For Buyers

One Homebuying Step You Don’t Want To Skip: Pre-Approval

Student loans are back in the spotlight. And whether you’ve been following the headlines closely or just catching bits and pieces here and there, there’s a good chance they’ve been on your mind lately.

And if you’re questioning whether you have to hit pause on your plans to buy a home, here’s the thing you have to remember:

Having student loans doesn’t automatically mean buying a home has to wait.

The Biggest Myth About Student Loans and Buying a Home

One of the most common misconceptions among first-time buyers is that they have to pay off their student loans before they can qualify for a mortgage. But in most cases, that’s just not true.

As an article from Redfin explains, student loans usually get evaluated the same way other debts do, like credit cards or car payments:

“Yes, you can get a mortgage with student loan debt. Lenders primarily assess your debt-to-income (DTI) ratio, which compares your monthly debt payments, including student loans, to your gross monthly income. Having student debt doesn’t automatically disqualify you if your DTI is within acceptable limits.”

So having that loan on your credit report isn’t some special red flag that immediately disqualifies you.

Instead, lenders look at your overall financial situation, including your income, credit history, and more. Student loans are one piece of that puzzle, but they’re not the entire picture.

You’re in Better Company Than You Think

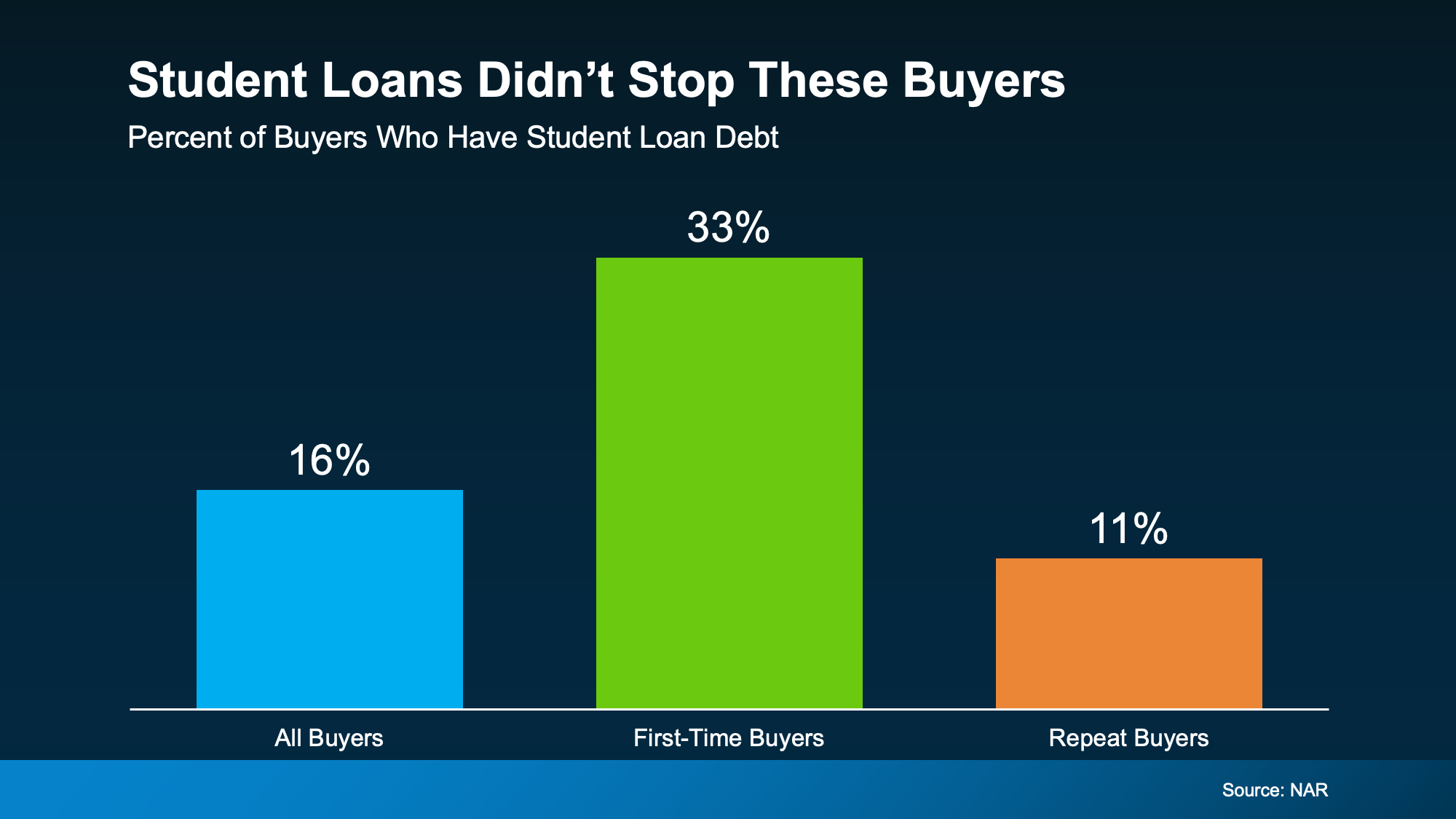

Just to really drive this home, here’s a stat from the National Association of Realtors (NAR) that proves you can have student debt and still buy a home. Their research shows 33% of first-time homebuyers still had student loan debt.

That’s 1 out of every 3 first-time buyers. The median amount they owed? $30,400.

Let that reassure you that people are buying homes with student debt every day. And carrying student loans doesn’t automatically put homeownership out of reach.

Don’t Count Yourself Out Before You Even Try

At the end of the day, here’s where a lot of buyers trip themselves up. They assume the worst and never even check what they could actually qualify for. But your situation is more unique than a blanket “no.”

If your income is steady and the rest of your finances are in decent shape, buying a home could be more realistic than you think. The only way to know for sure is to actually run the numbers with someone who does this for a living.

You may discover you’re closer to buying than you think.

Bottom Line

Student loans don’t have to be the thing standing between you and owning a home. If you’ve been putting off your homebuying plans because of that debt, talk to a lender about your options. It may not be the barrier you think it is.

Buying or selling a home is a big financial decision. And right now, it feels even bigger. Inflation is high, costs are high, and you want to be sure the timing is right before you make your move.

But if you do decide to go for it, whether you’re buying or selling, here’s something reassuring to hold onto. Not only does your move change your own life, but it also gives your whole community a boost.

Real estate is a huge part of the economy. In 2025, it added up to about $5.6 trillion, according to the National Association of Realtors (NAR). A good share of that comes from everyday people buying and selling homes, just like you.

Your Move Puts Real Money Into the Local Economy

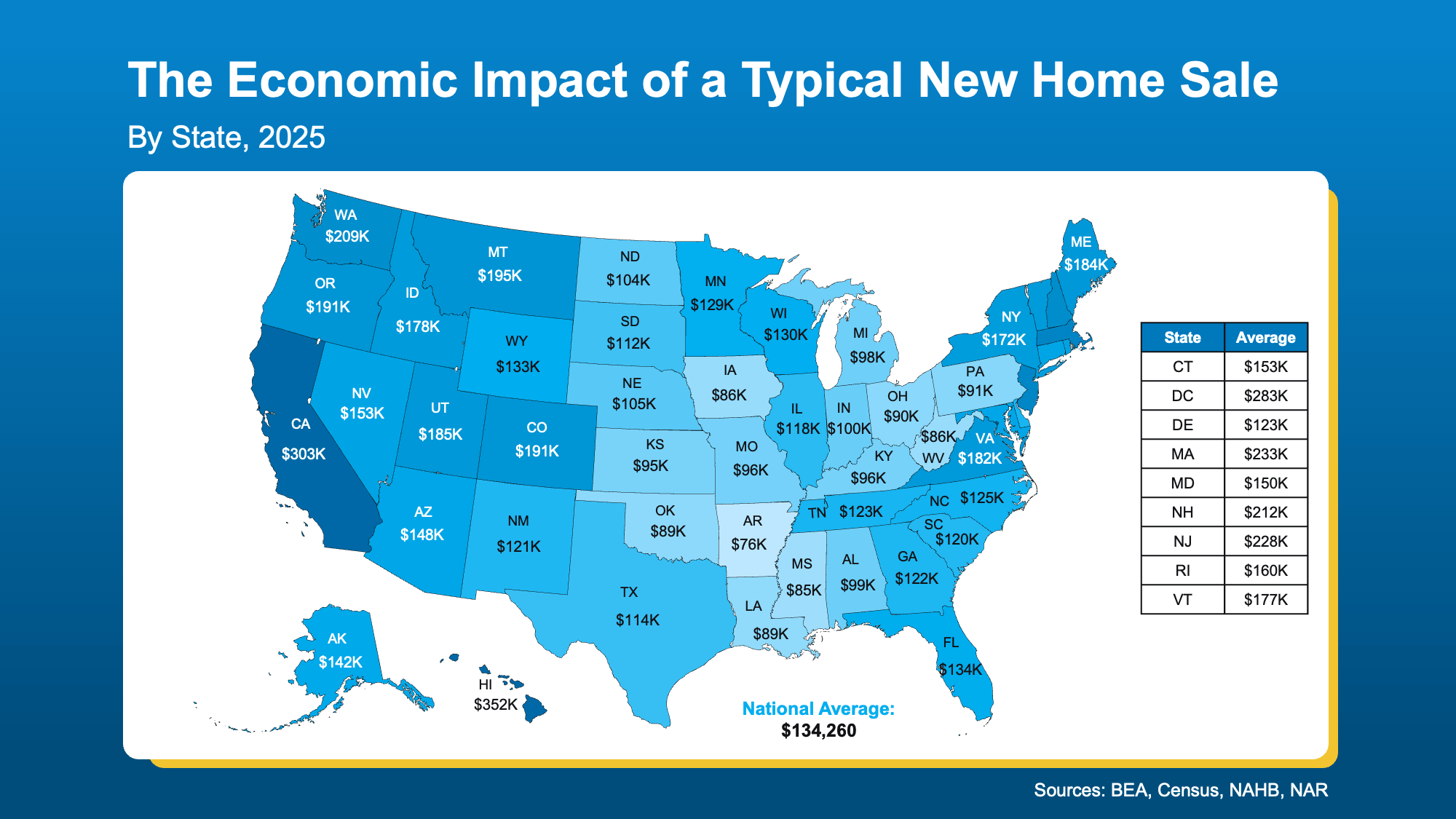

Every sale sends money flowing through your area. NAR data shows that buying an existing home (one that’s already been lived in) adds about $64,000 to the local economy. Buy a newly built home, and that number climbs to more than $134,000 (see graph below):

Over half of that comes from the work of building the home itself. The rest flows to real estate services, like agent and lender fees, plus what you spend settling in afterward, on things like furniture and remodeling.

And the money doesn’t stop there. As local businesses earn it, they spend it again in your area, so a single sale ripples further than the sale price alone.

One Sale Keeps a Lot of People Working

Behind every sale is a whole network of people doing their jobs. Contractors, lenders, inspectors, movers, and more. When you buy or sell, you help keep them busy. Lawrence Yun, Chief Economist at NAR, puts it this way:

“Increased home sales mean more economic activity — lawn care, furniture purchases, moving services, mortgage originations and other related business activities all get a boost.“

So, your move supports your neighbors’ livelihoods, too. The deal that gets you into your next home also helps a local crew make payroll. In a year when every paycheck counts, that’s no small thing.

Your Local Impact May Be Even Bigger

What your move financially adds to your community depends a lot on where you live. To help you see how it can vary, here’s a look at the impact of a typical newly built home sale by state.

The national average for a newly built home is about $134,000, but some states see far more (see map below):

In California, a single sale adds more than $300,000 to the local economy. In Hawaii, it’s over $350,000. Even in the most affordable states, the number lands in the tens of thousands.

Want to know what a move would mean where you live? A local agent can show you the figure close to home.

Bottom Line

Moving is both a personal milestone and an investment in your community. So, if the time is right for you, connect with a local agent. You’ll make a difference for more people than you know.

Saving for a down payment can feel like the hardest part of buying a home. And with affordability as tight as it’s been lately, it’s fair to wonder how anyone manages it right now. Here’s something you may not have seen coming.

Some people are getting their foot in the door with a smaller down payment.

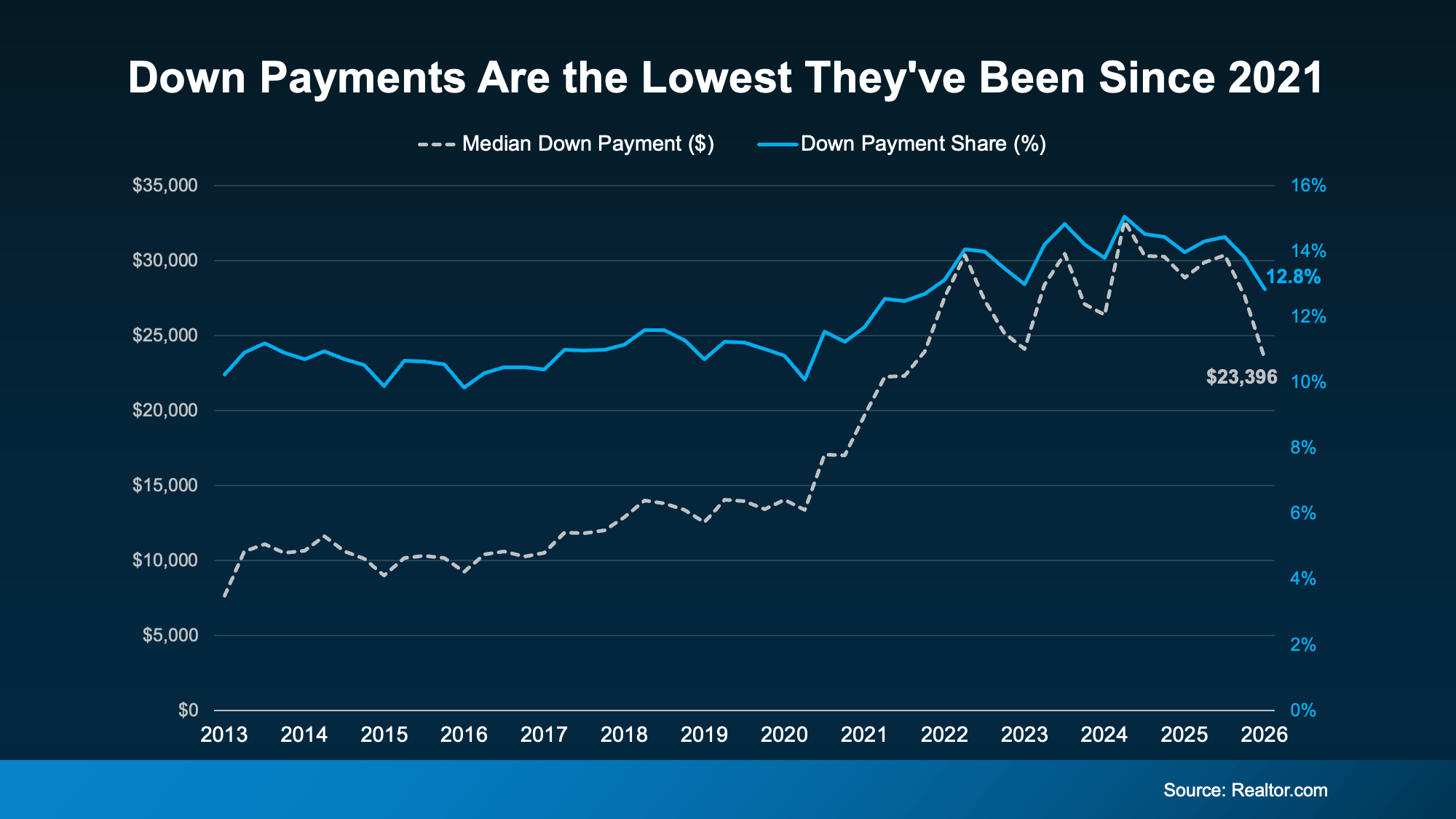

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that’s around $5,000 below what was typical the year before (a 19% drop year over year). That’s the lowest down payments have been since 2021 (see graph below):

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

There are a few things driving the trend:

-

Less competition between buyers. Part of it comes down to a more balanced market. With buyers facing less competition than they did a few years ago, there’s less pressure to put a big sum down just to stand out.

-

More moderate home prices. Your down payment is a percentage of the purchase price. So, as price growth cools, the amount you need to put down may change too. In a lot of markets, prices have slowed or leveled off, and some areas are even seeing slight dips. That can translate into smaller down payments.

-

Buyers opting for loans with lower down payments. More buyers are also turning to government-backed loans, like FHA and VA, which often need little or no money down. FHA loans have made up more than 24% of purchase mortgages for five straight quarters, and VA loans recently hit their highest share in over a decade, according to Mortgage Professional America.

But even a smaller down payment is still a significant chunk of cash, and saving it can be hard. So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

Help You May Not Know You Qualify For

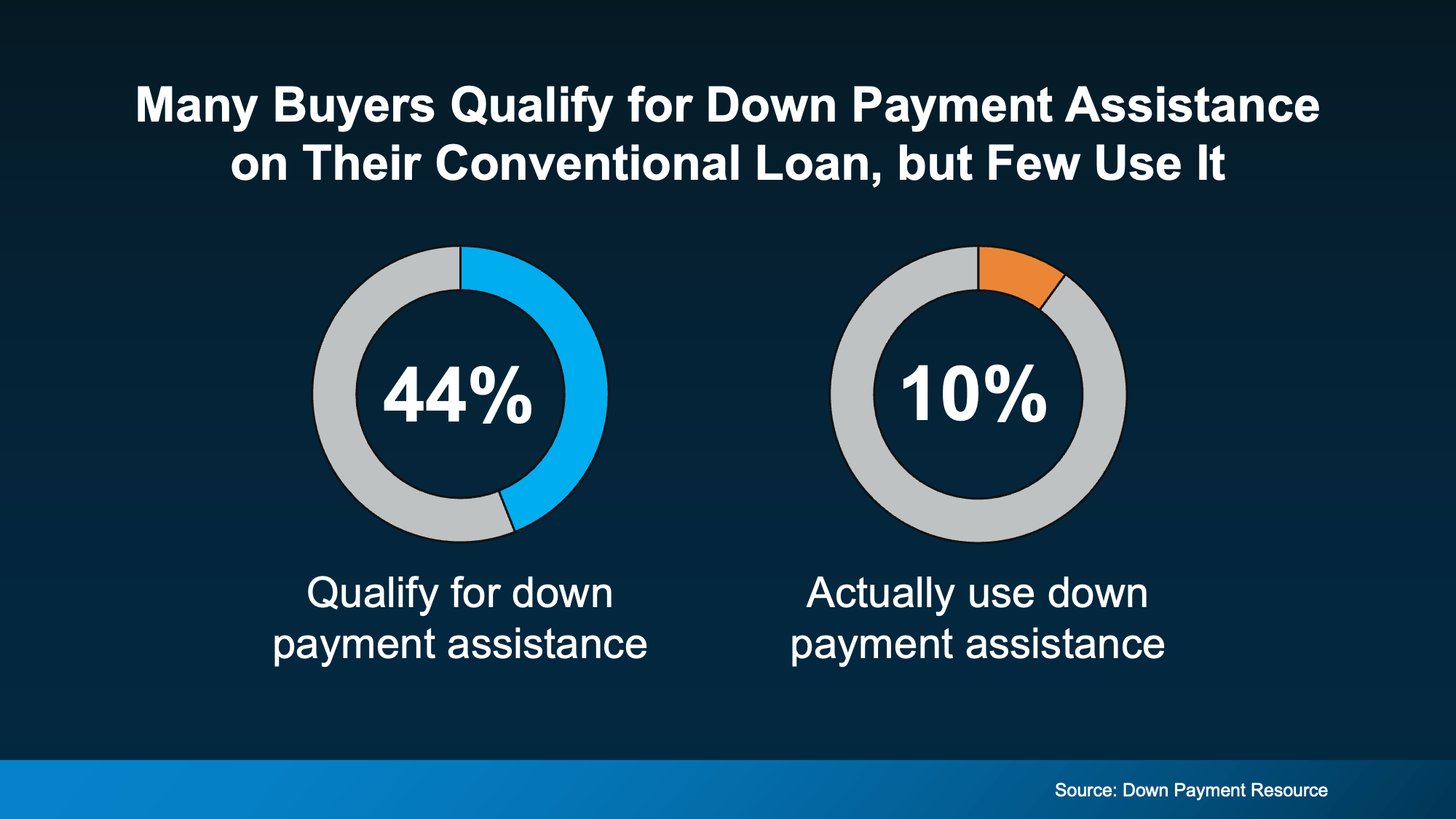

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

-

There are more than 2,600 down payment assistance programs available

-

More than half (62%) are designed to help first-time buyers

-

38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

-

62% are open to buyers earning $100,000 or more

A Boost from Loved Ones

For a growing number of buyers, help comes from closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support most often goes toward the down payment, followed by help qualifying for a mortgage and covering closing costs. Chris Birk, VP of Mortgage Insight at Veterans United, puts it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, it can make a real difference in how soon you can buy.

Bottom Line

Down payments are smaller than they’ve been in years, and that opens the door for more buyers.

And with added help from assistance programs and a little help from loved ones, you may have more ways forward than you realized. Connect with a trusted lender to talk through your options.

Student Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

What Buying or Selling a Home Gives Back to Your Community

Down Payments Are Smaller Than They’ve Been Since 2021

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoTwo Big Reasons To Move This Summer

-

Affordability4 weeks ago

Affordability4 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers3 weeks ago

For Sellers3 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers3 weeks ago

For Buyers3 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

-

Affordability2 weeks ago

Affordability2 weeks agoThat House That’s Been Sitting Could Be Your Best Shot at a Deal

-

Economy2 weeks ago

Economy2 weeks agoMore Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Agent Value3 weeks ago

Agent Value3 weeks agoIs It Still a Seller’s Market? Here’s What the Data Says.

-

Agent Value2 weeks ago

Agent Value2 weeks agoYour House Didn’t Sell. Here’s How To Turn It Around.

You must be logged in to post a comment Login