For Sellers

If Your House’s Price Is Not Compelling, It’s Not Selling

Most sellers come into the market with one number in mind. And it’s often the one that costs them the most. That’s their asking price.

A survey from Realtor.com shows about 8 in 10 (80%) of sellers expect to sell at or above their asking price today. But here’s where things get interesting.

In reality, only about 4 out of every 10 (roughly 40%) actually do.

That’s a big gap. And it’s where a lot of sellers get caught off guard. So, why the disconnect? And how can you set yourself up to be one of the 4 in 10 that get top dollar?

Let’s break it down.

What Should You Really Expect To Get for Your House?

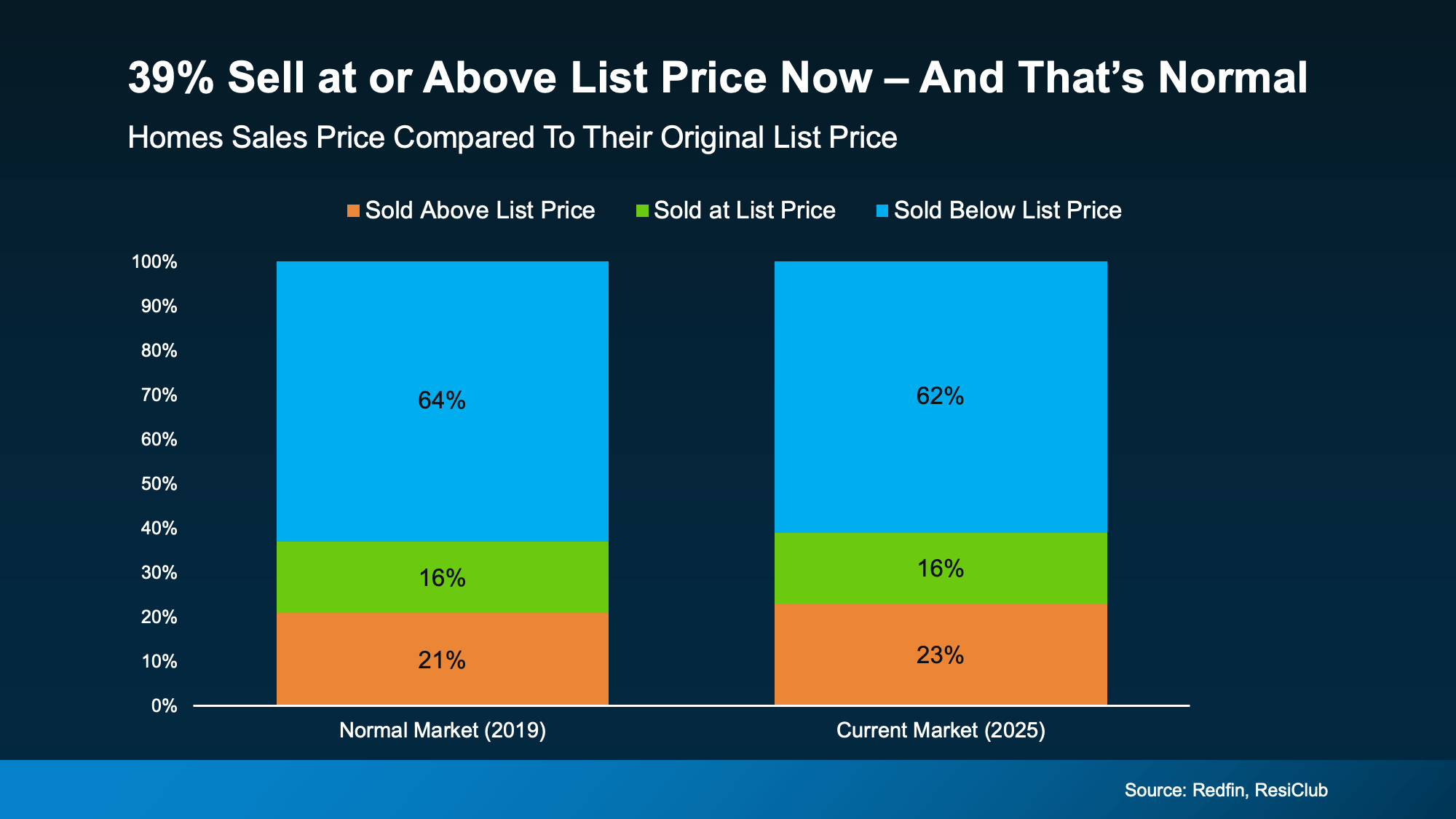

That 40% may sound low at first, but it’s not.

If you look back to the last typical year for the housing market (2019), what we’re really seeing is a return to what’s normal (see chart below). If anything, slightly more homeowners are able to sell above list price today compared to 2019:

It only feels low because the past few years were anything but typical. Between 2020 and mid-2022, buyer demand was sky-high and the number of homes for sale was at record lows. Almost everything sold over asking.

It only feels low because the past few years were anything but typical. Between 2020 and mid-2022, buyer demand was sky-high and the number of homes for sale was at record lows. Almost everything sold over asking.

Now, the market has shifted.

There are more homes for sale. Buyers have more options. And that means they’re more selective about how they spend their money.

In other words, the rules have changed – and pricing like it’s still 2021 is where sellers run into trouble. You have to meet the market where it is if you really want to cash in big.

What Happens When a Home Is Priced Too High

Here’s the reality. It’s easy to think pricing high gives you room to negotiate. But it usually does the opposite.

When your home is priced above what buyers expect, in this market, they don’t negotiate. They move on.

Because buyers notice price first. And if your home doesn’t line up with similar options in your area, it may not even get a showing. And that’s when things start to snowball:

-

A high price gets less interest from buyers.

-

Less interest means fewer offers.

-

And fewer offers usually means more time on the market.

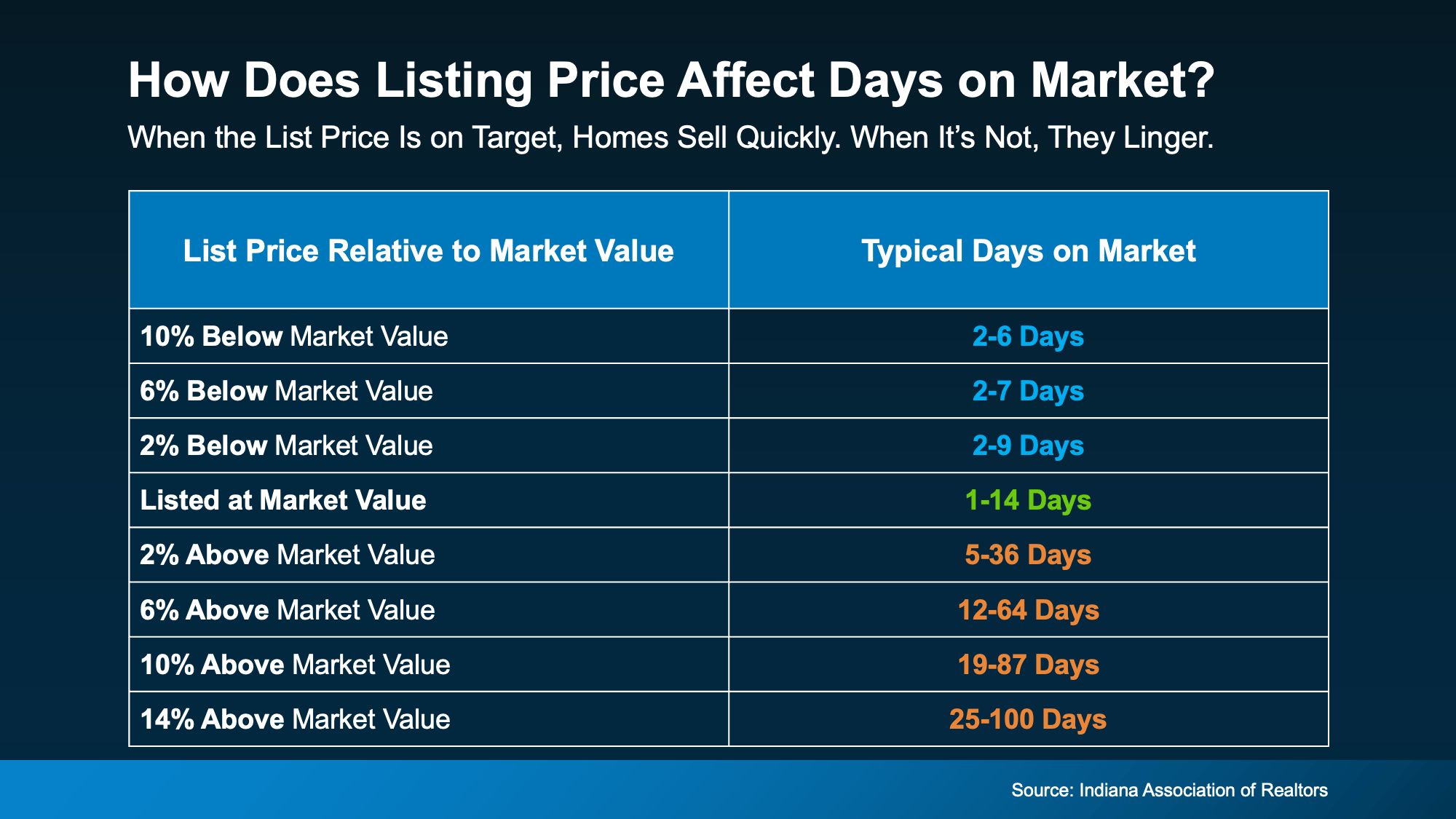

Take a look at this table from the Indiana Association of Realtors. While this data is from one state, the general trend is going to hold true across many markets in the country. It shows that homes listed at or under market value sell fast. But homes priced high? They linger. And that delay comes at a very real cost.

The Price Cut Trap (And How To Avoid It)

The Price Cut Trap (And How To Avoid It)

When a home sits that long without offers, a lot of sellers will do a price reduction. According to Realtor.com, 16.7% of sellers are going that route today.

But here’s the real problem. Even a price cut doesn’t guarantee a sale.

In fact, some buyers will see a reduction as a sign something’s wrong with the house – even when nothing is.

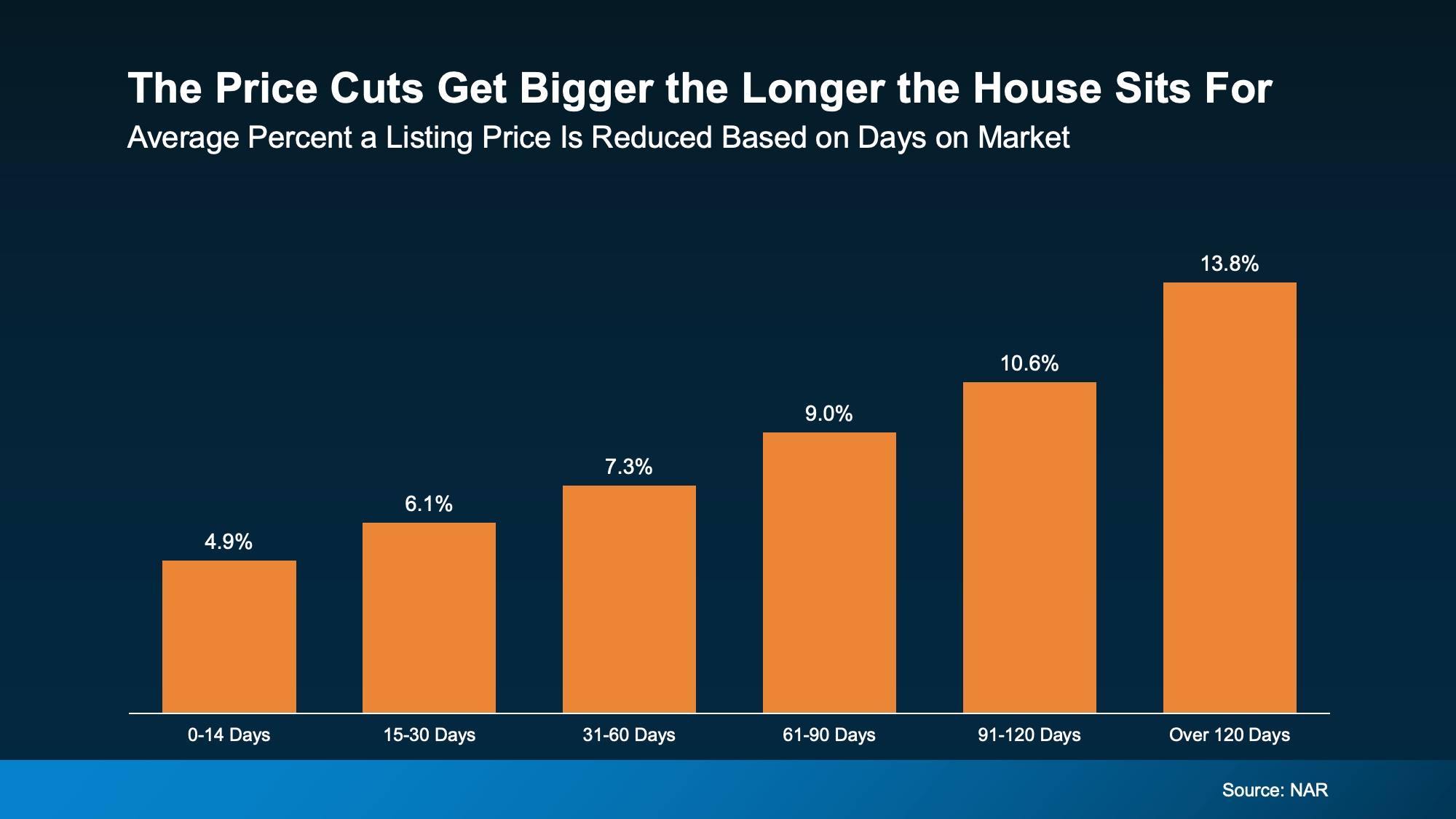

That’s why data from the National Association of Realtors (NAR) shows the longer a home sits, the bigger that price cut tends to be to attract buyers back:

So, what starts as a strategy to “leave room” for negotiate can end up costing you more in the long run.

So, what starts as a strategy to “leave room” for negotiate can end up costing you more in the long run.

Why Pricing Right from Day One Matters

Even though listing at or even just shy of market value may sound counter intuitive if you’re looking to get as much money for your house as possible, a lot of the time it really is the best strategy.

Because the goal isn’t just to list your house to see what price sticks. It’s to price it in a way that creates demand from day one.

NAR puts it best:

“While some sellers are pricing their homes higher than ever, a more ‘goldilocks’ frame of mind is a better approach to avoid price cuts and lingering time on the market.”

In other words, there’s a sweet spot. Too high, and buyers disappear. Too low, and they question the value.

But right in the middle? That’s where the magic happens.

And that’s where the right agent comes in.

They help you understand what buyers are actually paying right now, how your home compares, and how to price it so it stands out immediately. And in today’s market, that strategy is the difference between:

-

Listing high, watching it sit, and selling for less later.

-

Or, pricing it right, creating competition, and putting yourself in a position to win from the start.

Bottom Line

A lot of homeowners think they can list high now and negotiate later, but that’s a mistake that costs them. And it’s the reason only 4 out of every 10 sellers are getting their asking price or more.

If you want to be in that group, it starts with getting the price right from day one.

Connect with a local agent to make sure you are.

You’ve probably seen the headlines saying, “foreclosures are on the rise,” and maybe your mind jumped straight to 2008. That’s understandable. A lot of people remember that crash and all the foreclosures that happened during that window, and they’re hoping something like that never happens again.

But this isn’t a repeat of what happened back then. Here’s the context to prove it.

Foreclosures Are Rising, But They’re Still Historically Low

Yes, foreclosure filings are up 26% from a year ago, according to ATTOM. And they’ve been rising for 5 straight quarters. That’s a real trend worth paying attention to. But the full picture isn’t scary like the headlines suggest.

The reality is the increase we’re seeing is a sign of the market normalizing.

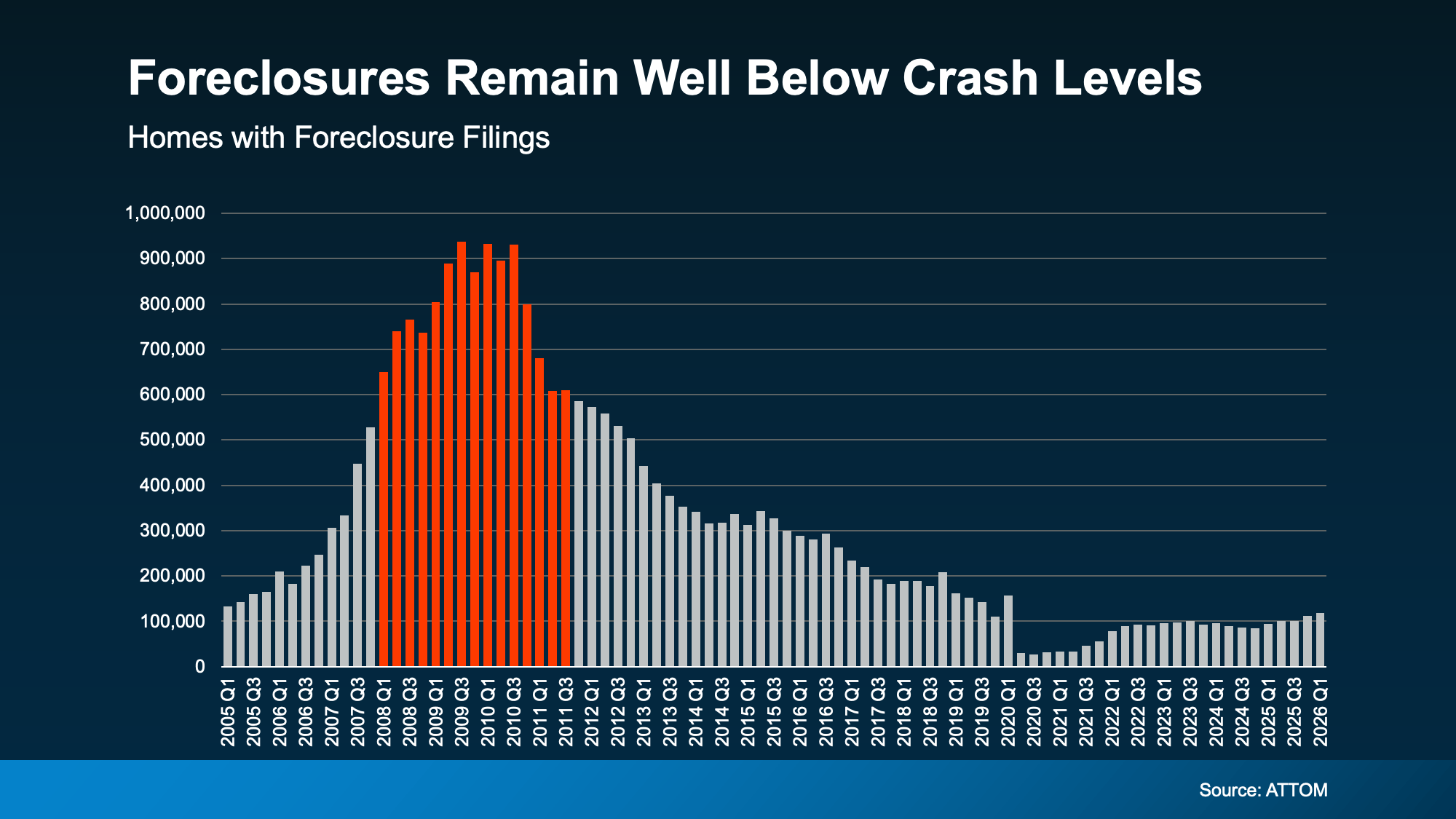

Here’s an important thing to know about this chart. The extremely low numbers you see in 2020 and 2021 don’t represent what’s “normal.” That’s when the government put a moratorium on foreclosures to help homeowners get through the pandemic. Those years were an exception, not the baseline.

Instead, compare where we are today to 2017, 2018, and 2019 – the last years the market was running normally. Today’s numbers are still lower. So, we’re not even back to what’s typical, yet. That means this can’t be a crash. (see graph below):

While today’s numbers are getting closer to pre-pandemic levels, they’re still below historical norms. And just look at what was happening around 2008. Even with the recent increase, we’re nowhere near those levels. This is a market returning to normal, not heading toward a crisis.

While today’s numbers are getting closer to pre-pandemic levels, they’re still below historical norms. And just look at what was happening around 2008. Even with the recent increase, we’re nowhere near those levels. This is a market returning to normal, not heading toward a crisis.

Why Today’s Equity Picture Changes Everything

Most of those filings won’t even end in a completed foreclosure. That’s because today’s homeowners have something most people in 2008 simply didn’t have. And that’s equity.

The average homeowner today is sitting on roughly $295,000 in home equity right now, according to Cotality. Back in 2008, many people owed more than their homes were worth. Selling wasn’t an option. And foreclosure was often the only door available.

Today, that’s not the case. If you have enough equity to cover what you owe and the cost of selling, you could sell your home, pay off your debt, protect your credit, and potentially walk away with money in your pocket.

That’s a completely different situation than what homeowners faced during the last crash, and it’s a big reason we’re unlikely to see foreclosures spiral the way they did back then.

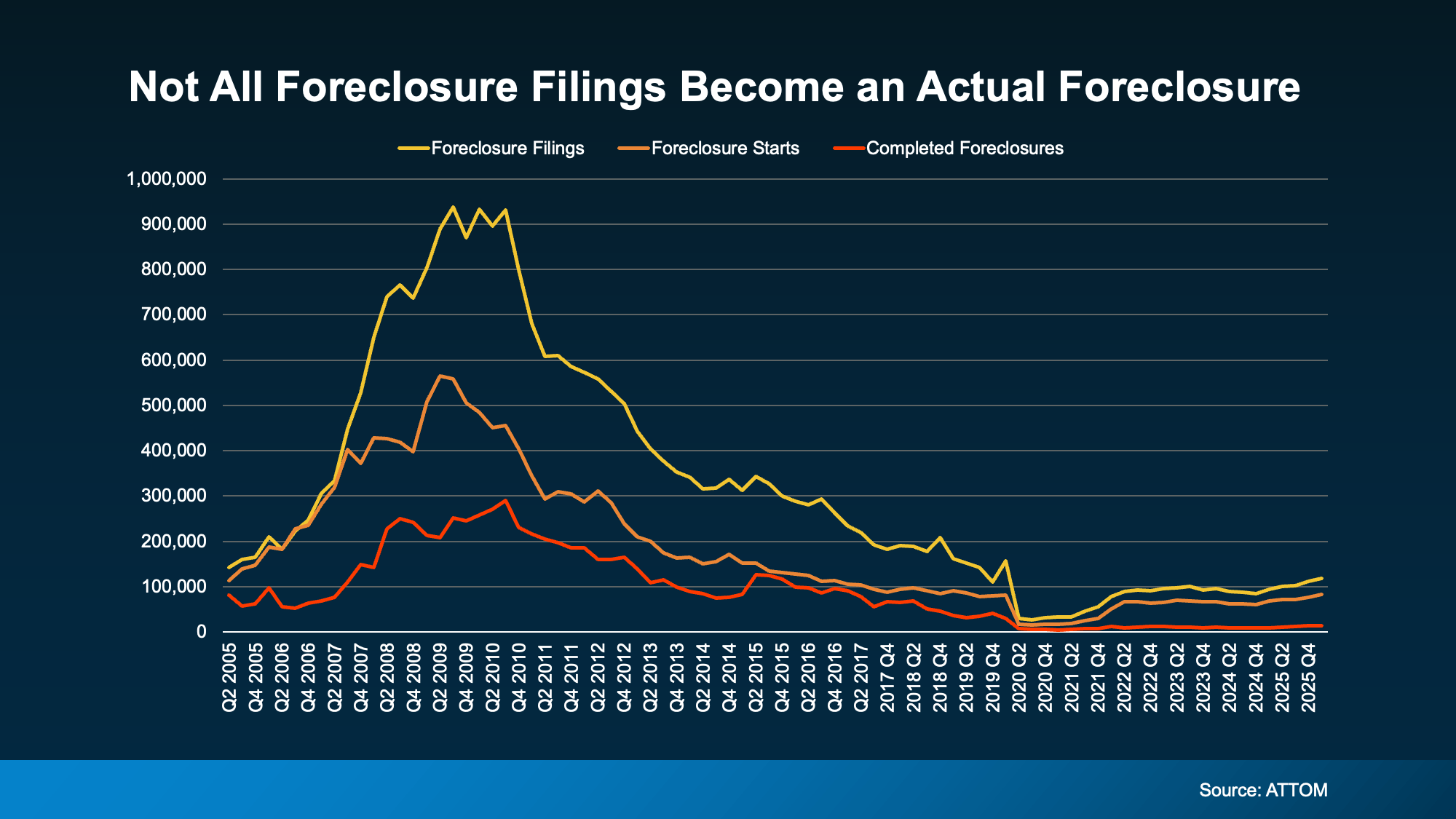

Check out the graph below. It shows foreclosure data from ATTOM going back to 2005. Here’s how to read it:

- The yellow line tracks all foreclosure filings.

- The orange line tracks foreclosure starts, meaning the process has officially begun.

- And the red line at the bottom tracks completed foreclosures (the ones where a homeowner actually lost their home).

See how the red line stays well below the other two? That gap tells the real story. A lot of homeowners who enter the foreclosure process never end up losing their home because they find another way forward first.

See how the red line stays well below the other two? That gap tells the real story. A lot of homeowners who enter the foreclosure process never end up losing their home because they find another way forward first.

Today’s equity is a big reason for that. So, even the filings we are seeing now won’t all end in foreclosure.

If You’re Struggling, You Have More Options Than You Think

Maybe you’re behind on payments. Maybe you’re stressed about what comes next. That’s an incredibly hard place to be, but it’s important to know that missing a payment or two doesn’t automatically mean you’ll lose your home.

Banks would much rather work with you than foreclose. It’s a complicated, costly process for them, too. They’re often willing to set up a repayment plan, offer forbearance (a temporary pause or reduction in your payments), or modify your loan to make things more manageable long-term.

Just know the sooner you reach out to your lender, the more options you’ll have. In some states (ones that don’t require the foreclosure process to go through a court) things can move faster than people expect. Getting ahead of it early gives you and your lender the most room to find a solution.

And if selling makes more sense for your situation, a real estate agent can help you understand what your home is worth and whether that’s a path worth exploring.

Bottom Line

Foreclosure filings may be rising, but they’re still low. And the equity most homeowners are sitting on today is a key reason this looks nothing like 2008.

Selling your house this season? You’ve probably heard you should stage it before it hits the market. But what does that really mean – and is it worth the effort?

The short answer is “yes,” especially right now.

With more houses for sale this year, you’re likely wondering how to make the most money possible without your house sitting on the market. The answer is staging. It can help your house stand out, bring in stronger offers, and sell faster. As Nadia Evangelou, Principal Economist at the National Association of Realtors (NAR), puts it:

“Staging matters. Preparing the home to be ‘buyer-ready’ attracts more buyers, especially now that inventory has increased.”

Here’s what staging actually involves and what it could do for your sale.

What Is Home Staging?

Home staging is the process of preparing your house, so it appeals to as many buyers as possible. That usually means decluttering, deep cleaning, rearranging furniture, and adding simple touches that help each room feel bright, open, and welcoming.

The goal is to help buyers fall in love with the space and picture themselves living there, which makes them more likely to make an offer.

Why Staging Is Worth the Effort

Staged houses tend to perform better on almost every metric that matters when you sell. According to Redfin, staged homes have been shown to sell up to 73% faster than unstaged homes. And they often close in under a month, compared to anywhere from two to three months for vacant ones.

There’s also a strong return on the money you spend.

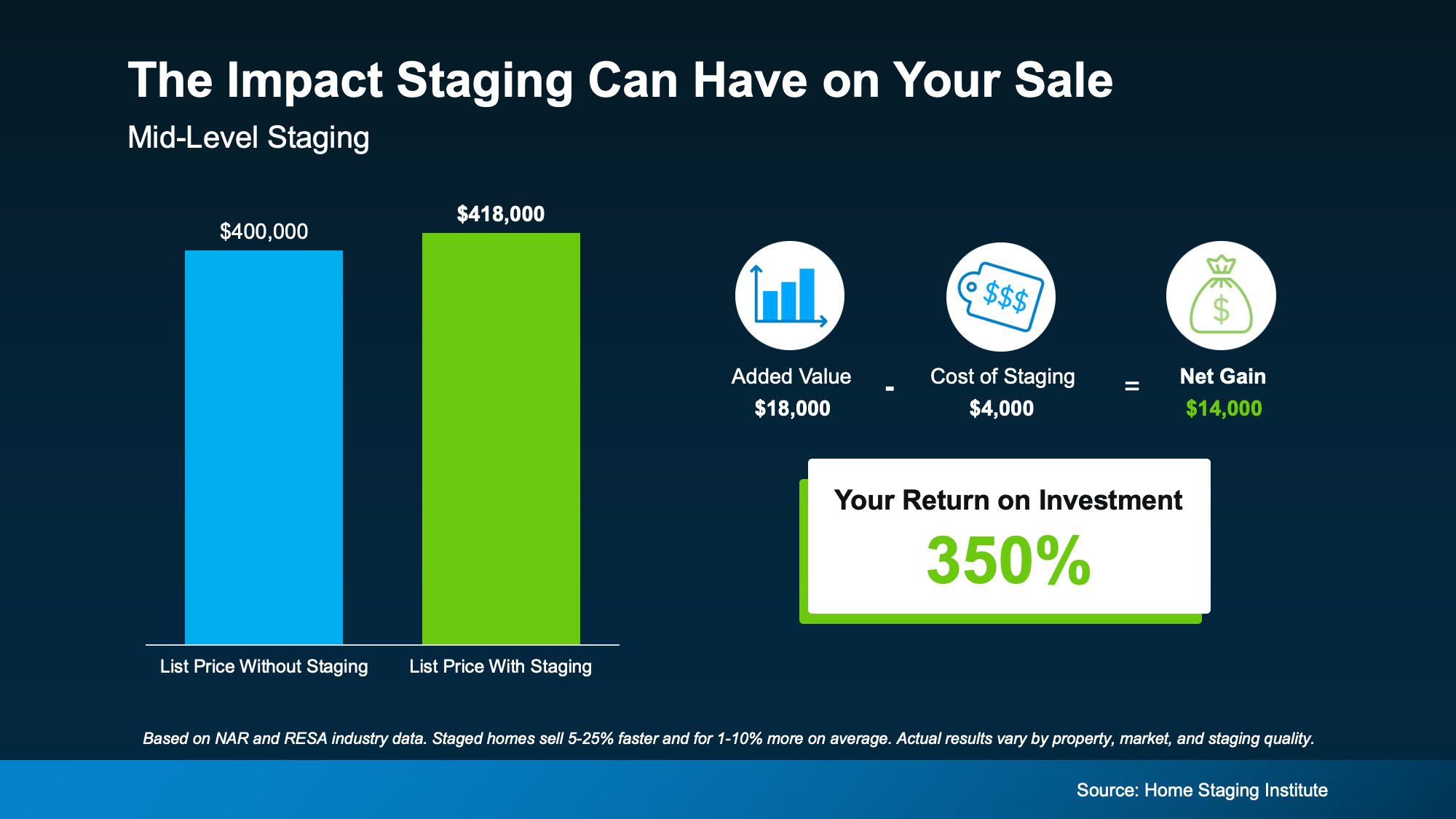

The Home Staging Institute says mid-level staging can deliver a 350% return on investment. On a $400k home, that turns the typical $4k cost into roughly $18k in added value when you sell (see graph below):

By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing.

By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing.

Your Staging Options

And just in case you’re seeing that $4k upfront investment above and thinking, “I’m not going to spend that,” here’s what you should know.

Staging doesn’t always have to mean hiring a full crew or filling your house with rented furniture. There are a few different paths you can take, depending on your budget and timeline. So, you could spend a lot less and still get a good return.

Here are a few options:

- Professional staging. A stager handles everything from layout to décor, often bringing in their own inventory. According to the Home Staging Institute, costs typically range from $500 to $5k or more, depending on the size of your house.

- Virtual staging. Digital furniture and styling are added to your listing photos, which can be a budget-friendly option for vacant houses.

- DIY staging. If your budget is tight and your home only needs minor updates, decluttering, deep cleaning, and arranging furniture for flow can still make a real difference.

Your agent can help you figure out which approach fits your house, your market, and your goals.

Agents see what buyers respond to in open houses and showings every week, so they can give you specific, personalized recommendations on what’s worth your time and money (and what isn’t).

That way you can get the most bang for your buck – no matter your budget.

Bottom Line

With more homes for sale right now, making a strong first impression matters. Staging can help your house sell faster and for more – and there’s an option for almost every budget.

If you’re getting ready to list, connect with a local real estate agent to talk through what level of staging makes the most sense for your house.

The Pricing Mistake That Could Cost You Your Sale

What the Foreclosure Headlines Aren’t Telling You

Why Staging Your House Could Pay Off This Spring

-

Affordability1 week ago

Affordability1 week agoCould Co-Buying Be the Answer for Some First-Time Buyers?

-

Featured2 weeks ago

Featured2 weeks ago3 Things That Are Not Going To Happen in Today’s Housing Market

-

For Buyers2 weeks ago

For Buyers2 weeks agoMore Options Are Popping Up This Spring

-

Equity2 weeks ago

Equity2 weeks agoRent or Buy? The Real Tradeoff Most People Don’t Talk About

-

Agent Value2 weeks ago

Agent Value2 weeks agoStay or Sell? How To Make the Right Call as You Age

-

Affordability2 weeks ago

Affordability2 weeks agoThink You Have To Put 20% Down? Most First-Time Homebuyers Don’t.

-

For Sellers2 weeks ago

For Sellers2 weeks agoIs Late May the Best Time To List Your House?

-

Affordability2 weeks ago

Affordability2 weeks agoThe 10 Best Markets for First-Time Buyers This Spring

You must be logged in to post a comment Login