First-Time Buyers

Tips for Younger Homebuyers: How To Make Your Dream a Reality

Whether you’re dreaming about buying your first home or wondering if it’s time to move on from the one you’re in, affordability is probably weighing on your mind. Home prices are still high in many markets, and even though things have improved a bit over the past year, making the numbers work can still feel like a stretch.

But the people finding ways to move right now usually have one thing in common. They didn’t wait for affordability to come to them. They went looking for it.

According to PODS, 61% of people across all generations say affordability is the biggest factor when deciding where to move. And it’s led a growing number of people to do one thing – broaden their search to include more affordable areas they hadn’t seriously considered before. As PODS, put it:

“. . . moving is increasingly driven by affordability, connection, and quality of life. As economic pressures persist, Americans are taking a more intentional, values-driven approach to where they choose to live.”

It’s Not Just the Home Price – It’s the Whole Cost of Living

Here’s where it gets really interesting. When people talk about moving for affordability, they’re not just talking about finding a cheaper house. They’re thinking about the full picture. What does it actually cost to live somewhere?

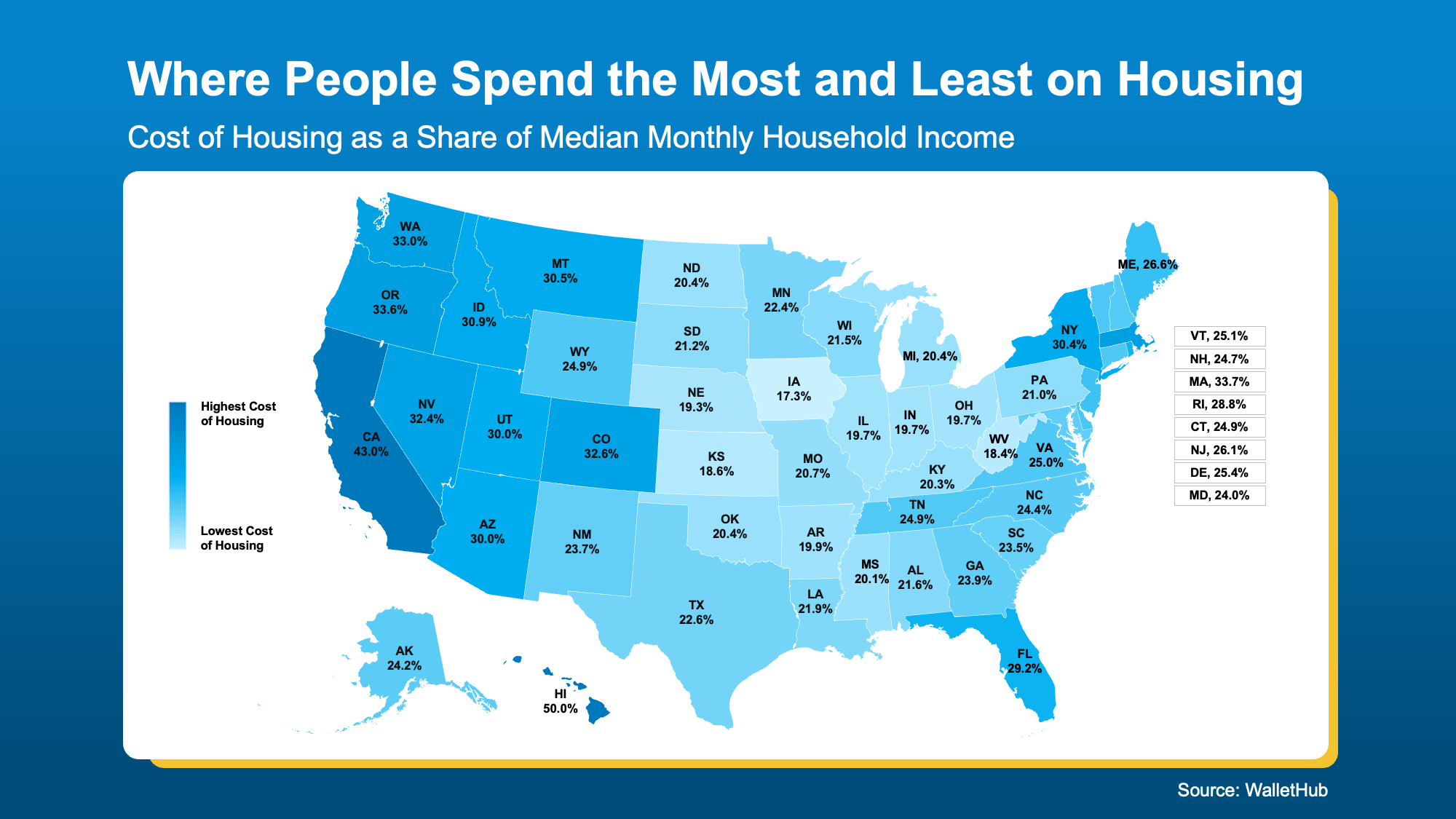

WalletHub looked at exactly this, measuring housing costs as a share of median monthly household income across every state (see map below).

Take a look at where you live on that map. The lighter the blue, the more affordable it generally is to live there. The darker the blue? Just the opposite.

If your state is showing up on the darker blue end of the scale, the cost of living may be putting a real pinch on your wallet, and it may be worth exploring what a lighter-blue area could mean for your finances.

Because if you’re less financially stretched, imagine how that could change things. Less stress. Less worry. More freedom and peace of mind.

You Don’t Have To Move to Another State To Find a Better Deal

But finding more affordable homeownership doesn’t have to mean a cross-country move. It doesn’t even have to mean leaving your state, your family, or your favorite coffee shop behind.

Every market has more affordable pockets that most buyers never think to explore – neighborhoods, towns, and communities where home prices are lower, property taxes are more manageable, and the overall cost of living just works better.

A great local real estate agent knows exactly where those places are.

And if you work remotely, or have any flexibility in where you’re based, your options open up even further. Remote work has already changed the way millions of people think about where to live, and that trend isn’t going away.

When location stops being tied to a daily commute, a more affordable area that’s a bit farther out suddenly becomes a very real option.

Bottom Line

Affordability is a real challenge, but it’s not an unsolvable one. The key is being open to places you might not have considered before. A local real estate agent can help you find them.

Ready to find out which areas have the best affordability right now? Reach out today.

You started shopping with a specific mental image of your future home in your mind. Then the houses in your budget came in smaller than you pictured.

That’s the reality for a lot of buyers right now. Affordability is tight.

But don’t let that discourage you. Going smaller might actually be a smart play in today’s market – and the upside can be bigger than you’d think. Let’s break down two places to look where smaller won’t necessarily feel like a compromise.

Homebuilders Are Focused on Smaller Options Lately

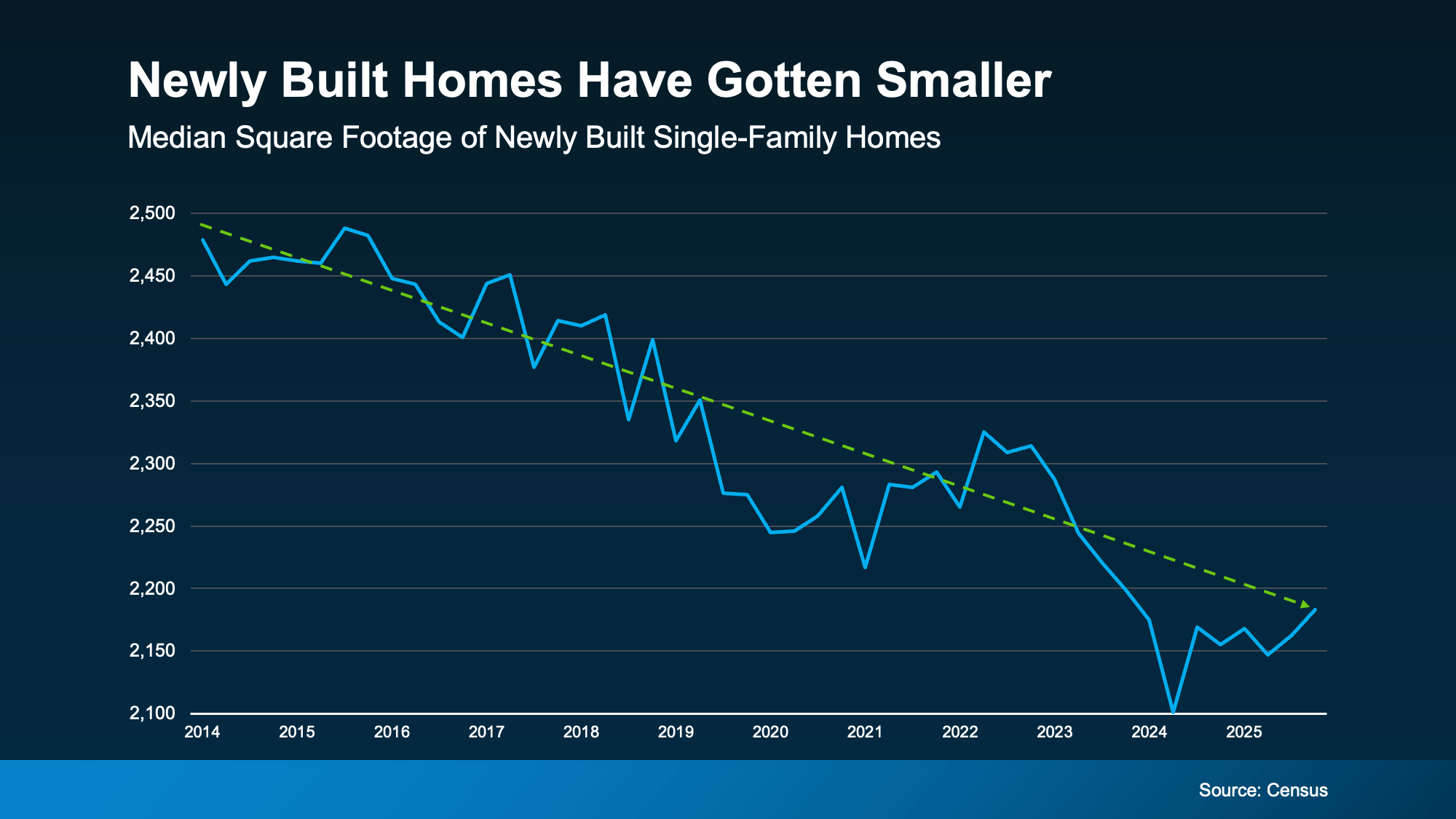

For starters, smaller is kind of on trend right now. Newly built homes have been shrinking for years. According to the latest data from the Census, the median square footage of new single-family homes has been falling overall since 2014 (see graph below):

Why? Builders focus on the types of homes consumers want the most. After all, they want to build what will actually sell. And for the past decade, buyers seem to agree less is more.

Especially right now, when affordability is a key concern, they’re building homes with smaller square footage than a decade ago. And that’s good because that may be more within budget for many buyers. It’s part of why new home prices recently hit a 5-year low.

So, if you’re not getting excited about any of the existing options at your price point, it may be time to check out what builders are doing in your area.

You may find brand-new options you really love with all the latest and greatest features. And if you’ve got modern appliances and design, maybe slightly less square footage doesn’t feel like that much of a compromise anymore, especially if the house is move-in ready.

Condos Are Opening Up Another Path

Just in case you don’t have a ton of new builds in your area, another avenue worth exploring is condominiums or condos.

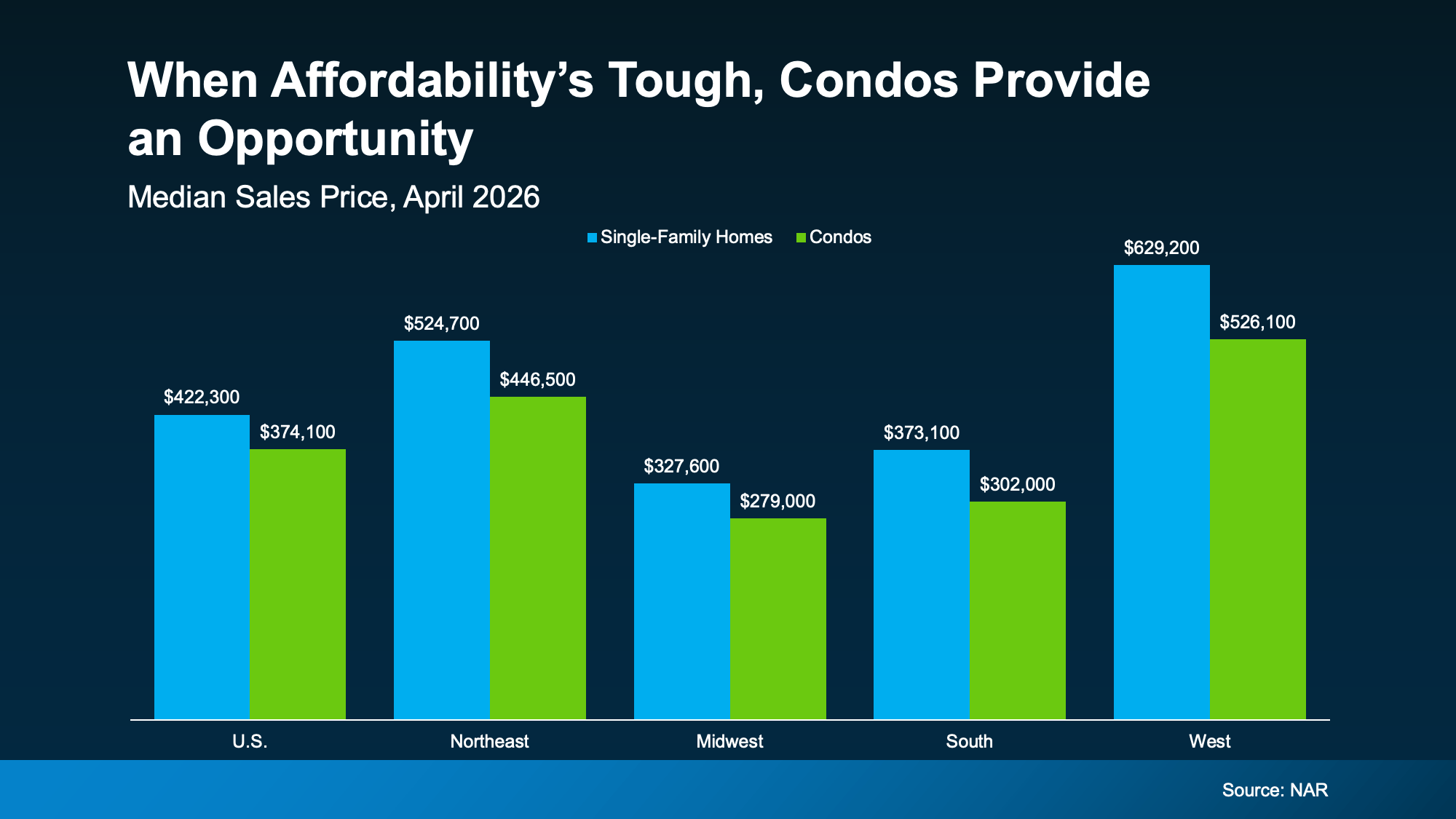

For buyers crunching numbers to make the math work, condos can take real pressure off the budget. According to the National Association of Realtors (NAR), the median price for condos is less than the median for single-family homes in every region (see graph below):

Part of that is because condos are typically smaller. And smaller square footage can come with a smaller price tag too. That’s a selling point to affordability-strapped buyers right now – and it’s one of the reasons we’re seeing a bump in condo sales.

The number of condos sold rose 2.7% from just a month ago. It’s also up year over year, according to NAR. Ali Wolf, Chief Economist for New Home Source, explains why more buyers are going this route:

“In addition to favoring smaller floor plans, more consumers are showing a willingness to live in an attached home. This shift is not driven by a preference for shared walls, but by a pursuit of value.”

The Community Does Some of the Heavy Lifting

Here’s why smaller may still work for you. Whether it’s a condo complex or a neighborhood of detached single-family homes, the right community can give you back in amenities what you trade in square footage.

Many developments are designed so the home is just one piece of where you actually spend your time. Master-planned communities often include walking trails, pools, fitness centers, co-working spaces, and outdoor gathering areas – the kind of features that pick up where your floor plan leaves off.

No room for a dedicated office? The co-working space might be just a five-minute walk away. Want a place to work out? It’s already built in with the shared gym. And features like that can make opting for a smaller footprint feel less like a compromise – and more like a big lifestyle upgrade.

Bottom Line

Today’s smaller single-family homes and condos have more going for them than the square footage suggests. They can give your budget some breathing room and put you in a community designed with lifestyle in mind.

Curious about the options in your area? Connect with a local real estate agent to walk through what’s available.

If you’ve always assumed a newly built home is just not in your budget, you should know the math just got a little friendlier.

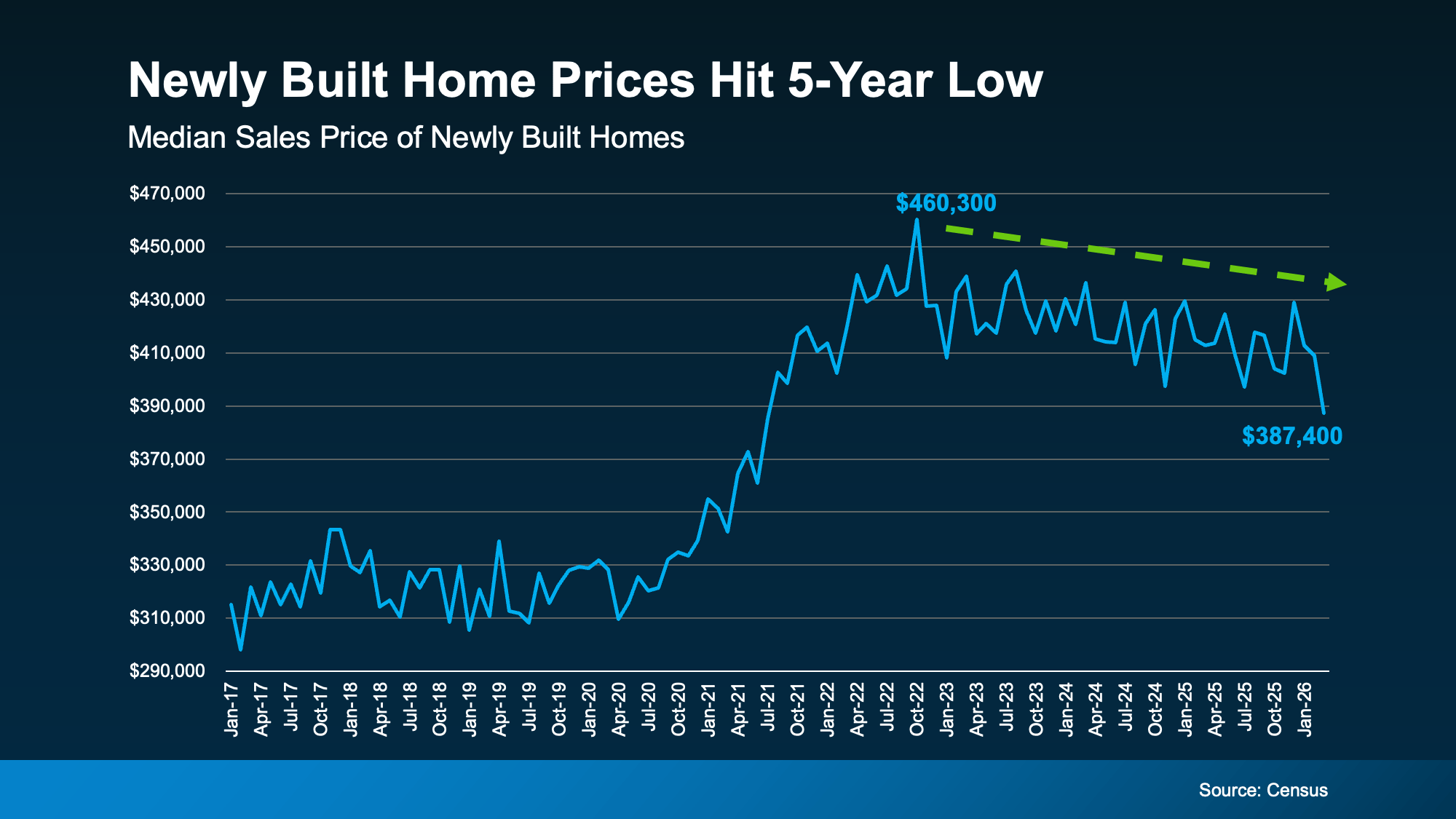

The median sale price of a newly built home is now at its lowest level since 2021, according to the latest data from the Census. And on top of that, builders are still rolling out incentives to bring buyers through the door.

Here’s what’s happening, and what it means if you’re shopping right now.

Prices on Newly Built Homes Have Come Down

After a steep climb during the pandemic years, prices have eased a bit. The median sale price of newly built homes is sitting at about $390,000. That’s the lowest it’s been in nearly five years (see graph below):

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

While local markets vary, the national trend is moving in your favor, especially if you’re a first-time buyer. According to Zonda, prices in the entry-level price range have dropped roughly 2.7% over the past 12 months – more than any other price tier.

That doesn’t mean every home in every market is suddenly affordable. But it does mean that, broadly, you’ll see the best prices on new builds since 2021, if you’re buying now.

Why This Isn’t a Repeat of 2008

And just in case you’re thinking it, lower prices don’t mean the new home market is in trouble. Builders today are being intentional about how much inventory they have, so it doesn’t pile up the way it did in 2008.

If you look back up at the graph, you’ll see that even after the recent improvement in new home prices, they’re still higher than pre-pandemic norms. So, this isn’t a crash. It’s a builder strategy to keep inventory moving.

Homebuilders Are Still Sweetening the Deal

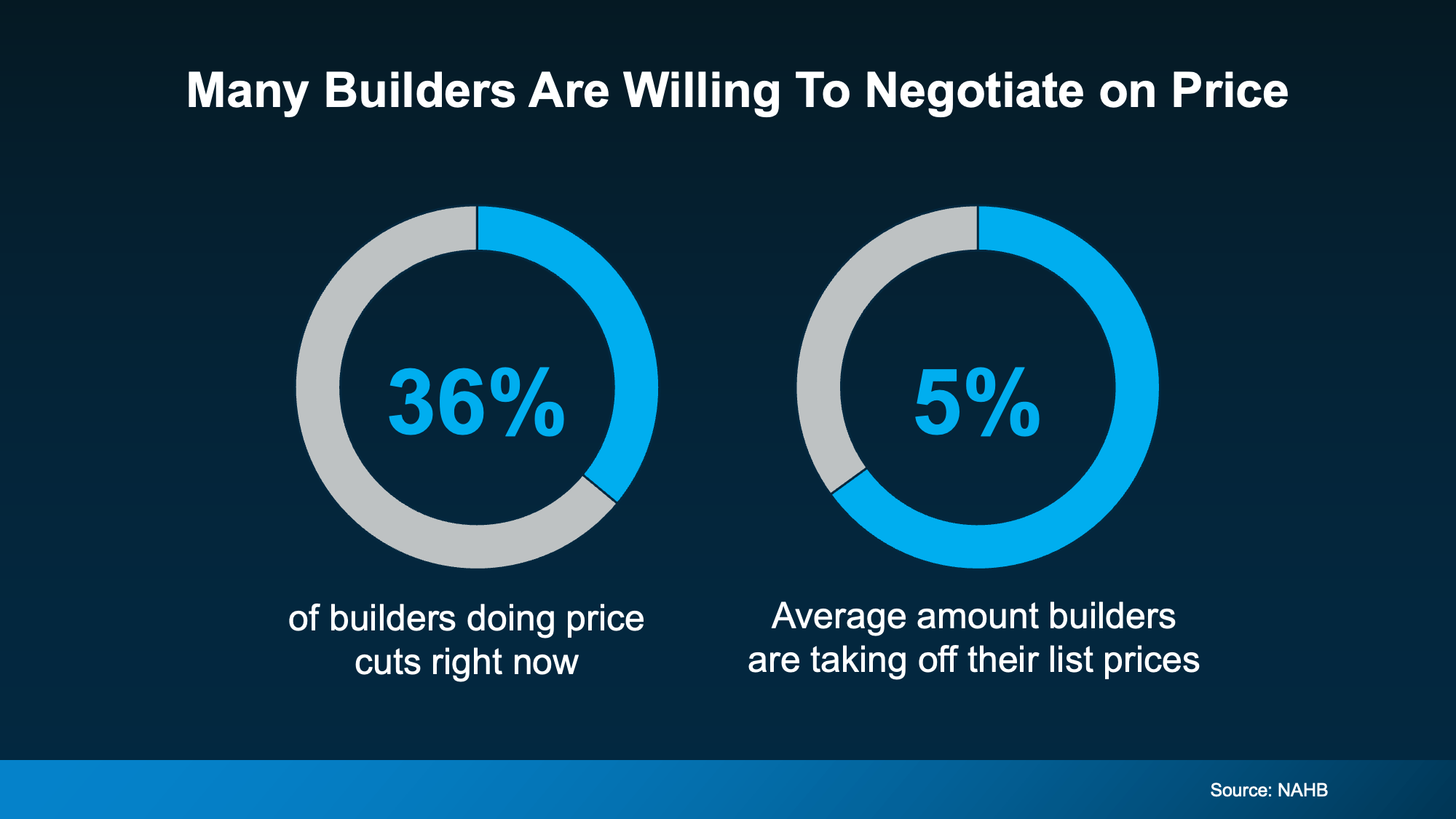

Lower sticker prices aren’t the only break buyers are getting. According to the National Association of Home Builders (NAHB), 60% of builders are currently offering some form of incentive to attract buyers. Those typically include:

- Help with closing costs: Some builders are covering thousands of dollars in fees to reduce the upfront cost of buying.

- Extra upgrades: Think premium finishes, appliance packages, and designer features, often added at no extra cost.

- Mortgage rate buydowns: When the builder pays to lower your mortgage rate, which reduces your monthly payment.

- Price cuts: Over one in three builders (36%) are cutting prices right now, averaging about 5% off list price (see graph below):

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

That last point catches a lot of buyers off guard – most assume that builders won’t budge on price.

But builders need to move what they’ve built. That’s a different mindset than a homeowner deciding whether to budge on price. So, you may find they’re more open to adjusting the price than you’d think. As Joel Berner, Senior Economist at Realtor.com, puts it:

“. . . many existing-home sellers resort to taking down their listing instead of taking less than their desired price, but builders are more motivated to sell their inventory than owner-occupants . . .”

And if you use the version of the graph that shows 2008 prices, you can even reference that in this explainer.

And if here, should I change the last sentence of the lede?

Bottom Line

Builder incentives and lower new home prices are working to your advantage in a way they haven’t in years. Connect with a local real estate agent to see what’s available in your area and what kind of deal a builder may be willing to make.

Could Moving a Bit Further Out Change Everything About Your Budget?

What Rising Inflation Means for Your Move

The Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Equity3 weeks ago

Equity3 weeks agoRecord High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out.

-

Agent Value4 weeks ago

Agent Value4 weeks agoThe Pricing Mistake That Could Cost You Your Sale

-

Agent Value4 weeks ago

Agent Value4 weeks agoWhy Staging Your House Could Pay Off This Spring

-

Equity3 weeks ago

Equity3 weeks agoAre Home Prices Going To Fall?

-

Equity4 weeks ago

Equity4 weeks agoWhat the Foreclosure Headlines Aren’t Telling You

-

Affordability3 weeks ago

Affordability3 weeks agoNewly Built Home Prices Hit a 5-Year Low

-

Affordability2 weeks ago

Affordability2 weeks agoWhat Most Veterans Don’t Know About Their VA Home Loan Benefit

-

Affordability2 weeks ago

Affordability2 weeks agoThe Truth About Affordability Today

You must be logged in to post a comment Login