For Buyers

Home Price Appreciation Is as Simple as Supply and Demand

Home price appreciation continues to accelerate. Today, prices are driven by the simple concept of supply and demand. Pricing of any item is determined by how many items are available compared to how many people want to buy that item. As a result, the strong year-over-year home price appreciation is simple to explain. The demand for housing is up while the supply of homes for sale hovers at historic lows.

Let’s use three maps to show how this theory continues to affect the residential real estate market.

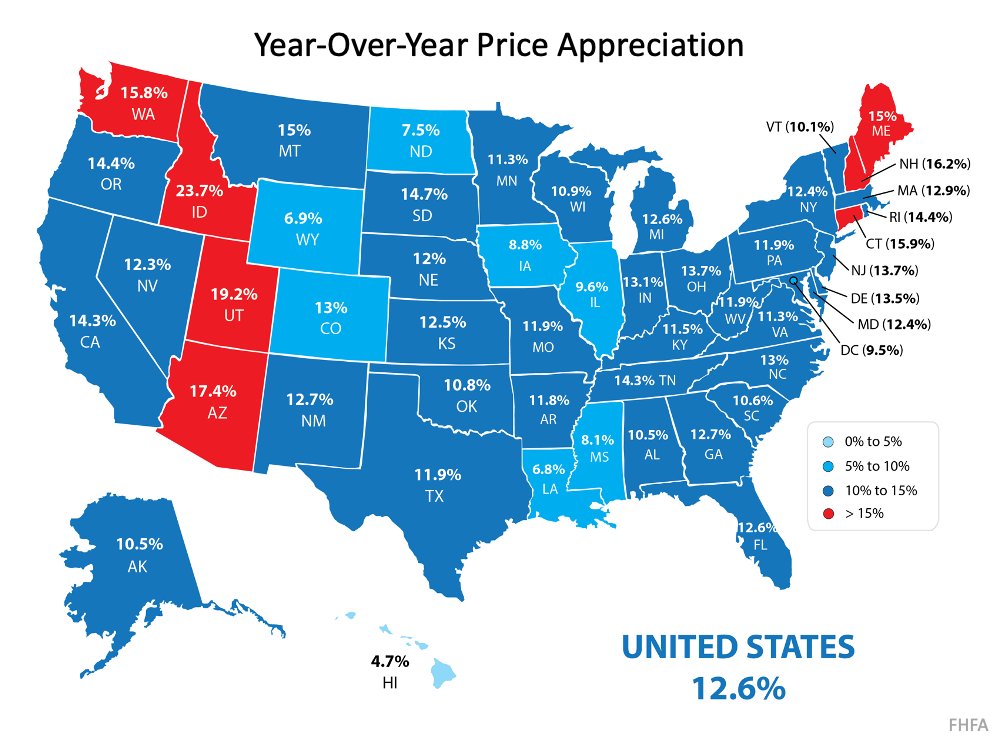

Map #1 – State-by-state price appreciation reported by the Federal Housing Finance Agency (FHFA) for the first quarter of 2021 compared to the first quarter of 2020: As the map shows, certain states (colored in red) have appreciated well above the national average of 12.6%.

As the map shows, certain states (colored in red) have appreciated well above the national average of 12.6%.

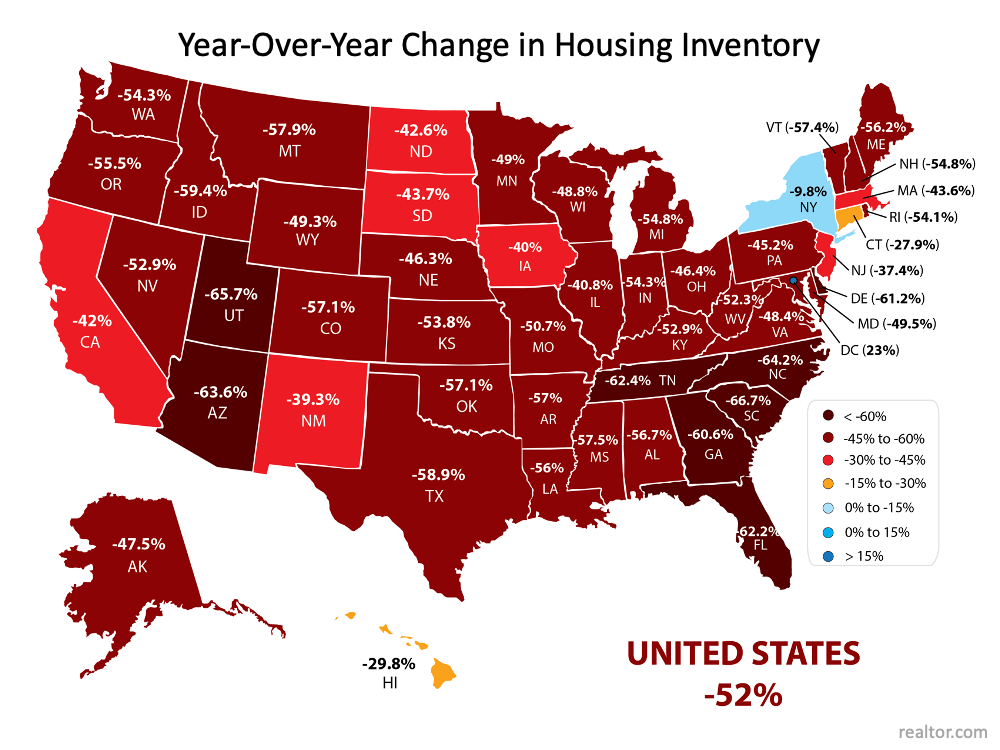

Map #2 – The change in state-by-state inventory levels year-over-year reported by realtor.com: Comparing the two maps shows a correlation between change in listing inventory and price appreciation in many states. The best examples are Idaho, Utah, and Arizona. Though the correlation is not as easy to see in every state, the overall picture is one of causation.

Comparing the two maps shows a correlation between change in listing inventory and price appreciation in many states. The best examples are Idaho, Utah, and Arizona. Though the correlation is not as easy to see in every state, the overall picture is one of causation.

The reason prices continue to accelerate is that housing inventory is still at all-time lows while demand remains high. However, this may be changing.

Is there relief around the corner?

The report by realtor.com also shows the monthly change in inventory for each state.

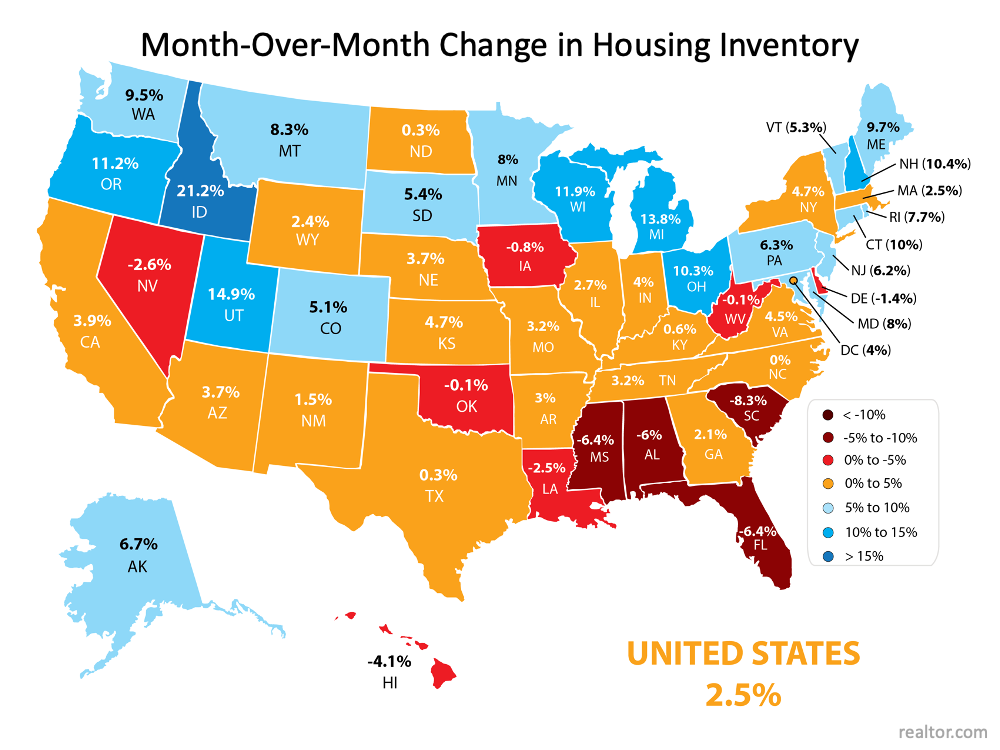

Map #3 – State-by-state changes in inventory levels month-over-month reported by realtor.com: As the map indicates, 39 of the 50 states (plus the District of Columbia) saw increases in inventory over the last month. This may be evidence that homeowners who have been afraid to let buyers in their homes during the pandemic are now putting their houses on the market.

As the map indicates, 39 of the 50 states (plus the District of Columbia) saw increases in inventory over the last month. This may be evidence that homeowners who have been afraid to let buyers in their homes during the pandemic are now putting their houses on the market.

We’ll know for certain as we move through the rest of the year.

Bottom Line

Some are concerned by the rapid price appreciation we’ve experienced over the last year. The maps above show that the increases were warranted based on great demand and limited supply. Going forward, if the number of homes for sale better aligns with demand, price appreciation will moderate to more historical levels.

Spend about 5 minutes online searching for news about the housing market, and odds are you’ll see something pop up about home prices. You may even stumble onto social media influencers saying we’re headed for a crash. Let’s get you the context you need.

The truth is prices are going to vary depending on where you live. But they’re not crashing.

Here’s what you need to know.

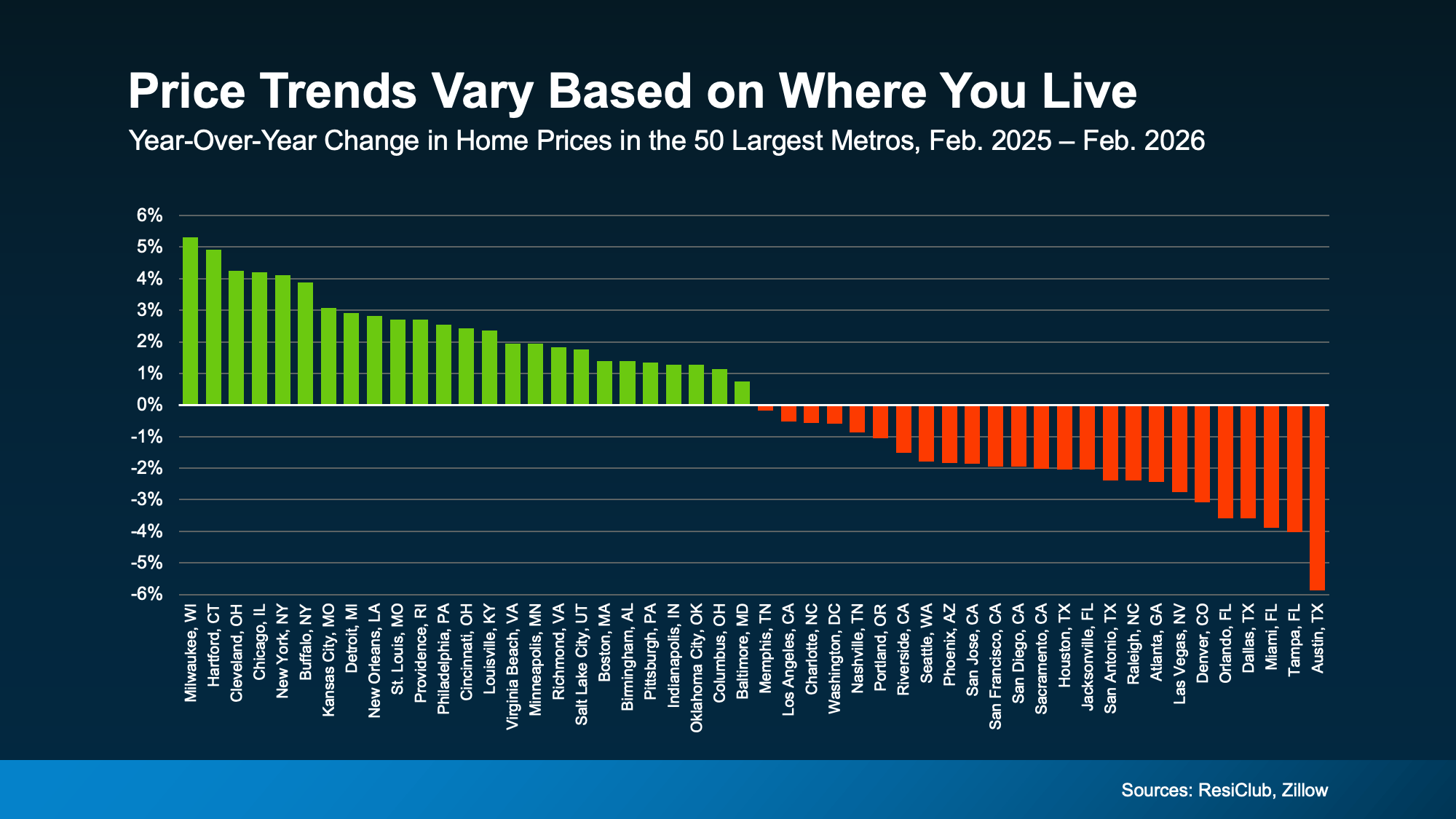

The Local Perspective: Home Price Trends by Area

The biggest thing feeding into the confusion online is how different home price trends are by area right now. Take a look at this data from ResiClub and Zillow (see graph below).

About half of the largest metros are seeing prices go up.

The other half are seeing some declines.

Unfortunately, the online chatter only focuses on the markets where prices are down – and that makes it sound like something bigger is happening.

Unfortunately, the online chatter only focuses on the markets where prices are down – and that makes it sound like something bigger is happening.

But, as you can see in this graph, that’s only one side of the story. The full picture is different.

The National Perspective: Moderate Price Growth

As a country, when you average it all together to get a true baseline, one thing becomes clear, home prices are still net positive at the national level.

According to the Redfin, national home prices were up about 1% year-over-year in February. So, what we’re seeing right now isn’t a collapse. It’s a market that’s normalizing after a period of unusually fast growth. And that impacts some local markets more than others – particularly those where prices rose too far, too fast during the pandemic.

A true crash, like what happened in 2008, would mean prices dropping sharply across the entire country. That’s just not what the data shows today. And it’s not where things are going either.

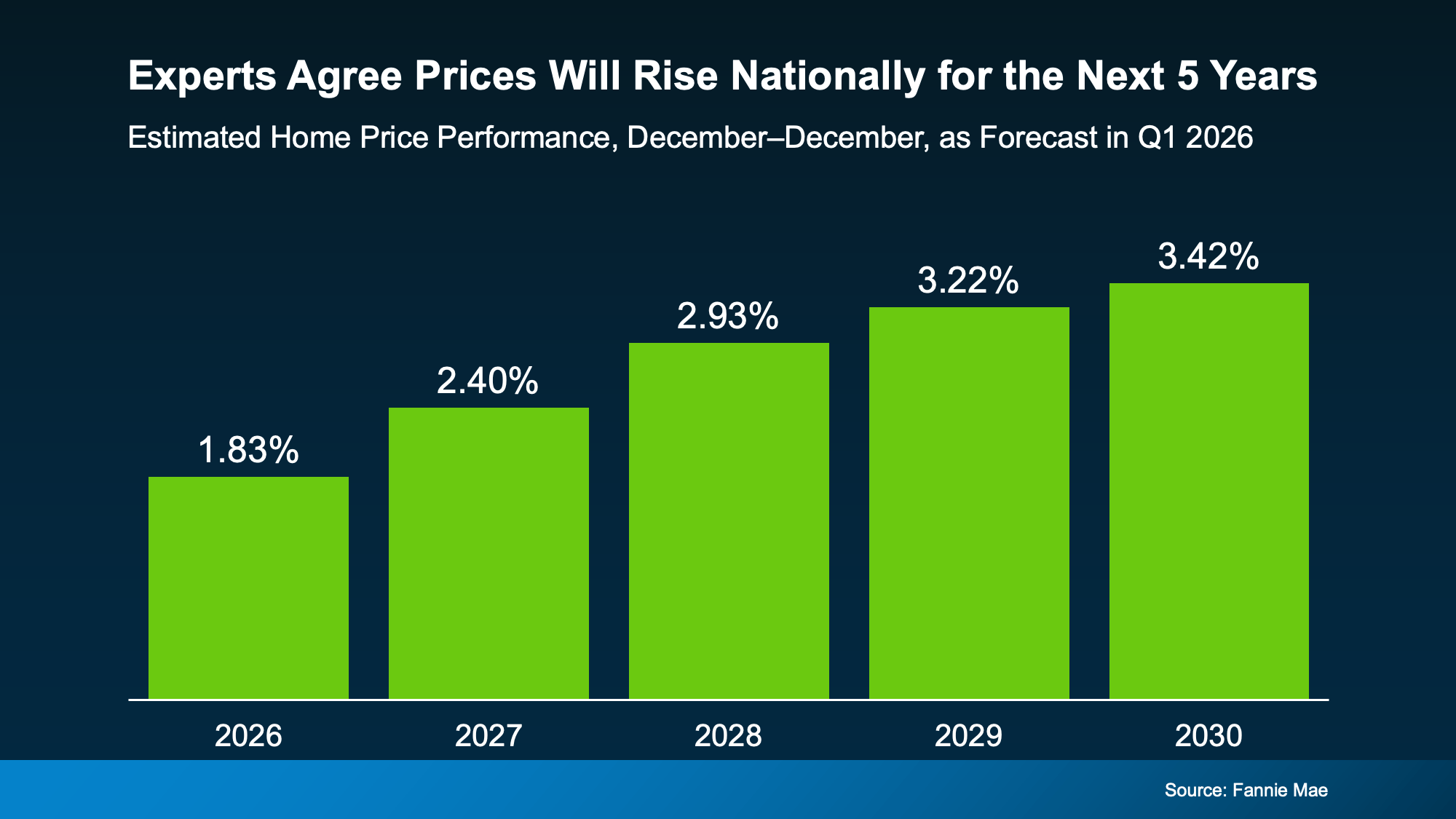

Experts Agree This Isn’t 2008

In fact, Fannie Mae surveyed over 100 housing market experts to ask their opinions on where prices are headed from here. And the experts agree, nationally, prices are expected to keep rising over the next five years:

That rise will be moderate, particularly this year, but the trend is clear. Nationally, prices are forecast to grow every year now through at least 2030 – and that’s normal. Daryl Fairweather, Chief Economist, at Redfin explains:

That rise will be moderate, particularly this year, but the trend is clear. Nationally, prices are forecast to grow every year now through at least 2030 – and that’s normal. Daryl Fairweather, Chief Economist, at Redfin explains:

“House prices aren’t going to fall on a national scale any time soon—and that’s actually a good thing. It’s normal for house prices to rise gradually over time . . .”

That’s why even in the select areas where prices have dropped slightly this year, the decline is expected to be temporary. According to that same quarterly Fannie Mae survey mentioned above, 85% of the experts say the markets that are seeing mild declines right now will return to positive price growth before the end of 2027.

The main takeaway? This isn’t a crash. And prices aren’t expected to fall nationally. If anything, the few areas experiencing declines are expected to rebound in the next year or so.

Bottom Line

It’s easy to get caught up in headlines that make it sound like something big is about to happen. But don’t be fooled. The housing market isn’t crashing. It’s just shifting.

The key is understanding what’s actually happening in your market, so you can make the right move for you. Connect with a real estate agent if you want the local perspective.

There’s a lot of noise out there right now about investors in the housing market.

Some headlines make it sound like big Wall Street firms are buying up everything in sight. And if you’re trying to purchase a home yourself, that can make it feel like the odds are stacked against you.

But when you take a closer look at the data, a very different picture starts to come into focus.

Most Investors Are Just Everyday Owners

For starters, when you hear the word investor, you probably picture big corporations. And that misconception is a large part of what’s feeding into the myth that they’re buying up all the homes.

Most investors aren’t big companies, at all.

They’re everyday people just like you.

They’re someone who owns a second home (like a vacation house at the river), a neighbor who has 1 or 2 rentals, or even a homeowner who tried to sell their home, didn’t get the price they wanted, and decided to rent it instead.

And when all of these groups are lumped together in the headlines, the number of investors sounds high – especially if you’re operating under the assumption all investors are big investors.

But here’s what the numbers really show when you drill down.

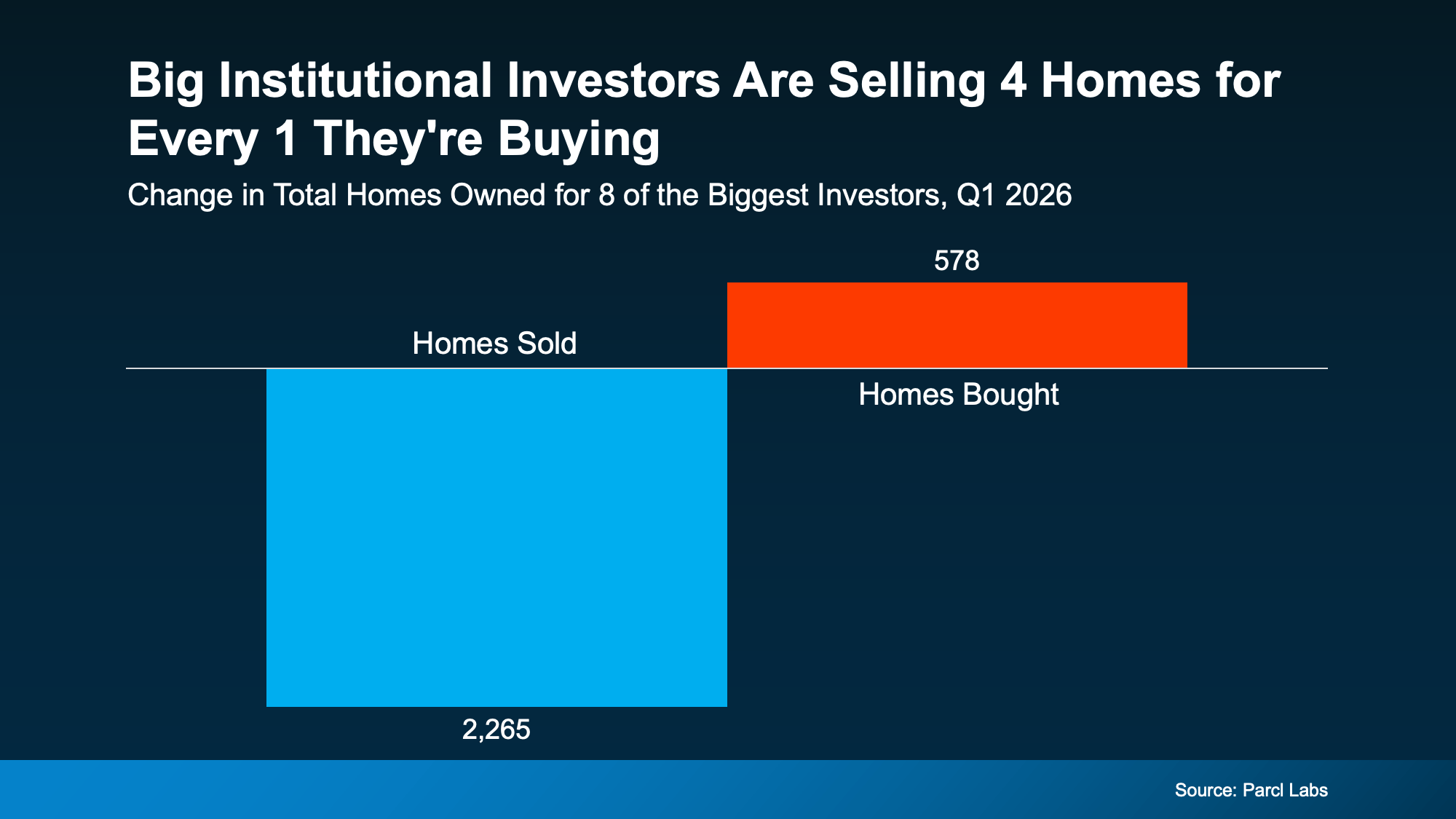

Institutional Investors Are a Small Slice of the Housing Market

Large institutional investors, those big companies buying homes, actually make up a very small share of the overall housing market.

According to BatchData, the largest investors (those with 1,000+ homes) own just 0.4% of the 86 million single-family homes in the country. And their share of the market is actually shrinking.

Data from Parcl Labs shows big investors are selling 4 homes for every 1 they’re buying right now (see visual below):

That means they’ve actually added almost 1.7k homes back into the market lately.

That means they’ve actually added almost 1.7k homes back into the market lately.

What This Means for You

The story is clear. Instead of aggressively buying up homes, most of these companies are stepping back, which means less competition from them than you might expect. If you were someone who thought they were dominating the market, let that give you some peace of mind.

Most of the competition you’ll face is from other everyday buyers – people just like you. And with most large investors stepping back, there may be more opportunity in the market than you think.

Bottom Line

It’s easy to assume big investors are taking over the housing market, but the data tells a different story. If you want an expert’s opinion on what investor activity looks like in our area, talk to a local agent.

Because odds are, it’s not as big a factor as you may think.

Your House Hasn’t Sold Yet. Should You Rent It Out Instead?

Before You Fall in Love with a House, Do This First.

Don’t Let Home Prices Headlines Fool You

-

Agent Value4 weeks ago

Agent Value4 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability4 weeks ago

Affordability4 weeks agoShould You Wait for Lower Rates?

-

For Buyers4 weeks ago

For Buyers4 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

-

Agent Value3 weeks ago

Agent Value3 weeks agoThe #1 Reason Buyers Walk Away (And How To Get Ahead of It)

-

For Buyers7 days ago

For Buyers7 days agoDon’t Let Home Prices Headlines Fool You

-

Affordability3 weeks ago

Affordability3 weeks agoAffordability Has Improved in All 50 States

-

Agent Value3 weeks ago

Agent Value3 weeks ago3 Must-Do’s for First-Time Home Buyers

-

Equity2 weeks ago

Equity2 weeks agoThe Remodel You’ve Been Dreaming About May Be Closer Than You Think

You must be logged in to post a comment Login