Economy

Two Reasons Why the Housing Market Won’t Crash

You may have heard chatter recently about the economy and talk about a possible recession. It’s no surprise that kind of noise gets some people worried about a housing market crash. Maybe you’re one of them. But here’s the good news – there’s no need to panic. The housing market is not set up for a crash right now.

Real estate journalist Michele Lerner says:

“A housing market crash happens when home values plummet due to a lack of demand for homes or an oversupply.”

With that definition in mind, here are two reasons why this just isn’t on the horizon.

1. Demand for Homes Is Higher than Supply

One of the biggest reasons the housing market crashed back in 2008 was an oversupply of homes. Today, though, it’s a very different story.

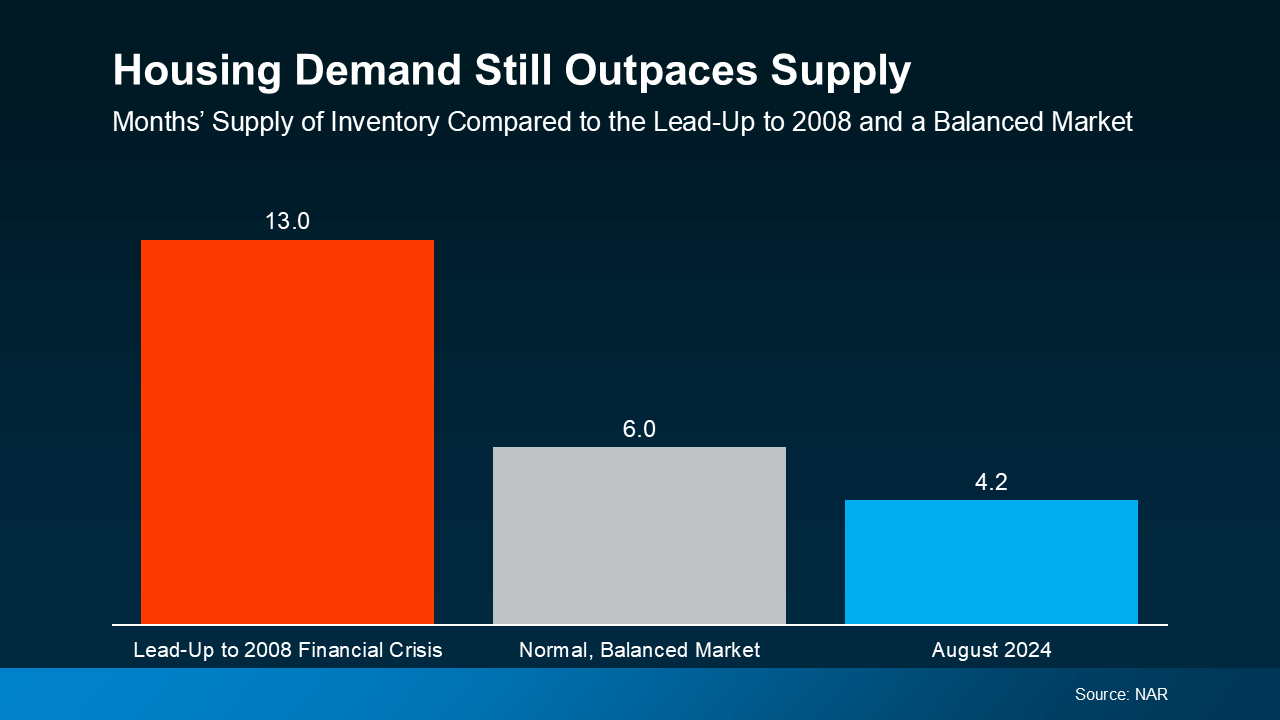

It’s a general rule of thumb that a market where supply and demand are balanced has a six-month supply of homes. A higher number means supply outpaces demand, and a lower number means demand outpaces supply. The graph below uses data from NAR to put today’s situation into context:

The graph compares housing supply during three different periods of time. The red bar shows there were 13 months of supply before the 2008 crisis, which was far too much. The gray bar shows a balanced market with six months of supply, for context. And the blue bar shows there are only 4.2 months of supply today.

The graph compares housing supply during three different periods of time. The red bar shows there were 13 months of supply before the 2008 crisis, which was far too much. The gray bar shows a balanced market with six months of supply, for context. And the blue bar shows there are only 4.2 months of supply today.

Put simply, there are more people who want to buy homes than there are homes available to buy right now. So, demand is greater than supply. When that happens, home prices stay steady or rise – the opposite of a housing market crash.

It’s important to note that inventory levels differ from market to market. Some areas may be more balanced, while a few could have a slight oversupply, which can impact prices locally. However, most markets continue to experience a shortage of homes.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

2. Unemployment Is Still Low

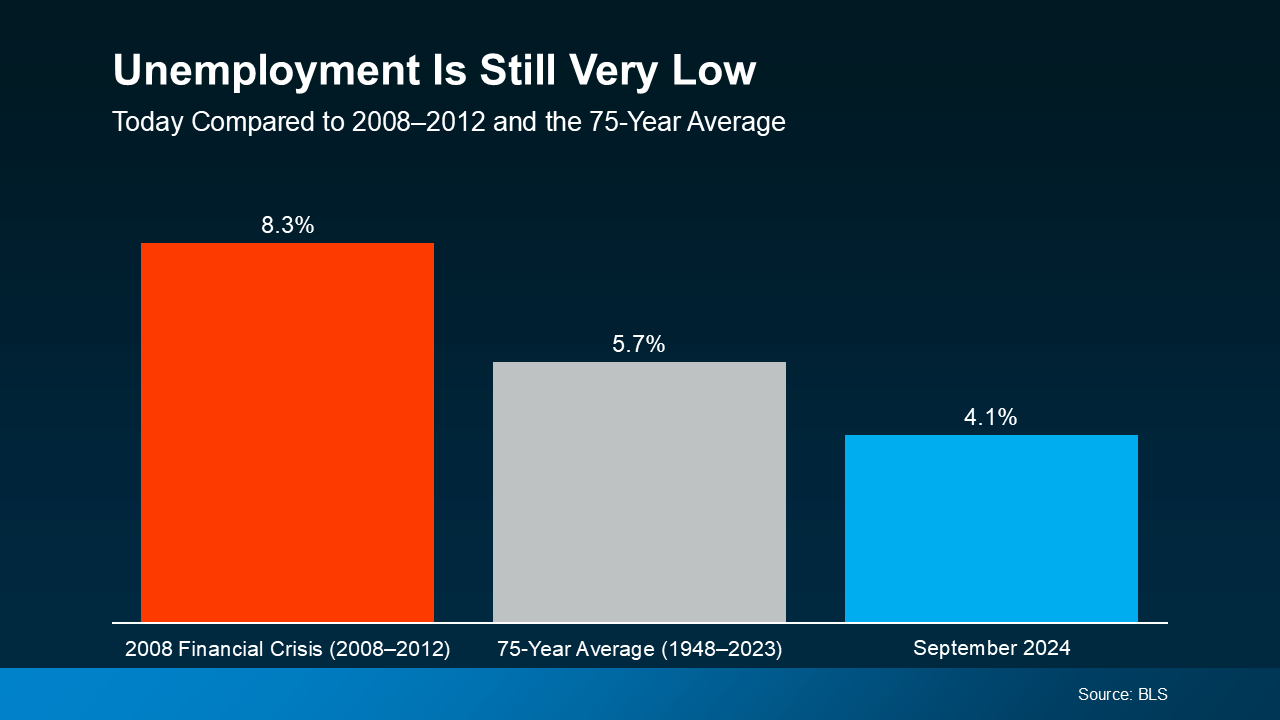

When people are unemployed, they’re more likely to have trouble making their mortgage payments and may be forced to sell or face foreclosure. That was a big problem during the 2008 financial crisis. Today, the employment situation is much more stable (see graph below):

Again, this graph shows three different periods of time, but this one is the unemployment rate. The red bar represents the 2008 financial crisis when unemployment was very high at 8.3%. The gray bar shows the 75-year average of 5.7%. And the blue bar shows the unemployment rate today, and it’s much lower at just 4.1%.

Again, this graph shows three different periods of time, but this one is the unemployment rate. The red bar represents the 2008 financial crisis when unemployment was very high at 8.3%. The gray bar shows the 75-year average of 5.7%. And the blue bar shows the unemployment rate today, and it’s much lower at just 4.1%.

Right now, people are working, earning an income, and making their mortgage payments. That’s one reason why the wave of foreclosures that happened in 2008 isn’t going to happen again this time. Plus, since so many people are employed right now, many are actually in a position to buy a home, and this demand keeps upward pressure on prices.

Today’s Housing Market Is Stronger than in 2008

While it’s understandable to be concerned when you hear talk of a recession and economic uncertainty, but know this: the housing market is in a much better place than it was in 2008. According to Rick Sharga, Founder and CEO at CJ Patrick Company:

“Literally everything is different about today’s housing market dynamics than the conditions that led to the housing crisis.”

Demand for homes still outpaces supply, and unemployment remains low. And these are two key factors that will help prevent the housing market from crashing any time soon.

Bottom Line

The housing market is in a much better place than it was in 2008, but it’s important to remember that real estate is very local.

So, it’s always a good idea to stay informed about your specific market. If you have any questions or want to discuss how these factors are playing out in your area, reach out to a local real estate agent.

Data shows inflation is moving in the wrong direction. But before the headlines send anyone into a panic, here’s what’s actually going on, why it matters for the housing market, and what it means if you’re thinking about buying or selling.

Inflation Went Up – Here’s What That Actually Means

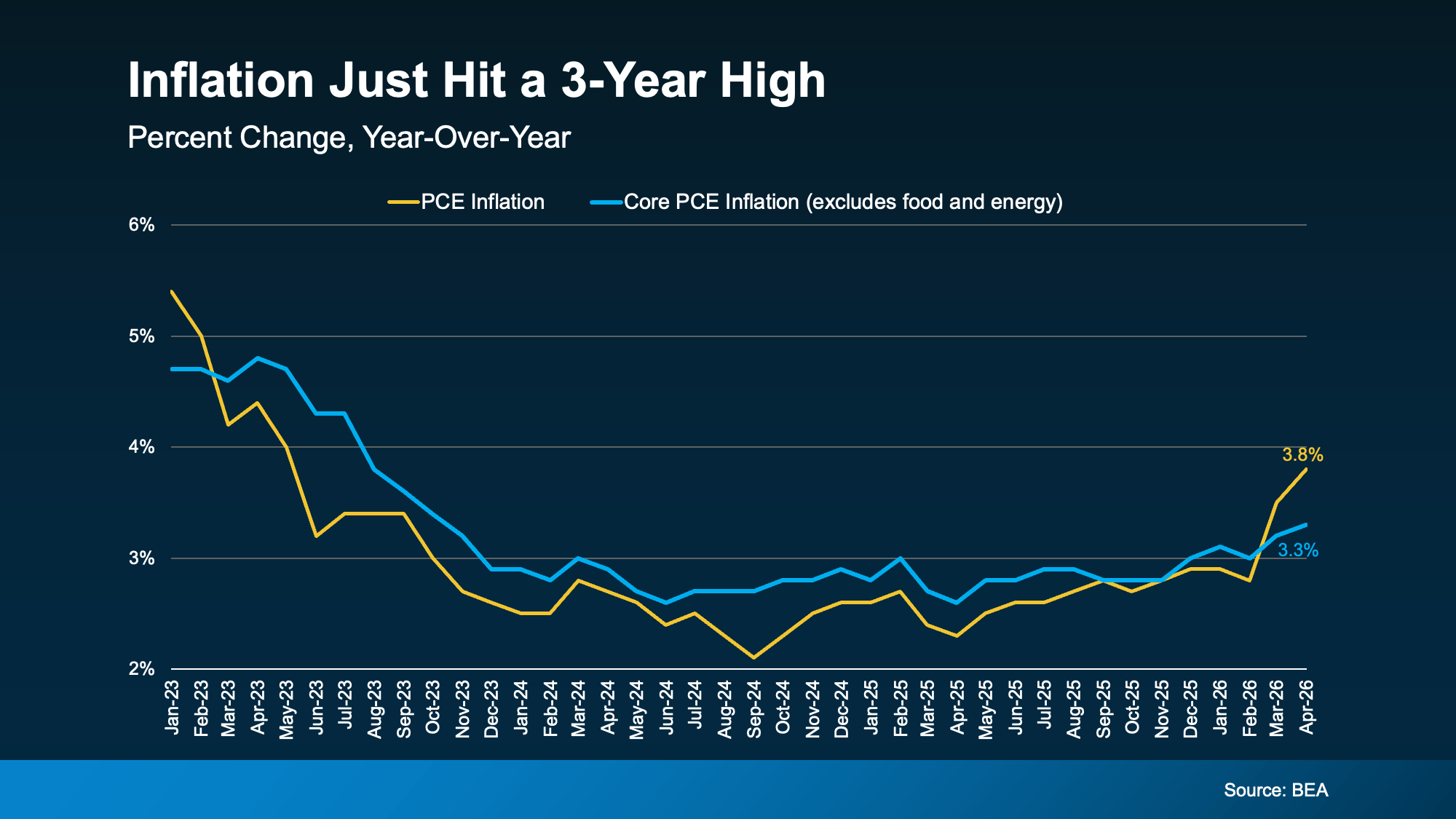

The government tracks inflation in a variety of ways. One is something called PCE – the Personal Consumption Expenditures Price Index. It measures how much more (or less) people are paying for goods and services compared to a year ago. And just based on your own expenses, you can probably guess which way that’s trending.

That’s the one everyone is talking about right now. Check out the yellow line to see how that’s spiked since February (see graph below). A big driver of this jump is the ongoing conflict in the Middle East, which has pushed gas and energy prices significantly higher.

Now, you may have noticed there’s a second line. The blue line shows core PCE. That’s the same measure, but with gas and energy prices stripped out. The Federal Reserve (the Fed) actually watches this number most closely because energy prices swing around a lot and can be misleading.

And here’s the somewhat encouraging part.

Core PCE is rising, but not nearly as fast as the overall number. That suggests a good chunk of the inflation spike we’re seeing right now is tied directly to what’s happening overseas. So, when that situation settles down, inflation may settle a bit, too.

Why This Matters for Mortgage Rates

Here’s the housing connection. When inflation is high, the Fed tends to keep the Federal Funds Rate elevated or even raise it to try to taper spending and cool inflation back down. And while it’s not a one-for-one relationship, that Federal Funds Rate can have an impact on your mortgage rate when you buy.

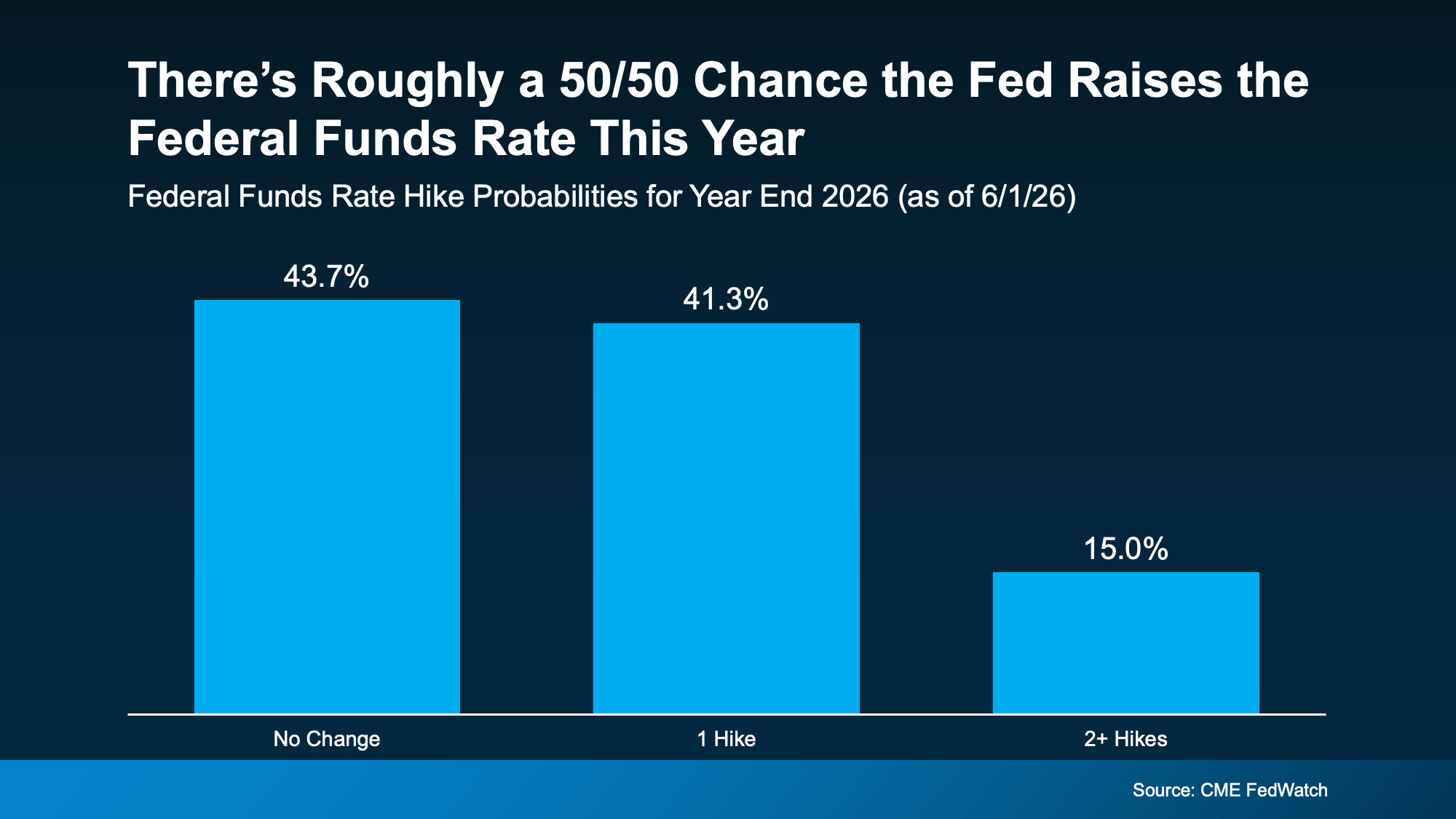

Right now, based on the information we have, there’s roughly a 50/50 chance the Fed actually raises the Federal Funds Rate before the end of 2026, according to CME FedWatch (see graph below):

While it’s too soon to say where this goes for certain and if we’re headed for a rate hike, it does mean mortgage rates are probably not coming down as soon as most people were hoping.

If you’ve been waiting for rates to drop significantly before making a move, this report is a reminder that “higher for longer” is still very much on the table. It really all depends on where the economy goes from here. According to Bankrate:

“Oil prices and bond yields have dropped a bit . . . but they’re still way up compared to the start of spring. Until there’s a resolution to the war, look for both inflation and mortgage rates to stay high.”

But This Is Not 2008 – Not Even Close

Just remember, a tough economy does not equal a housing crash. The conditions today are very different from what led to the 2008 collapse. Here’s why:

-

Inventory is still relatively low. There’s no flood of homes hitting the market.

-

Most homeowners today have strong equity in their homes.

-

Lending standards are far stricter than they were before 2008.

-

Today’s challenge is affordability, not a wave of distressed underwater sellers.

Uncomfortable and unhealthy are not the same thing. The market feels hard right now, but “hard” and “crashing” are very different.

You Still Have Options. Here’s What To Do.

High rates don’t mean homeownership is out of reach. It just means the path looks a little different. There are real strategies that can help, depending on your situation:

-

Ask your lender about different loan options. Adjustable-rate mortgages (ARMs) or rate buydowns may help lower your monthly payment in the short term.

-

Explore first-time buyer programs, down payment assistance, or seller concessions that could help offset costs.

-

Stay in close touch with a trusted agent and lender. When rates shift, and they will, you’ll want to be ready to move fast.

The right strategy, tailored to your goals, matters a lot more than waiting for the perfect moment that may never come.

Bottom Line

Inflation is still above where the Fed wants it, and that means mortgage rates are likely to stay elevated for a while. But for people who need to move, strategy matters far more than trying to perfectly time the market.

Wondering what this means for your specific situation? Connect with a local agent or lender.

If the housing market feels confusing right now, you’re not alone.

Mortgage rates have risen. Home sales haven’t picked up like expected. And many buyers and sellers are wondering when things are going to feel easier or be more affordable.

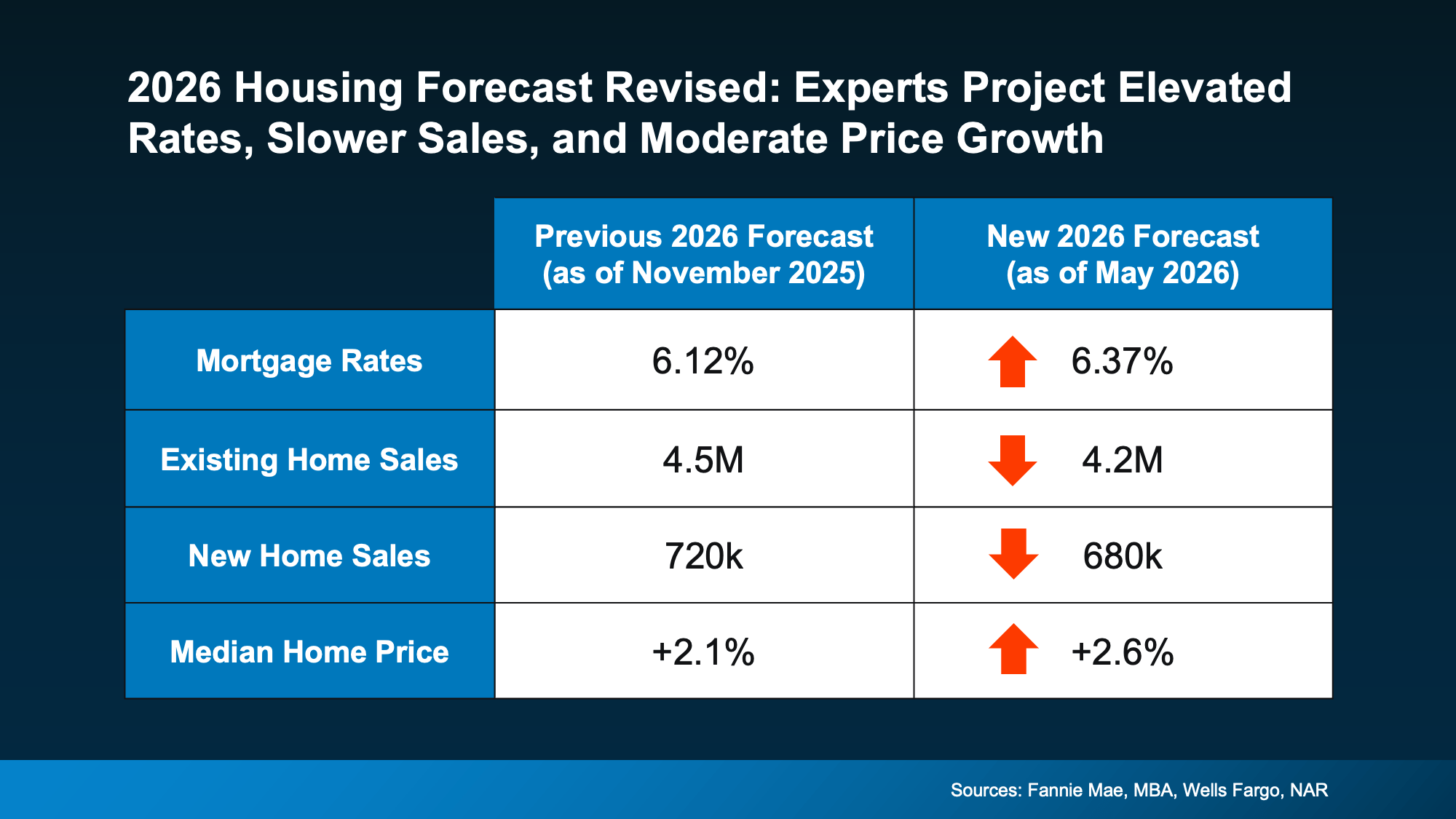

The truth is: a lot changed over the first half of this year.

Back at the end of 2025, economists were forecasting a much stronger housing market for 2026. They expected mortgage rates to come down, affordability to improve more dramatically, and home sales to rebound.

But lingering inflation, economic uncertainty, and growing geopolitical tensions overseas pushed mortgage rates higher than expected. And because rates stayed elevated for longer, many buyers continued to hold off.

That’s why experts recently revised their housing forecasts for the rest of the year (see graph below):

So, what does this actually mean for you? Let’s break it down.

Mortgage Rates May Remain Elevated

While just about everyone wants mortgage rates to go back to the uppers 5s or low 6s we saw at the start of the year, as of right now, the experts don’t think that’s likely to happen this year.

Instead, forecasts have been updated from the low 6s they originally projected. Many industry organizations are saying rates will stay in roughly the mid 6s this year. The good news is, that’s still lower than rates were a year ago.

Of course, this is based on what we know today. If the conflict overseas comes to an end or inflation drops, this could change. But if you’re waiting for lower rates, it may not pay off in the way you expect.

Existing Home Sales Revised Lower

Back in late 2025, experts expected we’d sell an average of 4.5 million homes this year. Now? That’s dropped down a bit to 4.2 million.

That tells us something important: buyers are still hesitant because affordability remains challenging.

Higher mortgage rates have made monthly payments harder to manage, especially for first-time buyers. And that’s slowed the pace of the market compared to what was originally expected. But even though the forecast was revised down, we’re still expected to sell more homes than last year.

Once geopolitical tensions resolve and rates begin to settle down, many experts believe that group of buyers will be ready to jump back in. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

There has already been a few glimmers of renewed hope lately. In recent months, pending homes sale have been improving month-over-month despite higher rates.

So, if you’re able to afford a home at today’s rates, it could still make sense to buy now. Because otherwise, if you wait, you’ll have more competition (and potentially fewer homes to choose from) when those others buyers jump back in.

New Home Sales Also Slowed

Builders also expected to have a stronger year. Earlier forecasts projected new home sales would top 700k in 2026. Now, economists expect we’ll be just shy of that number.

Again, mortgage rates are a major reason why.

But the upside for buyers is that builders may be even more motivated to sell. That means builder incentives, negotiation opportunities, and pricing flexibility may continue in many markets. So, if you live somewhere where there’s more new construction, this may actually be a bright spot for you.

Builders could be more ready to negotiate, and that gives you more leverage to get a better deal.

Home Prices Are Still Expected To Rise

This is one of the most important takeaways from the entire forecast. Even though sales activity is slower, on average, experts did not revise their home price forecast downward.

They still expect prices to rise nationally this year.

Why? Because while buyer demand has softened, the number of homes for sale is still relatively limited overall. That imbalance is helping support prices, even in a slower market.

Of course, conditions vary depending on where you live. Some markets are cooling more than others. But nationally, experts are still projecting steady price growth — not a major decline. And that should be a comfort whether you’re buying or selling.

Because sellers don’t want a major drop in prices. And while buyers may think they do, generally you feel better about a big purchase when it doesn’t depreciate right away.

Bottom Line

The housing market hasn’t rebounded as quickly as experts originally hoped. But that doesn’t mean it’s stalled.

Higher inflation and lingering economic uncertainty caused economists to revise their forecasts for this year. But importantly, when those two things settle down, many experts believe the market will regain its momentum.

So don’t see this revision in forecasts as a sign of trouble. See it as a temporary reaction to overall conditions and uncertainty.

If you want to know what’s happening in your local market, and what it could mean for your plans for the rest of this year, talk to a local agent.

Let’s be real with each other for a second about affordability. Because you deserve someone who will be honest and transparent about what’s going on, especially if you’ve got a move on your mind.

Here’s the full picture of what’s happening and why. The good – and the bad. So, you know what it truly means for your move. Because while rates are certainly a big part of affordability, they’re not the only factor at play.

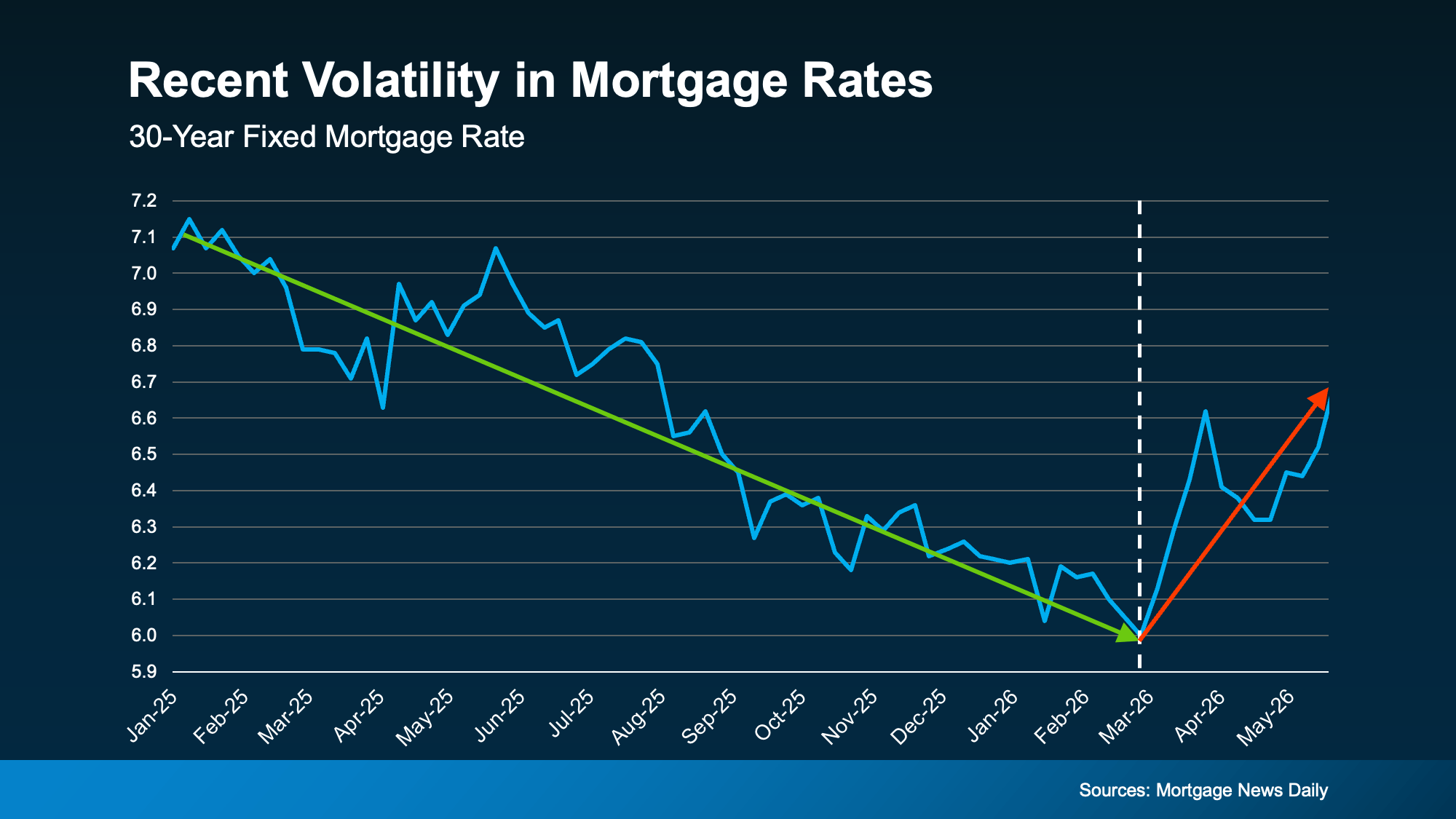

Mortgage Rates Have Been Rising

After a year or more of rates trending down, they’ve started to climb again. And, if you’re looking to buy, that’s not what you want to see. But it has happened. And here’s why.

Uncertainty is the enemy of mortgage rates.

And with lingering global uncertainty, ongoing tensions in the Middle East, and inflation refusing to fully cool off, there’s a lot that’s having an effect on rates. Colin Robertson, Founder of The Truth About Mortgage, put it plainly:

“You can’t have $100 a barrel oil and not expect inflation to rise, which translates to higher bond yields and mortgage rates.”

Take a look at the graph below. It uses data from Mortgage News Daily to show just how much all of those factors have had an impact:

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s possible. But it all depends on how the ongoing geopolitical conflict plays out and whether inflation continues to run hot afterwards – and for how long.

Rates probably aren’t heading down until both of those things improve. And even when that does happen, experts agree rates likely won’t be dramatically lower – maybe in the low to mid-6s. That’s the reality, and it’s worth knowing.

So, should you wait for lower rates? The general consensus is, if you can afford to buy and you find a home you like, it’s still worth it. Because no one knows for sure when rates will start to come back down – and how long do you really want to put your life on hold?

Wages Are Outpacing Home Prices

You’ve probably heard that inflation is making everything more expensive, and there’s no shortage of headlines about the cost-of-living outpacing paychecks. It’s a legitimate concern. And maybe you’re feeling the pinch yourself. But here’s what doesn’t make the headlines. It’s not all bad news.

Data from the Federal Reserve Bank of Atlanta and Redfin shows wages have actually been growing faster than home prices.

-

Recently, wages have been increasing at around 4% year-over-year.

-

And home price growth is closer to 2% year-over-year.

As a buyer, you want your income to rise faster than prices because that helps make your purchase more manageable financially, and it quietly chips away at the affordability challenge over time. That’s exactly what we’re seeing lately. And every little bit is going to help.

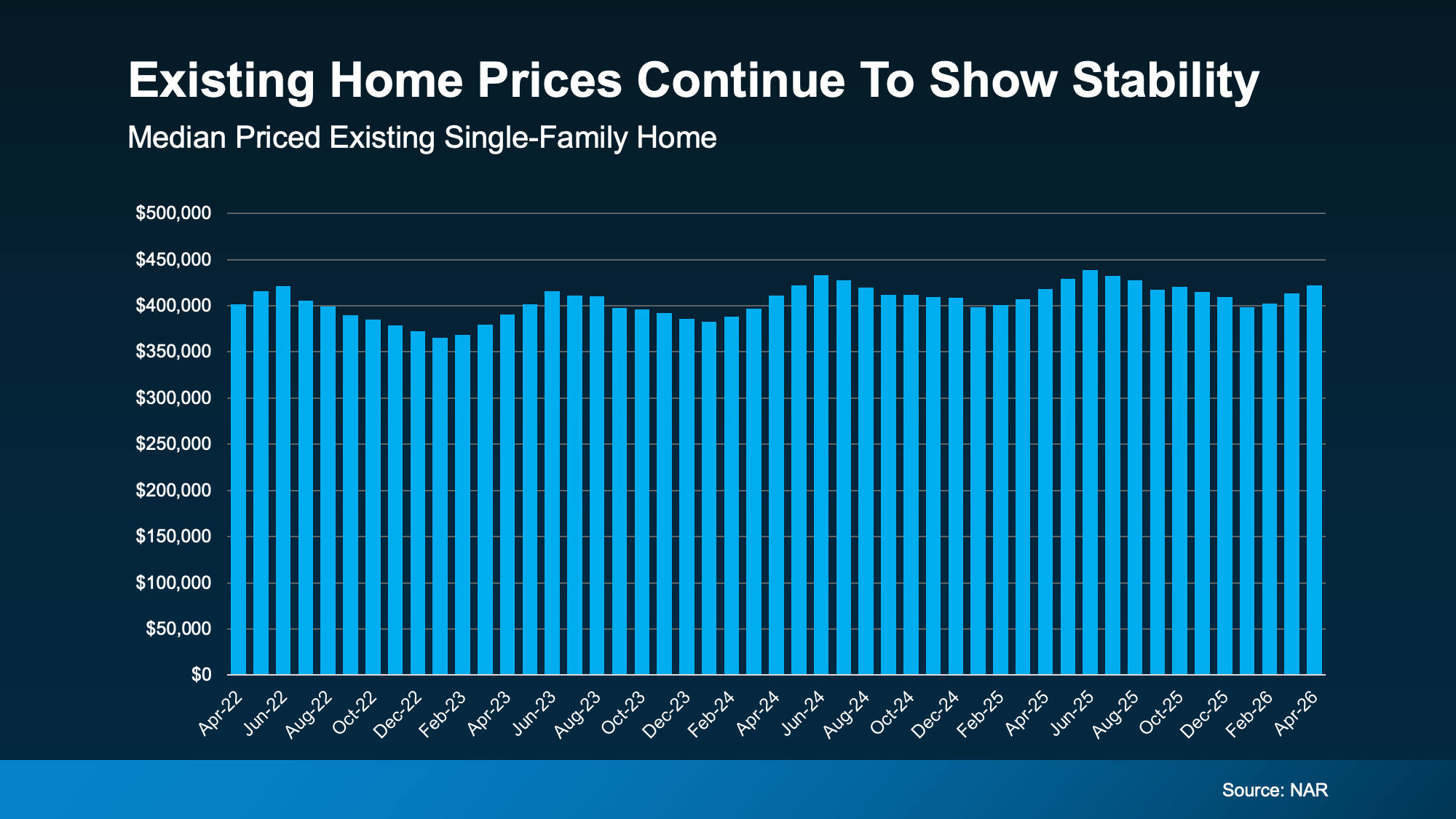

A big reason wages have been gaining ground on home prices? Home prices have actually stayed pretty steady.

Existing Home Prices Have Held Steady

Check out the graph below. It shows home price data from the National Association of Realtors (NAR) over the past 4 years. Notice anything? There’s been no dramatic runup, and no crash either. Just relative stability and slow growth:

Part of what’s keeping prices this stable is that buyers finally have more choices. That means less competition, more negotiating power, and more time to find the home that actually fits your life, not just the one you had to grab before someone else did.

And that gives you a chance to hopefully find something that works for your budget, even with today’s rates. At the same time, you’re not losing ground pricewise while you take time to make a careful decision.

Bottom Line

Yes, rates have been volatile, and global instability is keeping them from settling down anytime soon. There’s no sugarcoating that. But the full picture of affordability is more nuanced than the headlines suggest.

Want to run the real numbers for your situation? Talk with a local real estate agent. They’d love to show you what’s actually possible in today’s market. Reach out to set up a quick, no-pressure conversation.

Should You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

Two Big Reasons To Move This Summer

Lower Asking Prices Are a Win for Today’s Buyers

-

Equity4 weeks ago

Equity4 weeks agoRecord High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out.

-

Equity4 weeks ago

Equity4 weeks agoAre Home Prices Going To Fall?

-

Affordability4 weeks ago

Affordability4 weeks agoNewly Built Home Prices Hit a 5-Year Low

-

Affordability3 weeks ago

Affordability3 weeks agoWhat Most Veterans Don’t Know About Their VA Home Loan Benefit

-

Affordability3 weeks ago

Affordability3 weeks agoThe Truth About Affordability Today

-

Affordability2 weeks ago

Affordability2 weeks agoWhat Rising Inflation Means for Your Move

-

For Sellers3 weeks ago

For Sellers3 weeks agoThe Real Reason Some People Are Still Moving Right Now

-

Economy2 weeks ago

Economy2 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

You must be logged in to post a comment Login