Affordability

Is a Fixer Upper Right for You?

Looking to buy a home but feeling like almost everything is out of reach? Here’s the thing. There’s still a way to become a homeowner, even when affordability seems like a huge roadblock – and it might be with a fixer upper. Let’s dive into why buying a fixer upper could be your ticket to homeownership and how you can make it work.

What Is a Fixer Upper?

A fixer upper is a home that’s in livable condition but needs some work. The amount of work varies by home – some may need cosmetic updates like wallpaper removal and new flooring, while others might require more extensive repairs like replacing a roof or updating plumbing.

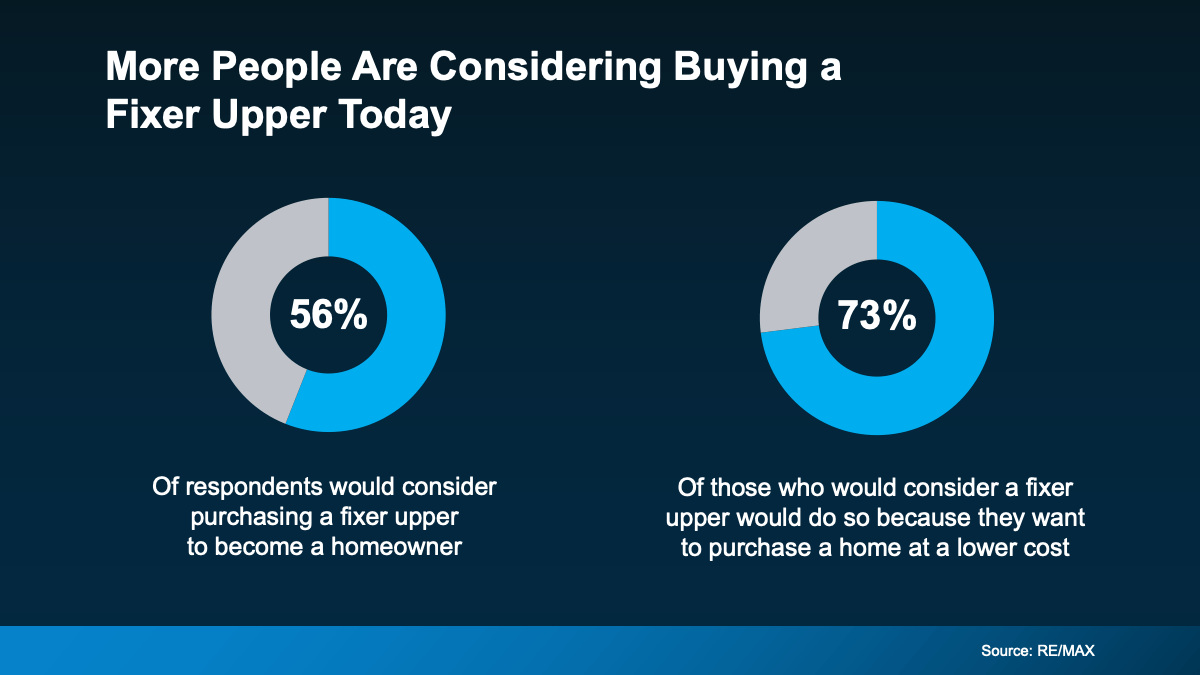

Because they need some elbow grease, these homes typically have a lower price point, based on local market value. In fact, a survey from StorageCafe explains that fixer uppers generally cost about 29% less than move-in-ready homes.

And that’s why, according to a recent survey, more buyers are considering homes that need a little extra work right now (see below):

If you’re looking for an option to get your foot in the door, and you’re willing to roll up your sleeves and do a bit of work, a house with untapped potential may be a good option.

If you’re looking for an option to get your foot in the door, and you’re willing to roll up your sleeves and do a bit of work, a house with untapped potential may be a good option.

Tips for Buying a Home That Needs Some Work

Before you buy a home that may need a makeover, here are a few things to keep in mind:

- Choose a Good Location: You can repair a house, but you can’t change where it is. Make sure the home is in a neighborhood you like or one with increasing property values and a growing number of local amenities. This way, even after you spend money fixing it up, the house will be worth more later.

- Budget for Surprises: Fixing up a house can take more time and money than you might think. Make sure you save room in your budget for unexpected repairs or other unknowns that might come up while you’re working on the house.

- Get a Home Inspection: Before you buy, hire an inspector to check out the house. They’ll help you determine the necessary repairs, so you don’t end up with expensive surprises later.

- Plan Your Priorities: When deciding what to tackle first, it helps to categorize your goals. Think of your home in three ways: the must-haves (essential repairs), the nice-to-haves (upgrades that would make life easier), and the dream-state features (luxuries you can add later). This will help you prioritize and stick to your budget.

Remember, the perfect home is the one you perfect after buying it. By starting with a fixer upper, you have the opportunity to customize a home to your liking while saving money on the initial purchase price. With careful planning, budgeting, and a little bit of vision, you can turn a house that needs some love into your perfect home.

Real estate agents are great at finding homes with potential. They know the local market and can guide you to homes where smart upgrades can add value. With their help, you’re more likely to find a house that fits your total budget and has room for worthwhile improvements.

Bottom Line

In today’s market, where the cost of homeownership can be intimidating, finding a move-in-ready home that fits your budget can feel like a real challenge. But if you’re open to putting in a little work, you can transform a fixer upper into your ideal home over time. A local real estate agent can help you explore what’s possible and find a place that’ll work for you.

Today’s home prices have a lot of buyers – especially first-time buyers – wondering if there’s even anything out there that’s in their budget. But owning a home may be more within reach than you think. Sometimes, it just means considering a different type of home.

Condos and townhomes can be a great way to buy without stretching every last dollar. And right now, two things make them worth a serious look.

There Are More Condos and Townhomes To Choose From

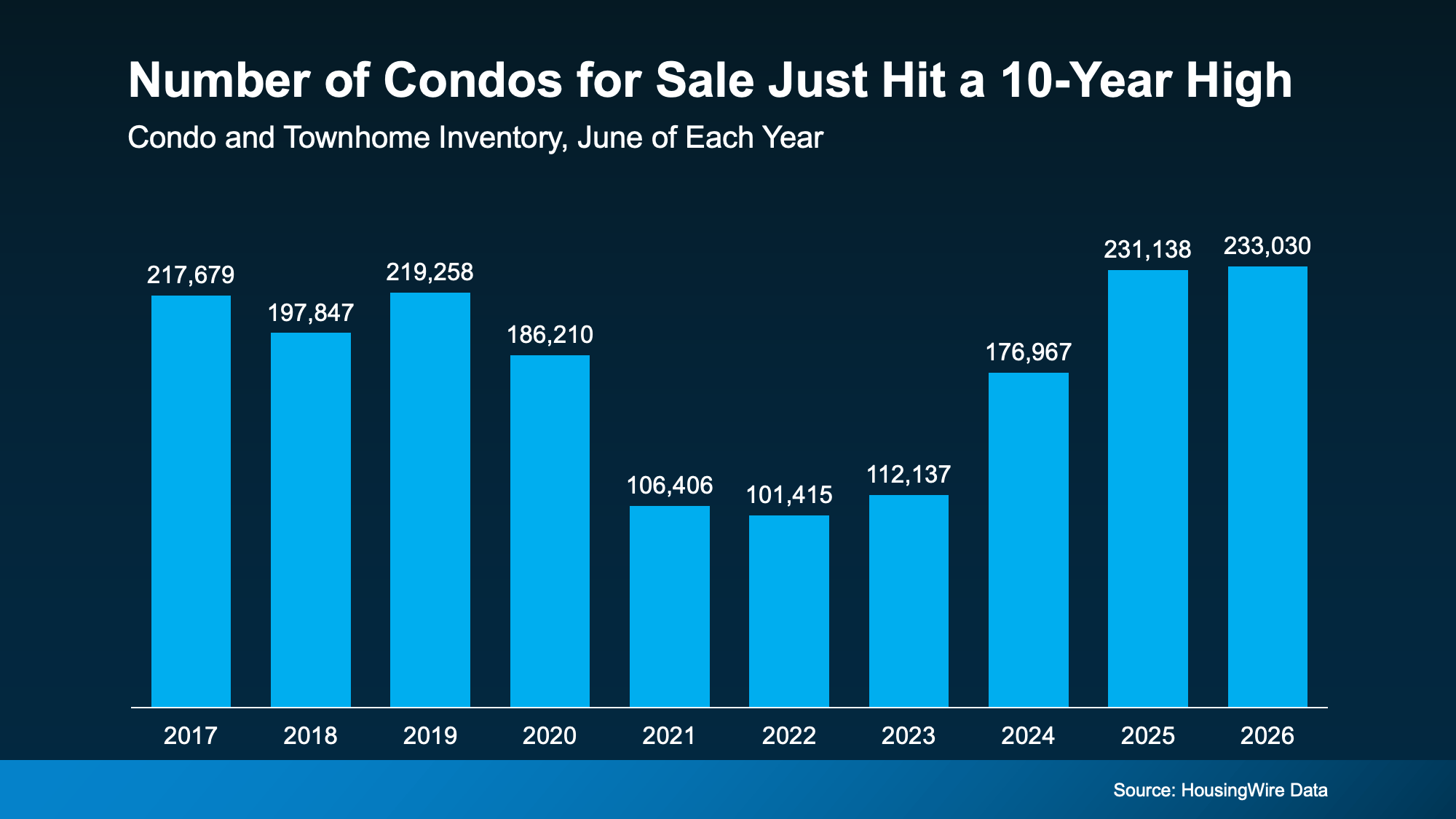

Maybe you feel like there’s just nothing out there for you, and you’ve exhausted all your options. But have you considered condos or townhomes? A lot of buyers start by looking for a single-family, detached home without even realizing what that search omits from their pool of choices.

According to HousingWire Data, there were 233,030 condos and townhomes for sale this June. That’s more than any June in at least the past decade, and more than double the number available back in 2022 (see graph below):

That means there are more options out there in this segment of the market – and that’s especially good news for first-time buyers. These types of homes can be a great way to break into the market for less.

Just remember, that’s the national number. What’s available will depend on where you’re looking. But generally speaking, more options means less competition, more time to decide, and more room to negotiate.

They Also Tend To Cost Less Than Single-Family Homes

Price is the other big draw. According to the National Association of Realtors (NAR), the median condo price was $380,000 in June. In contrast, the median single-family home price was $446,400 (see graph below):

That’s a difference of more than $66,000.

A big reason why? Condos are usually smaller than single-family homes. And smaller homes can come with smaller price tags.

And if you don’t need all that extra space, that lower entry price could be exactly what gets you through the door.

Condo or Townhome? How They’re Different.

For buyers who feel priced out of the market, a condo or townhome could be a way in. But there are some things to know. Before you start checking out homes, it’s good to understand how these two compare to each other – and to a single-family home.

-

With a single-family detached home, you own the house and the land it sits on, and you don’t share any walls with neighbors. That means the most space and privacy. But it also usually comes with a higher tag, and all the maintenance is on you.

-

With a townhome, you own the building and the lot it sits on. They’re usually multi-level, so you get more space, and you share two walls at most. You’ll also have more say over how your home looks and how repairs get done, but more of that upkeep falls on you.

-

With a condo, you own just the inside of your unit and may have access to community features like a pool or gym. The building and shared space belong to everyone who lives there, which means you have less maintenance responsibilities. But you’ll also likely have more neighbors around you, less control over building decisions, and higher HOA fees since the HOA handles the exterior and common areas.

Bottom Line

A condo or townhome could be your path to owning a home without blowing your budget. Connect with a local real estate agent to see what’s for sale in your area and figure out which type of home fits your lifestyle, and your bottom line.

If the first half of this year has left you feeling stuck, you’re not the only one. Mortgage rates stayed higher than people wanted. Affordability remained tight. And uncertainty overseas added another layer of pressure nobody saw coming.

That’s why so many people are asking the same question: Will the second half of the year be any better for the housing market?

While nobody has a crystal ball, there are a few encouraging signs things could start moving in a better direction. Here’s what to watch.

Mortgage Rates Could Be Near a Turning Point

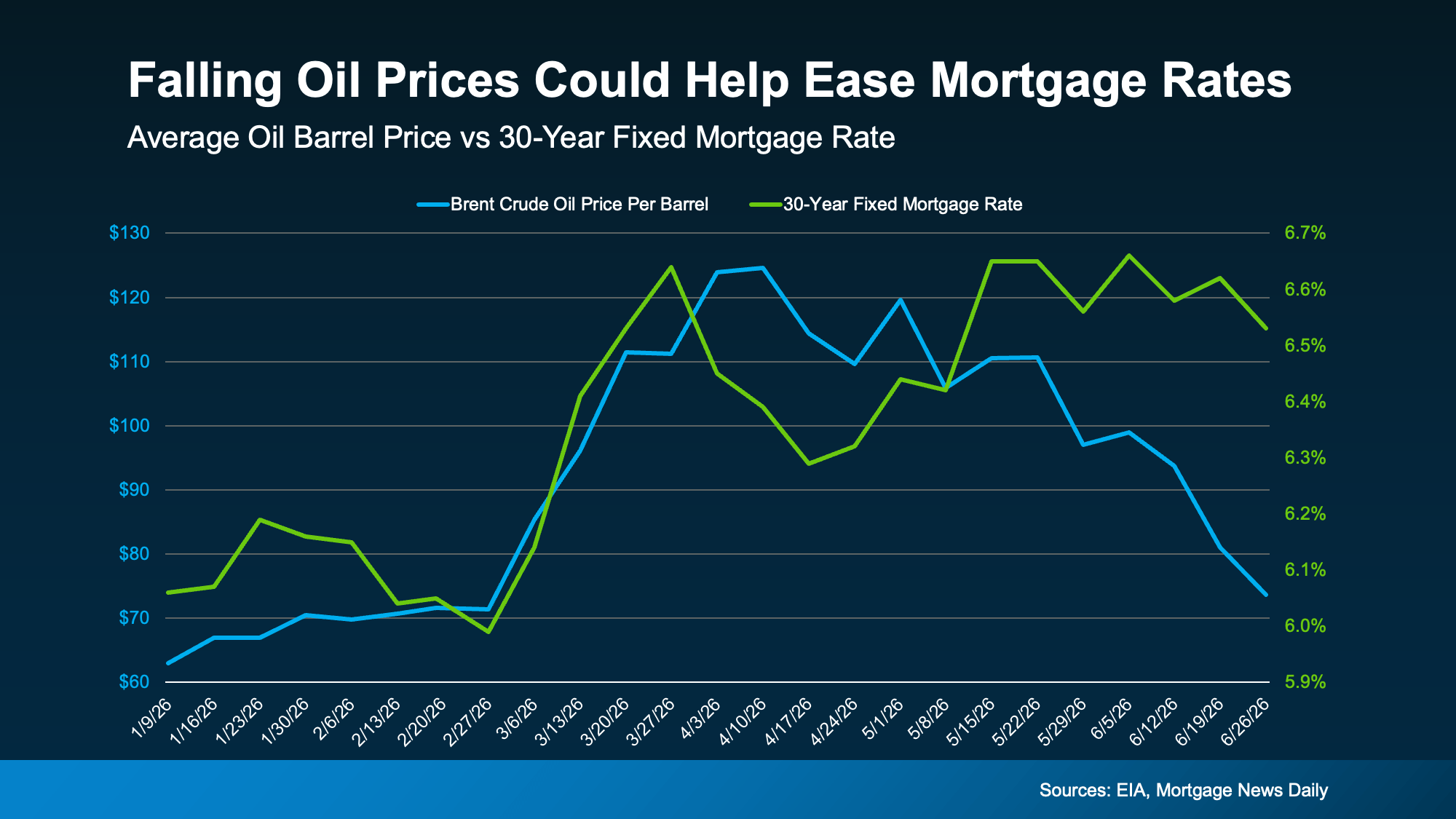

One of the biggest reasons mortgage rates haven’t come down yet is inflation. And higher energy prices and uncertainty overseas are at least part of the reason inflation is still elevated. The encouraging news?

Oil prices have already started coming back down.

That may not sound like it has much to do with buying a home. But historically, mortgage rates and oil prices tend to move in the same direction.

Take a look at the graph below. Generally, they rise and fall together. Both went up in February when the conflict began. While there’s been some volatility lately, experts at the U.S. Energy Information Administration (EIA) say oil prices are forecast to come down. And since oil prices have been on an overall downward trend lately, mortgage rates could come down too:

It’s too soon to say exactly when that will happen (or by how much they’ll fall), but if energy prices go down, inflation cools off, and tensions overseas ease, mortgage rates could come down in the second half of the year.

And that’s good news for anyone thinking about moving. The first half of the year tested everyone’s patience. The second half may finally reward it.

Home Prices Could Pick Back Up

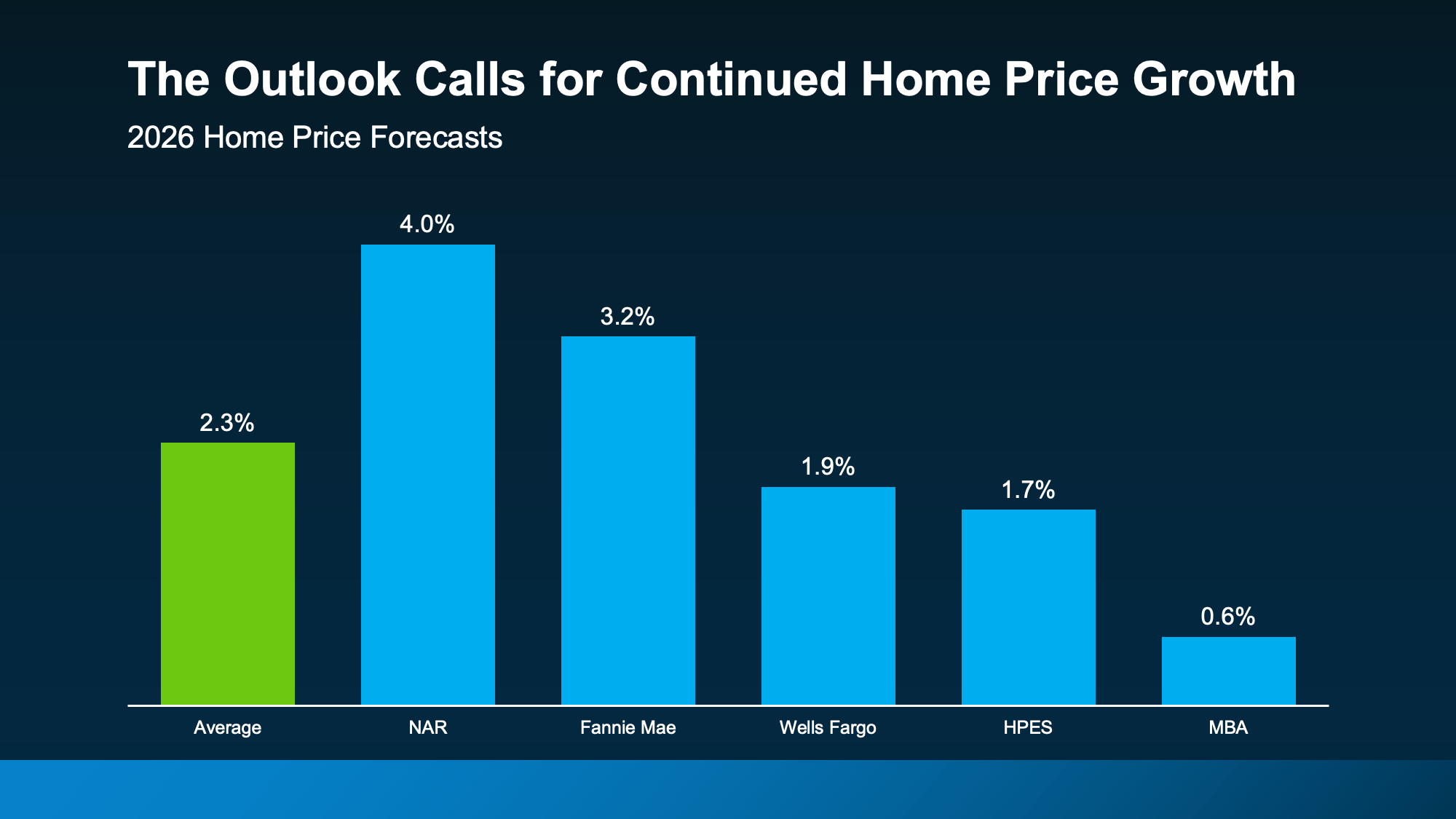

A lot of people want home prices to fall too. But that’s not what most forecasts show.

While price trends are going to vary by area, and some places are seeing mild declines, experts still expect home prices to net positive this year at the national level.

In fact, they’re projecting prices will rise by an average of 2.3% in 2026 (see graph below):

What does that mean for you? Right now, Federal Housing Finance Agency (FHFA)data shows prices are up about 1.7% nationally year-over-year. The average forecast for all of 2026? 2.3%.

Based on those projections, home price growth would have to pick up a bit during the second half of the year. Nothing dramatic, just enough to finish the year around that projected 2.3% gain.

Here’s why that’s possible.

The number of homes for sale has grown, but that growth may be starting to slow down. And if rates improve, more buyers could jump back into the market. More buyers competing could put modest upward pressure on prices, especially if inventory’s not growing as fast.

That’s why buyers shouldn’t assume waiting will guarantee a lower price later. And for sellers, that’s great news if you’ve been worried about your home’s value.

More Homes Are Expected To Sell

If you’ve been wondering why the housing market has felt quieter lately, you’re not imagining it. Home sales have been slower than many experts expected. But that doesn’t mean people have stopped wanting to move.

A lot of people still want or need to make a change. They’ve just been waiting for more certainty, better affordability, or a clearer read on where the market is headed. And early signs show that may be on the horizon.

If rates ease and confidence improves, more people may finally move. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Overall, we expect pent-up demand to continue emerging gradually. But the pace of recovery will vary significantly across markets and will depend on the path of rates, labor market conditions and inventory growth.”

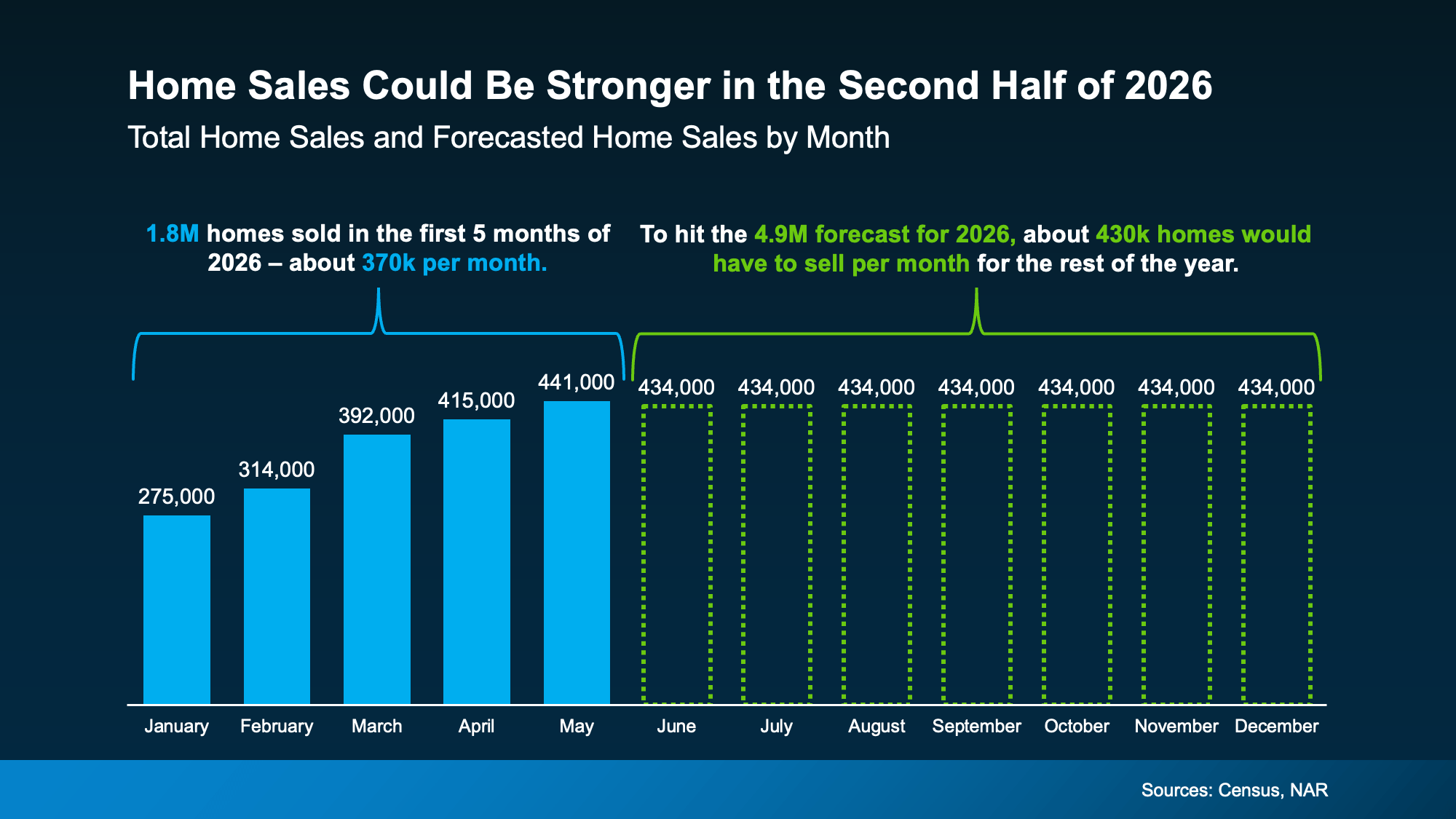

Based on the latest forecasts, to hit the number of sales expected this year, here’s what would have to happen. The second half of the year would need to outperform the first in sales (see graph below):

In fact, each month for the rest of 2026 would have to come close to matching the best month we’ve had so far this year (May). That’s a sign the experts are calling for more momentum headed into the second half.

More people will finally make their move happen – and you’ve got the chance to be one of them.

Bottom Line

The second half of the year probably won’t be perfect. But it could be better.

Mortgage rates may ease. Home sales could pick up. And prices are expected to continue rising at a healthier, more sustainable pace. If you’ve been waiting for signs of progress, this is it.

If you want to understand what these forecasts mean for your plans and what’s happening in your local market, connect with an agent.

Saving for a down payment can feel like the hardest part of buying a home. And with affordability as tight as it’s been lately, it’s fair to wonder how anyone manages it right now. Here’s something you may not have seen coming.

Some people are getting their foot in the door with a smaller down payment.

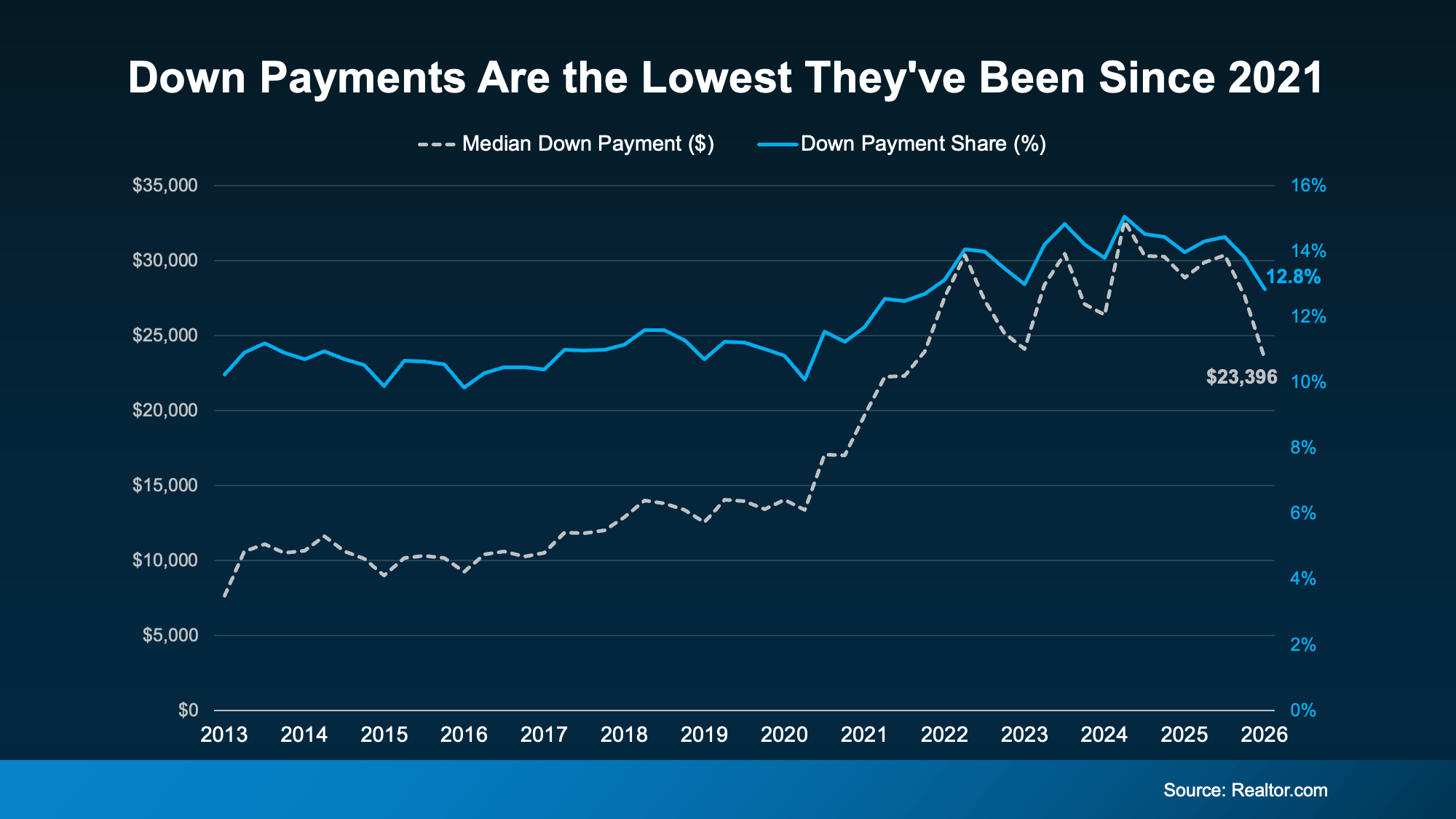

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that’s around $5,000 below what was typical the year before (a 19% drop year over year). That’s the lowest down payments have been since 2021 (see graph below):

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

There are a few things driving the trend:

-

Less competition between buyers. Part of it comes down to a more balanced market. With buyers facing less competition than they did a few years ago, there’s less pressure to put a big sum down just to stand out.

-

More moderate home prices. Your down payment is a percentage of the purchase price. So, as price growth cools, the amount you need to put down may change too. In a lot of markets, prices have slowed or leveled off, and some areas are even seeing slight dips. That can translate into smaller down payments.

-

Buyers opting for loans with lower down payments. More buyers are also turning to government-backed loans, like FHA and VA, which often need little or no money down. FHA loans have made up more than 24% of purchase mortgages for five straight quarters, and VA loans recently hit their highest share in over a decade, according to Mortgage Professional America.

But even a smaller down payment is still a significant chunk of cash, and saving it can be hard. So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

Help You May Not Know You Qualify For

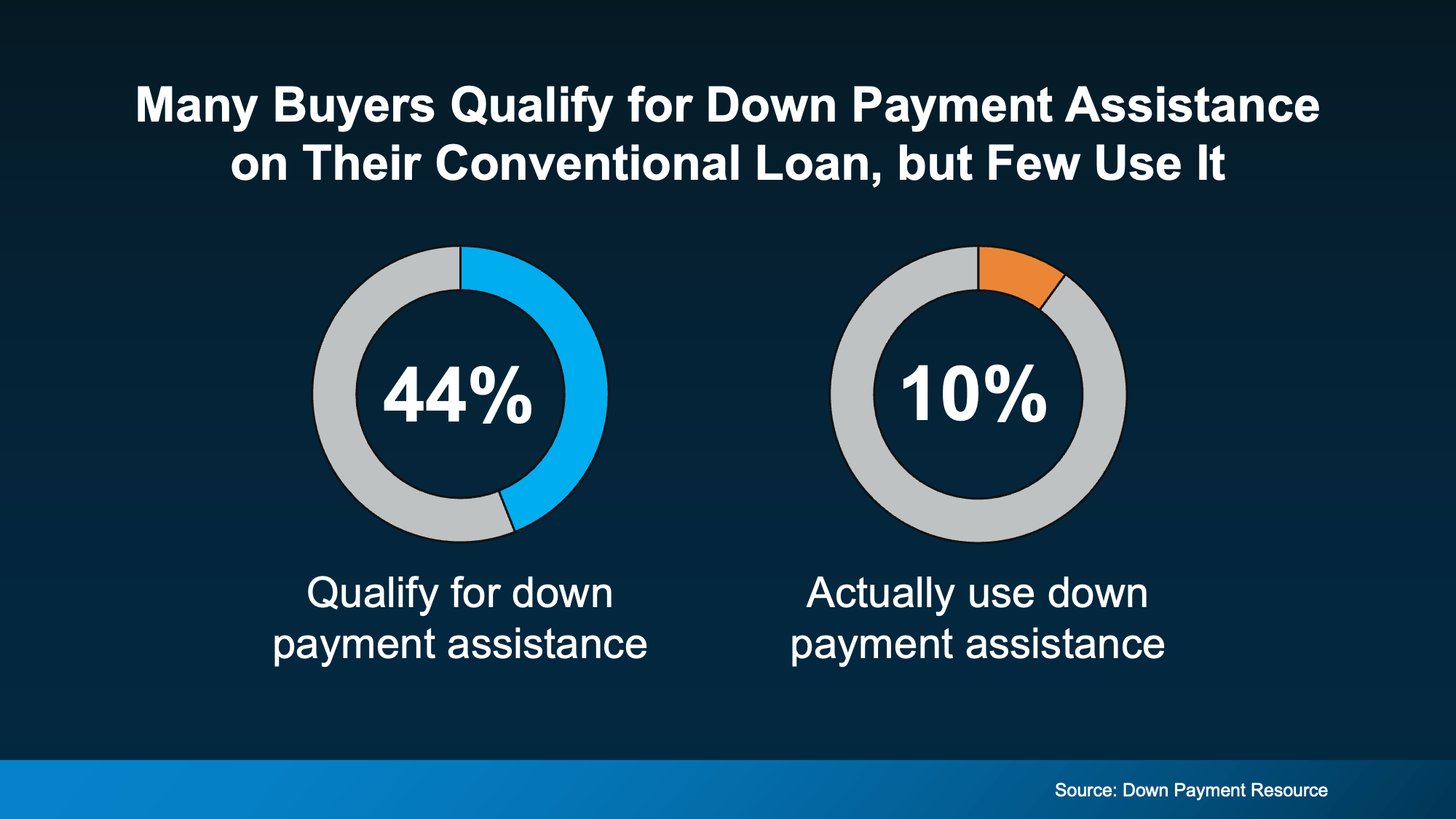

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

-

There are more than 2,600 down payment assistance programs available

-

More than half (62%) are designed to help first-time buyers

-

38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

-

62% are open to buyers earning $100,000 or more

A Boost from Loved Ones

For a growing number of buyers, help comes from closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support most often goes toward the down payment, followed by help qualifying for a mortgage and covering closing costs. Chris Birk, VP of Mortgage Insight at Veterans United, puts it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, it can make a real difference in how soon you can buy.

Bottom Line

Down payments are smaller than they’ve been in years, and that opens the door for more buyers.

And with added help from assistance programs and a little help from loved ones, you may have more ways forward than you realized. Connect with a trusted lender to talk through your options.

The House That Started It All Could Kickstart What’s Next

Priced Out? A Condo or Townhome Could Be Your Way In.

More Homes, Better Prices: A Buyer’s Summer

-

Economy4 weeks ago

Economy4 weeks agoMore Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Agent Value4 weeks ago

Agent Value4 weeks agoYour House Didn’t Sell. Here’s How To Turn It Around.

-

Equity3 weeks ago

Equity3 weeks agoThe Housing Market Is Stronger Than You Think

-

Economy2 weeks ago

Economy2 weeks agoWhat Buying or Selling a Home Gives Back to Your Community

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoThe 1 Factor That Explains Everything Happening with Home Prices Right Now

-

Affordability3 weeks ago

Affordability3 weeks agoDown Payments Are Smaller Than They’ve Been Since 2021

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoStudent Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

-

Affordability2 weeks ago

Affordability2 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

You must be logged in to post a comment Login