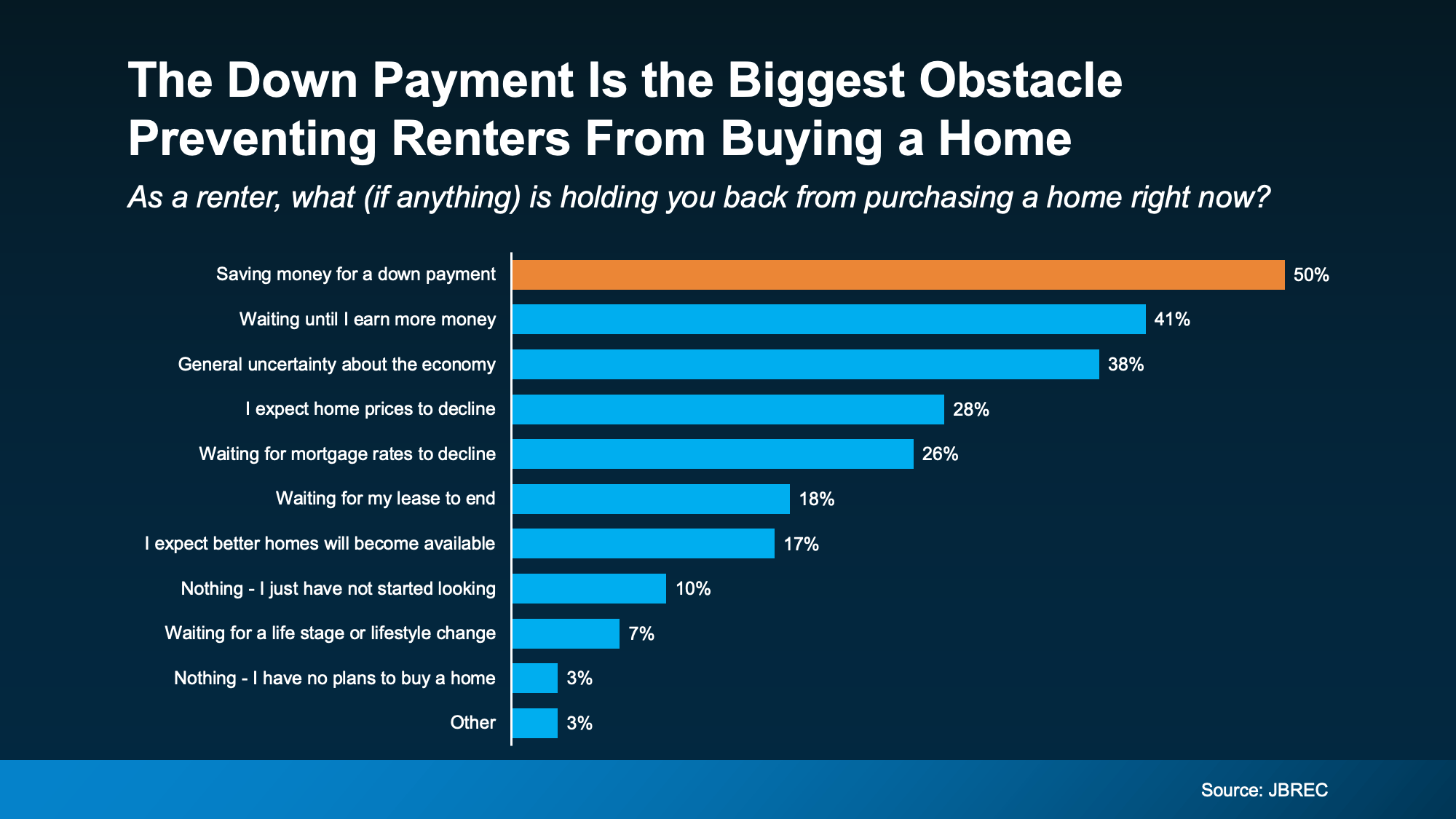

The #1 Thing Holding Young Buyers Back

When John Burns Research & Consulting (JBREC) asked renters what’s keeping them from buying, the top answer wasn’t mortgage rates or home prices. It was the upfront cost, particularly saving enough for their down payment (see graph below):

That’s where you may be able to make more of a difference than you realize. You can’t control rates or prices. But you may be able to use your equity to help with this upfront expense. And giving money to your loved one so they buy a home doesn’t mean putting your own future at risk.

That’s where you may be able to make more of a difference than you realize. You can’t control rates or prices. But you may be able to use your equity to help with this upfront expense. And giving money to your loved one so they buy a home doesn’t mean putting your own future at risk.

Even a small portion of your equity can put them in a position to finally get the keys to their first place – and, if you’re strategic about it, you’d still have a lot leftover for when you retire.

With an estimated $68 and $84 trillion of wealth expected to transfer from older generations to younger ones over the next two decades, many families are already thinking differently about when and how that wealth will be passed down. Maybe it makes sense for your family to think about too.

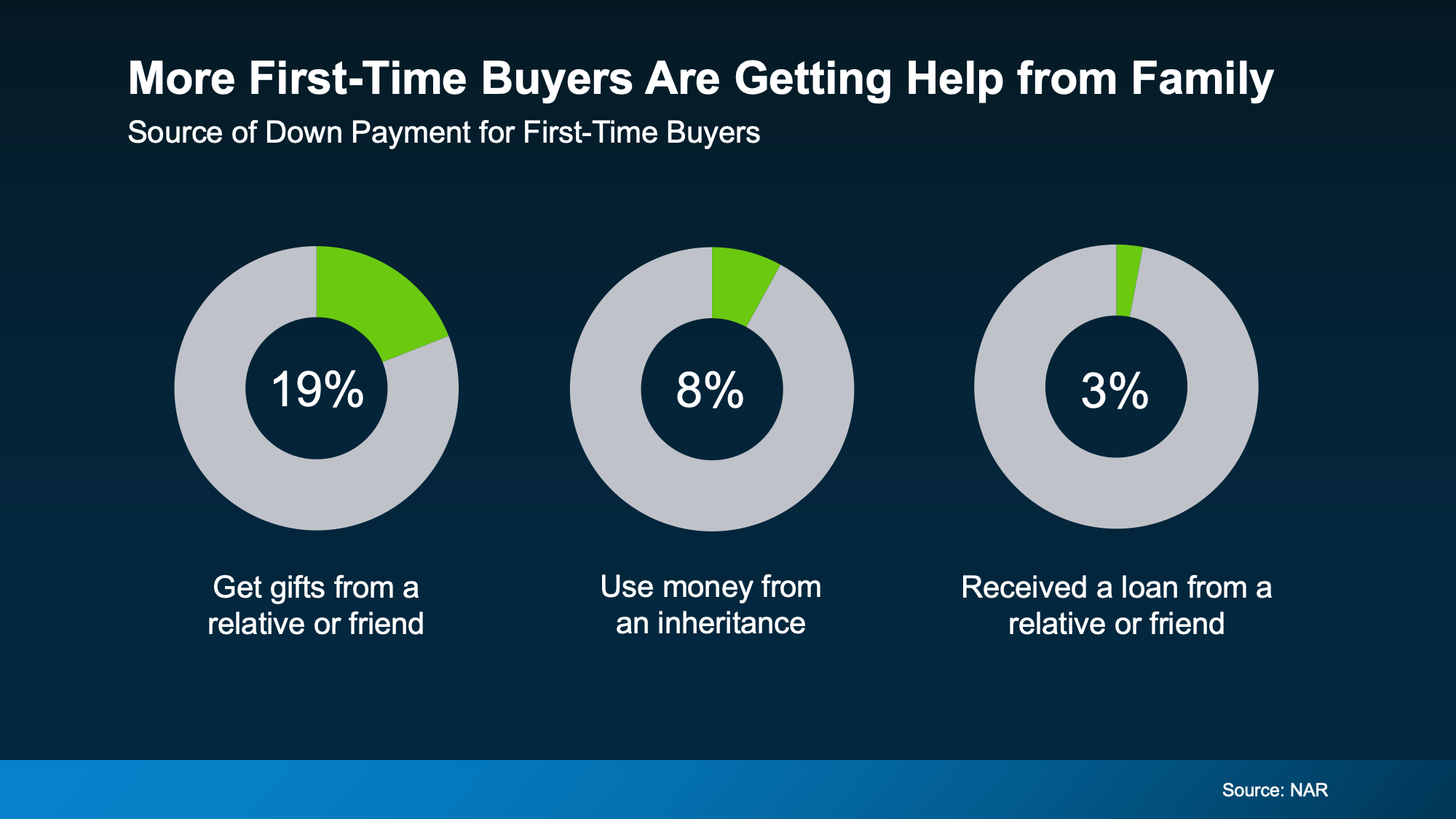

Help from Loved Ones Is Making a Move Possible for Many First-Time Buyers

A growing share of young buyers are using gifts and loans from their loved ones to springboard into homeownership. According to the National Association of Realtors (NAR), nearly 1 in 5 first-time buyers use a cash gift from their family or loved ones for their down payment.

And other young buyers are using their inheritance or a loan from someone they know to finally break into the market (see charts below):

This Is About Opportunity, Not Obligation

This Is About Opportunity, Not Obligation

Every family’s situation is different, and your decision should be made carefully. It’s just that, if you’ve built up a lot of equity, you may have more room to help than you think.

It’s not just a financial gift. It’s giving stability, security, and a foundation that could change their lives for the better – especially at a time when they may not be able to do it on their own.

Bottom Line

If you’re curious what your home equity could make possible, for you or for your loved ones, start with a simple conversation with a local real estate agent. Because sometimes the most meaningful investment you can make is for the next generation.

There’s one decision you’re going to make when you sell that determines whether your house sells quickly, or it sits. Whether buyers make an offer, or scroll past it. Whether you walk away with the maximum return, or you end up cutting the price later.

And that’s your asking price.

The #1 Mistake Sellers Make Today: Trusting the Wrong Number

If you’re thinking of moving and trying to figure out what your house may sell for, it’s tempting to start with an online home value tool. They’re fast, free, and easy. And you don’t have to talk to anyone. But here’s the problem: they don’t know your house.

And that can be a bigger drawback than you realize.

Where Online Estimates Fall Short

Online tools often lag behind the market. They look in the rearview mirror, relying on closed sales and delayed information. And in that sense, they’re using incomplete data.

That’s not a miss in how these systems are built. Some information just isn’t available online. Bankrate explains:

“While these tools can be a useful starting point, keep in mind that they typically do not provide the most accurate pricing. Algorithms can only rely on the information available; they can’t account for things like a home’s condition or renovations made since the last public information was updated.”

They can’t see:

- The unique features that make your house special

- All the work you’ve put in to keep it in good condition

- Or, how in-demand your specific neighborhood is right now

So, while they may do a good job in some cases, they can’t be as accurate as a local agent who has boots on the ground day in and day out.

In a market where buyers have more options, a seemingly small margin of error can cost you thousands if you price too low, or weeks of lost momentum and time if you price too high.

If you want to sell for the most money and in the least amount of time, you don’t want the fast answer on how to price your house. You want the right one.

That’s why the savviest homeowners today don’t rely on algorithms when it actually matters. They rely on people, specifically trusted local agents.

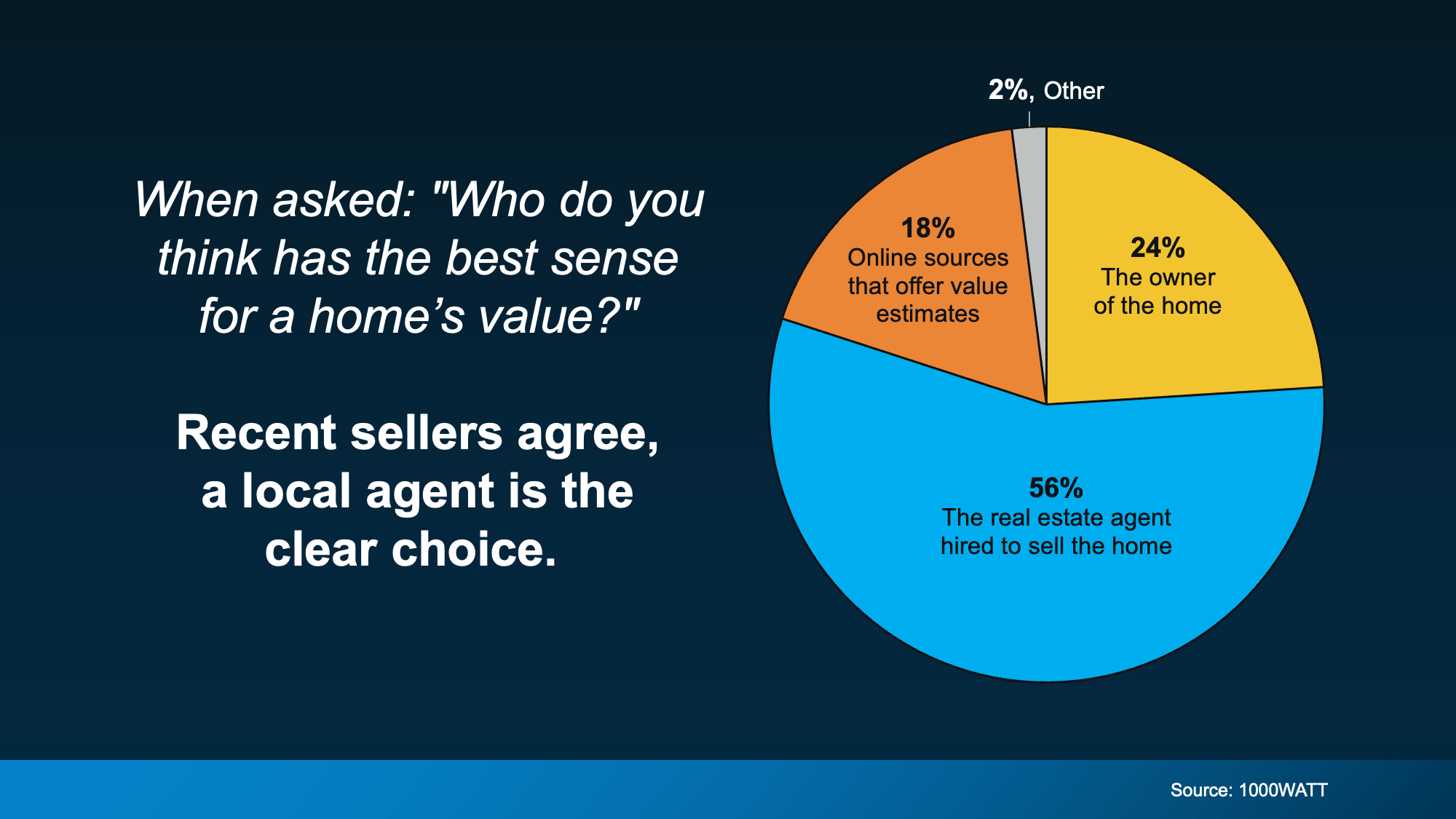

What an Expert Agent Brings to the Table

According to 1000WATT, sellers overwhelmingly believe real estate agents have the best sense of a home’s true value, far more than any automated tools.

That confidence isn’t accidental. As Bankrate puts it:

That confidence isn’t accidental. As Bankrate puts it:

“A professional appraiser or real estate agent can visit the home in person, assess the neighborhood as a whole as well as the individual property, perform more thorough market research, and consider subjective details.”

And those details matter. A skilled local agent doesn’t just pull reports. They know what’s happening right now:

- What buyers are paying this month, not last month, or even last year

- How your home compares to the current competition in your neighborhood

- Which features add value based on what buyers are willing to pay for today

- How to price your house to create urgency in this market

And once an agent steps foot in your house, they may even find your online estimate undershot your value. So, if you stuck with the estimate you got online, you’d actually be leaving money on the table. And no one wants that.

Bottom Line

While online tools can give you a rough starting point, only a local expert can give you a price that actually works.

If you want to know the right number for your house, not just the easiest one to find, connect with a local real estate agent.

Top Mistakes Homeowners Are Making in 2026 (And How To Avoid Them)

Renting vs. Buying: The Numbers Might Surprise You

How Your Equity Could Help Younger Generations Buy a Home

-

Downsize4 weeks ago

Downsize4 weeks agoWhy So Many Homeowners Are Downsizing Right Now

-

Affordability3 weeks ago

Affordability3 weeks agoIt’s Getting More Affordable To Buy a Home

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoHome Insurance Costs Are Rising: What Buyers Should Plan For

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoTop 3 Reasons To Buy a Home Before Spring

-

Affordability3 weeks ago

Affordability3 weeks agoWhy Townhomes Are Popular with Today’s First-Time Buyers

-

Equity2 weeks ago

Equity2 weeks agoFour Ways Your Home Equity Can Work for You

-

For Buyers2 weeks ago

For Buyers2 weeks agoInventory Is Making a Comeback in 2026

-

For Buyers2 weeks ago

For Buyers2 weeks agoMove-Up Buyers Are Choosing New Construction

You must be logged in to post a comment Login