For Sellers

What To Do When Your House Didn’t Sell

A lot of people who want to move are telling themselves the same thing: “Maybe I’ll just wait until later this year once things calm down.”

While waiting sounds like a good plan, there’s something worth knowing before you decide. Rates aren’t expected to change much, so if that’s the #1 reason you’re waiting, it may not pay off. And there may be other things you miss out on in the meantime.

Historically, Summer is one of the strongest seasons of the year for both buyers and sellers. And if you delay your move until Fall or Winter, some of those opportunities may already be fading.

Buyers: Fresh Inventory Is Your Real Summer Advantage

One of the biggest frustrations buyers have faced over the past few years has been a lack of affordable options. Maybe you’ve run into that yourself:

-

You find a house you like, but it’s out of your budget.

-

You find something in your budget, but you don’t like it.

-

Or worse, nothing interesting hits the market for weeks.

Historically, Summer helps with that.

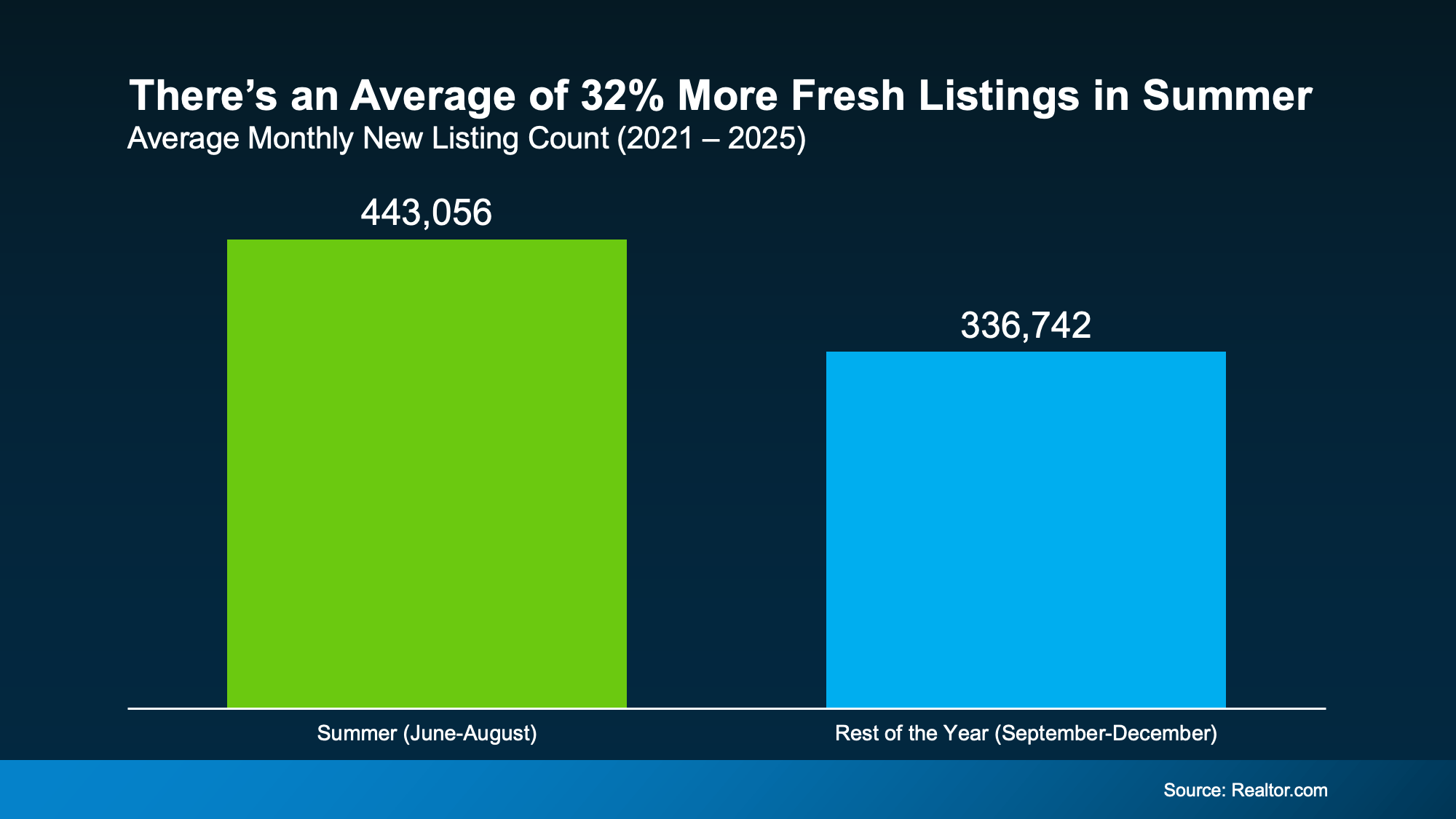

Looking at data from the last few years, Summer months consistently bring more sellers into the market than later in the year. And that gives buyers a real window of fresh choices.

According to Realtor.com, any given Summer month typically sees about 32% more fresh options than the average month from September-December.

With more newly listed homes, there’s a better chance of finding one you like where the numbers actually work.

Because all it really takes is one home to completely change your search. And if you’ve got more popping onto the market to choose from, maybe one of those is exactly what you need.

But keep in mind, this seasonal window isn’t open forever. Fresh inventory tends to slow down once Summer ends.

Many homeowners who planned to sell this year have already listed by then. Families who wanted to move before school starts have often already gotten it done, or at least, set it into motion. So, new listing activity usually cools as we head into Fall and Winter.

Of course, every year is different. But if finding the right home at the right price has been your biggest challenge, waiting until later in the year may not necessarily give you more options. In fact, recent history suggests it may do just the opposite.

Sellers: Homes Usually Sell for More in the Summer

If you’re thinking of selling, you may be considering holding off because you’ve seen headlines about lower asking prices, price cuts, and softer conditions in some markets. But those headlines don’t tell the whole story or convey just how much it varies by area.

Here’s what you really need to know. Even though the market’s becoming more balanced and some pockets are experiencing price declines, that doesn’t mean you’ve missed your chance to sell.

Seasonality can still work in your favor no matter where you are. And this Summer could still give you the chance to sell for a good price.

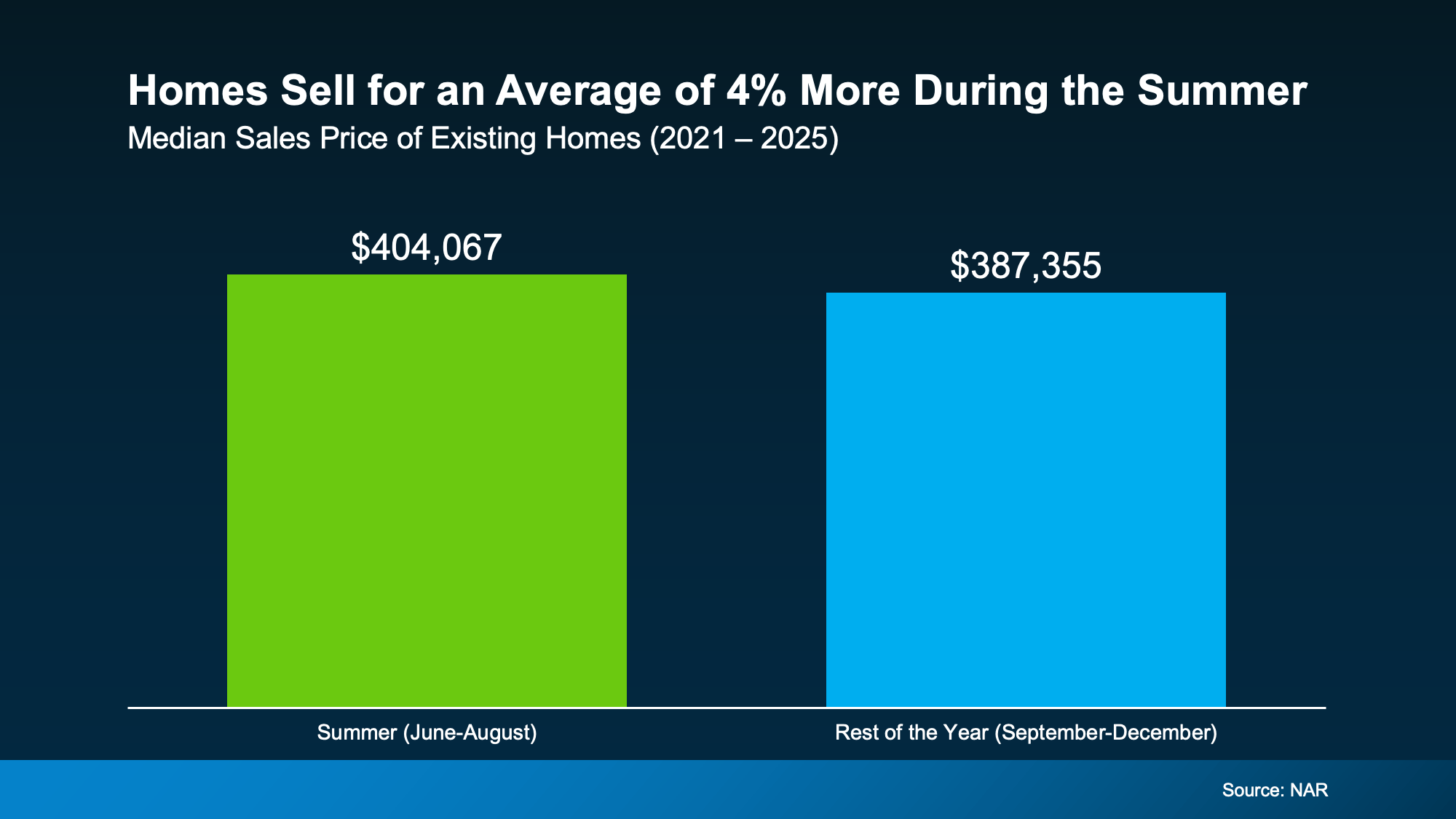

According to the National Association of Realtors (NAR), homes sold during a Summer month usually sell for about 4% more than homes sold during the typical month from September-December:

Why? Summer buyers are usually operating on a set timeframe. They’re trying to move before the next school year or when they have more PTO and warmer weather to tour houses. That urgency can translate into better offers.

Now, that doesn’t mean you should price your house 4% higher this Summer. That would actually be a mistake in today’s market.

It just means if you’re looking to get as much for your house as you reasonably can, a Summer move could be a smarter play than waiting until later this year.

Because based on typical seasonality, you may get more for your house than you would if you waited until the Fall or Winter (when there are typically fewer buyers active).

And if you’re considering a move anyway, that’s worth factoring in.

Bottom Line

Could waiting until later this year work out? Sure. But it’s important to understand what you may gain by moving now too – that way you have the full picture before you decide.

If a 2026 move is on your radar, talk to an agent about what matters most to you. Depending on your priorities, Summer could be your moment.

If the housing market feels confusing right now, you’re not alone.

Mortgage rates have risen. Home sales haven’t picked up like expected. And many buyers and sellers are wondering when things are going to feel easier or be more affordable.

The truth is: a lot changed over the first half of this year.

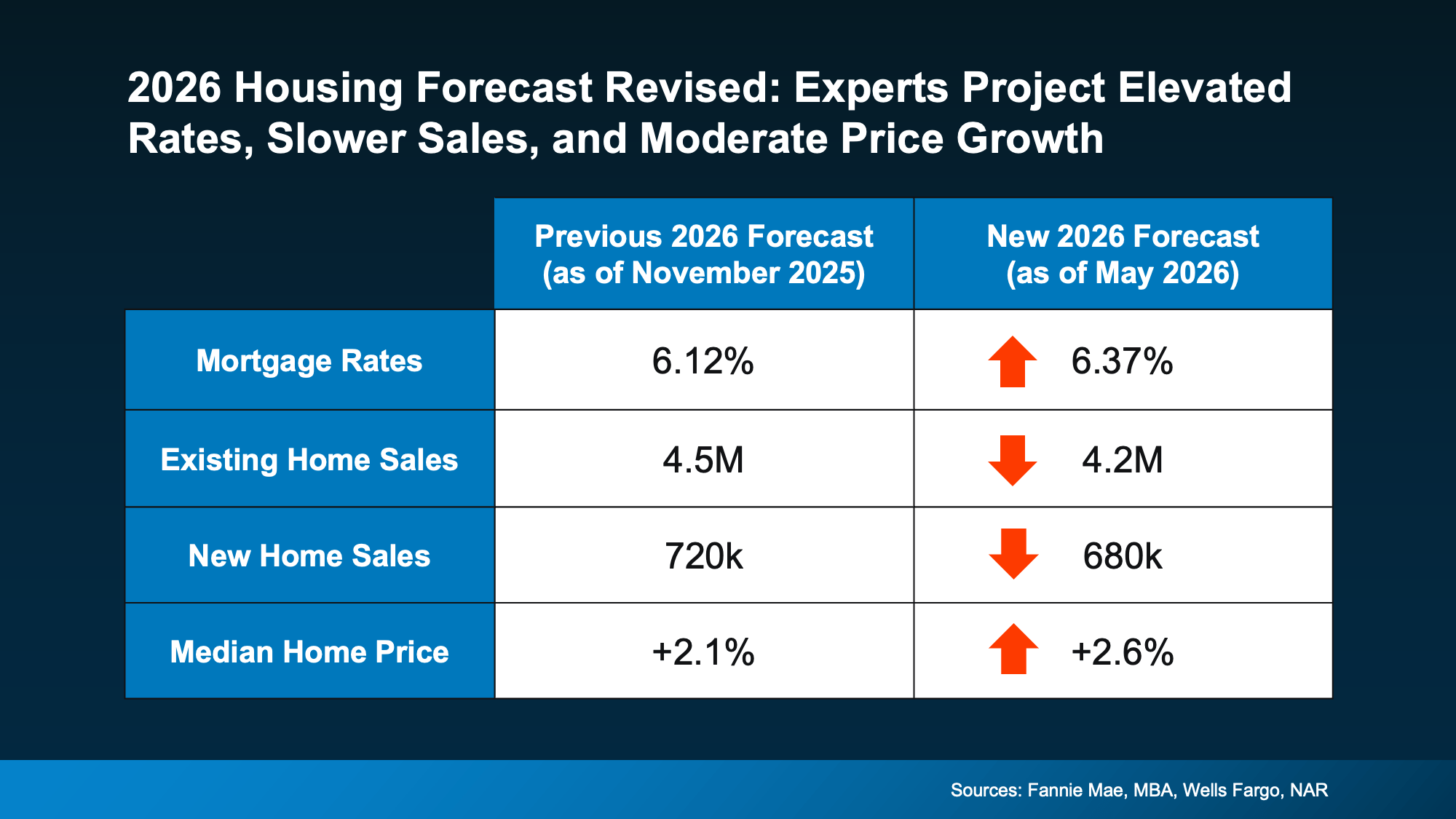

Back at the end of 2025, economists were forecasting a much stronger housing market for 2026. They expected mortgage rates to come down, affordability to improve more dramatically, and home sales to rebound.

But lingering inflation, economic uncertainty, and growing geopolitical tensions overseas pushed mortgage rates higher than expected. And because rates stayed elevated for longer, many buyers continued to hold off.

That’s why experts recently revised their housing forecasts for the rest of the year (see graph below):

So, what does this actually mean for you? Let’s break it down.

Mortgage Rates May Remain Elevated

While just about everyone wants mortgage rates to go back to the uppers 5s or low 6s we saw at the start of the year, as of right now, the experts don’t think that’s likely to happen this year.

Instead, forecasts have been updated from the low 6s they originally projected. Many industry organizations are saying rates will stay in roughly the mid 6s this year. The good news is, that’s still lower than rates were a year ago.

Of course, this is based on what we know today. If the conflict overseas comes to an end or inflation drops, this could change. But if you’re waiting for lower rates, it may not pay off in the way you expect.

Existing Home Sales Revised Lower

Back in late 2025, experts expected we’d sell an average of 4.5 million homes this year. Now? That’s dropped down a bit to 4.2 million.

That tells us something important: buyers are still hesitant because affordability remains challenging.

Higher mortgage rates have made monthly payments harder to manage, especially for first-time buyers. And that’s slowed the pace of the market compared to what was originally expected. But even though the forecast was revised down, we’re still expected to sell more homes than last year.

Once geopolitical tensions resolve and rates begin to settle down, many experts believe that group of buyers will be ready to jump back in. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

There has already been a few glimmers of renewed hope lately. In recent months, pending homes sale have been improving month-over-month despite higher rates.

So, if you’re able to afford a home at today’s rates, it could still make sense to buy now. Because otherwise, if you wait, you’ll have more competition (and potentially fewer homes to choose from) when those others buyers jump back in.

New Home Sales Also Slowed

Builders also expected to have a stronger year. Earlier forecasts projected new home sales would top 700k in 2026. Now, economists expect we’ll be just shy of that number.

Again, mortgage rates are a major reason why.

But the upside for buyers is that builders may be even more motivated to sell. That means builder incentives, negotiation opportunities, and pricing flexibility may continue in many markets. So, if you live somewhere where there’s more new construction, this may actually be a bright spot for you.

Builders could be more ready to negotiate, and that gives you more leverage to get a better deal.

Home Prices Are Still Expected To Rise

This is one of the most important takeaways from the entire forecast. Even though sales activity is slower, on average, experts did not revise their home price forecast downward.

They still expect prices to rise nationally this year.

Why? Because while buyer demand has softened, the number of homes for sale is still relatively limited overall. That imbalance is helping support prices, even in a slower market.

Of course, conditions vary depending on where you live. Some markets are cooling more than others. But nationally, experts are still projecting steady price growth — not a major decline. And that should be a comfort whether you’re buying or selling.

Because sellers don’t want a major drop in prices. And while buyers may think they do, generally you feel better about a big purchase when it doesn’t depreciate right away.

Bottom Line

The housing market hasn’t rebounded as quickly as experts originally hoped. But that doesn’t mean it’s stalled.

Higher inflation and lingering economic uncertainty caused economists to revise their forecasts for this year. But importantly, when those two things settle down, many experts believe the market will regain its momentum.

So don’t see this revision in forecasts as a sign of trouble. See it as a temporary reaction to overall conditions and uncertainty.

If you want to know what’s happening in your local market, and what it could mean for your plans for the rest of this year, talk to a local agent.

You may be telling yourself you’re going to wait to move – maybe you’re hoping mortgage rates will come down, prices will fall, or the market will feel a little easier.

And honestly? A lot of people feel that way right now. But here’s what some are starting to realize.

Waiting doesn’t usually fix the thing that made you want to move in the first place.

Your family still desperately needs more room. Your empty nest still feels too…empty.

Your parents or grandparents still need you to live closer.

You just got married… or divorced.

Your vision of retirement has you living somewhere else.

Eventually, life can reach a point where waiting feels harder than moving.

That’s why some people are still deciding to buy right now, even in today’s market. Not because conditions are perfect. But because the life changes behind their move never really went away.

And maybe that’s exactly where you are too. If so, you’re certainly not alone.

The Real Reasons People Move

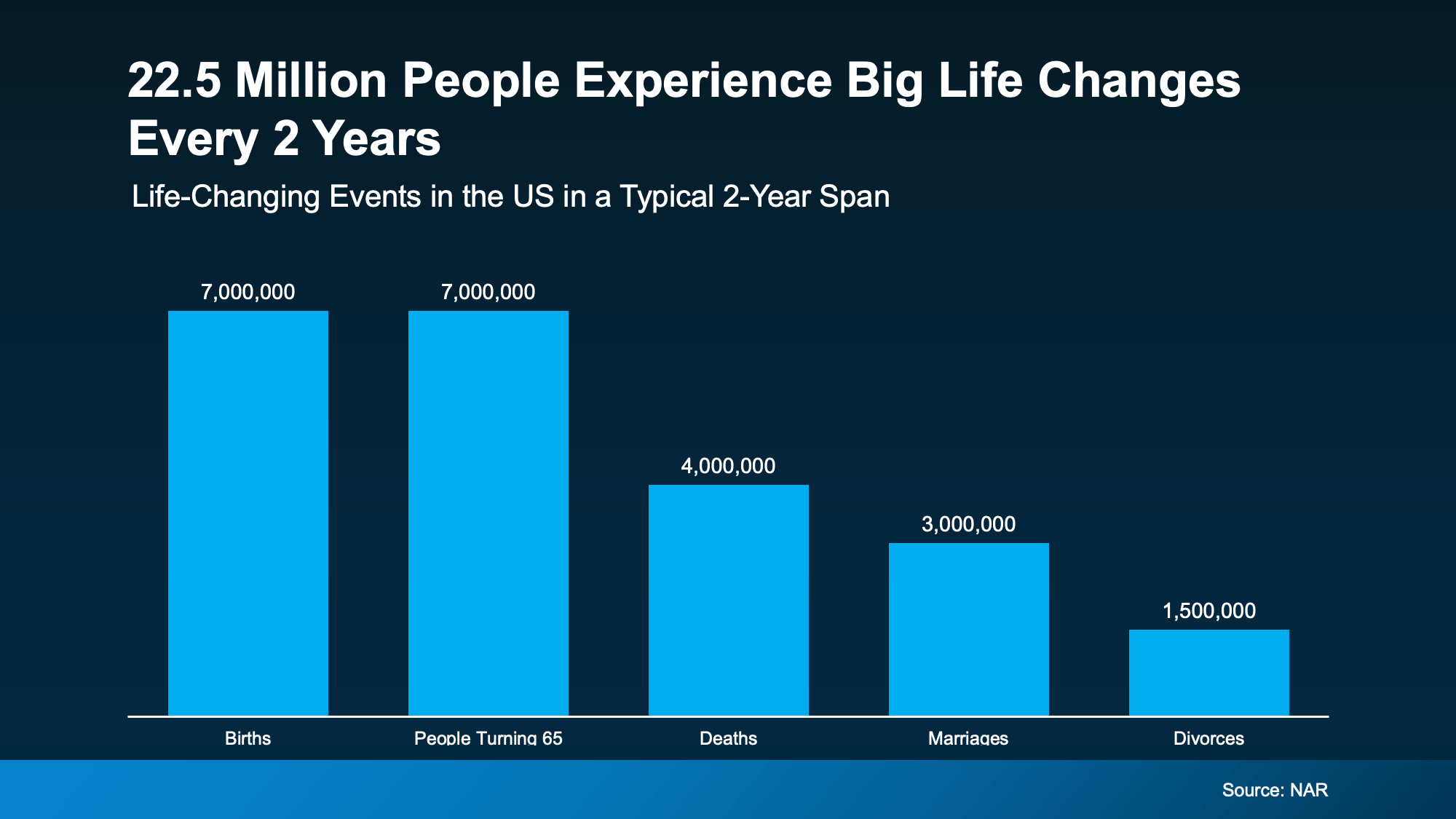

Data from the National Association of Realtors (NAR) shows 1 in 5 buyers last year said they felt like they had to purchase a home at that time, no matter the market.

That’s an important reminder right now. Sure, the dollars and cents of your move have to make sense for you. But big life changes happen whether mortgage rates and home prices are high, low, or somewhere in between.

And those big life events happen more than you may think. NAR says roughly 22.5 million people experience major life changes in a typical two-year span (see graph below):

These are exactly the kinds of things that can change how much space you need, where you want to live, or what kind of lifestyle makes sense now. Chen Zhao, Head of Economics Research at Redfin, explains:

“Life doesn’t stand still—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood.”

And that’s what makes waiting so hard. Every month you spend hoping the market changes is another month living in a house that no longer works for your life. It’s stressful to feel stuck. And that feeling usually doesn’t disappear.

There May Be More Opportunity Than You Think

But while affordability is still a challenge, there may still be a way for you to make your move.

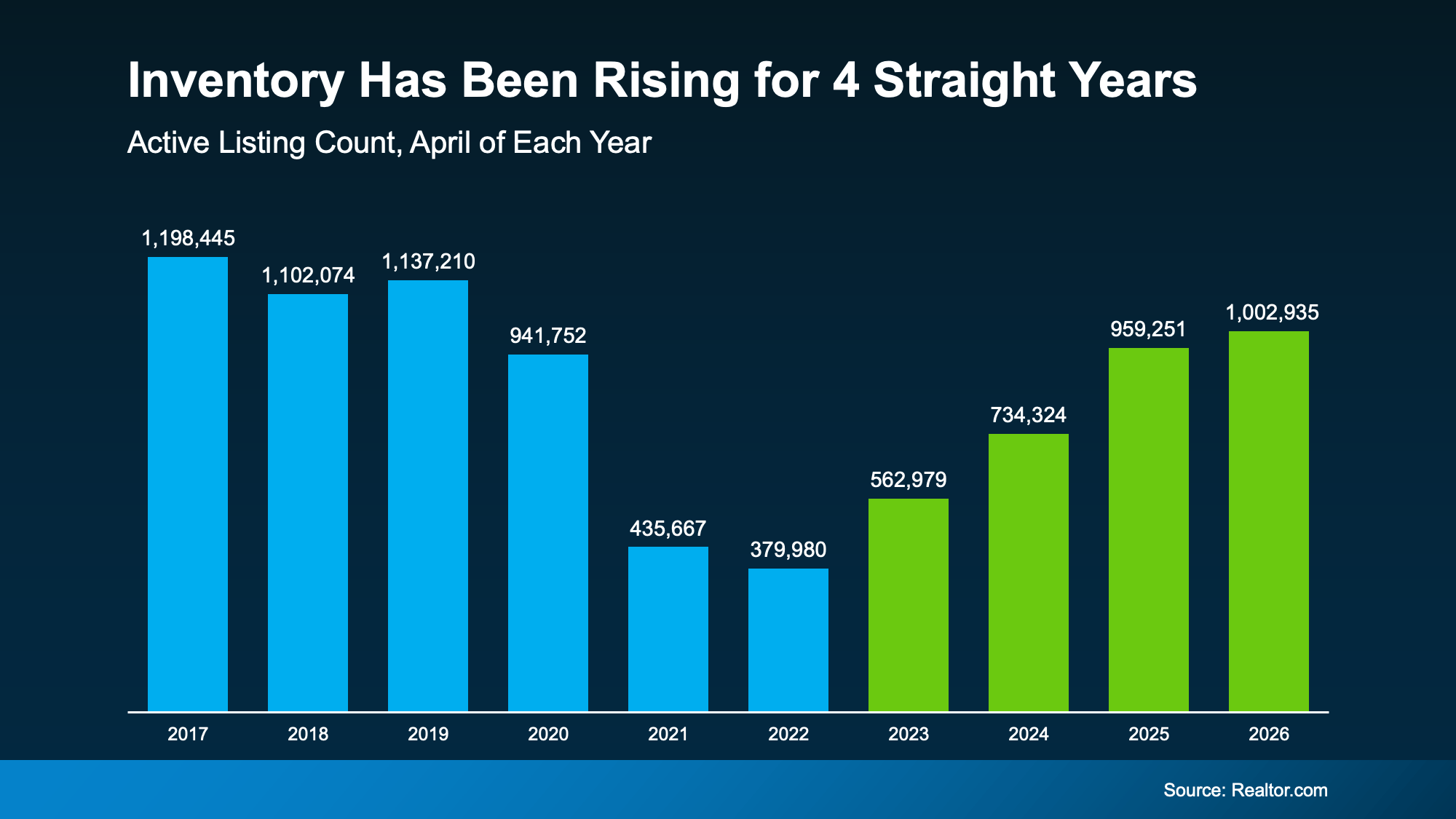

The number of homes for sale has been growing for 4 straight years (see graph below). That means more homes to choose from and, in some markets, more room to negotiate than buyers had just a few years ago.

That doesn’t mean moving is suddenly easy. But it does mean some buyers are finding ways to make a move work. So, if you’ve been putting your plans on hold, maybe the question isn’t just:

“What’s the market doing?” or “When will it get better?”

Maybe ask yourself this, too: “Can I still live where I’m at right now and make it work?”

If the answer to that second question is “no,” it may be worth having a conversation about what your options look like today – despite where rates or prices are. You could find your move is still possible after all. With more homes for sale, there’s a better chance to find one that fits your life (and your budget) right now.

Bottom Line

Life changes. Priorities shift. Families grow. Kids move out. Careers evolve. And eventually, the house you’re in may stop fitting the life you’re living.

If that’s been weighing on you lately, talk to an agent about what your options could realistically look like today, no matter where rates or prices are.

Life can’t always wait for perfect market conditions. Maybe you don’t have to either.

Two Big Reasons To Move This Summer

Lower Asking Prices Are a Win for Today’s Buyers

Could Moving a Bit Further Out Change Everything About Your Budget?

-

Equity3 weeks ago

Equity3 weeks agoRecord High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out.

-

Agent Value4 weeks ago

Agent Value4 weeks agoThe Pricing Mistake That Could Cost You Your Sale

-

Equity4 weeks ago

Equity4 weeks agoAre Home Prices Going To Fall?

-

Affordability3 weeks ago

Affordability3 weeks agoNewly Built Home Prices Hit a 5-Year Low

-

Affordability3 weeks ago

Affordability3 weeks agoWhat Most Veterans Don’t Know About Their VA Home Loan Benefit

-

Affordability2 weeks ago

Affordability2 weeks agoThe Truth About Affordability Today

-

For Sellers2 weeks ago

For Sellers2 weeks agoThe Real Reason Some People Are Still Moving Right Now

-

Economy1 week ago

Economy1 week agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

You must be logged in to post a comment Login