Buying Tips

Today’s Biggest Housing Market Myths

Have you ever heard the phrase: don’t believe everything you hear? That’s especially true if you’re thinking about buying or selling a home in today’s housing market. There’s a lot of misinformation out there. And right now, making sure you have someone you can go to for trustworthy information is extra important.

If you partner with a real estate agent, they can clear up some common misconceptions and reassure you by backing them up with research-driven facts. Here are just a few misconceptions they can help disprove.

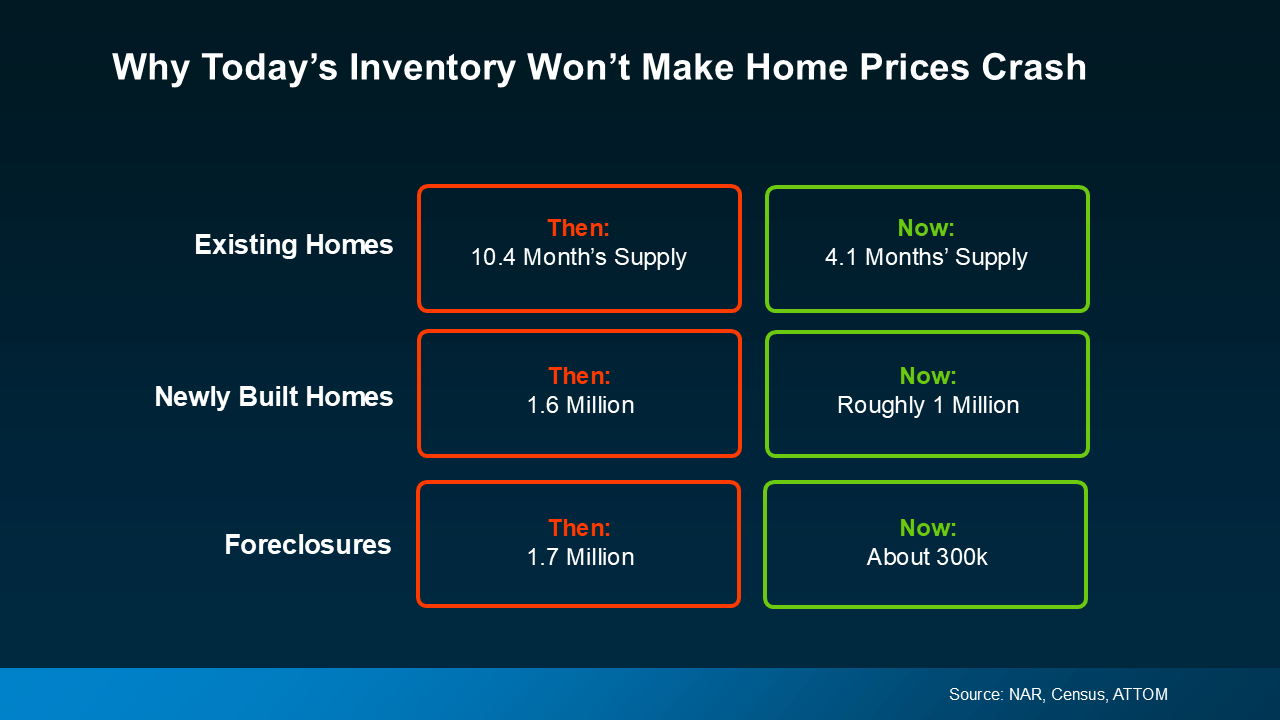

1. I’ll Get a Better Deal Once Prices Crash

If you’ve heard home prices are going to come crashing down, it’s time to look at what’s actually happening. While prices vary by local market, there’s a lot of data out there from numerous sources that shows a crash is not going to happen. Back in 2008, there was a dramatic oversupply of homes that led to prices crashing. Across the board, there’s an undersupply of homes for sale today. That makes this market a whole different scenario (see chart below):

So, if you think waiting will score you a deal, know that data shows there’s not a crash on the horizon, and waiting isn’t going to pay off the way you’d hoped.

So, if you think waiting will score you a deal, know that data shows there’s not a crash on the horizon, and waiting isn’t going to pay off the way you’d hoped.

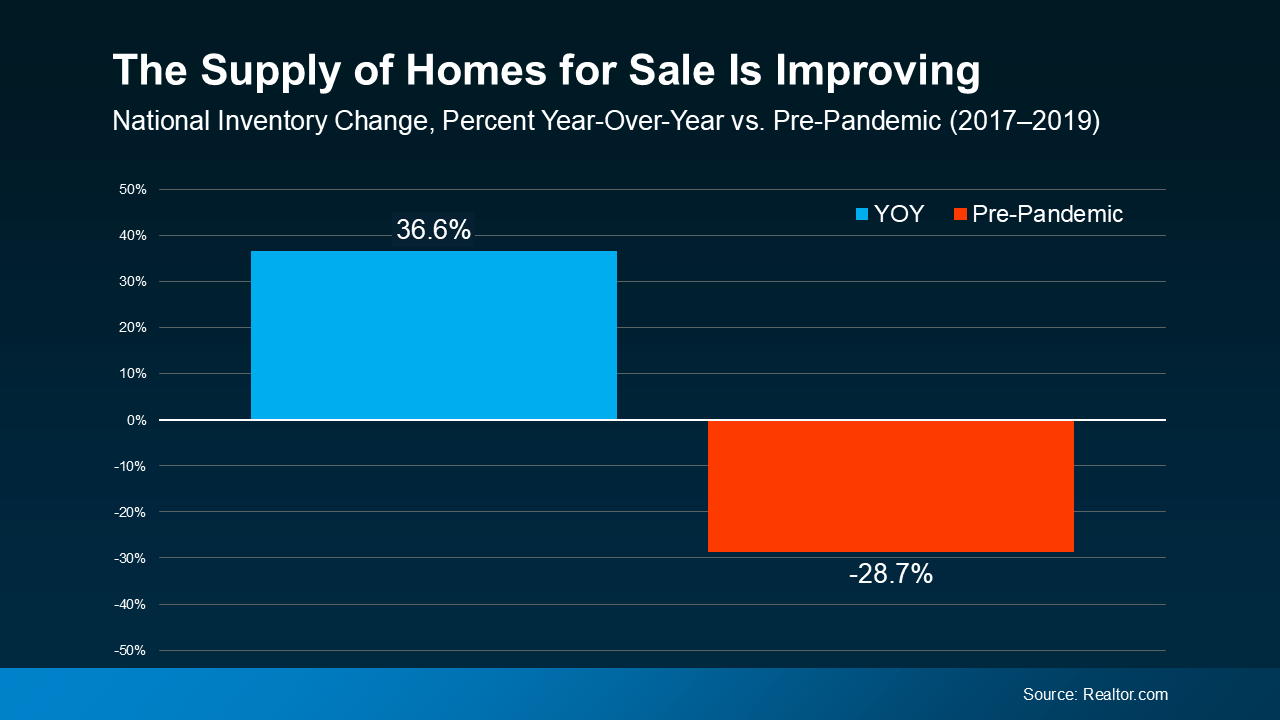

2. I Won’t Be Able To Find Anything To Buy

If this nagging fear about finding the right home if you move is still holding you back, you probably haven’t talked with an expert real estate agent lately. Throughout the year, the supply of homes for sale has grown. Data from Realtor.com helps put this into context. While there are still fewer homes on the market than in a more normal year like 2019, inventory is still above where it was at this time last year (see graph below):

So, if you’re remembering all that media coverage about record-low supply during the pandemic, you can rest a bit easier. While the market isn’t back to normal just yet, inventory is moving in a healthier direction. And that means as your options improve, you can let go of this now outdated myth because finding a home to buy won’t feel quite so impossible anymore.

So, if you’re remembering all that media coverage about record-low supply during the pandemic, you can rest a bit easier. While the market isn’t back to normal just yet, inventory is moving in a healthier direction. And that means as your options improve, you can let go of this now outdated myth because finding a home to buy won’t feel quite so impossible anymore.

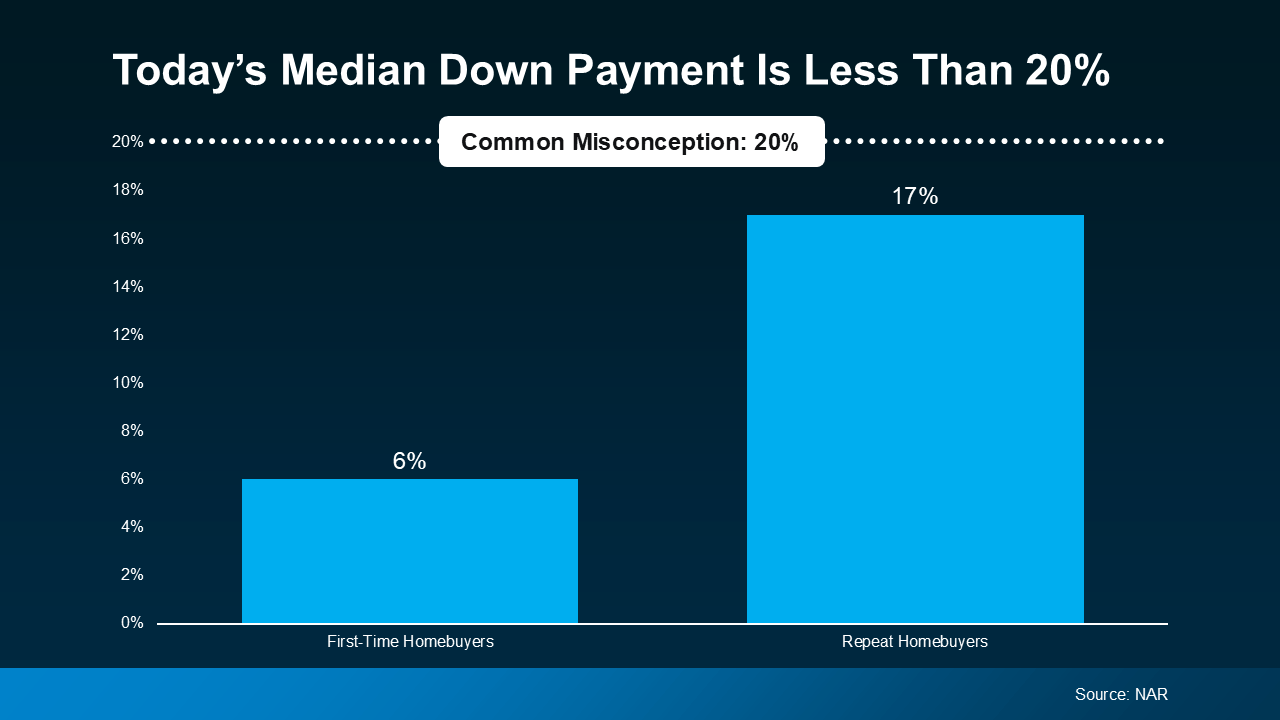

3. I Have To Wait Until I Have Enough for a 20% Down Payment

Many people still believe you need a 20% down payment to buy a home. To show just how widespread this myth is, Fannie Mae says:

“Approximately 90% of consumers overstate or don’t know the minimum required down payment for a typical mortgage.”

And if you look at the data from the National Association of Realtors (NAR), you can see the typical homeowner isn’t putting down as much as you might expect (see graph below):

First-time homebuyers are typically only putting down 6%. That’s far less than the 20% so many people think they need. And if you’re looking at that graph and you’re more focused on how the number for repeat buyers is closer to 20%, here’s what you need to realize. That’s only because they have so much equity built up in their current house that can be used to make a larger down payment for their next move.

This goes to show you don’t have to put 20% down, unless it’s specified by your loan type or lender. Many people put down a lot less. Not to mention, depending on the type of home loan you get, you may only need to put 3.5% or even 0% down. So, if you’re buying your first home, you likely don’t need nearly as much for your down payment as you may think.

An Agent’s Role in Fighting Misconceptions

If you put your move on pause because you heard one or more of these myths yourself, it’s time to talk to a trusted agent. An expert agent has more data and the facts, just like this, to reassure you and help break through any misconceptions that may be holding you back.

Bottom Line

If you have questions about what you’re hearing or reading, connect with a real estate agent. You deserve to have someone you can trust to get the facts.

Student loans are back in the spotlight. And whether you’ve been following the headlines closely or just catching bits and pieces here and there, there’s a good chance they’ve been on your mind lately.

And if you’re questioning whether you have to hit pause on your plans to buy a home, here’s the thing you have to remember:

Having student loans doesn’t automatically mean buying a home has to wait.

The Biggest Myth About Student Loans and Buying a Home

One of the most common misconceptions among first-time buyers is that they have to pay off their student loans before they can qualify for a mortgage. But in most cases, that’s just not true.

As an article from Redfin explains, student loans usually get evaluated the same way other debts do, like credit cards or car payments:

“Yes, you can get a mortgage with student loan debt. Lenders primarily assess your debt-to-income (DTI) ratio, which compares your monthly debt payments, including student loans, to your gross monthly income. Having student debt doesn’t automatically disqualify you if your DTI is within acceptable limits.”

So having that loan on your credit report isn’t some special red flag that immediately disqualifies you.

Instead, lenders look at your overall financial situation, including your income, credit history, and more. Student loans are one piece of that puzzle, but they’re not the entire picture.

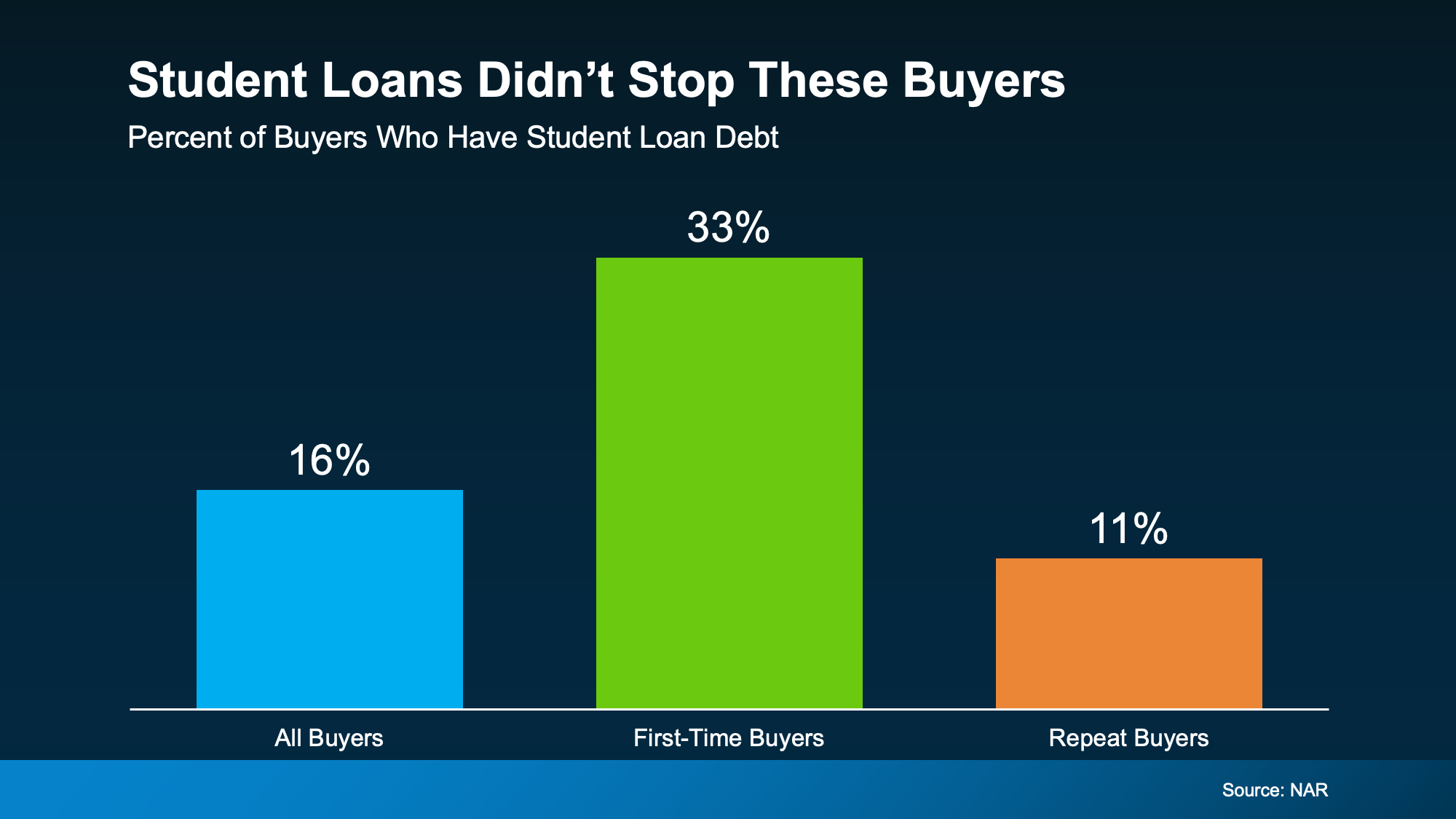

You’re in Better Company Than You Think

Just to really drive this home, here’s a stat from the National Association of Realtors (NAR) that proves you can have student debt and still buy a home. Their research shows 33% of first-time homebuyers still had student loan debt.

That’s 1 out of every 3 first-time buyers. The median amount they owed? $30,400.

Let that reassure you that people are buying homes with student debt every day. And carrying student loans doesn’t automatically put homeownership out of reach.

Don’t Count Yourself Out Before You Even Try

At the end of the day, here’s where a lot of buyers trip themselves up. They assume the worst and never even check what they could actually qualify for. But your situation is more unique than a blanket “no.”

If your income is steady and the rest of your finances are in decent shape, buying a home could be more realistic than you think. The only way to know for sure is to actually run the numbers with someone who does this for a living.

You may discover you’re closer to buying than you think.

Bottom Line

Student loans don’t have to be the thing standing between you and owning a home. If you’ve been putting off your homebuying plans because of that debt, talk to a lender about your options. It may not be the barrier you think it is.

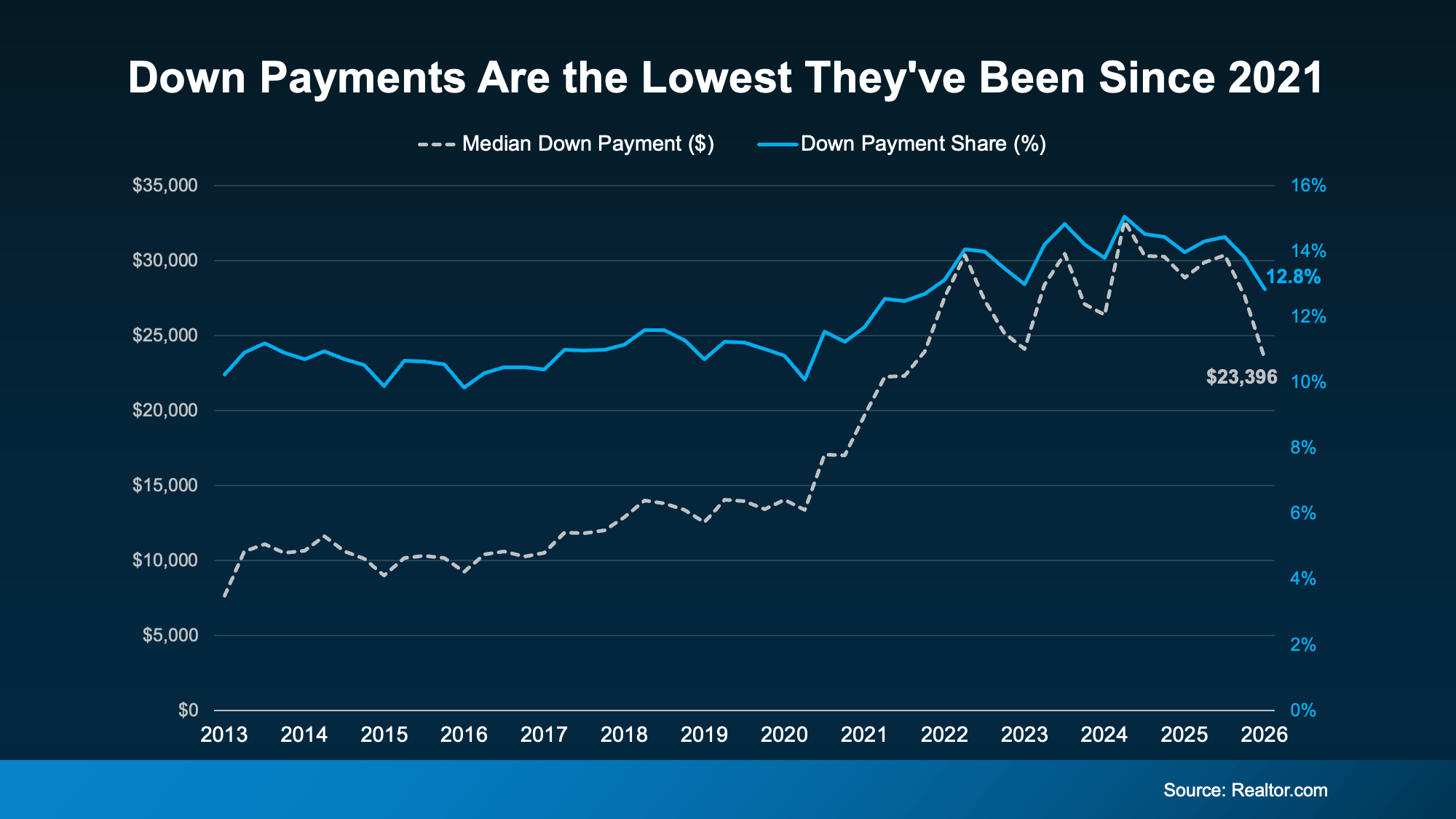

Saving for a down payment can feel like the hardest part of buying a home. And with affordability as tight as it’s been lately, it’s fair to wonder how anyone manages it right now. Here’s something you may not have seen coming.

Some people are getting their foot in the door with a smaller down payment.

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that’s around $5,000 below what was typical the year before (a 19% drop year over year). That’s the lowest down payments have been since 2021 (see graph below):

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

There are a few things driving the trend:

-

Less competition between buyers. Part of it comes down to a more balanced market. With buyers facing less competition than they did a few years ago, there’s less pressure to put a big sum down just to stand out.

-

More moderate home prices. Your down payment is a percentage of the purchase price. So, as price growth cools, the amount you need to put down may change too. In a lot of markets, prices have slowed or leveled off, and some areas are even seeing slight dips. That can translate into smaller down payments.

-

Buyers opting for loans with lower down payments. More buyers are also turning to government-backed loans, like FHA and VA, which often need little or no money down. FHA loans have made up more than 24% of purchase mortgages for five straight quarters, and VA loans recently hit their highest share in over a decade, according to Mortgage Professional America.

But even a smaller down payment is still a significant chunk of cash, and saving it can be hard. So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

Help You May Not Know You Qualify For

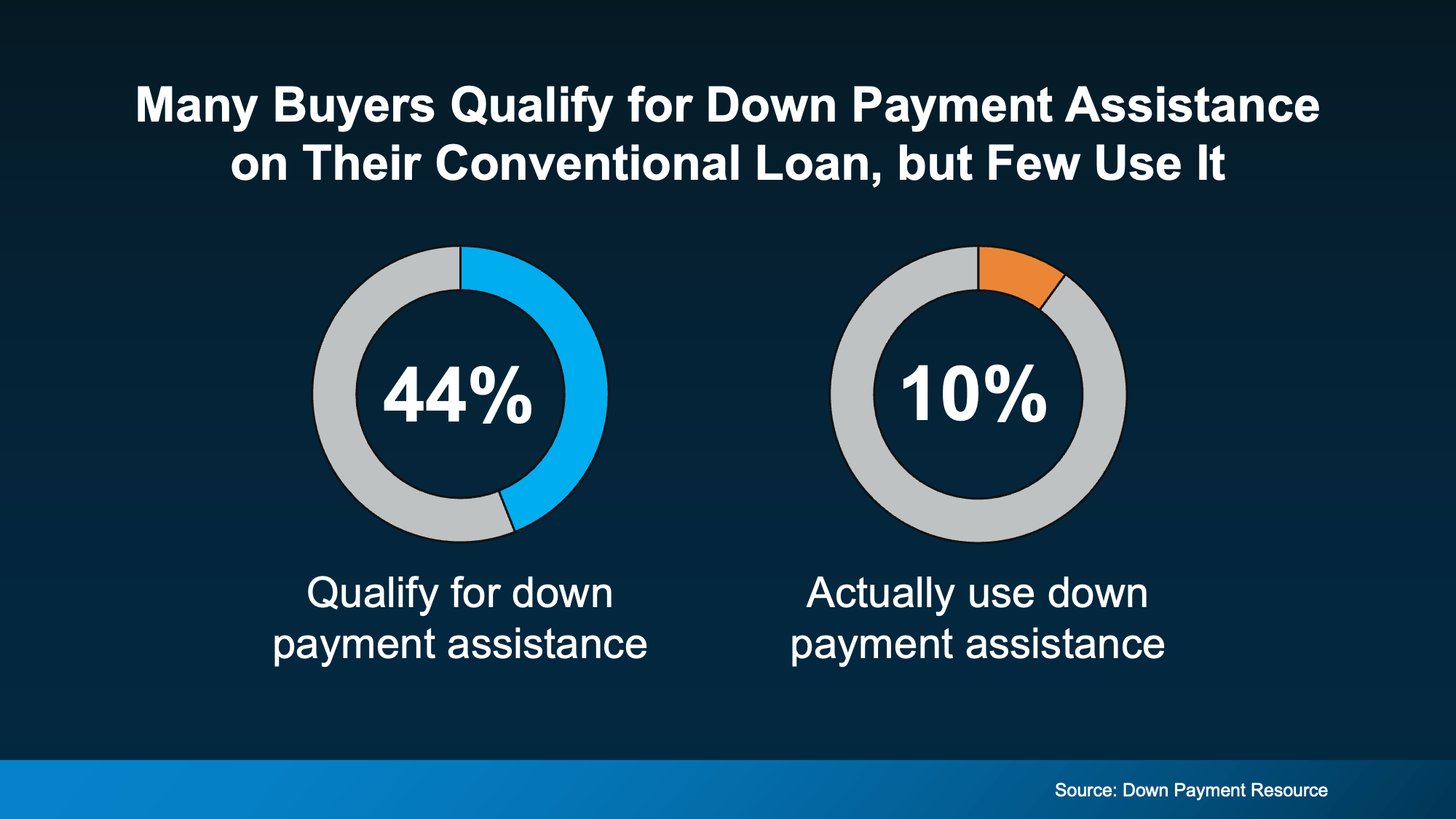

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

-

There are more than 2,600 down payment assistance programs available

-

More than half (62%) are designed to help first-time buyers

-

38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

-

62% are open to buyers earning $100,000 or more

A Boost from Loved Ones

For a growing number of buyers, help comes from closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support most often goes toward the down payment, followed by help qualifying for a mortgage and covering closing costs. Chris Birk, VP of Mortgage Insight at Veterans United, puts it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, it can make a real difference in how soon you can buy.

Bottom Line

Down payments are smaller than they’ve been in years, and that opens the door for more buyers.

And with added help from assistance programs and a little help from loved ones, you may have more ways forward than you realized. Connect with a trusted lender to talk through your options.

You’ve probably heard that home prices are cooling off. And that’s true – nationally. But zoom in on individual markets across the country, and the picture looks completely different depending on where you are.

Some areas are still seeing solid price growth. Others have gone flat. A few have actually dipped slightly negative. So, what’s causing all of that variation?

It All Comes Down to Inventory

Here’s the simple version:

-

When there are more homes for sale, buyers have options.

-

More options, means less competition.

-

Less competition means sellers can’t push prices as high.

On the flip side, when inventory is tight, buyers are competing over a small pool of homes, and that pushes prices up.

That dynamic is playing out right now in a really visible way across the country.

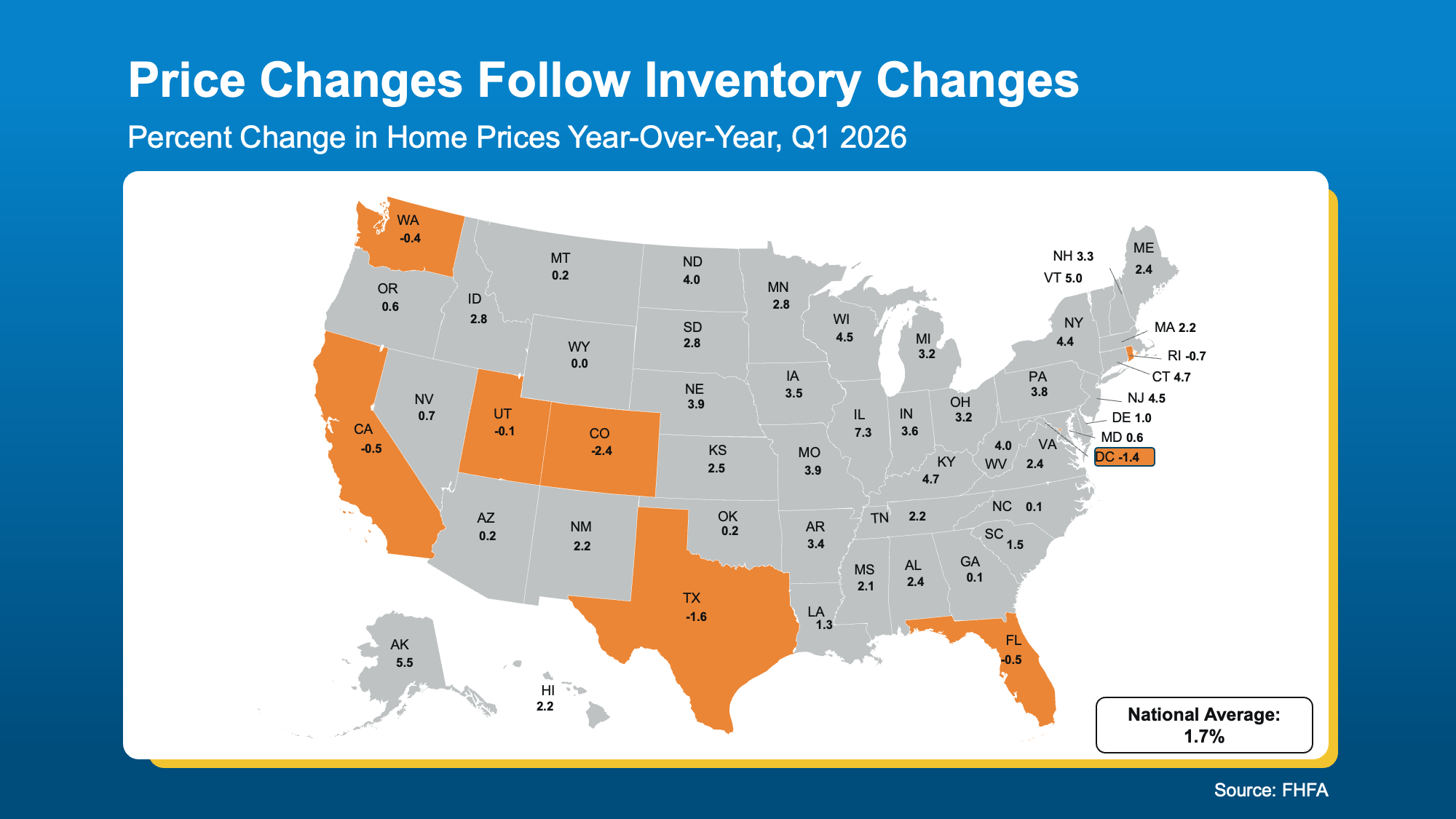

Markets where inventory has climbed back to, or above, normal pre-pandemic levels are seeing prices flatten or fall slightly. Markets where inventory is still well below those 2019 benchmarks are still seeing prices rise. As Lance Lambert, CEO of ResiClub, puts it:

“Home prices are still climbing a little year-over-year in many regions where active inventory remains well below pre-pandemic 2019 levels, such as pockets of the Northeast and Midwest.

In contrast, some pockets in states like Texas, Florida, and Colorado — where active inventory exceeds pre-pandemic 2019 levels by a solid clip — are seeing modest home price pullbacks or flat pricing.”

The Maps Say It All

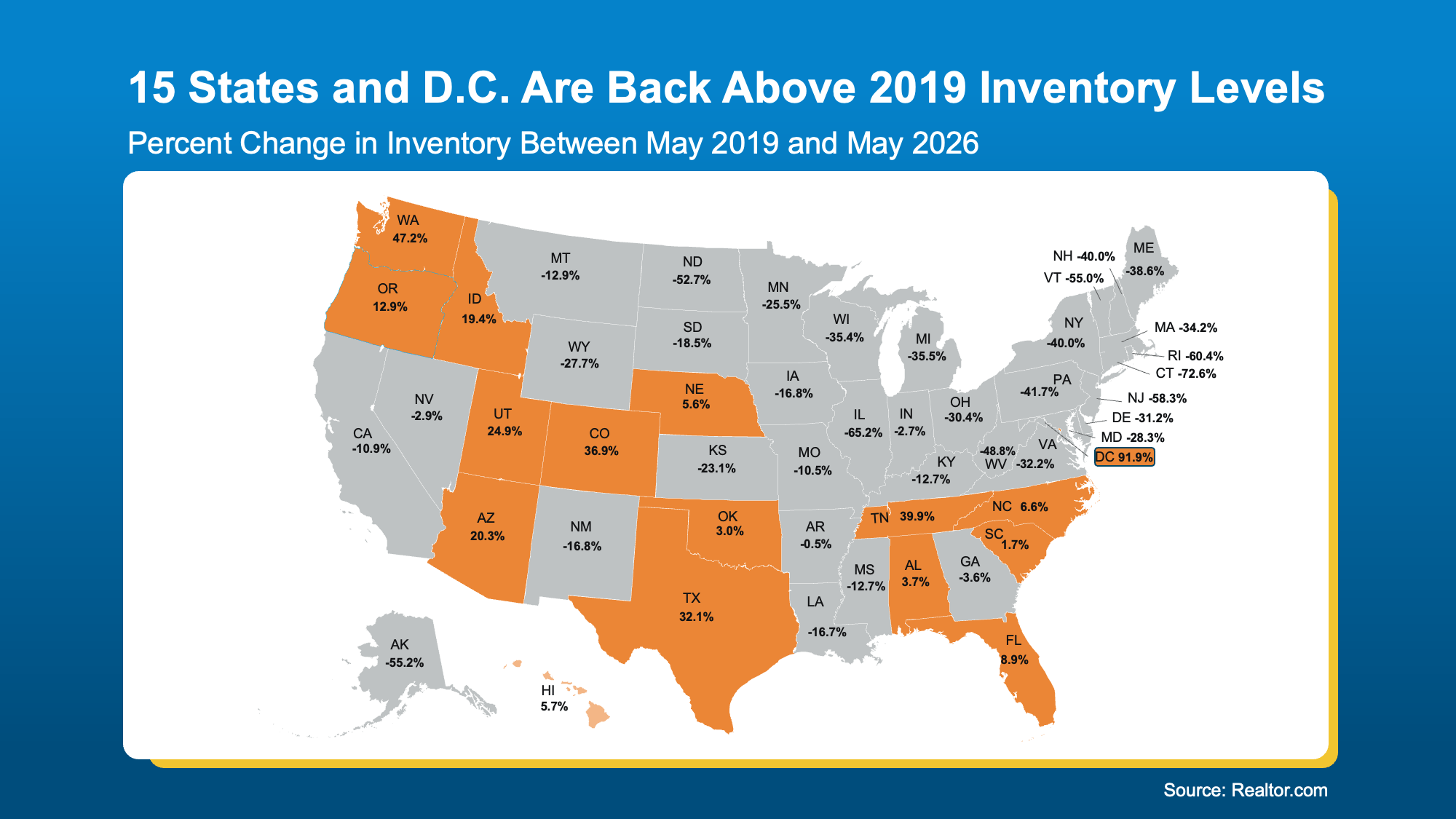

Take a look at where inventory stands today compared to 2019. In most places (the states in gray below), inventory still falls short of where we were back then. And that’s exactly why prices are climbing, albeit moderately, in the vast majority of states.

But you’re probably more interested in where prices are falling a bit, since that’s what is making headlines. So, let’s prove out how much inventory affects prices in those spots.

According to Realtor.com, 15 states and Washington, D.C. are now back above pre-pandemic inventory levels, and some by a wide margin (see the orange in the map below):

Now, let’s look at the latest Federal Housing Finance Agency (FHFA) data to see what’s happened to home prices in those same states over the past year (again, you’ll want to focus on the orange in the next map).

Now, let’s look at the latest Federal Housing Finance Agency (FHFA) data to see what’s happened to home prices in those same states over the past year (again, you’ll want to focus on the orange in the next map).

See how those line up pretty closely with the areas seeing more homes for sale today?

The overlap isn’t a coincidence. It’s cause and effect.

The national average of 1.7% price growth is accurate, but it’s an average of two very different stories happening at the same time – the few areas experiencing mild declines and the overwhelming majority that are still seeing prices rise.

What This Means If You’re Buying or Selling

If you’re a buyer, the market you’re shopping in matters a lot right now. In places like Texas, Colorado, or Florida, you may have real negotiating power – more choices, less competition, and sellers who are more motivated to make a deal. In tighter markets like much of the Northeast, you’re still likely facing a lot of competition.

If you’re a seller, pricing strategy is everything. In markets where inventory has risen, overpricing is one of the fastest ways to linger on the market and eventually sell for less than you would have with the right price from day one. In markets where inventory is still low, you’re in a strong spot, but getting your price right still matters if you want to attract serious buyers quickly. Either way, that’s where a local real estate agent earns their keep.

Bottom Line

When it comes to prices, where you are matters more than ever right now, and a local real estate agent is the best person to help you make sense of it.

Reach out to a local real estate agent today and work together to build a plan that fits your market.

What To Expect from the Housing Market in the Second Half of 2026

Student Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

What Buying or Selling a Home Gives Back to Your Community

-

For Sellers4 weeks ago

For Sellers4 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers4 weeks ago

For Buyers4 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

-

Affordability3 weeks ago

Affordability3 weeks agoThat House That’s Been Sitting Could Be Your Best Shot at a Deal

-

Economy3 weeks ago

Economy3 weeks agoMore Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Agent Value3 weeks ago

Agent Value3 weeks agoIs It Still a Seller’s Market? Here’s What the Data Says.

-

Agent Value2 weeks ago

Agent Value2 weeks agoYour House Didn’t Sell. Here’s How To Turn It Around.

-

Equity2 weeks ago

Equity2 weeks agoThe Housing Market Is Stronger Than You Think

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoThe 1 Factor That Explains Everything Happening with Home Prices Right Now

You must be logged in to post a comment Login