First-Time Buyers

Should You Still Expect a Bidding War?

If you’re still worried about having to deal with a bidding war when you buy a home, you may be able to let some of that fear go.

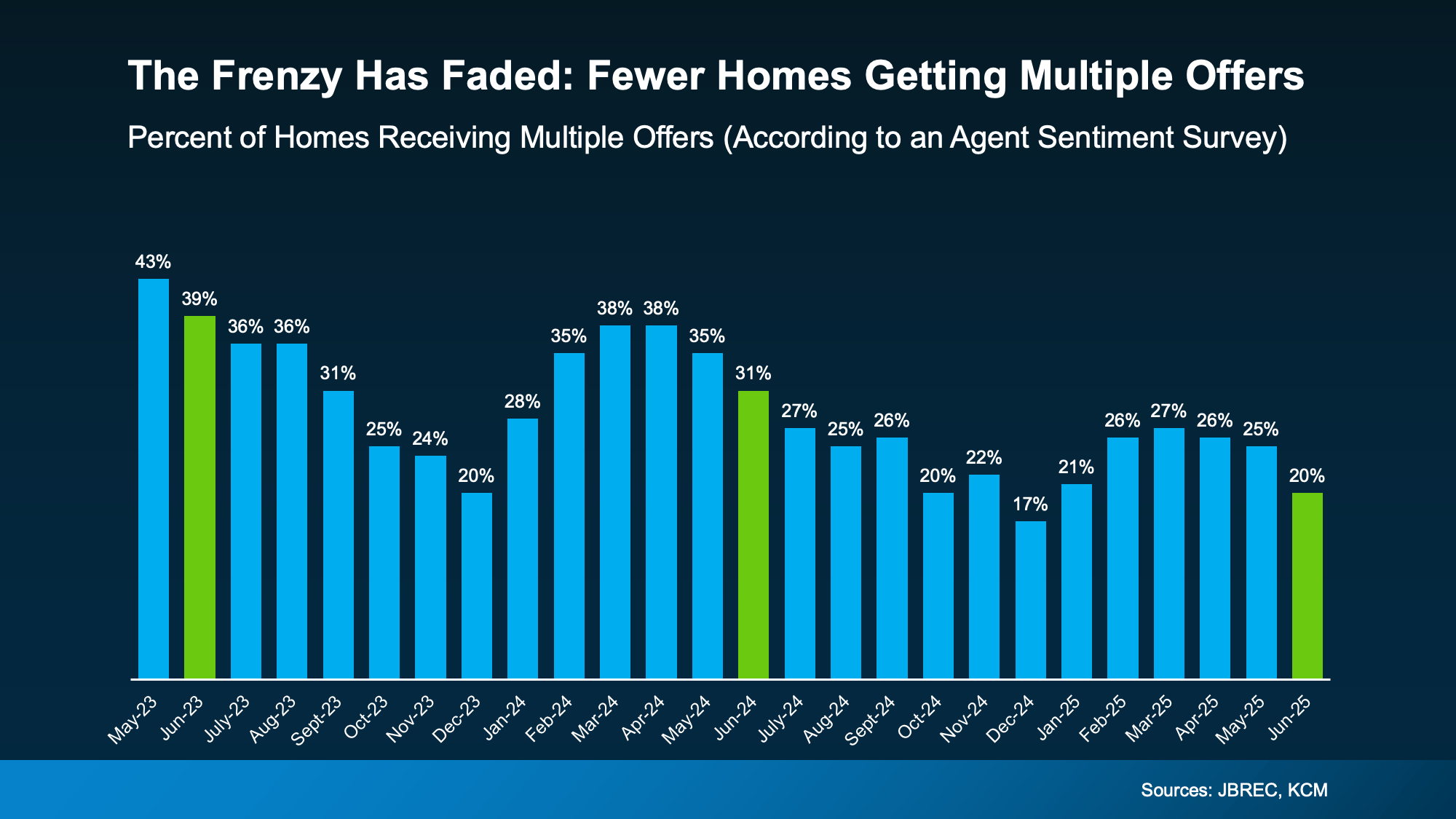

While multiple-offer situations haven’t disappeared entirely, they’re not nearly as common as they used to be. In fact, a recent survey shows agents reported only 1 in 5 homes (20%) nationally received multiple offers in June 2025.

That’s down from nearly 1 in 3 (31%) just a year ago – and dramatically lower than in June 2023 (39%) (see graph below):

This trend means you should face less competition when you buy. That gives you more time to make decisions and the ability to negotiate price or terms.

This trend means you should face less competition when you buy. That gives you more time to make decisions and the ability to negotiate price or terms.

It Still Depends on Where You’re Buying

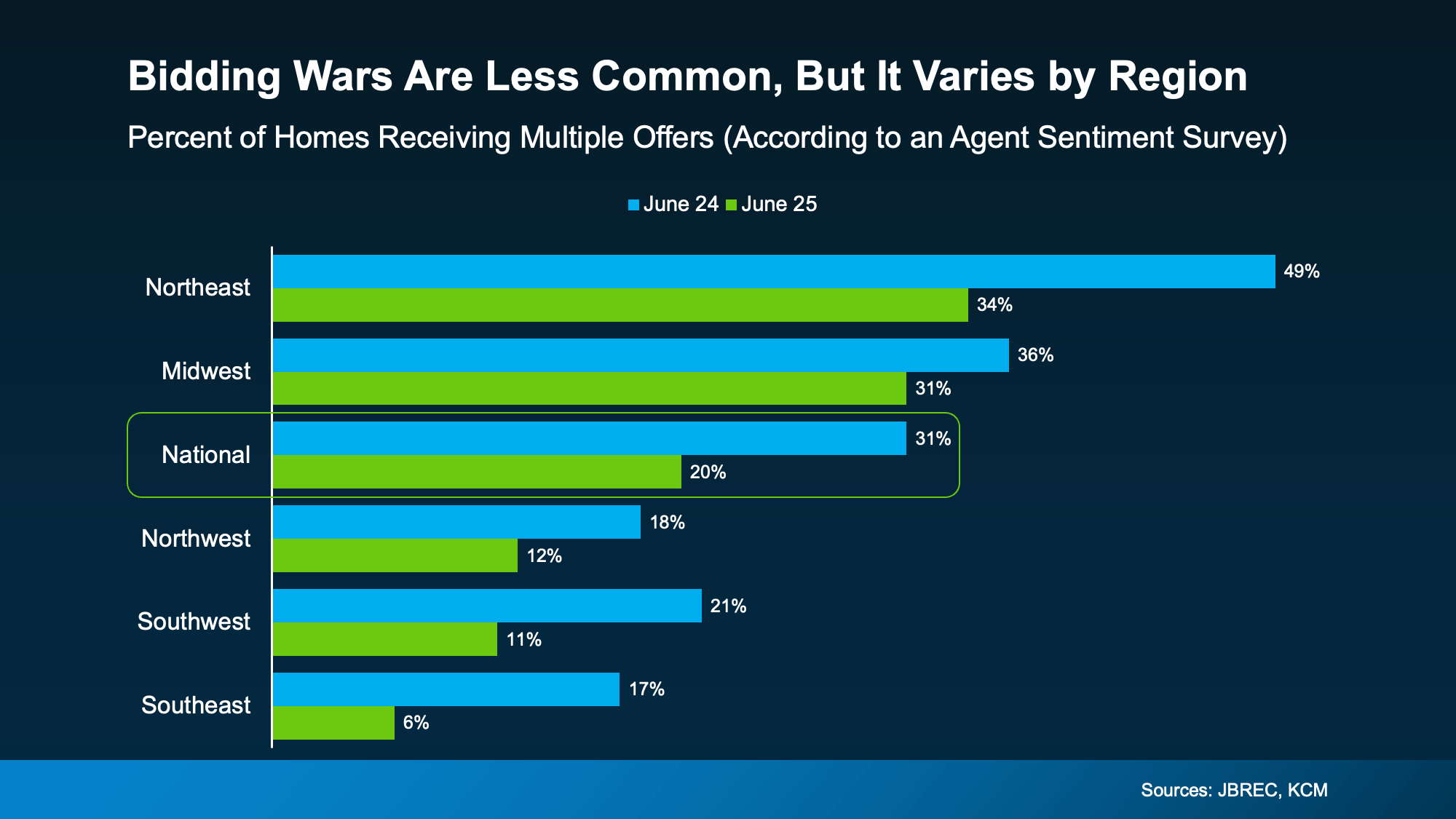

Of course, national trends don’t tell the full story. Local dynamics matter, a lot. This second graph uses survey data from John Burns Research & Consulting (JBREC) and Keeping Current Matters (KCM) to break things down by region to prove just how true that is. It shows, while the share of homes getting multiple offers has dropped pretty much everywhere, some areas are still seeing more offers than others:

In the Northeast, 34% of homes (roughly 1 in 3) are still receiving multiple offers. That’s more than the national average. But in Southeast, that number drops to just 6%.

In the Northeast, 34% of homes (roughly 1 in 3) are still receiving multiple offers. That’s more than the national average. But in Southeast, that number drops to just 6%.

What’s behind the difference? In general, the areas still seeing bidding wars tend to have lower-than-normal inventory. That imbalance between buyers and available homes keeps pressure on prices and competition. But markets with more listings are seeing conditions cool – and that means fewer bidding wars.

Sellers Are More Flexible Than You Might Think

Here’s another shift to show you just how much things have changed. According to a Redfin report, almost half of sellers are offering concessions, like covering their buyer’s closing costs or dropping their asking price to get their house sold.

That’s a clear sign this isn’t the same ultra-competitive market we saw a few years ago. Back then, sellers rarely compromised. And buyers often waived their inspection or appraisal to try to make their offer stand out. Now, things are different.

But again, how often this is happening is going to vary based on where you’re looking to buy. And that’s why you need a local agent’s expertise.

Bottom Line

If concerns about bidding wars have been holding you back, it may be time to take another look. Nationally, competition is down. In some markets, it’s down significantly. And with more sellers offering concessions, buyers today have more power and flexibility than they’ve had in a long time.

Want to find out what the market looks like where you’re buying? Connect with a local agent.

For the past few years, affordability has been what’s stopped a lot of buyers in their tracks. Maybe it stopped you, too.

At some point you probably did the math, looked at the monthly payment, and decided to pause your search and wait for things to get better. But here’s something you may have missed while you’ve been sitting on the sidelines.

Over the last year, housing affordability has improved in all 50 states. Yes, you read that right. It’s gotten better in every single state.

That’s based on new research coming out of First American. And while housing is still fairly expensive compared to historical standards, the pressure buyers felt over the last few years is finally starting to ease.

Some Areas Are Seeing Bigger Improvements

The first thing you need to know is that this isn’t just happening in one region or in a small handful of cities. The trend is happening almost everywhere.

Sure, individual states, cities, and even neighborhoods are going to vary – sometimes by a lot. But overall, more buyers are able to buy again. And in 48 of the top 50 metros, affordability has improved over the past year.

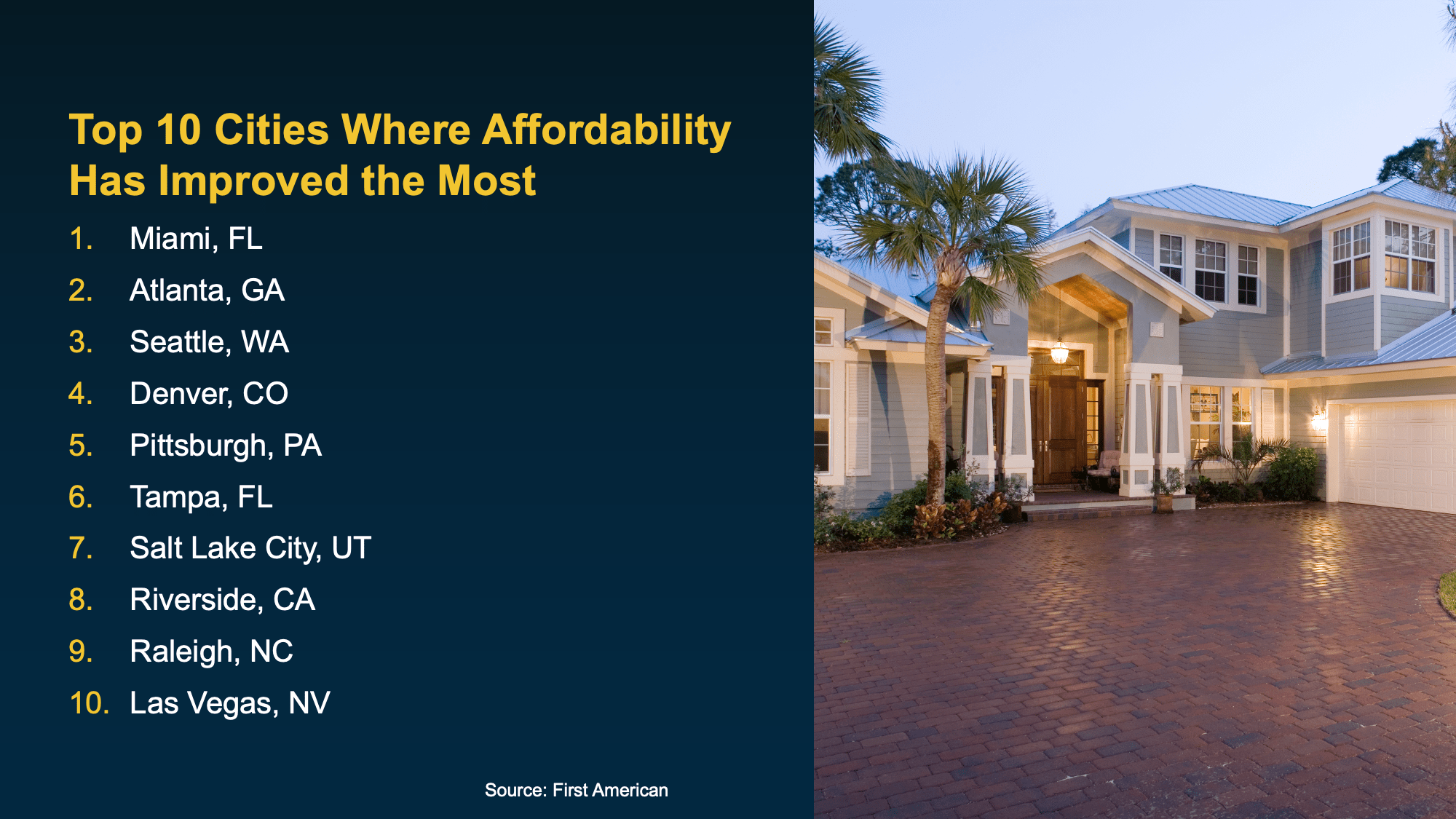

That same research breaks down which cities are seeing the biggest gains:

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

When buyers have more choices, it creates a healthier balance in the market and that can help bring affordability back within reach. With homes up for grabs, it opens the door a bit wider for buyers to negotiate with sellers for credits, price cuts, and more. And it gives you more chances to find a house that works for your needs and budget.

It may make more of a difference than you think.

None of this means affordability challenges have completely disappeared. Buying a home is still a big financial decision. But the trend is moving in a direction many buyers have been waiting for.

As Chen Zhao, Head of Economic Research at Redfin, puts it:

“The housing affordability crisis is showing signs of easing . . . opening the door for more Americans to make the jump to homeownership.”

Bottom Line

If you were holding off on buying, this could be exactly the signal you’ve been waiting so long for. To find out how much affordability’s improved in your area, connect with a local real estate agent.

Before You Fall in Love with a House, Do This First.

Don’t Let Home Prices Headlines Fool You

This’ll Change What You Think About Investors in Today’s Housing Market

-

Agent Value4 weeks ago

Agent Value4 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability4 weeks ago

Affordability4 weeks agoShould You Wait for Lower Rates?

-

For Buyers3 weeks ago

For Buyers3 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

-

Agent Value3 weeks ago

Agent Value3 weeks agoThe #1 Reason Buyers Walk Away (And How To Get Ahead of It)

-

For Buyers4 days ago

For Buyers4 days agoDon’t Let Home Prices Headlines Fool You

-

Affordability2 weeks ago

Affordability2 weeks agoAffordability Has Improved in All 50 States

-

Agent Value3 weeks ago

Agent Value3 weeks ago3 Must-Do’s for First-Time Home Buyers

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoYou Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

You must be logged in to post a comment Login