For Sellers

What To Do When Your House Didn’t Sell

Remember how exciting it was to buy your first place? It felt like crossing a long-awaited finish line. It gave you a place to build your life. Maybe it’s where you lived when you got married. Or where you welcomed a child or a pet into the family.

But that was just the beginning.

For most people, your first house was never meant to be your forever home. It’s a stepping stone for what comes next.

And if your life looks different today than it did when you got the keys, you’re not stuck. Moving may be more realistic than you think.

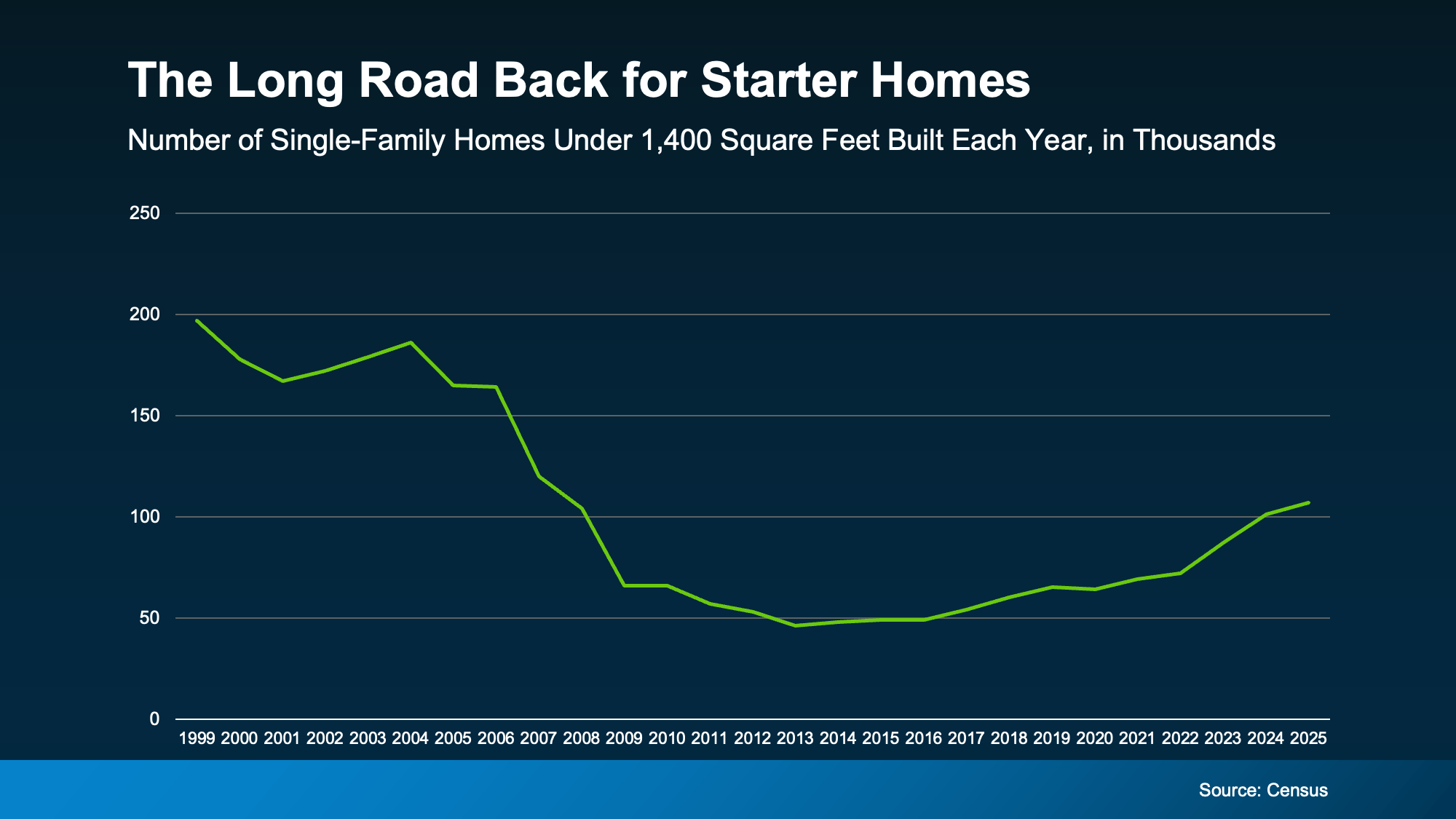

Starter Home Inventory Is Still Relatively Low

If you’ve been wondering whether now is the right time to move up, here’s something worth knowing. Starter homes remain one of the hardest types of homes to find. And that’s good news if you’re thinking about selling your first place.

Historically, we haven’t been building enough homes for first-time buyers. And even though homebuilders have shifted more attention toward smaller, entry-level homes lately, the Census shows there’s a long way to go to re-build supply (see graph below):

That means your current house is in demand – and that’s a dream scenario for sellers. But that’s only half the story. You also need somewhere to go.

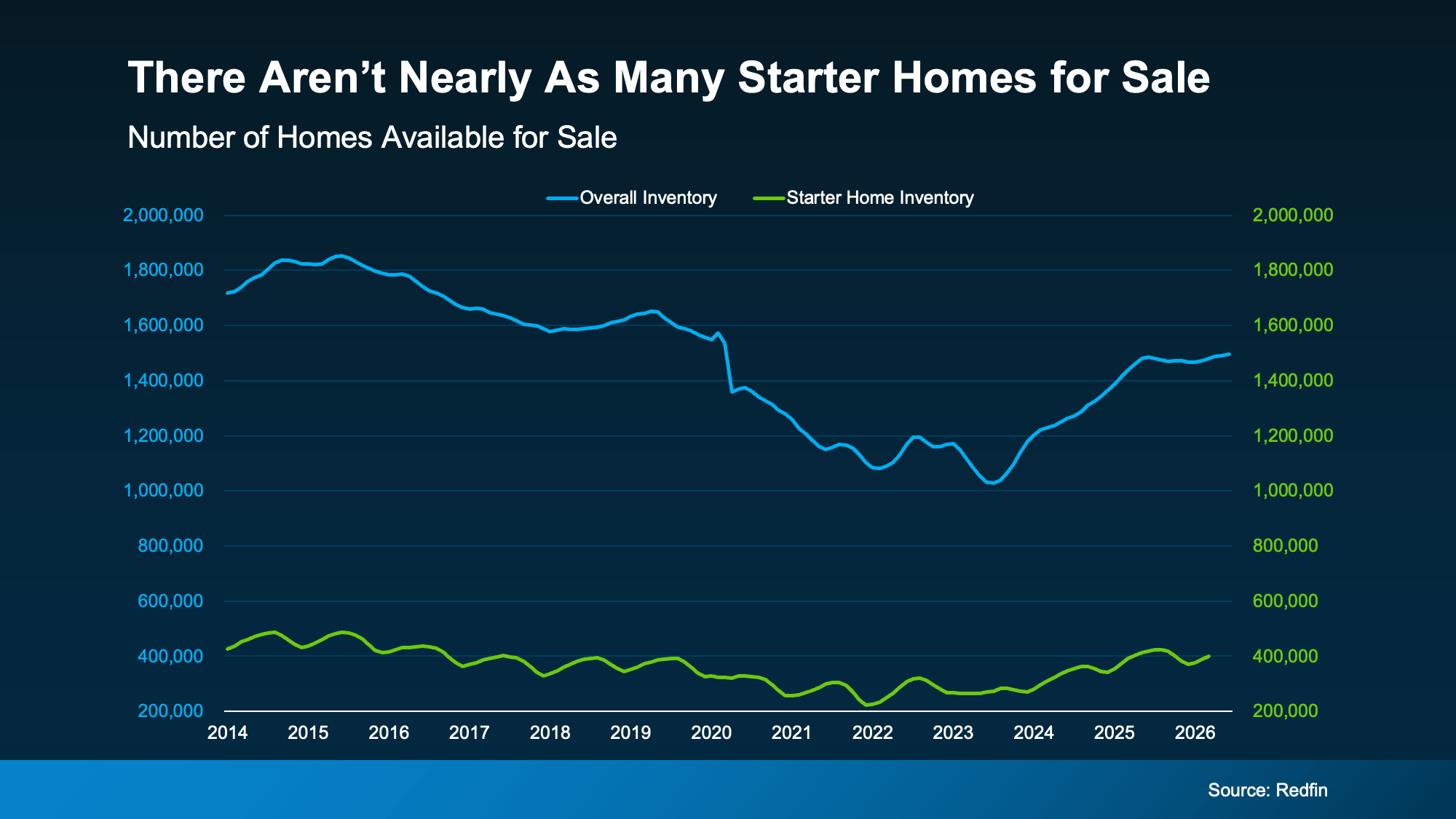

There Are More Move-Up Homes on the Market

Here’s where this gets interesting. While the supply of starter homes remains tight (the green line), data from Redfin shows that the number of homes for sale has been climbing overall (the blue line):

As Nadia Evangelou, Principal Economist and Director of Real Estate Research at the National Association of Realtors (NAR), explains:

“Too much of the inventory available today remains concentrated at higher price points, leaving a shortage of options for entry-level and middle-income buyers.”

That means you may have more choices for your move up than you’d expect. Whether you’re hoping for another bedroom, a home office, a bigger backyard, or simply more room for this next stage of life, today’s market may finally be giving you the chance to find it.

At the same time, your current house may be exactly what someone else has been looking for because homes like yours are still in short supply. That’s a unique advantage for move-up buyers. And it could help you sell for a stronger price. As Zillow says:

“Starter home value appreciation has outpaced other types of homes nationally, mostly because they’re so in demand.”

Your Biggest Advantage May Be Your Equity

Here’s the cherry on top. There’s one more thing your first home has been doing behind the scenes, and that’s building equity. Every mortgage payment you’ve made and every year your home’s value has grown has quietly increased your ownership stake in your house.

According to Cotality, the average homeowner with a mortgage has $295k in equity built up. While your number may be different, once you sell, it could become the down payment on your next home or help reduce the amount you need to borrow at today’s rates.

Put it all together and your move up becomes a lot more realistic than you think:

-

The house you’re selling is in demand.

-

The house you’re buying may be easier to find.

-

And the equity you’ve built can help bridge the gap between the two.

Your first home did exactly what it was supposed to do. It gave you a place to start.

Now, it may be the thing that helps you take the next step.

Bottom Line

Your first home was never meant to be your forever home. It was meant to help you build a life and build the financial foundation for whatever came next.

If your current home no longer fits the life you’re living today, connect with an agent. You may be closer to your next chapter than you realize.

If you’ve been thinking about selling, you’ve probably seen plenty of headlines suggesting buyers have just about disappeared. But there’s a big difference between a slow market and a stalled one.

Yes, mortgage rates are still higher than most people would like. Homes aren’t selling as fast as they were. And every week seems to bring another headline about buyers sitting on the sidelines. But here’s what you haven’t heard.

Despite everything going on, buyer demand has been remarkably resilient.

In fact, more sellers are getting to put up the “pending sale” sign now than during the last two years. What’s even more surprising is that they’re doing it at a time of year when activity usually starts to slow down.

And if you’re thinking about selling, that’s a trend worth paying attention to.

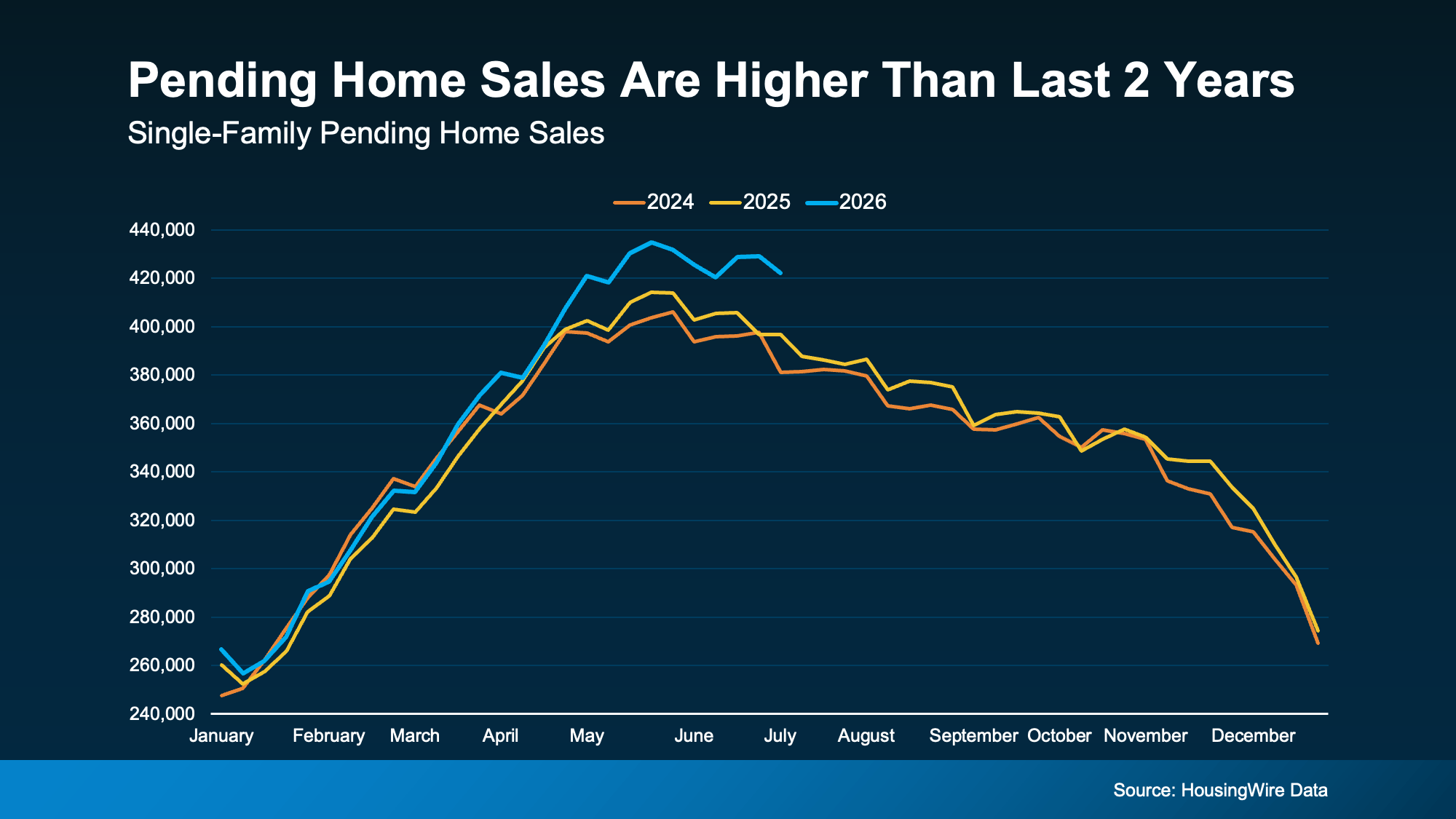

Buyers Are More Active Than You Think

One of the best ways to measure buyer demand is by looking at pending home sales. Those are homes that have gone under contract but haven’t closed yet. Think of them as a real-time pulse check on the market and whether buyers are still buying.

HousingWire Data shows more homes are going under contract than at the same time the past 2 years (see graph below):

While it may come as a surprise, the numbers speak for themselves. It doesn’t mean buyers are everywhere, but it does mean they’re still active right now. And even if this ebbs and flows a bit in the weeks ahead, right now we’re still ahead of where we’ve been lately. That’s encouraging news if you’re thinking about selling because it tells us something important…

People haven’t stopped buying homes. Serious buyers are still making moves.

And a lot of these people are buying because they decided they can’t keep waiting. Whether it’s a growing family, a new job, retirement, or simply wanting a different home, life keeps moving… even when mortgage rates stay higher than we’d like. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“A late spring buyer rush—even with mortgage rates not budging—is an indication of pent-up housing demand and consumers’ acceptance of above-6% mortgage rates as the new normal.”

So, if you’ve been worried no one’s buying, this data should give you some confidence. Today’s buyers aren’t just casually browsing open houses on a Sunday afternoon, they’ve spent months waiting for rates to improve and now they realize they can’t wait anymore.

That means they have a purposeand a timeline. And that’s exactly the kind of motivated buyer you want to work with.

What This Means for Your Sale

Does that mean every house will sell instantly? No.

Today’s market is more balanced than it was a few years ago. So, you can’t just price your house however you want or skip preparing it for the market.

Now buyers have choices, and they’re willing to wait for the right home at the right price. But sellers who understand today’s market (and price and position their homes right) are still finding success. Because the idea that “no one’s buying right now” just isn’t supported by the data.

The buyers are there.

The opportunity is there.

The key is having the right strategy to capture it.

Bottom Line

This year’s housing market may be moving slower than many of us hoped. But, buyer demand is more resilient than the headlines suggest.

If you’re wondering whether there are enough buyers for your house, connect with a local agent. They can show you what’s happening in your local market and build a strategy that helps you take advantage of the momentum that’s already here.

Negotiations are back. More buyers are asking for better deals, and more sellers are giving them. Builders are throwing in extras, too.

That’s why whether you’re buying or selling today, there are two terms you’ll hear a lot: concession and incentive.

-

A concession is something a seller agrees to during negotiations to get a deal done.

-

An incentive is a perk a builder (or a seller) advertises upfront to attract buyers.

Let’s run through what you need to know about both and how they could play a role in your move.

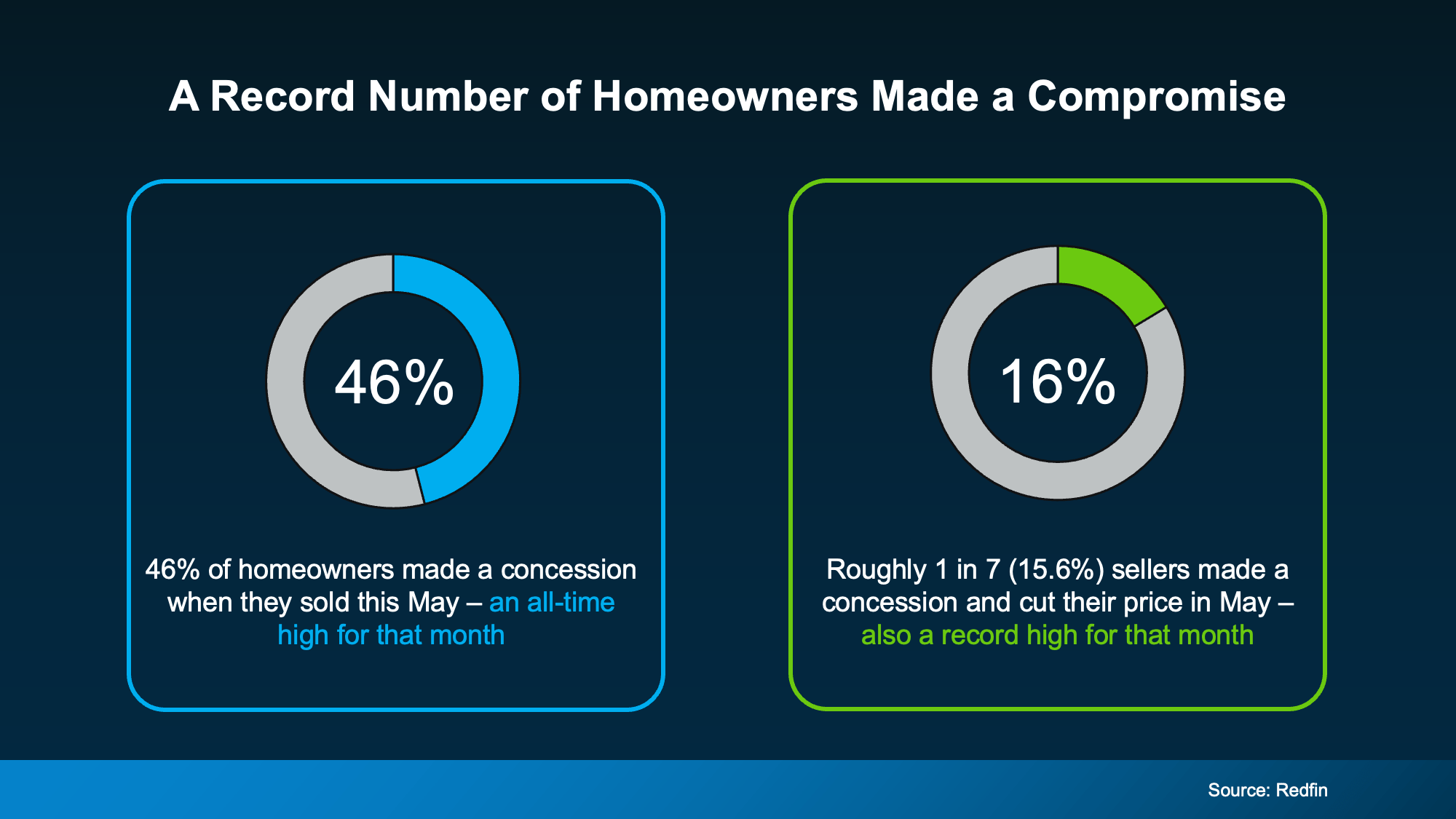

More Sellers Are Agreeing to Concessions

Almost half (46%) of homeowners who sold recently gave the buyer a concession, according to Redfin. That’s the highest share on record for this time of year. And roughly 1 in 7 (16%) sellers went a step further, cutting their asking price and offering a concession on top (see chart below):

So, what kind of concessions are we talking about?

A seller might cover part of your closing costs, take care of a repair, or offer a credit that trims your upfront costs. It’s how they keep a deal on track when buyers have more options to choose from – and homeowners aren’t the only ones compromising.

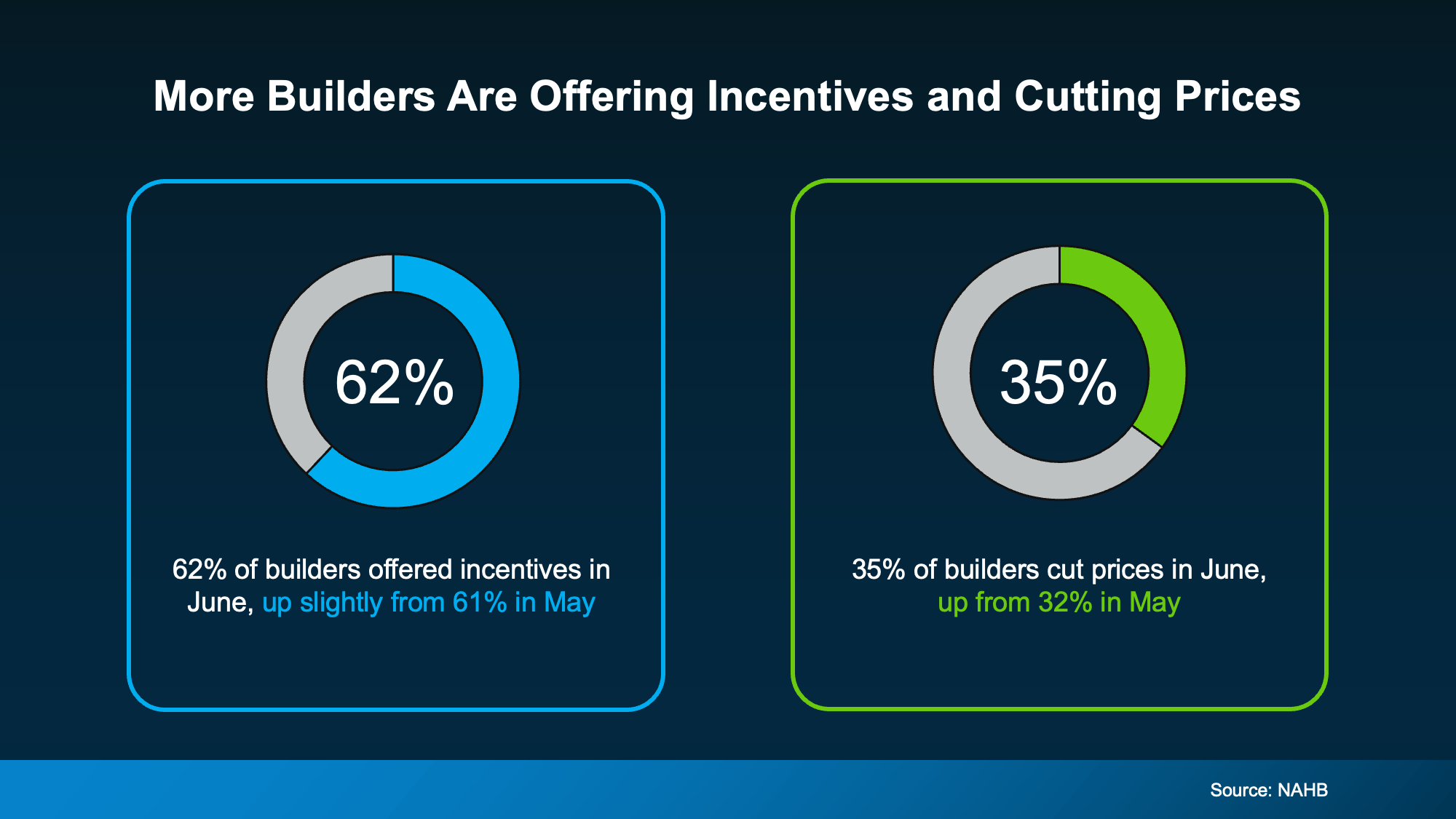

Builders Are Cutting Prices, Too

Newly built homes are seeing the same push and pull. According to the National Association of Home Builders (NAHB), 62% of builders are offering incentives right now. And about 35% are cutting prices outright (see chart below):

Those incentives often look like:

-

Mortgage rate buydowns

-

Free upgrades, like nicer finishes or appliances

Danielle Hale, Chief Economist at Realtor.com, explains why:

“New construction has been one of the steadiest parts of the housing market over the past few years, but builders are clearly responding to today’s affordability pressures and higher levels of existing-home inventory.”

Even builders, who many people think rarely negotiate, are competing on price and perks. They have been for over a year now. The same data shows this is the 15th straight month where more than 60% of builders have offered incentives to sweeten the deal. And that’s significant.

What This Means for Your Move

If you’re buying, this is a good time to ask. Whether you have your eye on an existing house or a newly built home, there’s a chance the seller or builder will meet you partway on price, terms, or both.

If you’re selling, expect buyers to ask. Even builders of brand-new homes are making concessions more often than not right now. Holding firm on every term could mean more time on the market, or a lost sale altogether.

Bottom Line

Sellers and builders are both giving buyers more to work with this year. A local agent can tell you what to expect in concessions and incentives based on inventory and competition in your local market.

The House That Started It All Could Kickstart What’s Next

Priced Out? A Condo or Townhome Could Be Your Way In.

More Homes, Better Prices: A Buyer’s Summer

-

Equity3 weeks ago

Equity3 weeks agoThe Housing Market Is Stronger Than You Think

-

Economy3 weeks ago

Economy3 weeks agoWhat Buying or Selling a Home Gives Back to Your Community

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThe 1 Factor That Explains Everything Happening with Home Prices Right Now

-

Affordability3 weeks ago

Affordability3 weeks agoDown Payments Are Smaller Than They’ve Been Since 2021

-

Affordability2 weeks ago

Affordability2 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoStudent Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

-

For Sellers1 week ago

For Sellers1 week agoThink Nobody’s Buying Homes Right Now? Think Again.

You must be logged in to post a comment Login