For Buyers

More Homes, Slower Price Growth – What It Means for You as a Buyer

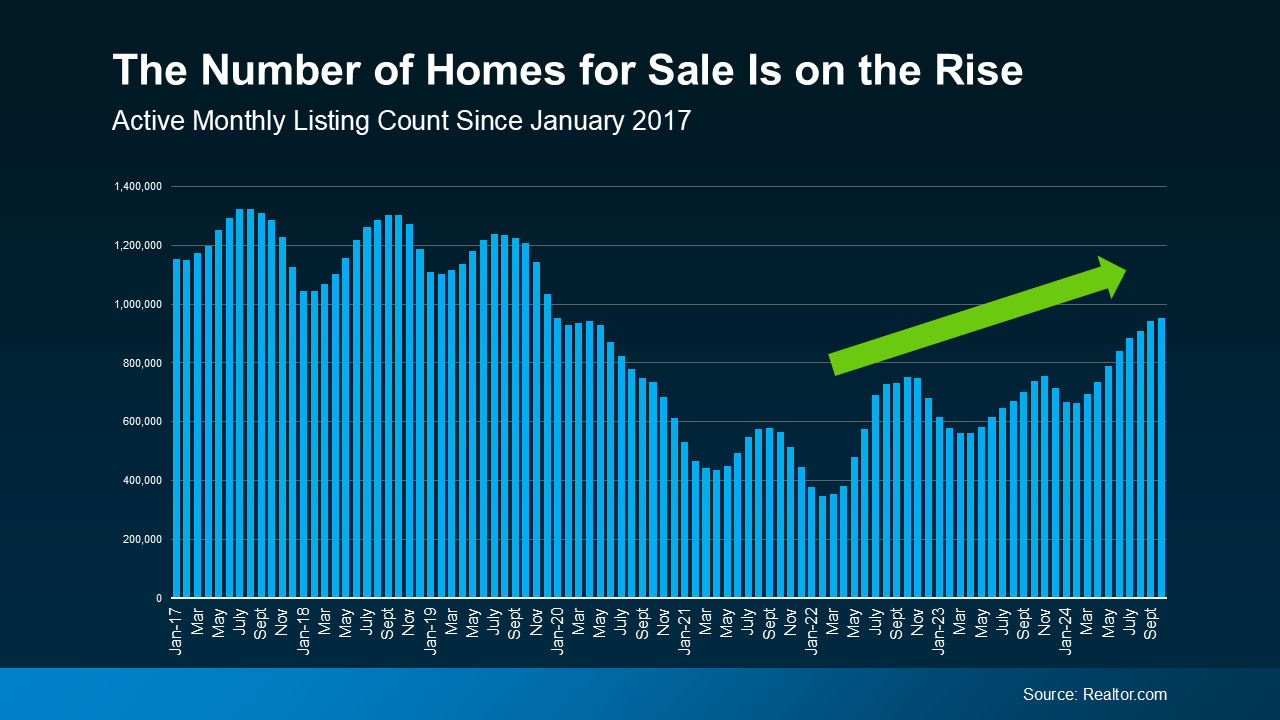

There are more homes on the market right now than there have been in years – and that could be a game changer for you if you’re ready to buy. Let’s look at two reasons why.

You Have More Options To Choose From

An article from Realtor.com helps explain just how much the number of homes for sale has gone up this year:

“There were 29.2% more homes actively for sale on a typical day in October compared with the same time in 2023, marking the twelfth consecutive month of annual inventory growth and the highest count since December 2019.”

And while the number of homes on the market still isn’t quite back to where it was in the years leading up to the pandemic, this is definitely an improvement (see graph below):

With more homes available for sale now, you have more options to choose from. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, explains:

With more homes available for sale now, you have more options to choose from. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, explains:

“Though still lower than pre-pandemic, burgeoning home supply means buyers have more options . . .”

That means you have a better chance of finding a house that meets your needs. It also means the buying process doesn’t have to feel quite as rushed, because more options on the market means you’ll likely face less competition from other buyers.

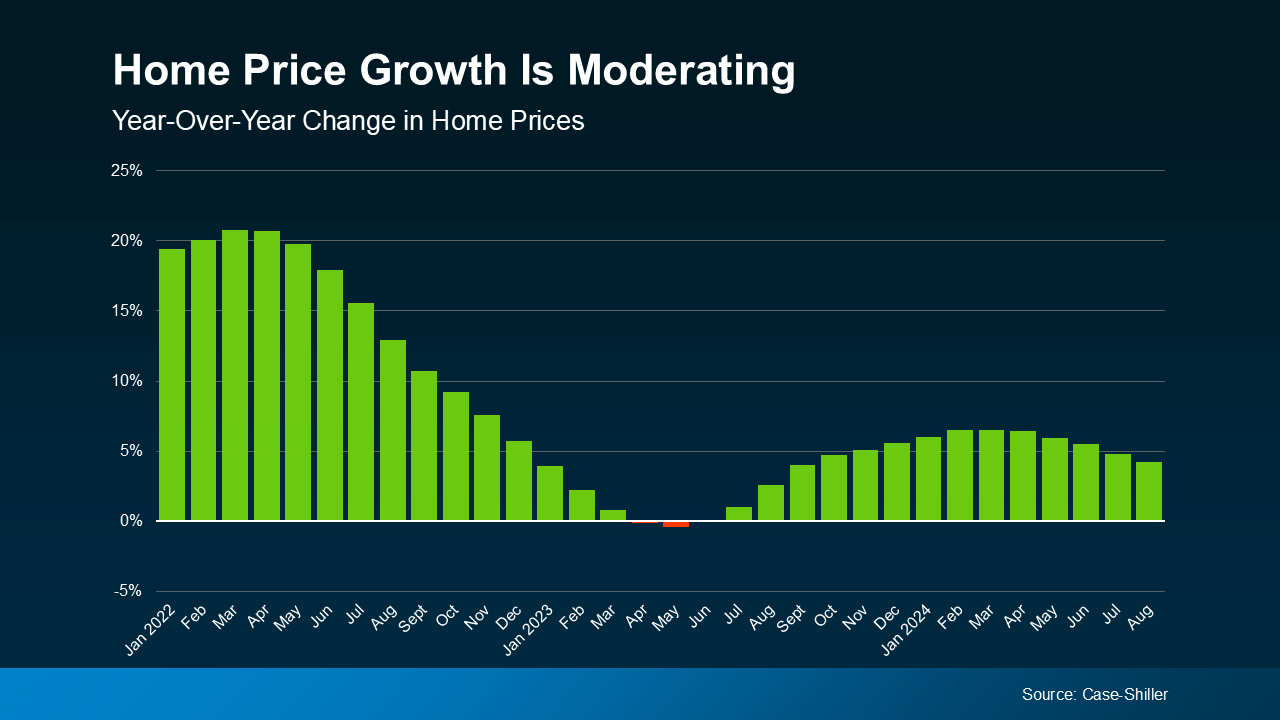

Home Price Growth Is Slowing

When there aren’t many homes for sale, buyers have to compete more fiercely for the ones that are available. That’s what happened a few years ago, and it’s what drove prices up so quickly.

But now, the increasing number of homes on the market is causing home price growth to slow down (see graph below):

In certain markets, the number of available homes has not only bounced back to normal, but has even surpassed pre-pandemic levels. In those areas, home price growth has slowed or stalled completely. As Lance Lambert, Co-Founder of ResiClub, explains:

In certain markets, the number of available homes has not only bounced back to normal, but has even surpassed pre-pandemic levels. In those areas, home price growth has slowed or stalled completely. As Lance Lambert, Co-Founder of ResiClub, explains:

“Generally speaking, housing markets where active inventory has returned to pre-pandemic 2019 levels have seen home price growth soften or even decline outright from their 2022 peak.”

Slower or stalled price growth could give you a better chance of finding something within your budget. As Dr. Anju Vajja, Deputy Director at the Federal Housing Finance Agency (FHFA), says:

“For the third consecutive month U.S. house prices showed little movement . . . relatively flat house prices may improve housing affordability.”

But remember, inventory levels and home prices are going to vary by market.

So, having a real estate agent who knows the local area can be a big advantage. They can help you understand the trends in your community, which can make a real difference in finding a home that fits your needs and budget.

Bottom Line

More housing options – and the slower home price growth they bring – can help you find and buy a home that works for your lifestyle and budget. So don’t hesitate to reach out to a local real estate agent if you want to talk about the growing number of choices you have right now.

A lot of people who want to move are telling themselves the same thing: “Maybe I’ll just wait until later this year once things calm down.”

While waiting sounds like a good plan, there’s something worth knowing before you decide. Rates aren’t expected to change much, so if that’s the #1 reason you’re waiting, it may not pay off. And there may be other things you miss out on in the meantime.

Historically, Summer is one of the strongest seasons of the year for both buyers and sellers. And if you delay your move until Fall or Winter, some of those opportunities may already be fading.

Buyers: Fresh Inventory Is Your Real Summer Advantage

One of the biggest frustrations buyers have faced over the past few years has been a lack of affordable options. Maybe you’ve run into that yourself:

-

You find a house you like, but it’s out of your budget.

-

You find something in your budget, but you don’t like it.

-

Or worse, nothing interesting hits the market for weeks.

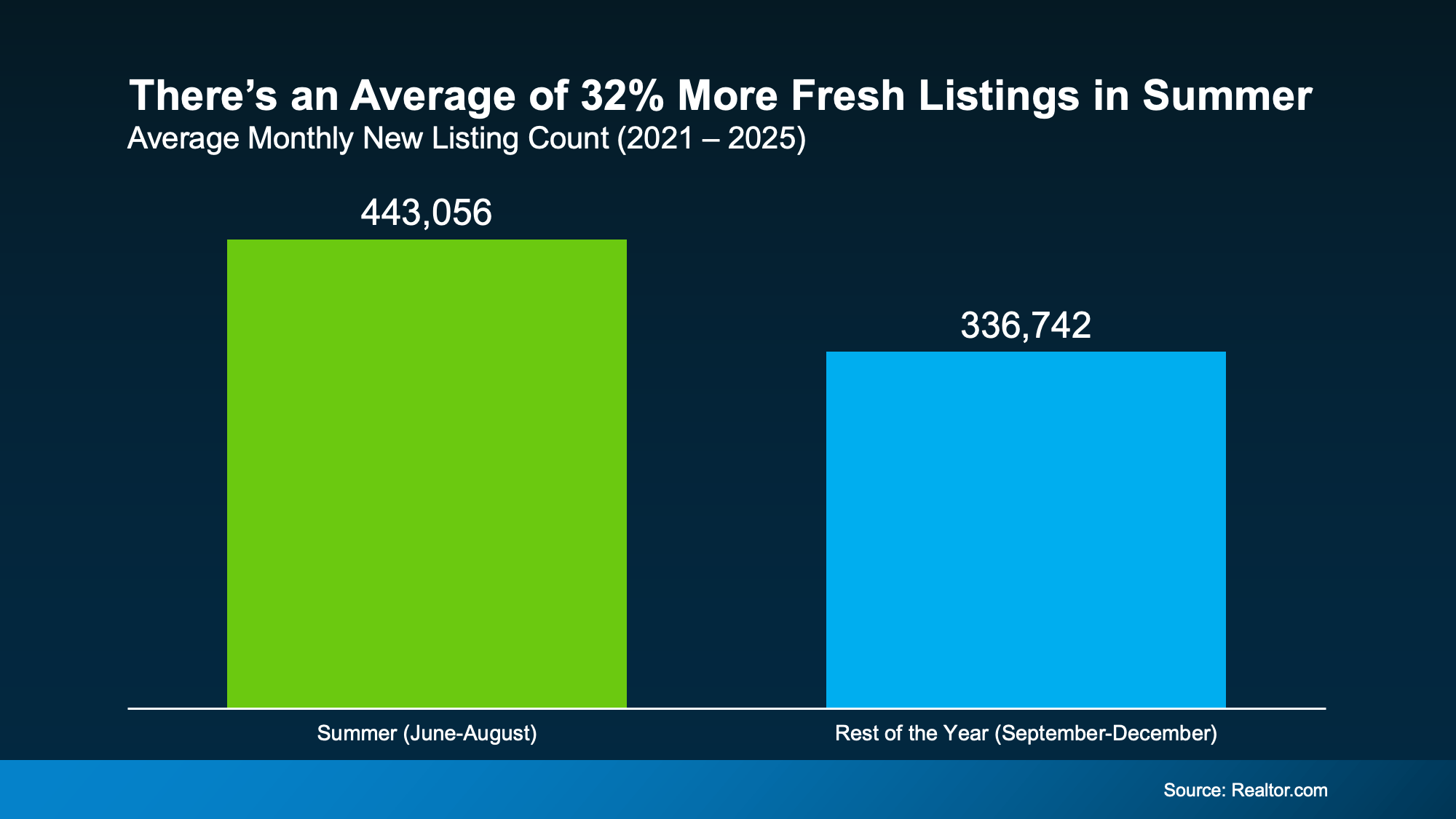

Historically, Summer helps with that.

Looking at data from the last few years, Summer months consistently bring more sellers into the market than later in the year. And that gives buyers a real window of fresh choices.

According to Realtor.com, any given Summer month typically sees about 32% more fresh options than the average month from September-December.

With more newly listed homes, there’s a better chance of finding one you like where the numbers actually work.

Because all it really takes is one home to completely change your search. And if you’ve got more popping onto the market to choose from, maybe one of those is exactly what you need.

But keep in mind, this seasonal window isn’t open forever. Fresh inventory tends to slow down once Summer ends.

Many homeowners who planned to sell this year have already listed by then. Families who wanted to move before school starts have often already gotten it done, or at least, set it into motion. So, new listing activity usually cools as we head into Fall and Winter.

Of course, every year is different. But if finding the right home at the right price has been your biggest challenge, waiting until later in the year may not necessarily give you more options. In fact, recent history suggests it may do just the opposite.

Sellers: Homes Usually Sell for More in the Summer

If you’re thinking of selling, you may be considering holding off because you’ve seen headlines about lower asking prices, price cuts, and softer conditions in some markets. But those headlines don’t tell the whole story or convey just how much it varies by area.

Here’s what you really need to know. Even though the market’s becoming more balanced and some pockets are experiencing price declines, that doesn’t mean you’ve missed your chance to sell.

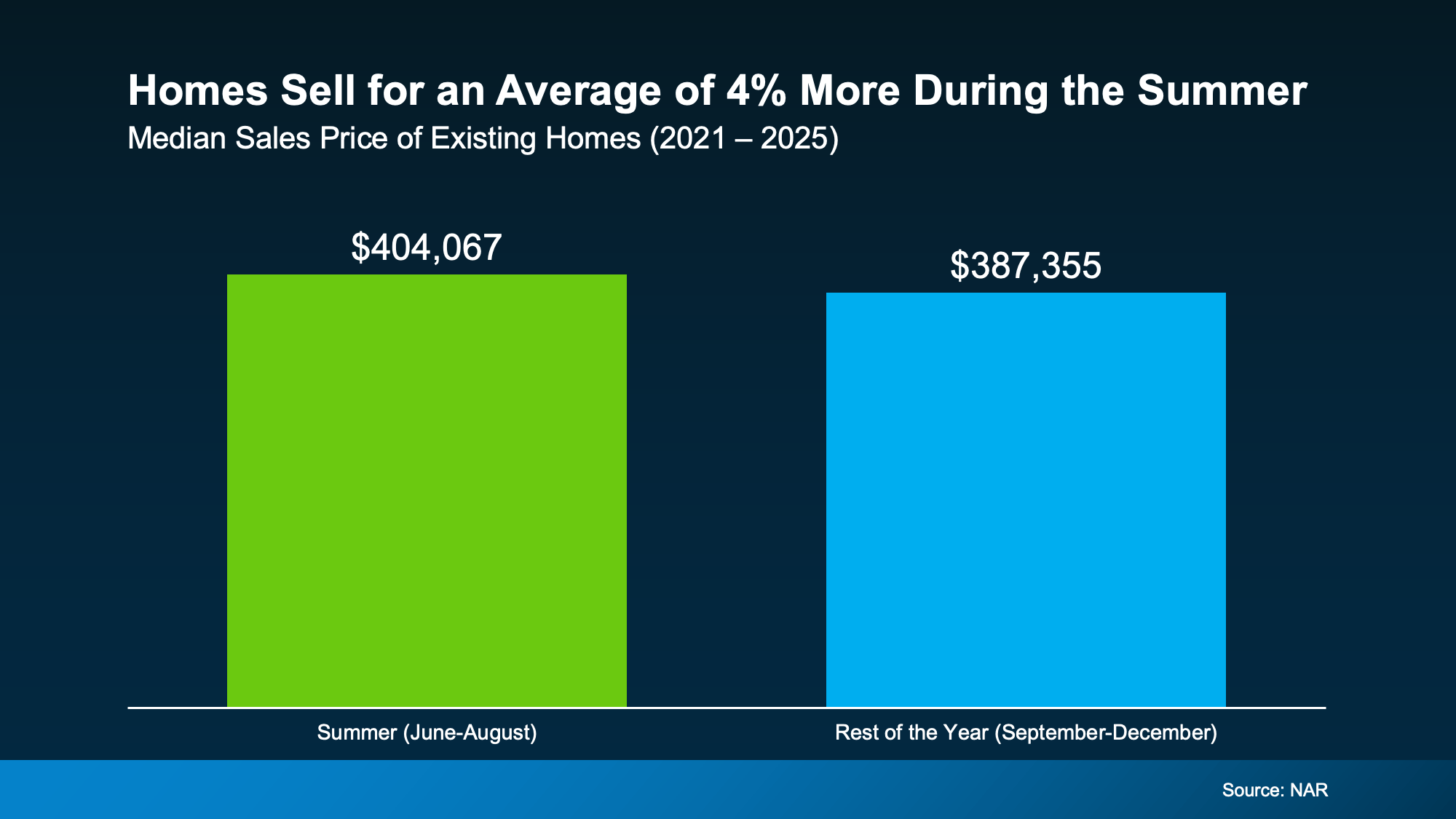

Seasonality can still work in your favor no matter where you are. And this Summer could still give you the chance to sell for a good price.

According to the National Association of Realtors (NAR), homes sold during a Summer month usually sell for about 4% more than homes sold during the typical month from September-December:

Why? Summer buyers are usually operating on a set timeframe. They’re trying to move before the next school year or when they have more PTO and warmer weather to tour houses. That urgency can translate into better offers.

Now, that doesn’t mean you should price your house 4% higher this Summer. That would actually be a mistake in today’s market.

It just means if you’re looking to get as much for your house as you reasonably can, a Summer move could be a smarter play than waiting until later this year.

Because based on typical seasonality, you may get more for your house than you would if you waited until the Fall or Winter (when there are typically fewer buyers active).

And if you’re considering a move anyway, that’s worth factoring in.

Bottom Line

Could waiting until later this year work out? Sure. But it’s important to understand what you may gain by moving now too – that way you have the full picture before you decide.

If a 2026 move is on your radar, talk to an agent about what matters most to you. Depending on your priorities, Summer could be your moment.

If affordability has been the biggest thing standing between you and a home, there’s a little good news.

Asking prices have started to come down.

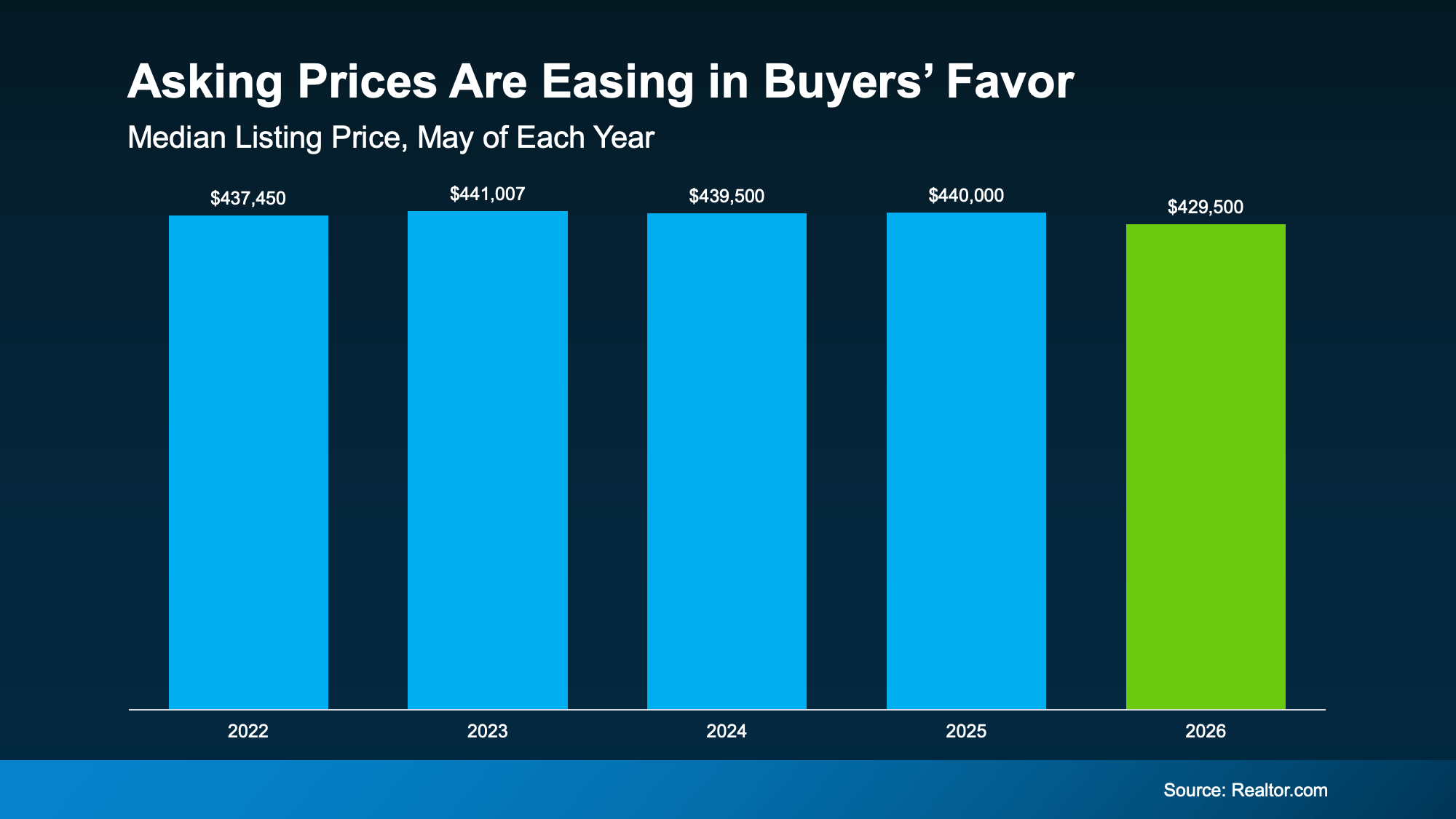

The typical seller listed their house for a median of $429,500 in May. That’s 2.4% lower than a year ago, according to Realtor.com. On its own, that won’t transform what you can afford, but in today’s market every little bit helps and it signals a broader shift taking place.

Buyers Are Finally Catching a Break

Check out this data from Realtor.com and you can see this is the first May in years where buyers have caught any sort of break price-wise.

Each May from 2022-2025, things held pretty steady. But this year? You can see that more noticeable shift in your favor (see graph below):

While the dip from $440,000 to $429,500 isn’t a big one, it gives you more breathing room. And that’s not a small thing when affordability has been this tough.

Now, lower asking prices don’t mean every home is suddenly within your range. But they do show buyers are gaining a little ground.

And in today’s market, a little ground can go a long way.

What That Means for the Housing Market

And just in case this crossed your mind, this is good news for your move, not bad news for the market as a whole.

The subtle dip from last May to this one shows prices are easing, but they’re not dropping off a cliff. What this is actually a sign of is that the market’s rebalancing now that the number of homes for sale has grown.

Buyers have a bit more power again, and sellers know they can’t name just any price and expect their house to sell. They either meet the market where it is, or face a price cut later. And in general, sellers would rather avoid a price cut. As the New York Post explains:

“Rather than swinging for the fences with pandemic-era price tags, sellers are increasingly coming to terms with a new reality. The share of listings featuring price cuts actually fell to 17.5% in May, suggesting homeowners are doing their homework before putting up a “For Sale” sign instead of chasing unrealistic numbers and cutting later.“

This signals a broader change in the market.

Seller expectations have been skewed a little high since the pandemic buying frenzy – you’ve probably felt that firsthand. But now, things are starting to normalize. It could mean less back-and-forth to land on a fair number. And homes should be priced a bit more realistically from the start.

Bottom Line

If affordability has been your top concern, the recent dip in prices is an opening. Connect with a local real estate agent to see what that looks like in your area.

Whether you’re dreaming about buying your first home or wondering if it’s time to move on from the one you’re in, affordability is probably weighing on your mind. Home prices are still high in many markets, and even though things have improved a bit over the past year, making the numbers work can still feel like a stretch.

But the people finding ways to move right now usually have one thing in common. They didn’t wait for affordability to come to them. They went looking for it.

According to PODS, 61% of people across all generations say affordability is the biggest factor when deciding where to move. And it’s led a growing number of people to do one thing – broaden their search to include more affordable areas they hadn’t seriously considered before. As PODS, put it:

“. . . moving is increasingly driven by affordability, connection, and quality of life. As economic pressures persist, Americans are taking a more intentional, values-driven approach to where they choose to live.”

It’s Not Just the Home Price – It’s the Whole Cost of Living

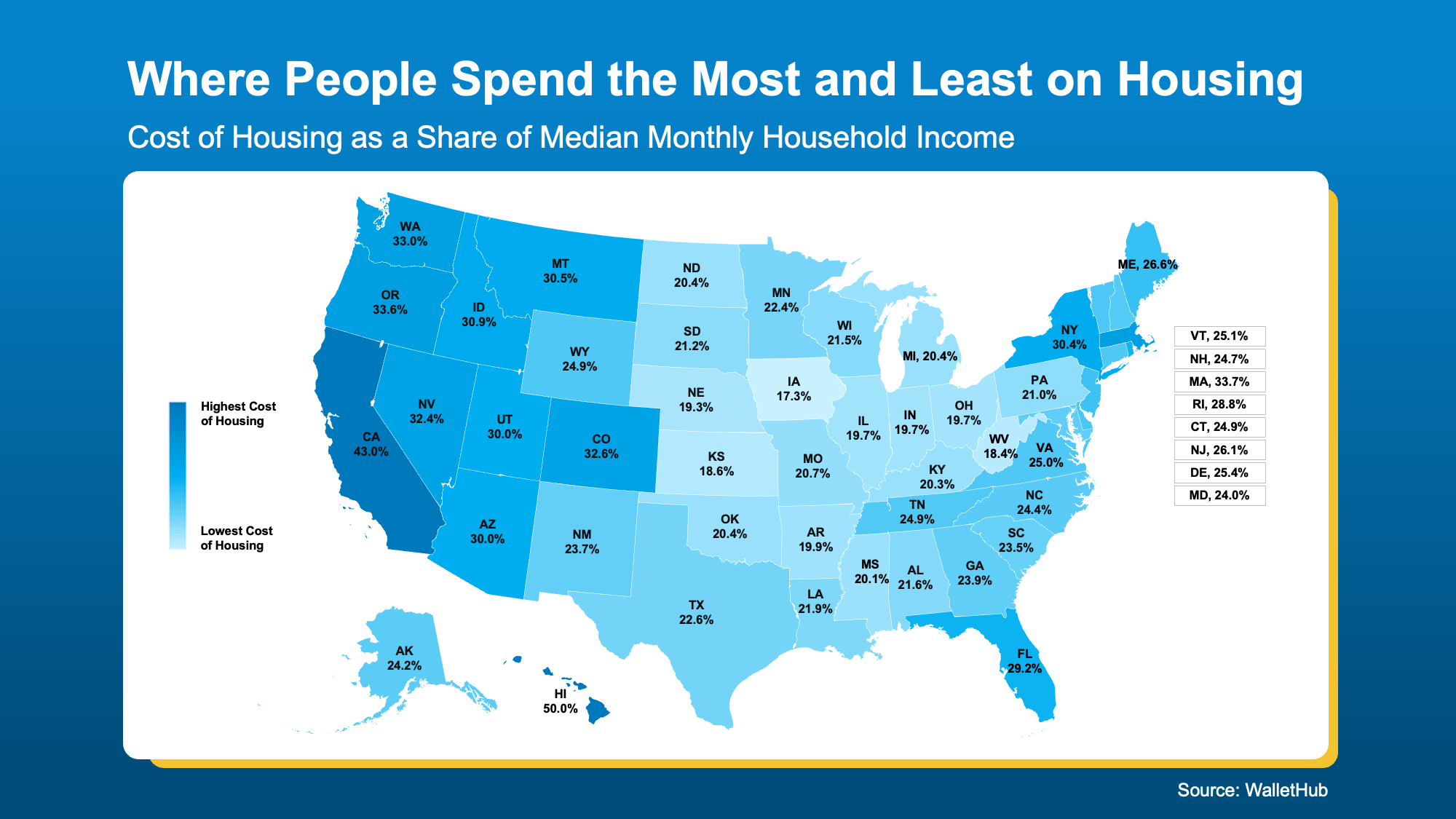

Here’s where it gets really interesting. When people talk about moving for affordability, they’re not just talking about finding a cheaper house. They’re thinking about the full picture. What does it actually cost to live somewhere?

WalletHub looked at exactly this, measuring housing costs as a share of median monthly household income across every state (see map below).

Take a look at where you live on that map. The lighter the blue, the more affordable it generally is to live there. The darker the blue? Just the opposite.

If your state is showing up on the darker blue end of the scale, the cost of living may be putting a real pinch on your wallet, and it may be worth exploring what a lighter-blue area could mean for your finances.

Because if you’re less financially stretched, imagine how that could change things. Less stress. Less worry. More freedom and peace of mind.

You Don’t Have To Move to Another State To Find a Better Deal

But finding more affordable homeownership doesn’t have to mean a cross-country move. It doesn’t even have to mean leaving your state, your family, or your favorite coffee shop behind.

Every market has more affordable pockets that most buyers never think to explore – neighborhoods, towns, and communities where home prices are lower, property taxes are more manageable, and the overall cost of living just works better.

A great local real estate agent knows exactly where those places are.

And if you work remotely, or have any flexibility in where you’re based, your options open up even further. Remote work has already changed the way millions of people think about where to live, and that trend isn’t going away.

When location stops being tied to a daily commute, a more affordable area that’s a bit farther out suddenly becomes a very real option.

Bottom Line

Affordability is a real challenge, but it’s not an unsolvable one. The key is being open to places you might not have considered before. A local real estate agent can help you find them.

Ready to find out which areas have the best affordability right now? Reach out today.

Two Big Reasons To Move This Summer

Lower Asking Prices Are a Win for Today’s Buyers

Could Moving a Bit Further Out Change Everything About Your Budget?

-

Equity4 weeks ago

Equity4 weeks agoRecord High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out.

-

Equity4 weeks ago

Equity4 weeks agoAre Home Prices Going To Fall?

-

Affordability4 weeks ago

Affordability4 weeks agoNewly Built Home Prices Hit a 5-Year Low

-

Affordability3 weeks ago

Affordability3 weeks agoWhat Most Veterans Don’t Know About Their VA Home Loan Benefit

-

Affordability3 weeks ago

Affordability3 weeks agoThe Truth About Affordability Today

-

For Sellers3 weeks ago

For Sellers3 weeks agoThe Real Reason Some People Are Still Moving Right Now

-

Economy2 weeks ago

Economy2 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability2 weeks ago

Affordability2 weeks agoWhat Rising Inflation Means for Your Move

You must be logged in to post a comment Login