For Buyers

Do Elections Impact the Housing Market?

The 2024 Presidential election is just months away. As someone who’s thinking about potentially buying or selling a home, you’re probably curious about what effect, if any, elections have on the housing market.

It’s a great question because buying or selling a home is a major decision, and it’s natural to wonder how such a major event might impact your plans.

Historically, Presidential elections have only had a small, temporary impact on the housing market. Here’s the latest on exactly what’s happened to home sales, prices, and mortgage rates throughout those time periods.

Home Sales

During the month of November, in years when the Presidential election takes place, there’s typically a slight slowdown in home sales. As Ali Wolf, Chief Economist at Zonda, explains:

“Usually, home sales are unchanged compared to a non-election year with the exception being November. In an election year, November is slower than normal.”

This is mostly because some people feel uncertain and hesitant about making big decisions during such a pivotal time. However, it’s important to know this slowdown is temporary. Historically, home sales bounce back in December and continue to rise the following year.

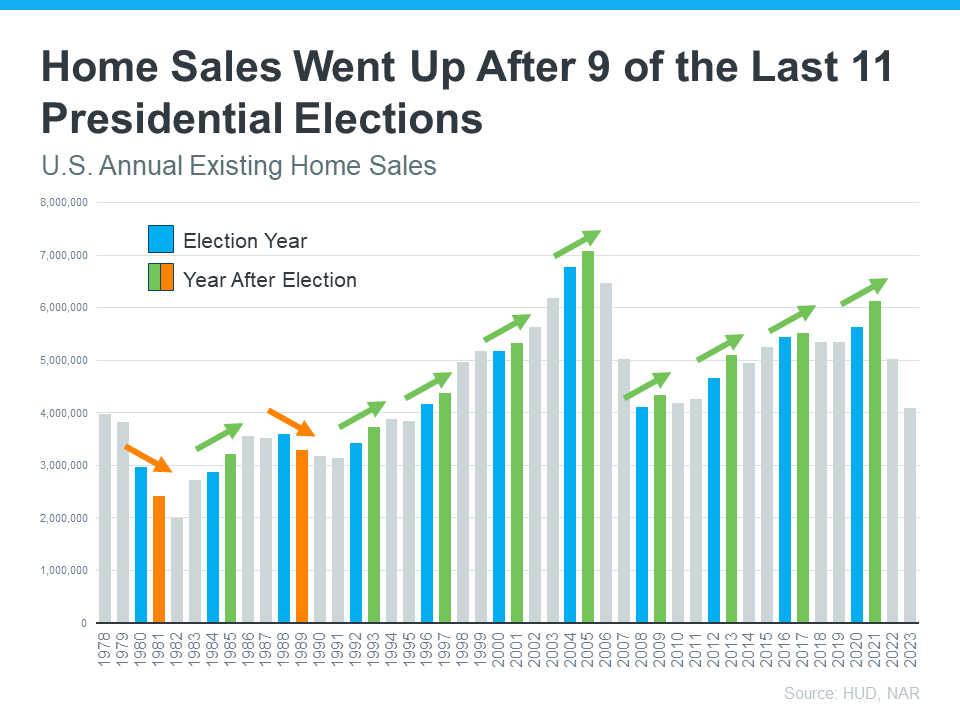

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after nine of the last 11 Presidential elections, home sales went up the next year (see graph below):

The graph shows annual home sales going back to 1978. Each year with a Presidential election is noted in blue. The year immediately after each election is green if existing home sales rose that year. The two orange bars represent the only years when home sales decreased after an election.

Home Prices

What about home prices? Do they drop during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist puts it:

“An election year doesn’t alter the price trend that is already happening in the market.”

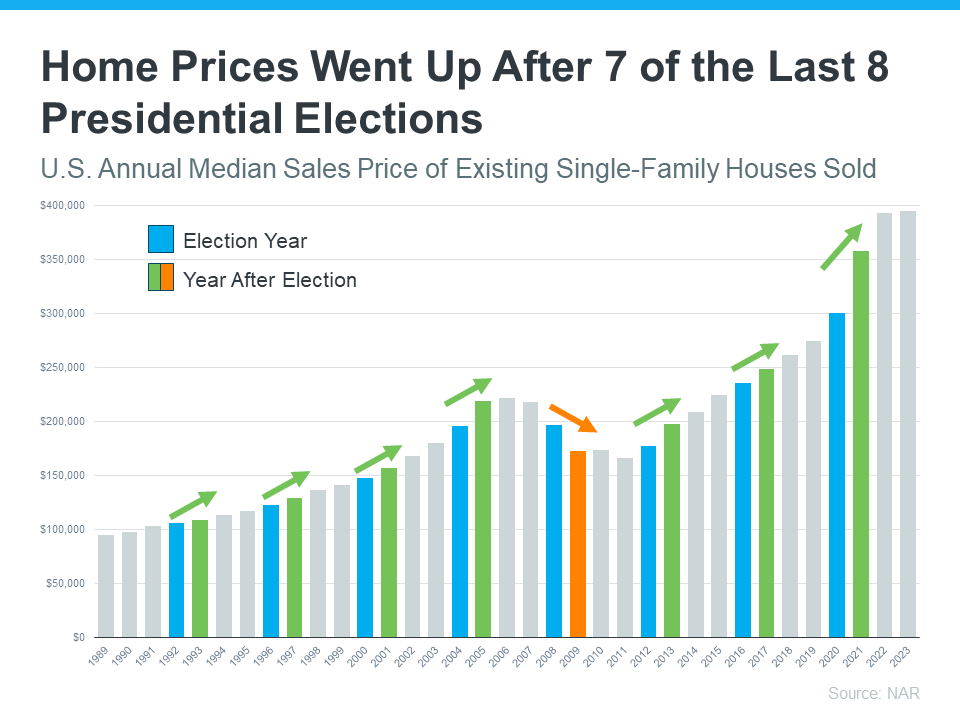

Home prices are pretty resilient. They generally rise year-over-year, regardless of elections. The latest data from NAR shows after seven of the last eight Presidential elections, home prices increased the following year (see graph below):

Just like the previous graph, this shows election years in blue. The only year when prices declined after an election is in orange. That was during the housing market crash, which was far from a typical year. Today’s market is different than it was back then.

All the green bars represent when prices rose the following year. So, if you’re worried about your home losing value because of an election, you can rest easy knowing prices rise after most Presidential elections.

Mortgage Rates

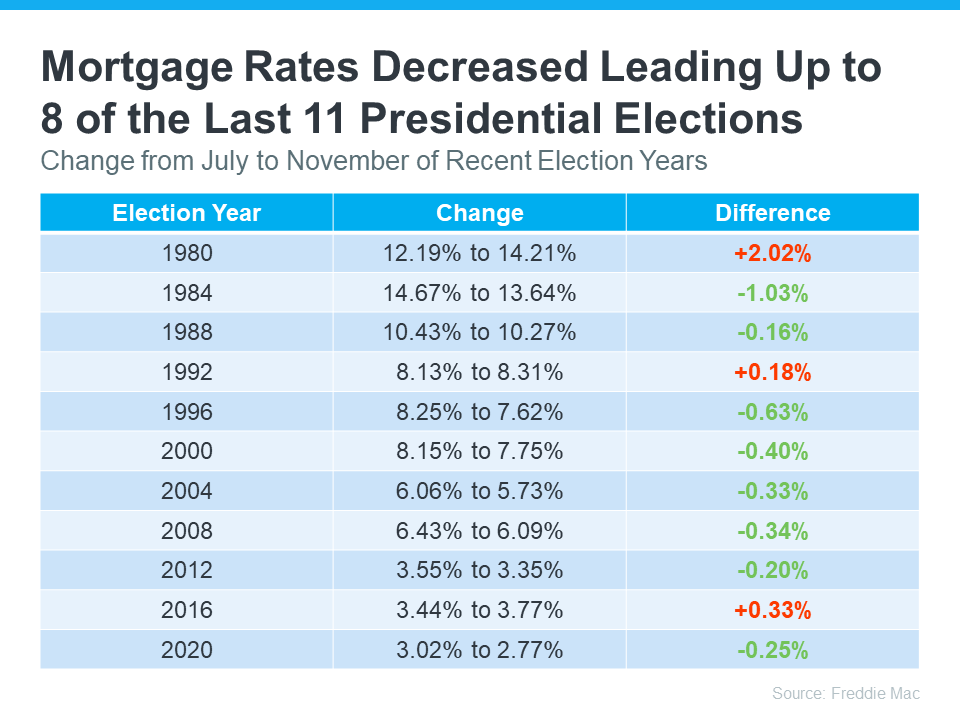

Mortgage rates are important because they affect how much your monthly payment will be when you buy a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in eight of them (see chart below):

Most forecasts expect mortgage rates to ease slightly throughout the remainder of the year. If they’re right, this year will follow the trend of declining rates leading up to most previous elections. And if you’re looking to buy a home in the coming months, this could be good news, as lower rates could mean a lower monthly payment.

What This Means for You

So, what’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually small and temporary. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Bottom Line

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. If you have questions, reach out to a local real estate agent. They’re here to help you navigate the market, election year or not.

If buying a home is on your radar, you’ve probably been keeping an eye on mortgage rates and home prices. But don’t forget about homeowners insurance.

Homeowners insurance has always been part of owning a home. But over the past few years, it’s become a larger expense for many homeowners – something that’s especially frustrating when affordability already feels tight.

The good news? While premiums are still rising, the latest data shows those increases are beginning to slow. Here’s what buyers should know.

Home Insurance Costs Have Gone Up

You’ve probably heard stories from friends or family about their premiums going up. And that’s not really a surprise when you consider data from the Pew Research Center shows 71% of homeowners say their insurance costs have gone up over the past few years.

While no one likes rising costs, knowing what to expect can help you plan ahead. Your first insurance payment is typically included in your closing costs, but after that it’ll become part of your monthly housing expenses.

Getting an insurance quote early can help you build a more realistic budget and avoid surprises later.

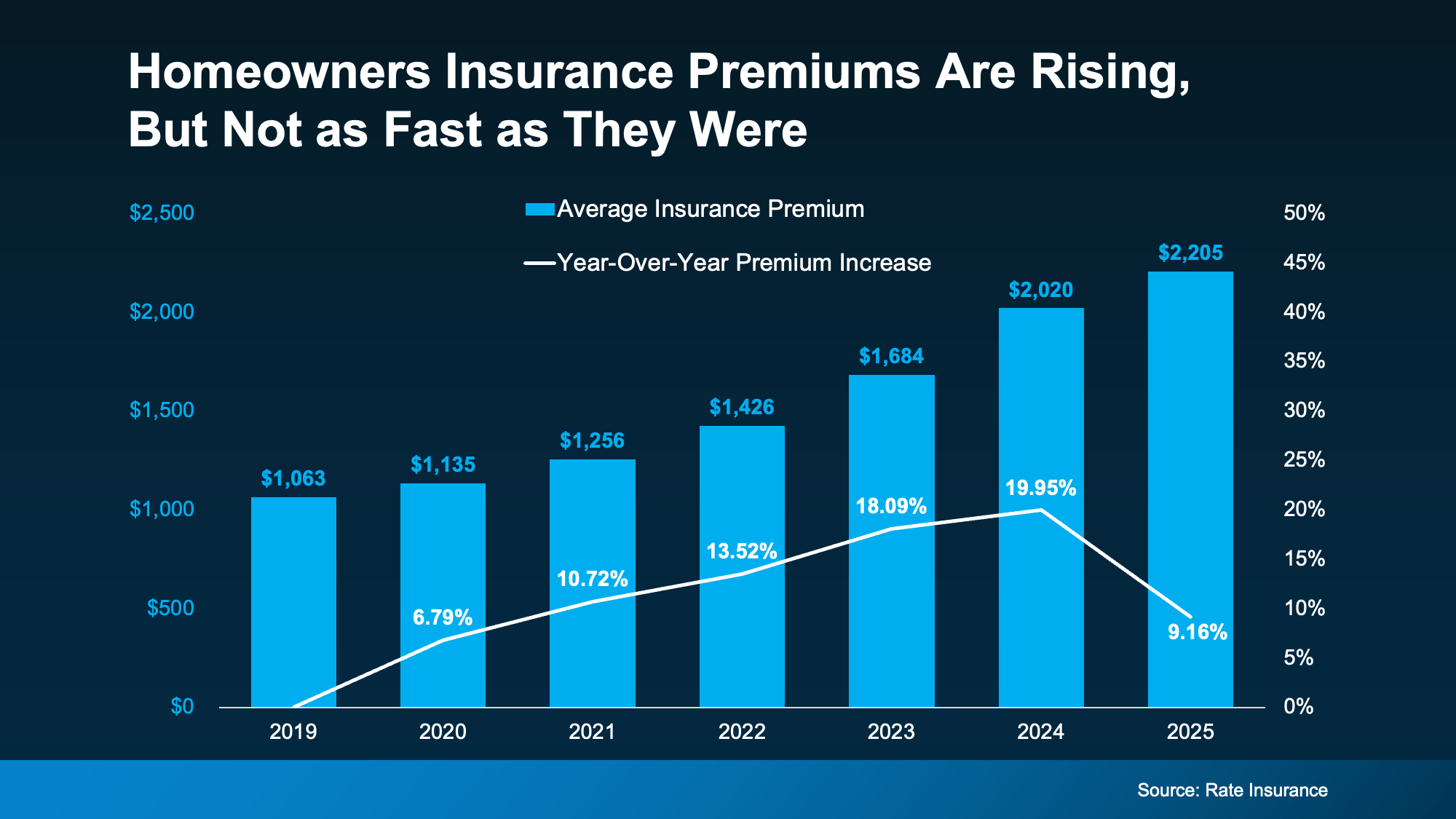

Premiums Are Rising, But Not as Fast as They Were

Most of the headlines focus on how home insurance is getting more expensive. And that’s true. But here’s the part that’s easy to miss.

Insurance premiums are still rising.

But they’re not rising as fast as they were.

According to the latest report from Rate Insurance, 2025 saw the first slowdown in annual premium increases since 2019 (see graph below):

That doesn’t mean premiums are getting cheaper. It simply means the rapid increases of the past several years may finally be starting to ease – a small but welcome step in the right direction.

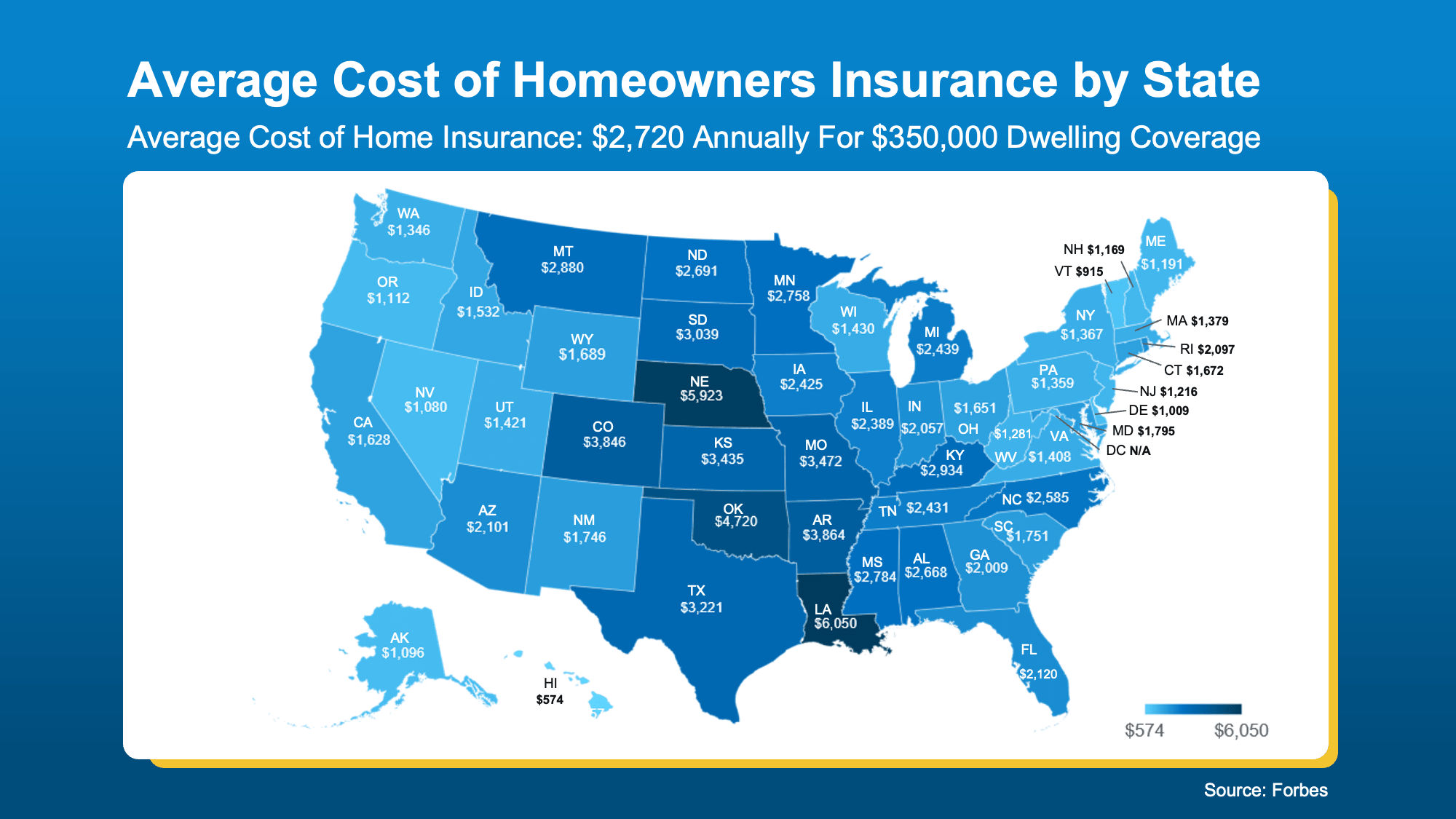

But what you’ll pay in one part of the country can look very different from what someone pays somewhere else.

Where You Buy Can Make a Big Difference

Insurance costs vary because some parts of the country experience more claims than others. That’s why it’s important to look at what’s happening locally.

Your premium will depend on things like where you’re buying, the home itself, and the coverage you choose.

Forbes data can give a rough idea of your state’s typical premiums. Check out the map below – the darker the blue, the higher the costs tend to be in that state:

Ways To Lower Your Costs

While you can’t control every cost that comes with buying a home, you can control how prepared you are. If you’re crunching the numbers and trying to find ways to save, Insurify and NerdWallet offer these tips that can help you get the best insurance price possible:

-

Shop Around – Compare quotes from multiple companies.

-

Bundle Policies – Combine home and auto to see if a bundle price is cheaper.

-

Ask If There Are Discounts – Don’t miss out on savings you may qualify for.

-

Highlight Upgrades – Features like a new roof or storm windows can cut costs.

-

Improve Your Credit – A stronger credit score can mean better premiums.

One of the smartest things you can do is get an insurance quote before you make an offer. That way, you’ll know what your monthly housing costs are likely to be before you commit.

An insurance professional can walk you through your options and help you find coverage that fits both your needs and your budget.

Bottom Line

Homeowners insurance has become a bigger part of the homebuying conversation. But it doesn’t have to become a bigger source of stress.

The key is knowing what to expect before you buy. Get an insurance quote early, factor it into your budget, and lean on trusted local professionals to help you make the most informed decision possible.

After more than a year of headlines talking about how home prices are going to crash, the latest data shows that price growth may be starting to pick back up again. And depending on whether you’re buying or selling, that shift means something different for you.

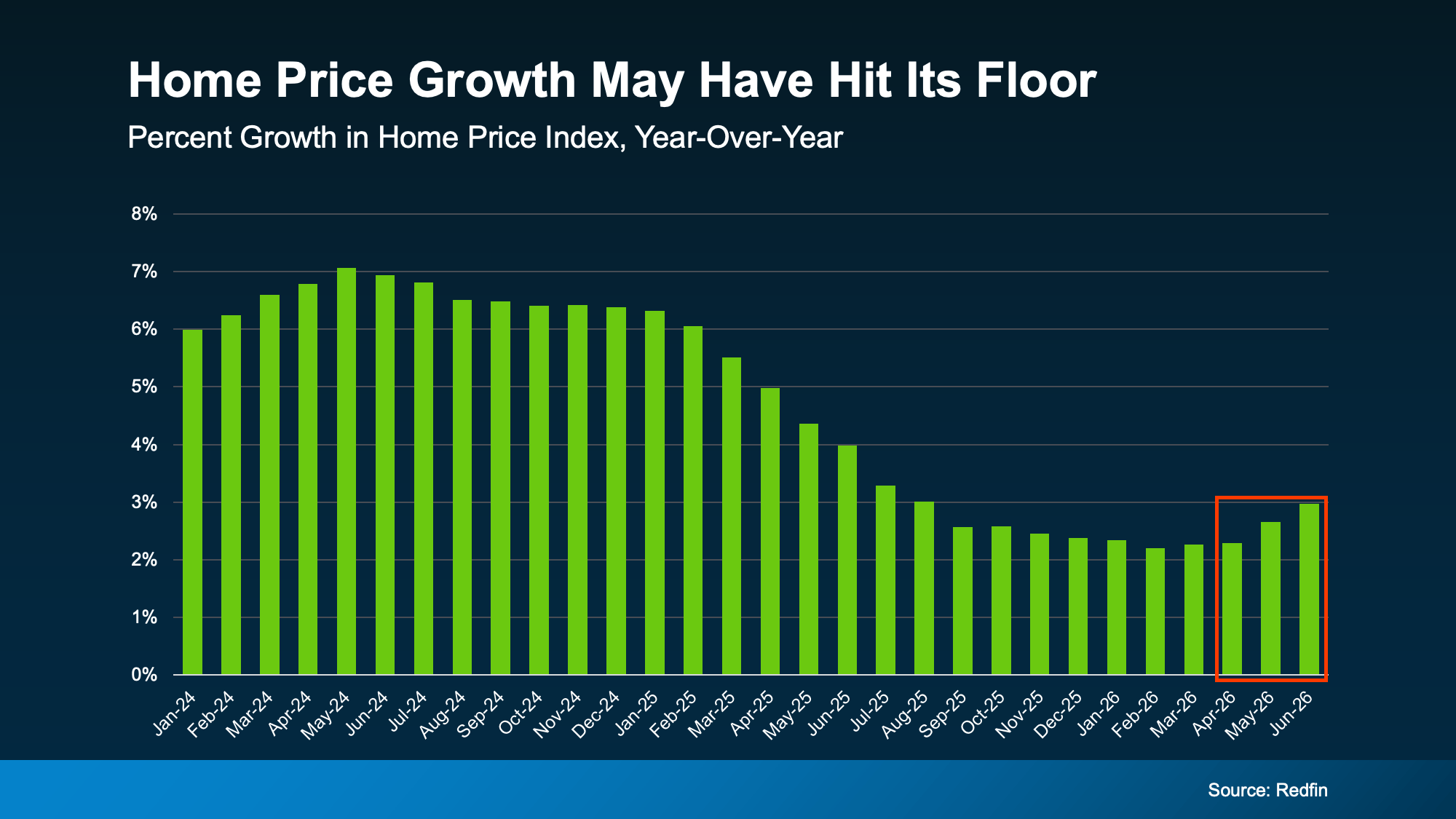

The Numbers May Be Starting To Turn

For the past couple of years, home price growth has been moderating – cooling from around 7% in mid-2024, according to Redfin (see graph below). But look at the right side of that graph. The pace of that growth appears to have hit its low point and started to turn.

While a couple months of data doesn’t necessarily mean this will be a lasting trend, there are some other signs that this could continue.

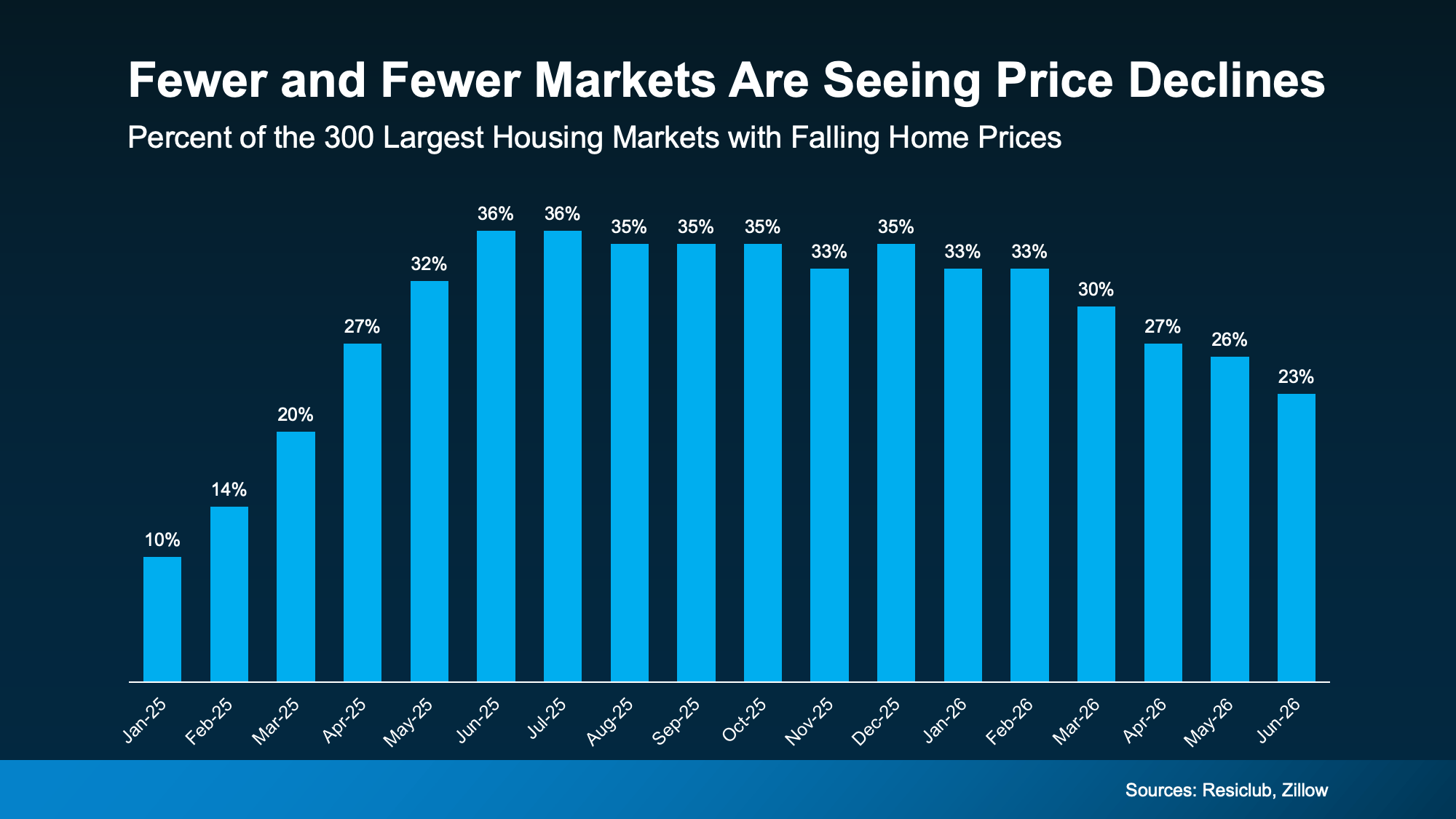

For example, fewer markets are seeing prices decline. According to ResiClub and Zillow, about 36% of the 300 largest housing markets had falling prices as of the middle of last year. Since the start of this year, that share has been shrinking. Now? Only 23% are experiencing those mild dips (see graph below):

When fewer markets see prices falling, that means more markets are seeing prices rise again.

And forecasts suggest this shift has room to run. On average, experts project home prices will rise about 2.3% nationally this year. And for that to happen, price growth would have to pick up a bit in the second half of 2026.

But Remember, Real Estate Is Local

While it looks like national prices may be starting to pick back up a tiny bit, that doesn’t mean that’s what’s happening in your neighborhood.

National home prices are really just an average of hundreds of local markets. Some are climbing faster. Others are still cooling. But one reason the national average may be looking up is because a growing number of metros may actually be net positive for prices this year.

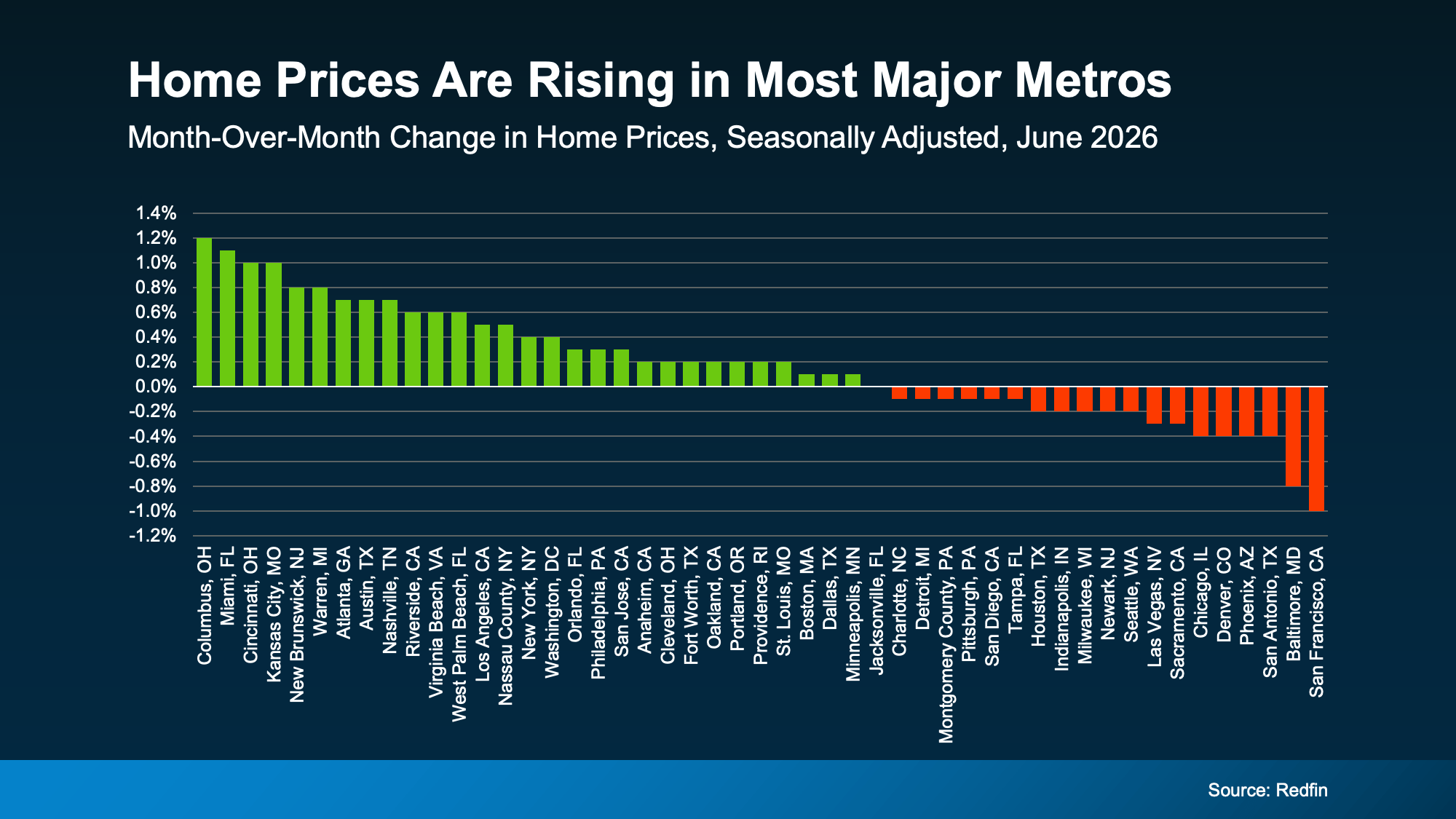

Not long ago, the major metros were split about 50/50 – half seeing prices rise and half seeing them fall. Now, that balance looks like it’s starting to tip in a more positive direction. Just last month, more than half of the major metros saw prices go up, according to Redfin (see graph below):

As Selma Hepp, Chief Economist at Cotality, explains:

“. . . local markets continue to tell very different stories. Annual home price growth has changed little since the start of the year, but some markets, especially those supported by strong job and income growth in the West and more affordable Midwest markets, have seen notable acceleration in price gains.”

What This Means for You

Home price headlines can be confusing because they don’t always tell the full picture. Lean on an agent to understand what’s happening in your local market and what the early signs say for where prices may go from here.

That’s the best way to stay one step ahead of the market.

If you’re buying: slower price growth has worked in your favor. You’ve had more room to negotiate and a budget you could plan around. If price growth is picking up in your area, buying now may mean paying less than you would later this year.

If you own a home: you’ve been gaining equity all along, even while growth moderated. If growth keeps picking up, those gains could speed up, too. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), projects the typical homeowner will gain roughly $16,000 in housing wealth this year. And if you’re thinking about selling, this shift is a good early sign for you. Just remember, the market is still pretty balanced and buyer-friendly in a lot of areas right now.

Home price growth slowed way down, and now it’s showing early signs of picking back up. Whether you’re buying or selling, let’s connect so you can see exactly what prices are doing in our local market and what that means for your plans.

Bottom Line

Home price growth slowed way down, and now it’s showing early signs of picking back up. Whether you’re buying or selling, connect with a local real estate agent so you can see exactly what prices are doing in your local market and what that means for your plans.

Today’s home prices have a lot of buyers – especially first-time buyers – wondering if there’s even anything out there that’s in their budget. But owning a home may be more within reach than you think. Sometimes, it just means considering a different type of home.

Condos and townhomes can be a great way to buy without stretching every last dollar. And right now, two things make them worth a serious look.

There Are More Condos and Townhomes To Choose From

Maybe you feel like there’s just nothing out there for you, and you’ve exhausted all your options. But have you considered condos or townhomes? A lot of buyers start by looking for a single-family, detached home without even realizing what that search omits from their pool of choices.

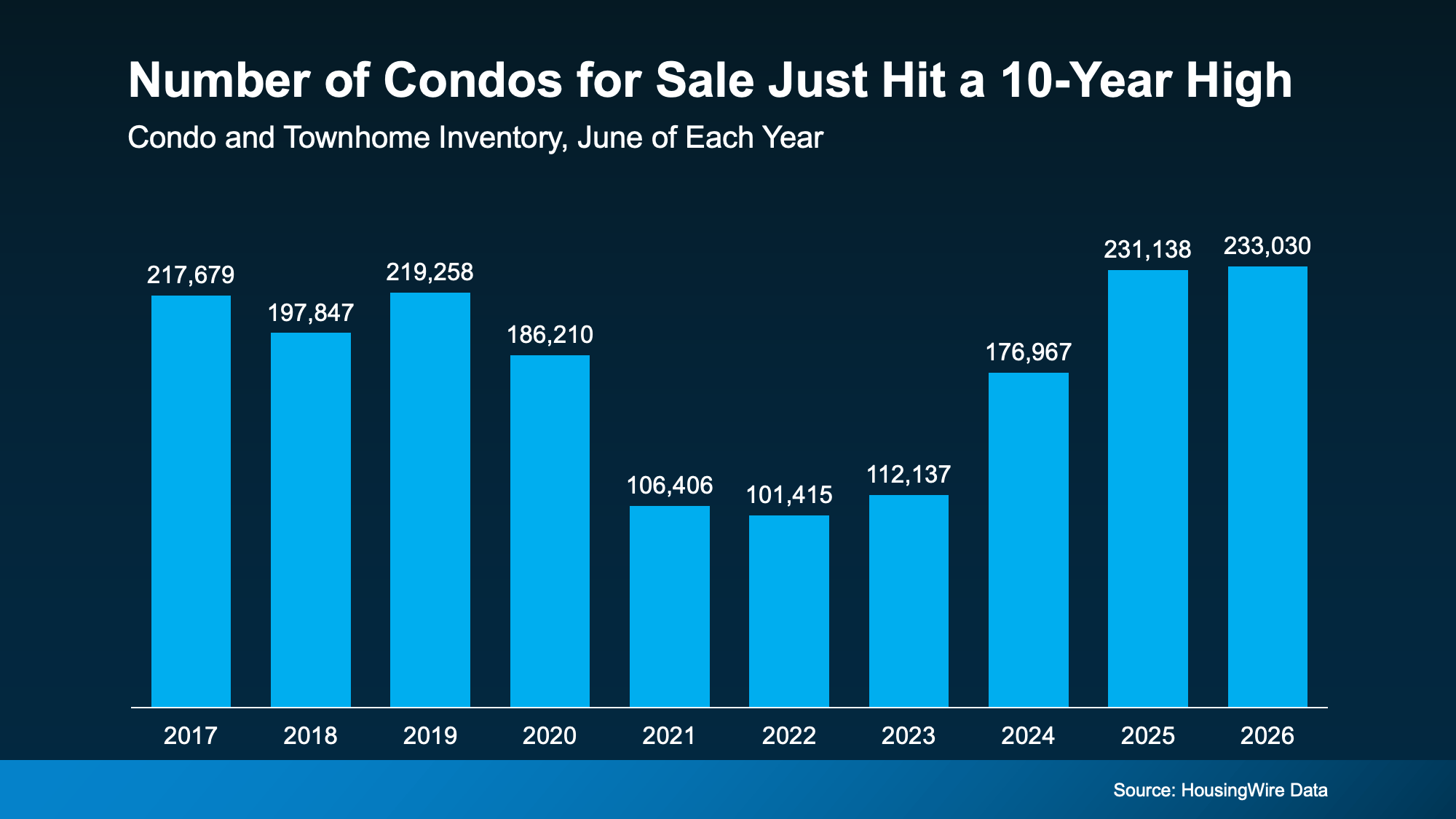

According to HousingWire Data, there were 233,030 condos and townhomes for sale this June. That’s more than any June in at least the past decade, and more than double the number available back in 2022 (see graph below):

That means there are more options out there in this segment of the market – and that’s especially good news for first-time buyers. These types of homes can be a great way to break into the market for less.

Just remember, that’s the national number. What’s available will depend on where you’re looking. But generally speaking, more options means less competition, more time to decide, and more room to negotiate.

They Also Tend To Cost Less Than Single-Family Homes

Price is the other big draw. According to the National Association of Realtors (NAR), the median condo price was $380,000 in June. In contrast, the median single-family home price was $446,400 (see graph below):

That’s a difference of more than $66,000.

A big reason why? Condos are usually smaller than single-family homes. And smaller homes can come with smaller price tags.

And if you don’t need all that extra space, that lower entry price could be exactly what gets you through the door.

Condo or Townhome? How They’re Different.

For buyers who feel priced out of the market, a condo or townhome could be a way in. But there are some things to know. Before you start checking out homes, it’s good to understand how these two compare to each other – and to a single-family home.

-

With a single-family detached home, you own the house and the land it sits on, and you don’t share any walls with neighbors. That means the most space and privacy. But it also usually comes with a higher tag, and all the maintenance is on you.

-

With a townhome, you own the building and the lot it sits on. They’re usually multi-level, so you get more space, and you share two walls at most. You’ll also have more say over how your home looks and how repairs get done, but more of that upkeep falls on you.

-

With a condo, you own just the inside of your unit and may have access to community features like a pool or gym. The building and shared space belong to everyone who lives there, which means you have less maintenance responsibilities. But you’ll also likely have more neighbors around you, less control over building decisions, and higher HOA fees since the HOA handles the exterior and common areas.

Bottom Line

A condo or townhome could be your path to owning a home without blowing your budget. Connect with a local real estate agent to see what’s for sale in your area and figure out which type of home fits your lifestyle, and your bottom line.

Buying a Home? Here’s What You Should Know About Home Insurance Costs.

Home Price Growth Slowed Down. That May Be Changing.

Selling a Luxury House? Here’s Why Now Is a Good Time

-

Equity4 weeks ago

Equity4 weeks agoThe Housing Market Is Stronger Than You Think

-

Economy3 weeks ago

Economy3 weeks agoWhat Buying or Selling a Home Gives Back to Your Community

-

Affordability4 weeks ago

Affordability4 weeks agoDown Payments Are Smaller Than They’ve Been Since 2021

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoStudent Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

-

Affordability3 weeks ago

Affordability3 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

-

For Sellers2 weeks ago

For Sellers2 weeks agoThink Nobody’s Buying Homes Right Now? Think Again.

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

-

First-Time Buyers2 weeks ago

First-Time Buyers2 weeks ago14 Years Running: Why Real Estate Is Still America’s Favorite Investment

You must be logged in to post a comment Login