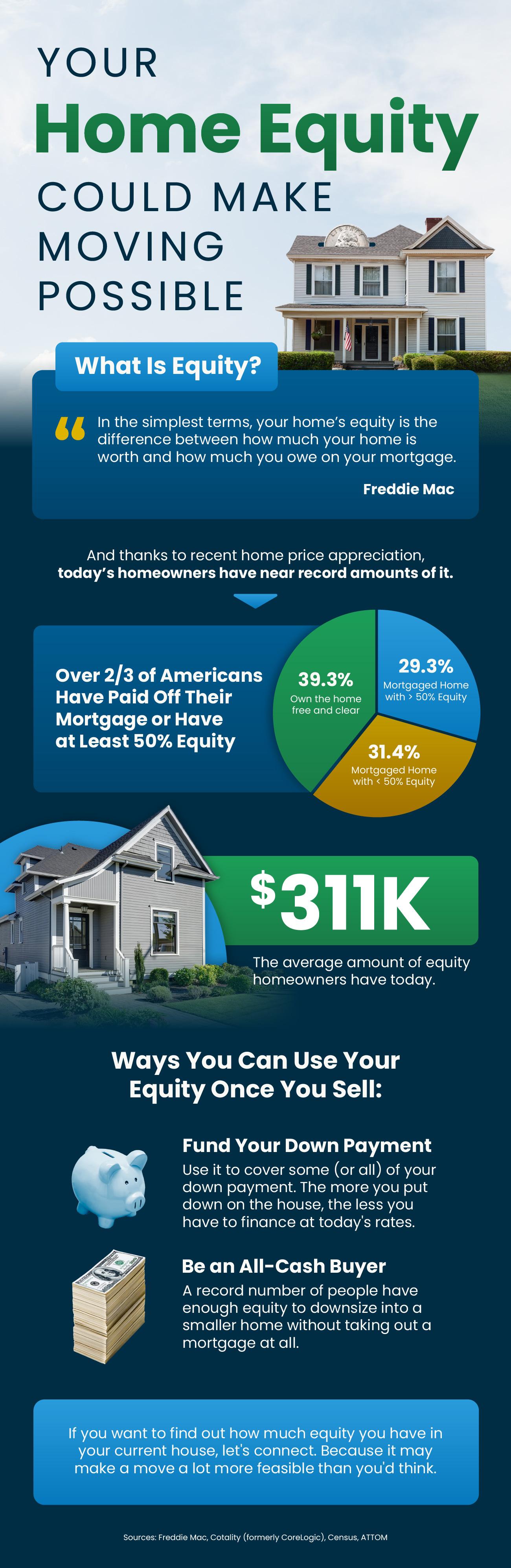

Equity

Your Home Equity Could Make Moving Possible

Some Highlights

- Thanks to recent home price appreciation, homeowners have near record amounts of equity – and you may too. On average, homeowners have $311K worth of equity.

- Once you sell, you can use it to fund your down payment on your next home or maybe even to buy a smaller house in cash.

- If you want to find out how much equity you have, connect with an agent. Because it may make a move a lot more feasible than you’d think.

You’ve probably seen the headlines saying, “foreclosures are on the rise,” and maybe your mind jumped straight to 2008. That’s understandable. A lot of people remember that crash and all the foreclosures that happened during that window, and they’re hoping something like that never happens again.

But this isn’t a repeat of what happened back then. Here’s the context to prove it.

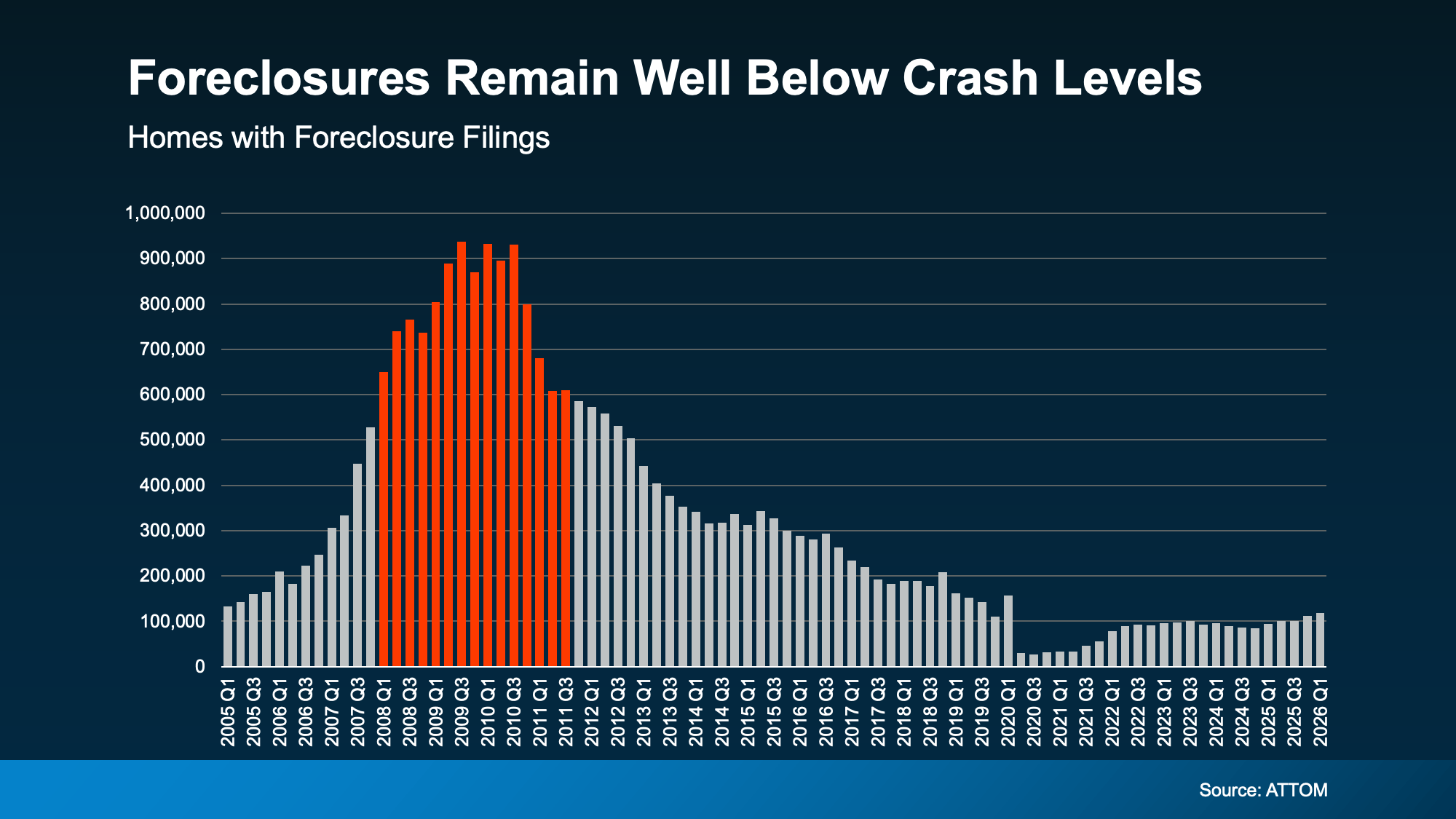

Foreclosures Are Rising, But They’re Still Historically Low

Yes, foreclosure filings are up 26% from a year ago, according to ATTOM. And they’ve been rising for 5 straight quarters. That’s a real trend worth paying attention to. But the full picture isn’t scary like the headlines suggest.

The reality is the increase we’re seeing is a sign of the market normalizing.

Here’s an important thing to know about this chart. The extremely low numbers you see in 2020 and 2021 don’t represent what’s “normal.” That’s when the government put a moratorium on foreclosures to help homeowners get through the pandemic. Those years were an exception, not the baseline.

Instead, compare where we are today to 2017, 2018, and 2019 – the last years the market was running normally. Today’s numbers are still lower. So, we’re not even back to what’s typical, yet. That means this can’t be a crash. (see graph below):

While today’s numbers are getting closer to pre-pandemic levels, they’re still below historical norms. And just look at what was happening around 2008. Even with the recent increase, we’re nowhere near those levels. This is a market returning to normal, not heading toward a crisis.

While today’s numbers are getting closer to pre-pandemic levels, they’re still below historical norms. And just look at what was happening around 2008. Even with the recent increase, we’re nowhere near those levels. This is a market returning to normal, not heading toward a crisis.

Why Today’s Equity Picture Changes Everything

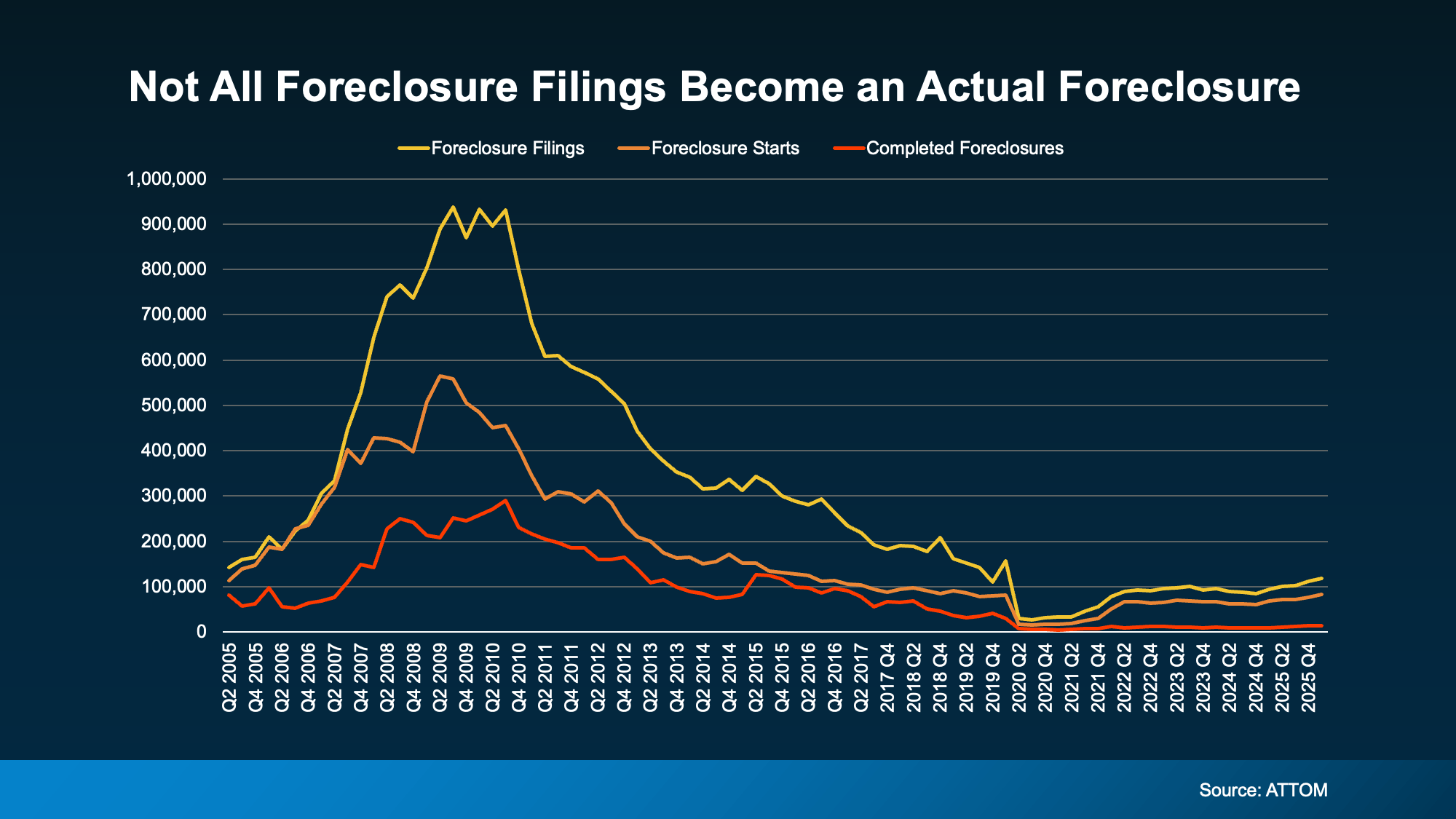

Most of those filings won’t even end in a completed foreclosure. That’s because today’s homeowners have something most people in 2008 simply didn’t have. And that’s equity.

The average homeowner today is sitting on roughly $295,000 in home equity right now, according to Cotality. Back in 2008, many people owed more than their homes were worth. Selling wasn’t an option. And foreclosure was often the only door available.

Today, that’s not the case. If you have enough equity to cover what you owe and the cost of selling, you could sell your home, pay off your debt, protect your credit, and potentially walk away with money in your pocket.

That’s a completely different situation than what homeowners faced during the last crash, and it’s a big reason we’re unlikely to see foreclosures spiral the way they did back then.

Check out the graph below. It shows foreclosure data from ATTOM going back to 2005. Here’s how to read it:

- The yellow line tracks all foreclosure filings.

- The orange line tracks foreclosure starts, meaning the process has officially begun.

- And the red line at the bottom tracks completed foreclosures (the ones where a homeowner actually lost their home).

See how the red line stays well below the other two? That gap tells the real story. A lot of homeowners who enter the foreclosure process never end up losing their home because they find another way forward first.

See how the red line stays well below the other two? That gap tells the real story. A lot of homeowners who enter the foreclosure process never end up losing their home because they find another way forward first.

Today’s equity is a big reason for that. So, even the filings we are seeing now won’t all end in foreclosure.

If You’re Struggling, You Have More Options Than You Think

Maybe you’re behind on payments. Maybe you’re stressed about what comes next. That’s an incredibly hard place to be, but it’s important to know that missing a payment or two doesn’t automatically mean you’ll lose your home.

Banks would much rather work with you than foreclose. It’s a complicated, costly process for them, too. They’re often willing to set up a repayment plan, offer forbearance (a temporary pause or reduction in your payments), or modify your loan to make things more manageable long-term.

Just know the sooner you reach out to your lender, the more options you’ll have. In some states (ones that don’t require the foreclosure process to go through a court) things can move faster than people expect. Getting ahead of it early gives you and your lender the most room to find a solution.

And if selling makes more sense for your situation, a real estate agent can help you understand what your home is worth and whether that’s a path worth exploring.

Bottom Line

Foreclosure filings may be rising, but they’re still low. And the equity most homeowners are sitting on today is a key reason this looks nothing like 2008.

You’ve probably asked yourself lately: Is it even worth trying to buy a home right now? It’s a question a lot of people are asking.

With today’s home prices and mortgage rates, renting can feel like the easier path. In some cases, it might even seem like the only realistic option right now. And if that’s where you are, there’s nothing wrong with that.

But if you’re weighing the decision, there’s one part of the conversation that doesn’t get talked about enough.

It’s what each choice does for your future.

What Renting Really Gets You (And What It Doesn’t)

Depending on your situation, renting does have some advantages:

- Lower upfront costs.

- Less responsibility.

- More flexibility to move when you want.

But even with those benefits, a Bank of America survey found 70% of aspiring homeowners worry about what long-term renting means for their future. And that concern comes down to one thing: you’re not building anything for your future. As Yahoo Finance explains:

“Paying rent doesn’t build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

So, while renting may feel easier, the flexibility you get comes at a cost.

How Homeownership Builds Your Wealth Over Time

On the other hand, owning a home is one of the most consistent ways people build wealth over time. Why? When you’re a homeowner, you gain something called equity. That’s the difference between what your home is worth and what you owe.

That equity grows with every monthly payment you make. It also gets a boost as home values go up through the years – and it adds up quicker than you may think.

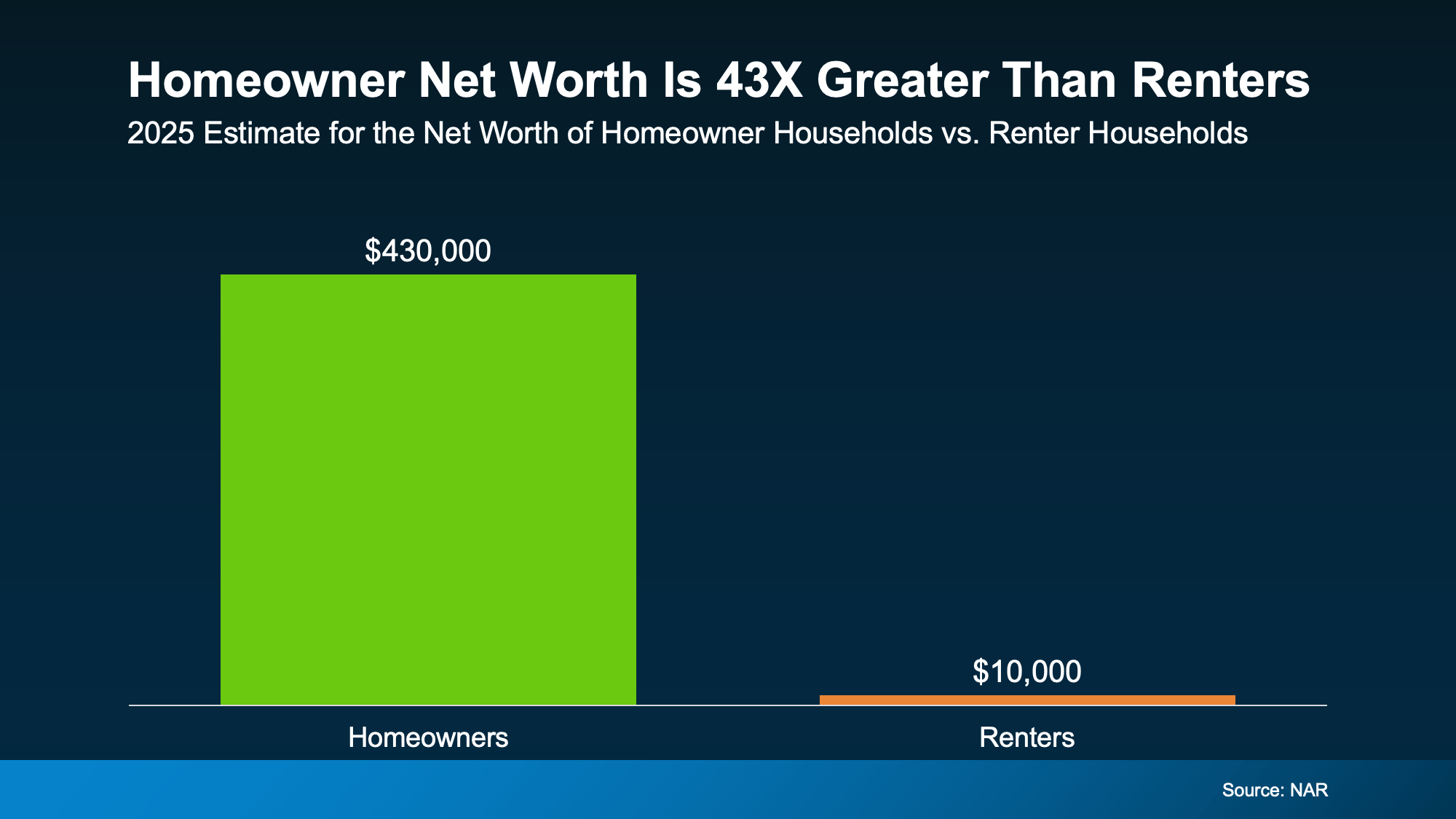

Today, the National Association of Realtors (NAR) says the average homeowner’s net worth is 43X greater than that of a renter:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

- Homeowners: $430k

- Renters: $10k

And it’s not because homeowners make wildly different decisions day to day. It’s because over time, one path builds something, and the other doesn’t.

So sure, buying comes with some upfront costs and more responsibility. But it’s basically a savings account you can live in.

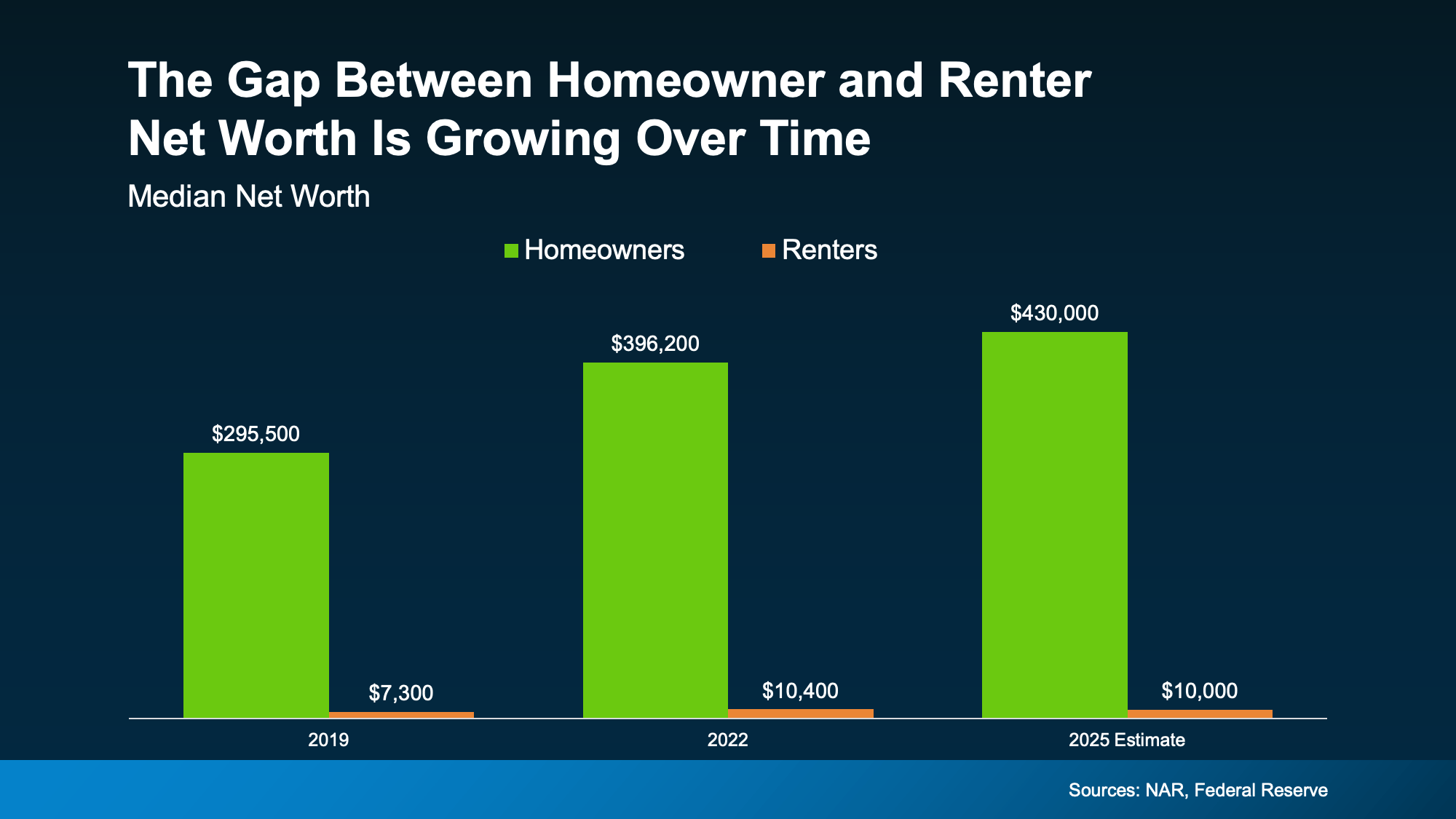

The Gap Is Growing Over Time

And here’s something else interesting. That net worth gap between renters and homeowners has been widening over time, not shrinking.

If you look back at the reports on net worth through the years, you can see the gap is growing as homeowners gain wealth and renters stay stuck in the rental trap (see graph below):

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

When you can afford it and you’re ready for the responsibility, history shows buying is usually worth it in the long run. Because either way, you’re paying for someone’s mortgage and building someone’s net worth.

When you rent, it’s your landlord’s mortgage – not yours. But when you buy? Your monthly payments help build equity.

The question is: whose do you want to pay? Yours or theirs?

So, Should You Buy a Home Now?

The short answer is, it depends on your situation.

While the long-term benefits of buying are clear, that doesn’t mean the timing is right for everyone right now. And that’s okay. You should only buy a home once you’re ready and the numbers work for you.

But whether you’re looking to buy now or planning for the future, the first step is the same. You should have a quick conversation with a local real estate agent about your goals, timeline, and budget.

They can help you run the numbers and see what’s realistic. You may find buying is closer than you thought. And if not, you’ll at least know exactly what it will take to get there.

Because the sooner you have a plan, the sooner you can decide when it makes sense, instead of wondering if it ever will.

Bottom Line

Renting may feel more do-able today. But over time, it could cost you.

If you want to ditch renting and start building something for your future, it starts with a simple conversation. Connect with a real estate agent to talk about your specific goals, and explore your options – so you’re ready when the time is right for you.

That kitchen you’ve been mentally redesigning…

The bathroom that really needs a refresh…

Or the outdoor space you keep saying you’ll get to someday…

What if you already have what you need to finally make it happen? Because a growing number of homeowners are realizing just that.

Homeowners are expected to spend over $522 billion on home improvements by the end of 2026 – and they’re not draining their savings accounts to get it done. Many are using their home equity.

And if you’ve owned your home for 10+ years, there’s a chance you could use your equity to fund some home upgrades too. Let’s break down what you need to know first.

What Is Equity? And How Does It Help?

Equity is the difference between what your house is worth and what you owe on your mortgage.

And according to Cotality, the average homeowner has about $313,000 worth of equity today. That’s more than enough to finally knock some projects off your list. And more people are realizing they can use that to give their home a little TLC.

Research coming out of Meridian Link says home improvements are the top thing people are using their equity for today.

Top Motivations for Equity-Based Borrowing:

- Funding home improvements (45%)

- Using it to pay down other debts / debt consolidation (16%)

- Investing in other properties (16%)

Maybe it makes sense for you to do the same. But here’s what’s important. Just because you can use your equity doesn’t mean you have to. It also doesn’t mean every project makes sense.

What Projects Are Actually Worth It?

If you’re going to go this route, you’ll want to focus on upgrades that actually pay off. A good renovation should be something that improves the value of your home. Because, even if you’re not planning to sell soon, you want to make sure you’re setting yourself up for success when you do.

And an agent is the best resource as you weigh your options. They know what other homeowners are doing and what buyers in your area like. And that can be really helpful as you narrow down your project list. As the National Association of Realtors (NAR) puts it:

“Being able to help sellers prioritize home improvements and maximize their net on the sale is a key value real estate agents offer.”

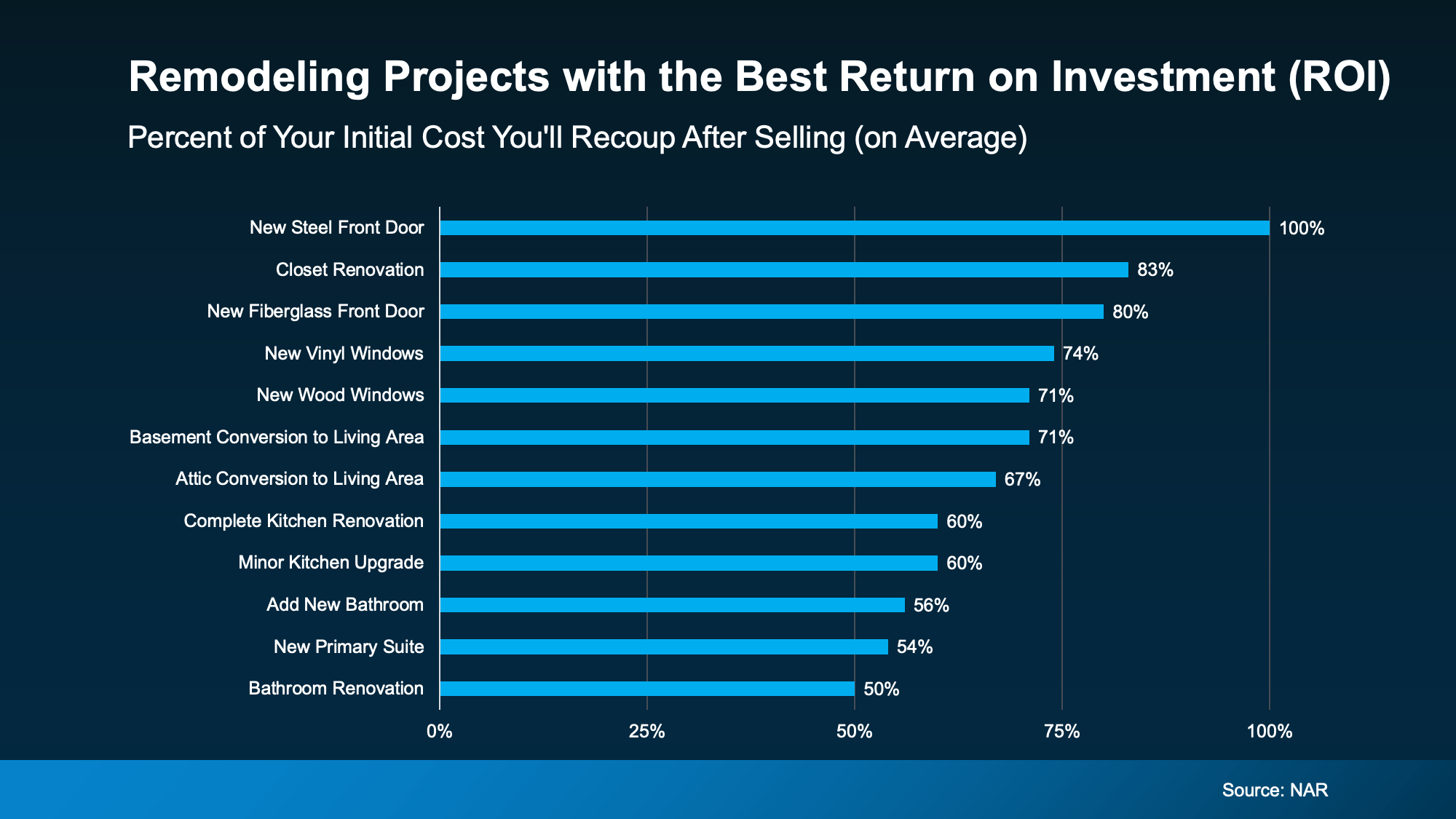

Here’s a quick rundown of the projects with the best potential to recoup your costs according to NAR (see graph below). While it’s a good starting point, just remember it can’t match the expertise an agent can provide.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

A new front door is a great project. But it’s not something to use your equity for. But revamping your kitchen? That’s where your equity can come in and lighten the load.

Where To Go from Here

Whether the project you’ve been thinking about is on this list or not, chat with an agent to make sure it’s worth the time, money, and effort before calling in any contractors.

Because the goal isn’t to do everything, it’s to invest where it counts.

And if you want to use your equity to get one of the bigger projects done, meet with a financial advisor too. Because you’ll want to make sure you’ll maintain a good loan-to-value (LTV) threshold even after using your equity. That way you have all the information you need to make your decision.

Bottom Line

Whether you’re selling next year or just giving your house some TLC, the right home improvements today can set you up for success tomorrow. And the best part? Your equity may be the key to making it happen.

What’s one upgrade you’ve been thinking about – and wondering if it’s worth it?

Have a quick conversation with an agent to find out if it’s the right decision for your home.

The Pricing Mistake That Could Cost You Your Sale

What the Foreclosure Headlines Aren’t Telling You

Why Staging Your House Could Pay Off This Spring

-

Affordability1 week ago

Affordability1 week agoCould Co-Buying Be the Answer for Some First-Time Buyers?

-

Featured2 weeks ago

Featured2 weeks ago3 Things That Are Not Going To Happen in Today’s Housing Market

-

For Buyers2 weeks ago

For Buyers2 weeks agoMore Options Are Popping Up This Spring

-

Equity2 weeks ago

Equity2 weeks agoRent or Buy? The Real Tradeoff Most People Don’t Talk About

-

Agent Value2 weeks ago

Agent Value2 weeks agoStay or Sell? How To Make the Right Call as You Age

-

Affordability2 weeks ago

Affordability2 weeks agoThink You Have To Put 20% Down? Most First-Time Homebuyers Don’t.

-

For Sellers2 weeks ago

For Sellers2 weeks agoIs Late May the Best Time To List Your House?

-

Affordability2 weeks ago

Affordability2 weeks agoThe 10 Best Markets for First-Time Buyers This Spring

You must be logged in to post a comment Login