Rent vs. Buy

The Perks of Buying over Renting

Thinking about buying a home? While today’s mortgage rates might seem a bit intimidating, here are two solid reasons why, if you’re ready and able, it could still be a smart move to get your own place.

1. Home Values Typically Go Up Over Time

There’s been some confusion over the past year or so about which way home prices are headed. Make no mistake, nationally they’re still going up. In fact, over the long-term, home prices almost always go up (see graph below):

Using data from the Federal Reserve (the Fed), you can see the overall trend is home prices have climbed steadily for the past 60 years. There was an exception during the 2008 housing crash when prices didn’t follow the normal pattern, but generally, home values kept rising.

This is a big reason why buying a home can be better than renting. As prices go up and you pay down your mortgage, you build equity. Over time, this growing equity can really increase your net worth. The Urban Institute says:

“Homeownership is critical for wealth building and financial stability.”

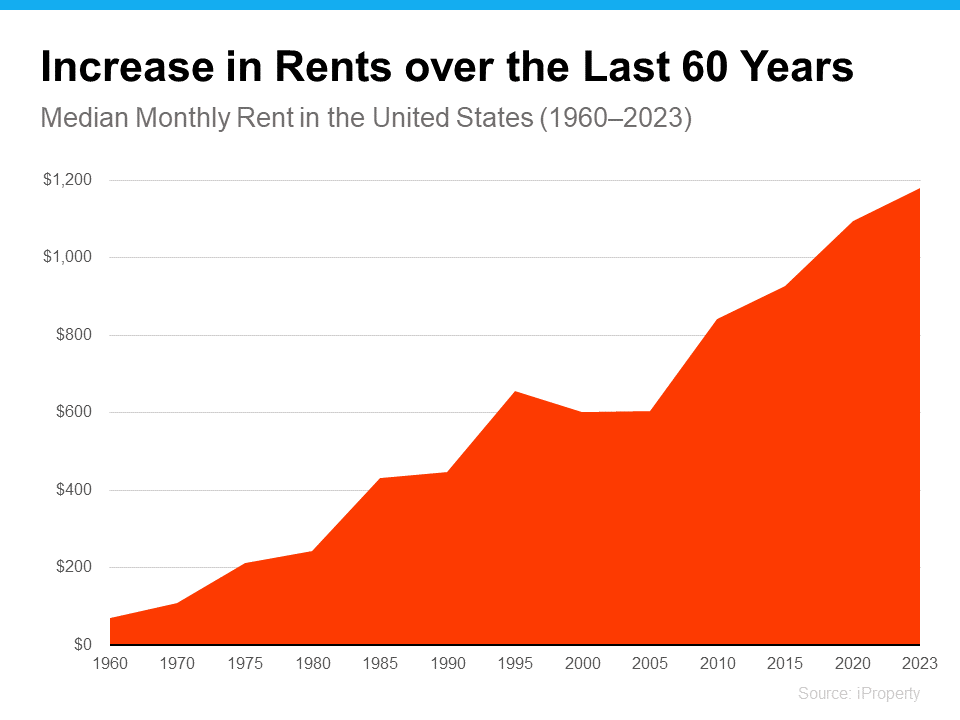

2. Rent Keeps Rising in the Long Run

Here’s another reason you may want to think about buying a home instead of renting – rent just keeps going up over the years. Sure, it might be cheaper to rent right now in some areas, but every time you renew your lease or sign a new one, you’re likely to feel the squeeze of your rent getting higher. According to data from iProperty Management, rent has been going up pretty consistently for the last 60 years, too (see graph below):

So how do you escape the cycle of rising rents? Buying a home with a fixed-rate mortgage helps you stabilize your housing costs and say goodbye to those annoying rent increases. That kind of stability is a big deal.

Your housing payments are like an investment, and you’ve got a decision to make. Do you want to invest in yourself or keep paying your landlord?

When you own your home, you’re investing in your own future. And even when renting is cheaper, that money you pay every month is gone for good.

As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), says:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Bottom Line

If you’re tired of your rent going up and want to explore the many benefits of homeownership, talk to a local real estate agent to explore your options.

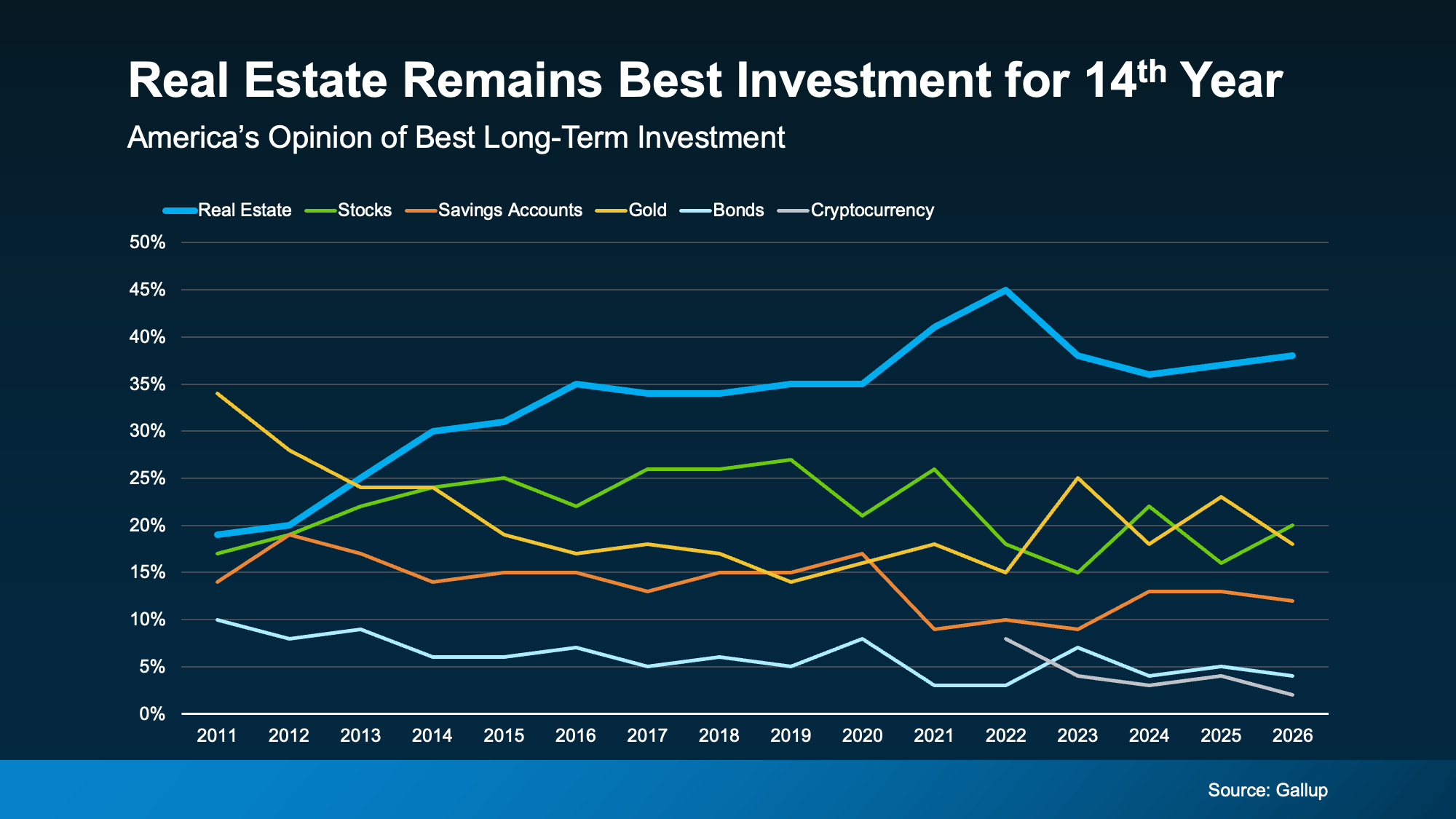

Quick gut reaction. Which investment do Americans trust more than stocks, gold, savings accounts, and bonds? The answer hasn’t changed in 14 years.

It’s real estate. And this year, that answer comes with even more conviction behind it. New data shows people aren’t just saying homeownership is a smart move, they’re feeling better about it than they have in years. Let’s dig into why.

Real Estate Takes the Top Spot – Again

Every year, Gallup asks Americans to name the best long-term investment. And for the 14th year in a row, real estate came out on top (see graph below):

That’s not a fluke or a hot streak. That’s 14 straight years of beating out stocks, gold, and everything else.

Think about everything that’s happened in that stretch – rising rates, market swings, election years, you name it. Through all of it, Americans kept picking real estate. That kind of staying power says something about how people view homeownership – and it makes sense. Historically, it’s one of the best ways to build wealth in this country.

As Michelle Egan, Head of Credit Solutions, Impact Finance at JPMorgan Chase, explains:

“Owning a home has long been considered one of the most reliable ways to build wealth. Beyond providing shelter, a home is a valuable asset that can appreciate over time, build equity, and serve as a financial resource for generations.”

Now, you may have seen chatter online saying home prices are falling and wondered if that changes the math. It really shouldn’t. Nationally, home prices are still rising – just at a slower pace than a few years ago.

Yes, some local markets are seeing slight dips, but those dips are small compared to how much home values have grown over the past 5 years. Generally speaking, home prices almost always rise. As long as you plan to live there for a good length of time, you should still have the chance to build equity.

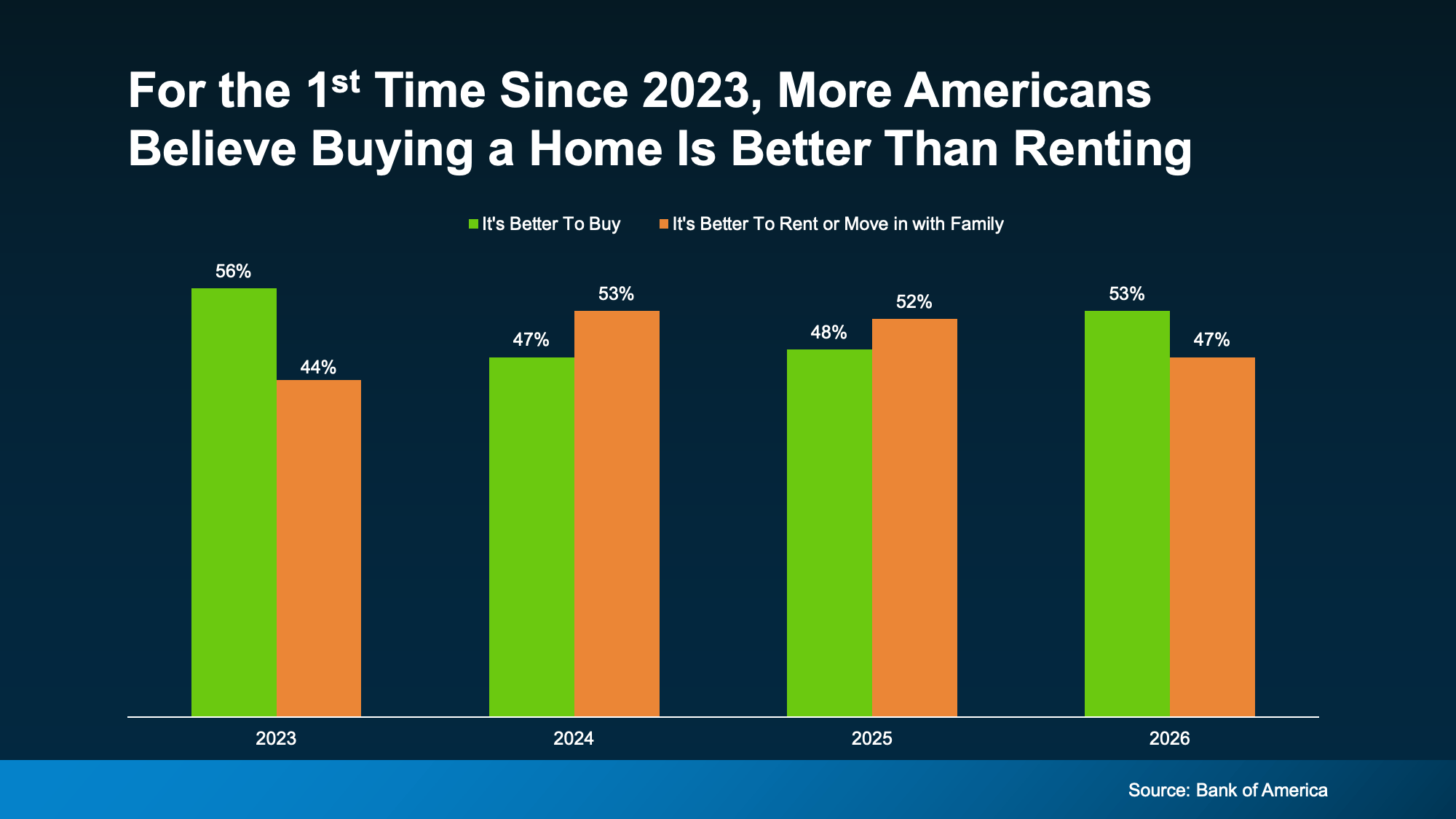

More People Say Buying Beats Renting

And while it’s true homeownership has been seen as a worthwhile pursuit for years now, something interesting is happening. It may actually be gaining a bit more popularity again.

According to Bank of America‘s latest Homebuyer Insights Report, 53% of people now say it’s better to buy a home than to rent or move in with family. That’s the first time buying has taken the lead since 2023 (see graph below):

In that same report, here are a few other signals that confidence in homeownership is on the rise:

-

90% of people say a home is a valuable investment, up from 79% just last year.

-

And 94% say owning a home provides stability, up from 83% the year prior.

Those are relatively big jumps in a short amount of time. And here’s what may be driving it.

It’s About More Than Money

Sure, affordability is still tight and some markets are still hard to break into, but that hasn’t changed what people feel about homeownership as a goal. And the reason why is simple – it’s not just a financial decision. It’s a lifestyle choice.

A home pays you back in ways stocks never could. As Sheharyar Bokhari, Principal Economist at Redfin, says:

“For many homeowners, a home is more than a place to sleep and store belongings—it’s a reflection of who they are. Homeownership can help people put down roots, build relationships and create a space that feels uniquely their own.”

You can’t get that from a brokerage account. A home is the one investment that grows your wealth and gives you a place to build your life. And that means something.

Bottom Line

For 14 years straight, Americans have called real estate the best long-term investment, and confidence in owning a home is on the rise. If you’ve been weighing whether buying is worth it, connect with a local real estate agent and talk through what that first step could look like for you.

It’s one of the biggest hold ups some buyers have right now: “What if I buy, and home prices go down?”

With everything in the news, that concern makes some sense. No one wants to make a big financial decision at the wrong time. But here’s what’s important to know. You don’t want to get hung up on the few places seeing slight declines right now.

When you zoom out and look at the full picture, home prices usually rise over time.

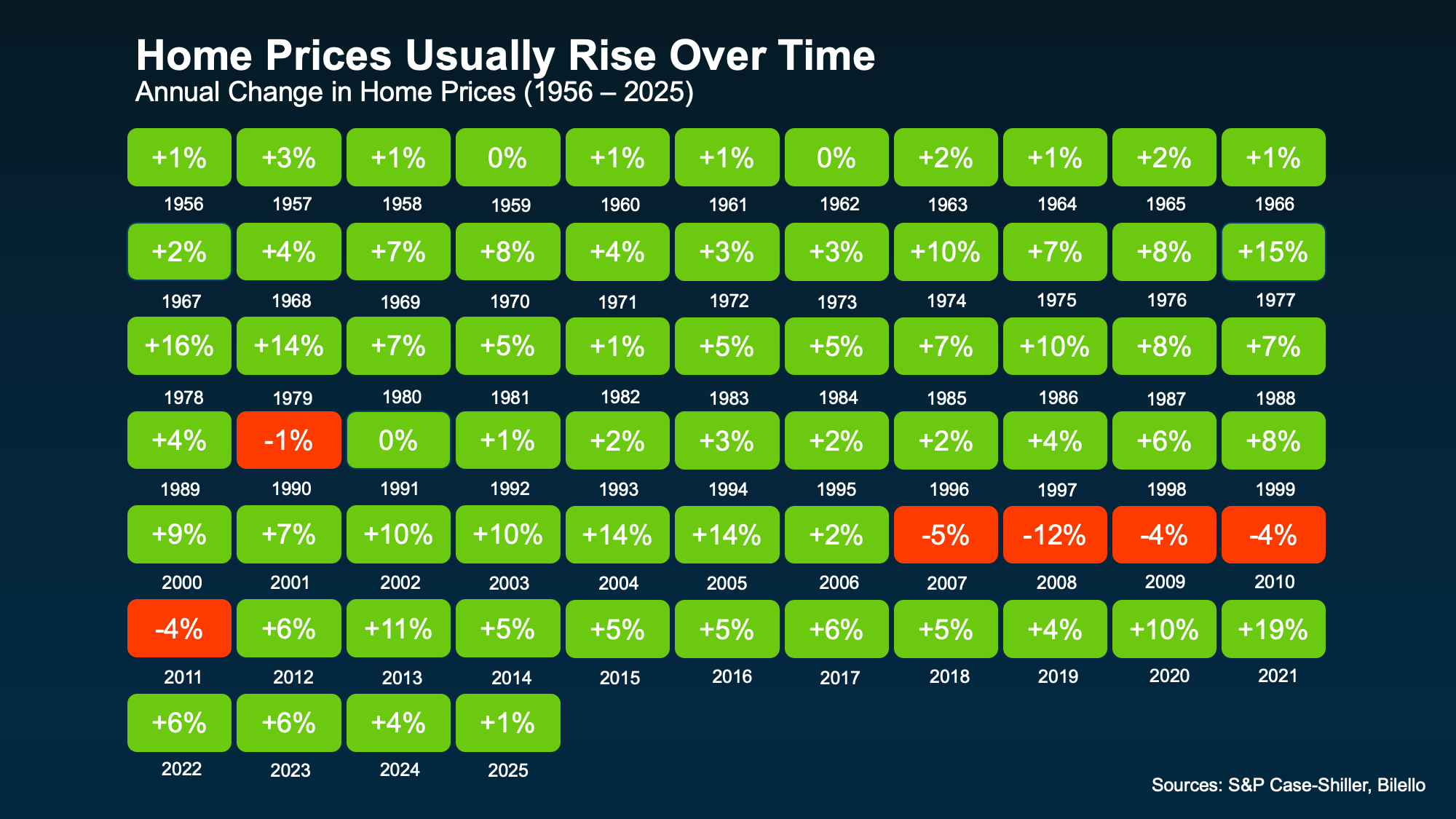

What the Data Really Shows

Take a look at the visual below. It uses data from Case-Shiller and Bilello to show how home prices have changed year by year going all the way back to the 1950s.

Here’s the key takeaway.

Outside of the housing crash, home prices have either held steady or increased in just about every year for decades (see visual below):

That’s a remarkably consistent track record. And it shows something a lot of headlines miss.

That’s a remarkably consistent track record. And it shows something a lot of headlines miss.

While short-term shifts can happen, it’s the long-term gains that really matter.

Why Prices Tend To Rise Over Time

There are a few core reasons prices usually go up each year:

- There are always people who need to move. People need a place to live, and that demand will never fully go away. It may ebb and flow, but someone will always have to move as big changes happen in their life. So, homes stay in demand.

- There still aren’t enough homes for sale. While the number of homes for sale has grown, nationally there’s still an undersupply based on how many people want a home. That keeps upward pressure on prices.

- Inflation has an impact. Over time, the cost of goods (including homes) naturally increases. That pushes home values higher.

What That Means for You as a Buyer

It’s easy to get caught up in what might happen with home prices next month or next year, especially if you’re a first-time buyer and you’re feeling a little anxious about making such a big financial commitment. But the big picture is clear. Prices usually rise.

That doesn’t mean prices will go up every single year in every market. Real estate is local, and there can be short-term ups and downs. We’re seeing that in some places right now. You can even see it in the few annual dips in the visual above.

But historically, the declines have been temporary.

That’s why it’s generally recommended to buy a home only if you plan to stay for a while – typically at least five years. That’s normally enough time to see your house grow in value. And, it’s enough so you can ride out any short-term changes in the market.

Because when you can do that, something powerful happens. Those rising home values grow your net worth, and by extension, help you build wealth.

The right decision isn’t about timing the market perfectly. It’s about making a move that works for your life and staying in it long enough to benefit from the bigger trend.

Bottom Line

Home prices have a long track record of going up over time. And that’s why buying a home is generally considered a safe long-term investment.

That certainly doesn’t mean you have to buy now. You should only move when it makes sense, and you plan to live there for a while.

But if you’re interested, let this reassure you. If you want to talk about what home prices are doing in our market, your goals, or your timelines, reach out to a local agent.

You’ve probably asked yourself lately: Is it even worth trying to buy a home right now? It’s a question a lot of people are asking.

With today’s home prices and mortgage rates, renting can feel like the easier path. In some cases, it might even seem like the only realistic option right now. And if that’s where you are, there’s nothing wrong with that.

But if you’re weighing the decision, there’s one part of the conversation that doesn’t get talked about enough.

It’s what each choice does for your future.

What Renting Really Gets You (And What It Doesn’t)

Depending on your situation, renting does have some advantages:

- Lower upfront costs.

- Less responsibility.

- More flexibility to move when you want.

But even with those benefits, a Bank of America survey found 70% of aspiring homeowners worry about what long-term renting means for their future. And that concern comes down to one thing: you’re not building anything for your future. As Yahoo Finance explains:

“Paying rent doesn’t build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

So, while renting may feel easier, the flexibility you get comes at a cost.

How Homeownership Builds Your Wealth Over Time

On the other hand, owning a home is one of the most consistent ways people build wealth over time. Why? When you’re a homeowner, you gain something called equity. That’s the difference between what your home is worth and what you owe.

That equity grows with every monthly payment you make. It also gets a boost as home values go up through the years – and it adds up quicker than you may think.

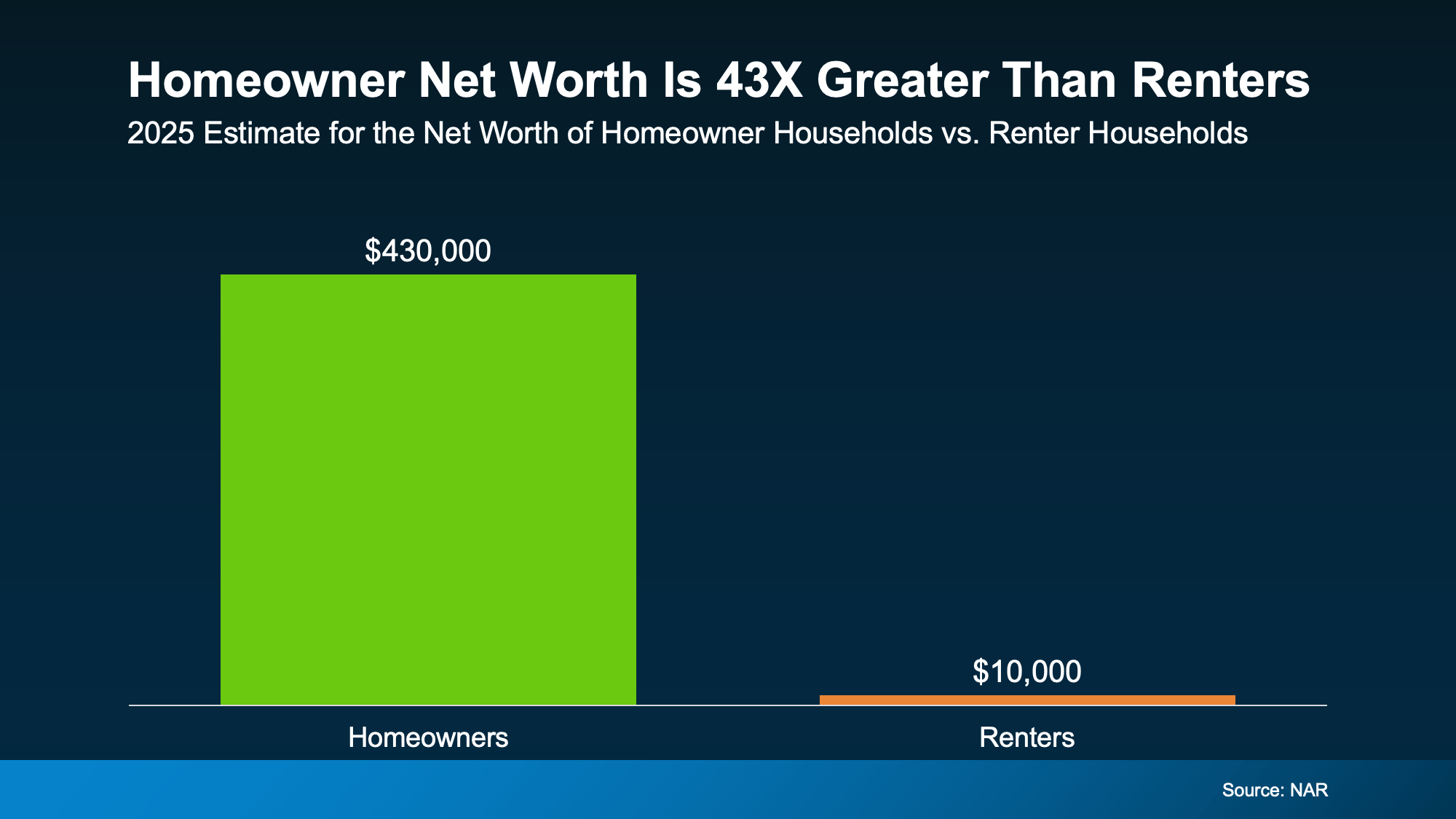

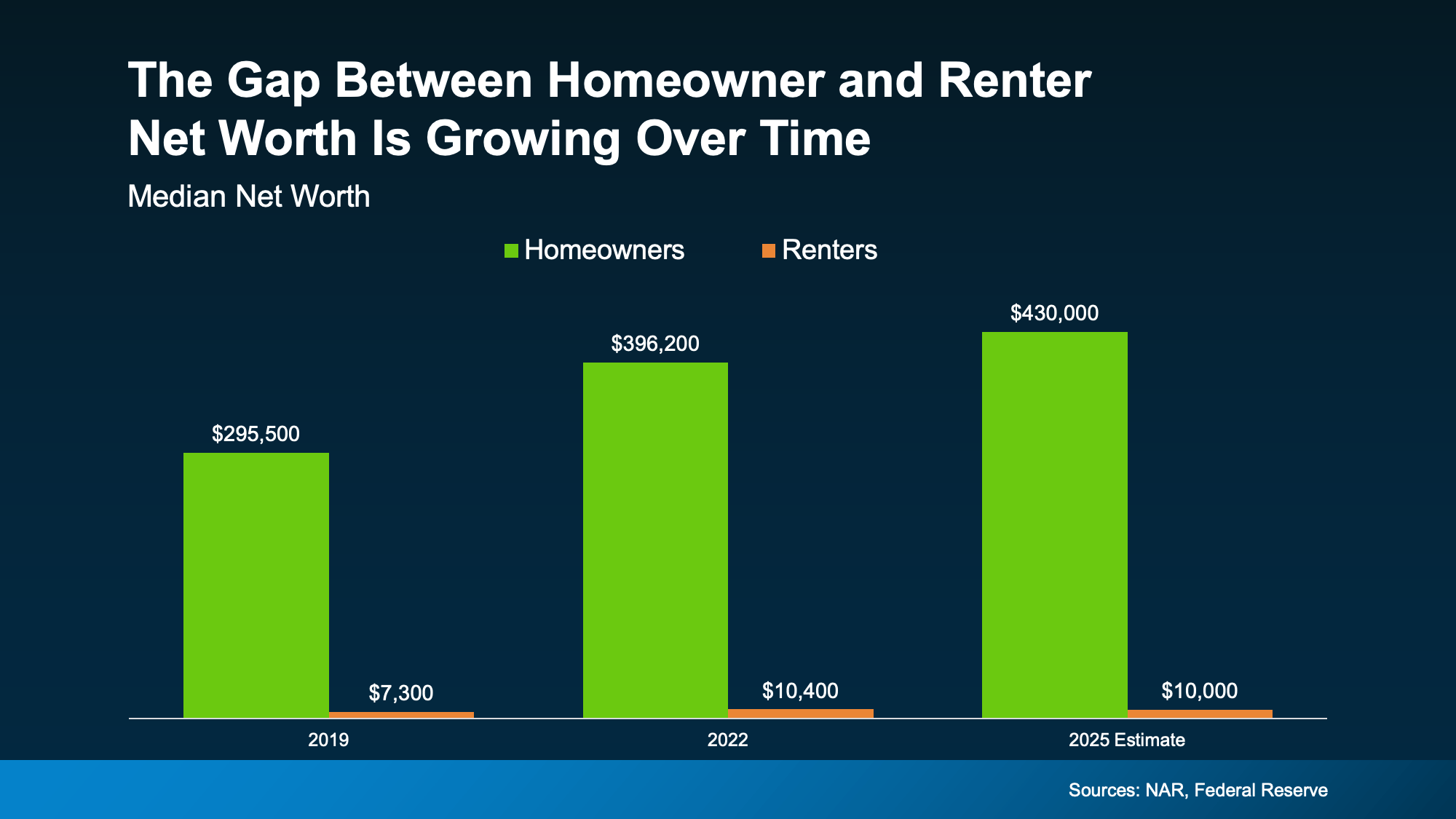

Today, the National Association of Realtors (NAR) says the average homeowner’s net worth is 43X greater than that of a renter:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

- Homeowners: $430k

- Renters: $10k

And it’s not because homeowners make wildly different decisions day to day. It’s because over time, one path builds something, and the other doesn’t.

So sure, buying comes with some upfront costs and more responsibility. But it’s basically a savings account you can live in.

The Gap Is Growing Over Time

And here’s something else interesting. That net worth gap between renters and homeowners has been widening over time, not shrinking.

If you look back at the reports on net worth through the years, you can see the gap is growing as homeowners gain wealth and renters stay stuck in the rental trap (see graph below):

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

When you can afford it and you’re ready for the responsibility, history shows buying is usually worth it in the long run. Because either way, you’re paying for someone’s mortgage and building someone’s net worth.

When you rent, it’s your landlord’s mortgage – not yours. But when you buy? Your monthly payments help build equity.

The question is: whose do you want to pay? Yours or theirs?

So, Should You Buy a Home Now?

The short answer is, it depends on your situation.

While the long-term benefits of buying are clear, that doesn’t mean the timing is right for everyone right now. And that’s okay. You should only buy a home once you’re ready and the numbers work for you.

But whether you’re looking to buy now or planning for the future, the first step is the same. You should have a quick conversation with a local real estate agent about your goals, timeline, and budget.

They can help you run the numbers and see what’s realistic. You may find buying is closer than you thought. And if not, you’ll at least know exactly what it will take to get there.

Because the sooner you have a plan, the sooner you can decide when it makes sense, instead of wondering if it ever will.

Bottom Line

Renting may feel more do-able today. But over time, it could cost you.

If you want to ditch renting and start building something for your future, it starts with a simple conversation. Connect with a real estate agent to talk about your specific goals, and explore your options – so you’re ready when the time is right for you.

Buying a Home? Here’s What You Should Know About Home Insurance Costs.

Home Price Growth Slowed Down. That May Be Changing.

Selling a Luxury House? Here’s Why Now Is a Good Time

-

Equity4 weeks ago

Equity4 weeks agoThe Housing Market Is Stronger Than You Think

-

Economy3 weeks ago

Economy3 weeks agoWhat Buying or Selling a Home Gives Back to Your Community

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoStudent Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

-

Affordability4 weeks ago

Affordability4 weeks agoDown Payments Are Smaller Than They’ve Been Since 2021

-

Affordability3 weeks ago

Affordability3 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

-

For Sellers2 weeks ago

For Sellers2 weeks agoThink Nobody’s Buying Homes Right Now? Think Again.

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

-

First-Time Buyers2 weeks ago

First-Time Buyers2 weeks ago14 Years Running: Why Real Estate Is Still America’s Favorite Investment

You must be logged in to post a comment Login