Agent Value

How To Determine if You’re Ready To Buy a Home

When your house doesn’t sell, it’s not just disappointing. It messes with your timing. Your plans. Your confidence. You start second-guessing everything, including the decision to move in the first place. And that raises 2 big questions:

Do you try again?

Is that even worth it?

Here’s the secret to getting a better outcome the second time around.

Different Agent. Different Results.

Most sellers who re-list and ultimately sell don’t wait for market to magically change. They change their approach. And there’s data to back that up.

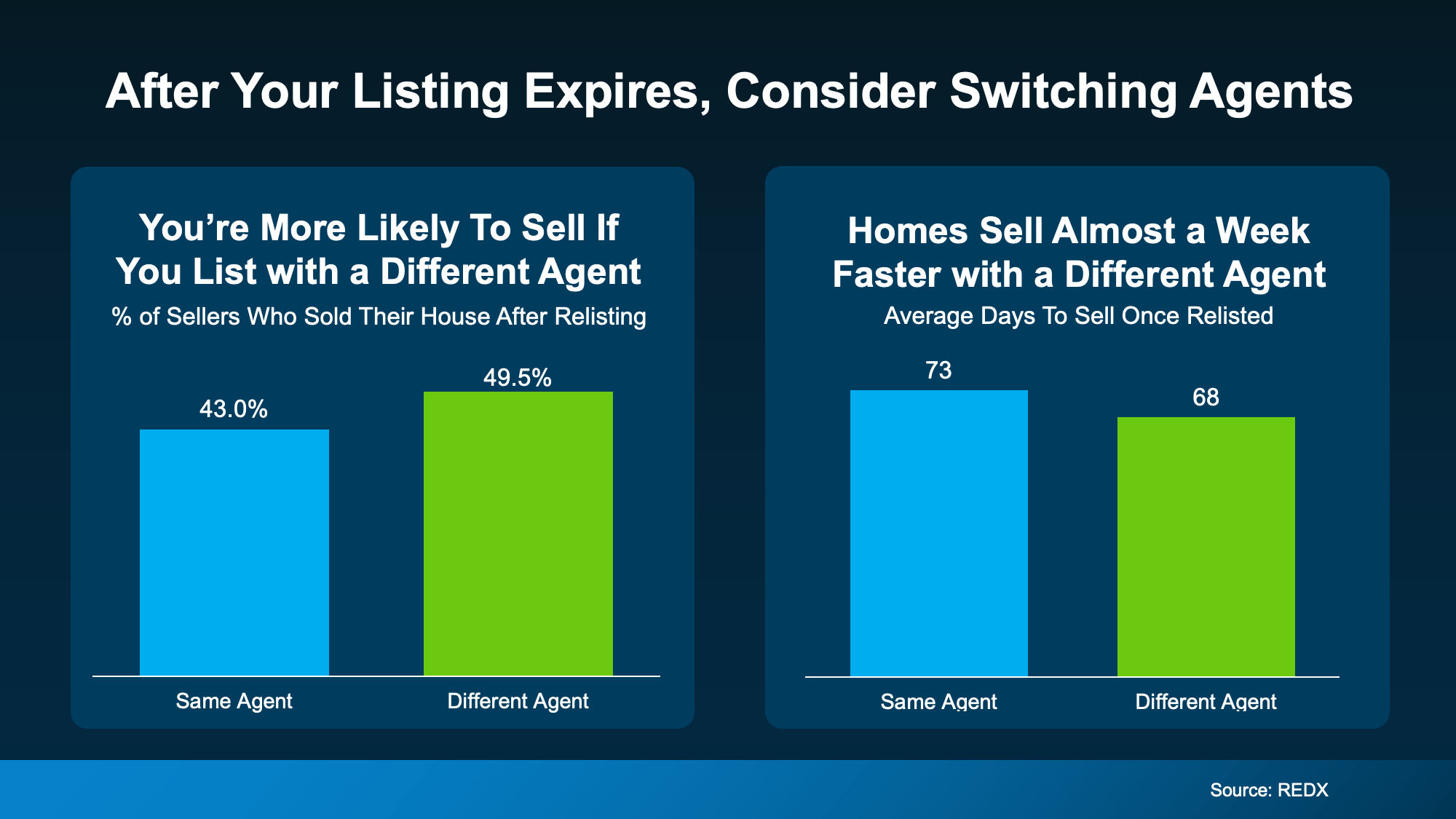

Research from REDX shows homeowners who put their house back on the market with a different agent are more likely to sell than homeowners who re-used the same agent. Not to mention, they see their homes sell faster (see graph below):

That’s the power of a fresh set of eyes. Because in a moment like this, the worst thing you can do is rerun the same set of plays and expect a different outcome. A different agent can bring a new perspective on where things went off track – and a lot of the time, one of these things happened.

1. The Asking Price Didn’t Match Buyer Reality

There’s a saying that’s especially important in today’s market, and it’s: “if your price isn’t compelling, it’s not selling.” Maybe that’s what happened with your house.

With mortgage rates where they are and inflation driving up the cost of everyday purchases, buyers have less room to stretch. If they feel like your house is priced even a little high, it’s going to get skipped over. And if no one looks at it, it’s not going to sell.

The Fix: Price to draw buyers in, not push them away. Have an agent pull fresh data from recent sales so your asking price matches what buyers are actually paying right now.

2. The First Impression Didn’t Win the Click

Most buyers decide whether they want to tour a home in seconds. If the photos look dark, or dated, they scroll right past. And while you may think: “If they just saw it in person, they’d get it,” you may not get that chance.

And honestly, even in person, small things can quietly kill momentum – worn down paint, outdated fixtures, clutter, or a yard that feels high-maintenance. Individually, they’re small. Stacked together, they create doubt.

The Fix: Walk the house like you’re a buyer, not the owner. Start with what’s easy and obvious – paint, lighting, curb appeal, decluttering. Then update the photos so they match the best version of your house.

3. The Marketing Was Too “Set It and Forget It”

Today, the number of homes for sale has grown in many areas. Buyers have more options, which means your house needs a plan to stand out. A generic description and a basic upload to the MLS can blend in fast.

The Fix: Find an agent who can build stronger exposure through digital marketing and social platforms, plus content that makes buyers stop – strong photos, a smart description, a video walk-through, and a plan for open houses and follow-up.

4. There Was No Clear Plan for Feedback

Sometimes the house gets showings, but no offers. If that was your experience, it actually tells you something important. Buyers liked it enough online to come see it. So, something else was holding them back.

Those buyers were sending a message. It just wasn’t translated into action.

The Fix: Make sure your agent has a clear plan for seeking out and acting on feedback quickly. That dialogue often points to the one change that would get a house sold.

5. The Deal Couldn’t Get Over the Finish Line

Even when a house is priced well and marketed right, deals fall apart when there’s no plan for the human side of the transaction.

Buyers today are more likely to ask for repairs, credits, or help with closing costs than a few years ago. In this type of market, being unwilling to negotiate can cost you more than a reasonable concession ever would.

The Fix: Decide ahead of time what matters most to you and where you can be flexible. Keep the dialogue open and lean on your agent for advice.

Bottom Line

If your house didn’t sell the first time, you’re not stuck. You just need a different strategy, and maybe a different partner.

When you’re ready for a fresh set of eyes on what happened and what to change first, connect with a local agent.

Remember a few years back when sellers held all the power and buyers were stuck offering way over asking or waiving inspections just to get a chance at the house? In many markets, those days are behind us.

While it’s going to vary by area, more metros are slowly shifting to favor buyers, and the market is starting to look a lot more like a two-way street again.

And that balance is something we haven’t had in a while.

Whether you’re buying or selling, here’s what you need to know about what’s changing and what it means for your move.

The Most Buyer-Friendly Market in Years

The national data tells an interesting story right now. According to Realtor.com:

“The national housing market is balanced but gradually loosening as the cycle moves in a more buyer-friendly direction . . .“

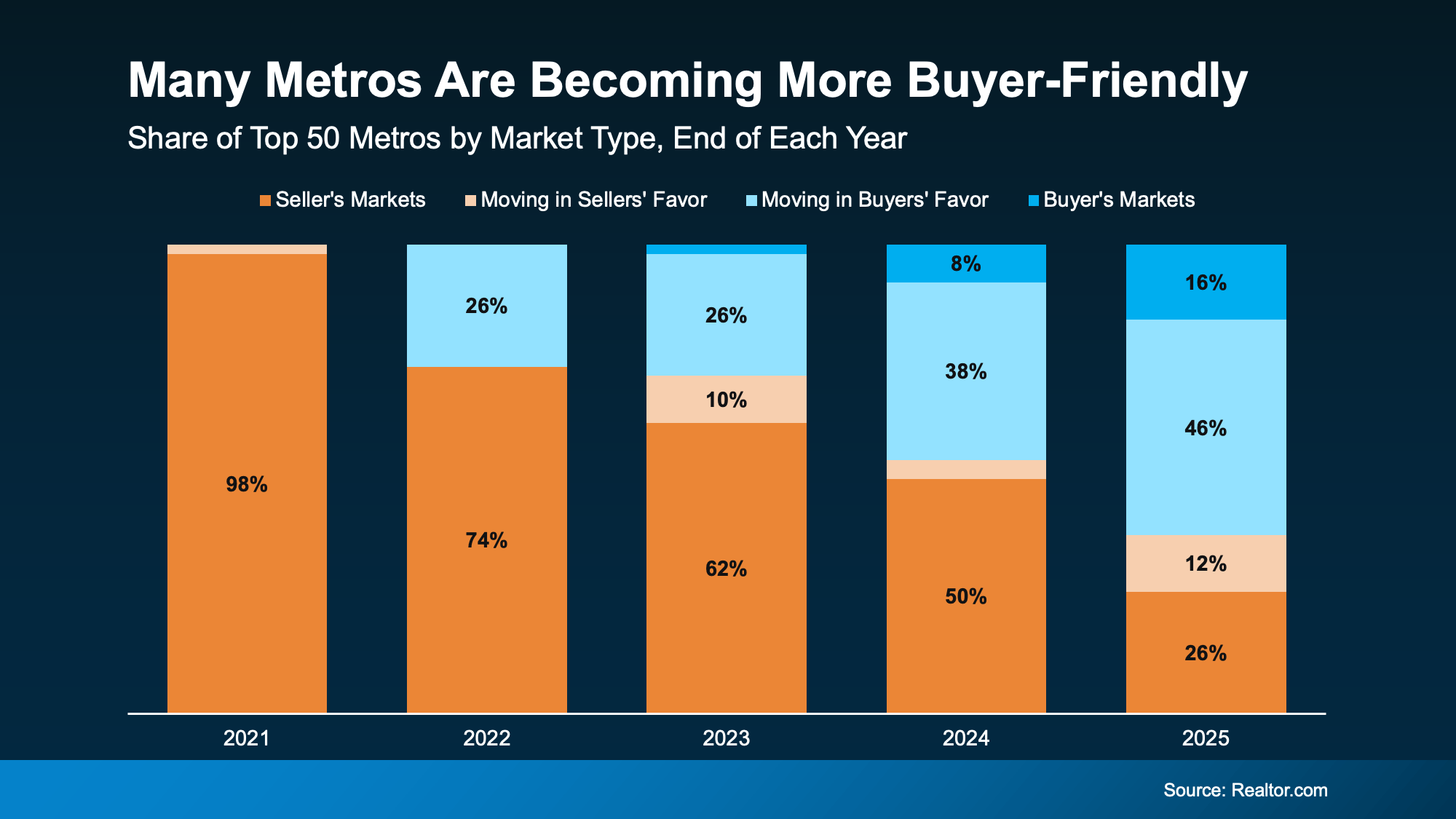

That’s because, over the past few years, more and more metros have been flipping back to more buyer-friendly terms as inventory’s grown. And when you zoom in on the latest Realtor.com data for the top 50 metro markets over time, the trend becomes really clear (see graph below).

Back in 2021, almost all major metros were seller’s markets. By the end of 2025, only 1 in 3 still favored sellers. That’s an obvious shift.

And that changes how the market is going to feel for everyone. Sellers shouldn’t still expect 2021 conditions, but neither should buyers. At least, not generally speaking.

It’s Not the Same Story Everywhere

That said, who has the power ultimately depends on where you live. While more metros are leaning buyer-friendly lately, there are still plenty of strong seller’s markets right now, too.

It really comes down to how much housing supply and demand there is in your area. And that varies enormously by region.

Sun Belt cities like Austin, Tampa, and San Antonio saw major building booms in recent years, giving buyers more options and more negotiating room. Meanwhile, cities in the Northeast and Midwest – think Rochester, Hartford, and Buffalo – didn’t see that same wave, so inventory stayed tight and competition stayed fierce. As Jeff Ostrowski, Housing Analyst at Bankrate, explains:

“The formerly hot Sun Belt markets have cooled, while the Northeast and Midwest have stayed hot. The big driver here is construction activity. The softest markets now [have] experienced big booms that spurred new building, and that has led to a large supply of new and existing homes on the market in those places.”

Practical Advice for Your Move

To find out who has the power in your local market, talk to an agent. Because knowing what’s happening locally is going to be the key to setting the right strategy for your move.

If the market is working in your favor, great. Lean in and use it to your benefit. But if it’s not, all hope isn’t lost. Your agent can help you figure out how to approach any market.

Here’s some practical advice if there’s a mismatch between your goal and local market conditions.

If you’re buying in a seller’s market:

-

Get pre-approved before you start shopping. It shows sellers you’re serious.

-

Be ready to act fast when the right home hits the market.

-

Consider offering a quick closing date or flexible terms.

-

Work closely with your agent to craft a competitive offer.

If you’re selling in a buyer’s market:

-

Price it right from day one. Overpricing will cost you time and money.

-

Focus on curb appeal and staging to stand out in areas with more inventory.

-

Be open to offering incentives, like covering closing costs or a home warranty.

-

Expect buyers to negotiate and be ready to be flexible.

Bottom Line

Right now, local markets are moving in very different directions. And your strategy as a buyer or seller should reflect your market.

Want to know which way your local market is leaning and what that means for your move? Talk to a local real estate agent.

Whether you’re dreaming about buying your first home or wondering if it’s time to move on from the one you’re in, affordability is probably weighing on your mind. Home prices are still high in many markets, and even though things have improved a bit over the past year, making the numbers work can still feel like a stretch.

But the people finding ways to move right now usually have one thing in common. They didn’t wait for affordability to come to them. They went looking for it.

According to PODS, 61% of people across all generations say affordability is the biggest factor when deciding where to move. And it’s led a growing number of people to do one thing – broaden their search to include more affordable areas they hadn’t seriously considered before. As PODS, put it:

“. . . moving is increasingly driven by affordability, connection, and quality of life. As economic pressures persist, Americans are taking a more intentional, values-driven approach to where they choose to live.”

It’s Not Just the Home Price – It’s the Whole Cost of Living

Here’s where it gets really interesting. When people talk about moving for affordability, they’re not just talking about finding a cheaper house. They’re thinking about the full picture. What does it actually cost to live somewhere?

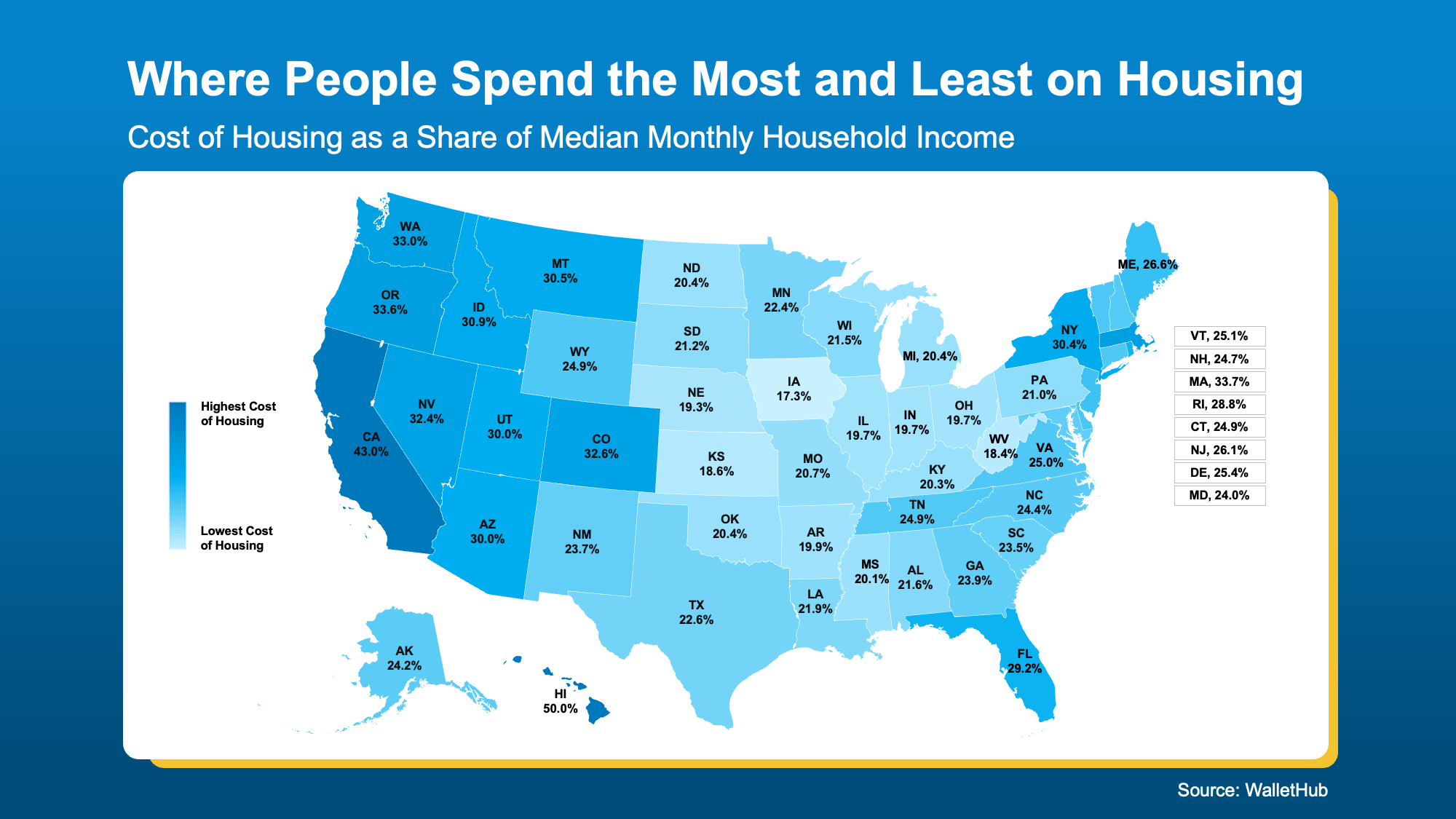

WalletHub looked at exactly this, measuring housing costs as a share of median monthly household income across every state (see map below).

Take a look at where you live on that map. The lighter the blue, the more affordable it generally is to live there. The darker the blue? Just the opposite.

If your state is showing up on the darker blue end of the scale, the cost of living may be putting a real pinch on your wallet, and it may be worth exploring what a lighter-blue area could mean for your finances.

Because if you’re less financially stretched, imagine how that could change things. Less stress. Less worry. More freedom and peace of mind.

You Don’t Have To Move to Another State To Find a Better Deal

But finding more affordable homeownership doesn’t have to mean a cross-country move. It doesn’t even have to mean leaving your state, your family, or your favorite coffee shop behind.

Every market has more affordable pockets that most buyers never think to explore – neighborhoods, towns, and communities where home prices are lower, property taxes are more manageable, and the overall cost of living just works better.

A great local real estate agent knows exactly where those places are.

And if you work remotely, or have any flexibility in where you’re based, your options open up even further. Remote work has already changed the way millions of people think about where to live, and that trend isn’t going away.

When location stops being tied to a daily commute, a more affordable area that’s a bit farther out suddenly becomes a very real option.

Bottom Line

Affordability is a real challenge, but it’s not an unsolvable one. The key is being open to places you might not have considered before. A local real estate agent can help you find them.

Ready to find out which areas have the best affordability right now? Reach out today.

Your House Didn’t Sell. Here’s How To Turn It Around.

More Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

That House That’s Been Sitting Could Be Your Best Shot at a Deal

-

Affordability3 weeks ago

Affordability3 weeks agoWhat Rising Inflation Means for Your Move

-

Economy3 weeks ago

Economy3 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability3 weeks ago

Affordability3 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Affordability4 weeks ago

Affordability4 weeks agoLess House, More Home: Why Smaller Homes Are Paying Off for Today’s Buyers

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoTwo Big Reasons To Move This Summer

-

Affordability2 weeks ago

Affordability2 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers2 weeks ago

For Sellers2 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers1 week ago

For Buyers1 week agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

You must be logged in to post a comment Login