Affordability

Why Moving to a More Affordable Area Makes Sense

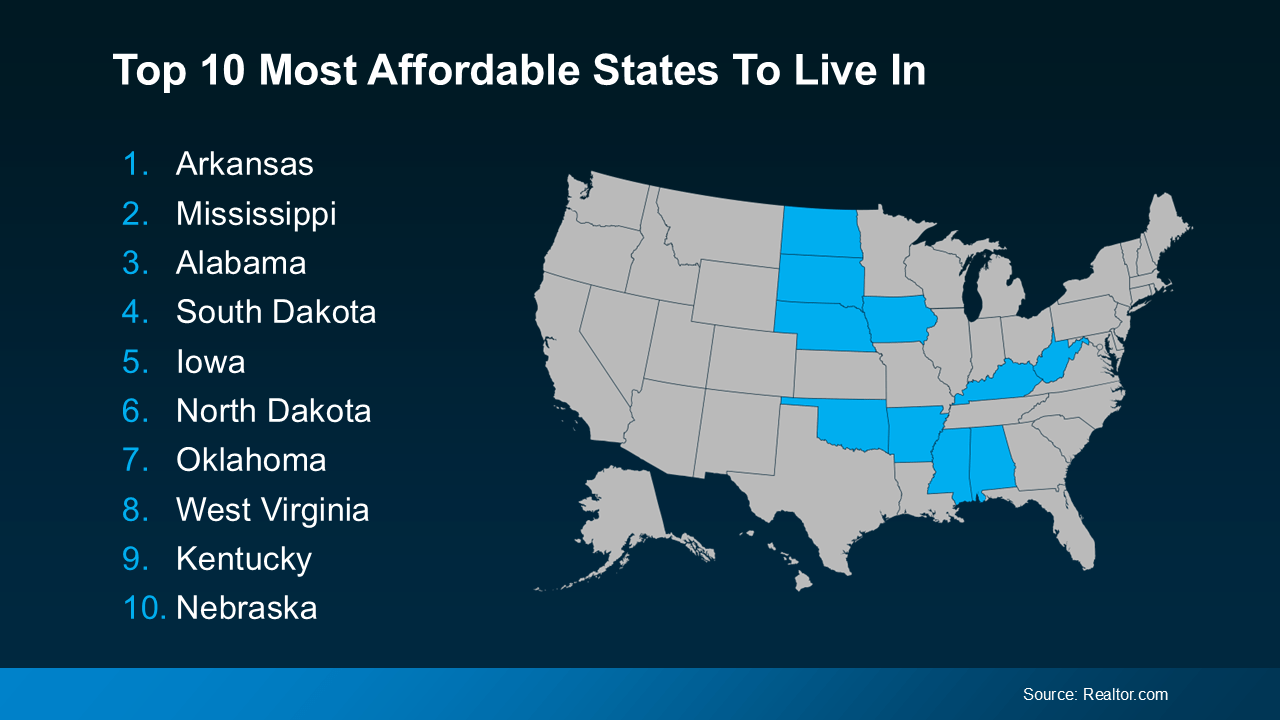

Moving to a more affordable area could be the fresh start you need to get ahead financially. While some markets are certainly more affordable than others, know that working with a trusted real estate agent to find what fits your budget and your desired location – no matter where you want to be – is always the best plan. And with the rising cost of living, many people are rethinking where they live and looking for ways to cut expenses. If that sounds like you, here’s a great place to start (see visual below):

These states are well known for lower housing costs, reduced insurance premiums, and more budget-friendly daily living expenses – but they’re not the only places to find a hidden gem. If you’re open to relocating, you might discover the savings you’re looking for.

These states are well known for lower housing costs, reduced insurance premiums, and more budget-friendly daily living expenses – but they’re not the only places to find a hidden gem. If you’re open to relocating, you might discover the savings you’re looking for.

Why Move to a Lower-Cost Area?

Life is getting more expensive by the day. From rising home prices to higher grocery bills, it feels like everything costs more than it used to. Housing, the largest expense for most people, has become especially costly.

In fact, according to data from Case-Shiller, home prices increased 3.9% from September 2023 to September 2024. And data from GOBankingRates shows insurance costs are up too, with home insurance premiums averaging $2,151 annually – a significant jump compared to recent years.

These rising costs can feel like a lot to handle. That’s why more people are considering lower-cost areas. An article from the National Association of Realtors (NAR) says:

“With the past decade of rising home prices, buyers are looking for more affordable areas . . . As housing affordability continues to shape migration patterns, these areas may provide an opportunity . . . for those looking for more cost-effective alternatives to the nation’s larger, pricier metropolitan areas.”

Lower-cost areas typically offer more affordable housing, less expensive home insurance, and reduced costs for daily living like groceries and gas. Transportation expenses and car insurance premiums also tend to be lower. For anyone feeling stretched thin, moving to a less expensive area can provide meaningful financial relief.

Planning Your Big Move

Whether it’s finding a home that fits your budget or cutting down on other expenses, making the right move in any market can bring significant financial relief. Of course, moving isn’t a decision to take lightly.

Whether you’re moving just a few towns over or to a completely different state, there’s a lot to consider. From job opportunities, to schools, to local amenities – it all has an impact on finding the right home for you.

This is where a knowledgeable local real estate agent can be your best resource. Not only can they help you navigate the housing market in your new or desired area, but they’ll also guide you to neighborhoods that balance affordability with your needs.

And don’t worry if none of the states on the affordability list seem like the right fit for you. An agent can still help you identify budget-friendly options wherever you need to be.

Bottom Line

If the rising cost of living has you feeling stuck, know that you have options. Moving to a more affordable area could be the fresh start you need to get ahead financially and improve your quality of life.

But don’t try to tackle the process alone. With the help of an agent who knows the area, you’ll be well-prepared to make a move. When you’re ready to take the first step, reach out to a local real estate agent.

Whether you’re dreaming about buying your first home or wondering if it’s time to move on from the one you’re in, affordability is probably weighing on your mind. Home prices are still high in many markets, and even though things have improved a bit over the past year, making the numbers work can still feel like a stretch.

But the people finding ways to move right now usually have one thing in common. They didn’t wait for affordability to come to them. They went looking for it.

According to PODS, 61% of people across all generations say affordability is the biggest factor when deciding where to move. And it’s led a growing number of people to do one thing – broaden their search to include more affordable areas they hadn’t seriously considered before. As PODS, put it:

“. . . moving is increasingly driven by affordability, connection, and quality of life. As economic pressures persist, Americans are taking a more intentional, values-driven approach to where they choose to live.”

It’s Not Just the Home Price – It’s the Whole Cost of Living

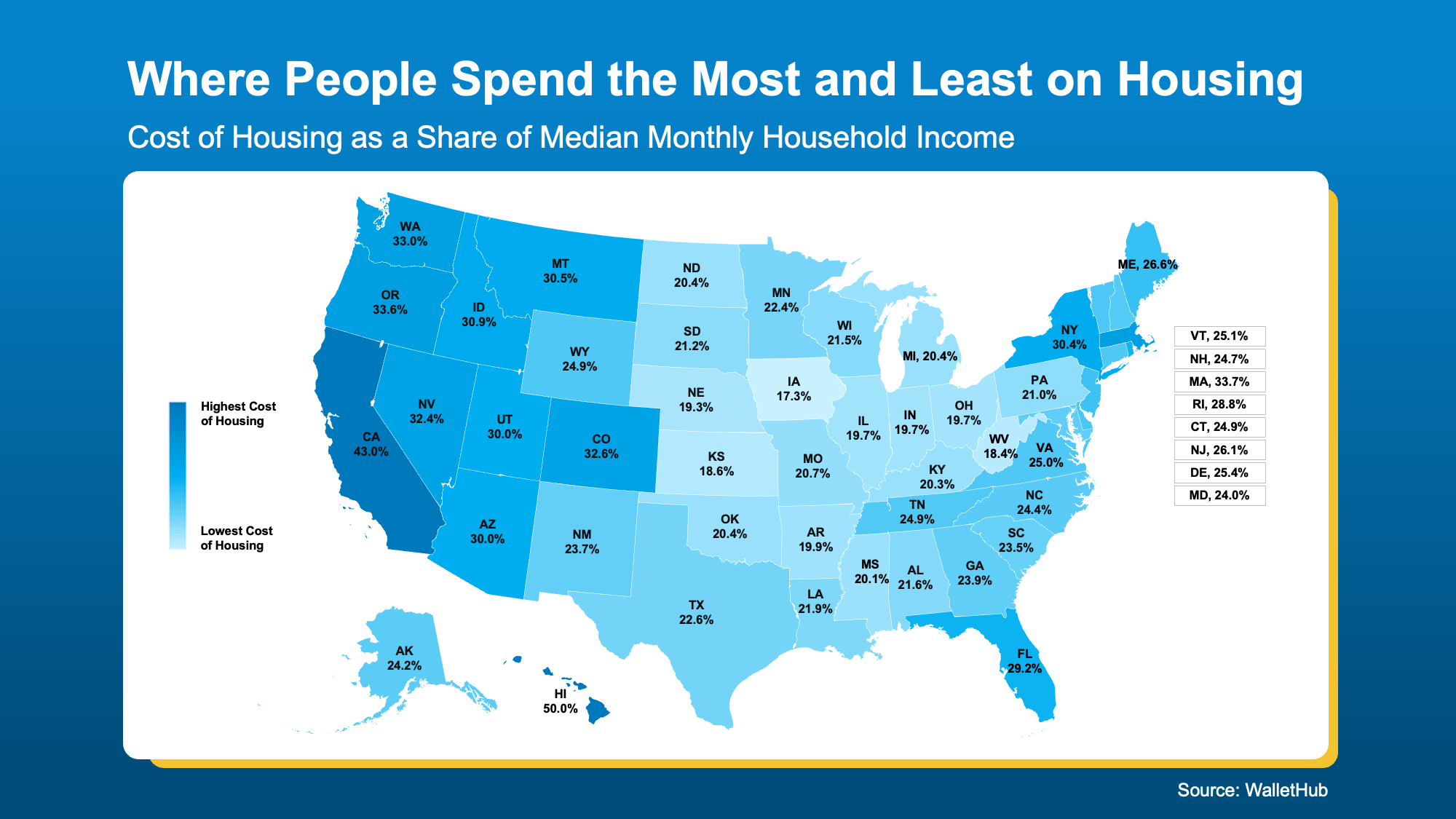

Here’s where it gets really interesting. When people talk about moving for affordability, they’re not just talking about finding a cheaper house. They’re thinking about the full picture. What does it actually cost to live somewhere?

WalletHub looked at exactly this, measuring housing costs as a share of median monthly household income across every state (see map below).

Take a look at where you live on that map. The lighter the blue, the more affordable it generally is to live there. The darker the blue? Just the opposite.

If your state is showing up on the darker blue end of the scale, the cost of living may be putting a real pinch on your wallet, and it may be worth exploring what a lighter-blue area could mean for your finances.

Because if you’re less financially stretched, imagine how that could change things. Less stress. Less worry. More freedom and peace of mind.

You Don’t Have To Move to Another State To Find a Better Deal

But finding more affordable homeownership doesn’t have to mean a cross-country move. It doesn’t even have to mean leaving your state, your family, or your favorite coffee shop behind.

Every market has more affordable pockets that most buyers never think to explore – neighborhoods, towns, and communities where home prices are lower, property taxes are more manageable, and the overall cost of living just works better.

A great local real estate agent knows exactly where those places are.

And if you work remotely, or have any flexibility in where you’re based, your options open up even further. Remote work has already changed the way millions of people think about where to live, and that trend isn’t going away.

When location stops being tied to a daily commute, a more affordable area that’s a bit farther out suddenly becomes a very real option.

Bottom Line

Affordability is a real challenge, but it’s not an unsolvable one. The key is being open to places you might not have considered before. A local real estate agent can help you find them.

Ready to find out which areas have the best affordability right now? Reach out today.

Data shows inflation is moving in the wrong direction. But before the headlines send anyone into a panic, here’s what’s actually going on, why it matters for the housing market, and what it means if you’re thinking about buying or selling.

Inflation Went Up – Here’s What That Actually Means

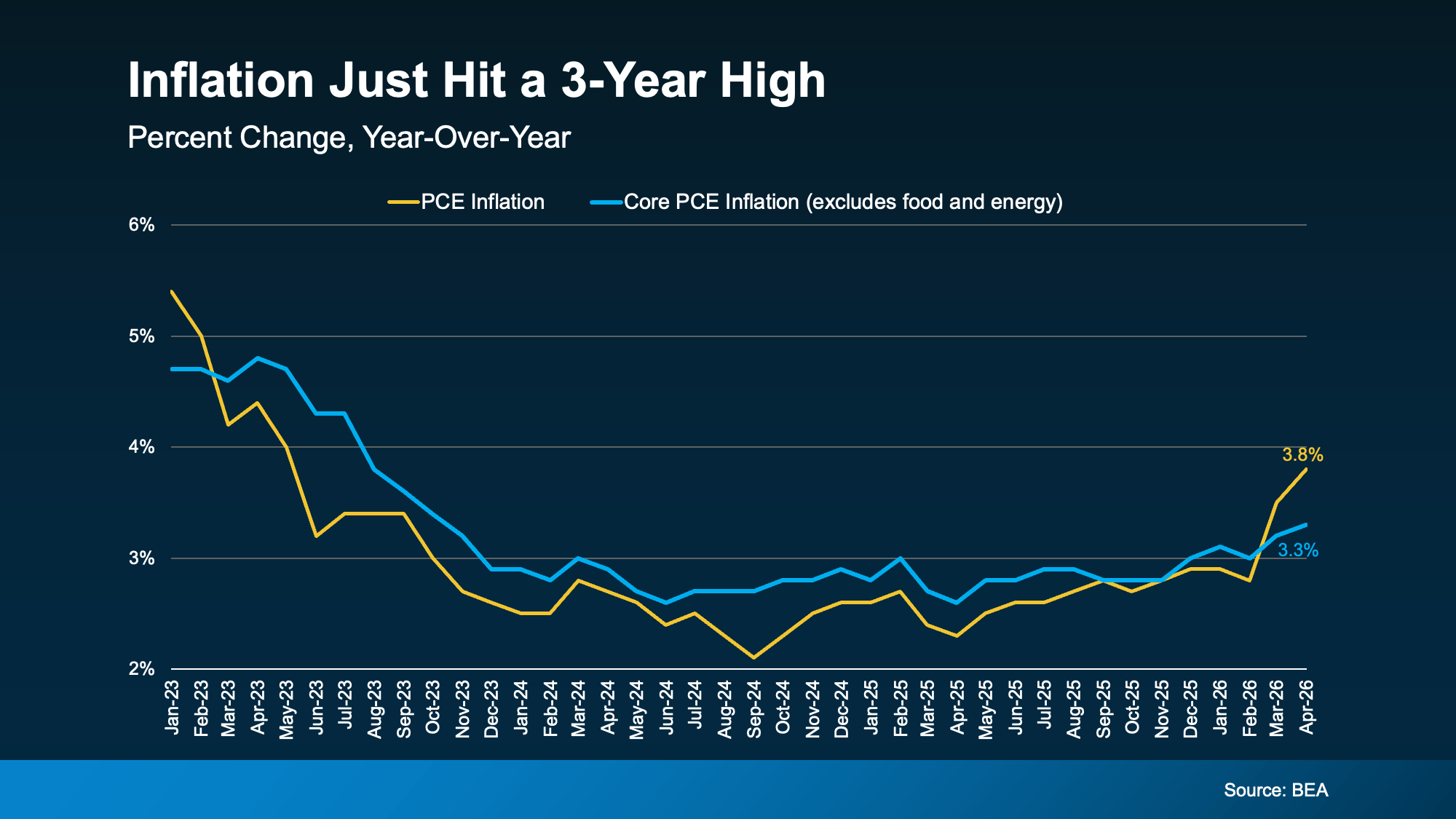

The government tracks inflation in a variety of ways. One is something called PCE – the Personal Consumption Expenditures Price Index. It measures how much more (or less) people are paying for goods and services compared to a year ago. And just based on your own expenses, you can probably guess which way that’s trending.

That’s the one everyone is talking about right now. Check out the yellow line to see how that’s spiked since February (see graph below). A big driver of this jump is the ongoing conflict in the Middle East, which has pushed gas and energy prices significantly higher.

Now, you may have noticed there’s a second line. The blue line shows core PCE. That’s the same measure, but with gas and energy prices stripped out. The Federal Reserve (the Fed) actually watches this number most closely because energy prices swing around a lot and can be misleading.

And here’s the somewhat encouraging part.

Core PCE is rising, but not nearly as fast as the overall number. That suggests a good chunk of the inflation spike we’re seeing right now is tied directly to what’s happening overseas. So, when that situation settles down, inflation may settle a bit, too.

Why This Matters for Mortgage Rates

Here’s the housing connection. When inflation is high, the Fed tends to keep the Federal Funds Rate elevated or even raise it to try to taper spending and cool inflation back down. And while it’s not a one-for-one relationship, that Federal Funds Rate can have an impact on your mortgage rate when you buy.

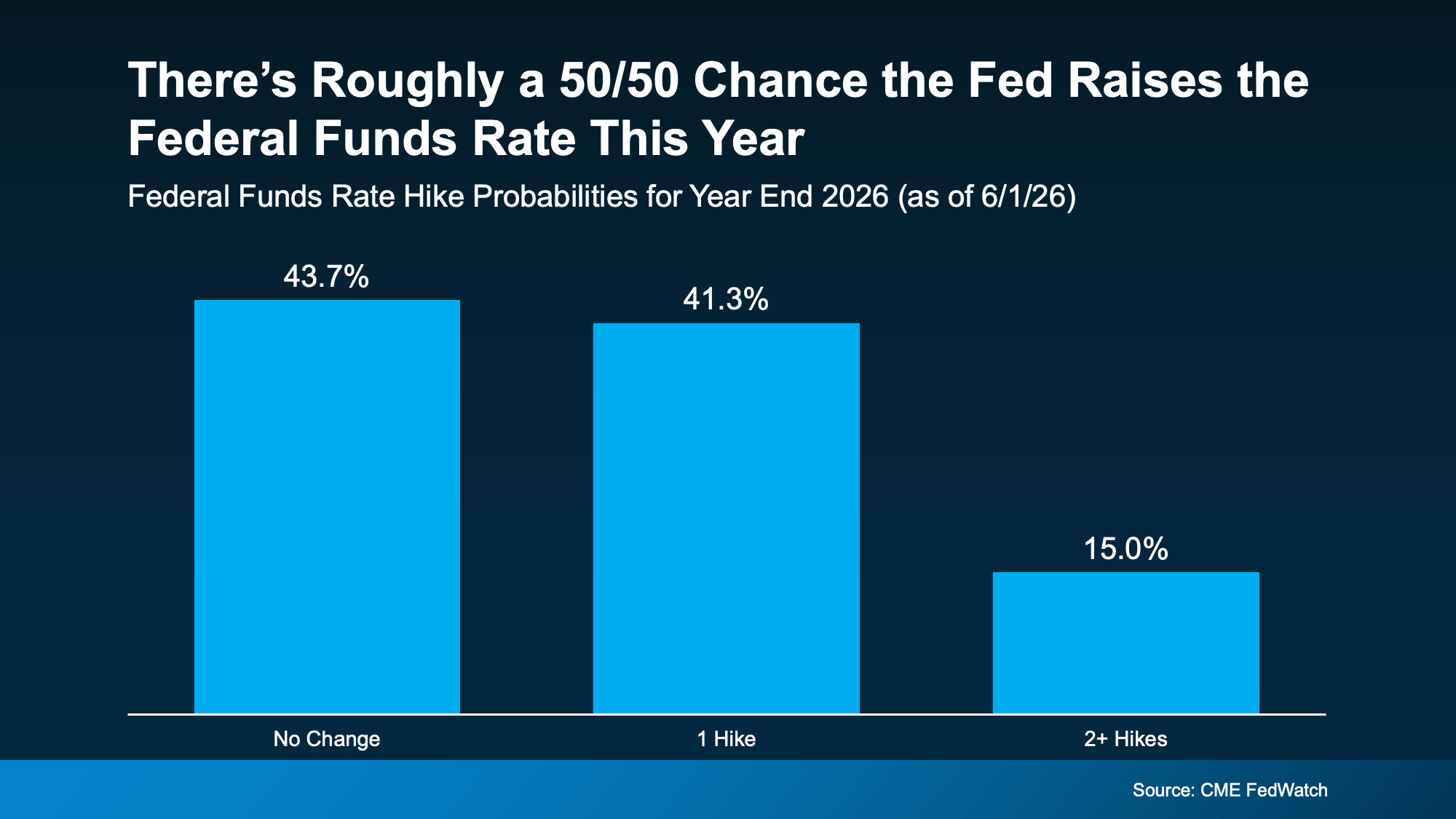

Right now, based on the information we have, there’s roughly a 50/50 chance the Fed actually raises the Federal Funds Rate before the end of 2026, according to CME FedWatch (see graph below):

While it’s too soon to say where this goes for certain and if we’re headed for a rate hike, it does mean mortgage rates are probably not coming down as soon as most people were hoping.

If you’ve been waiting for rates to drop significantly before making a move, this report is a reminder that “higher for longer” is still very much on the table. It really all depends on where the economy goes from here. According to Bankrate:

“Oil prices and bond yields have dropped a bit . . . but they’re still way up compared to the start of spring. Until there’s a resolution to the war, look for both inflation and mortgage rates to stay high.”

But This Is Not 2008 – Not Even Close

Just remember, a tough economy does not equal a housing crash. The conditions today are very different from what led to the 2008 collapse. Here’s why:

-

Inventory is still relatively low. There’s no flood of homes hitting the market.

-

Most homeowners today have strong equity in their homes.

-

Lending standards are far stricter than they were before 2008.

-

Today’s challenge is affordability, not a wave of distressed underwater sellers.

Uncomfortable and unhealthy are not the same thing. The market feels hard right now, but “hard” and “crashing” are very different.

You Still Have Options. Here’s What To Do.

High rates don’t mean homeownership is out of reach. It just means the path looks a little different. There are real strategies that can help, depending on your situation:

-

Ask your lender about different loan options. Adjustable-rate mortgages (ARMs) or rate buydowns may help lower your monthly payment in the short term.

-

Explore first-time buyer programs, down payment assistance, or seller concessions that could help offset costs.

-

Stay in close touch with a trusted agent and lender. When rates shift, and they will, you’ll want to be ready to move fast.

The right strategy, tailored to your goals, matters a lot more than waiting for the perfect moment that may never come.

Bottom Line

Inflation is still above where the Fed wants it, and that means mortgage rates are likely to stay elevated for a while. But for people who need to move, strategy matters far more than trying to perfectly time the market.

Wondering what this means for your specific situation? Connect with a local agent or lender.

You started shopping with a specific mental image of your future home in your mind. Then the houses in your budget came in smaller than you pictured.

That’s the reality for a lot of buyers right now. Affordability is tight.

But don’t let that discourage you. Going smaller might actually be a smart play in today’s market – and the upside can be bigger than you’d think. Let’s break down two places to look where smaller won’t necessarily feel like a compromise.

Homebuilders Are Focused on Smaller Options Lately

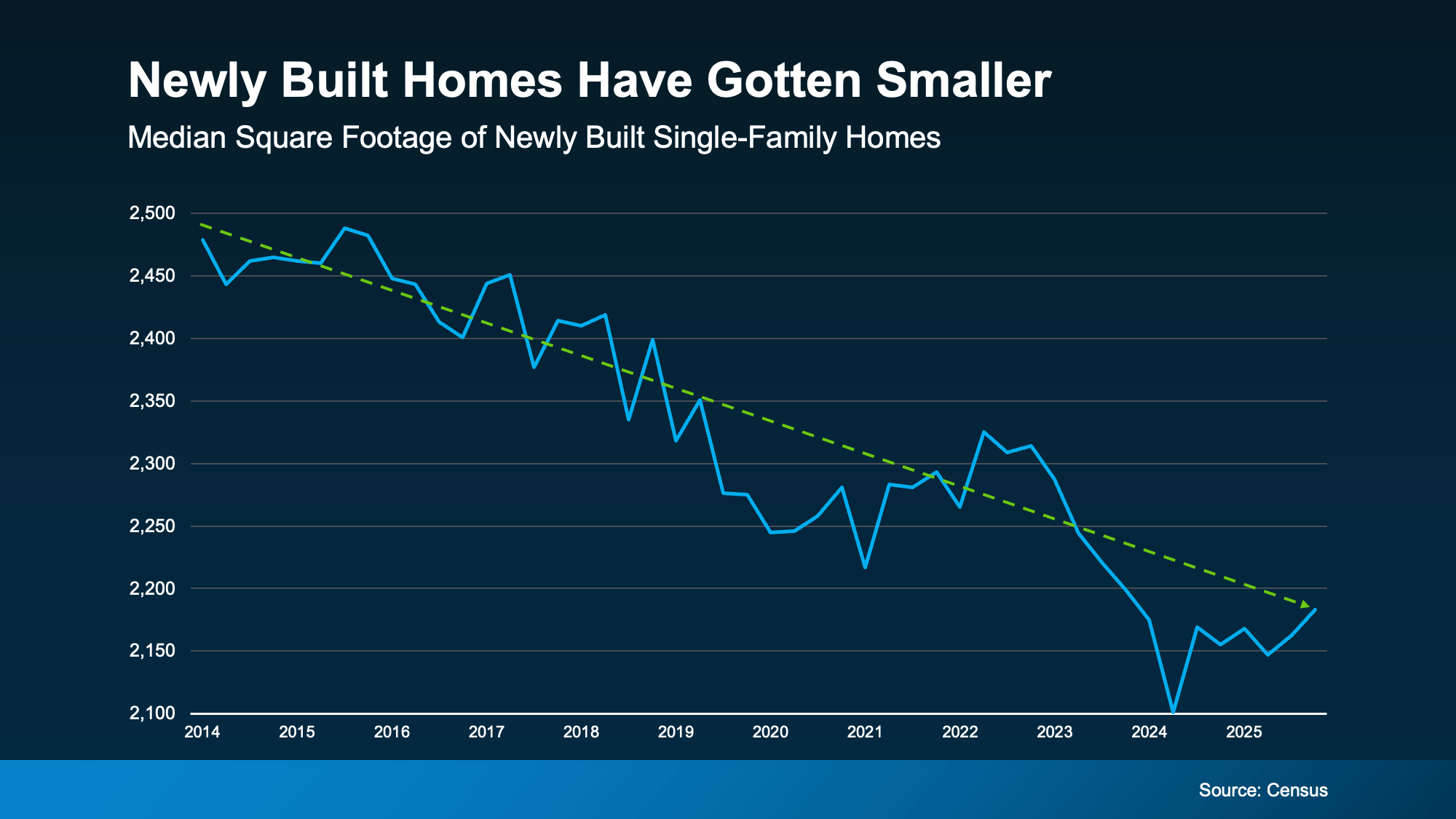

For starters, smaller is kind of on trend right now. Newly built homes have been shrinking for years. According to the latest data from the Census, the median square footage of new single-family homes has been falling overall since 2014 (see graph below):

Why? Builders focus on the types of homes consumers want the most. After all, they want to build what will actually sell. And for the past decade, buyers seem to agree less is more.

Especially right now, when affordability is a key concern, they’re building homes with smaller square footage than a decade ago. And that’s good because that may be more within budget for many buyers. It’s part of why new home prices recently hit a 5-year low.

So, if you’re not getting excited about any of the existing options at your price point, it may be time to check out what builders are doing in your area.

You may find brand-new options you really love with all the latest and greatest features. And if you’ve got modern appliances and design, maybe slightly less square footage doesn’t feel like that much of a compromise anymore, especially if the house is move-in ready.

Condos Are Opening Up Another Path

Just in case you don’t have a ton of new builds in your area, another avenue worth exploring is condominiums or condos.

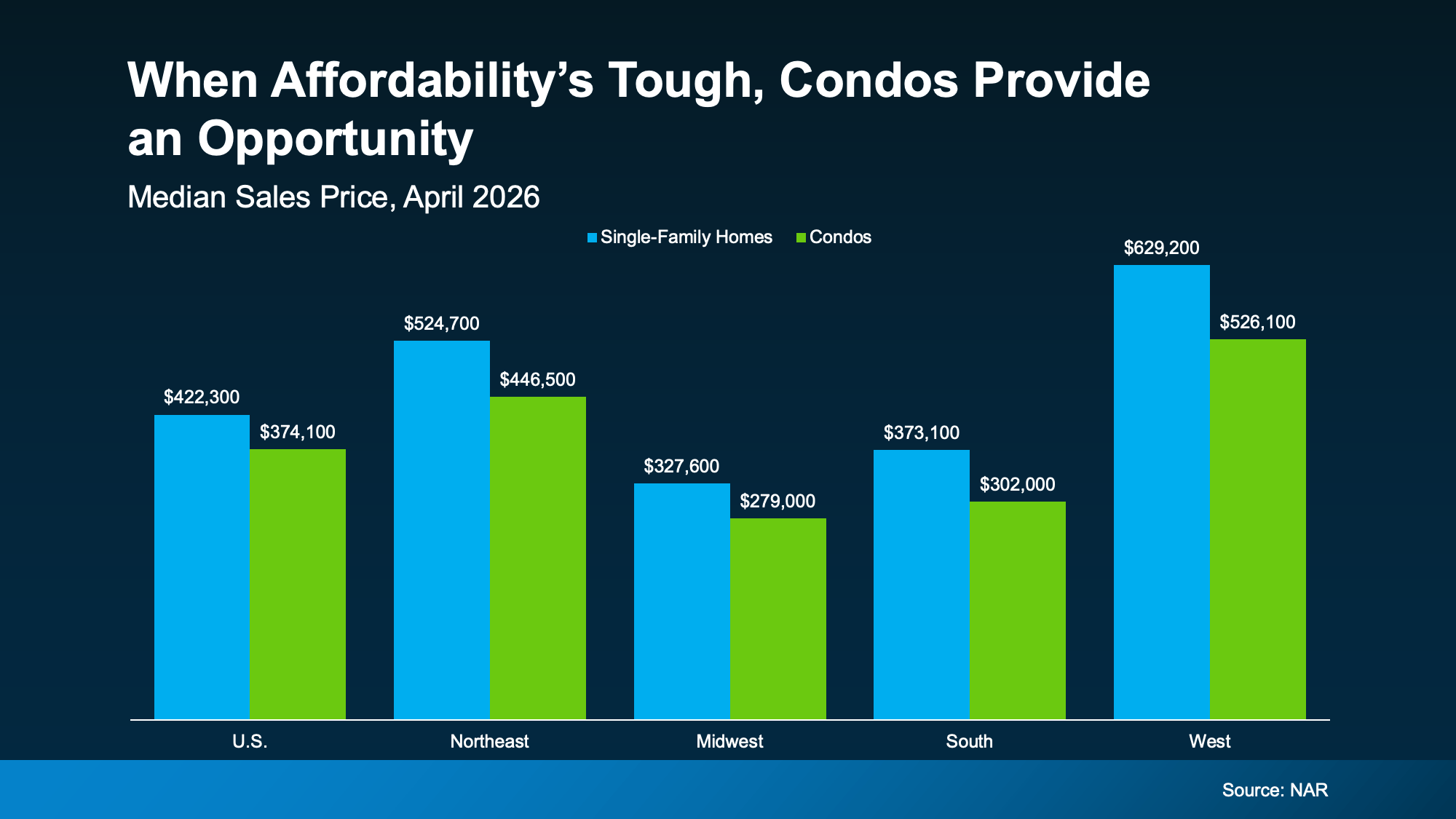

For buyers crunching numbers to make the math work, condos can take real pressure off the budget. According to the National Association of Realtors (NAR), the median price for condos is less than the median for single-family homes in every region (see graph below):

Part of that is because condos are typically smaller. And smaller square footage can come with a smaller price tag too. That’s a selling point to affordability-strapped buyers right now – and it’s one of the reasons we’re seeing a bump in condo sales.

The number of condos sold rose 2.7% from just a month ago. It’s also up year over year, according to NAR. Ali Wolf, Chief Economist for New Home Source, explains why more buyers are going this route:

“In addition to favoring smaller floor plans, more consumers are showing a willingness to live in an attached home. This shift is not driven by a preference for shared walls, but by a pursuit of value.”

The Community Does Some of the Heavy Lifting

Here’s why smaller may still work for you. Whether it’s a condo complex or a neighborhood of detached single-family homes, the right community can give you back in amenities what you trade in square footage.

Many developments are designed so the home is just one piece of where you actually spend your time. Master-planned communities often include walking trails, pools, fitness centers, co-working spaces, and outdoor gathering areas – the kind of features that pick up where your floor plan leaves off.

No room for a dedicated office? The co-working space might be just a five-minute walk away. Want a place to work out? It’s already built in with the shared gym. And features like that can make opting for a smaller footprint feel less like a compromise – and more like a big lifestyle upgrade.

Bottom Line

Today’s smaller single-family homes and condos have more going for them than the square footage suggests. They can give your budget some breathing room and put you in a community designed with lifestyle in mind.

Curious about the options in your area? Connect with a local real estate agent to walk through what’s available.

Could Moving a Bit Further Out Change Everything About Your Budget?

What Rising Inflation Means for Your Move

The Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Equity3 weeks ago

Equity3 weeks agoRecord High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out.

-

Agent Value4 weeks ago

Agent Value4 weeks agoThe Pricing Mistake That Could Cost You Your Sale

-

Agent Value4 weeks ago

Agent Value4 weeks agoWhy Staging Your House Could Pay Off This Spring

-

Equity3 weeks ago

Equity3 weeks agoAre Home Prices Going To Fall?

-

Equity4 weeks ago

Equity4 weeks agoWhat the Foreclosure Headlines Aren’t Telling You

-

Affordability3 weeks ago

Affordability3 weeks agoNewly Built Home Prices Hit a 5-Year Low

-

Affordability2 weeks ago

Affordability2 weeks agoWhat Most Veterans Don’t Know About Their VA Home Loan Benefit

-

Affordability2 weeks ago

Affordability2 weeks agoThe Truth About Affordability Today

You must be logged in to post a comment Login