Rent vs. Buy

The Perks of Buying over Renting

Thinking about buying a home? While today’s mortgage rates might seem a bit intimidating, here are two solid reasons why, if you’re ready and able, it could still be a smart move to get your own place.

1. Home Values Typically Go Up Over Time

There’s been some confusion over the past year or so about which way home prices are headed. Make no mistake, nationally they’re still going up. In fact, over the long-term, home prices almost always go up (see graph below):

Using data from the Federal Reserve (the Fed), you can see the overall trend is home prices have climbed steadily for the past 60 years. There was an exception during the 2008 housing crash when prices didn’t follow the normal pattern, but generally, home values kept rising.

This is a big reason why buying a home can be better than renting. As prices go up and you pay down your mortgage, you build equity. Over time, this growing equity can really increase your net worth. The Urban Institute says:

“Homeownership is critical for wealth building and financial stability.”

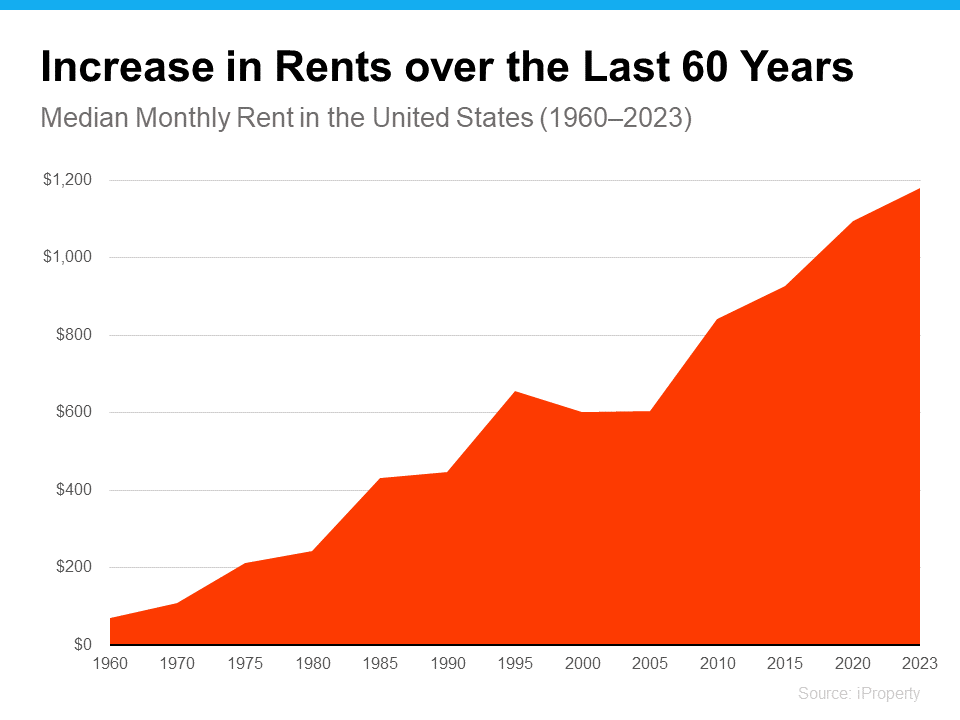

2. Rent Keeps Rising in the Long Run

Here’s another reason you may want to think about buying a home instead of renting – rent just keeps going up over the years. Sure, it might be cheaper to rent right now in some areas, but every time you renew your lease or sign a new one, you’re likely to feel the squeeze of your rent getting higher. According to data from iProperty Management, rent has been going up pretty consistently for the last 60 years, too (see graph below):

So how do you escape the cycle of rising rents? Buying a home with a fixed-rate mortgage helps you stabilize your housing costs and say goodbye to those annoying rent increases. That kind of stability is a big deal.

Your housing payments are like an investment, and you’ve got a decision to make. Do you want to invest in yourself or keep paying your landlord?

When you own your home, you’re investing in your own future. And even when renting is cheaper, that money you pay every month is gone for good.

As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), says:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Bottom Line

If you’re tired of your rent going up and want to explore the many benefits of homeownership, talk to a local real estate agent to explore your options.

You’ve probably asked yourself lately: Is it even worth trying to buy a home right now? It’s a question a lot of people are asking.

With today’s home prices and mortgage rates, renting can feel like the easier path. In some cases, it might even seem like the only realistic option right now. And if that’s where you are, there’s nothing wrong with that.

But if you’re weighing the decision, there’s one part of the conversation that doesn’t get talked about enough.

It’s what each choice does for your future.

What Renting Really Gets You (And What It Doesn’t)

Depending on your situation, renting does have some advantages:

- Lower upfront costs.

- Less responsibility.

- More flexibility to move when you want.

But even with those benefits, a Bank of America survey found 70% of aspiring homeowners worry about what long-term renting means for their future. And that concern comes down to one thing: you’re not building anything for your future. As Yahoo Finance explains:

“Paying rent doesn’t build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

So, while renting may feel easier, the flexibility you get comes at a cost.

How Homeownership Builds Your Wealth Over Time

On the other hand, owning a home is one of the most consistent ways people build wealth over time. Why? When you’re a homeowner, you gain something called equity. That’s the difference between what your home is worth and what you owe.

That equity grows with every monthly payment you make. It also gets a boost as home values go up through the years – and it adds up quicker than you may think.

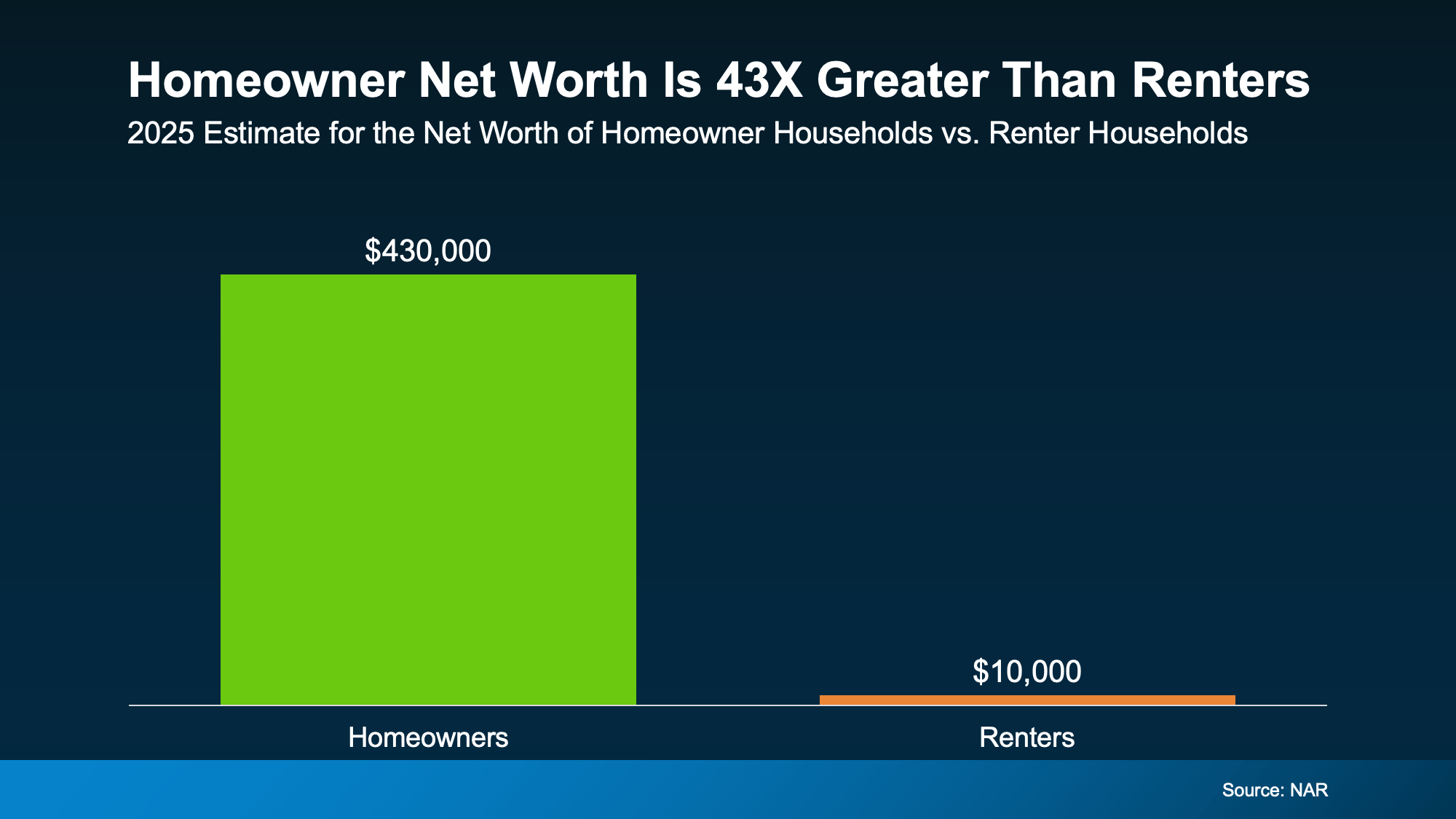

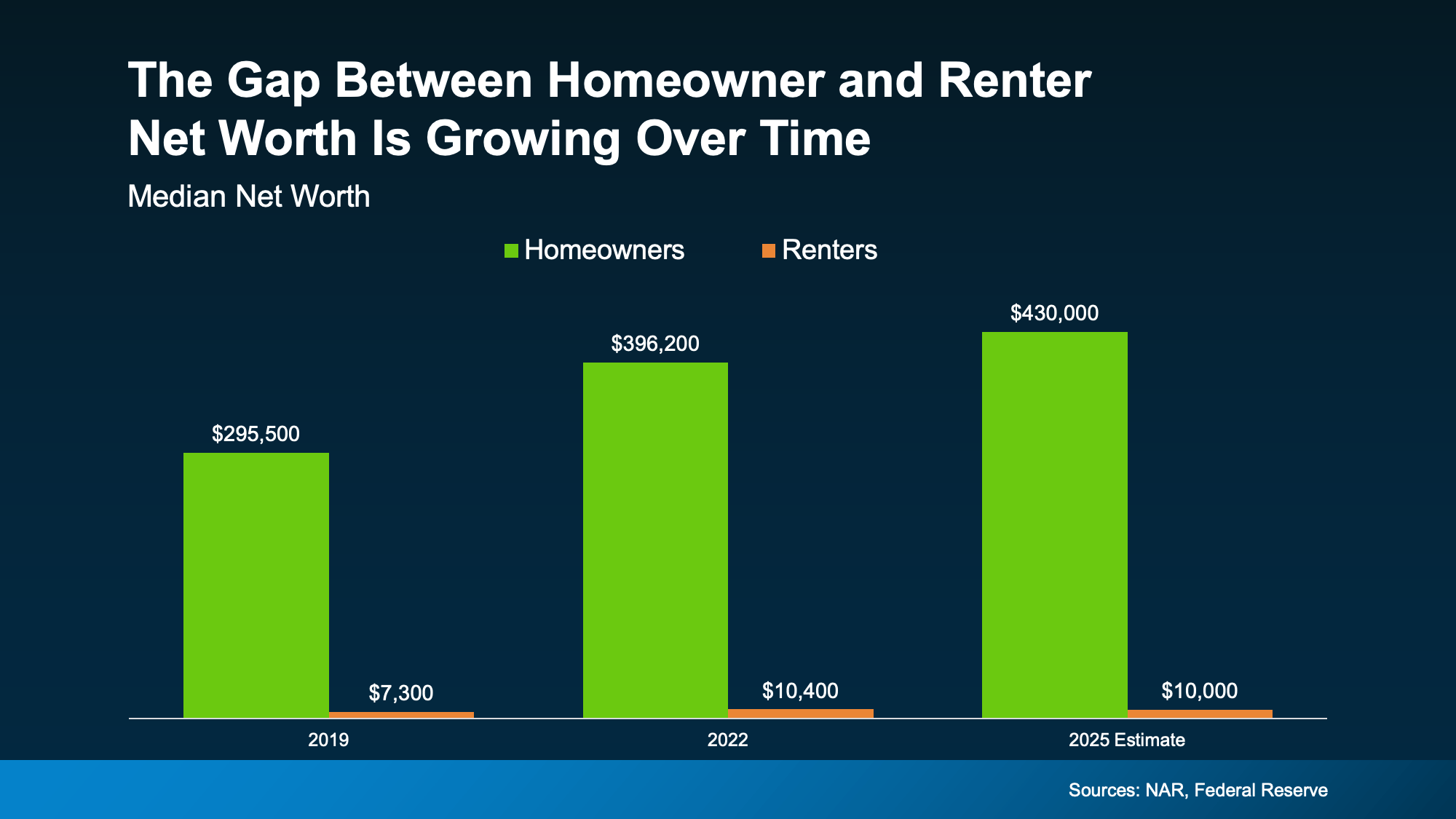

Today, the National Association of Realtors (NAR) says the average homeowner’s net worth is 43X greater than that of a renter:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

- Homeowners: $430k

- Renters: $10k

And it’s not because homeowners make wildly different decisions day to day. It’s because over time, one path builds something, and the other doesn’t.

So sure, buying comes with some upfront costs and more responsibility. But it’s basically a savings account you can live in.

The Gap Is Growing Over Time

And here’s something else interesting. That net worth gap between renters and homeowners has been widening over time, not shrinking.

If you look back at the reports on net worth through the years, you can see the gap is growing as homeowners gain wealth and renters stay stuck in the rental trap (see graph below):

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

When you can afford it and you’re ready for the responsibility, history shows buying is usually worth it in the long run. Because either way, you’re paying for someone’s mortgage and building someone’s net worth.

When you rent, it’s your landlord’s mortgage – not yours. But when you buy? Your monthly payments help build equity.

The question is: whose do you want to pay? Yours or theirs?

So, Should You Buy a Home Now?

The short answer is, it depends on your situation.

While the long-term benefits of buying are clear, that doesn’t mean the timing is right for everyone right now. And that’s okay. You should only buy a home once you’re ready and the numbers work for you.

But whether you’re looking to buy now or planning for the future, the first step is the same. You should have a quick conversation with a local real estate agent about your goals, timeline, and budget.

They can help you run the numbers and see what’s realistic. You may find buying is closer than you thought. And if not, you’ll at least know exactly what it will take to get there.

Because the sooner you have a plan, the sooner you can decide when it makes sense, instead of wondering if it ever will.

Bottom Line

Renting may feel more do-able today. But over time, it could cost you.

If you want to ditch renting and start building something for your future, it starts with a simple conversation. Connect with a real estate agent to talk about your specific goals, and explore your options – so you’re ready when the time is right for you.

Renting can feel like the easier choice right now. There’s no big down payment. No dealing with surprise repairs. And no long-term commitment.

But then your rent goes up again. And again. And suddenly the thing that seemed flexible starts looking… expensive, especially considering you’re not building any equity. And once that happens, it’s easy to feel a little trapped in the cycle.

That’s because there’s so much chatter today about how buying a home isn’t affordable. But the truth is, the math may work out better than you’d expect based on what’s changed recently.

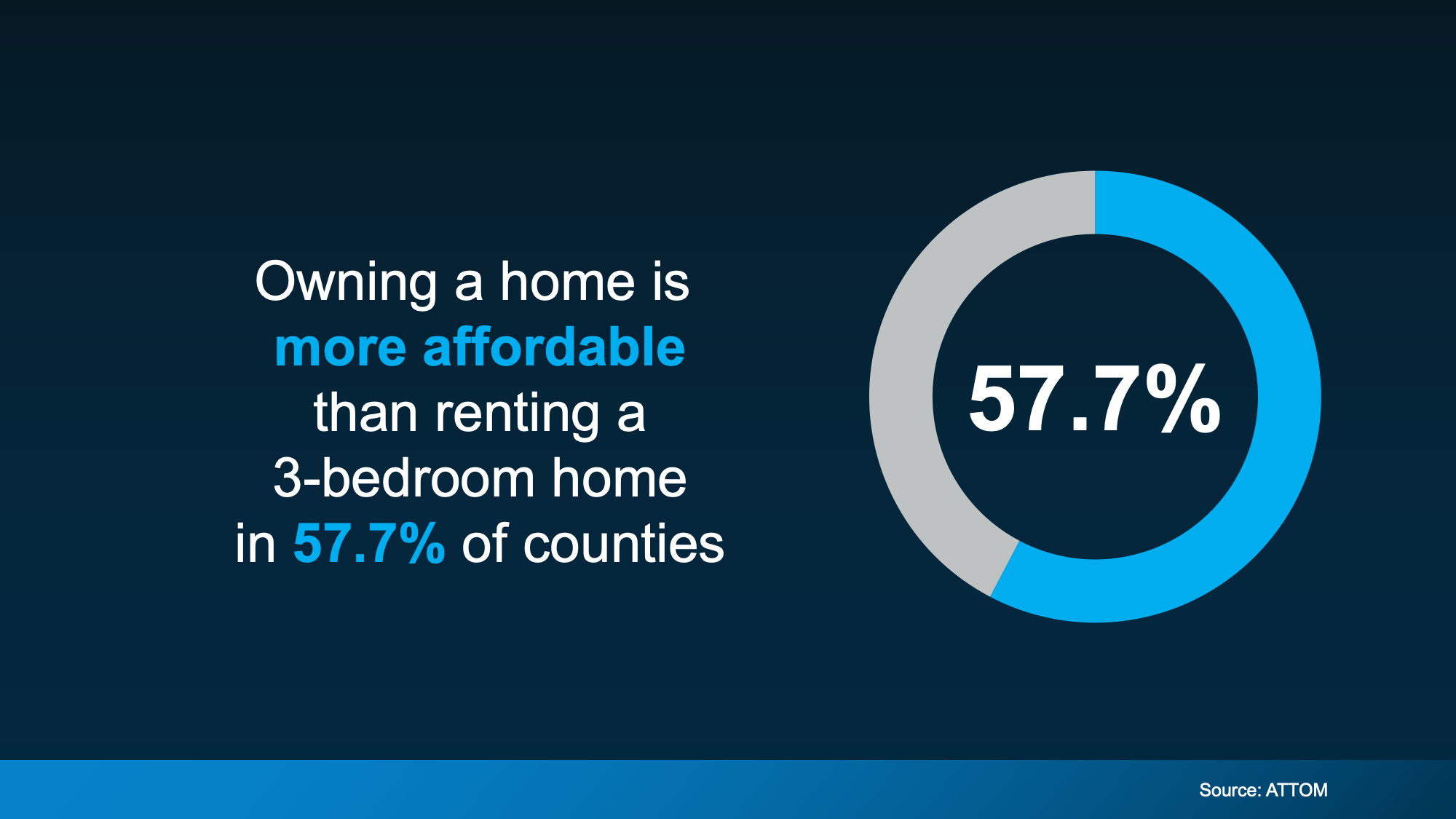

Buying Is More Affordable Than Renting in Many Areas

In a lot of places today, owning a home actually costs less each month than renting a 3-bedroom home. And recent data from ATTOM shows that’s true in nearly 58% of counties across the U.S. (see chart below).

And that’s after you factor in things like insurance and typical maintenance costs.

In other words, even though it may feel like a bit of a shock, the numbers show rent often stretches monthly budgets more than owning does. That’s thanks to slower home price growth, more homes for sale, and monthly mortgage payments starting to ease as rates come down.

In other words, even though it may feel like a bit of a shock, the numbers show rent often stretches monthly budgets more than owning does. That’s thanks to slower home price growth, more homes for sale, and monthly mortgage payments starting to ease as rates come down.

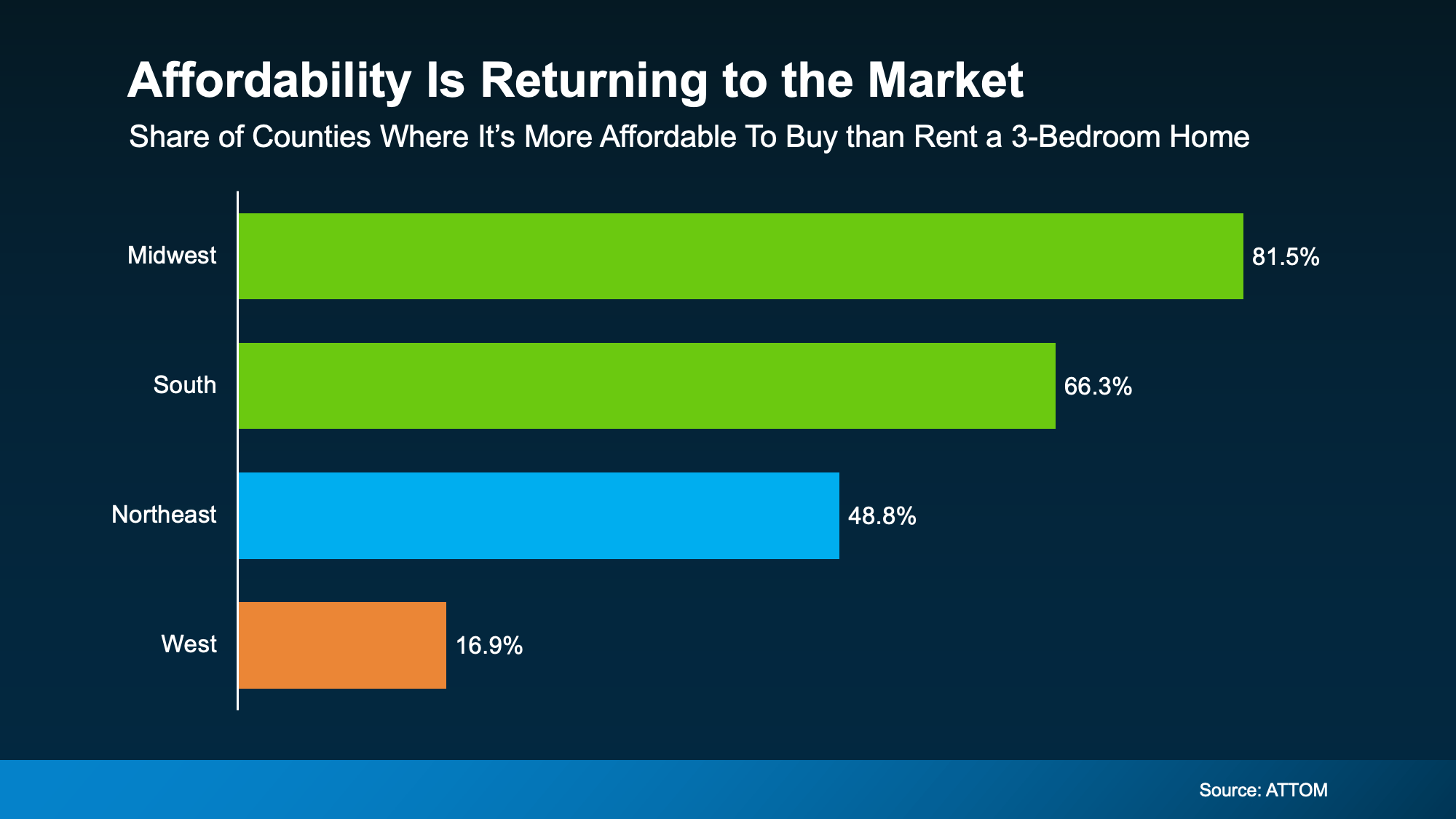

Affordability Still Varies by Region

Now, even though nationally the balance has shifted, that doesn’t mean buying is more affordable in every market or for every renter.

While buying is more affordable than renting in nearly 58% of counties nationwide, that share looks different depending on your region (see graph below):

The biggest improvement is happening in the Midwest and South. But if you’re living in the West, things could still feel tight.

The takeaway? How affordable buying is really depends on where you live. And the only way to know how this plays out where you live is to look at the numbers locally.

So, What’s Still Holding Buyers Back?

Maybe you’re nodding along so far but thinking, “Okay, but I still can’t afford the upfront costs.” If that’s your reaction, you’re not the only one.

For many renters, the biggest hurdle isn’t the monthly payment alone. It’s the down payment, too.

But you’re not out of options. Here’s the part most people don’t hear enough about: there are thousands of down payment assistance programs available across the country, and many buyers qualify without realizing it.

And the average benefit? Roughly $18,000.

That kind of support can help cover part of your down payment or closing costs, which means you may not need to save nearly as much as you think to get started.

When you combine that with monthly payments that may work better than expected, especially as rates continue to ease and prices cool, buying may feel far more realistic than it looks at first glance.

Bottom Line

The point isn’t that everyone should rush out and buy a home tomorrow.

It’s that renting isn’t always the more affordable option people assume it is – and buying may be more realistic than it feels once you look at the full picture.

If you’re renting and feeling stuck in the “someday” loop, it might be worth a simple conversation with a local real estate agent or lender. Just a chance to see what’s possible and whether it makes sense for you.

Would-be homebuyers aren’t sitting on the sidelines because they don’t want to buy. They’re sitting out because they think they can’t. And sometimes, it’s their credit score that’s holding them back.

According to a Bankrate survey, 2 out of every 5 (42%) Americans believe you need excellent credit to qualify for a mortgage. That may be why, when renters are asked why they don’t own yet, “my credit isn’t good enough” comes up often.

Maybe you’re in the same boat. You look at your score, see it’s not where you want it to be, and assume buying your first place just isn’t realistic right now.

But here’s what you need to know.

Even though a lot of people assume you need flawless credit to buy a house, that’s not necessarily the case.

You Don’t Need Perfect Credit To Buy a Home

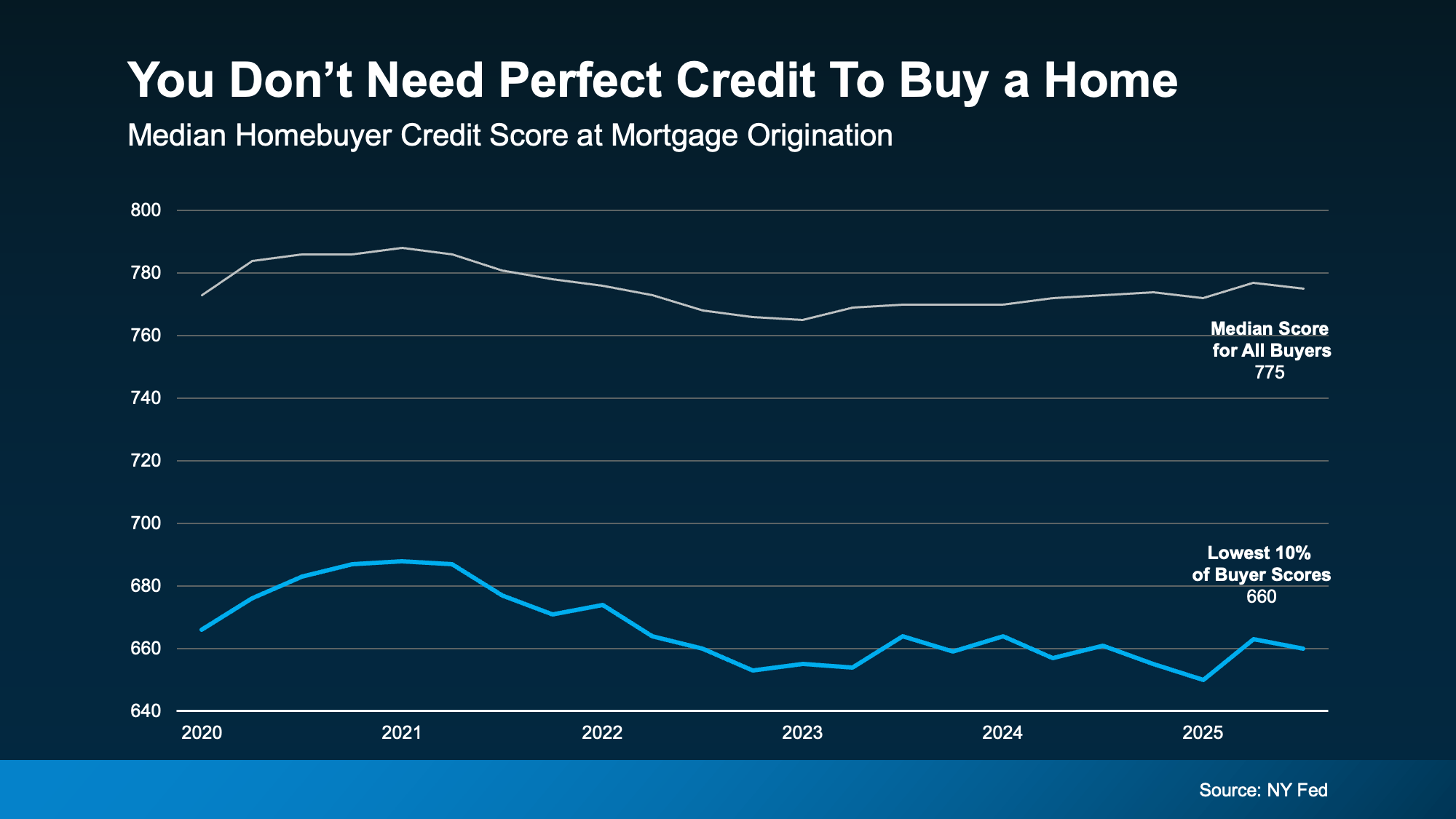

So, where’s this myth come from? Part of the confusion stems from the fact that the typical homebuyer today does have a fairly strong credit score. In fact, according to data from the NY Fed, the median credit score for all buyers is 775.

But that doesn’t mean you need a score that high to qualify.

Looking at recent homebuyers, a number were able to get a mortgage with scores below that threshold. Data shows 10% of scores were around 660. Which means some were higher than that and some were lower, but the median in that lowest 10th percentile was around that range (see graph below):

So, even if your score isn’t as high as you want, that doesn’t automatically close the door. FICO explains there is no universal credit score you absolutely have to have when buying a home:

So, even if your score isn’t as high as you want, that doesn’t automatically close the door. FICO explains there is no universal credit score you absolutely have to have when buying a home:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

The best thing to do is to talk to a trusted lender to see what’s possible for you. Because a portion of buyers are buying with scores in the 600s – and maybe that means you can too.

Bottom Line

Your credit score is important. But that doesn’t mean it has to be perfect.

If credit has been the reason you’ve been waiting to buy a home, it might be time to take another look at your options. If you want help understanding where you stand and what your next step could be, connect with a local lender.

You don’t need to have everything figured out to start the conversation.

The Pricing Mistake That Could Cost You Your Sale

What the Foreclosure Headlines Aren’t Telling You

Why Staging Your House Could Pay Off This Spring

-

Affordability2 weeks ago

Affordability2 weeks agoCould Co-Buying Be the Answer for Some First-Time Buyers?

-

Featured2 weeks ago

Featured2 weeks ago3 Things That Are Not Going To Happen in Today’s Housing Market

-

For Buyers2 weeks ago

For Buyers2 weeks agoMore Options Are Popping Up This Spring

-

Equity2 weeks ago

Equity2 weeks agoRent or Buy? The Real Tradeoff Most People Don’t Talk About

-

Agent Value2 weeks ago

Agent Value2 weeks agoStay or Sell? How To Make the Right Call as You Age

-

Affordability2 weeks ago

Affordability2 weeks agoThink You Have To Put 20% Down? Most First-Time Homebuyers Don’t.

-

For Sellers2 weeks ago

For Sellers2 weeks agoIs Late May the Best Time To List Your House?

-

Affordability2 weeks ago

Affordability2 weeks agoThe 10 Best Markets for First-Time Buyers This Spring

You must be logged in to post a comment Login