Buying Tips

Thinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

If you’ve been looking for a home lately, you’ve probably felt how tough affordability still is. And that’s exactly why more buyers are opting for adjustable-rate mortgages, or ARMs.

Here’s what you need to understand about how they work, and whether they make sense for you.

What Is an Adjustable-Rate Mortgage?

Since a lot of people aren’t familiar with this type of loan, let’s start with a definition. This is how Business Insider explains the main difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Basically, one doesn’t change much over the life of your loan.

And one could change… either by a little, or a lot.

Of course, things like taxes or homeowner’s insurance can still have an impact on a fixed-rate loan, but the baseline of your mortgage payment is fairly steady. But the big difference is that with an ARM, your monthly payment could change over time.

Why Adjustable-Rate Mortgages Are Getting More Attention

So, why do some buyers choose this option? It’s simple. It’s because of the upfront savings. Business Insider explains it like this:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

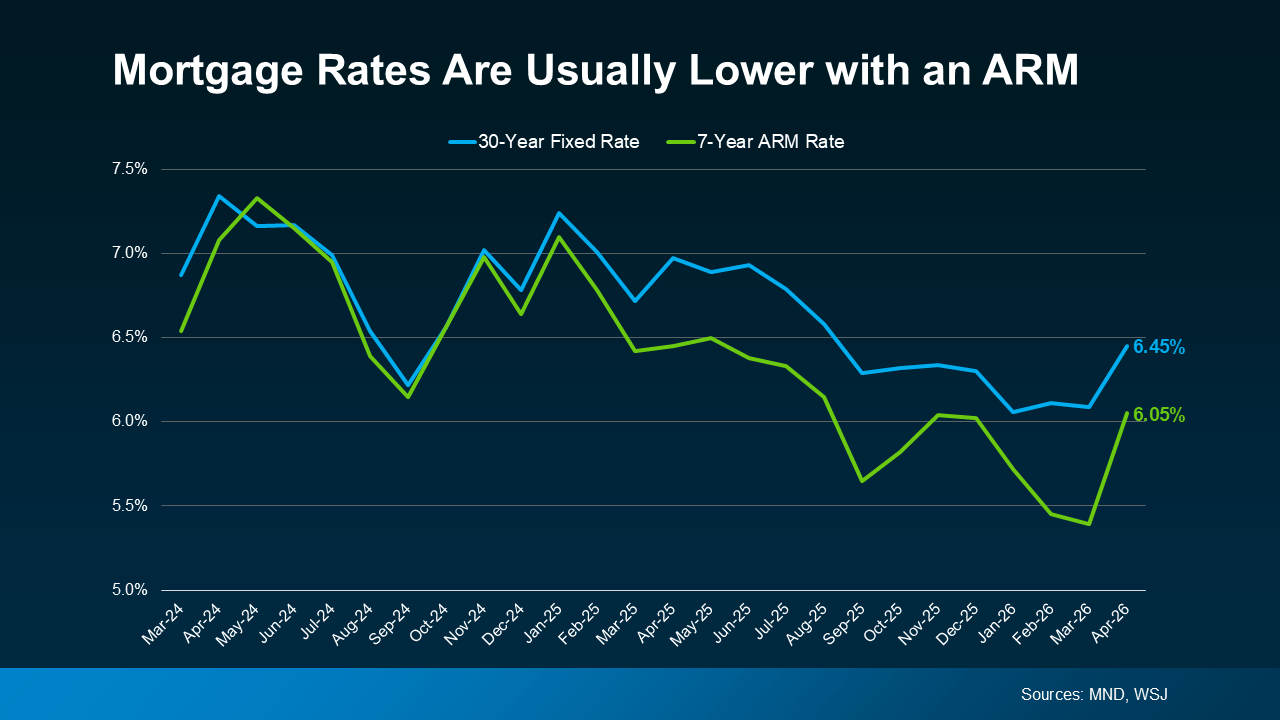

And right now, according to Mortgage News Daily and the Wall Street Journal, the upfront rate on an ARM is lower than a 30-year fixed mortgage (see graph below):

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

For some people, that’s enough to make a difference.

More Buyers Are Choosing Adjustable-Rate Mortgages Today

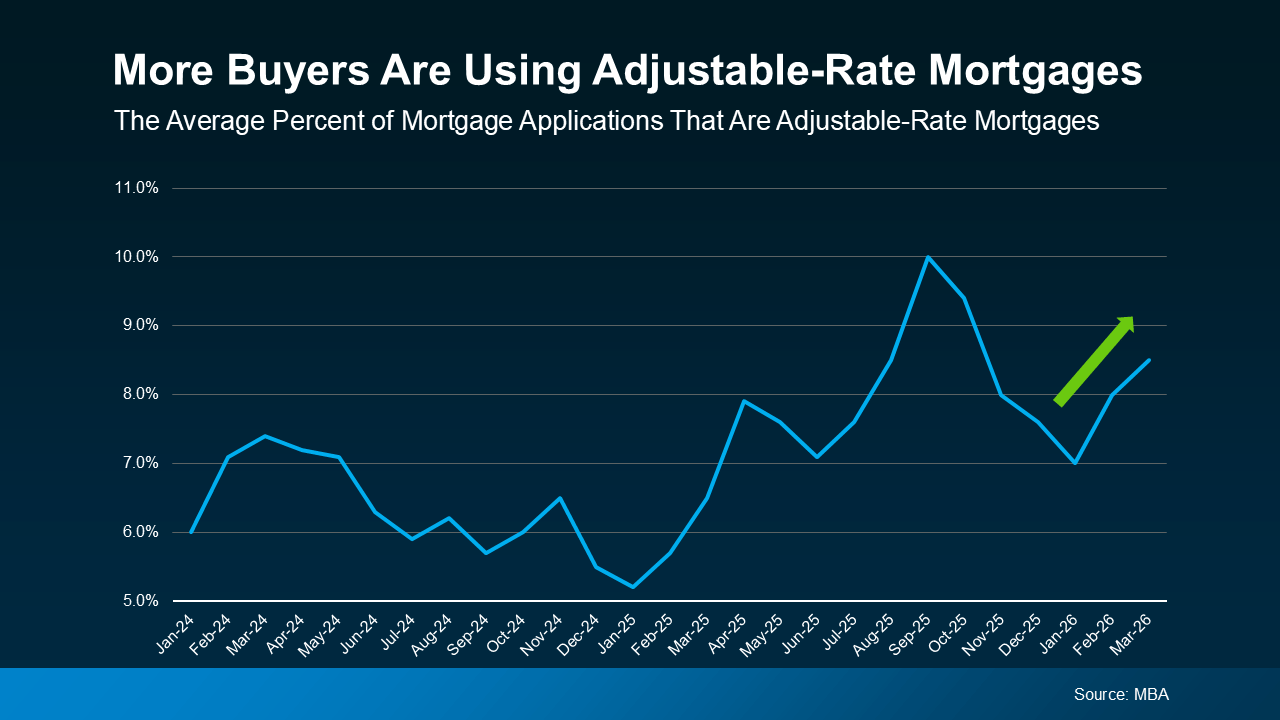

A growing number of buyers are willing to trade the uncertainty later for a lower payment now. Data from the Mortgage Bankers Association (MBA) shows the share of buyers choosing ARMs has increased, especially over the last few years (see graph below).

This doesn’t mean ARMs are becoming the go-to option for everyone. It only means some buyers are opting for this type of mortgage, so they can still buy today.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

Back then, some buyers were given loans they couldn’t afford once rates adjusted.

Today, lending standards are stricter, and lenders evaluate whether borrowers could still handle the payment if rates rise. So, the return of ARMs doesn’t signal another widespread crash. It just reflects how some buyers are adapting to today’s affordability challenges.

The Trade-Off – What You Need To Consider

If you’re considering an adjustable-rate mortgage yourself, just remember it really all depends on your situation and your risk tolerance.

An ARM may make sense if you plan to move before your rate would adjust or if you expect you’ll make a higher income in the future. But there are trade-offs you need to think through.

For example, once the fixed period ends, your rate can adjust, and your payment could increase, potentially by a meaningful amount depending on where rates are at that time.

And keep in mind, there’s also no guarantee mortgage rates will come down in the future, which means refinancing later isn’t always an option. That’s why it’s important to think through your plan, understand your long-term earning potential, and work closely with a trusted lender before you choose an ARM.

Bottom Line

ARMs are getting more attention again because they can make buying a home more affordable in the short term. But they’re not right for everyone.

The key is understanding how they work, what the risks are, and whether they fit your plan. And that’s why you need to talk to a trusted lender and financial advisor before you make any decisions.

Nearly half of Veterans (49%) feel homeownership is currently out of reach, according to a recent survey from NewDay USA.

But many are closer than they think. And you might be, too.

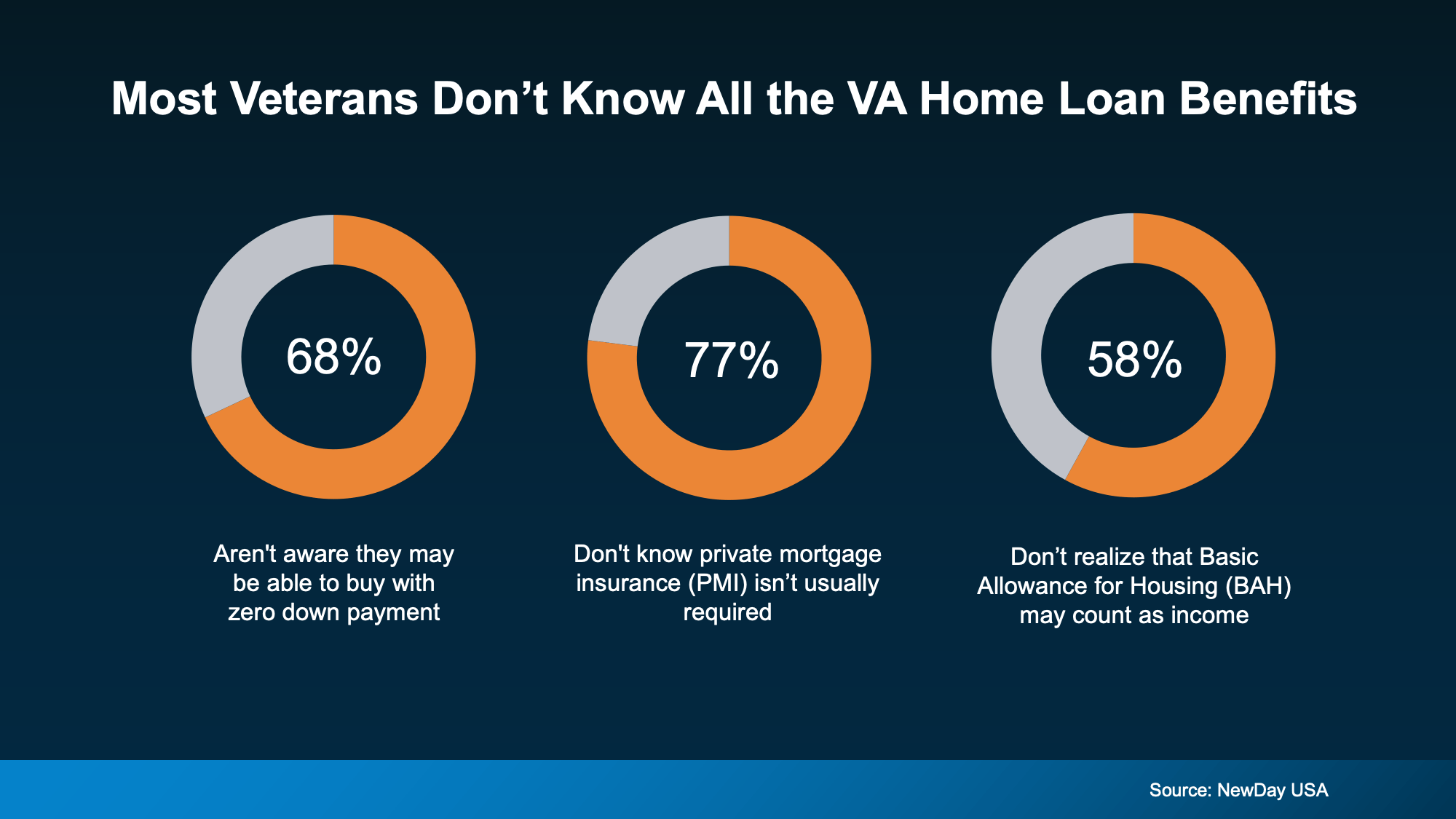

If you’re a Veteran, you probably know the Veterans Affairs (VA) home loan benefit exists – it’s been around for over 80 years. What you might not know is what it actually covers. Three misconceptions trip up Veterans the most (see graph below):

Any one of those beliefs could be holding you back. Let’s walk through all three, so you have the information you really need.

Any one of those beliefs could be holding you back. Let’s walk through all three, so you have the information you really need.

You May Not Have To Put Any Money Down

The potential to put zero money down is probably the biggest perk of a VA loan, but most homebuyers don’t even realize that’s an option. According to the NewDay USA survey, many respondents guessed they’d need to save somewhere between $10,000 and $19,900 before they could buy. That’s years of saving for an upfront cost that isn’t always required.

You May Have Lower Closing Costs

According to the Department of Veterans Affairs, with VA loans, there can be limits on the types of closing costs buyers have to pay. That means more money stays in your pocket on closing day – and you have less to save up for before you can buy. The benefit combined with the down payment perk can speed up your buying timeline.

Your Monthly PMI Costs Could Be $0

Unlike many other loan options, VA loans typically don’t require private mortgage insurance (PMI), even with low or no money down. If you take out a conventional loan instead, you could pay $100 to $300 a month in PMI until you hit 20% equity, according to NewDay USA. Over time, that’s a difference of thousands of dollars.

Your BAH & BAS May Help You Qualify for More

If you’re on active duty or if you’re a qualifying reservist, your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward income qualification on a VA loan. So, if you were running the numbers without factoring your BAH or BAS in, you could qualify for more than you thought. Both BAH and BAS are non-taxable, so they can help raise the amount you can qualify for.

Bottom Line

VA home loans can put homeownership within reach, and a trusted lender can help make sure you understand the details before you move forward.

If you’re active duty, you’ve served, or know someone who has, connect with a trusted lender who can walk you through whether you’d qualify and what the VA benefit offers. You may be able to buy a home sooner than you thought.

If you’ve always assumed a newly built home is just not in your budget, you should know the math just got a little friendlier.

The median sale price of a newly built home is now at its lowest level since 2021, according to the latest data from the Census. And on top of that, builders are still rolling out incentives to bring buyers through the door.

Here’s what’s happening, and what it means if you’re shopping right now.

Prices on Newly Built Homes Have Come Down

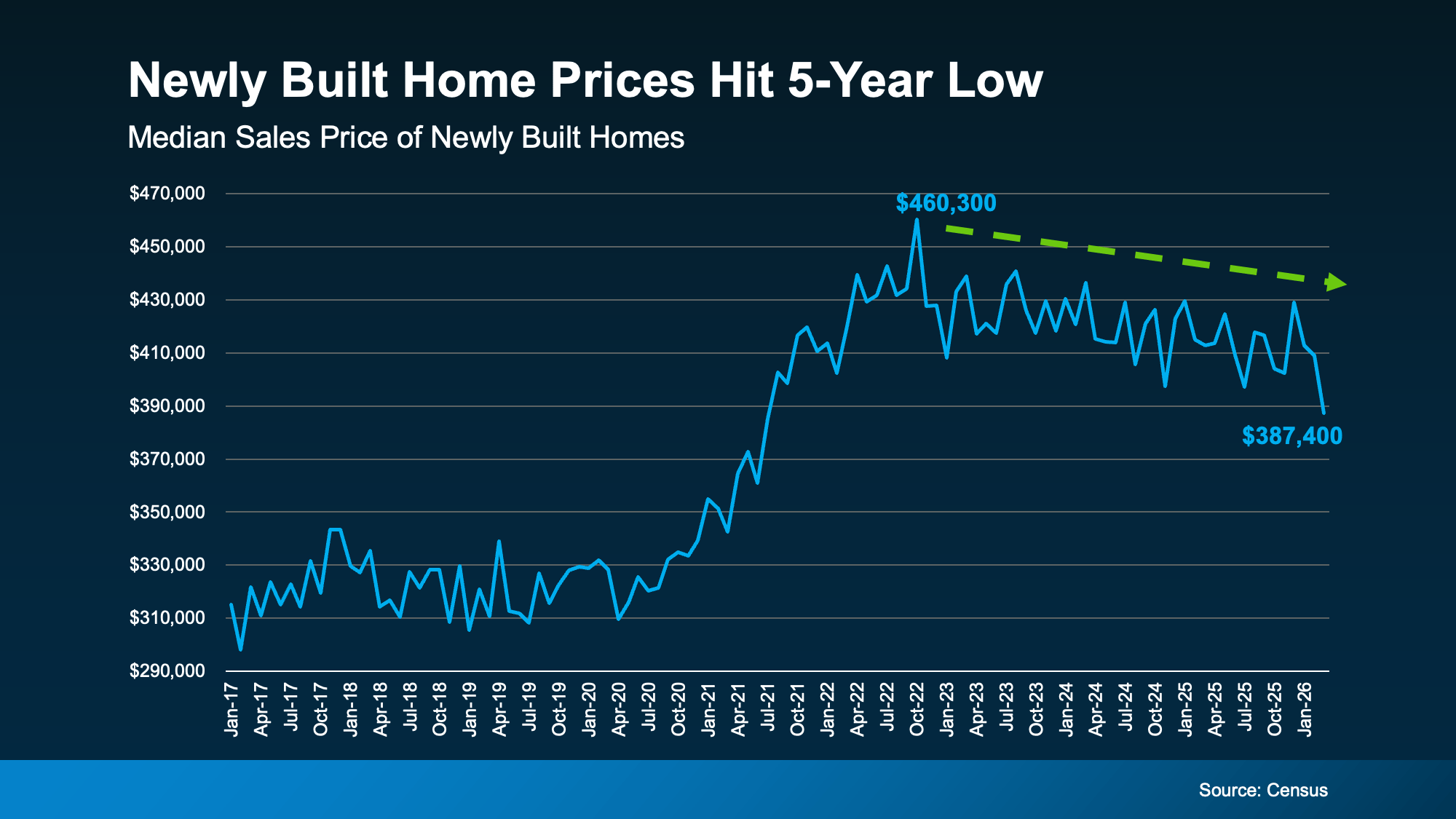

After a steep climb during the pandemic years, prices have eased a bit. The median sale price of newly built homes is sitting at about $390,000. That’s the lowest it’s been in nearly five years (see graph below):

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

That doesn’t mean every home in every market is suddenly affordable. But it does mean that, broadly, you’ll see the best prices on new builds since 2021, if you’re buying now.

Why This Isn’t a Repeat of 2008

And just in case you’re thinking it, lower prices don’t mean the new home market is in trouble. Builders today are being intentional about how much inventory they have, so it doesn’t pile up the way it did in 2008.

If you look back up at the graph, you’ll see that even after the recent improvement in new home prices, they’re still higher than pre-pandemic norms. So, this isn’t a crash. It’s a builder strategy to keep inventory moving.

Homebuilders Are Still Sweetening the Deal

Lower sticker prices aren’t the only break buyers are getting. According to the National Association of Home Builders (NAHB), 60% of builders are currently offering some form of incentive to attract buyers. Those typically include:

- Help with closing costs: Some builders are covering thousands of dollars in fees to reduce the upfront cost of buying.

- Extra upgrades: Think premium finishes, appliance packages, and designer features, often added at no extra cost.

- Mortgage rate buydowns: When the builder pays to lower your mortgage rate, which reduces your monthly payment.

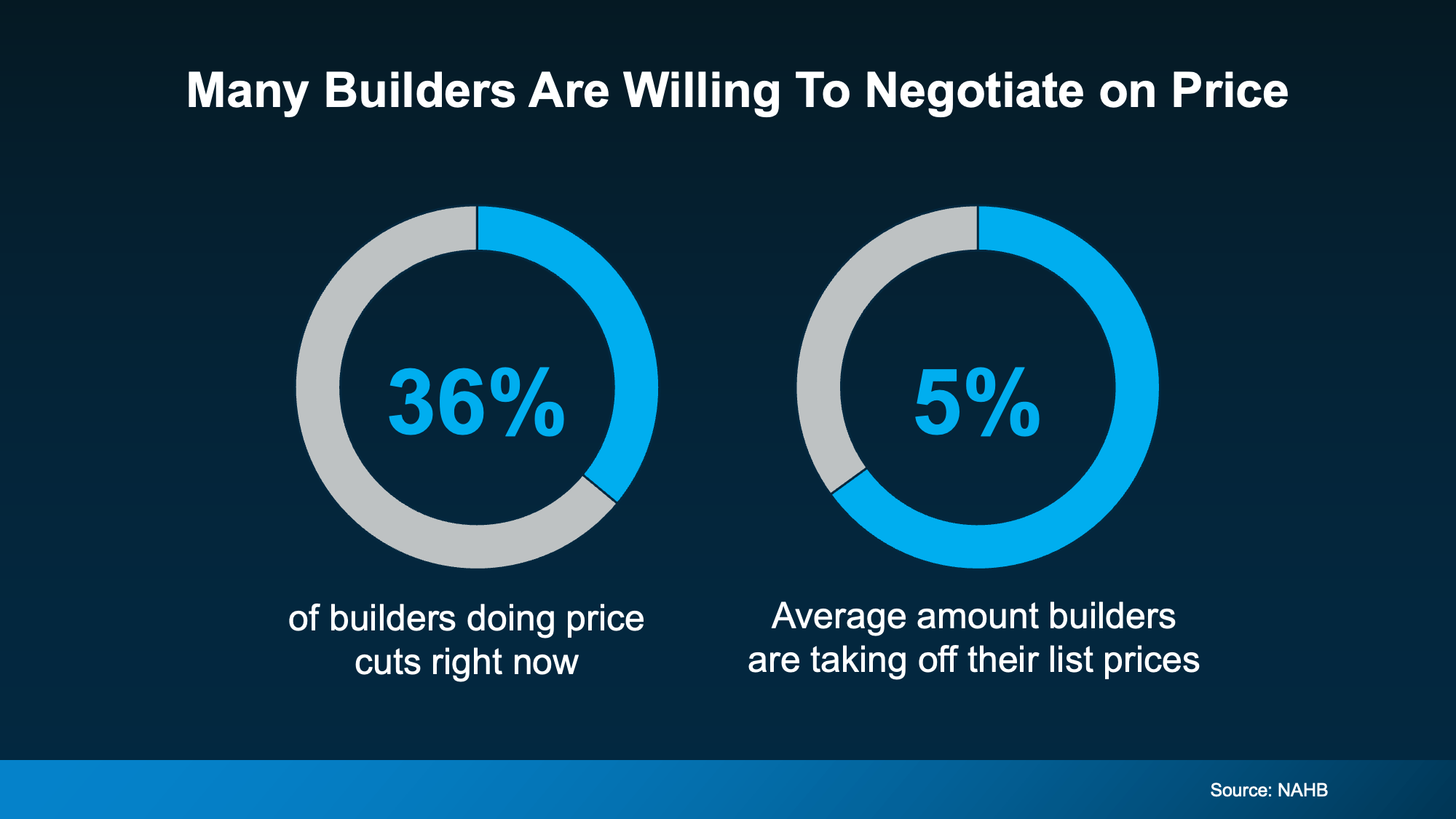

- Price cuts: Over one in three builders (36%) are cutting prices right now, averaging about 5% off list price (see graph below):

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

But builders need to move what they’ve built. That’s a different mindset than a homeowner deciding whether to budge on price. So, you may find they’re more open to adjusting the price than you’d think. As Joel Berner, Senior Economist at Realtor.com, puts it:

“. . . many existing-home sellers resort to taking down their listing instead of taking less than their desired price, but builders are more motivated to sell their inventory than owner-occupants . . .”

And if you use the version of the graph that shows 2008 prices, you can even reference that in this explainer.

And if here, should I change the last sentence of the lede?

Bottom Line

Builder incentives and lower new home prices are working to your advantage in a way they haven’t in years. Connect with a local real estate agent to see what’s available in your area and what kind of deal a builder may be willing to make.

For a lot of would-be first-time buyers, affordability is the thing that’s standing in the way. But some buyers are getting creative and finding a way to still make the numbers work – and that’s through co-buying.

The Dream Is Still Alive. The Math Just Isn’t Working for Everyone.

Young people haven’t given up on the dream of owning a home – not even close. According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation.

The problem? 73% of Gen Z and millennial buyers cite affordability as the reason for not making homeownership a priority. And it shows. First-time buyers now make up just 21% of all home purchases, the lowest share since the National Association of Realtors (NAR) started tracking the data in 1981.

But still, some buyers are making it happen. And a portion of them are turning to co-buying to get their foot in the door.

So, What’s Co-Buying?

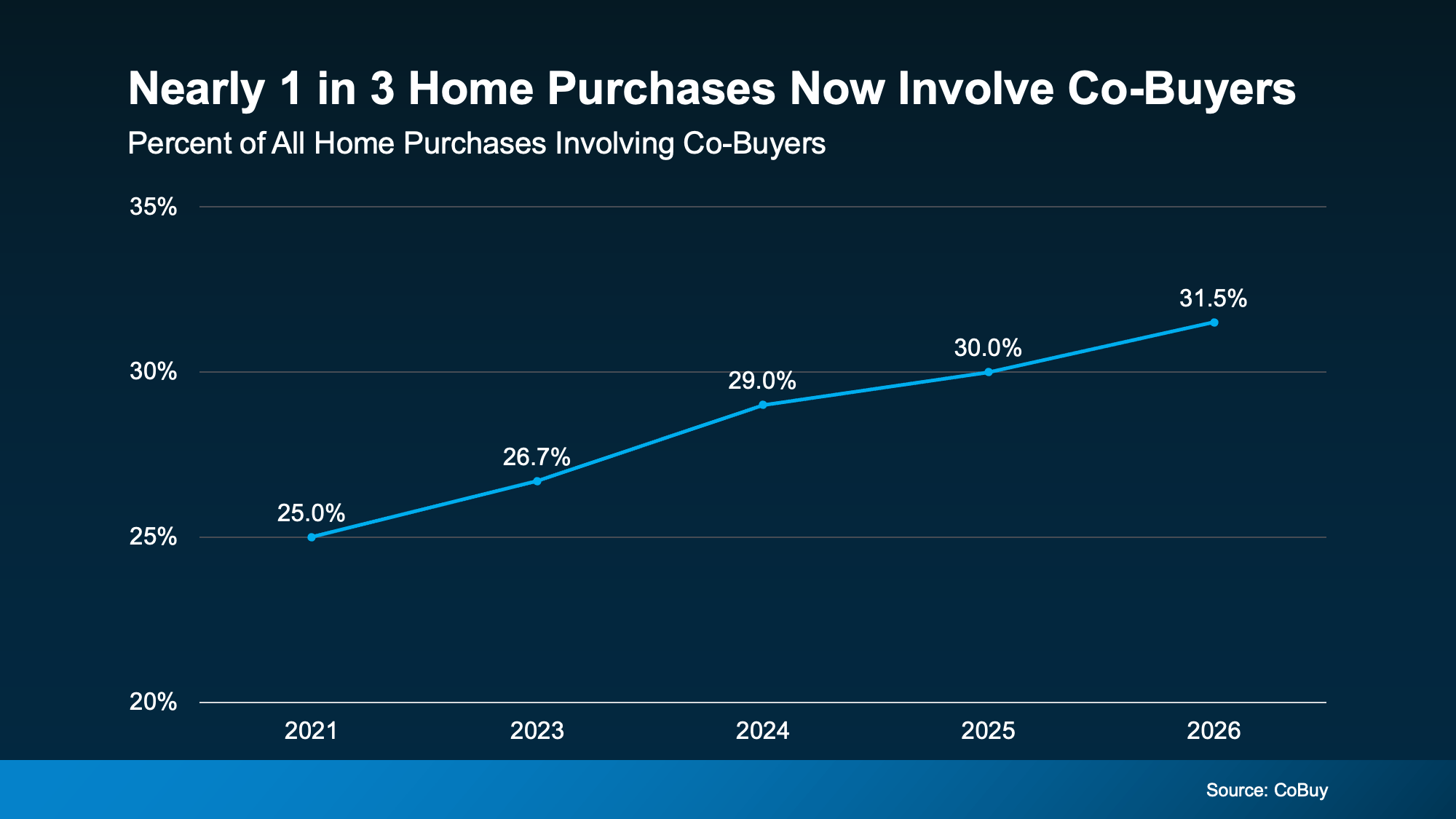

Co-buying means purchasing a home with someone else, like a friend, sibling, or unmarried partner. You combine incomes, split the down payment, and share monthly costs. For some people, it’s a creative way to turn “someday” into a concrete move-in date that’s just around the corner.

And it’s catching on fast, just look at where things stand today. According to CoBuy.io, 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers (see graph below):

Why It Works

Why It Works

Here are just a few of the top reasons buyers are going this route, according to NerdWallet:

- Quicker path to homeownership: If owning a home is a serious goal for you, buying with someone else can help make that reality on a shorter timeline. Two or more people can save up a down payment a lot faster than one. That’s less time waiting and more time building equity in a place that’s yours.

- More purchasing power: With multiple incomes going toward the home purchase, you might be able to afford a nicer home or live in a more popular neighborhood. Sometimes teaming up means getting the home you actually want, not just the one you can barely afford on your own.

- Easier loan qualification: Added income from more than one buyer can also help with your debt-to-income (DTI) ratio, which the lender will calculate based on all the borrowers.

- Lower housing costs: Splitting up a mortgage payment multiple ways could maybe even make owning less expensive than renting. Plus, sharing costs can make repairs or renovations more manageable, too.

Things To Keep in Mind

If you’re considering going this route, there are some things you’ll want to think over. For starters, co-buying works best with people you trust and share financial goals with. So, before moving forward, make sure everyone agrees on how costs are split, who handles what, and what happens if one person wants to sell down the road.

That’s why a written co-ownership agreement can be a smart move. It keeps everyone on the same page and helps avoid headaches down the line. Think of it less like a legal formality and more like a game plan for your new investment.

Bottom Line

Affordability challenges are real, but they don’t have to mean waiting indefinitely. Co-buying is helping some first-time buyers stop waiting and start putting down roots.

If you’re curious whether it could work for your situation, talk with a local real estate agent. Reach out today and figure out your path to homeownership together.

What Most Veterans Don’t Know About Their VA Home Loan Benefit

Newly Built Home Prices Hit a 5-Year Low

Record High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out.

-

Affordability3 weeks ago

Affordability3 weeks agoCould Co-Buying Be the Answer for Some First-Time Buyers?

-

Featured3 weeks ago

Featured3 weeks ago3 Things That Are Not Going To Happen in Today’s Housing Market

-

Agent Value3 weeks ago

Agent Value3 weeks agoStay or Sell? How To Make the Right Call as You Age

-

Equity3 weeks ago

Equity3 weeks agoRent or Buy? The Real Tradeoff Most People Don’t Talk About

-

For Buyers3 weeks ago

For Buyers3 weeks agoMore Options Are Popping Up This Spring

-

Affordability3 weeks ago

Affordability3 weeks agoThink You Have To Put 20% Down? Most First-Time Homebuyers Don’t.

-

For Sellers3 weeks ago

For Sellers3 weeks agoIs Late May the Best Time To List Your House?

-

Buying Tips3 weeks ago

Buying Tips3 weeks ago4 Ways To Give Your Offer an Edge This Spring

You must be logged in to post a comment Login