For Sellers

If Your House Hasn’t Sold Yet, It May Be Overpriced

When you put your house on the market, you don’t just want it to sell. You want it to sell fast. But the thing is, nationally, it’s taking a little longer to sell lately. And that slowdown can feel frustrating if you want a fast process. Here’s what you need to realize.

In every market right now, there’s one clear exception:

Well-priced, well-presented homes are still selling, and it’s often faster than you’d expect.

If you can tap into that, you can still set yourself up to move quickly, too. Here’s how to get it done.

How Long It Takes To Sell Today

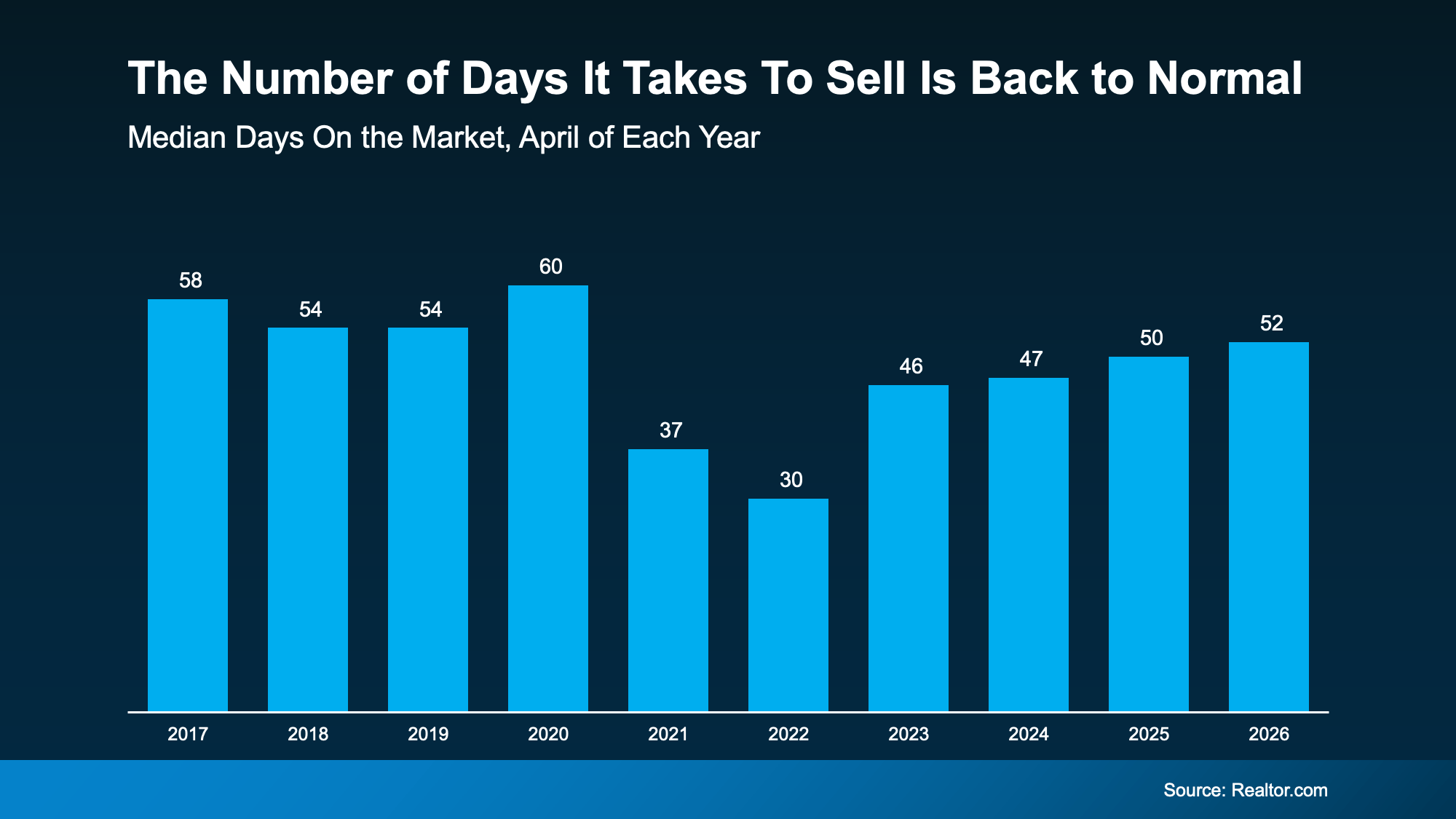

According to Realtor.com, homes are selling in about 52 days right now. That’s how long the process takes from the day it hits the market until closing day.

And while that may sound slow to you, it’s not slow. It’s normal.

That’s because it’s pretty much right in line with what it was during the last normal years in the market (see 2018-2019 in the graph below):

It just feels slow when you’re eager to move – or when you think back a few years to when homes seemed to sell almost instantly.

It just feels slow when you’re eager to move – or when you think back a few years to when homes seemed to sell almost instantly.

But here’s what matters most. The market is normalizing. Not at a standstill.

This is the norm for timing from start to finish. You may have an accepted offer in hand even faster than this.

Markets Where Homes Still Sell Quickly, Even Now

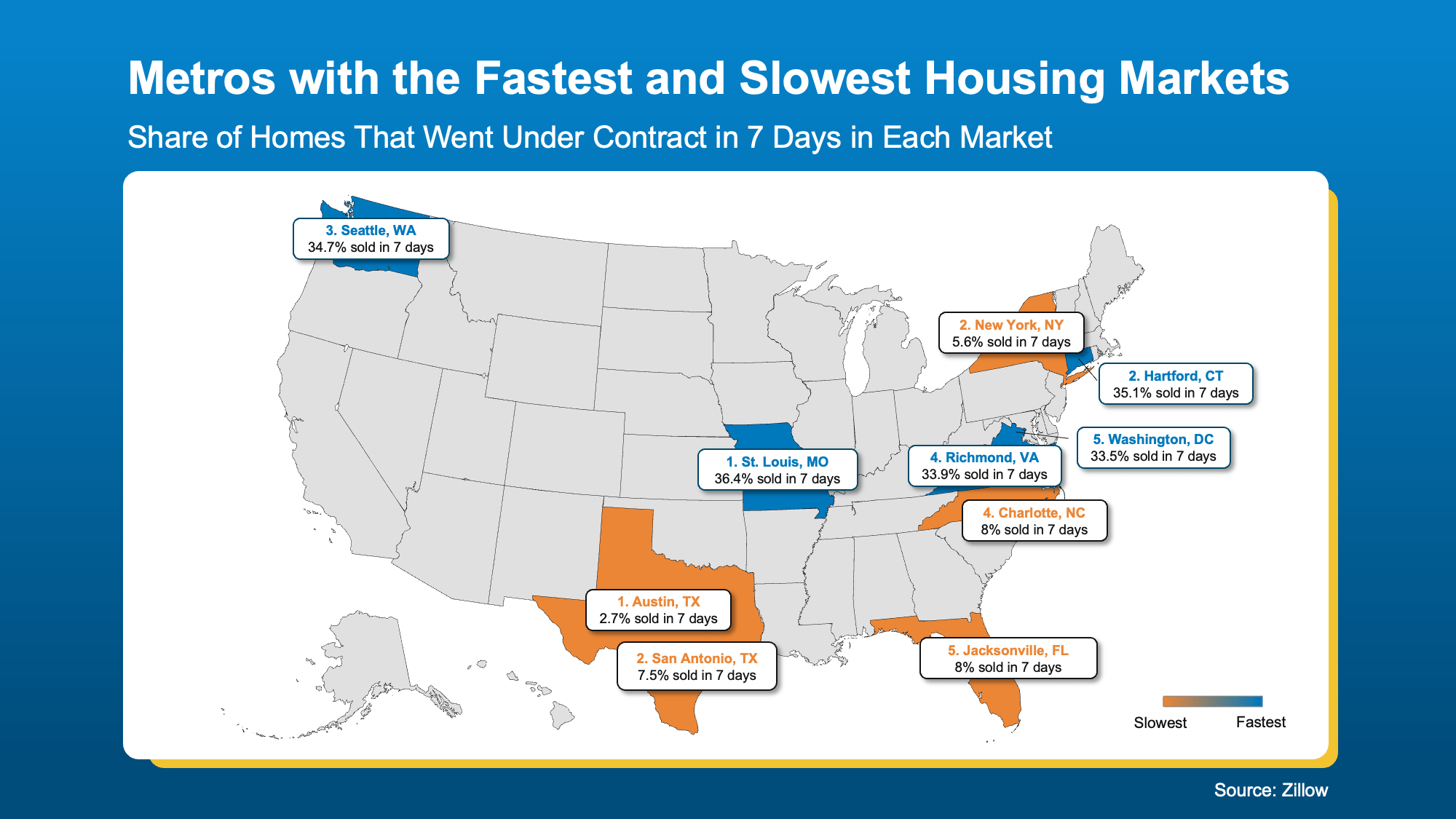

Zillow says the typical home will go “pending” or “under contract” in 19 days. Some homes even see it happen in as little as 7 days. It just depends on where you are – and how you prep your house.

So, don’t let the slowing pace of sales stress you out. Homes can still sell fast, if they’re positioned right.

Just to show you, here’s a quick look at some of the markets that are moving faster than the norm, according to Zillow (see map below). This’ll show you how different it can be based on where you live.

The key things you need to remember when looking at this visual:

The key things you need to remember when looking at this visual:

- It varies a lot based on where you live. Within the same state, individual neighborhoods or pockets may sell much faster than the norm.

- Even in slower moving states, you can still sell quickly. As the map shows, in those places there are still homes that go under contract in as little as a week.

So don’t worry about if your state made either list. As Orphe Divounguy, Senior Economist at Zillow, says:

“The cream of the crop is still selling fast, even in markets that have slowed considerably. . .”

The Big Reasons Some Homes Sit, and Some Sell Fast

And here’s the big secret. While location can definitely play a role, it’s not just about location. It’s about strategy.

Today’s buyers are paying attention to condition. They’re comparing photos, upgrades, layout, location, and price. And they’re choosing homes that feel move-in ready and well worth the value.

The homes that check those boxes? They’re not sitting for long – no matter where they are.

As the Wall Street Journal (WSJ) explains:

“. . . some homes are still flying off the shelves. These houses are often in the Midwest or Northeast, where the lack of new construction keeps a lid on supply. Certain homes in other markets are selling quickly, too, often when a home is move-in ready.”

Because in any market – hot or not – if a home is overpriced, needs too much work, or just doesn’t meet current buyer expectations, it’s not going to sell.

In this market, the sellers who win are the ones who get real about their house. They’re honest about how their home compares to other listings, realistic about price, and they work with an agent who truly understands today’s market and what it takes to sell.

When your agent knows how to price strategically, spotlight the strengths of your home, and move quickly when the market gives clear signals, that’s when the results follow.

Bottom Line

Today’s housing market rewards the right strategy. Because even in a slower area, the homes that are priced realistically and positioned well are still selling – sometimes faster than you may expect.

Connect with a local agent if you’re ready to make yours one of them.

You may have heard April 12-18 was the “best week” to list your house. That’s based on a report from Realtor.com. But now that it’s passed, you may be wondering if you missed your moment.

Here’s the good news – you didn’t.

Because the reality is, there isn’t just one perfect week to sell your house this Spring. There’s a window. And right now, you’re still in it.

Your Window To Sell Is Still Wide Open

Here’s why. Different organizations run studies like this every year. And they don’t always land on the exact same week. That’s okay. It’s because they’re using different research methods and even different definitions of what “best” means.

But the fact that the results vary points to a larger trend. While there may be sweet spots, the entire Spring season gives sellers an opportunity to get some of the best conditions (and best sales prices) of the year.

And it’s definitely not too late to jump in.

Why Listing in Late May Is the Perfect Play

According to Zillow, the best time to list your house this year is the last 2 weeks of May. And that’s approaching fast.

Based on their analysis, this is the ideal time to do it if you want to make top dollar. Because, in this 2-week window, homes sell for more. Sometimes, quite a bit more.

Depending on where you are and the price point in your area, some homeowners may even net tens of thousands of dollars extra in this sweet spot. As Zillow explains:

“Why late spring? Buyer demand typically peaks before Memorial Day. Families want to move during the summer and settle in before the new school year. More buyers shopping at once can spark competition and lift prices.”

And they’re not the only ones saying listing in May could be the key to selling for more. ATTOM Data analyzed almost 52 million home sales over the past 10 years and found sellers in May are achieving some of the highest returns.

That means the ideal window this year is very much still open.

What This Means for You

If your goal is to sell for the strongest possible price, this is where timing and strategy come together. And you want to be sure you’re ready to make the most of it.

So, what should you be doing right now?

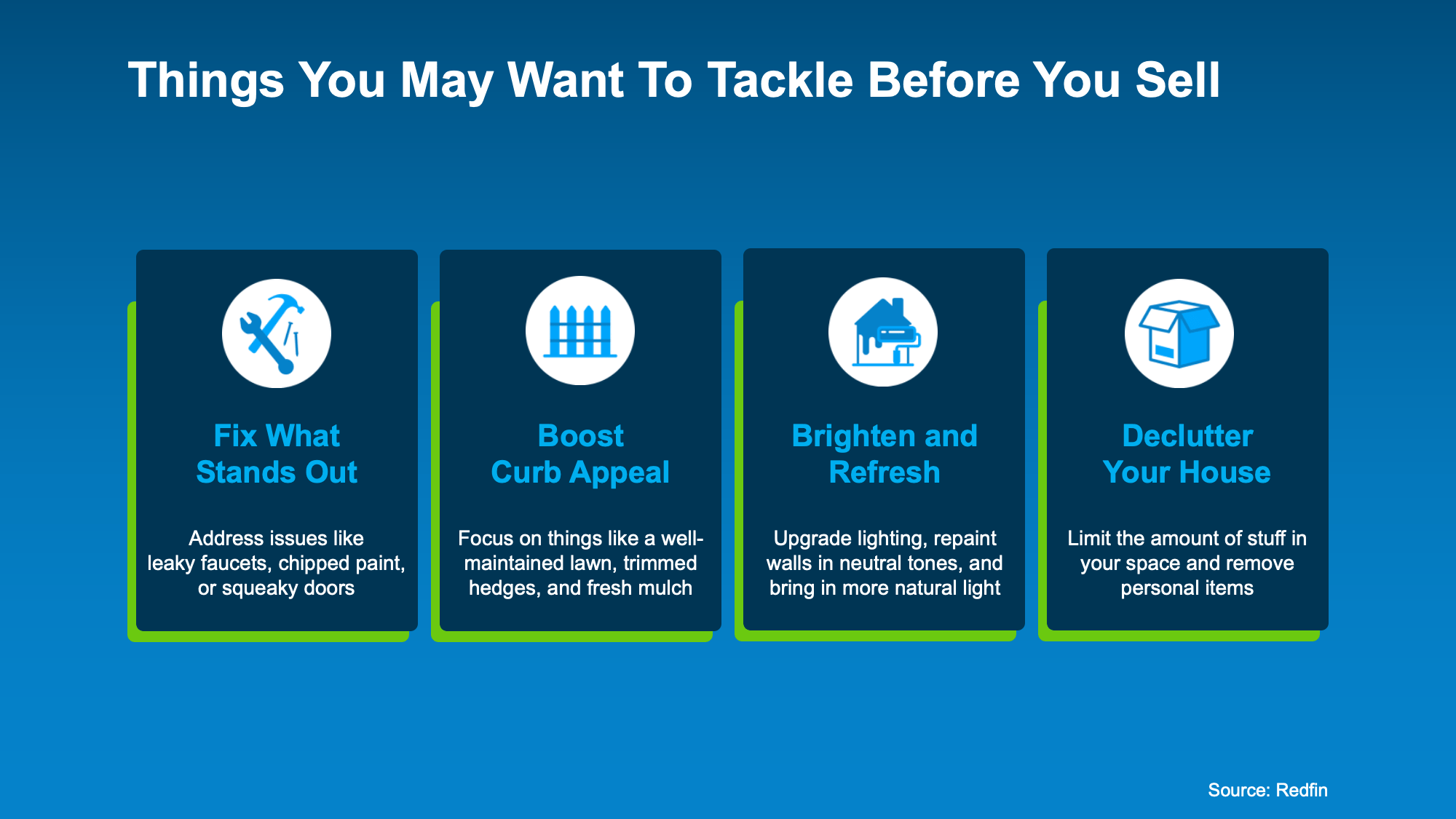

When prepping for a fast-moving window like this, you don’t want to waste time or money on the wrong prep work. And your agent is your go-to to make sure you’re focusing on the right things.

They’ll be able to tell you if the “best week” is slightly different in your market. And what quick repairs or updates can help you get a higher price, without taking a ton of time or effort.

Here’s a quick example of things an agent may recommend based on information from Redfin:

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

Bottom Line

Zillow says the best time to list your house is just around the corner. Are you ready to make the most of it?

If you want to take advantage of this Spring sweet spot and get top dollar for your house, talk to a local agent about what you need to do now to get ready to hit the market.

At some point, as you start thinking about the years ahead, this question tends to come up:

“Could I stay here long-term… or would it make more sense to move?”

It’s not always urgent. It often shows up in small moments, like going up and down the stairs, keeping up with the maintenance, or just thinking about what the next chapter of your life might look like in this home.

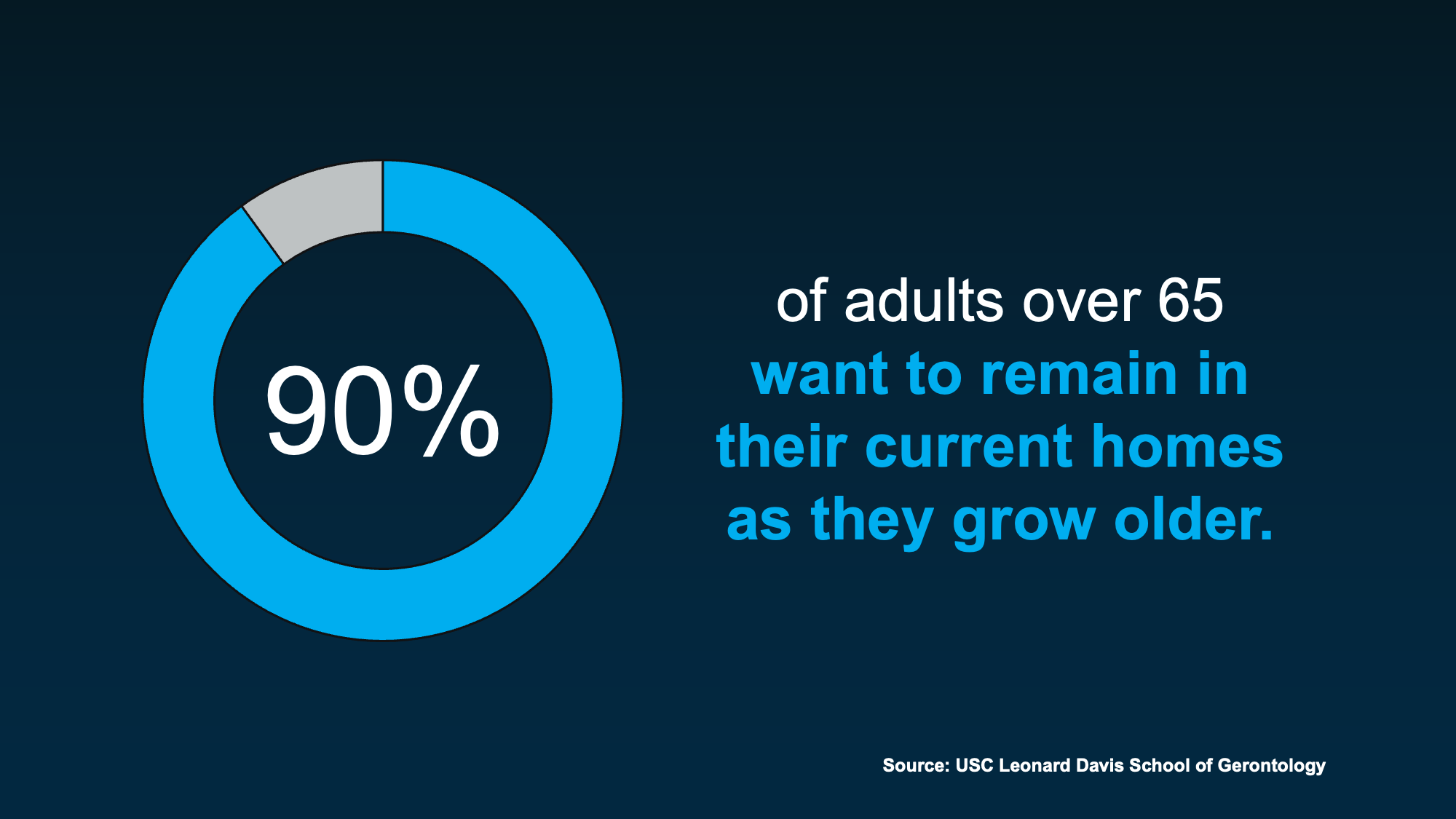

And for most people, the answer is simple. They want to stay.

The USC Leonard Davis School of Gerontology found about 90% of adults over 65 prefer to stay in their homes as they get older (see below):

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

What You Need To Plan for If You’re Staying in Your Home

Aging in place is definitely possible. But it’s better if you have a plan. And here’s why. The home that once worked perfectly may need to change with you over the years. And it’s easier if you can anticipate those expenses.

- Sometimes that means small updates: like adding grab bars in the shower.

- Other times, you’ll have to make bigger decisions: like reworking layouts or moving key spaces to the first floor.

Some of those changes are going to be simple. Others can be a meaningful investment. And that’s why thinking about it early matters. Not because you need to decide anything right now, but because it gives you time.

- Time to understand what your home may need.

- Time to explore your options.

- Time to find the right contractors.

- Time to space out the expense of the upgrades.

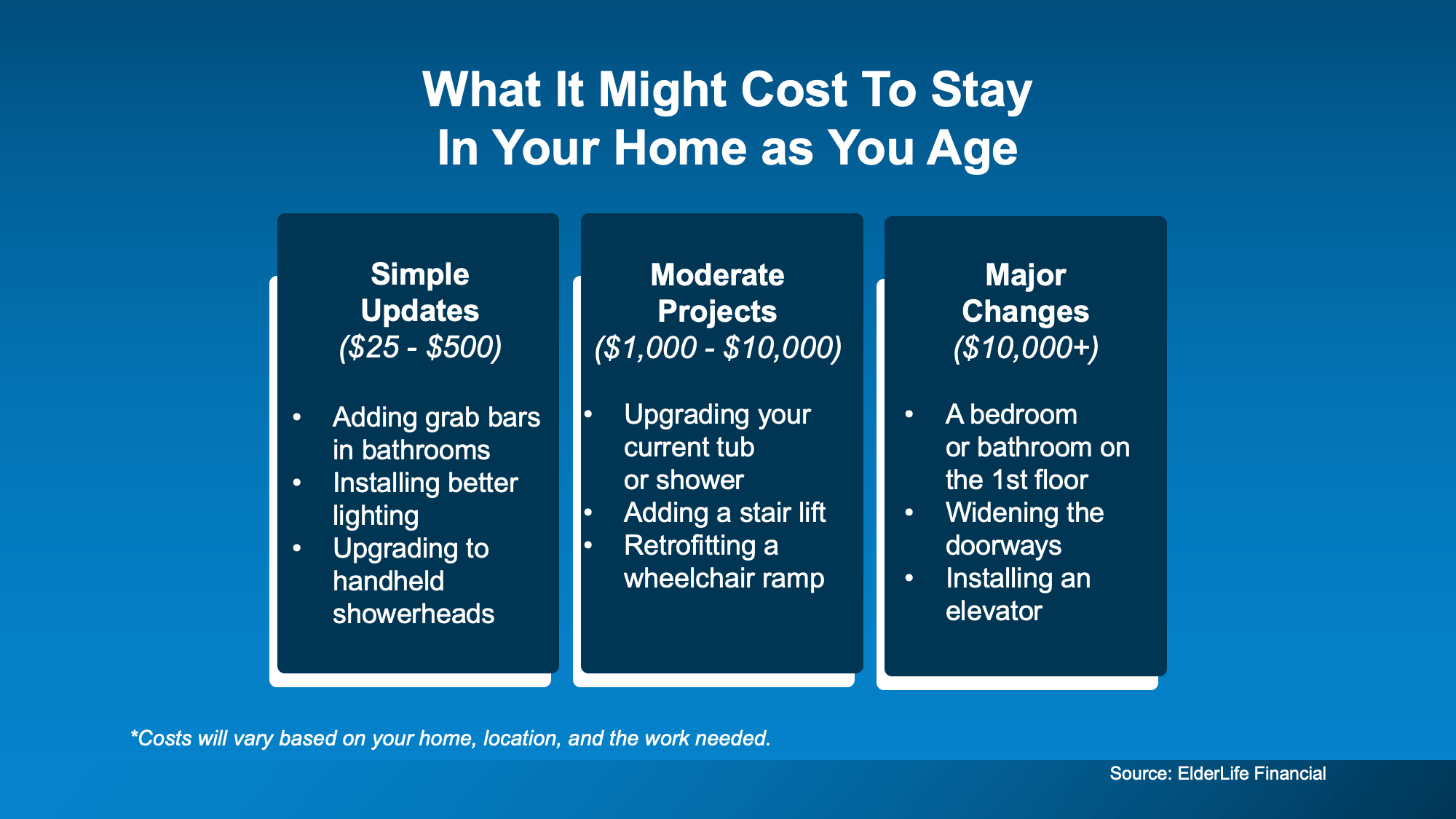

According to ElderLife Financial, here’s a rough baseline of what it could cost depending on what needs to be done (see below):

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

Just remember, if you’re thinking about making updates, it’s always worth having a quick conversation before you start. A real estate agent can help you understand which changes tend to make sense for your situation and how they may impact your home’s value based on your local market.

When Moving Might Make More Sense

But staying isn’t always the best fit for every situation. According to Pegasus Senior Living:

“While most seniors hope to age in place, practical considerations sometimes make selling a home the wiser choice.”

Sometimes, it comes down to a simple shift: when the home that once made life easier, starts to make it harder.

That might look like:

- Maintenance or yardwork that’s starting to feel overwhelming

- Stairs or layouts that are getting harder to manage day-to-day

- Or needing more support or care or being too far from loved ones

And sometimes, it’s not about necessity at all. It’s about lifestyle. Some homeowners just don’t want to live through major renovations. Others are ready to simplify, downsize, or move somewhere that better fits this next chapter, whether that’s a smaller home, a 55+ community, or a place closer to family.

For them, moving simply means making daily life easier.

Bottom Line

There’s no one-size-fits-all answer here.

Some people stay and make updates. Others move to simplify things. Either can be the right choice. The goal isn’t to pick one today. It’s to understand your options early, so when the time comes, you feel confident instead of rushed.

And if you ever want a sounding board to think through what the future could look like for you, a local real estate agent is there to help.

The Secret To Selling Fast, No Matter the Market

4 Ways To Give Your Offer an Edge This Spring

Is Late May the Best Time To List Your House?

-

Affordability4 weeks ago

Affordability4 weeks agoWhen Buying a Home Feels Out of Reach, Some Families Do This Instead

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

-

Agent Value2 days ago

Agent Value2 days agoStay or Sell? How To Make the Right Call as You Age

-

For Buyers2 days ago

For Buyers2 days agoMore Options Are Popping Up This Spring

-

Affordability2 days ago

Affordability2 days agoThink You Have To Put 20% Down? Most First-Time Homebuyers Don’t.

-

Affordability2 days ago

Affordability2 days agoThe 10 Best Markets for First-Time Buyers This Spring

-

Equity2 days ago

Equity2 days agoRent or Buy? The Real Tradeoff Most People Don’t Talk About

-

Featured2 days ago

Featured2 days ago3 Things That Are Not Going To Happen in Today’s Housing Market

You must be logged in to post a comment Login