Downsize

Why Moving to a Smaller Home After Retirement Makes Life Easier

Retirement is a time for relaxation, adventure, and enjoying the things you love. As you imagine this exciting new chapter in your life, it’s important to think about whether your current home still fits your needs.

If it’s too big, too costly, or just not convenient anymore, downsizing might help you make the most of your retirement years. To find out if a smaller, more manageable home might be the perfect fit for your new lifestyle, ask yourself these questions:

- Do the original reasons I bought my current house still stand, or have my needs changed since then?

- Do I really need and want the space I have right now, or could somewhere smaller be a better fit?

- What are my housing expenses right now, and how much do I want to try to save by downsizing?

If you answered yes to any of these, consider the benefits that come with downsizing.

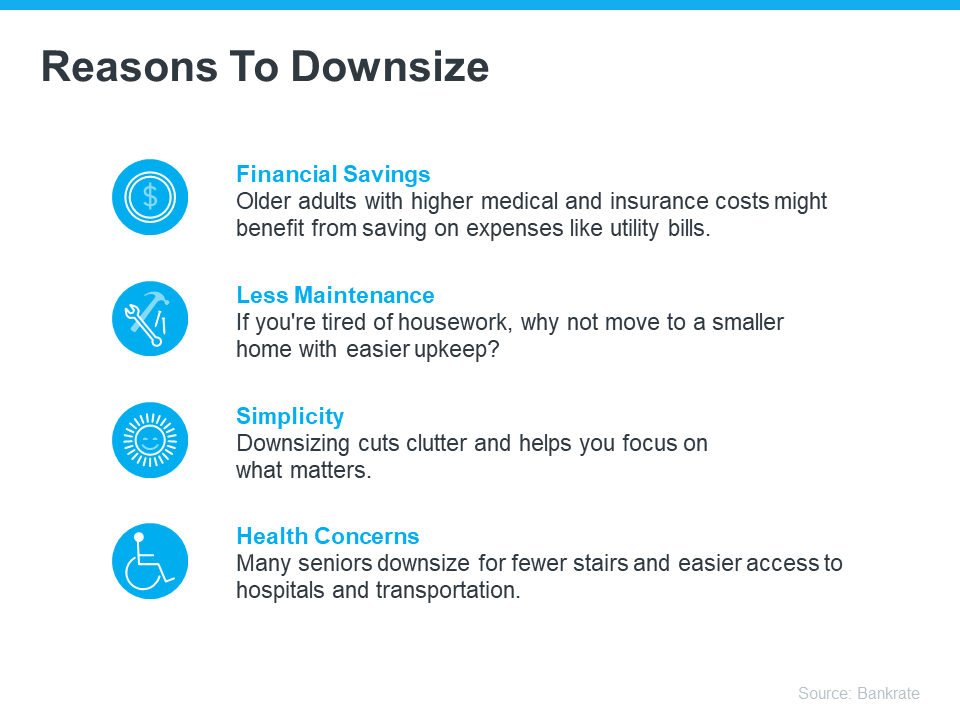

The Benefits of Moving into a Smaller Home

There are many reasons why you should downsize. Here are just a few from Bankrate:

Your Equity Can Help Make Downsizing Possible

If those perks sound like something you’d want, you may already have what you need to make it happen. A recent article from Seniors Guide shares:

“And at a time when homeowners age 62 and older have more than $12 trillion in home equity, downsizing makes sense . . .”

If you’ve been in your house for a while, odds are you’re one of those homeowners who’s built up a considerable amount of equity. And that equity is something you can use to help you buy a home that better fits your needs today. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Downsizing can mean taking that equity when the home is sold and using it to pay cash or make a large down payment on a lower-priced home, reducing your monthly living expenses.”

When you’re ready to use all that equity to fuel your next move, your real estate agent will be your guide through every step of the process. That includes setting the right price for your current house when you sell, finding the home that best fits your evolving needs, and understanding what you can afford at today’s mortgage rate.

Bottom Line

Starting your retirement journey? Think about downsizing – it could really help. When you’re ready, talk to a local real estate agent about your housing goals this year.

At some point, as you start thinking about the years ahead, this question tends to come up:

“Could I stay here long-term… or would it make more sense to move?”

It’s not always urgent. It often shows up in small moments, like going up and down the stairs, keeping up with the maintenance, or just thinking about what the next chapter of your life might look like in this home.

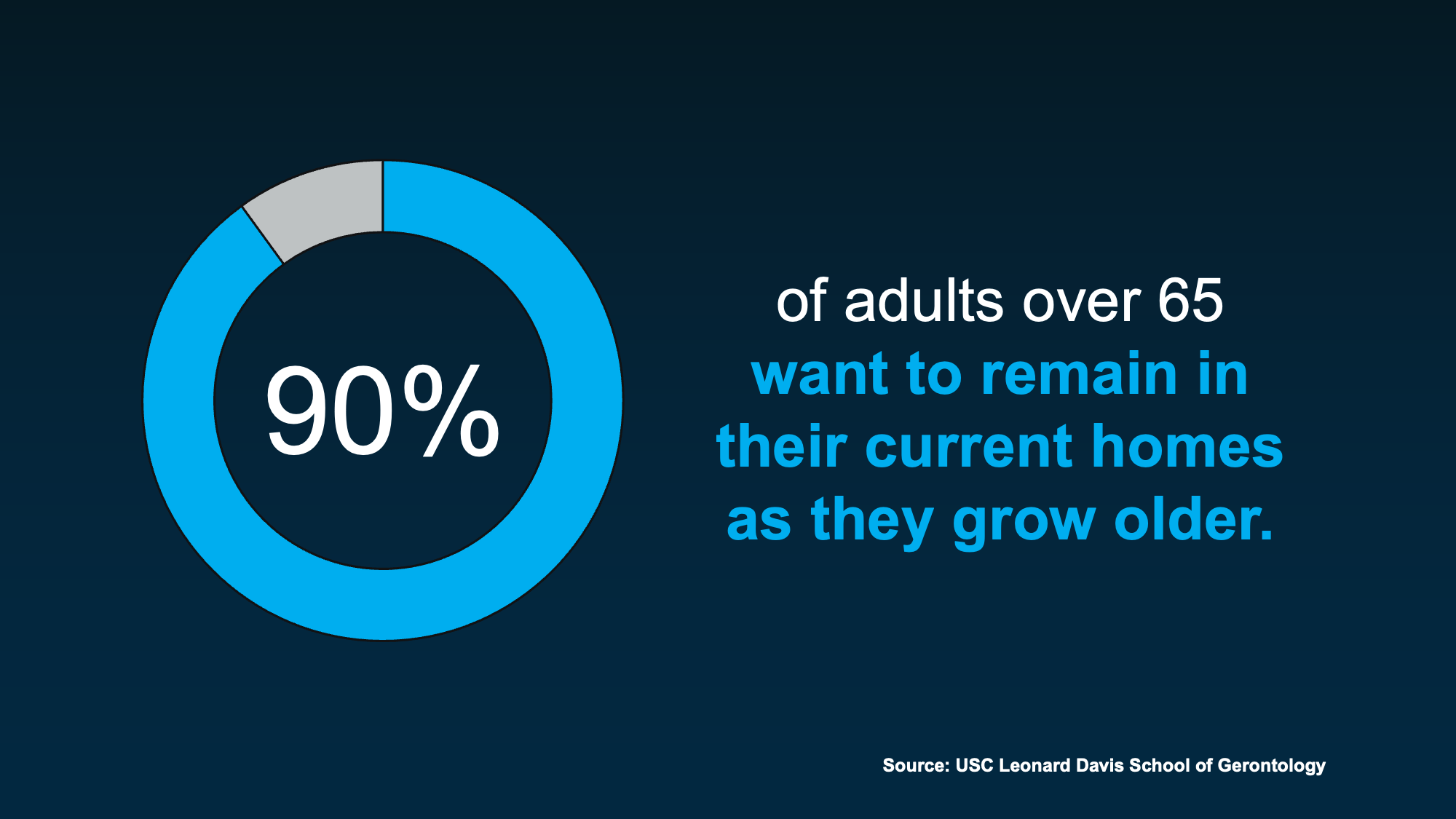

And for most people, the answer is simple. They want to stay.

The USC Leonard Davis School of Gerontology found about 90% of adults over 65 prefer to stay in their homes as they get older (see below):

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

What You Need To Plan for If You’re Staying in Your Home

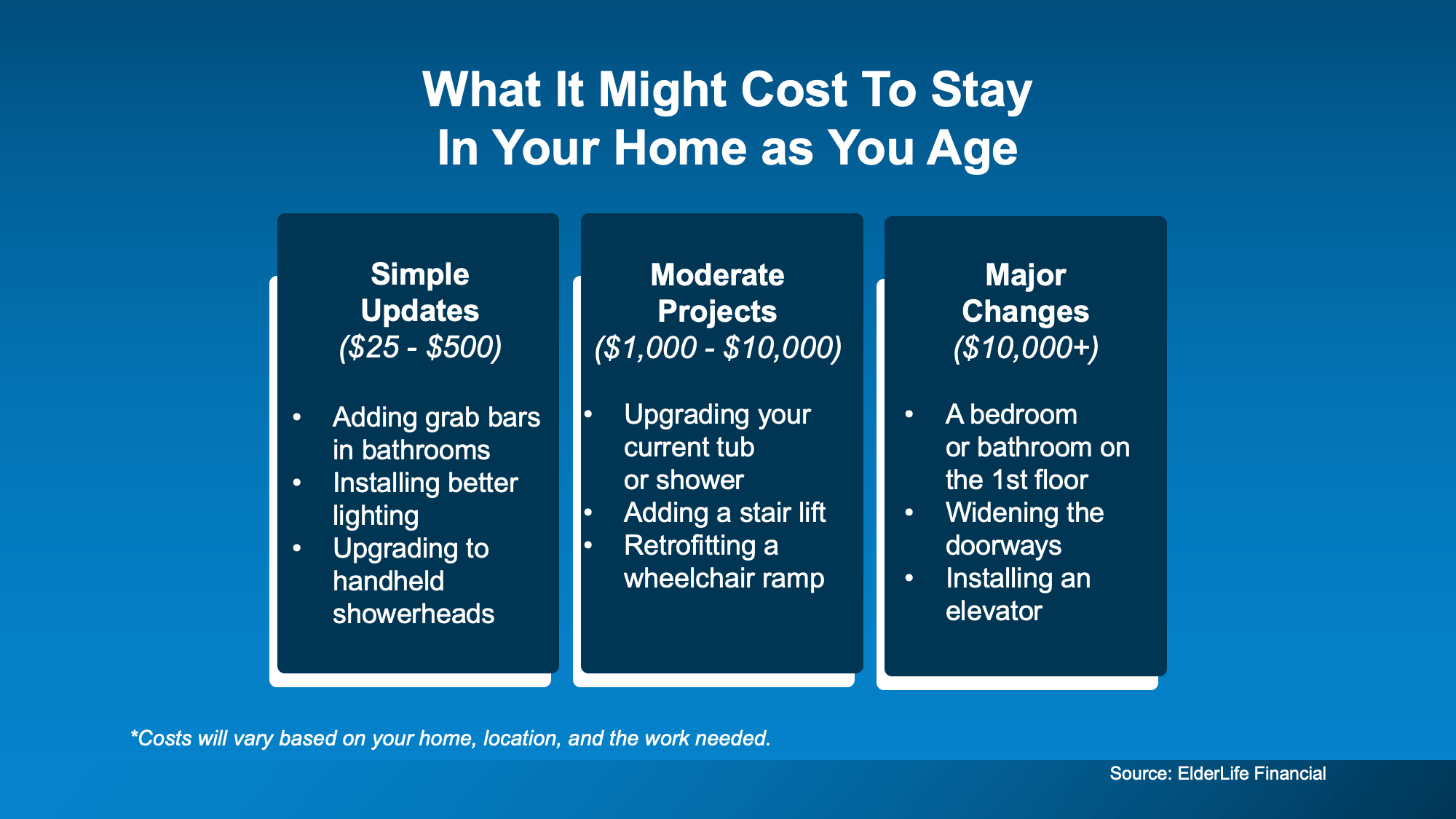

Aging in place is definitely possible. But it’s better if you have a plan. And here’s why. The home that once worked perfectly may need to change with you over the years. And it’s easier if you can anticipate those expenses.

- Sometimes that means small updates: like adding grab bars in the shower.

- Other times, you’ll have to make bigger decisions: like reworking layouts or moving key spaces to the first floor.

Some of those changes are going to be simple. Others can be a meaningful investment. And that’s why thinking about it early matters. Not because you need to decide anything right now, but because it gives you time.

- Time to understand what your home may need.

- Time to explore your options.

- Time to find the right contractors.

- Time to space out the expense of the upgrades.

According to ElderLife Financial, here’s a rough baseline of what it could cost depending on what needs to be done (see below):

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

Just remember, if you’re thinking about making updates, it’s always worth having a quick conversation before you start. A real estate agent can help you understand which changes tend to make sense for your situation and how they may impact your home’s value based on your local market.

When Moving Might Make More Sense

But staying isn’t always the best fit for every situation. According to Pegasus Senior Living:

“While most seniors hope to age in place, practical considerations sometimes make selling a home the wiser choice.”

Sometimes, it comes down to a simple shift: when the home that once made life easier, starts to make it harder.

That might look like:

- Maintenance or yardwork that’s starting to feel overwhelming

- Stairs or layouts that are getting harder to manage day-to-day

- Or needing more support or care or being too far from loved ones

And sometimes, it’s not about necessity at all. It’s about lifestyle. Some homeowners just don’t want to live through major renovations. Others are ready to simplify, downsize, or move somewhere that better fits this next chapter, whether that’s a smaller home, a 55+ community, or a place closer to family.

For them, moving simply means making daily life easier.

Bottom Line

There’s no one-size-fits-all answer here.

Some people stay and make updates. Others move to simplify things. Either can be the right choice. The goal isn’t to pick one today. It’s to understand your options early, so when the time comes, you feel confident instead of rushed.

And if you ever want a sounding board to think through what the future could look like for you, a local real estate agent is there to help.

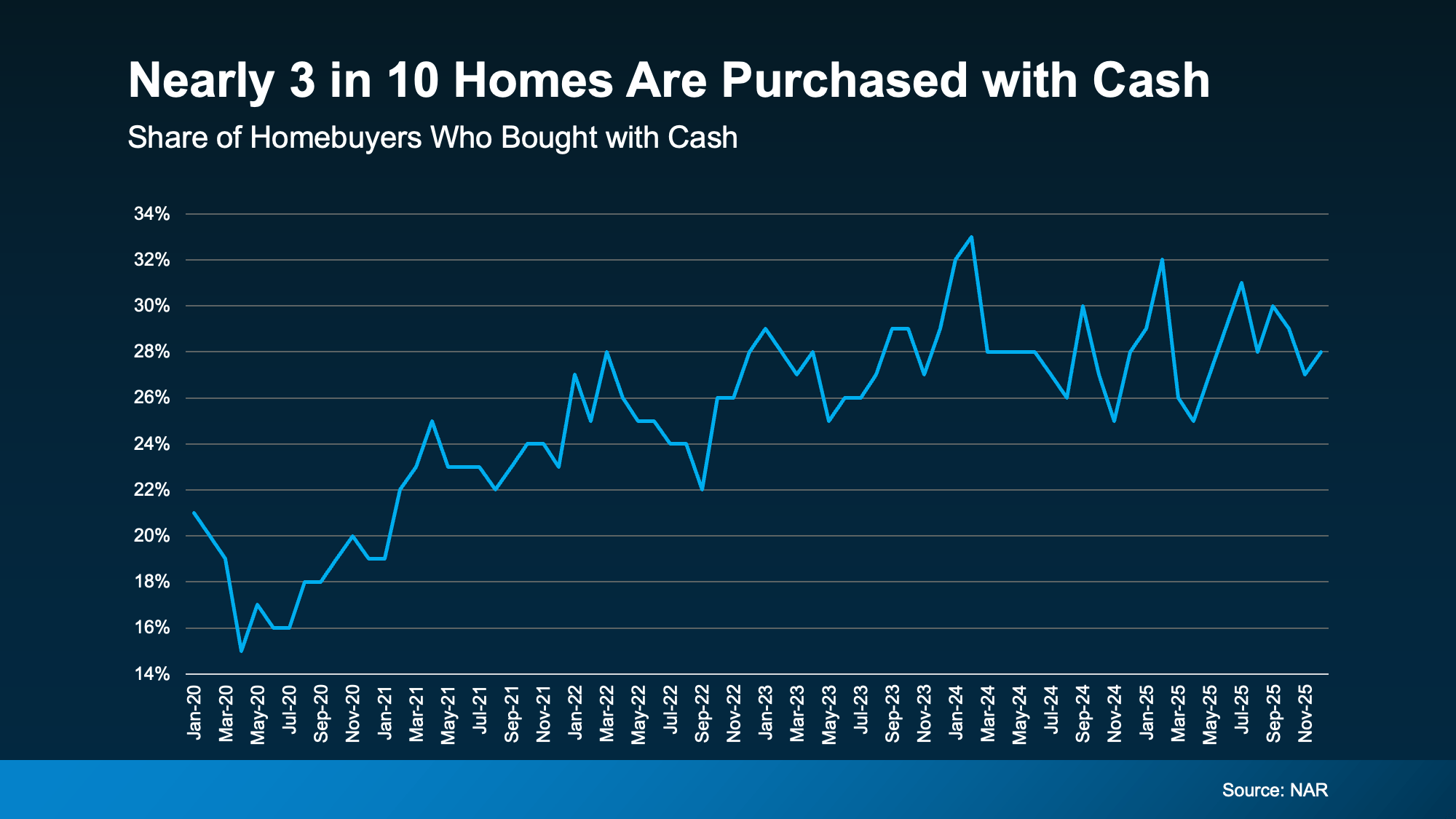

What if you didn’t have a mortgage payment on your next house? It may sound a little unrealistic. But for a number of homeowners, it’s actually doable.

Nearly 3 in 10 homes purchased today are bought in cash, according to the National Association of Realtors (NAR). That’s far more than the pre-pandemic norm (see graph below):

So, how are so many buyers pulling that off? The answer is simple: home equity.

So, how are so many buyers pulling that off? The answer is simple: home equity.

Back in 2020-2021, mortgage rates and the number of homes for sale were both at all-time lows. And that combination pushed home prices up, fast.

If you owned a home during that time, it likely gained significant value – maybe even enough to buy your next house in cash. NAR explains:

“. . . rising home equity has armed many existing homeowners with the financial leverage to make cash offers, allowing them to convert years of price appreciation into immediate purchasing power.”

Here’s why you may want to go that route yourself, if you have enough equity to do it.

1. Your Offer Becomes More Attractive

Sellers value certainty. And an all-cash offer removes one of the biggest unknowns in a transaction: financing. As Rocket Mortgage explains:

“Cash offers are attractive to sellers. Sellers often prefer to work with cash buyers if they can because they don’t have to worry about a buyer’s financing falling through at the last minute.”

In many markets, an all-cash offer can give you a serious edge.

2. You Can Close Faster

And since you don’t have to worry about underwriting, lender approvals, and loan processing, the time it takes to close shrinks. Cotality puts it this way:

“Cash buyers have always enjoyed an edge over borrowers. They remove financing risk, reduce delays, and often close in days rather than weeks.”

If the owner of the house you’re buying is already under contract on their next home or they just need to move fast (like for a new job), that speed is a real draw.

3. You Won’t Have Monthly Mortgage Payments

When you buy in cash, you don’t have to finance your purchase. That means you don’t have to worry about what today’s mortgage rates are and you own the house outright from the day you close. And that’s a big deal.

No mortgage.

No monthly payment.

Full ownership.

That financial freedom opens the door for other big lifestyle benefits. Zillow explains:

“Paying in cash means you own your home outright. This eliminates the need for monthly mortgage payments, freeing up your finances for other priorities like savings, travel, or home improvements.”

4. You May Get a Better Deal

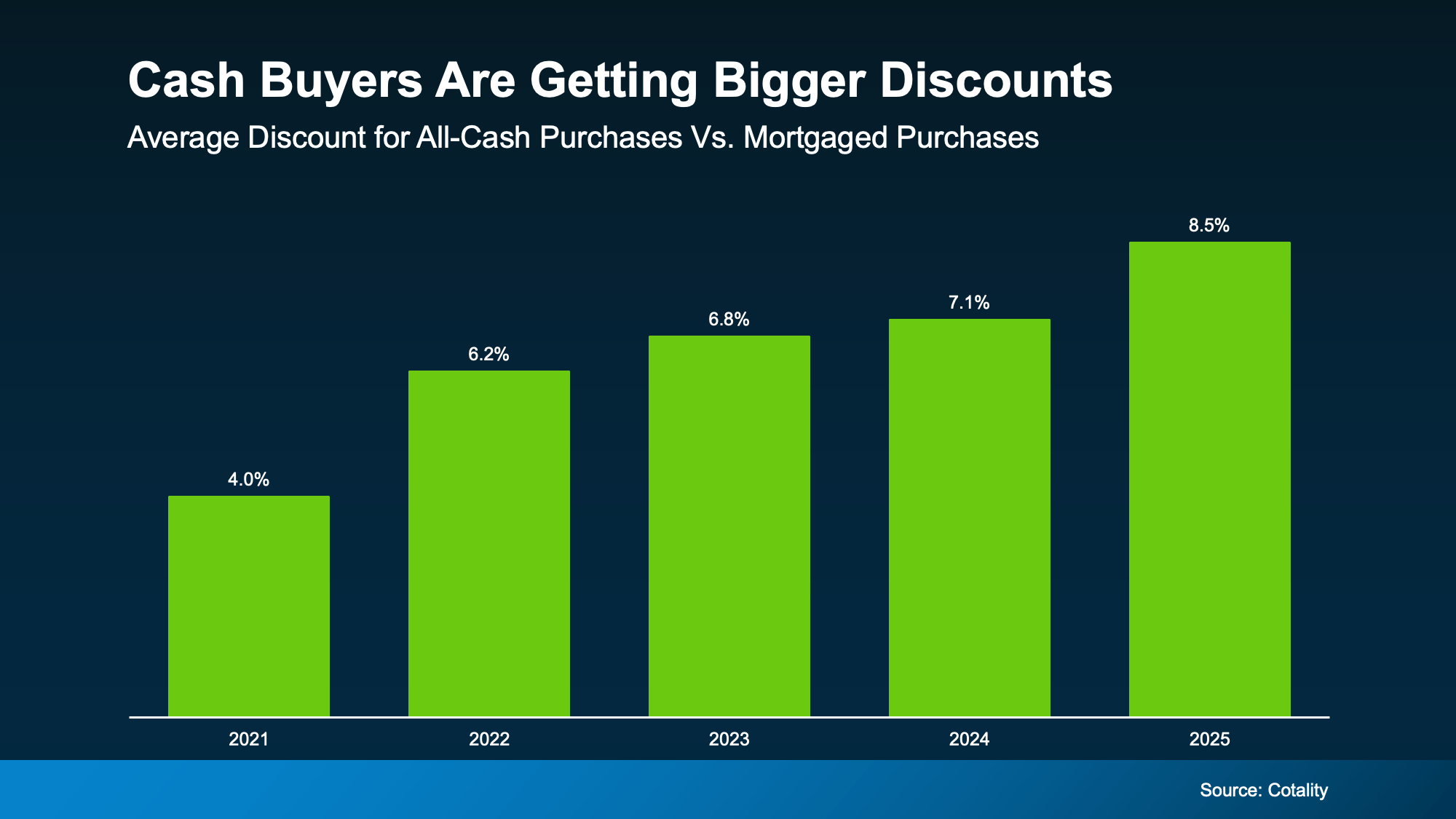

And here’s one more thing that surprises a lot of homeowners: cash buyers often pay less for the house.

According to Cotality, all-cash buyers tend to spend roughly 9% less on the house than buyers who use a mortgage. That’s because some sellers are willing to accept lower offers to get a deal done quickly, with more certainty of closing, and fewer financing hoops to jump through. As Cotality explains:

“From a seller’s point of view, a lower but reliable offer can feel preferable to a higher one that may collapse weeks later.”

And that advantage grows with each passing year (see graph below):

Is an All-Cash Move Realistic for You?

Is an All-Cash Move Realistic for You?

Not every homeowner will buy their next house outright in cash. And that’s okay.

But the bigger takeaway is this: the equity you’ve built may give you more options than you think.

Whether that means downsizing and eliminating a mortgage entirely, or just relocating with stronger negotiating power, your current house may be what makes it possible.

Bottom Line

Before assuming you’ll need another traditional mortgage, it’s worth asking one simple question: How much equity do you really have? Because the answer might change what you thought your next move could look like.

Curious what your home equity could do for you? Ask a local real estate agent to run the numbers and see what kind of buying power you’re really sitting on.

For a growing number of homeowners, retirement isn’t some distant idea anymore. It’s starting to feel very real.

According to Realtor.com and the Census, nearly 12,000 people will turn 65 every day for the next two years. And the latest data shows as many as 15% of those older Americans are planning to retire in 2026. And another 23% will do the same in 2027.

If you’re considering retiring soon too, here’s what you should be thinking about.

Why Downsize?

Now’s the perfect time to reflect on what you want your life to look like in retirement. Because even though your finances will be going through a big change, you don’t necessarily want to feel like you’re living with less.

But odds are, what you do want is for life to feel easier.

Easier to enjoy.

Easier to manage.

Easier to maintain day-to-day.

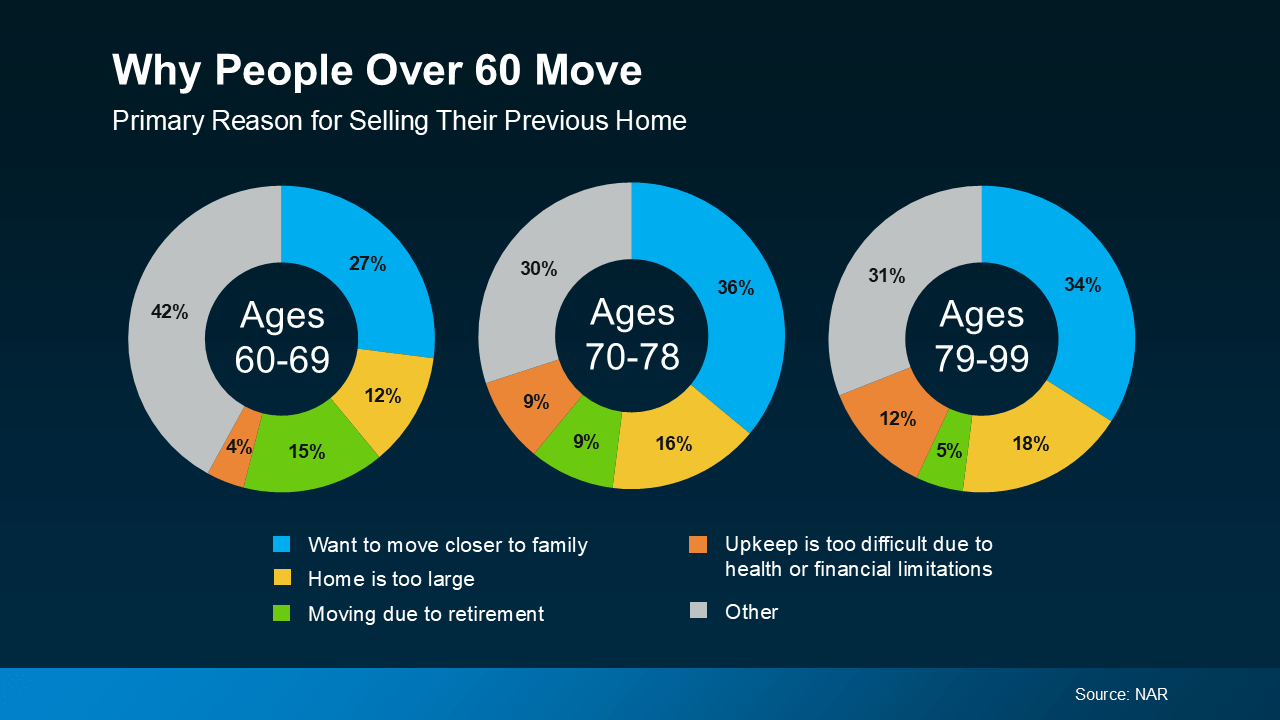

The Top Reasons People Over 60 Move

You can see these benefits show up in the data when you look at why people over 60 are moving. The National Association of Realtors (NAR) finds the top 4 reasons aren’t about timing the market or chasing top dollar. They’re about lifestyle:

- Being closer to children, grandchildren, or long-time friends so it’s easier to spend more time with the people who matter most

- Wanting a smaller, more functional home with fewer stairs and easier upkeep

- Retiring and no longer needing to live near the office, so it’s easier to move wherever you want

- Opting for something smaller to reduce monthly expenses tied to utilities, insurance, and maintenance

No matter the reason, the theme is the same: downsizing isn’t about giving something up. It’s about gaining control and choosing simplicity. And it brings peace of mind to know your home fits the years ahead, not the years behind.

And the best part? It’s more financially feasible now than many homeowners would expect.

The #1 Thing Helping So Many Homeowners Downsize

Here’s the part that makes it possible. Thanks to how much home values have grown over the years, many longtime homeowners are realizing they’re in a stronger position than they thought to make that move.

According to Cotality, the average homeowner today has about $299,000 in home equity. And for older Americans, that number is often even higher – simply because they’ve lived in their homes longer.

When you stay in one place for years (or even decades), two things happen at the same time:

- Your home value has time to grow.

- Your mortgage balance shrinks or disappears altogether.

That combination creates more options than you’d expect, even in today’s market.

So, whether you just retired, or you’re about to, it’s not too soon to start thinking about what comes next. Sure, it can be hard to leave the house you made so many years of memories in, but maybe it’s time to close one chapter to open a new one that’s just as exciting.

Bottom Line

Downsizing is about setting yourself up for what comes next – on your terms.

If retirement is on the horizon and you’ve started wondering what your current house (and your equity) could make possible, the first step isn’t selling. It’s understanding your options.

It’s time to talk to an agent. A simple, no-pressure conversation can help you see what downsizing might look like – and whether it makes sense for you.

Student Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

What Buying or Selling a Home Gives Back to Your Community

Down Payments Are Smaller Than They’ve Been Since 2021

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoTwo Big Reasons To Move This Summer

-

Affordability4 weeks ago

Affordability4 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers3 weeks ago

For Sellers3 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers3 weeks ago

For Buyers3 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

-

Affordability2 weeks ago

Affordability2 weeks agoThat House That’s Been Sitting Could Be Your Best Shot at a Deal

-

Economy2 weeks ago

Economy2 weeks agoMore Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Agent Value3 weeks ago

Agent Value3 weeks agoIs It Still a Seller’s Market? Here’s What the Data Says.

-

Agent Value2 weeks ago

Agent Value2 weeks agoYour House Didn’t Sell. Here’s How To Turn It Around.

You must be logged in to post a comment Login