Buying Tips

Worried about Home Maintenance Costs? Consider This

Imagine waiting a year to buy a home, only to find mortgage rates haven’t changed much. That may sound frustrating.But it’s a real possibility.

A lot of people are putting their plans on hold because they believe much lower mortgage rates are right around the corner. But, based on today’s forecasts, that may not happen. And you should know that before you decide what to do.

Let’s look at why experts don’t expect a dramatic drop in rates – and the options that could help you buy anyway. Because even if rates don’t fall, you can still move. Here’s how.

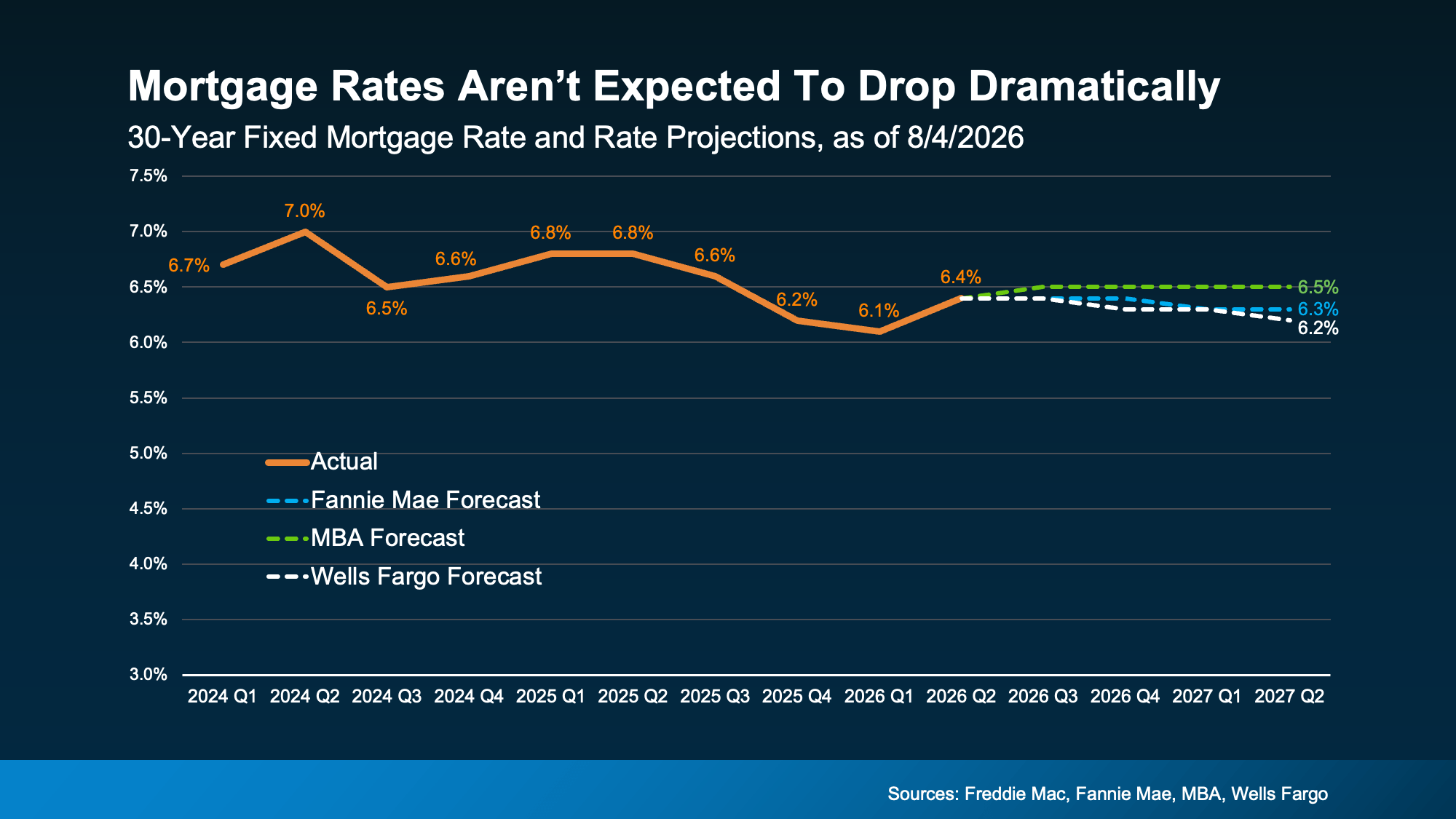

1. Mortgage Rates Aren’t Expected To Fall in a Meaningful Way

If you’re waiting for rates to fall, you’re not alone. A recent survey from Clever-Best Interest found 42% of people believe mortgage rates will drop below 5% this year.

The challenge is, that’s not what the experts who study mortgage rates every day are expecting.

Forecasts from Fannie Mae, the Mortgage Bankers Association, and Wells Fargo all show mortgage rates staying relatively steady in the low-to-mid 6% range through at least mid-2027 (see graph below):

Why? Rates are influenced by inflation, the overall economy, Treasury yields, Federal Reserve policy, global events, and a lot of other moving pieces. And right now, those factors simply aren’t pointing toward the kind of dramatic rate drop many buyers are waiting for.

Could rates move a little? Of course. But if you’re holding out for a bigger drop, today’s forecasts suggest you may be waiting a lot longer than you expect.

2. Inflation Is Still Elevated – And That’s Working Against Lower Rates

One reason experts aren’t expecting rates to fall much? Inflation. Generally speaking, high inflation is the enemy of lower mortgage rates.

And after a period of relative stability from mid 2023 to late 2025, recent data shows inflation has actually been trending higher lately (see graph below):

In other words, one of the biggest ingredients needed for much lower mortgage rates simply isn’t in place today. That helps explain why experts aren’t forecasting the kind of meaningful decline so many buyers are hoping for.

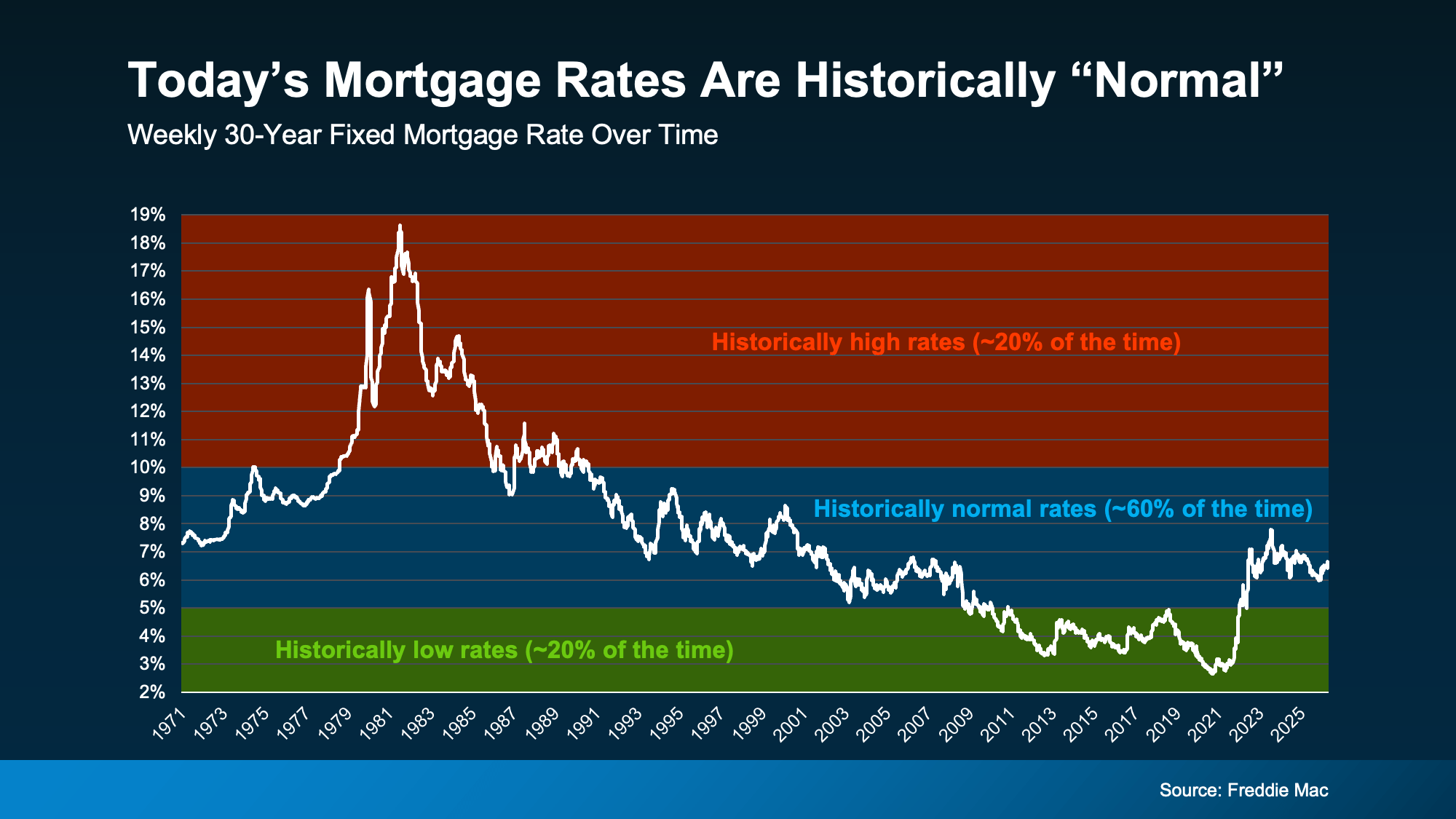

3. Today’s Rates Aren’t High, They’re “Normal”

And this may be the biggest mindset shift of all. The reality is, while today’s rates may feel high compared to a few years ago, they’re not high. They’re normal.

Historically, mortgage rates have spent the majority of their time somewhere between about 5% and 10%. And data from Freddie Mac shows we’re actually well in that range today. It just feels high because we all remember the ultra-low rates homeowners got during the pandemic (see graph below):

Now, this doesn’t suddenly make a 6% mortgage feel exciting. But it does remind us that waiting for super low rates again may not be a realistic strategy.

So… What Should You Do Instead?

None of this is meant to convince you that you have to buy today. You don’t. But if you need to because something in your life’s changed, there are still ways to find better affordability without waiting for mortgage rates to fall.

-

Check out newly built homes. Many builders are offering incentives to attract buyers, including price cuts, potentially lower rates, free upgrades, and more.

-

Ask about an adjustable-rate mortgage (ARM). If you don’t plan to stay in the home long-term, an ARM may offer a lower initial interest rate than a traditional 30-year fixed mortgage. It’s not the right choice for everyone, but it’s worth asking a lender if it fits your plans.

-

Look into mortgage rate buydowns. This is when you pay upfront to reduce your mortgage rate so you can get for a lower monthly payment without waiting for rates to fall.

-

Find out about assumable mortgages. An assumable mortgage allows you to take over the seller’s existing loan, including its lower mortgage rate.

The important thing is you shouldn’t assume waiting is your only option.

Talk with your real estate agent and lender about whether one of these strategies could be a good fit for you.

Bottom Line

If you’ve been putting your home search on hold because you’re convinced mortgage rates will be much lower soon, it may be worth taking another look at that strategy.

Connect with an agent or lender so you have an expert who can at least walk you through your options and decide whether waiting really puts you in a better position – or just keeps you on the sidelines a little longer.

If buying a home is on your radar, you’ve probably been keeping an eye on mortgage rates and home prices. But don’t forget about homeowners insurance.

Homeowners insurance has always been part of owning a home. But over the past few years, it’s become a larger expense for many homeowners – something that’s especially frustrating when affordability already feels tight.

The good news? While premiums are still rising, the latest data shows those increases are beginning to slow. Here’s what buyers should know.

Home Insurance Costs Have Gone Up

You’ve probably heard stories from friends or family about their premiums going up. And that’s not really a surprise when you consider data from the Pew Research Center shows 71% of homeowners say their insurance costs have gone up over the past few years.

While no one likes rising costs, knowing what to expect can help you plan ahead. Your first insurance payment is typically included in your closing costs, but after that it’ll become part of your monthly housing expenses.

Getting an insurance quote early can help you build a more realistic budget and avoid surprises later.

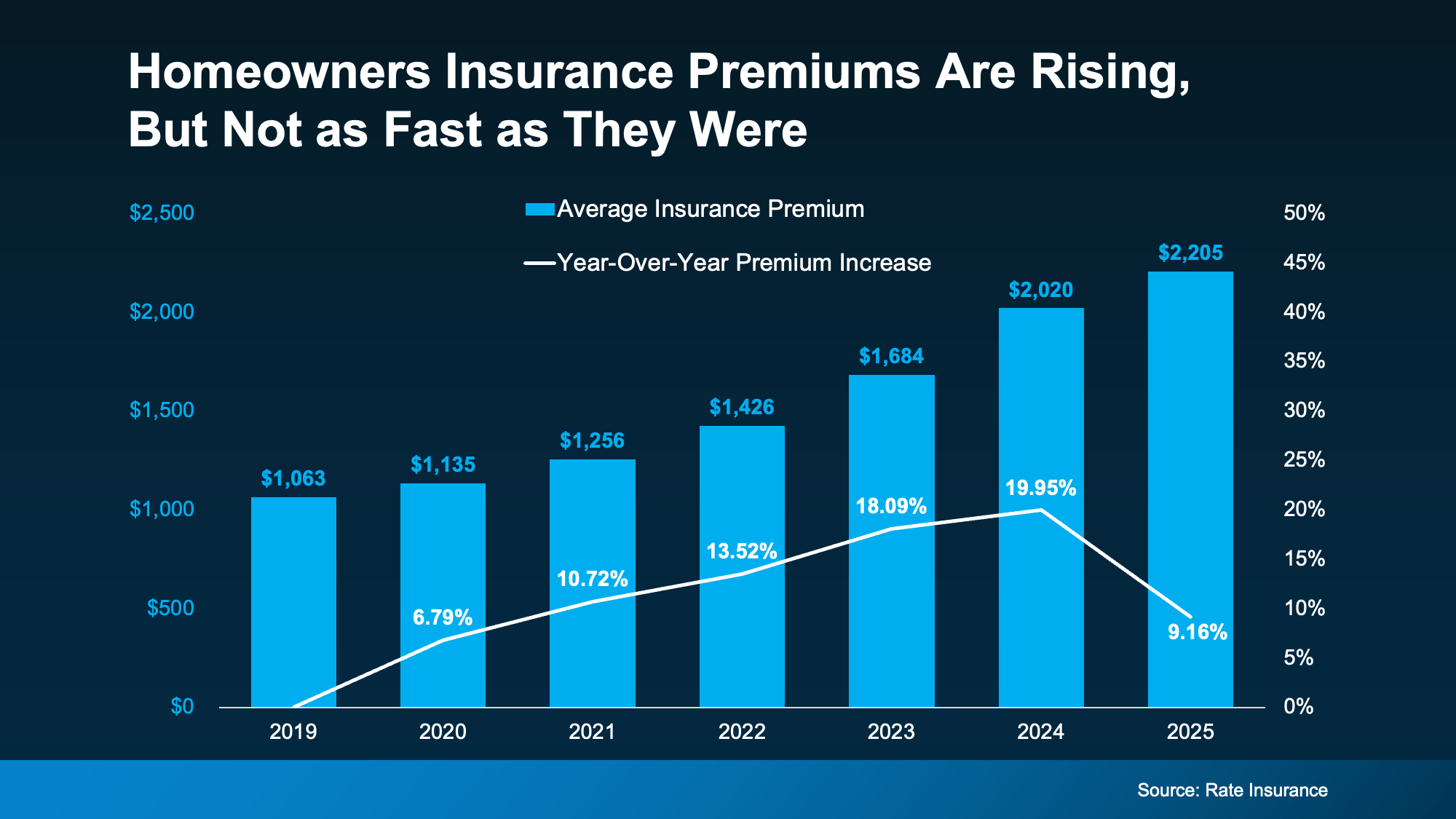

Premiums Are Rising, But Not as Fast as They Were

Most of the headlines focus on how home insurance is getting more expensive. And that’s true. But here’s the part that’s easy to miss.

Insurance premiums are still rising.

But they’re not rising as fast as they were.

According to the latest report from Rate Insurance, 2025 saw the first slowdown in annual premium increases since 2019 (see graph below):

That doesn’t mean premiums are getting cheaper. It simply means the rapid increases of the past several years may finally be starting to ease – a small but welcome step in the right direction.

But what you’ll pay in one part of the country can look very different from what someone pays somewhere else.

Where You Buy Can Make a Big Difference

Insurance costs vary because some parts of the country experience more claims than others. That’s why it’s important to look at what’s happening locally.

Your premium will depend on things like where you’re buying, the home itself, and the coverage you choose.

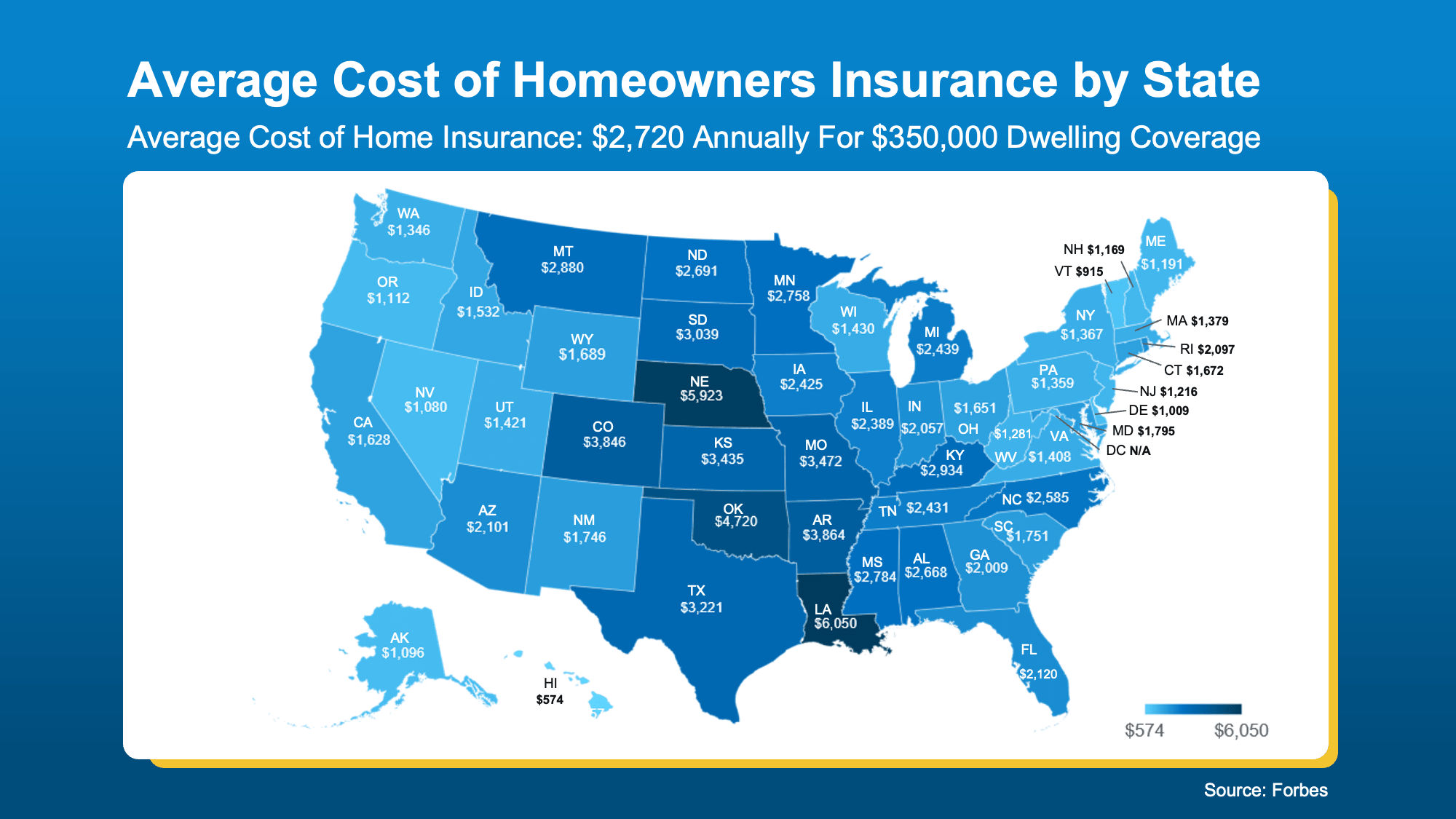

Forbes data can give a rough idea of your state’s typical premiums. Check out the map below – the darker the blue, the higher the costs tend to be in that state:

Ways To Lower Your Costs

While you can’t control every cost that comes with buying a home, you can control how prepared you are. If you’re crunching the numbers and trying to find ways to save, Insurify and NerdWallet offer these tips that can help you get the best insurance price possible:

-

Shop Around – Compare quotes from multiple companies.

-

Bundle Policies – Combine home and auto to see if a bundle price is cheaper.

-

Ask If There Are Discounts – Don’t miss out on savings you may qualify for.

-

Highlight Upgrades – Features like a new roof or storm windows can cut costs.

-

Improve Your Credit – A stronger credit score can mean better premiums.

One of the smartest things you can do is get an insurance quote before you make an offer. That way, you’ll know what your monthly housing costs are likely to be before you commit.

An insurance professional can walk you through your options and help you find coverage that fits both your needs and your budget.

Bottom Line

Homeowners insurance has become a bigger part of the homebuying conversation. But it doesn’t have to become a bigger source of stress.

The key is knowing what to expect before you buy. Get an insurance quote early, factor it into your budget, and lean on trusted local professionals to help you make the most informed decision possible.

After more than a year of headlines talking about how home prices are going to crash, the latest data shows that price growth may be starting to pick back up again. And depending on whether you’re buying or selling, that shift means something different for you.

The Numbers May Be Starting To Turn

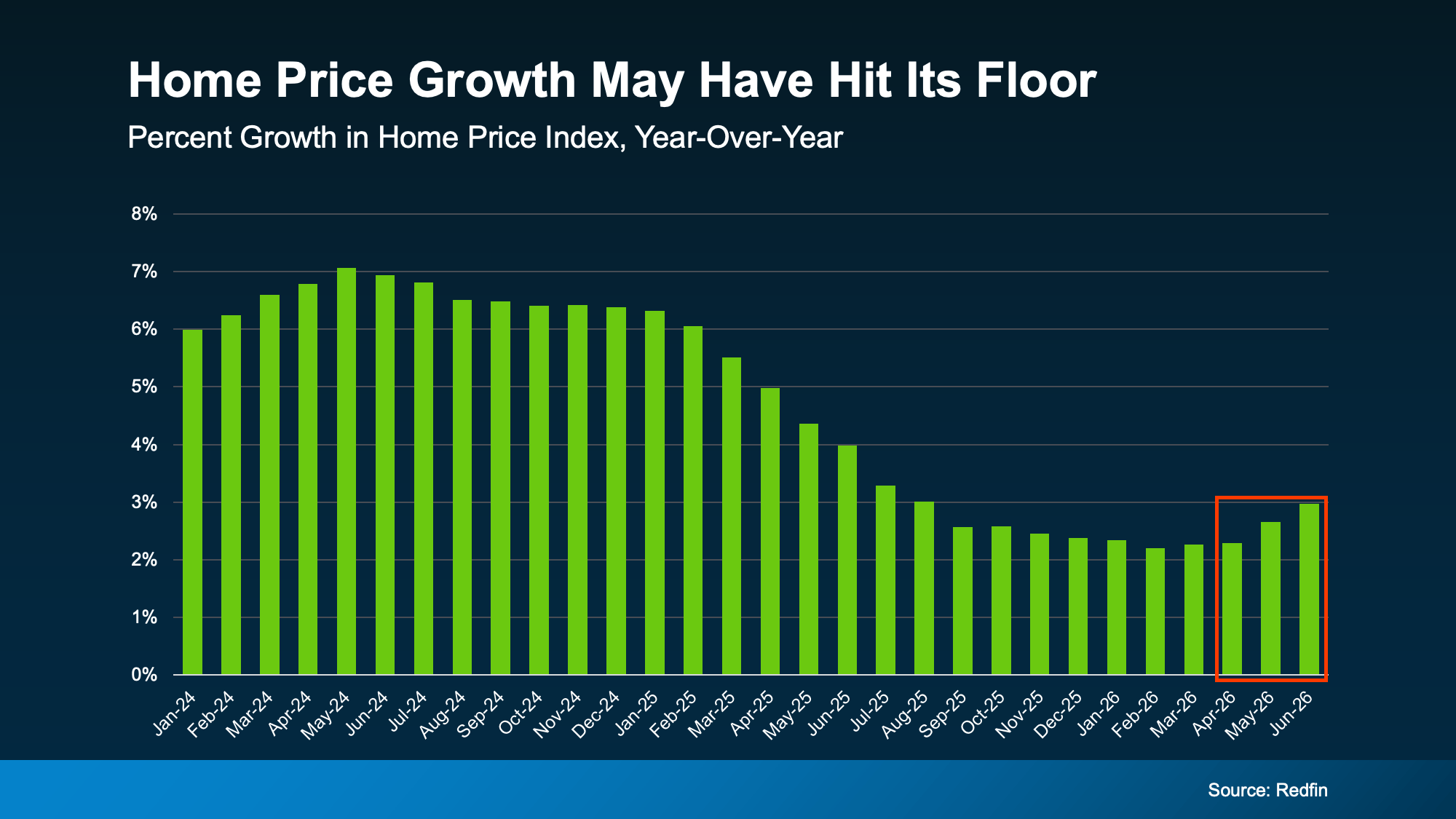

For the past couple of years, home price growth has been moderating – cooling from around 7% in mid-2024, according to Redfin (see graph below). But look at the right side of that graph. The pace of that growth appears to have hit its low point and started to turn.

While a couple months of data doesn’t necessarily mean this will be a lasting trend, there are some other signs that this could continue.

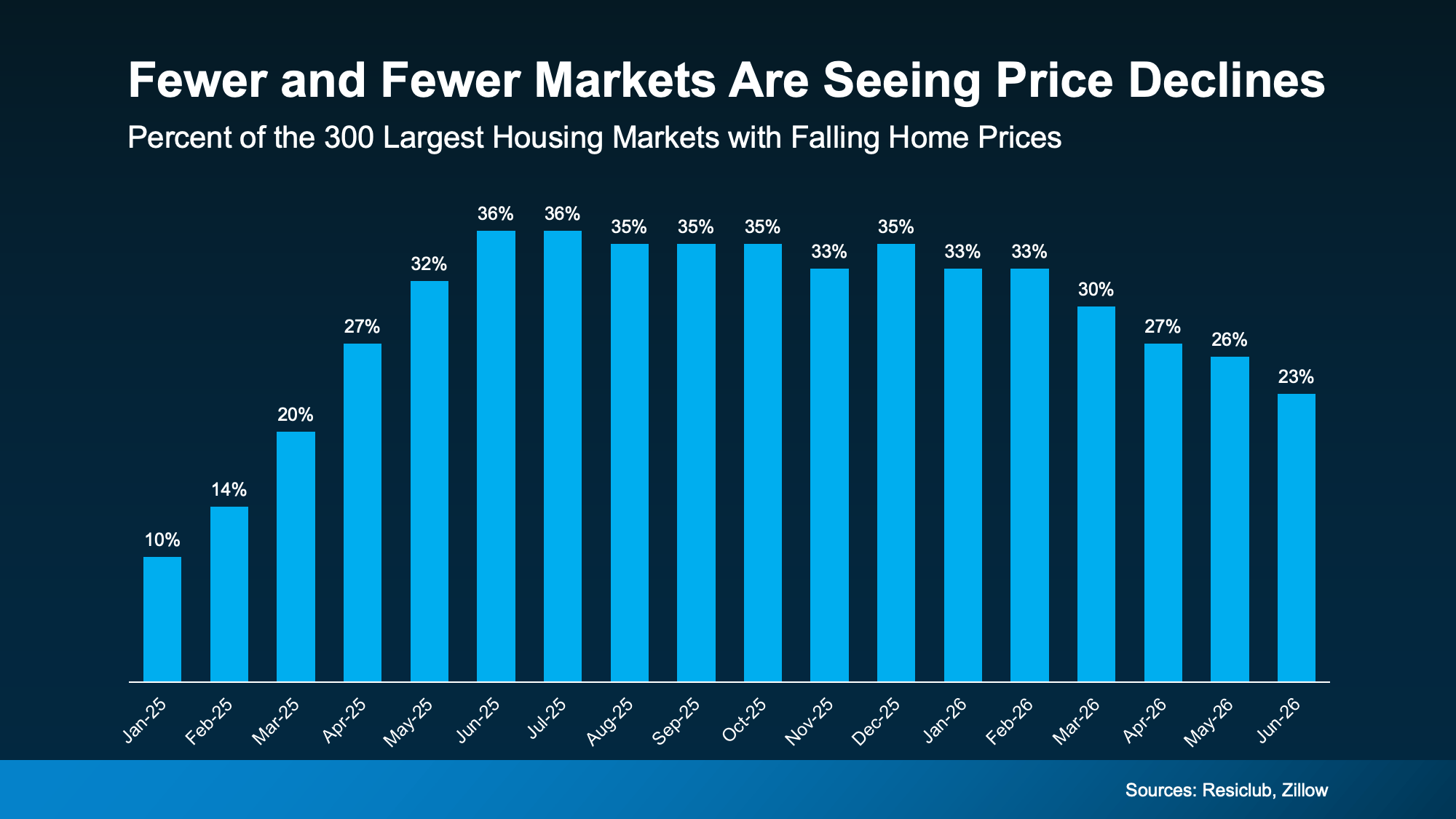

For example, fewer markets are seeing prices decline. According to ResiClub and Zillow, about 36% of the 300 largest housing markets had falling prices as of the middle of last year. Since the start of this year, that share has been shrinking. Now? Only 23% are experiencing those mild dips (see graph below):

When fewer markets see prices falling, that means more markets are seeing prices rise again.

And forecasts suggest this shift has room to run. On average, experts project home prices will rise about 2.3% nationally this year. And for that to happen, price growth would have to pick up a bit in the second half of 2026.

But Remember, Real Estate Is Local

While it looks like national prices may be starting to pick back up a tiny bit, that doesn’t mean that’s what’s happening in your neighborhood.

National home prices are really just an average of hundreds of local markets. Some are climbing faster. Others are still cooling. But one reason the national average may be looking up is because a growing number of metros may actually be net positive for prices this year.

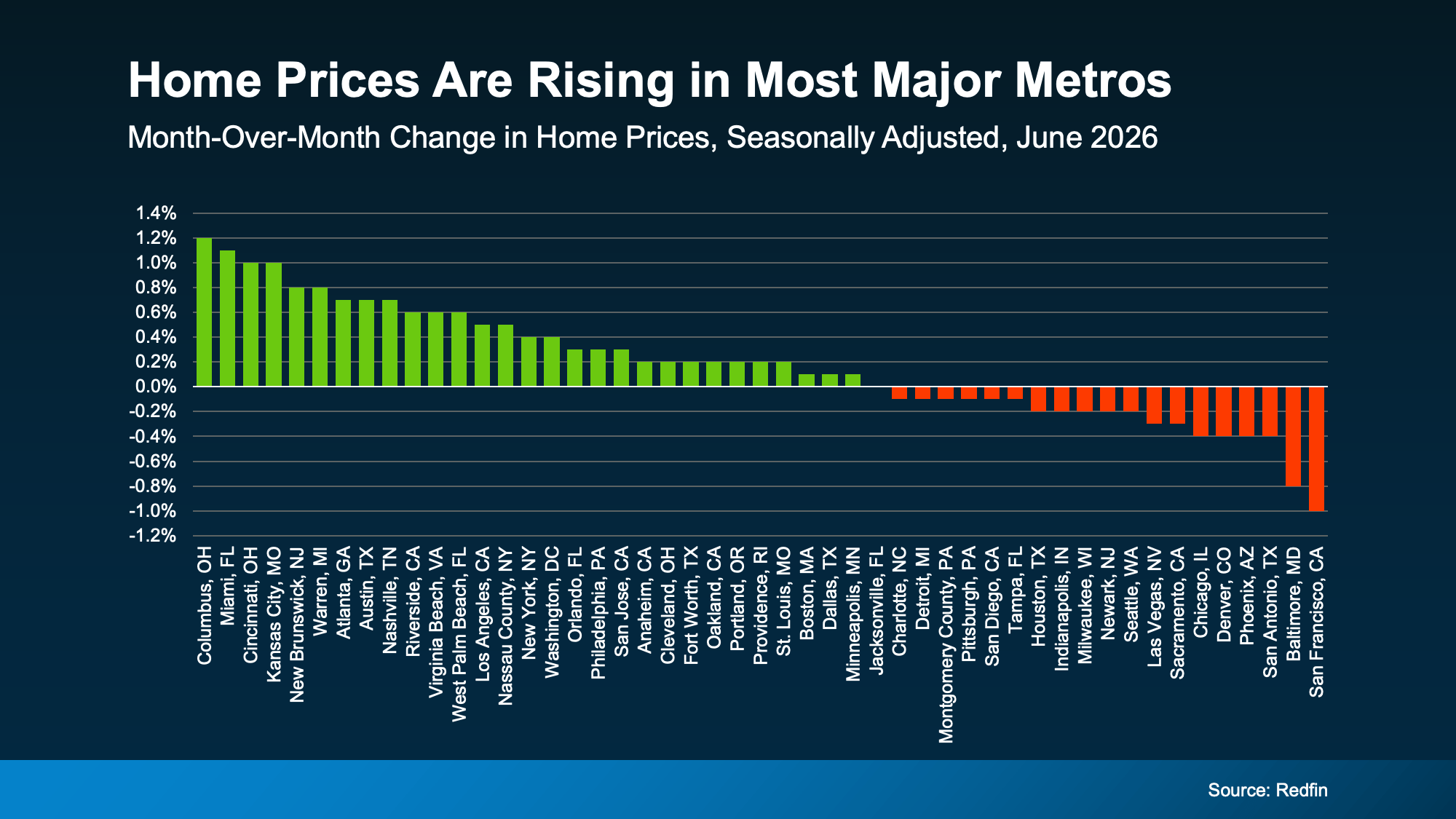

Not long ago, the major metros were split about 50/50 – half seeing prices rise and half seeing them fall. Now, that balance looks like it’s starting to tip in a more positive direction. Just last month, more than half of the major metros saw prices go up, according to Redfin (see graph below):

As Selma Hepp, Chief Economist at Cotality, explains:

“. . . local markets continue to tell very different stories. Annual home price growth has changed little since the start of the year, but some markets, especially those supported by strong job and income growth in the West and more affordable Midwest markets, have seen notable acceleration in price gains.”

What This Means for You

Home price headlines can be confusing because they don’t always tell the full picture. Lean on an agent to understand what’s happening in your local market and what the early signs say for where prices may go from here.

That’s the best way to stay one step ahead of the market.

If you’re buying: slower price growth has worked in your favor. You’ve had more room to negotiate and a budget you could plan around. If price growth is picking up in your area, buying now may mean paying less than you would later this year.

If you own a home: you’ve been gaining equity all along, even while growth moderated. If growth keeps picking up, those gains could speed up, too. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), projects the typical homeowner will gain roughly $16,000 in housing wealth this year. And if you’re thinking about selling, this shift is a good early sign for you. Just remember, the market is still pretty balanced and buyer-friendly in a lot of areas right now.

Home price growth slowed way down, and now it’s showing early signs of picking back up. Whether you’re buying or selling, let’s connect so you can see exactly what prices are doing in our local market and what that means for your plans.

Bottom Line

Home price growth slowed way down, and now it’s showing early signs of picking back up. Whether you’re buying or selling, connect with a local real estate agent so you can see exactly what prices are doing in your local market and what that means for your plans.

Thinking About Waiting for Lower Mortgage Rates? Read This First.

Big Investors Are Backing Off and That’s Your Opening

Here’s Where To Start if You’re Selling and Buying at the Same Time

-

For Sellers4 weeks ago

For Sellers4 weeks agoThink Nobody’s Buying Homes Right Now? Think Again.

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

-

First-Time Buyers3 weeks ago

First-Time Buyers3 weeks ago14 Years Running: Why Real Estate Is Still America’s Favorite Investment

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoMore Homes, Better Prices: A Buyer’s Summer

-

Equity2 weeks ago

Equity2 weeks agoThe House That Started It All Could Kickstart What’s Next

-

Affordability3 weeks ago

Affordability3 weeks agoPriced Out? A Condo or Townhome Could Be Your Way In.

-

For Sellers2 weeks ago

For Sellers2 weeks agoSelling a Luxury House? Here’s Why Now Is a Good Time

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoHome Price Growth Slowed Down. That May Be Changing.

You must be logged in to post a comment Login