First-Time Buyers

The Down Payment Assistance You Didn’t Know About

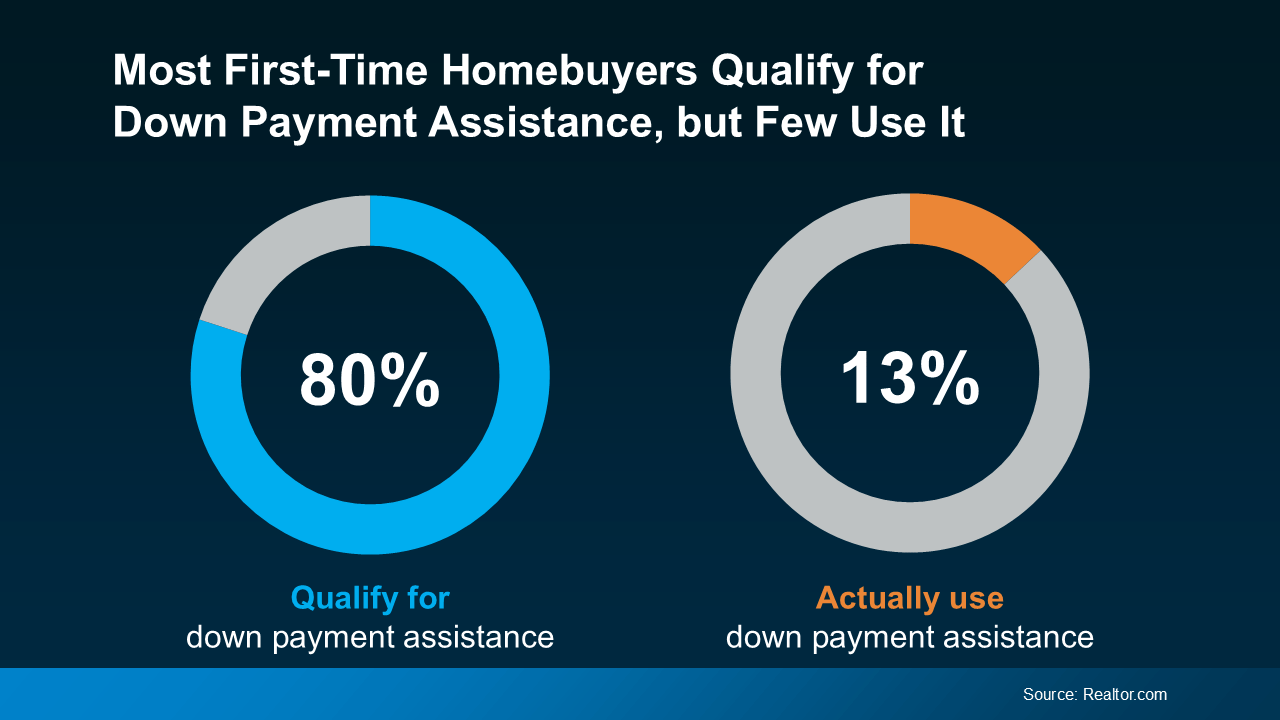

Believe it or not, almost 80% of first-time homebuyers qualify for down payment assistance, but only 13% actually use it. And if you’re hoping to buy a home, this is a mission-critical gap to close – fast (see graph below):

Here’s what you need to know to make the most of your down payment in today’s housing market.

Here’s what you need to know to make the most of your down payment in today’s housing market.

Amplify Your Down Payment Potential

For first-time buyers, the name of the game with down payments is making sure you’re taking advantage of all the resources out there designed to help you. And a bunch of them can get you to your goal faster than you may have thought possible.

For example, there are loan options that require as little as 3% down, or even 0% for certain qualified borrowers, like Veterans. And let’s not forget down payment assistance, like grants and other opportunities, that help you cover the upfront cost of your down payment.

If you’re interested in exploring those options and what you may be able to use to your advantage, connect with a trusted lender. Because if you don’t at least see what’s available, you could be leaving money on the table and missing your chance at buying a home. These resources can boost your down payment. And a higher down payment could help lower your eventual monthly mortgage payment, and even avoid or reduce your fees like private mortgage insurance.

Don’t Let News Headlines About Down Payments Scare You

There’s one more thing to address. News coverage has been talking about how the typical down payment is rising. A report from Redfin states:

“The typical down payment for U.S. homebuyers hit a record high of $67,500 in June, up 14.8% from $58,788 a year earlier . . . This was the 12th consecutive month the median down payment rose year over year.”

But don’t let those high dollars scare you. Just because the average down payment is rising doesn’t mean down payment requirements are going up. That’s a key piece of the puzzle to understand. It’s really just because people are choosing to put more down to try to offset higher mortgage rates, and current homeowners who are putting their equity to work are using that to increase their down payment on their next home. As HousingWire explains:

“. . . buyers are putting down a higher percentage of the purchase price to lower their monthly mortgage payment. And buyers also had more equity from their home sales, which gives them more cushion.”

Let’s break those two reasons down a bit:

1. A bigger down payment helps lower your monthly mortgage payment. Affordability has been a challenge for many buyers recently, which is why those who have the ability to make a bigger down payment are going to do so in an effort to lower their future housing costs.

2. Buyers who already own a home have a record amount of equity to leverage. Someone who bought a home a few years ago has gained a significant amount of value in their house, thanks to home price appreciation. These people can put down much more than the average first-time buyer who hasn’t owned a home yet.

Bottom Line

What’s the best thing to do? Talk with a trusted lender about your options. They’ll help you figure out where you stand today and how to access the resources you may qualify for. Because help is out there, you just need to work with a pro to take advantage of it.

For years, a lot of would-be homebuyers have worried about the same thing. How do you compete with big investors who can swoop in, pay cash, and snap up the houses you want?

Well, worry a little less. Because right now, those big investors aren’t buying up the market. They’re backing out of it.

Investors Are Buying Fewer Homes Than They Have in Years

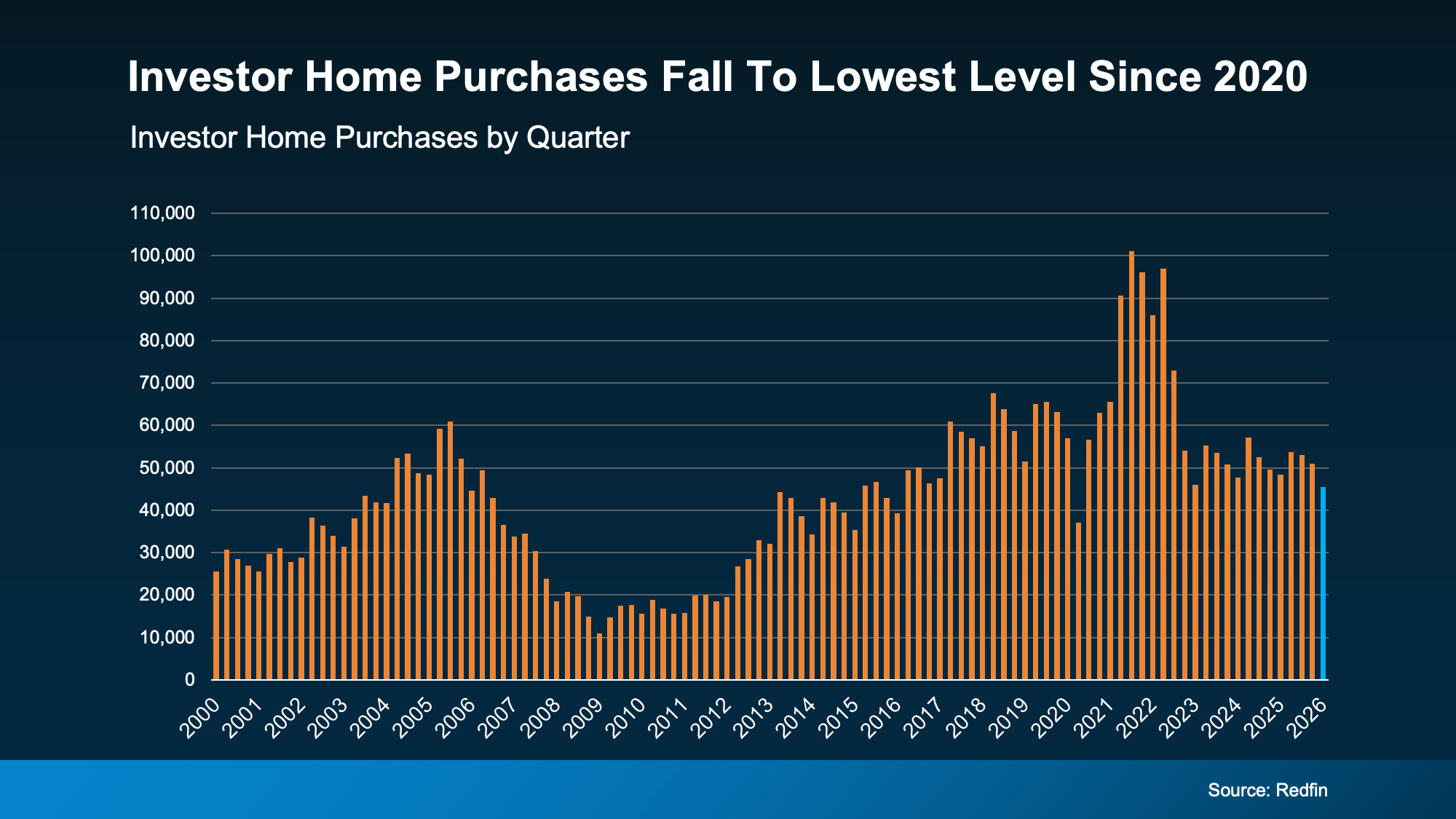

According to Redfin, investor home purchases just fell to their lowest level since 2020 – when the start of the pandemic temporarily caused pretty much all homebuying to pull way back. Before that, you’d have to go all the way back to 2016 to find a time when investors bought this few homes (see graph below):

Why the step back? Two big reasons.

First, Washington passed a housing law that takes aim at large institutional investors. To be clear, these mega investors were never as big a part of the market as the headlines made it sound. They’ve always made up a relatively small slice of housing pie. But the law still targeted the largest ones, and it worked fast. According to Thom Malone, Principal Economist at Cotality:

“When Washington announced its intention to curb institutional investors’ homebuying, the market reacted. . . Cotality data shows that investment by mega investors who own 1,000 or more properties retracted almost instantly.”

Second, the housing market has cooled. Price growth has slowed in much of the country, and in some markets, prices are dipping. That makes the math a lot less appealing for investors betting on quick gains. Lance Lambert, CEO of ResiClub, explains:

“Ever since rates spiked and the Pandemic Housing Boom fizzled out in spring 2022, institutional single-family rental (SFR) operators have pulled way back from buying up homes on the resale market—the math just isn’t as appealing right now. Home prices and rents are no longer ripping, holding costs (property taxes and insurance) have jumped, capital markets have shifted their attention elsewhere, and elevated materials prices make renovations expensive.”

They’re Not Just Buying Less – They’re Selling More

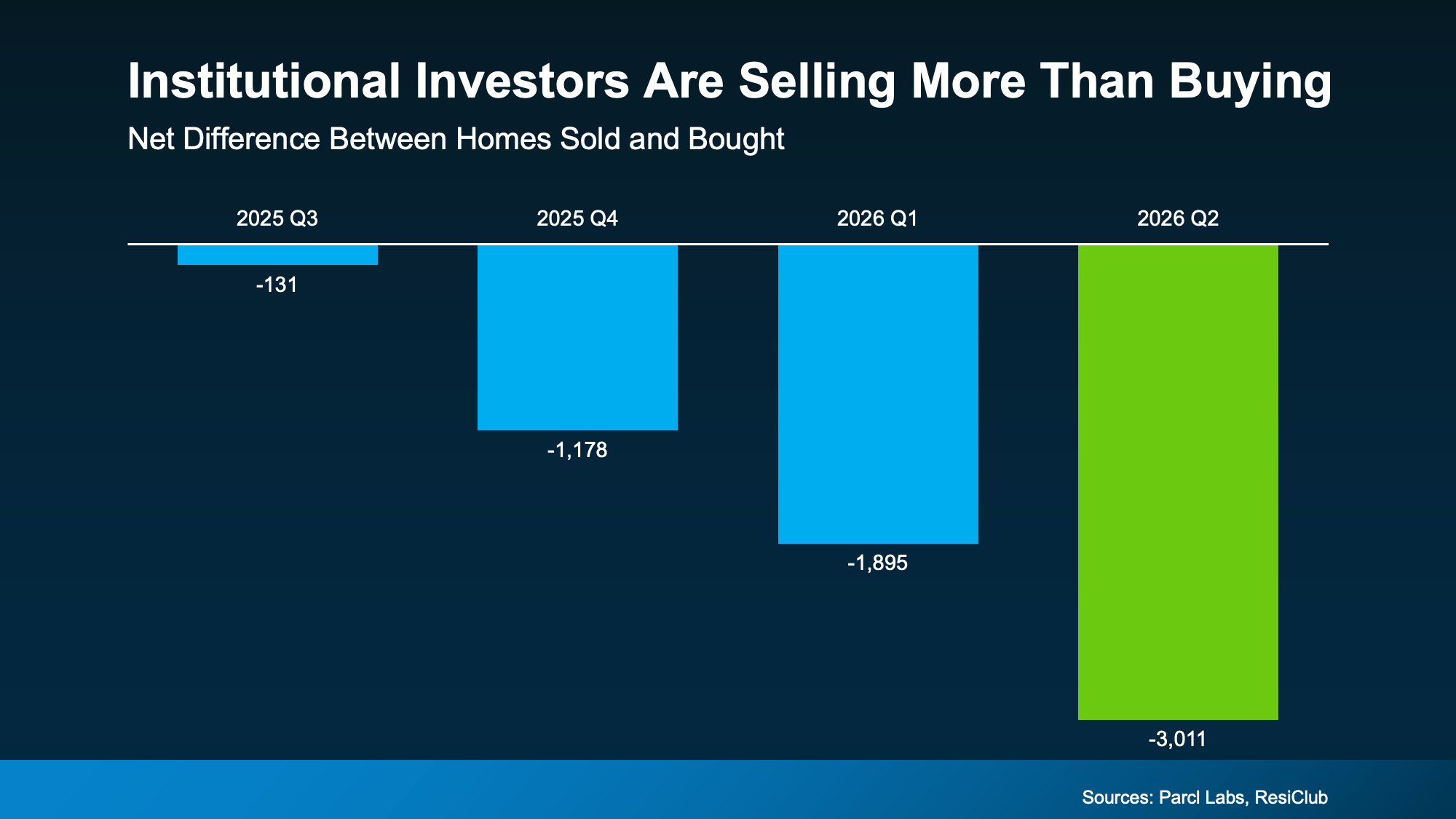

This is the part most people miss. Big investors aren’t just slowing down their purchases. Data from Parcl Labs and ResiClub shows the largest institutional investors are now selling more homes than they’re buying – and that gap is growing these past 4 quarters (see graph below):

Every one of those homes goes right back into the market for buyers like you. And since big investors tend to own homes at the lower end of the price range, a lot of what they’re selling is exactly the kind of home first-time buyers are looking for. As Malone puts it:

“. . . this sudden dropoff in institutional investment is a signal to first-time homebuyers that there’s an opening.”

Less competition from deep-pocketed buyers. More homes hitting the market. And many of them at prices that work for a first purchase. That’s a shift that works in your favor.

Bottom Line

Big investors are stepping back, and they’re adding homes to the market as they go. If you’ve been waiting for a better shot at buying, this could be it. Connect with a local agent to find out what’s popping up in your area. You may have more options than you think.

Today’s home prices have a lot of buyers – especially first-time buyers – wondering if there’s even anything out there that’s in their budget. But owning a home may be more within reach than you think. Sometimes, it just means considering a different type of home.

Condos and townhomes can be a great way to buy without stretching every last dollar. And right now, two things make them worth a serious look.

There Are More Condos and Townhomes To Choose From

Maybe you feel like there’s just nothing out there for you, and you’ve exhausted all your options. But have you considered condos or townhomes? A lot of buyers start by looking for a single-family, detached home without even realizing what that search omits from their pool of choices.

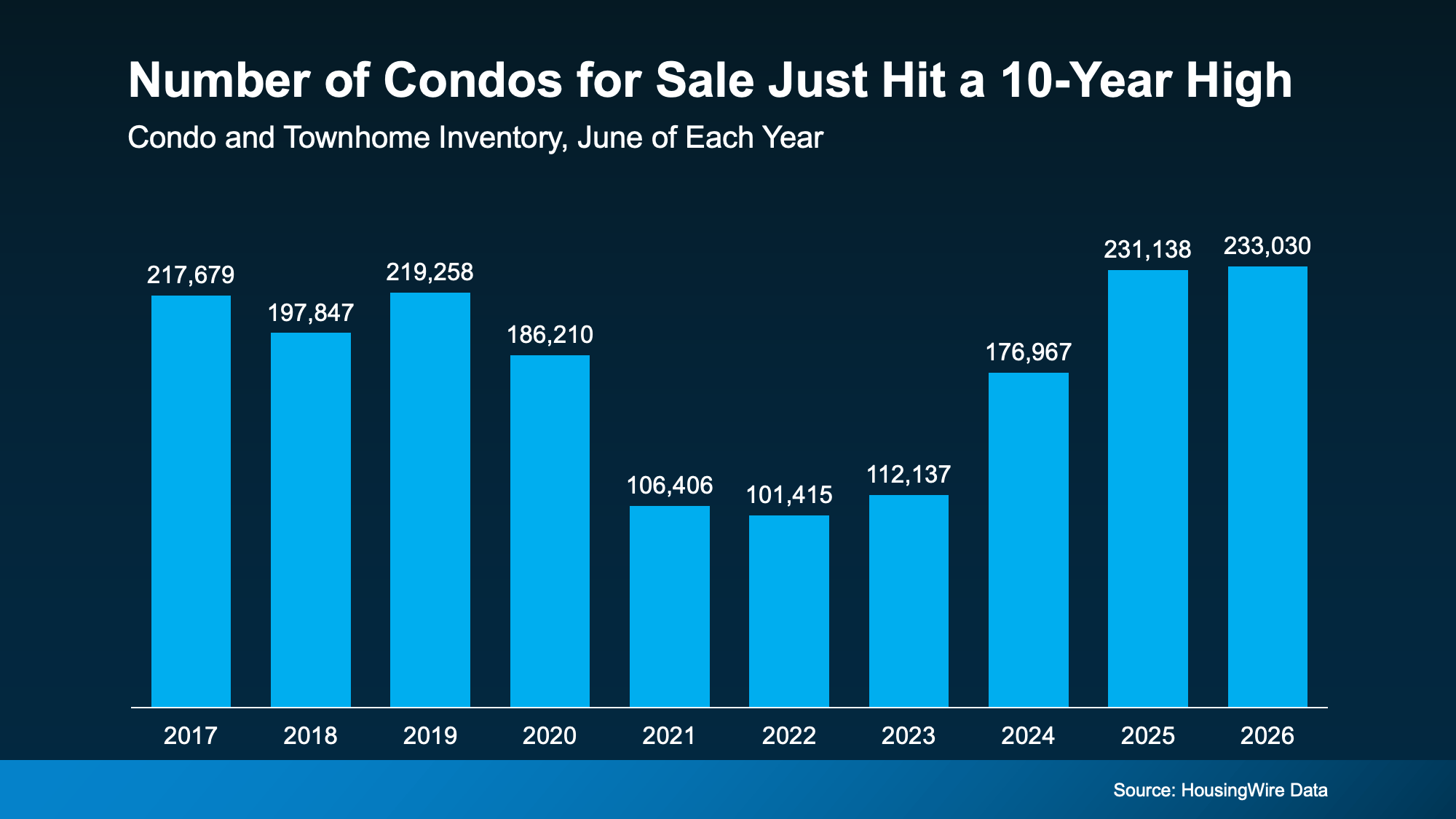

According to HousingWire Data, there were 233,030 condos and townhomes for sale this June. That’s more than any June in at least the past decade, and more than double the number available back in 2022 (see graph below):

That means there are more options out there in this segment of the market – and that’s especially good news for first-time buyers. These types of homes can be a great way to break into the market for less.

Just remember, that’s the national number. What’s available will depend on where you’re looking. But generally speaking, more options means less competition, more time to decide, and more room to negotiate.

They Also Tend To Cost Less Than Single-Family Homes

Price is the other big draw. According to the National Association of Realtors (NAR), the median condo price was $380,000 in June. In contrast, the median single-family home price was $446,400 (see graph below):

That’s a difference of more than $66,000.

A big reason why? Condos are usually smaller than single-family homes. And smaller homes can come with smaller price tags.

And if you don’t need all that extra space, that lower entry price could be exactly what gets you through the door.

Condo or Townhome? How They’re Different.

For buyers who feel priced out of the market, a condo or townhome could be a way in. But there are some things to know. Before you start checking out homes, it’s good to understand how these two compare to each other – and to a single-family home.

-

With a single-family detached home, you own the house and the land it sits on, and you don’t share any walls with neighbors. That means the most space and privacy. But it also usually comes with a higher tag, and all the maintenance is on you.

-

With a townhome, you own the building and the lot it sits on. They’re usually multi-level, so you get more space, and you share two walls at most. You’ll also have more say over how your home looks and how repairs get done, but more of that upkeep falls on you.

-

With a condo, you own just the inside of your unit and may have access to community features like a pool or gym. The building and shared space belong to everyone who lives there, which means you have less maintenance responsibilities. But you’ll also likely have more neighbors around you, less control over building decisions, and higher HOA fees since the HOA handles the exterior and common areas.

Bottom Line

A condo or townhome could be your path to owning a home without blowing your budget. Connect with a local real estate agent to see what’s for sale in your area and figure out which type of home fits your lifestyle, and your bottom line.

If you’ve thought about buying a home in the past few years, you may have run into two frustrations: asking prices that kept climbing and too few homes to choose from.

In many places, both sticking points are letting up this summer, with lower asking prices and more homes for sale. Let’s look at the trends, and what they mean for your search.

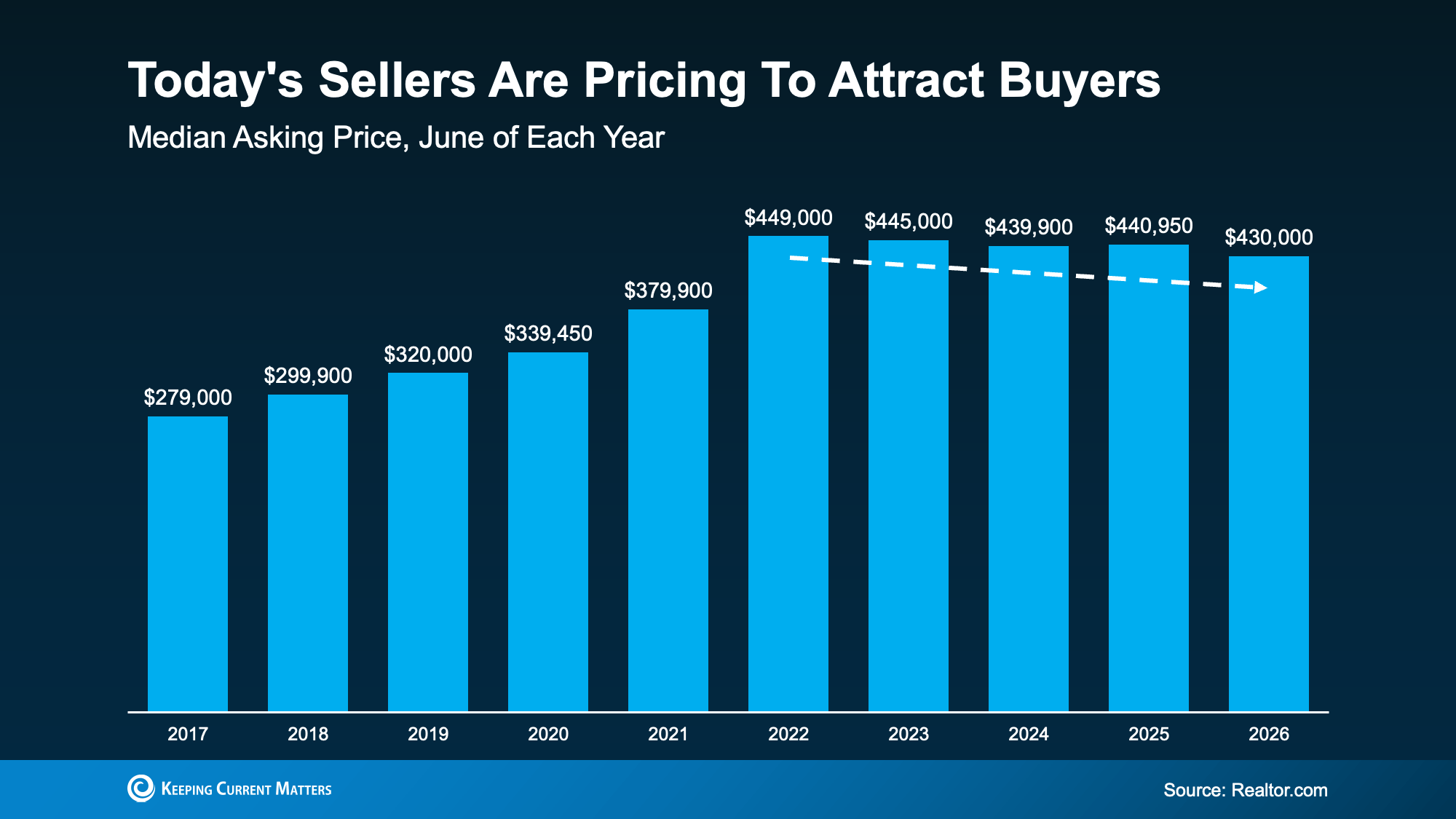

Sellers Are Pricing To Attract Buyers

According to Realtor.com, the national median asking price was $430,000 in June, nearly $11,000 under what it was the year before (see graph below):

That’s the eighth month in a row that the typical asking price has dipped below where they were the previous year, according to the same Realtor.com report.

And while falling prices can sound worrying, this isn’t a sign of an impending crash. We’re talking about asking prices, not sold prices. This is a sign that today’s sellers are meeting the market where it is and pricing to draw buyers. And that’s actually something normal we’d expect from the market. As Danielle Hale, Chief Economist at Realtor.com, puts it:

“Sellers are reading market conditions and are pricing accordingly from the start rather than listing high and cutting later, and buyers are taking note and making bids. This is a welcome sign that we are in a functioning market.”

Asking prices were never going to climb forever – now they’re just settling closer to what buyers can actually pay. That signals a healthier market, and sellers re-adjusting their expectations.

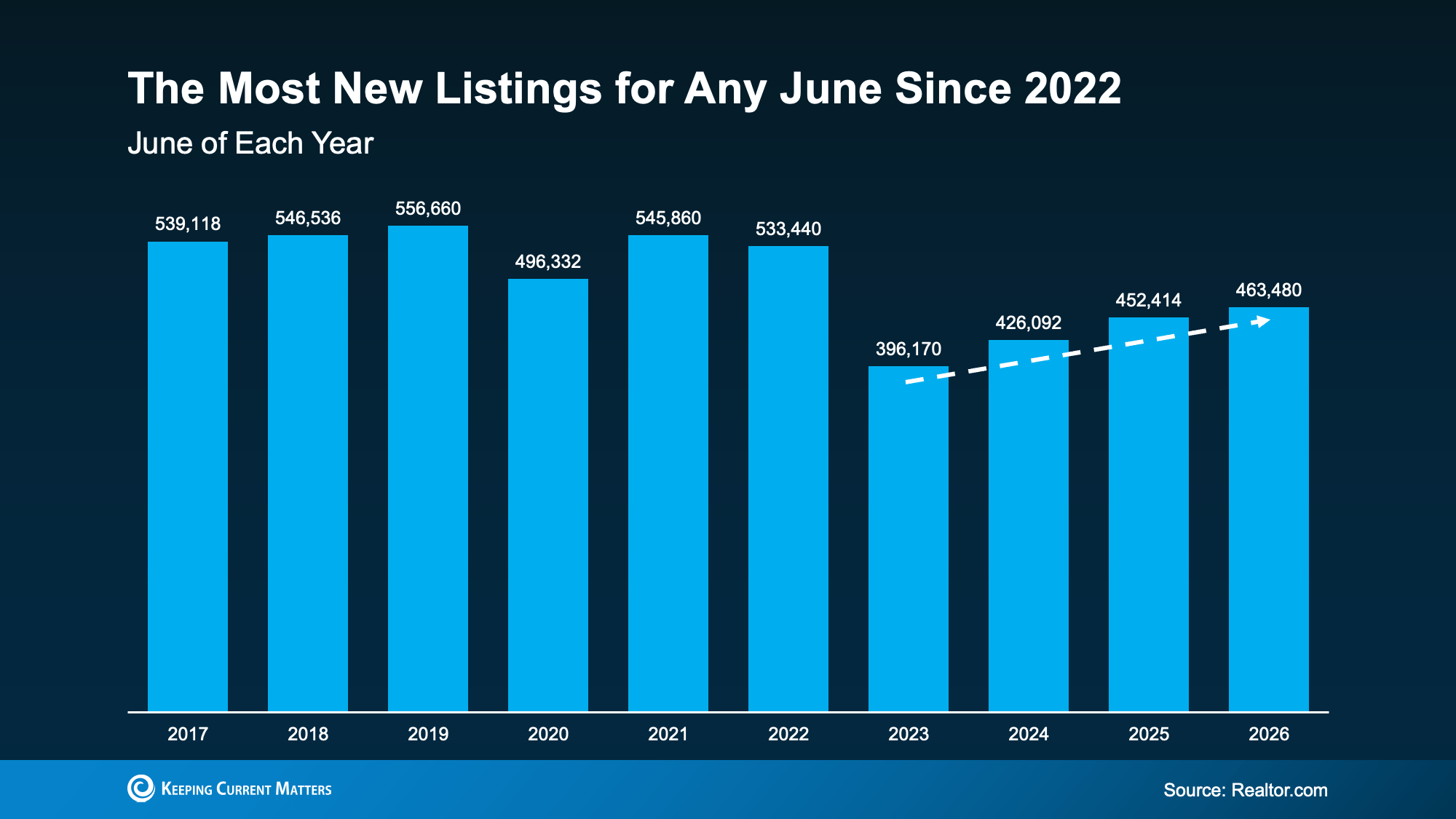

More Homes Are Available Now

If you’ve spent the past few years watching homes disappear before you could even schedule a tour, this is for you.

Supply is starting to catch up. According to Realtor.com, the number of homes listed for sale in June was the highest June number we’ve seen in three years (see graph below):

This means more options for you and less competition for each one.

Now, supply is not back to normal everywhere. As you can see, we’re still down from where we were back in 2017-2019. But in many places, it’s better than it’s been in a while. Here’s how that helps you.

You don’t have to rush an offer just to stay in the running, and you have better odds of finding and landing the right home, not just the one that’s available. Plus, you’ll have more room to negotiate, so you’re searching from a stronger position than buyers had even a year ago.

Why This Is Encouraging if You’re Buying Your First Home

For first-time buyers looking for lower-priced homes, these trends line up especially well. Mischa Fisher, Chief Economist at Zillow, explains:

“The lowest price tiers are exhibiting some softness in terms of price, they also had the most listing-activity growth, the first time since 2022 that’s been the case.”

So, if you’re searching for your first place or your next house, there’s a little more to choose from and a little more give on price.

Bottom Line

If a tight budget or a thin selection has kept you from buying a home, now might be the time to restart your search.

Connect with a local real estate agent to see what’s available where you’re looking.

Thinking About Waiting for Lower Mortgage Rates? Read This First.

Big Investors Are Backing Off and That’s Your Opening

Here’s Where To Start if You’re Selling and Buying at the Same Time

-

For Sellers3 weeks ago

For Sellers3 weeks agoThink Nobody’s Buying Homes Right Now? Think Again.

-

Affordability4 weeks ago

Affordability4 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

-

First-Time Buyers3 weeks ago

First-Time Buyers3 weeks ago14 Years Running: Why Real Estate Is Still America’s Favorite Investment

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoMore Homes, Better Prices: A Buyer’s Summer

-

Equity2 weeks ago

Equity2 weeks agoThe House That Started It All Could Kickstart What’s Next

-

Affordability2 weeks ago

Affordability2 weeks agoPriced Out? A Condo or Townhome Could Be Your Way In.

-

For Sellers2 weeks ago

For Sellers2 weeks agoSelling a Luxury House? Here’s Why Now Is a Good Time

You must be logged in to post a comment Login