Baby Boomers

How Buyers Can Win By Downsizing in 2020

Have you heard the term “Silver Tsunami” getting tossed around recently? If so, here’s what you really need to know. That phrase refers to the idea that a lot of baby boomers are going to move or downsize all at once. And the fear is that a sudden influx of homes for sale would have a big impact on housing. That’s because it would create a whole lot more competition for smaller homes and would throw off the balance of supply and demand, which ultimately would impact home prices.

But here’s the thing. There are a couple of faults in that logic. Let’s break them down and put your mind at ease.

Not All Baby Boomers Plan To Move

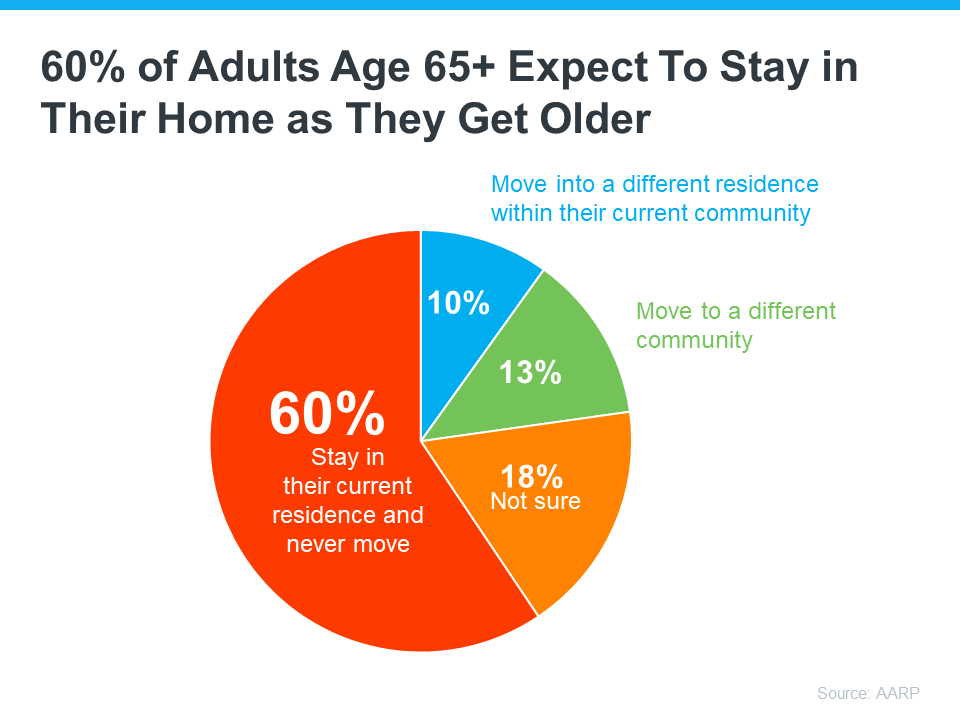

For starters, plenty of baby boomers don’t plan on moving at all. A study from the AARP says more than half of adults aged 65 and older want to stay in their homes and not move as they age (see graph below):

While it’s true circumstances may change and some people who don’t plan to move (the red in the chart above) may realize they need to down the road, the vast majority are counting on aging in place.

As for those who stay put, they’ll likely modify their homes as their needs change over time. And when updating their existing home won’t work, some will buy a second home and keep their original one as an investment to fuel generational wealth for their loved ones. As an article from Inman explains:

“Many boomers have no desire to retire fully and take up less space . . . Many will modify their current home, and the wealthiest will opt to have multiple homes.”

Even Those Who Do Move Won’t Do It All at Once

While not all baby boomers are looking to sell their homes and move – the ones who do won’t all do it at the same time. Instead, it’ll happen slowly over many years. As Freddie Mac says:

“We forecast the ‘tsunami’ will be more like a tide, bringing a gradual exit of 9.2 million Boomers by 2035 . . .”

As Mark Fleming, Chief Economist at First American, says:

“Demographics are never a tsunami. The baby boomer generation is almost two decades of births. That means they’re going to take about two decades to work their way through.”

Bottom Line

If you’re stressed about a Silver Tsunami shaking the housing market overnight, don’t be. Baby boomers will move slowly over a much longer period of time.

If you’re thinking about retirement or have already retired this year, it’s a good time to consider if your current house is still a good fit for the next chapter in your life.

Fortunately, you may be in a better position to make a move than you realize. Here are a few things to think about as you decide whether or not to sell and make a move.

How Long You’ve Been in Your Home

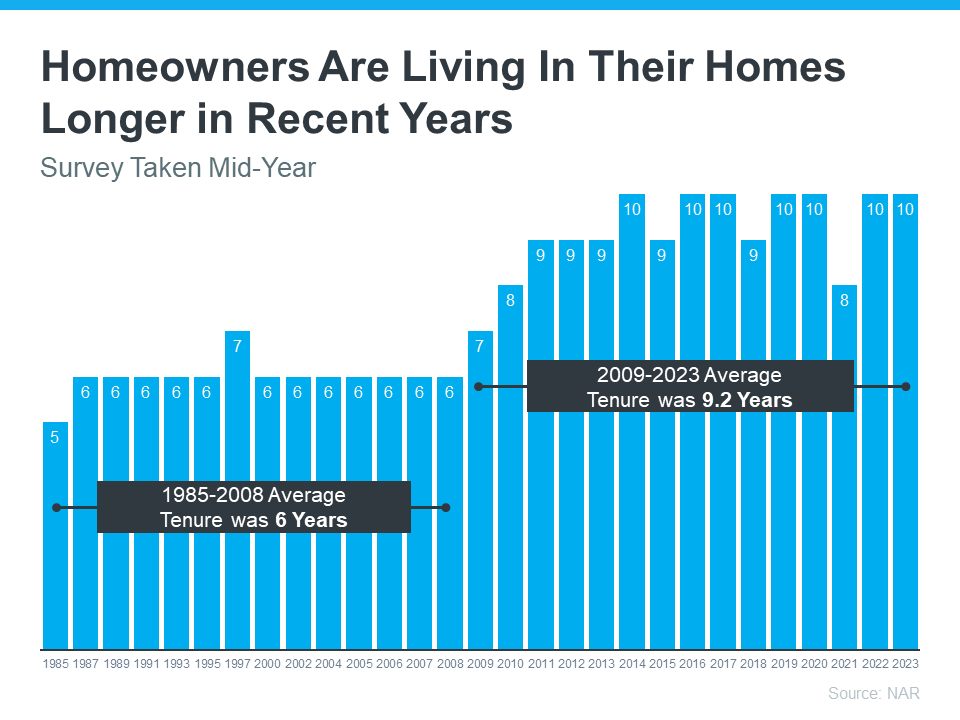

From 1985 to 2008, the average length of time homeowners typically stayed in their homes was only six years. But according to the National Association of Realtors (NAR), that number is rising today, meaning many homeowners are living in their houses even longer (see graph below):

When you live in a home for a significant period of time, it’s natural for you to experience a number of changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options waiting for you.

How Much Equity You’ve Gained

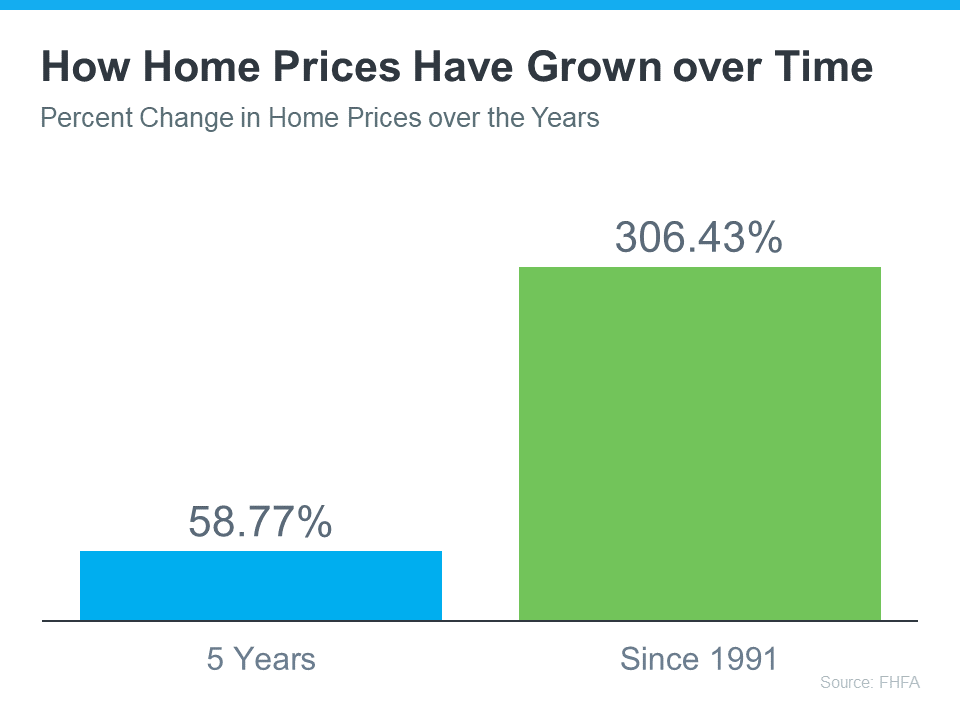

Additionally, if you’ve been in your house for more than a few years, you’ve likely built-up significant equity that can fuel your next move. That’s because the longer you’ve been in your house, the more likely it’s grown in value due to home price appreciation. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):

While home price growth varies by state and local area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home since 1991 saw it more than triple in value over that time.

Consider Your Retirement Goals

Whether you’re looking to downsize, relocate to a dream destination, or simply be closer to loved ones, your home equity can be a key to realizing your homeownership goals. NAR shares that for recent home sellers, the primary reason to move was to be closer to loved ones.

Whatever your home goals are, a trusted real estate agent can work with you to find the best option. They’ll help you sell your current house and guide you through buying the home that’s right for your lifestyle today.

Bottom Line

Retirement can bring about major changes in your life, including what you need from your home. Connect with a local real estate agent to explore the available homes in your area.

During the pandemic, many people distanced themselves from their loved ones for health reasons. Grandparents were told to stay away from their grandkids, especially as schools started to open. That’s because it would have been risky to visit with their grandchildren who may have gotten sick from school.

Now that the pandemic has passed, many grandparents want more than ever to be near their grandchildren again to make up for that lost time. But how are they getting that “Grandparent Wish?” The data tells us many are moving to make sure they’re getting more quality time.

Grandparents Are Moving To Be Near Loved Ones

Recent data from the National Association of Realtors (NAR) shows people between the ages of 55 and 74 are moving farther (more than 100 miles) than any other age group (see graph below):

The average age of grandparents in the U.S. is 67 years. The logical leap is that at least some of the people who are moving the furthest are grandparents. But what’s causing them to move so far?

The same report from NAR shows the top reason people move is to be closer to loved ones (see graph below):

Based on this data, it’s fair to say many grandparents are getting their wish of more quality time with their grandchildren by moving to be closer to them. And after experiencing isolation and loneliness during the COVID pandemic, that’s an especially good thing.

If you’re a grandparent, you know how important your grandchildren are. And you may be willing to sell and move just to be closer by. As Vance Cariaga, a journalist at Go Bank Rates, explains:

“Never underestimate the power of grandchildren – especially when it comes to lifestyle and financial decisions. Recent data shows that many baby boomers are relocating further away from home than they used to so they can be closer to their grandbabies.”

Bottom Line

The data shows grandparents are moving further to be near their grandchildren. If you have grandchildren of your own, maybe you can relate. When you decide it’s time to be closer to your loved ones, connect with a local real estate professional.

The House That Started It All Could Kickstart What’s Next

Priced Out? A Condo or Townhome Could Be Your Way In.

More Homes, Better Prices: A Buyer’s Summer

-

Agent Value4 weeks ago

Agent Value4 weeks agoYour House Didn’t Sell. Here’s How To Turn It Around.

-

Equity3 weeks ago

Equity3 weeks agoThe Housing Market Is Stronger Than You Think

-

Economy3 weeks ago

Economy3 weeks agoWhat Buying or Selling a Home Gives Back to Your Community

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThe 1 Factor That Explains Everything Happening with Home Prices Right Now

-

Affordability3 weeks ago

Affordability3 weeks agoDown Payments Are Smaller Than They’ve Been Since 2021

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoStudent Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

-

Affordability2 weeks ago

Affordability2 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

You must be logged in to post a comment Login