Buying Tips

What a Government Shutdown Really Means for the Housing Market

There’s been a lot of talk lately about how a government shutdown impacts the housing market. You might be wondering: Is it causing everything to grind to a halt?

The short answer? No.

The housing market doesn’t stop. It keeps moving. Homes are still being bought and sold, contracts are still being signed, and closings are still happening. The difference is that a few parts of the process may slow down a little, but overall, the market continues to function.

Here’s What Typically Happens

Whenever the government shuts down, some federal agencies temporarily close or scale back their operations. That can cause a few hiccups in real estate, especially when it comes to processing certain types of government loans and insurance requirements:

- “Applicants for FHA, VA, or USDA loans—which account for about one-quarter of all mortgage applications—may encounter significant processing delays due to agency furloughs.” – Selma Hepp, Chief Economist at Cotality

- “By recent estimates, more than 2,500 mortgage originations per working day are at risk of delays during a shutdown . . .” – Zillow

- Flood insurance approvals may also be paused. The National Flood Insurance Program can be temporarily affected, which delays closings in flood zones.

Even with those challenges and delays, most transactions still go through. Buyers keep buying, sellers keep selling, and agents keep helping people move forward.

The Housing Market Usually Bounces Back Fast

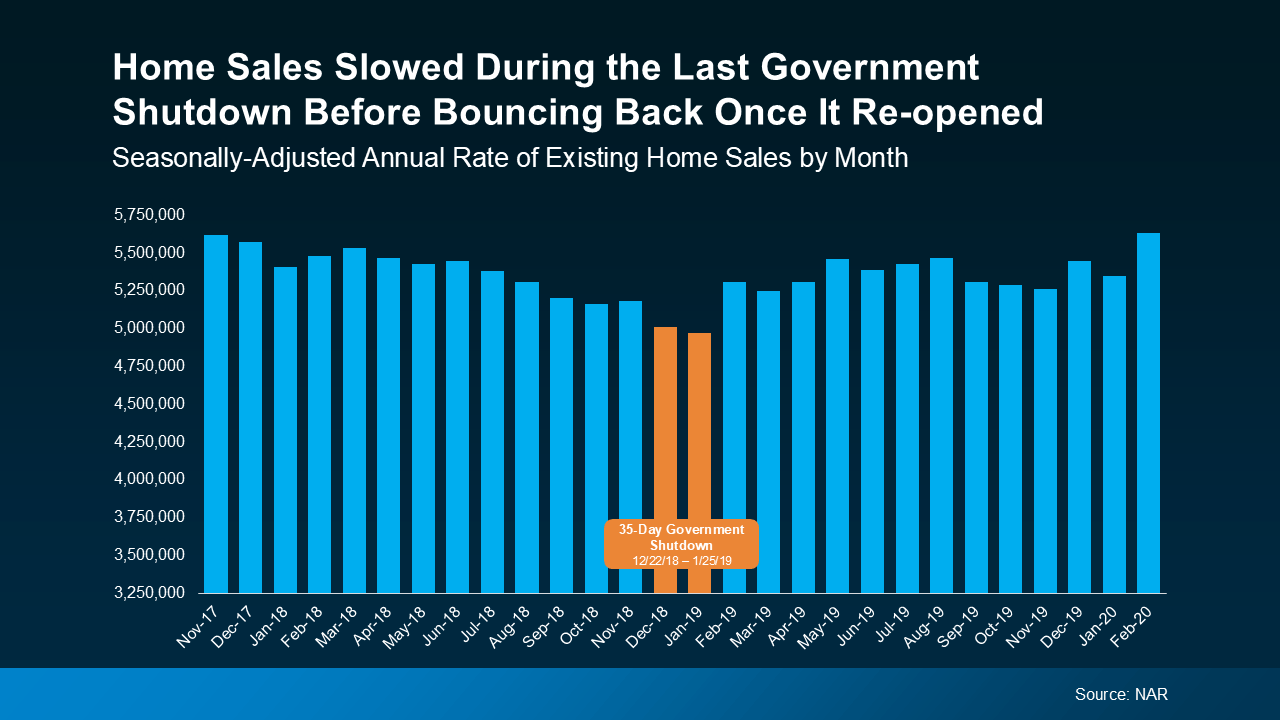

And you can see that play out in this data. If you look back at the most recent government shutdown that began at the end of 2018 and lasted for 35 days, sales activity dipped very slightly during the closure but picked right back up once the government reopened.

Data from the National Association of Realtors (NAR) shows existing home sales slowed for about two months, and then rebounded quickly as delayed closings worked their way through the system when the government reopened (see graph below):

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

What This Means for You

If you’re in the middle of buying or selling a home, don’t panic. Most deals will still move forward, even if it takes a few extra days. Jeff Ostrowski, Housing Market Analyst at Bankrate, explains:

“If you’re expecting to close in a week or a month, there could be some slight delay, but I think for most people, it’s probably going to be a blip more than a real deal killer.”

And if you’re just starting to think about buying or selling, this could actually work in your favor. Some buyers and sellers may become cautious and pause their plans during times of uncertainty, like this, and that can open a short window of opportunity.

When fewer people are active in the market, well-prepared buyers may find less competition for homes, and motivated sellers may be more willing to negotiate. These brief slowdowns often create a moment where you can make a move that would be harder once activity ramps back up.

Bottom Line

A government shutdown can cause short-term delays for some buyers, but it doesn’t derail the housing market. The last time this happened, sales picked back up as soon as the government re-opened.

If you’re unsure how this might affect your plans, or just want to make sense of what’s happening, connect with a local real estate agent.

You’ve probably heard that home prices are cooling off. And that’s true – nationally. But zoom in on individual markets across the country, and the picture looks completely different depending on where you are.

Some areas are still seeing solid price growth. Others have gone flat. A few have actually dipped slightly negative. So, what’s causing all of that variation?

It All Comes Down to Inventory

Here’s the simple version:

-

When there are more homes for sale, buyers have options.

-

More options, means less competition.

-

Less competition means sellers can’t push prices as high.

On the flip side, when inventory is tight, buyers are competing over a small pool of homes, and that pushes prices up.

That dynamic is playing out right now in a really visible way across the country.

Markets where inventory has climbed back to, or above, normal pre-pandemic levels are seeing prices flatten or fall slightly. Markets where inventory is still well below those 2019 benchmarks are still seeing prices rise. As Lance Lambert, CEO of ResiClub, puts it:

“Home prices are still climbing a little year-over-year in many regions where active inventory remains well below pre-pandemic 2019 levels, such as pockets of the Northeast and Midwest.

In contrast, some pockets in states like Texas, Florida, and Colorado — where active inventory exceeds pre-pandemic 2019 levels by a solid clip — are seeing modest home price pullbacks or flat pricing.”

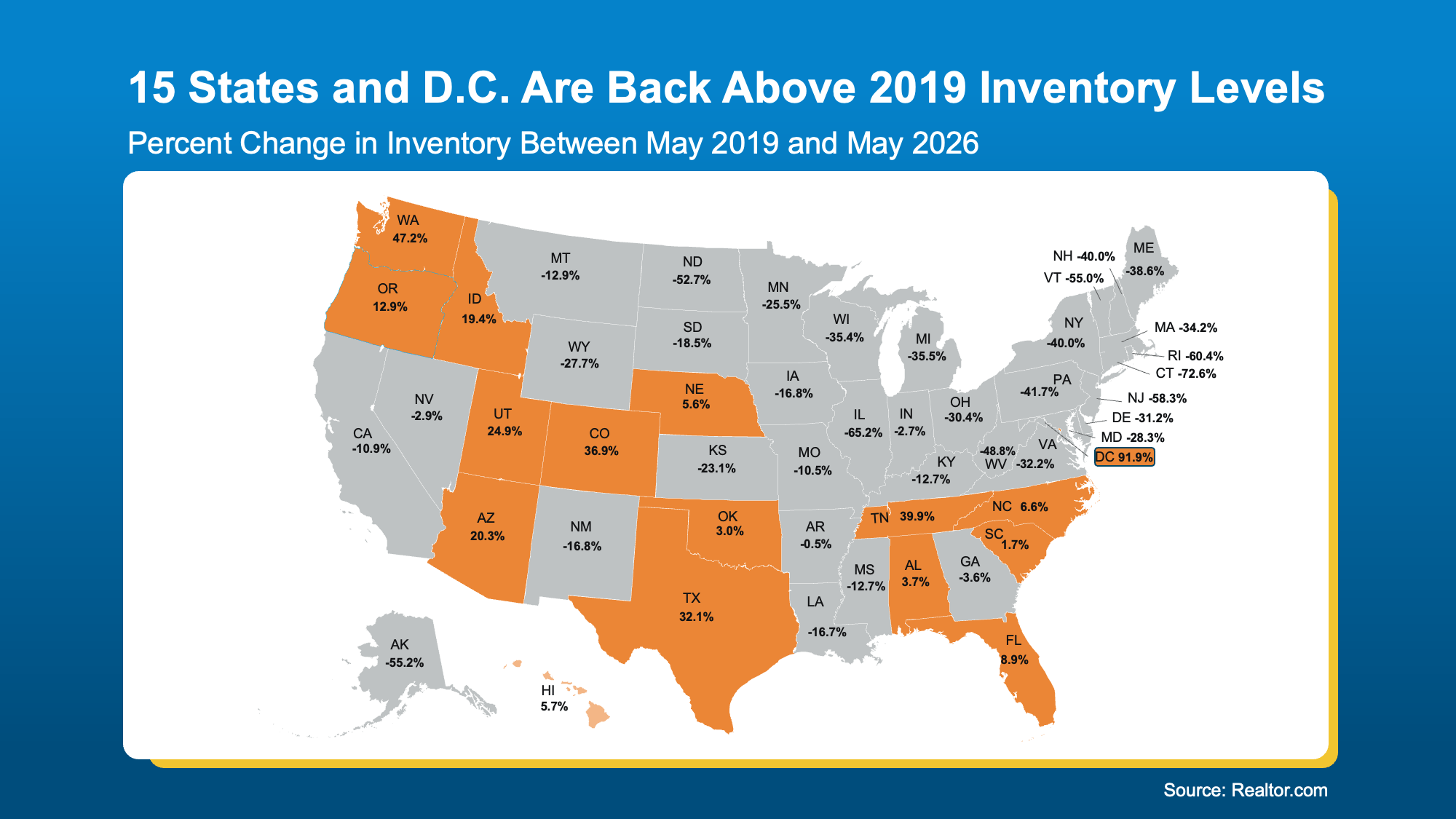

The Maps Say It All

Take a look at where inventory stands today compared to 2019. In most places (the states in gray below), inventory still falls short of where we were back then. And that’s exactly why prices are climbing, albeit moderately, in the vast majority of states.

But you’re probably more interested in where prices are falling a bit, since that’s what is making headlines. So, let’s prove out how much inventory affects prices in those spots.

According to Realtor.com, 15 states and Washington, D.C. are now back above pre-pandemic inventory levels, and some by a wide margin (see the orange in the map below):

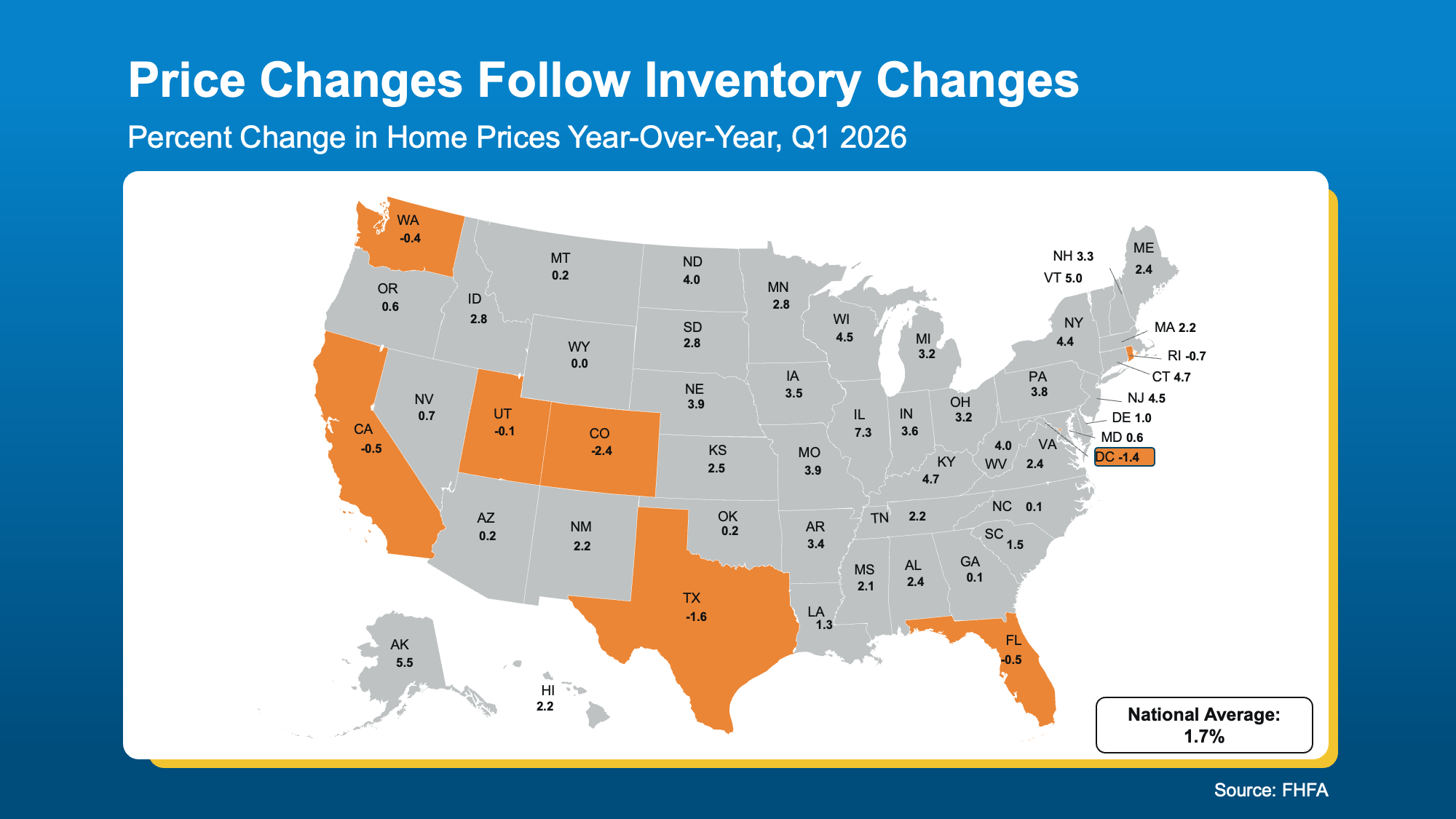

Now, let’s look at the latest Federal Housing Finance Agency (FHFA) data to see what’s happened to home prices in those same states over the past year (again, you’ll want to focus on the orange in the next map).

Now, let’s look at the latest Federal Housing Finance Agency (FHFA) data to see what’s happened to home prices in those same states over the past year (again, you’ll want to focus on the orange in the next map).

See how those line up pretty closely with the areas seeing more homes for sale today?

The overlap isn’t a coincidence. It’s cause and effect.

The national average of 1.7% price growth is accurate, but it’s an average of two very different stories happening at the same time – the few areas experiencing mild declines and the overwhelming majority that are still seeing prices rise.

What This Means If You’re Buying or Selling

If you’re a buyer, the market you’re shopping in matters a lot right now. In places like Texas, Colorado, or Florida, you may have real negotiating power – more choices, less competition, and sellers who are more motivated to make a deal. In tighter markets like much of the Northeast, you’re still likely facing a lot of competition.

If you’re a seller, pricing strategy is everything. In markets where inventory has risen, overpricing is one of the fastest ways to linger on the market and eventually sell for less than you would have with the right price from day one. In markets where inventory is still low, you’re in a strong spot, but getting your price right still matters if you want to attract serious buyers quickly. Either way, that’s where a local real estate agent earns their keep.

Bottom Line

When it comes to prices, where you are matters more than ever right now, and a local real estate agent is the best person to help you make sense of it.

Reach out to a local real estate agent today and work together to build a plan that fits your market.

Open up a home search and you’ll see them. Listings that have been on the market for two months. Three. Some longer.

Most buyers scroll right past them, assuming something’s wrong with the house. But that instinct could be costing you, since the longer a home sits, the more motivated the seller usually gets.

Where Some Buyers Are Finding Better Deals

If affordability has been your #1 hurdle to buying, here’s a surprisingly simple strategy that could help you finally get your foot in the door. Start with the homes that have been sitting the longest. That’s often where the best deals are.

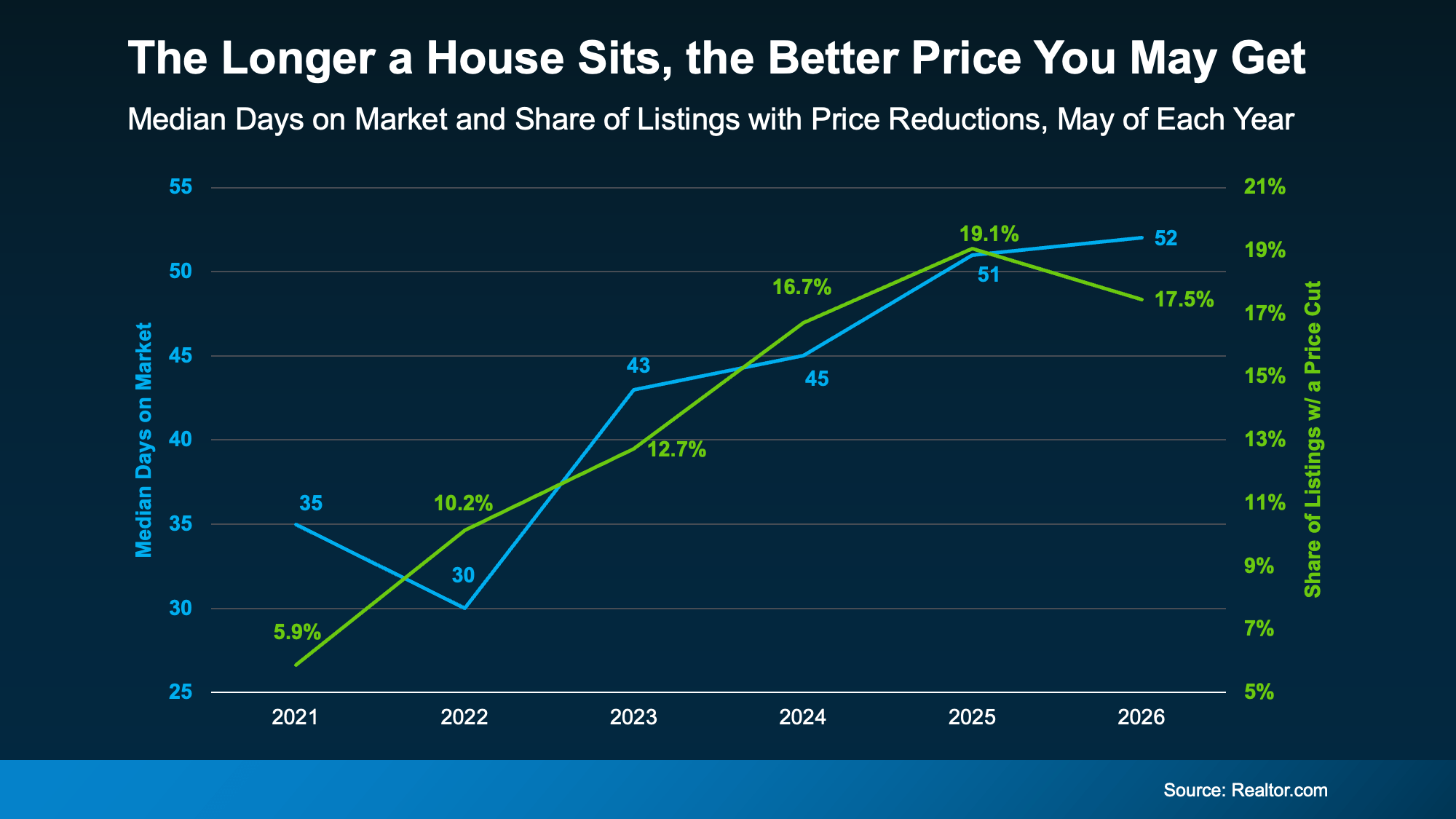

Here’s why. Data from Realtor.com shows there’s a connection between longer time on the market and lower sales prices. Basically, the longer a house sits, the more likely it is that the seller will reduce the price (see graph below):

The blue line tracks how long homes stay on the market, while the green line tracks the share of homes getting a price reduction. As one climbs, so does the other.

And if you focus on these homes that are just sitting and waiting, the opportunity for you is bigger than you may think right now.

Redfin data shows there’s $347 billion worth of stale listings on the market right now – more than ever before for this time of year. So, ask your agent to filter listings for you from oldest to newest. The home that fits your budget might already be there. Just further down the list than you thought.

Lingering Doesn’t Always Mean Something’s Wrong

Let’s say you do that and something catches your eye. Still, you might be questioning why the home has been sitting in the first place. Just remember, sometimes it has nothing to do with the home itself.

According to Redfin, common causes are:

-

The asking price was set too high to start

-

The home didn’t show well online

-

There are a lot of homes for sale in the area, so it just got buried

So, nothing that’s necessarily a dealbreaker, or even anything that’s wrong with the home itself. If there’s a real issue, a thorough inspection will surface it. And that’s information you can use to negotiate. Not a reason to assume it’s a house worth skipping over.

How To Turn a Lingering Listing into a Win

So how do you capitalize on a lingering listing? According to USA Today, you have two main levers to pull.

The first is price. Work with your agent to study what comparable homes recently sold for, then build an offer around that. Coming in below asking price is fair game when a home has been sitting.

The second is concessions. If a seller won’t budge much on price, they may still help in other ways, like covering some closing costs, repair credits, or even a mortgage rate buydown that lowers your monthly payment.

A local agent has the context to tell which homes are the real opportunities and which are skippable.

Bottom Line

A house sitting on the market isn’t always a glaring red flag. In today’s market, it may be your best opportunity yet.

For help deciding which lingering listings are actually worth a second look, connect with a local real estate agent.

Remember a few years back when sellers held all the power and buyers were stuck offering way over asking or waiving inspections just to get a chance at the house? In many markets, those days are behind us.

While it’s going to vary by area, more metros are slowly shifting to favor buyers, and the market is starting to look a lot more like a two-way street again.

And that balance is something we haven’t had in a while.

Whether you’re buying or selling, here’s what you need to know about what’s changing and what it means for your move.

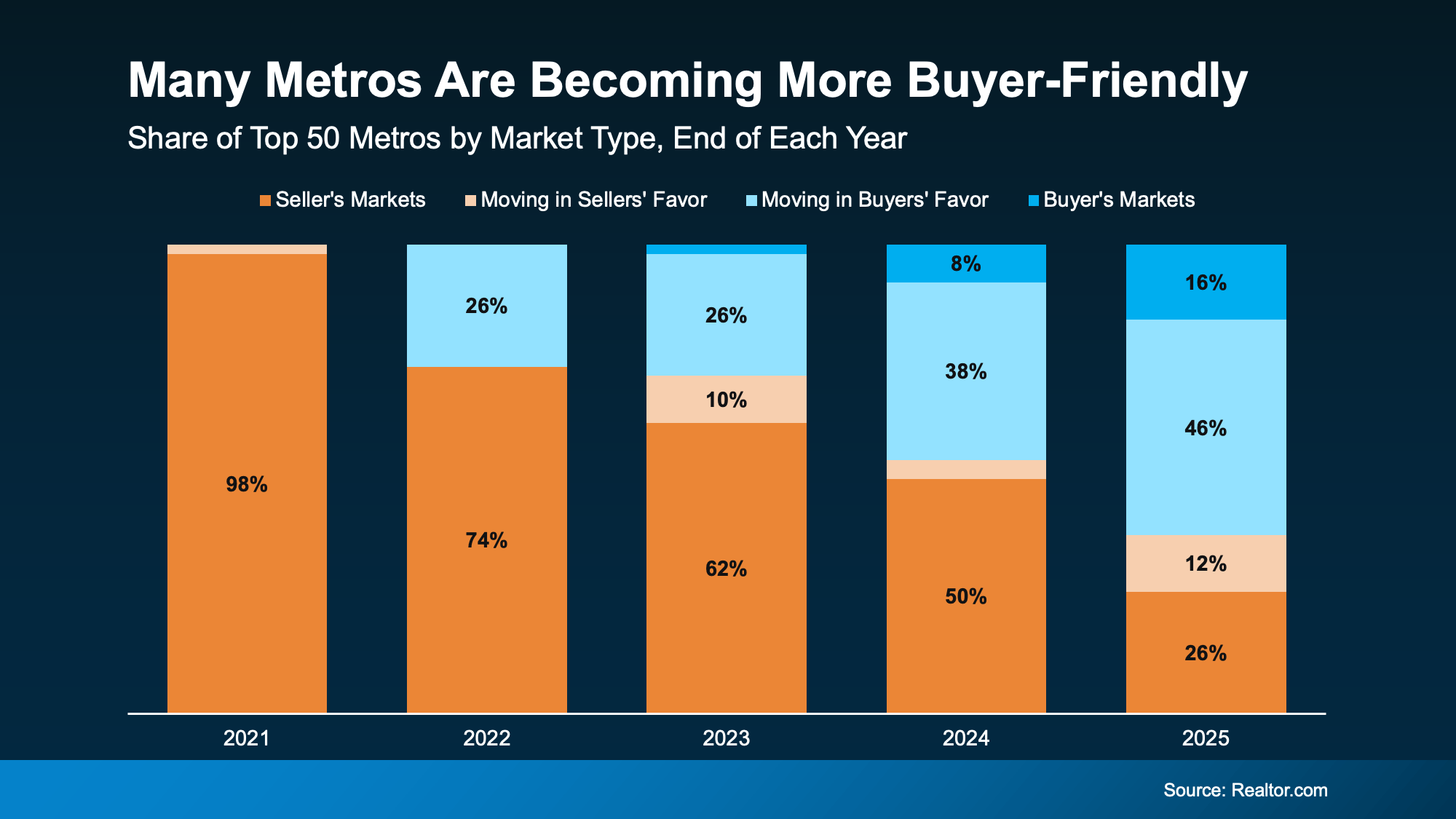

The Most Buyer-Friendly Market in Years

The national data tells an interesting story right now. According to Realtor.com:

“The national housing market is balanced but gradually loosening as the cycle moves in a more buyer-friendly direction . . .“

That’s because, over the past few years, more and more metros have been flipping back to more buyer-friendly terms as inventory’s grown. And when you zoom in on the latest Realtor.com data for the top 50 metro markets over time, the trend becomes really clear (see graph below).

Back in 2021, almost all major metros were seller’s markets. By the end of 2025, only 1 in 3 still favored sellers. That’s an obvious shift.

And that changes how the market is going to feel for everyone. Sellers shouldn’t still expect 2021 conditions, but neither should buyers. At least, not generally speaking.

It’s Not the Same Story Everywhere

That said, who has the power ultimately depends on where you live. While more metros are leaning buyer-friendly lately, there are still plenty of strong seller’s markets right now, too.

It really comes down to how much housing supply and demand there is in your area. And that varies enormously by region.

Sun Belt cities like Austin, Tampa, and San Antonio saw major building booms in recent years, giving buyers more options and more negotiating room. Meanwhile, cities in the Northeast and Midwest – think Rochester, Hartford, and Buffalo – didn’t see that same wave, so inventory stayed tight and competition stayed fierce. As Jeff Ostrowski, Housing Analyst at Bankrate, explains:

“The formerly hot Sun Belt markets have cooled, while the Northeast and Midwest have stayed hot. The big driver here is construction activity. The softest markets now [have] experienced big booms that spurred new building, and that has led to a large supply of new and existing homes on the market in those places.”

Practical Advice for Your Move

To find out who has the power in your local market, talk to an agent. Because knowing what’s happening locally is going to be the key to setting the right strategy for your move.

If the market is working in your favor, great. Lean in and use it to your benefit. But if it’s not, all hope isn’t lost. Your agent can help you figure out how to approach any market.

Here’s some practical advice if there’s a mismatch between your goal and local market conditions.

If you’re buying in a seller’s market:

-

Get pre-approved before you start shopping. It shows sellers you’re serious.

-

Be ready to act fast when the right home hits the market.

-

Consider offering a quick closing date or flexible terms.

-

Work closely with your agent to craft a competitive offer.

If you’re selling in a buyer’s market:

-

Price it right from day one. Overpricing will cost you time and money.

-

Focus on curb appeal and staging to stand out in areas with more inventory.

-

Be open to offering incentives, like covering closing costs or a home warranty.

-

Expect buyers to negotiate and be ready to be flexible.

Bottom Line

Right now, local markets are moving in very different directions. And your strategy as a buyer or seller should reflect your market.

Want to know which way your local market is leaning and what that means for your move? Talk to a local real estate agent.

The 1 Factor That Explains Everything Happening with Home Prices Right Now

Your House Didn’t Sell. Here’s How To Turn It Around.

More Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Affordability4 weeks ago

Affordability4 weeks agoWhat Rising Inflation Means for Your Move

-

Economy4 weeks ago

Economy4 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability4 weeks ago

Affordability4 weeks agoLess House, More Home: Why Smaller Homes Are Paying Off for Today’s Buyers

-

Affordability3 weeks ago

Affordability3 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoTwo Big Reasons To Move This Summer

-

Affordability3 weeks ago

Affordability3 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers2 weeks ago

For Sellers2 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers2 weeks ago

For Buyers2 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

You must be logged in to post a comment Login