For Buyers

Homebuilders Aren’t Overbuilding, They’re Catching Up

You may have heard that there are more brand-new homes available right now than the norm. Today, about one in three homes on the market are newly built. And if you’re wondering what that means for the housing market and for your own move, here’s what you need to know.

Why This Isn’t Like 2008

People remember what happened to the housing market back in 2008. And one of the factors that contributed to that crash was that there were too many homes for sale. While only part of the oversupply back then came from builders, the lasting impact is that some people still feel uneasy when they hear new home construction has ramped up.

Even though the supply of new homes has grown this year, the data shows there’s no need to worry. Builders aren’t overbuilding, they’re just catching up.

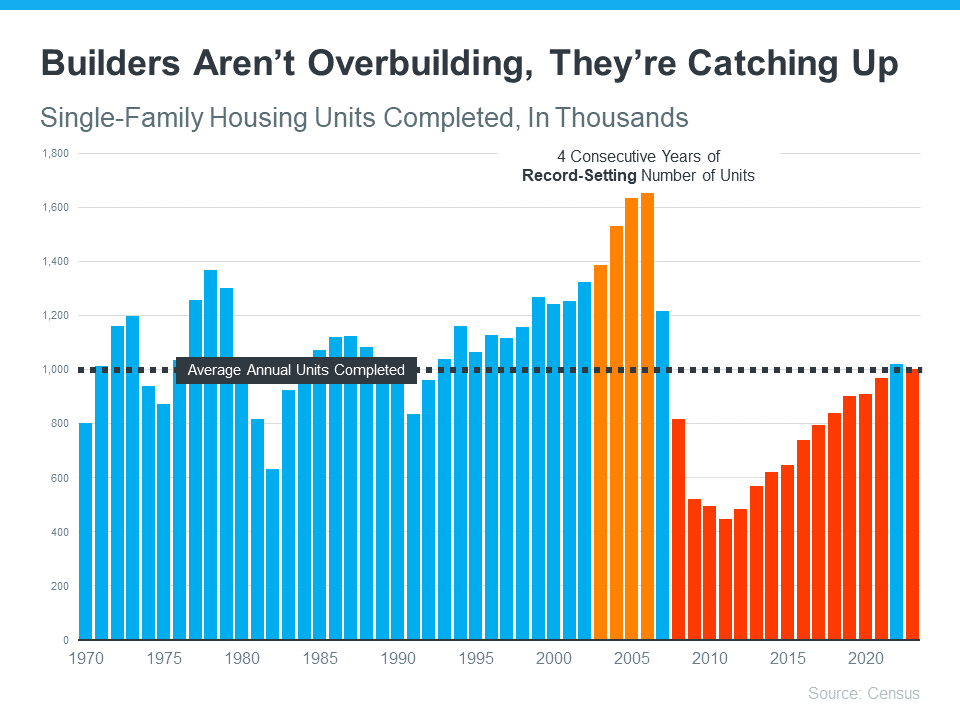

The graph below uses data from the Census to show the number of new houses built over the last 52 years. Following the crash in 2008, there was a long period of underbuilding (shown in red). And it wasn’t until recently that we finally met the long-term average for how many homes are built in a typical year.

This shows, that even with the increase in new builds we’ve seen lately, there won’t suddenly be an oversupply of homes for sale. There’s too much of a gap to make up after over a decade of underbuilding. And if you’re still worried builders are overdoing it, here’s something else that should be reassuring.

New Home Construction May Be at Its Peak for the Year

The latest data from the Census on housing starts (homes where builders just broke ground) and permits (homes where builders can start development soon) shows builders are slowing down their pace right now. Why is that?

They’re responding to still high mortgage rates and how those are impacting buyer demand. Basically, they’re pulling back appropriately in response to what’s happening in the market. As an article from HousingWire explains:

“Even with a massive housing shortage across the nation, homebuilders are completing their pipelines and not seeking as many permits to construct new single-family houses.”

Builders remember what happened when they overbuilt in the crash, and they’re looking to avoid a repeat of that. So, they’re being mindful and pulling back a bit.

You May Have More Options Now Versus Later

If you’re considering a newly built home, here’s how this impacts you. With builders seeking fewer permits and not breaking ground on as many new homes, we may be at the peak of new home construction for the year. This doesn’t mean new home construction is screeching to a stop – just that the pace is slowing down now, and that’ll impact what comes to market later this year. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Given the recent declines in housing starts, home completions will steadily show declines in about six months.”

So, if you’re ready and able to buy now, you may find you’ll have more newly built options to choose from now versus later on. This may be enough reason to kick off your search.

Just be sure to work with a local real estate agent you know and trust throughout the process. An agent will have valuable insight into builder reputations and other key factors specific to your market. And if there isn’t much new construction near you, they’ll be able to point you toward a nearby area where there is.

Bottom Line

While it’s true new home construction is a bigger segment of the market than the norm, that’s not a bad thing. Builders aren’t overbuilding, and they’re responding to market signals to avoid repeating the mistakes that were made in 2008.

If you want to buy now while new home options may be at their peak, reach out to a local real estate agent.

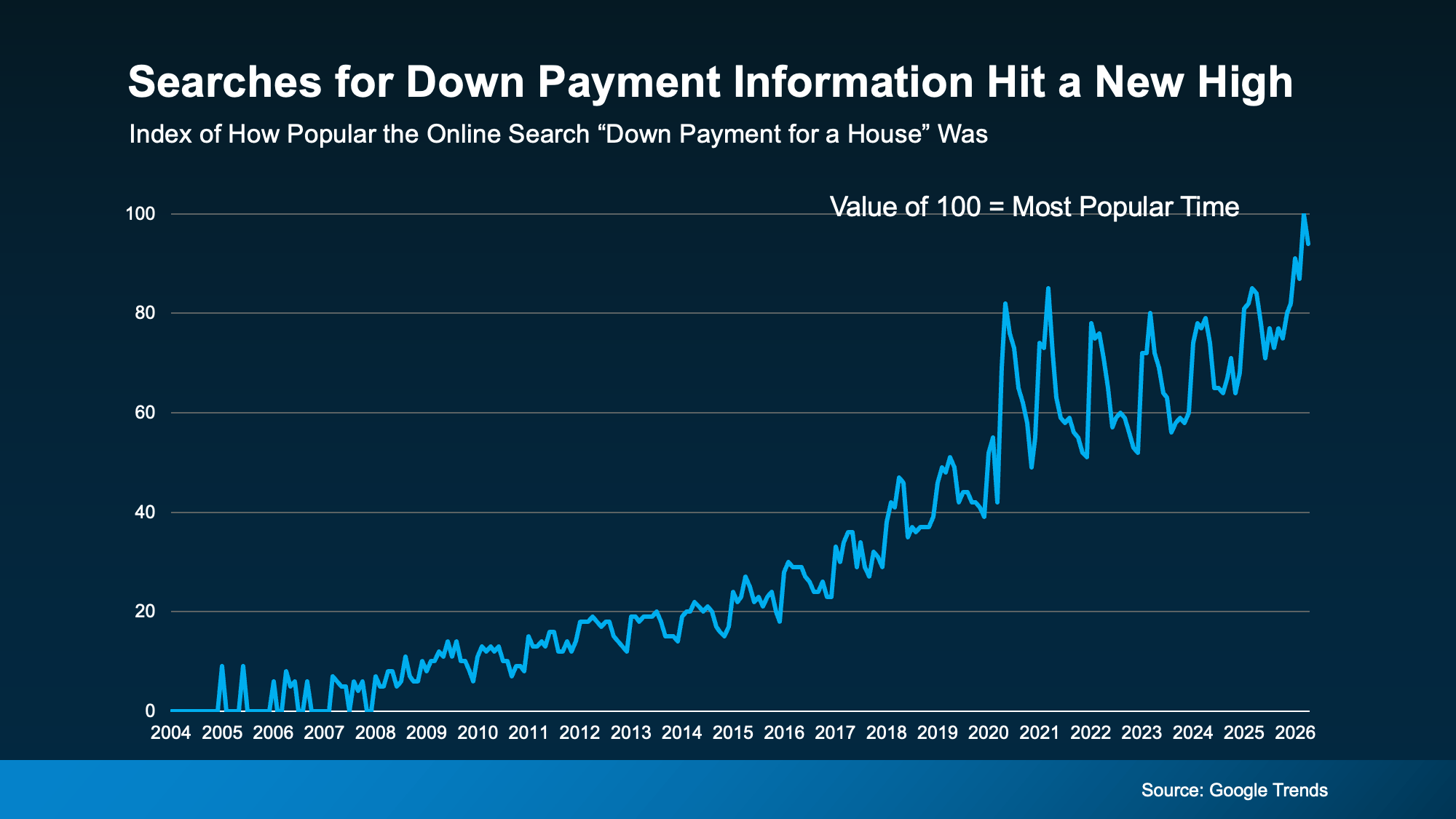

According to Google Trends, online searches for down payment information recently hit an all-time high. And that’s a clear sign more buyers are trying to figure out what they really need to save before making a move (see graph below):

If you’re wondering the same thing, you can always turn to the internet for answers. But a lot of the time, it’s better to ask a local expert. Because here’s what a pro would tell you.

If you’re wondering the same thing, you can always turn to the internet for answers. But a lot of the time, it’s better to ask a local expert. Because here’s what a pro would tell you.

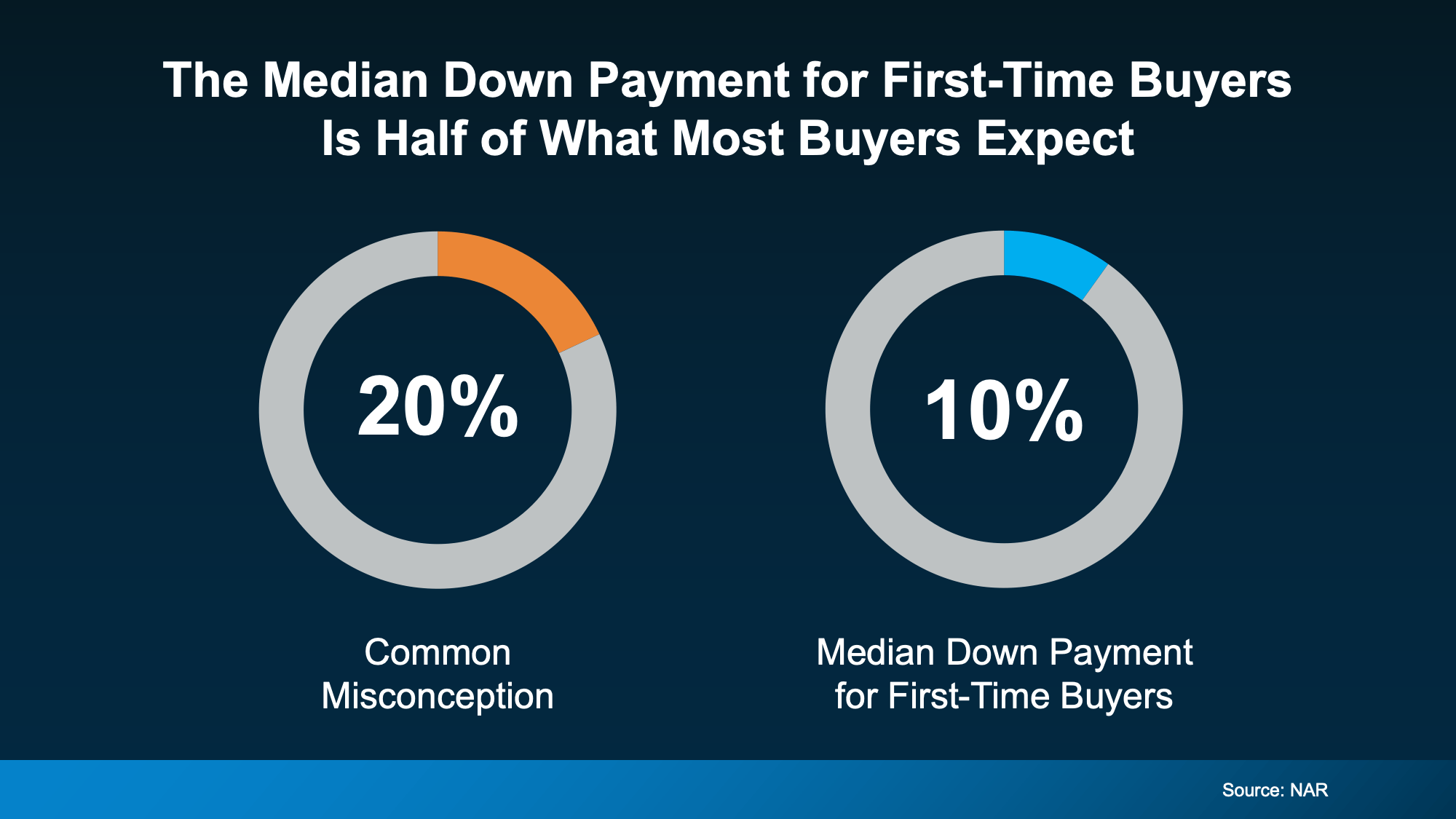

The 20% Down Payment Myth

The idea that you need 20% down to buy a home is one of the biggest misconceptions around the homebuying process. And the data debunks the myth.

While there are benefits to putting that much money down, most first-time buyers put down far less.

Here’s why. Unless it’s stated by your lender, you typically don’t have to have a 20% down payment. There are even some loan options designed to help you get into a home with a much smaller upfront cost. As the Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For example, FHA loans allow down payments as low as 3.5%, while VA and USDA loans offer zero down payment options for qualified applicants, like Veterans.

And those options are just one reason so many first-time buyers are able to buy without a 20% down payment.

What Buyers Are Actually Putting Down

So, if buyers aren’t doing 20%, how much do they actually put down?

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is only 10%. That’s half of what you probably expected.

That means if you’re aiming to save 20% because you think you have to, you may be setting a timeline that’s longer than necessary.

That means if you’re aiming to save 20% because you think you have to, you may be setting a timeline that’s longer than necessary.

And here’s some more good news. It’s not only that you may be able to buy with less money down than you thought, but there are also options to help you get to your down payment goal even faster.

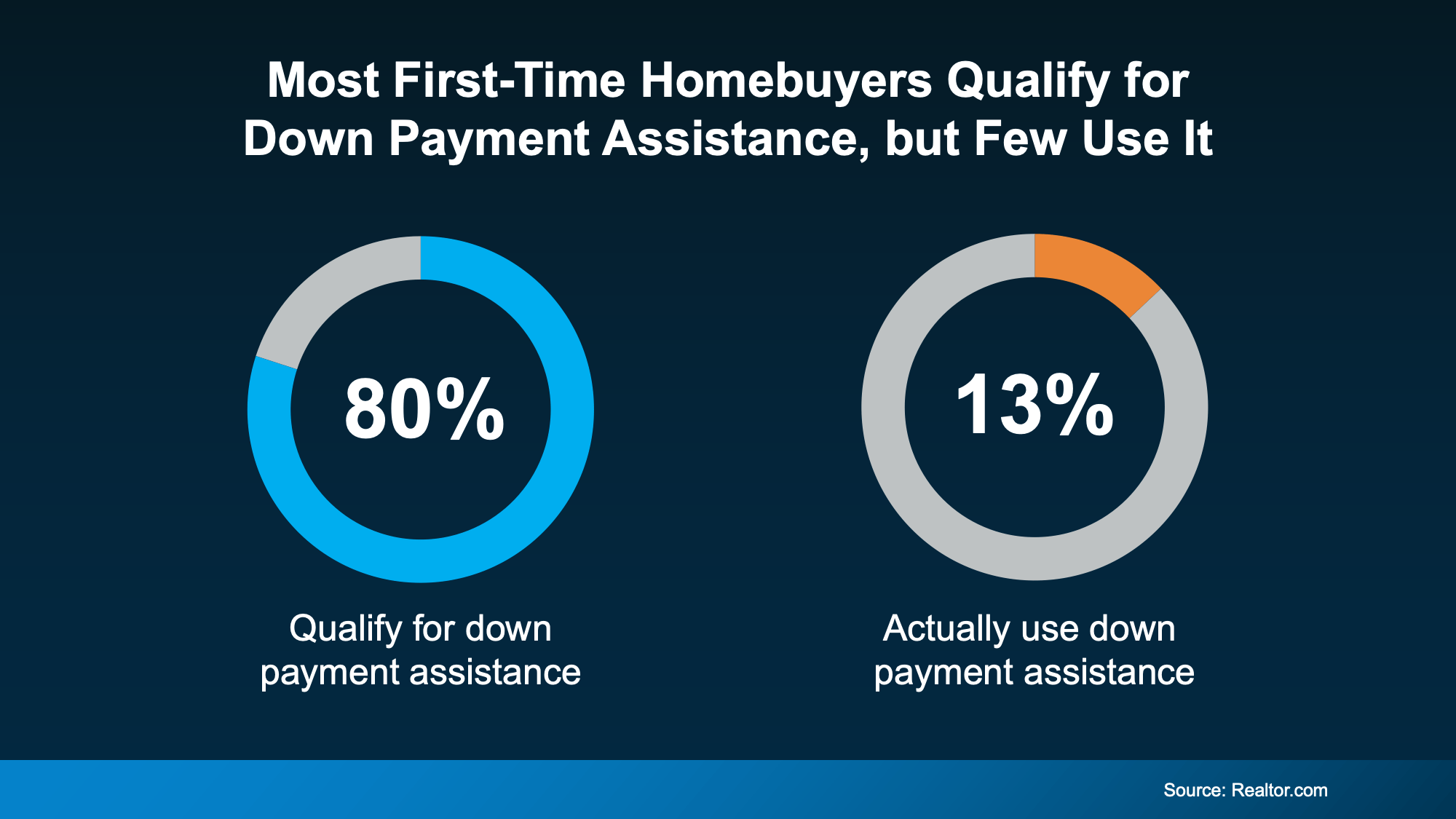

Why You Should Look into Down Payment Assistance Programs

There are a lot of programs designed to help you save for a down payment – and they can make a big difference in how fast you hit your savings target. Unfortunately, buyers don’t realize how many there are, or that they may qualify for help.

Research from Realtor.com shows almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% actually use it (see chart below):

And that’s another big miss holding would-be buyers like you back.

And that’s another big miss holding would-be buyers like you back.

In the U.S., there are over 2,600 homeownership programs available, many offering significant financial support. As Down Payment Resource shares:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

Imagine how much further your savings could go with an extra $18,000 you can use to buy. In some cases, you may even be able to stack multiple programs, giving what you’ve saved an even bigger boost.

Bottom Line

The simple truth is: most first-time buyers don’t put 20% down. And if you’ve been waiting to buy until you have that saved, you may be setting a timeline that’s longer than necessary.

To find out what you really need to save and if you qualify for any help, connect with a trusted lender who can walk you through your options. You may be able to buy sooner than you thought.

There’s a lot of uncertainty right now and that’s leading to some dramatic headlines. And if you’re thinking about buying a home, that can make you feel a little less sure about your decision.

A recent study by CNBC asked homebuyers what they’re most worried about, and three themes kept coming up again and again:

- Mortgage rates

- The number of homes for sale

- Home prices

But a lot of what you may be hearing on those is based more on misconceptions. Not facts. So, let’s break it down and separate fact from fiction.

Misconception #1: “I’ll Just Wait, Because Mortgage Rates Are Going To Fall Dramatically”

One idea doing its rounds on social is that mortgage rates are going to drop dramatically soon. So, it’s better to wait to buy.

But is that really what’s expected?

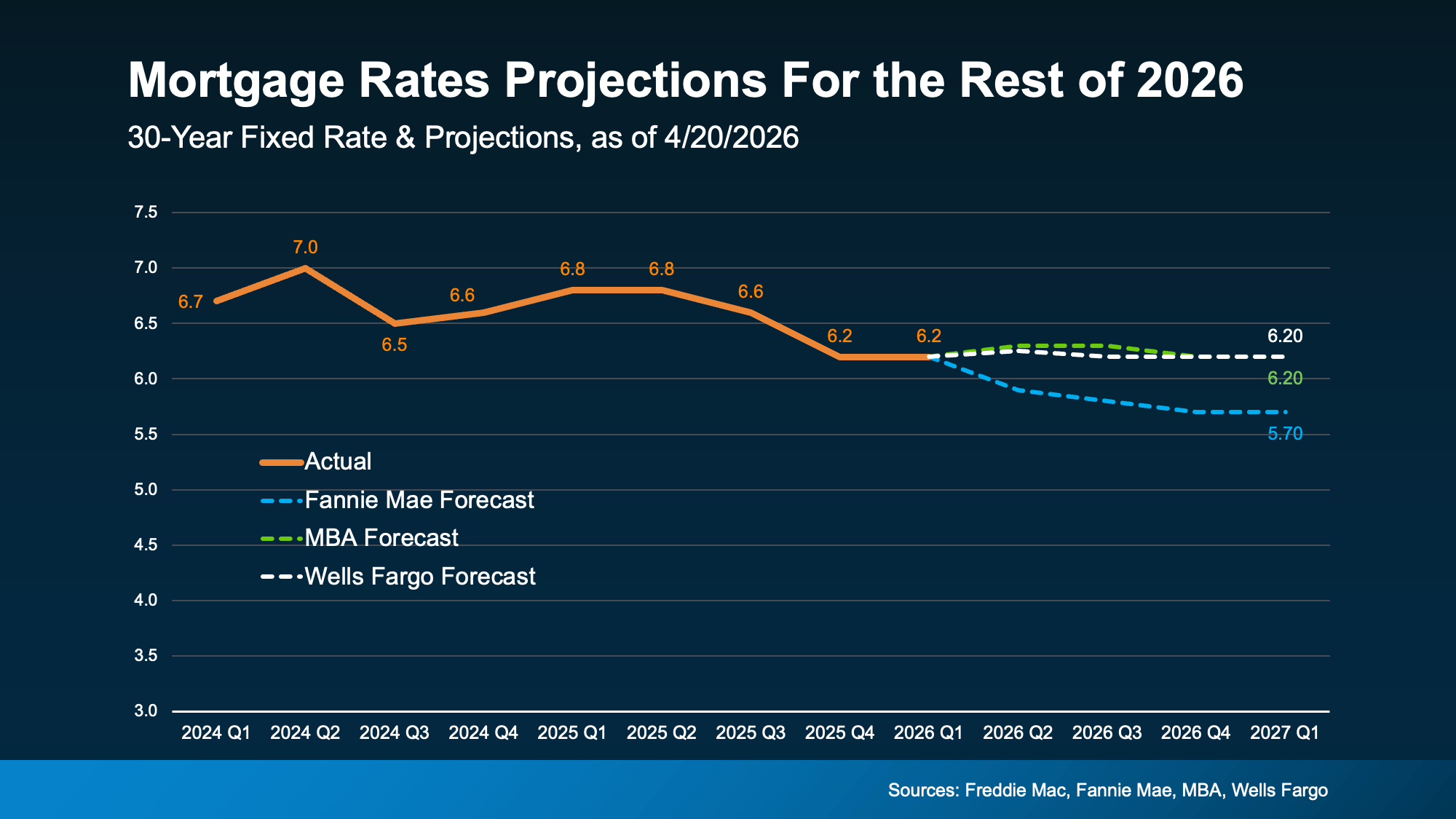

While mortgage rates have come down a bit in the last few weeks, forecasts don’t show a major drop ahead. The most likely scenario is that rates stay somewhere in the low 6% range this year.

And that’s not a big change from where rates are now (see graph below):

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. As U.S. News explains:

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. As U.S. News explains:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

Not to mention, even with rates where they are today, it’s already more affordable than a year ago. So, even if they don’t change much, it’s still better than it was.

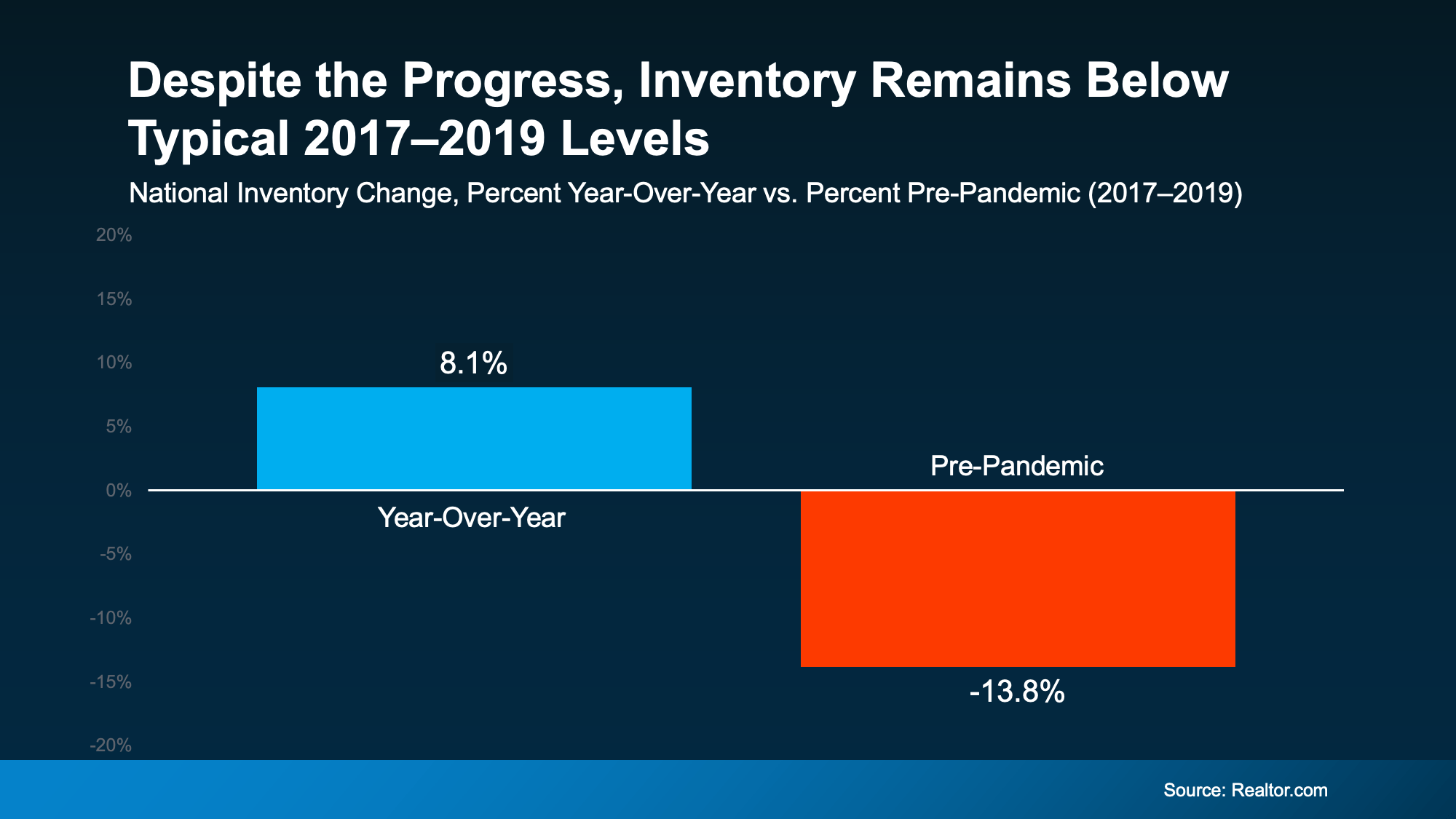

Misconception #2: “There Are Too Many Homes for Sale Right Now”

You’ve probably heard inventory is up. And nationally, it is. The number of homes for sale is 8% higher than this time last year. But that’s not a bad thing. In fact, it’s one of the reasons buyers have a bit more breathing room right now.

The problem is the headlines are making something good, sound bad. They’re focusing on how this is the most inventory we’ve had since 2019 or how many homes builders are building. And that can make it sound like the number of homes for sale is rising too far, too fast.

But that’s not what the bigger picture shows.

Data from Realtor.com proves that, even though inventory is up compared to last year, it’s still nearly 14% lower than it was during the last normal housing market (2017-2019):

While it can vary a lot based on where you live, only 9 states have more inventory than pre-pandemic today. That’s a key reason why there still aren’t enough homes for sale to trigger something like the crash back in 2008.

While it can vary a lot based on where you live, only 9 states have more inventory than pre-pandemic today. That’s a key reason why there still aren’t enough homes for sale to trigger something like the crash back in 2008.

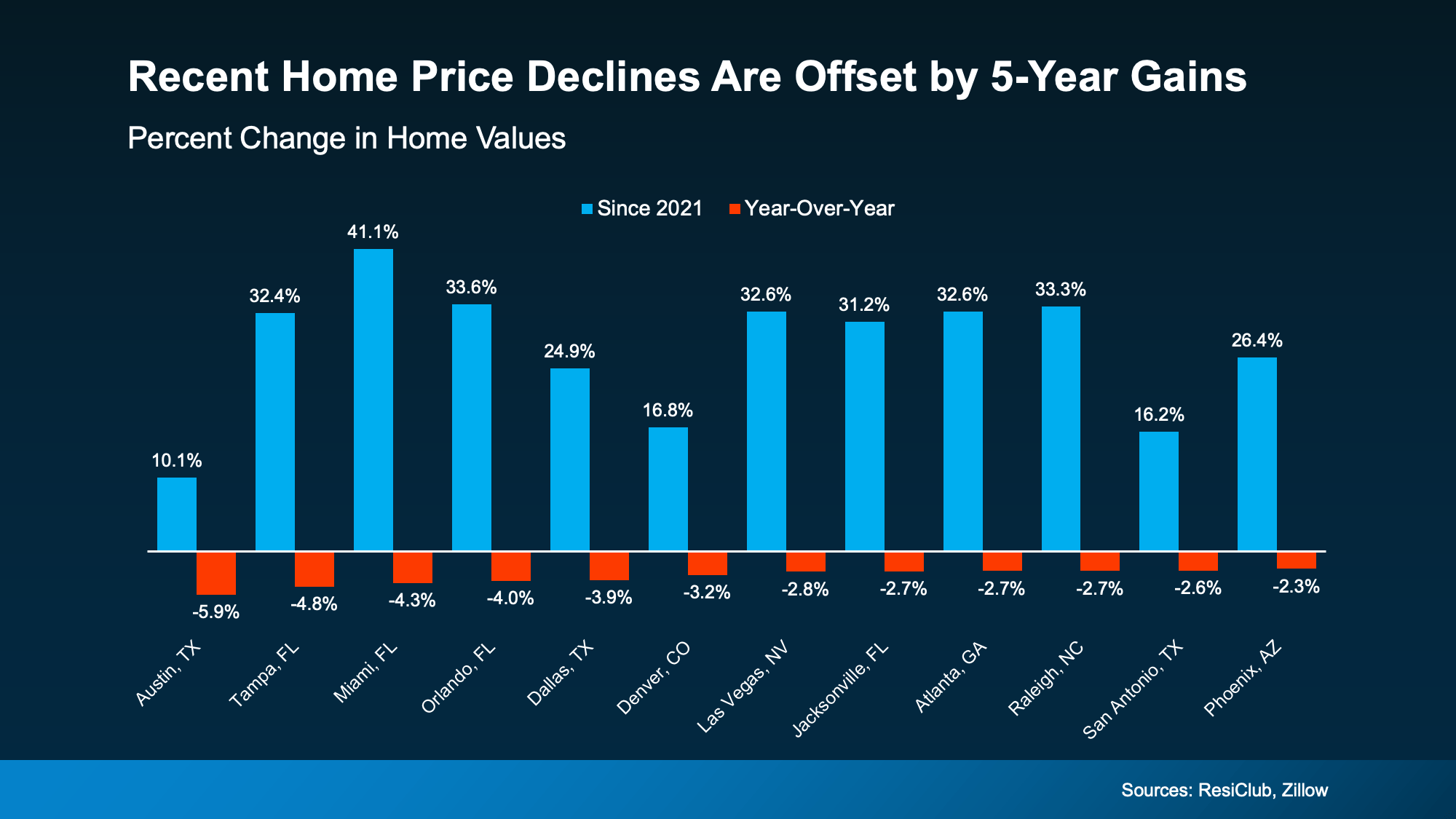

Misconception #3: “Home Prices Are About To Crash”

You’ve probably seen this one, too. The confusion is coming from the fact that some metros are experiencing slight price declines. And influencers are running with that and saying prices are crashing. But that’s not the reality.

Most areas are seeing prices rise, not fall. And that’s because:

- Many homeowners aren’t selling because they don’t want to give up the low mortgage rate they locked in a few years ago. And that’s keeping a lid on how much inventory can grow.

- Since inventory is still below pre-pandemic norms, there aren’t enough homes for sale to cause a price crash.

- And even in markets with more inventory, some sellers are choosing to pull their homes off the market instead of cutting prices.

And those are 3 big reasons prices aren’t headed for a crash.

And even in the markets experiencing mild declines, the drops aren’t enough to cancel out the big gains most homeowners have seen in the last 5 years (see graph below):

That’s not a crash. That’s just prices moderating after a few record-breaking years.

That’s not a crash. That’s just prices moderating after a few record-breaking years.

Bottom Line

Online posts are going to make things sound worse than they are. If you want a true, data-bound look at what’s really happening in today’s market, lean on a real estate agent.

Connect with a local agent so you have someone to separate fact from fiction today.

The Secret To Selling Fast, No Matter the Market

4 Ways To Give Your Offer an Edge This Spring

Is Late May the Best Time To List Your House?

-

Affordability4 weeks ago

Affordability4 weeks agoWhen Buying a Home Feels Out of Reach, Some Families Do This Instead

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

-

For Buyers2 days ago

For Buyers2 days agoMore Options Are Popping Up This Spring

-

Agent Value2 days ago

Agent Value2 days agoStay or Sell? How To Make the Right Call as You Age

-

Affordability2 days ago

Affordability2 days agoThink You Have To Put 20% Down? Most First-Time Homebuyers Don’t.

-

Affordability2 days ago

Affordability2 days agoThe 10 Best Markets for First-Time Buyers This Spring

-

Equity2 days ago

Equity2 days agoRent or Buy? The Real Tradeoff Most People Don’t Talk About

-

Featured2 days ago

Featured2 days ago3 Things That Are Not Going To Happen in Today’s Housing Market

You must be logged in to post a comment Login