Equity

How Much Home Equity Have You Gained? The Answer Might Surprise You

Have you ever stopped to think about how much wealth you’ve built up just from being a homeowner? As home values rise, so does your net worth. And, if you’ve been in your house for a few years (or longer), there’s a good chance you’re sitting on a pile of equity — maybe even more than you realize.

What Is Home Equity?

Home equity is the difference between what your house is worth and what you owe on your mortgage. For example, if your house is worth $500,000 and you still owe $200,000 on your home loan, you have $300,000 in equity. It’s essentially the wealth you’ve built through homeownership. Right now, homeowners across the country are seeing record amounts of equity.

According to Intercontinental Exchange (ICE), the average homeowner with a mortgage has $319,000 in home equity.

Why Have Homeowners Gained So Much Equity?

The rise in home equity over the years can be credited to two key factors:

1. Significant Home Price Growth

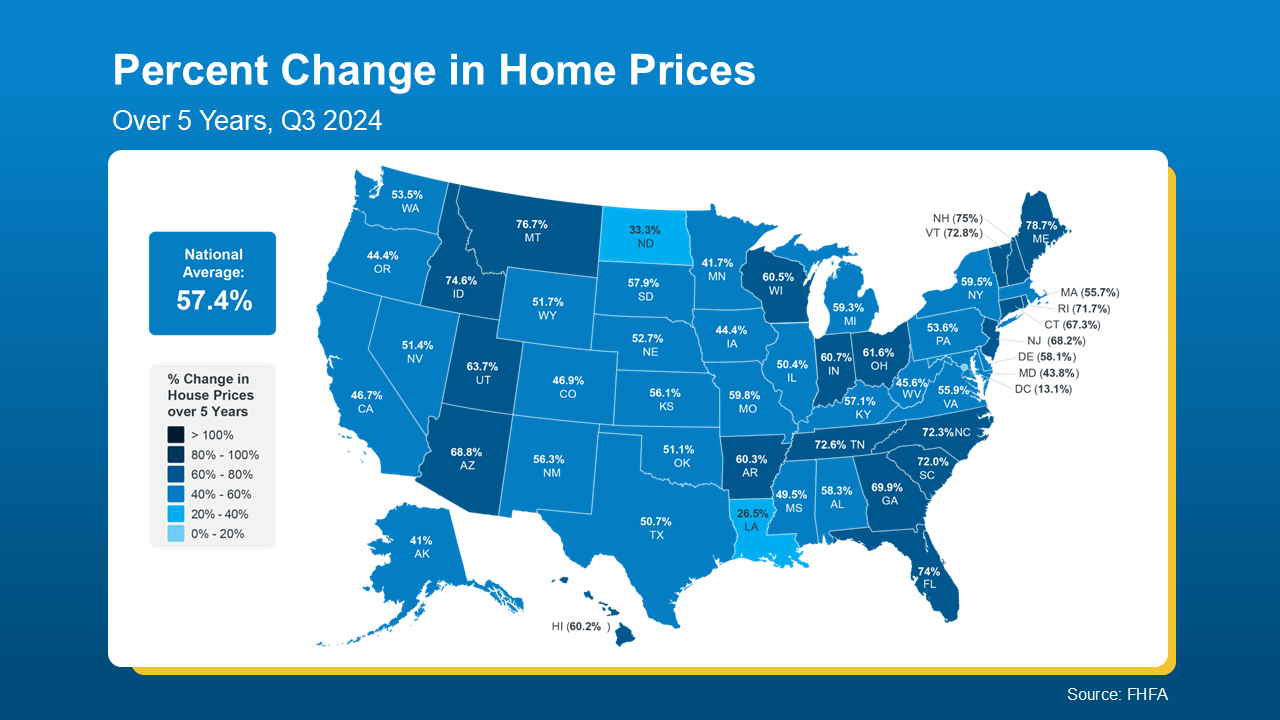

Home prices have climbed dramatically in recent years. In fact, according to the Federal Housing Finance Agency (FHFA), over the past five years, home prices nationwide have risen by 57.4% (see map below):

This appreciation means your house is likely worth much more now than when you first bought it.

This appreciation means your house is likely worth much more now than when you first bought it.

2. Longer Tenure in Homes

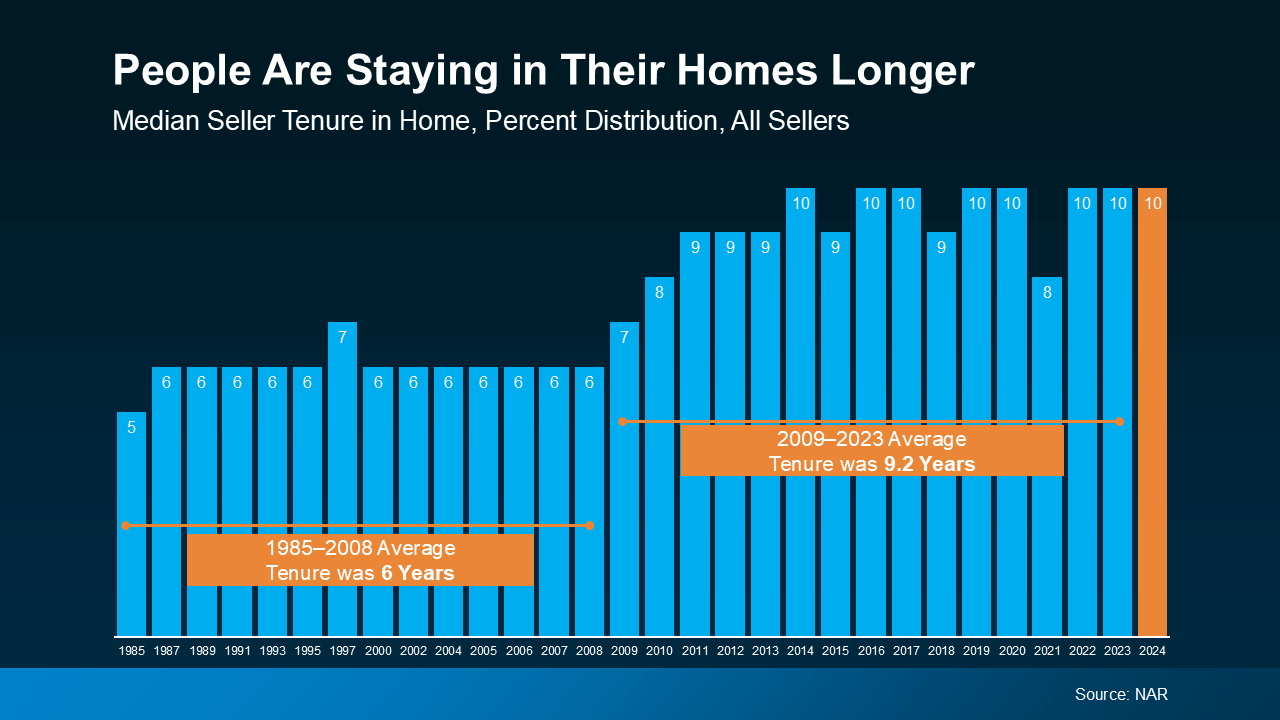

Data from the National Association of Realtors (NAR) shows people are staying in their homes for a decade (see graph below):

This increased tenure means homeowners benefit even more from home values growing over time. That’s because the longer someone has lived in their house, the more that home’s value has grown, which directly increases equity.

This increased tenure means homeowners benefit even more from home values growing over time. That’s because the longer someone has lived in their house, the more that home’s value has grown, which directly increases equity.

And if you’re one of those people who’s been in their home for 10 years or more, know this – according to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

The Benefits of Having Home Equity

What does that mean for you? It means your house might be your biggest financial asset — and it could open up some exciting opportunities for your future. Let’s break it down.

- Moving to Your Next Home

Your equity could help you cover the down payment for your next home. In some cases, it might even mean you can buy your next house all cash.

- Financing Home Improvements

Thinking about upgrading your kitchen, adding a home office, or tackling other projects? Your equity can provide the funds to make those improvements happen, increasing your home’s value and making it more enjoyable to live in too.

- Getting a Business Going

If you’ve been dreaming about starting your own business, your equity could be the kickstart you need. Whether it’s for startup costs, equipment, or marketing, leveraging your home’s value can help bring your entrepreneurial goals to life.

Bottom Line

Whether you’re thinking about selling, upgrading, or simply want to understand your options, your home equity is a powerful resource. If you’re wondering how much equity you’ve built or how you can use it to meet your goals, connect with a local real estate agent to explore the possibilities.

That kitchen you’ve been mentally redesigning…

The bathroom that really needs a refresh…

Or the outdoor space you keep saying you’ll get to someday…

What if you already have what you need to finally make it happen? Because a growing number of homeowners are realizing just that.

Homeowners are expected to spend over $522 billion on home improvements by the end of 2026 – and they’re not draining their savings accounts to get it done. Many are using their home equity.

And if you’ve owned your home for 10+ years, there’s a chance you could use your equity to fund some home upgrades too. Let’s break down what you need to know first.

What Is Equity? And How Does It Help?

Equity is the difference between what your house is worth and what you owe on your mortgage.

And according to Cotality, the average homeowner has about $313,000 worth of equity today. That’s more than enough to finally knock some projects off your list. And more people are realizing they can use that to give their home a little TLC.

Research coming out of Meridian Link says home improvements are the top thing people are using their equity for today.

Top Motivations for Equity-Based Borrowing:

- Funding home improvements (45%)

- Using it to pay down other debts / debt consolidation (16%)

- Investing in other properties (16%)

Maybe it makes sense for you to do the same. But here’s what’s important. Just because you can use your equity doesn’t mean you have to. It also doesn’t mean every project makes sense.

What Projects Are Actually Worth It?

If you’re going to go this route, you’ll want to focus on upgrades that actually pay off. A good renovation should be something that improves the value of your home. Because, even if you’re not planning to sell soon, you want to make sure you’re setting yourself up for success when you do.

And an agent is the best resource as you weigh your options. They know what other homeowners are doing and what buyers in your area like. And that can be really helpful as you narrow down your project list. As the National Association of Realtors (NAR) puts it:

“Being able to help sellers prioritize home improvements and maximize their net on the sale is a key value real estate agents offer.”

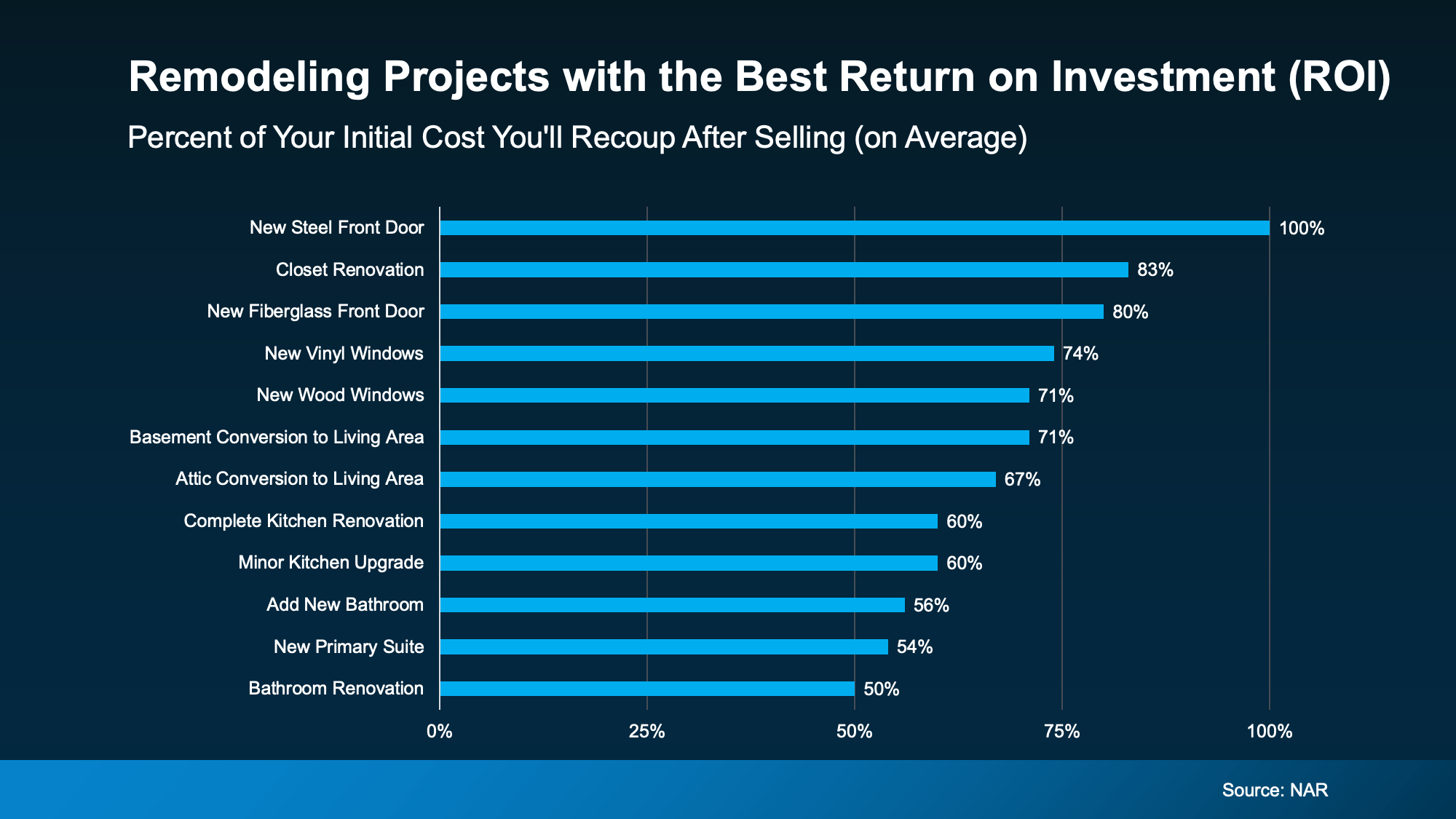

Here’s a quick rundown of the projects with the best potential to recoup your costs according to NAR (see graph below). While it’s a good starting point, just remember it can’t match the expertise an agent can provide.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

A new front door is a great project. But it’s not something to use your equity for. But revamping your kitchen? That’s where your equity can come in and lighten the load.

Where To Go from Here

Whether the project you’ve been thinking about is on this list or not, chat with an agent to make sure it’s worth the time, money, and effort before calling in any contractors.

Because the goal isn’t to do everything, it’s to invest where it counts.

And if you want to use your equity to get one of the bigger projects done, meet with a financial advisor too. Because you’ll want to make sure you’ll maintain a good loan-to-value (LTV) threshold even after using your equity. That way you have all the information you need to make your decision.

Bottom Line

Whether you’re selling next year or just giving your house some TLC, the right home improvements today can set you up for success tomorrow. And the best part? Your equity may be the key to making it happen.

What’s one upgrade you’ve been thinking about – and wondering if it’s worth it?

Have a quick conversation with an agent to find out if it’s the right decision for your home.

You’ve probably seen posts on social media talking about how “home prices are falling.” And when you see something like that, it’s normal to wonder:

Is this the start of a crash?

What does this mean for my house?

Let’s clear this up right away. This is not a crash. And your home is not suddenly losing a lot of value.

The National Story – Prices Are Still Going Up

Here’s what often gets left out of what you’re seeing online. While some markets are experiencing slight declines, they’re the minority. Most places are still seeing prices rise or at the very least, hold steady.

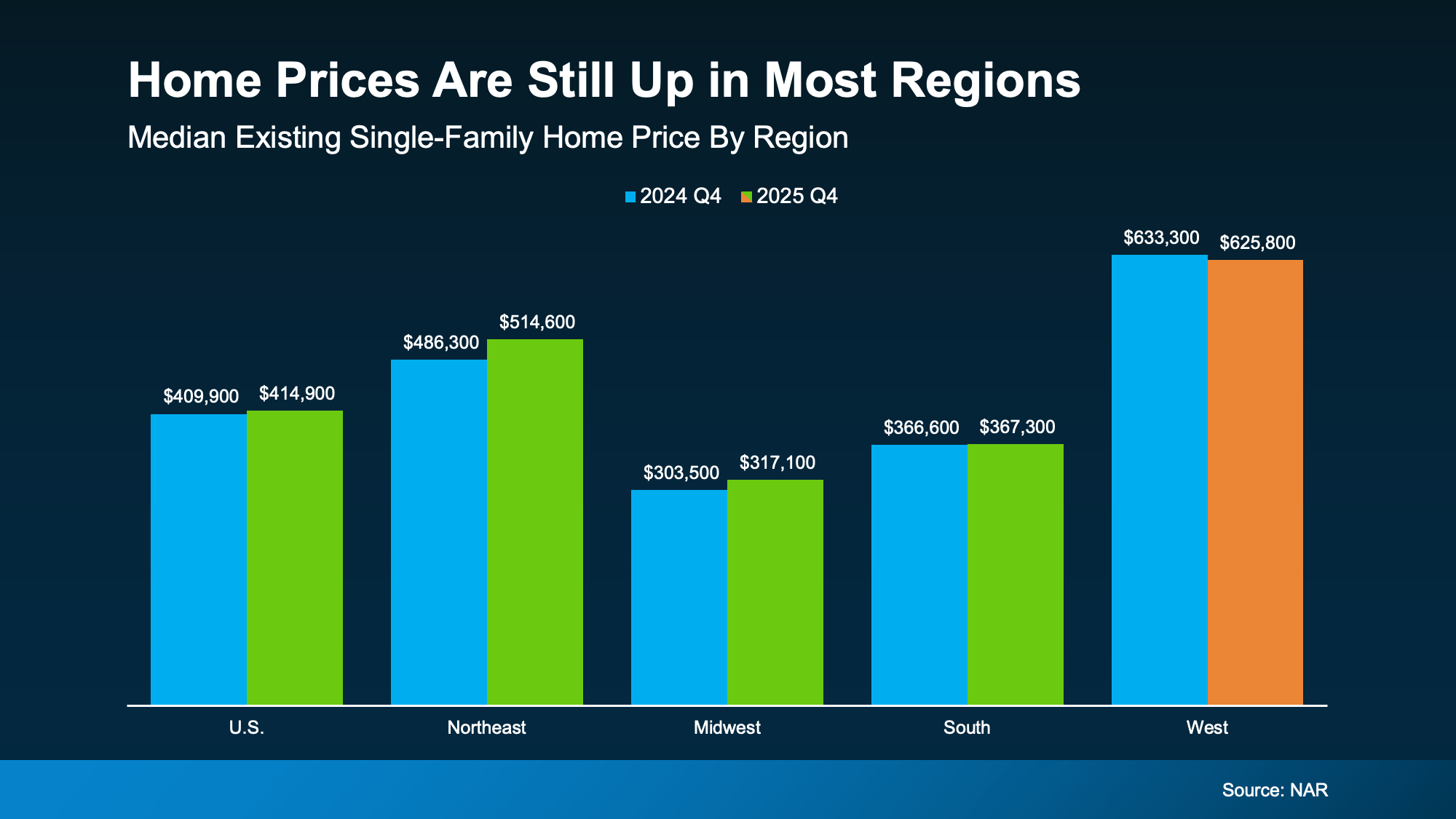

That’s why, at the national level, home prices are still rising, just at a slower pace. According to the National Association of Realtors (NAR):

“Home prices continued to rise in the fourth quarter of 2025. National median prices rose 1.2% year over year to $414,900.”

That’s not the rapid growth of a few years ago, but it’s not a downturn either. And just to really drive this home, here’s a look at the data from NAR at a regional level, so you can see that the negative narrative spun up online isn’t the whole truth (see graph below):

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

There is no wave of falling prices across the country. Instead, there are just a few pockets adjusting after several years of what’s typically considered unsustainable or exponential growth.

Yes, Some Markets Have Come Down, But Look at the Bigger Picture.

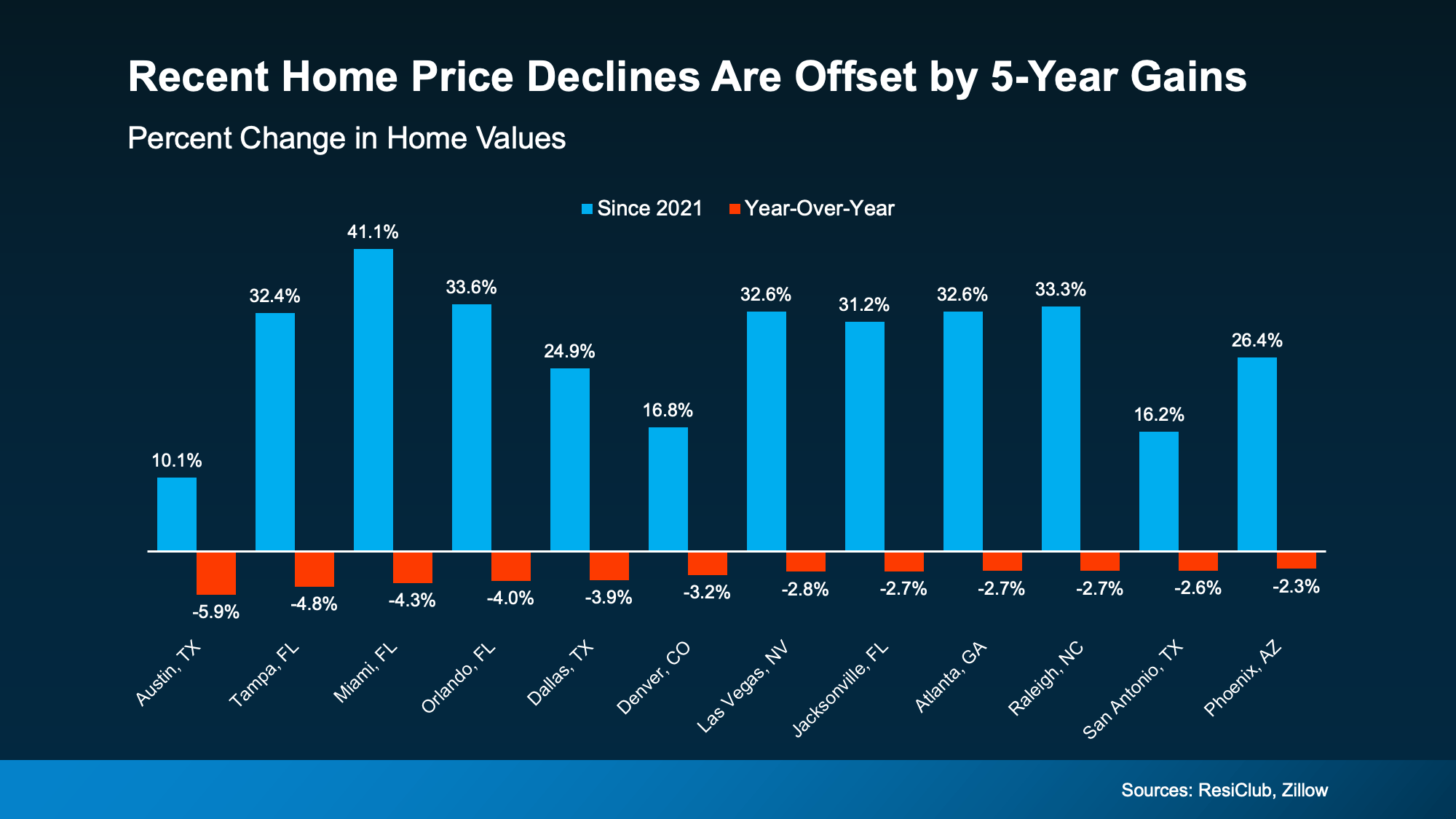

Okay, but what about the places where prices have declined? According to ResiClub and Zillow, that’s not a cause for major concern. When you zoom out and look at those same markets over the past five years, the story changes (see graph below):

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

Online chatter tends to shine a spotlight on the few areas that are down. But the bigger picture shows most homeowners are still in a very strong position.

Of course, every market, and every home, is different. But broadly speaking, home values are holding steady. And this isn’t a sign of widespread trouble in the market.

Bottom Line

Despite what you may be seeing online, home prices are rising or holding steady in most parts of the country.

If you’re curious what your home is worth today, take a look at the numbers with a local real estate agent. Because context, and local expertise, matter more than what you’re seeing online.

What if you didn’t have a mortgage payment on your next house? It may sound a little unrealistic. But for a number of homeowners, it’s actually doable.

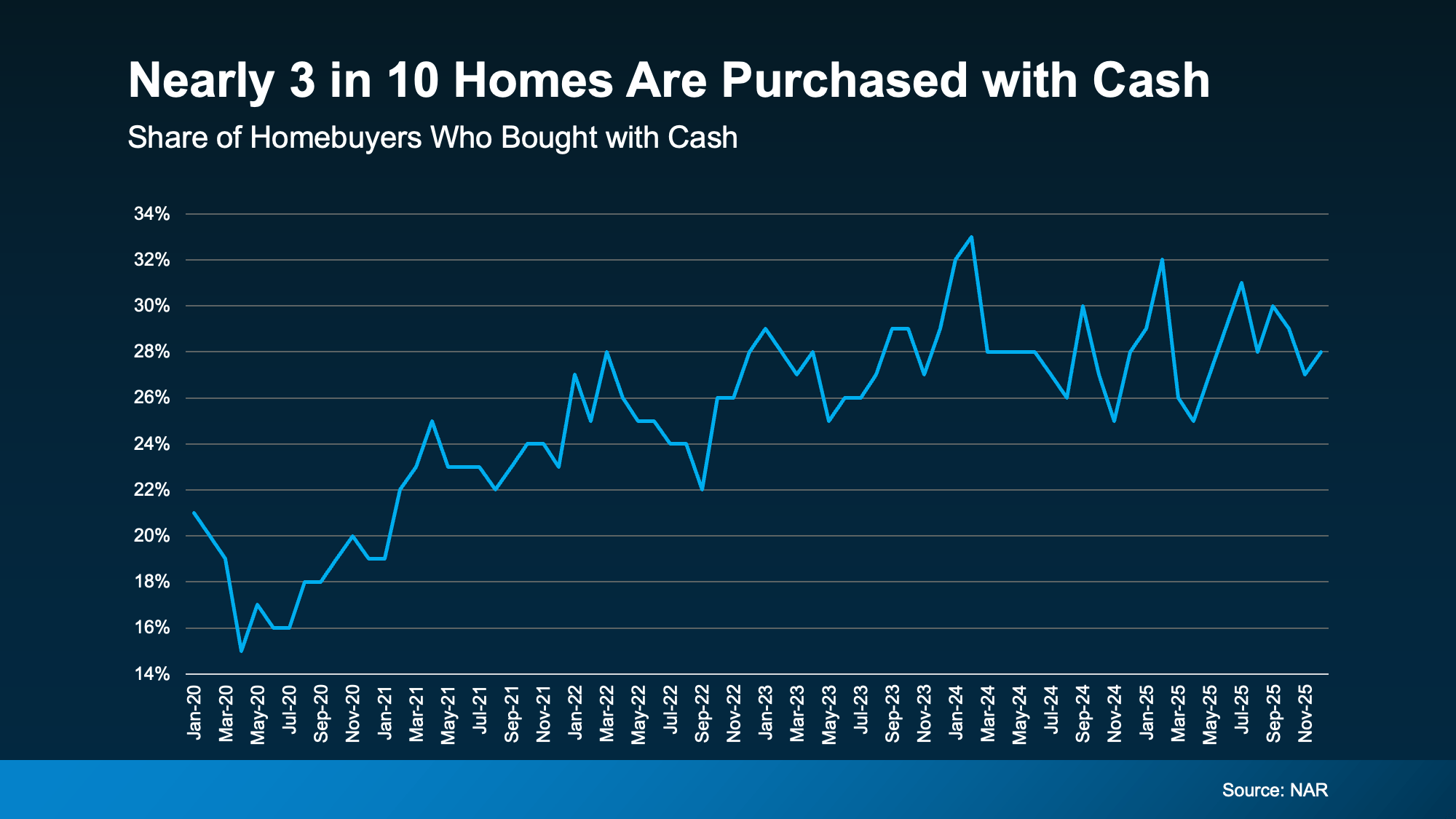

Nearly 3 in 10 homes purchased today are bought in cash, according to the National Association of Realtors (NAR). That’s far more than the pre-pandemic norm (see graph below):

So, how are so many buyers pulling that off? The answer is simple: home equity.

So, how are so many buyers pulling that off? The answer is simple: home equity.

Back in 2020-2021, mortgage rates and the number of homes for sale were both at all-time lows. And that combination pushed home prices up, fast.

If you owned a home during that time, it likely gained significant value – maybe even enough to buy your next house in cash. NAR explains:

“. . . rising home equity has armed many existing homeowners with the financial leverage to make cash offers, allowing them to convert years of price appreciation into immediate purchasing power.”

Here’s why you may want to go that route yourself, if you have enough equity to do it.

1. Your Offer Becomes More Attractive

Sellers value certainty. And an all-cash offer removes one of the biggest unknowns in a transaction: financing. As Rocket Mortgage explains:

“Cash offers are attractive to sellers. Sellers often prefer to work with cash buyers if they can because they don’t have to worry about a buyer’s financing falling through at the last minute.”

In many markets, an all-cash offer can give you a serious edge.

2. You Can Close Faster

And since you don’t have to worry about underwriting, lender approvals, and loan processing, the time it takes to close shrinks. Cotality puts it this way:

“Cash buyers have always enjoyed an edge over borrowers. They remove financing risk, reduce delays, and often close in days rather than weeks.”

If the owner of the house you’re buying is already under contract on their next home or they just need to move fast (like for a new job), that speed is a real draw.

3. You Won’t Have Monthly Mortgage Payments

When you buy in cash, you don’t have to finance your purchase. That means you don’t have to worry about what today’s mortgage rates are and you own the house outright from the day you close. And that’s a big deal.

No mortgage.

No monthly payment.

Full ownership.

That financial freedom opens the door for other big lifestyle benefits. Zillow explains:

“Paying in cash means you own your home outright. This eliminates the need for monthly mortgage payments, freeing up your finances for other priorities like savings, travel, or home improvements.”

4. You May Get a Better Deal

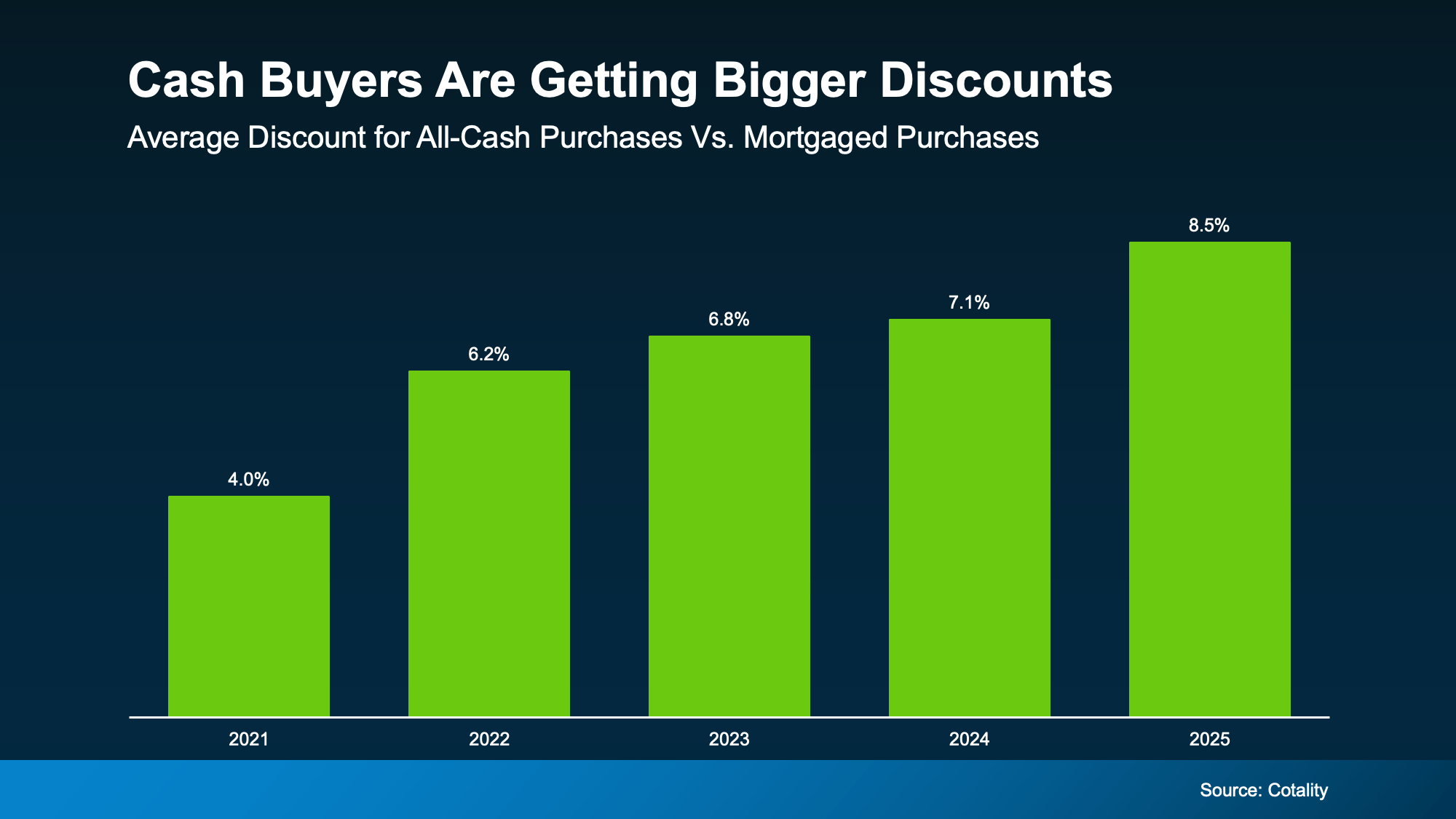

And here’s one more thing that surprises a lot of homeowners: cash buyers often pay less for the house.

According to Cotality, all-cash buyers tend to spend roughly 9% less on the house than buyers who use a mortgage. That’s because some sellers are willing to accept lower offers to get a deal done quickly, with more certainty of closing, and fewer financing hoops to jump through. As Cotality explains:

“From a seller’s point of view, a lower but reliable offer can feel preferable to a higher one that may collapse weeks later.”

And that advantage grows with each passing year (see graph below):

Is an All-Cash Move Realistic for You?

Is an All-Cash Move Realistic for You?

Not every homeowner will buy their next house outright in cash. And that’s okay.

But the bigger takeaway is this: the equity you’ve built may give you more options than you think.

Whether that means downsizing and eliminating a mortgage entirely, or just relocating with stronger negotiating power, your current house may be what makes it possible.

Bottom Line

Before assuming you’ll need another traditional mortgage, it’s worth asking one simple question: How much equity do you really have? Because the answer might change what you thought your next move could look like.

Curious what your home equity could do for you? Ask a local real estate agent to run the numbers and see what kind of buying power you’re really sitting on.

The Remodel You’ve Been Dreaming About May Be Closer Than You Think

Affordability Has Improved in All 50 States

3 Must-Do’s for First-Time Home Buyers

-

Affordability4 weeks ago

Affordability4 weeks agoRenting vs. Buying: The Numbers Might Surprise You

-

For Sellers4 weeks ago

For Sellers4 weeks agoTop Mistakes Homeowners Are Making in 2026 (And How To Avoid Them)

-

Equity4 weeks ago

Equity4 weeks agoHow Your Equity Could Help Younger Generations Buy a Home

-

For Sellers3 weeks ago

For Sellers3 weeks agoSpring Sellers Have an Edge. Here’s Why.

-

Downsize3 weeks ago

Downsize3 weeks agoThe Hidden Advantage Repeat Buyers Have Right Now

-

Equity3 weeks ago

Equity3 weeks agoAre Home Prices Dropping? Here’s the Real Story.

-

Agent Value2 weeks ago

Agent Value2 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability2 weeks ago

Affordability2 weeks agoShould You Wait for Lower Rates?

You must be logged in to post a comment Login