For Buyers

2 of the Factors That Impact Mortgage Rates

Remember the chatter in the headlines about all the homes big institutional investors were buying? If you were thinking about buying a home yourself, you may have wondered how you’d ever be able to compete with that. Here’s the thing. That’s not the challenge so many people think it is – especially right now.

Let’s break down what’s really going on and why the recent shift in the approach investors are taking could tip the scales in your favor.

Large Investors Are Pulling Back

The truth is institutional investors never represented as big a share of the housing market as people think. And now, they’re backing off even more.

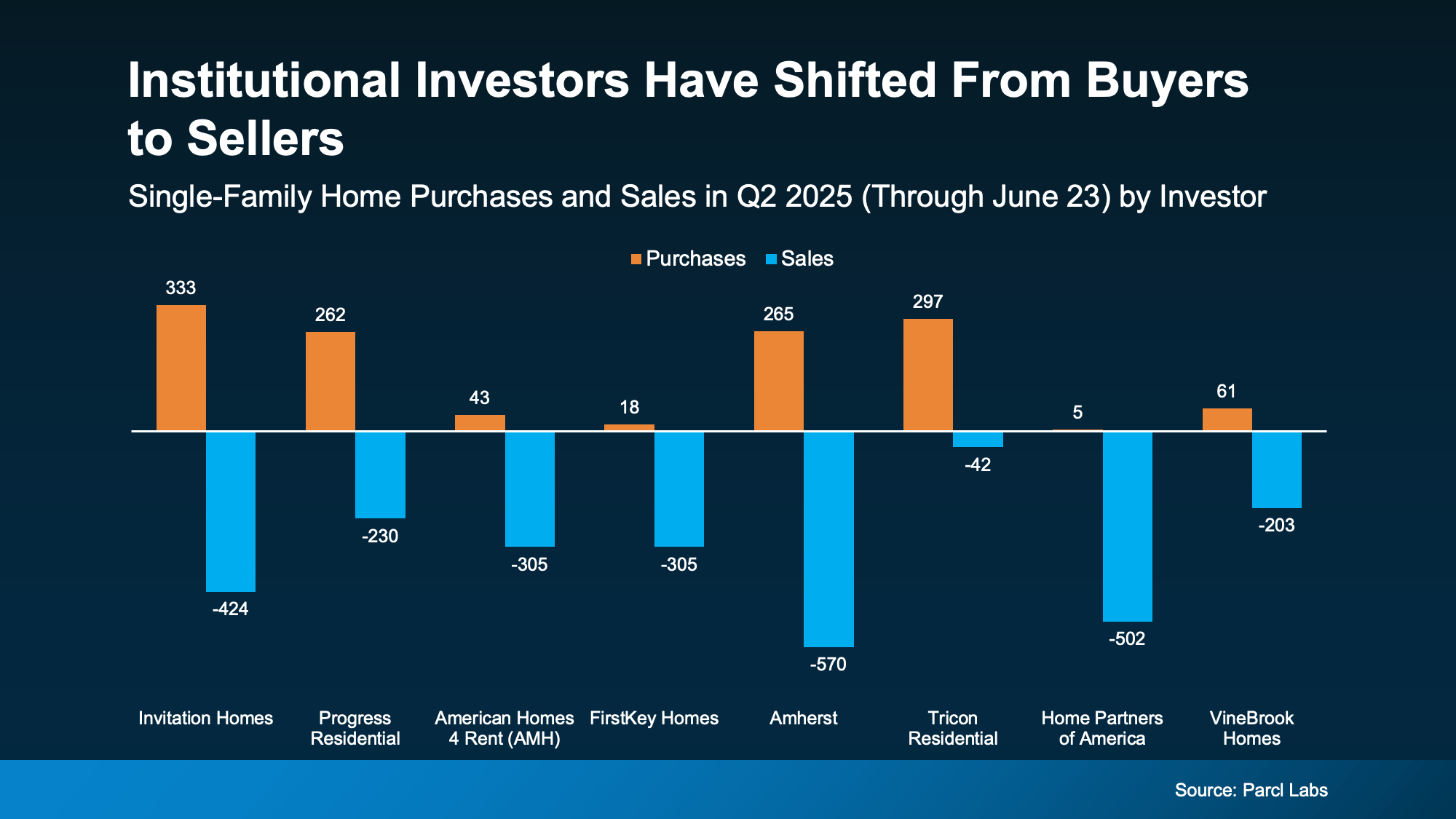

Today, big real estate investors aren’t buying as many homes. In fact, they’re actually selling more than they’re buying.

According to data from Parcl Labs, 6 out of 8 of the largest institutional single-family rental investment companies in America sold more homes than they bought in the second quarter of 2025 (see graph below):

And here’s the stat that really puts it in perspective. According to Dominion Financial, for every home being bought by big investors, about 1.75 are being sold.

What’s Causing Big Investors To Change Course?

The reason institutional investors aren’t buying as many homes now compared to recent years is actually pretty simple. It’s because home values aren’t rising as fast as they were a few years ago, but the costs associated with rental maintenance are.

Since most institutional investors buy homes to rent them out, those higher costs eat into their margins. Remember, to investors, homebuying is a business.

But you’re not buying a home just for this year or next. You’re buying a place to build a life, and that’s a long-term play.

Historically, home values tend to rise over time. So, while investors may be sidelined by what’s happening right now, you’re in a different position entirely. You have the chance to buy while competition is lower and benefit from potential long-term price appreciation – something most investors are choosing not to wait for as they focus on shorter-term returns.

What Does All This Mean for You?

According to a recent survey, about 55% of real estate investors have no plans to grow their rental portfolios now or in the near future. With big investors stepping back, that means less competition from deep-pocketed buyers. And since they’re adding to today’s for-sale inventory, it also creates more options for you.

Bottom Line

If you’ve been holding off on buying, now might be the time to take another look. Connect with a local real estate agent so you can get expert guidance on what’s available and what might be a good fit for you.

What kind of home would you be excited to make yours this year?

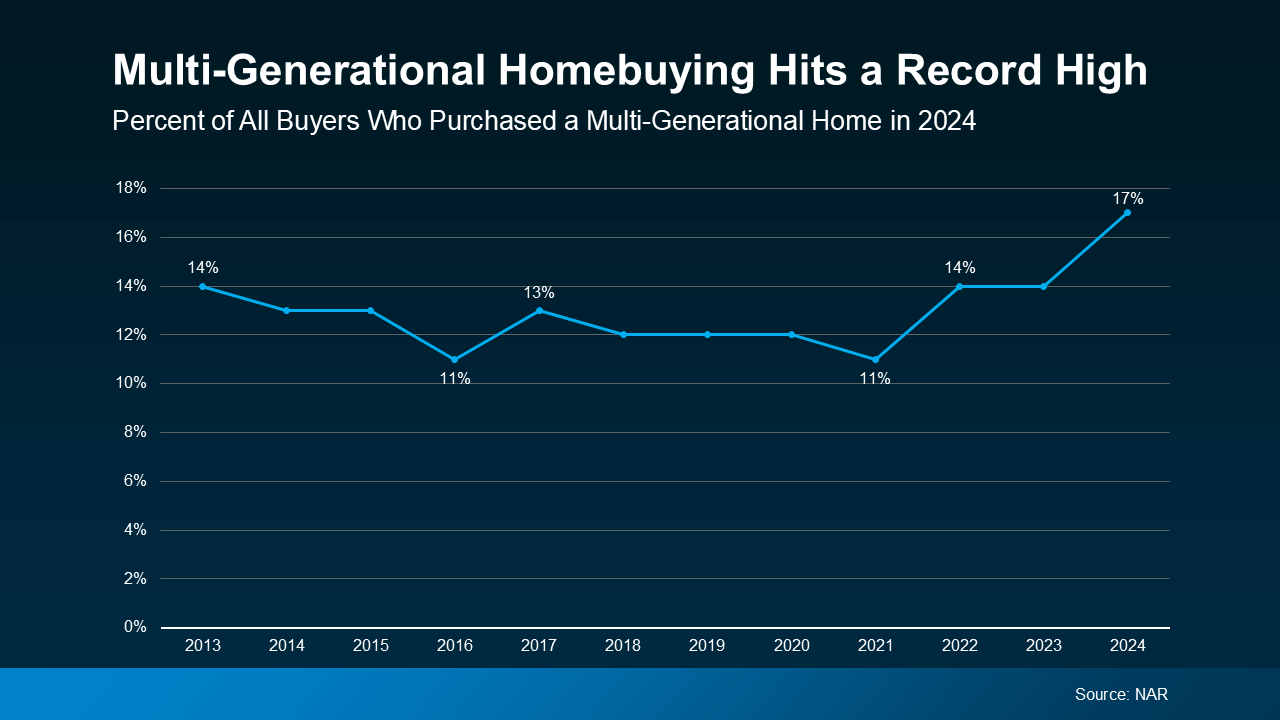

Multi-generational living is on the rise. According to the National Association of Realtors (NAR), 17% of homebuyers purchase a home to share with parents, adult children, or extended family. That’s the highest share ever recorded by NAR (see graph below):

And what’s behind the increase? Affordability. NAR explains:

And what’s behind the increase? Affordability. NAR explains:

“In 2024, a notable 36% of homebuyers cited “cost savings” as the primary reason for purchasing a multigenerational home—a significant increase from just 15% in 2015.”

In the past, caregiving was the leading motivator – especially for those looking to support aging parents. And while that’s still important, affordability is now the #1 motivator. And with current market conditions, that’s not really a surprise.

Pooling Resources Can Help Make Homeownership Possible

With today’s home prices and mortgage rates, it can be hard for people to afford a home on their own. That’s why more families are teaming up and pooling their resources.

By combining incomes and sharing expenses like the mortgage, utility bills, and more, multi-generational living offers a way to overcome financial challenges that might otherwise put homeownership out of reach. As Rick Sharga, Founder and CEO at CJ Patrick Company, explains:

“There are a few ways to improve affordability, at least marginally. . . purchase a property with a family member — there are a growing number of multi-generational households across the country today, and affordability is one of the reasons for this.”

But this strategy doesn’t just help with affordability. It may even allow you to get a larger home than you’d qualify for on your own and that gives everyone a bit more breathing room. As Chris Berk, VP of Mortgage Insights at Veterans United, explains:

“Multigenerational homes are more than a trend: They are a meaningful solution for families looking to care for one another while making the most of their homebuying power.”

And momentum may be growing. Nearly 3 in 10 (28%) of homebuyers say they’re planning to purchase a multi-generational home.

Maybe it’s a solution that would make sense for you too. The best way to find out? Talk to a local real estate agent who can help you decide if this option would work for you.

Bottom Line

If your budget feels tight, buying a multi-generational home could be a smart solution.

Would you ever consider buying a home with a family member? Why or why not?

Connect with an agent to talk through your options.

Fear of a recession is back in the headlines. And if you’re thinking about buying or selling sometime soon, that may leave you wondering if you should reconsider the timing of your move.

A recent survey by John Burns Research and Consulting (JBREC) and Keeping Current Matters (KCM) shows 68% of people are delaying plans to buy or sell due to economic uncertainty.

But it may not be for the reason you think. Not everyone is holding off because they’re worried. Some buyers are waiting because they’re hopeful. According to Realtor.com:

“In 2025Q1, 3 in 10 (29.8% of) surveyed homebuyers said a recession would make them at least somewhat more likely to purchase a home . . . This reflects a common dynamic where some buyers see a downturn as an opportunity. If the economy enters a recession, the Federal Reserve may respond by lowering interest rates to stimulate activity, potentially putting downward pressure on mortgage rates and easing affordability concerns. As a result, buyers—especially those with limited down payments—might view a recession as a more favorable time to enter the market.”

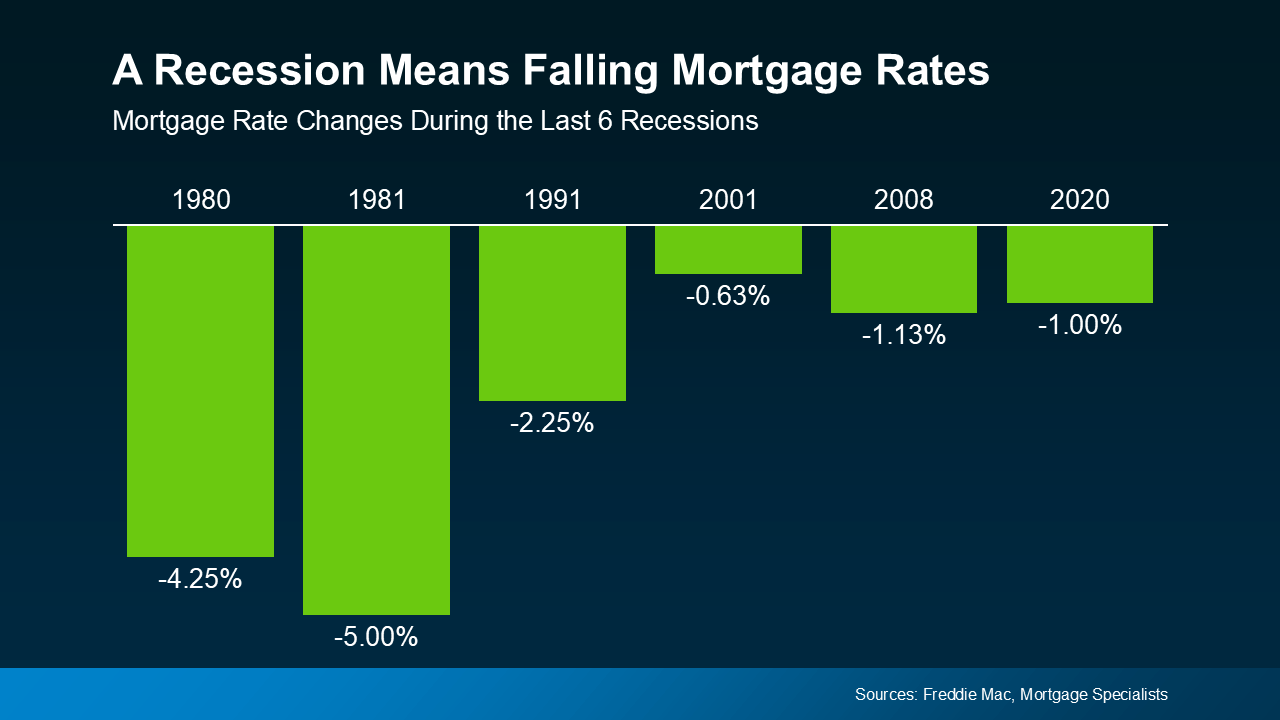

And there’s some truth to the idea that a recession could bring about lower mortgage rates. History shows mortgage rates usually drop during economic slowdowns. That’s not guaranteed – but it is a common pattern. Looking at data from the last six recessions, you can see mortgage rates fell each time (see graph below):

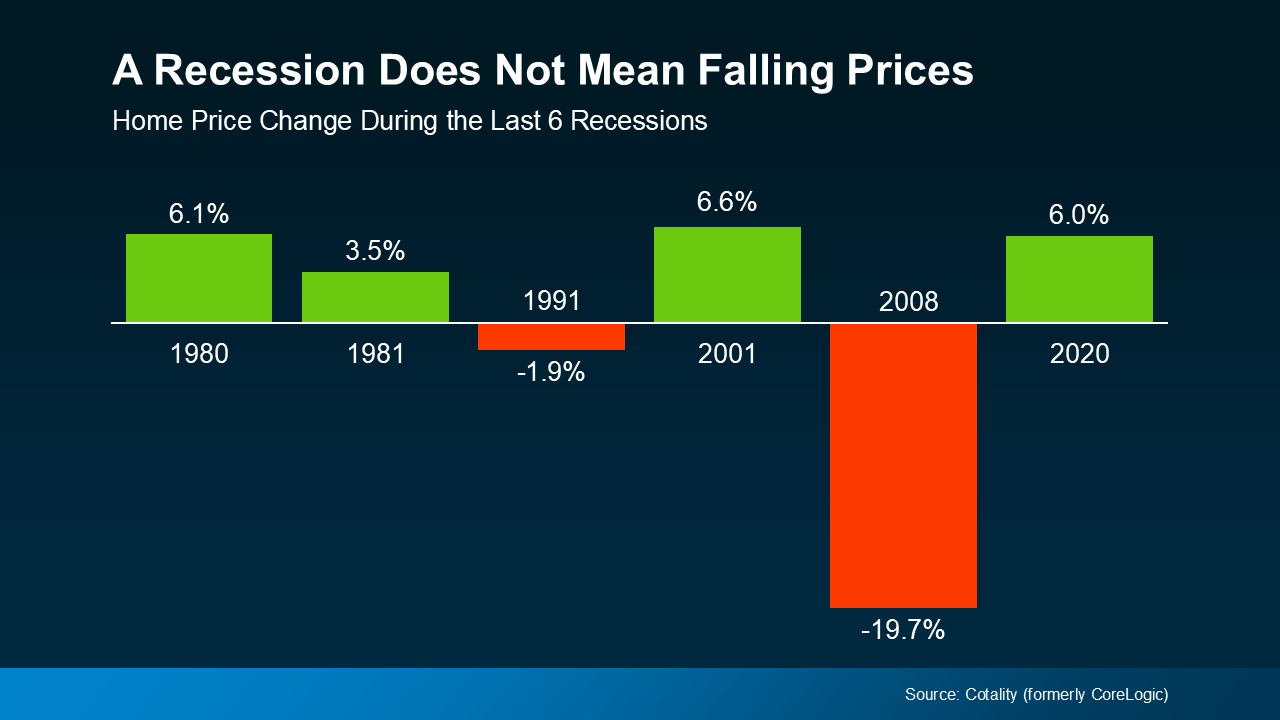

But here’s what those buyers may not be considering. Many of those hopeful buyers are assuming something else will happen too – that home prices will drop. And that’s where history tells a different story.

But here’s what those buyers may not be considering. Many of those hopeful buyers are assuming something else will happen too – that home prices will drop. And that’s where history tells a different story.

According to data from Cotality (formerly CoreLogic), home prices went up in four of the last six recessions (see graph below)

So, while many people think that if a recession hits, home prices will fall like they did in 2008, that was an exception, not the rule. It was the only time the market saw such a steep drop in prices. And it hasn’t happened since, mainly because there’s still a long-standing inventory deficit, even as the number of homes on the market is rising.

So, while many people think that if a recession hits, home prices will fall like they did in 2008, that was an exception, not the rule. It was the only time the market saw such a steep drop in prices. And it hasn’t happened since, mainly because there’s still a long-standing inventory deficit, even as the number of homes on the market is rising.

Since prices tend to stay on whatever path they’re already on, know this: prices are still holding steady or rising in most metros, although at a much slower pace. So, a big drop isn’t likely. As Robert Frick, Corporate Economist with Navy Federal Credit Union, explains:

“Hopes that an economic slowdown will depress housing prices are wishful thinking at this point . . .”

Bottom Line

If you’ve been waiting for a recession to make your move, it’s important to understand what really happens during one – and what likely won’t. Lower mortgage rates could be on the table. But lower home prices? That’s far less likely.

Don’t wait for a market that may never come. If you’re thinking about buying or selling, connect with an agent to talk through what today’s economy really means for you – and make a smart plan that works in your favor, regardless of what the headlines say.

Think No One’s Buying Homes Right Now? Think Again.

Why Big Investors Aren’t a Challenge for Today’s Homebuyer

Top 5 Reasons To Hire a Real Estate Agent When You Sell

-

Infographics2 weeks ago

Infographics2 weeks agoWhy Your Home’s Asking Price Matters More Today

-

Infographics4 weeks ago

Infographics4 weeks agoThe Big Difference Between a Homeowner’s and a Renter’s Net Worth

-

Affordability4 weeks ago

Affordability4 weeks agoBuying Your First Home? FHA Loans Can Help

-

Agent Value3 weeks ago

Agent Value3 weeks agoYour House Didn’t Sell. Here’s What To Do Now.

-

For Buyers4 weeks ago

For Buyers4 weeks agoIs Inventory Getting Back To Normal?

-

First-Time Buyers4 weeks ago

First-Time Buyers4 weeks agoThe Five-Year Rule for Home Price Perspective

-

Downsize3 weeks ago

Downsize3 weeks agoYou May Have Enough Equity To Downsize and Buy Your Next House in Cash

-

For Sellers3 weeks ago

For Sellers3 weeks agoWhy More Sellers Are Choosing To Move, Even with Today’s Rates

You must be logged in to post a comment Login