Agent Value

Why an Agent Is Essential When Buying a Newly Built Home

For some buyers, there’s a misconception that newly built homes aren’t made to last or fall short of the quality you can find in older homes. Unfortunately, this is turning some buyers away from what may be one of their best options in today’s housing market. As Builder Online says:

“As resale inventory remains limited and the price spread between new and resale homes narrows, new homes are increasingly an attractive value proposition for buyers, with incentives such as rate buydowns a way to help address ongoing affordability challenges.”

So, is there any merit to the myth? Let’s break down the best way to make sure you feel good about looking into new home construction. That way, you’re not missing out on such a great option today.

Choosing the Right Builder

The key to making sure you get a quality newly built home is to choose a good builder. Reputable builders adhere to strict building codes and standards, use advanced construction techniques, and often offer warranties that cover structural issues for several years. That’s why the Mortgage Reports offers this advice:

“When embarking on the journey of buying a new construction home, one of the most important steps is selecting the right builder. This decision can significantly impact the quality and satisfaction you derive from your new home.”

And while you could dig into research about all the builders in your area, there’s an easier option to get the job done: lean on a pro. When you work with a local real estate agent, they already know about the builders and the new home communities under construction in your area.

Beyond that, maybe they’ve even worked with other buyers who opted for a home in one of those neighborhoods. Here are just a few of the things your agent will help you with:

1. The Builder’s Reputation: Your agent will help point you toward builders with strong reputations and positive reviews from previous buyers. Additionally, your agent will make sure the builder is licensed and insured. Membership in professional organizations, such as the National Association of Home Builders (NAHB), is also a good sign of a builder’s commitment to industry standards.

2. Their Model Homes: Your agent will also be able to tell you if the builders have model homes you can tour. And when your agent walks through the model with you, they’ll draw your attention to the little details that matter most. Things like the quality of finishes, layout, and overall feel of the home.

3. Builder Warranties: Your agent will also be able to help you navigate any builder offers or incentives. Reputable builders often provide warranties to cover major structural elements of the home for a significant period of time. This is a testament to their confidence in the quality of their construction.

4. Getting Inspections: Even with new homes, inspections are crucial. Your agent will coordinate the inspections with licensed professionals to ensure the home meets safety and quality standards before you move in.

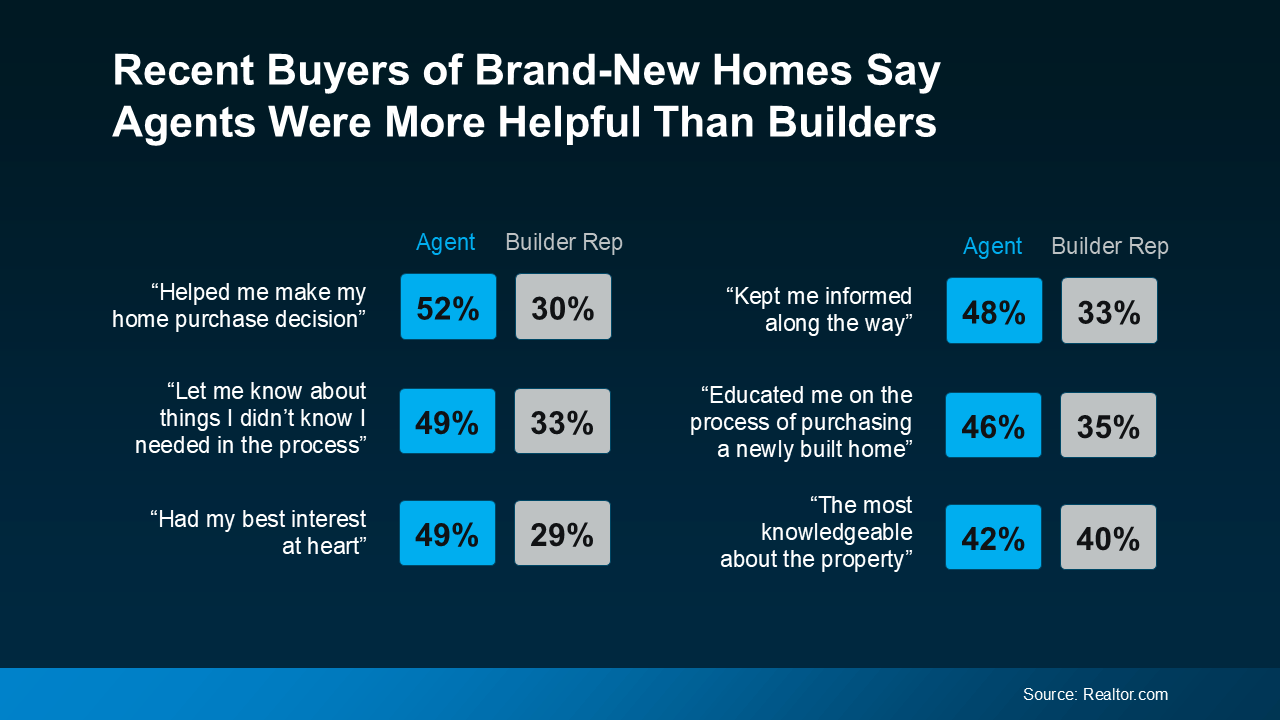

Agents Are the MVP When You’re Buying a Brand-New Home

Maybe that’s why data shows homebuyers unanimously scored their agents higher than their builders when looking back on their recent purchase:

So, you don’t need to worry that they just don’t make them like they used to. By working with a knowledgeable real estate agent to choose a reputable builder, you can feel confident when buying a newly built home today. As Realtor.com says:

So, you don’t need to worry that they just don’t make them like they used to. By working with a knowledgeable real estate agent to choose a reputable builder, you can feel confident when buying a newly built home today. As Realtor.com says:

“If you are interested in buying a new construction . . . You need your own real estate agent from the get-go. Even if it seems like plug and play to sign up with the builder’s on-site agent, you’re going to want someone representing your side of the deal.”

Bottom Line

If you’re considering buying a brand-new home, don’t let misconceptions hold you back. Work with a local real estate agent to find a home you’ll love and be proud to call your own.

Whether you’re dreaming about buying your first home or wondering if it’s time to move on from the one you’re in, affordability is probably weighing on your mind. Home prices are still high in many markets, and even though things have improved a bit over the past year, making the numbers work can still feel like a stretch.

But the people finding ways to move right now usually have one thing in common. They didn’t wait for affordability to come to them. They went looking for it.

According to PODS, 61% of people across all generations say affordability is the biggest factor when deciding where to move. And it’s led a growing number of people to do one thing – broaden their search to include more affordable areas they hadn’t seriously considered before. As PODS, put it:

“. . . moving is increasingly driven by affordability, connection, and quality of life. As economic pressures persist, Americans are taking a more intentional, values-driven approach to where they choose to live.”

It’s Not Just the Home Price – It’s the Whole Cost of Living

Here’s where it gets really interesting. When people talk about moving for affordability, they’re not just talking about finding a cheaper house. They’re thinking about the full picture. What does it actually cost to live somewhere?

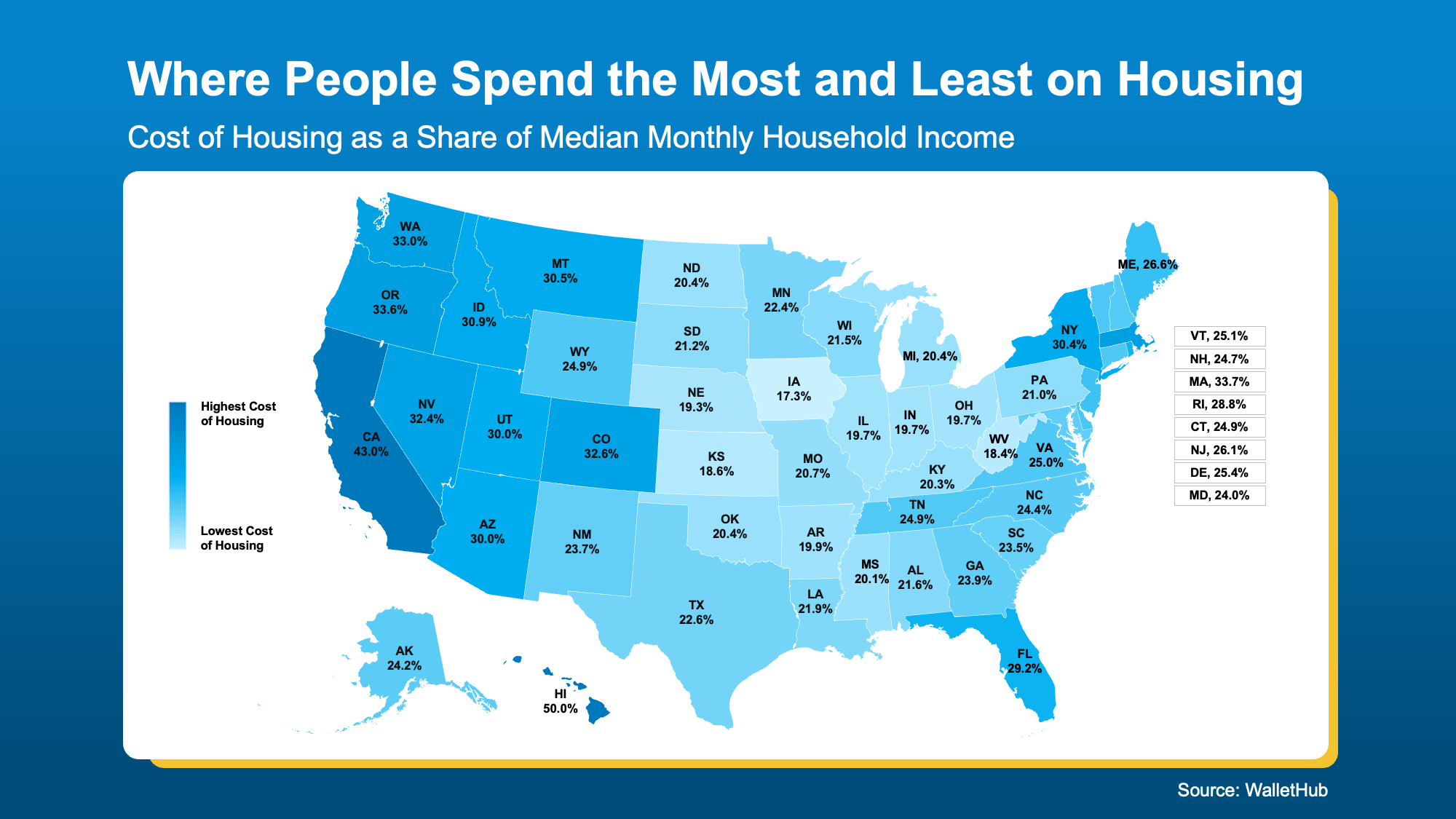

WalletHub looked at exactly this, measuring housing costs as a share of median monthly household income across every state (see map below).

Take a look at where you live on that map. The lighter the blue, the more affordable it generally is to live there. The darker the blue? Just the opposite.

If your state is showing up on the darker blue end of the scale, the cost of living may be putting a real pinch on your wallet, and it may be worth exploring what a lighter-blue area could mean for your finances.

Because if you’re less financially stretched, imagine how that could change things. Less stress. Less worry. More freedom and peace of mind.

You Don’t Have To Move to Another State To Find a Better Deal

But finding more affordable homeownership doesn’t have to mean a cross-country move. It doesn’t even have to mean leaving your state, your family, or your favorite coffee shop behind.

Every market has more affordable pockets that most buyers never think to explore – neighborhoods, towns, and communities where home prices are lower, property taxes are more manageable, and the overall cost of living just works better.

A great local real estate agent knows exactly where those places are.

And if you work remotely, or have any flexibility in where you’re based, your options open up even further. Remote work has already changed the way millions of people think about where to live, and that trend isn’t going away.

When location stops being tied to a daily commute, a more affordable area that’s a bit farther out suddenly becomes a very real option.

Bottom Line

Affordability is a real challenge, but it’s not an unsolvable one. The key is being open to places you might not have considered before. A local real estate agent can help you find them.

Ready to find out which areas have the best affordability right now? Reach out today.

Most sellers come into the market with one number in mind. And it’s often the one that costs them the most. That’s their asking price.

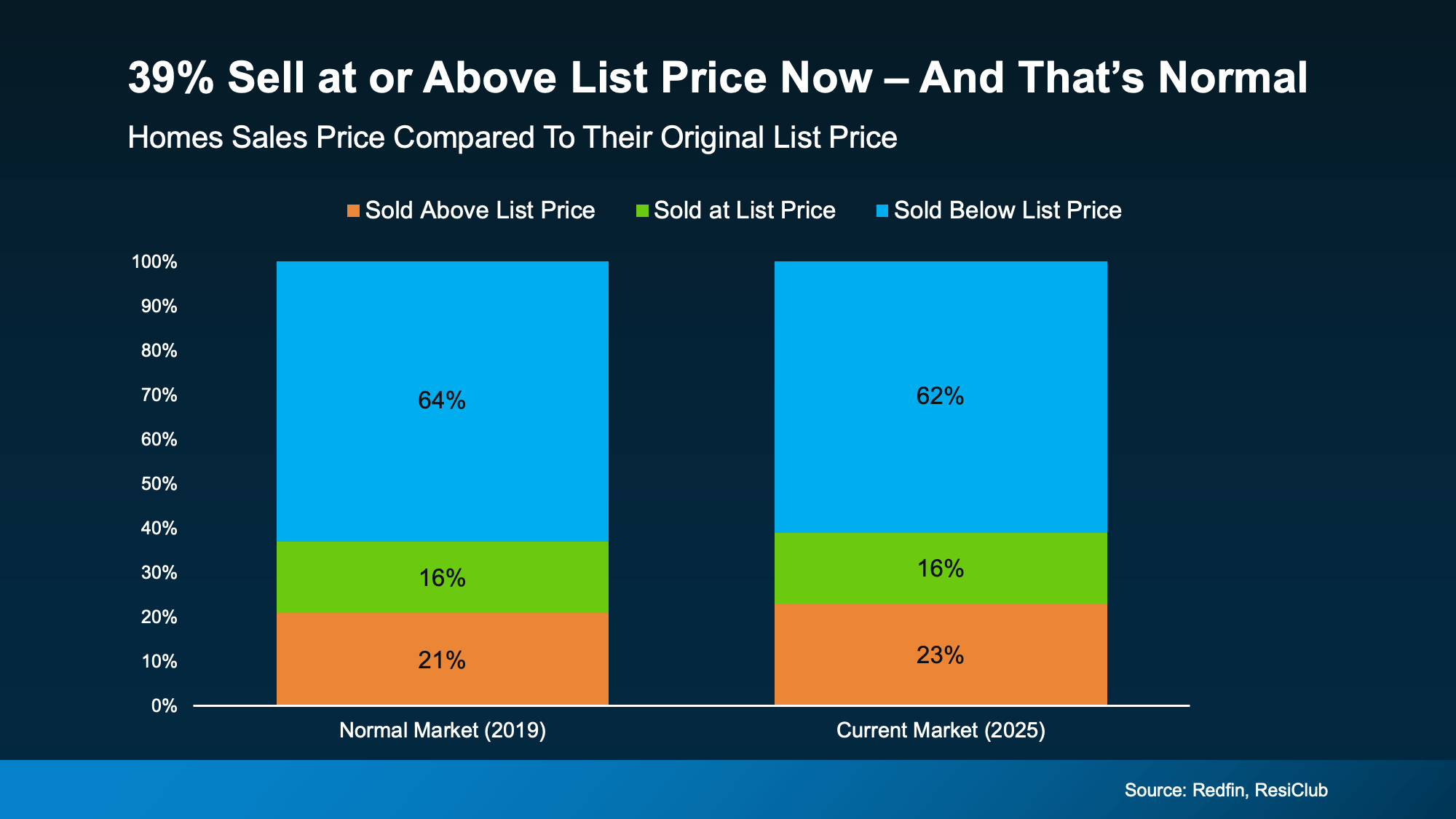

A survey from Realtor.com shows about 8 in 10 (80%) of sellers expect to sell at or above their asking price today. But here’s where things get interesting.

In reality, only about 4 out of every 10 (roughly 40%) actually do.

That’s a big gap. And it’s where a lot of sellers get caught off guard. So, why the disconnect? And how can you set yourself up to be one of the 4 in 10 that get top dollar?

Let’s break it down.

What Should You Really Expect To Get for Your House?

That 40% may sound low at first, but it’s not.

If you look back to the last typical year for the housing market (2019), what we’re really seeing is a return to what’s normal (see chart below). If anything, slightly more homeowners are able to sell above list price today compared to 2019:

It only feels low because the past few years were anything but typical. Between 2020 and mid-2022, buyer demand was sky-high and the number of homes for sale was at record lows. Almost everything sold over asking.

It only feels low because the past few years were anything but typical. Between 2020 and mid-2022, buyer demand was sky-high and the number of homes for sale was at record lows. Almost everything sold over asking.

Now, the market has shifted.

There are more homes for sale. Buyers have more options. And that means they’re more selective about how they spend their money.

In other words, the rules have changed – and pricing like it’s still 2021 is where sellers run into trouble. You have to meet the market where it is if you really want to cash in big.

What Happens When a Home Is Priced Too High

Here’s the reality. It’s easy to think pricing high gives you room to negotiate. But it usually does the opposite.

When your home is priced above what buyers expect, in this market, they don’t negotiate. They move on.

Because buyers notice price first. And if your home doesn’t line up with similar options in your area, it may not even get a showing. And that’s when things start to snowball:

-

A high price gets less interest from buyers.

-

Less interest means fewer offers.

-

And fewer offers usually means more time on the market.

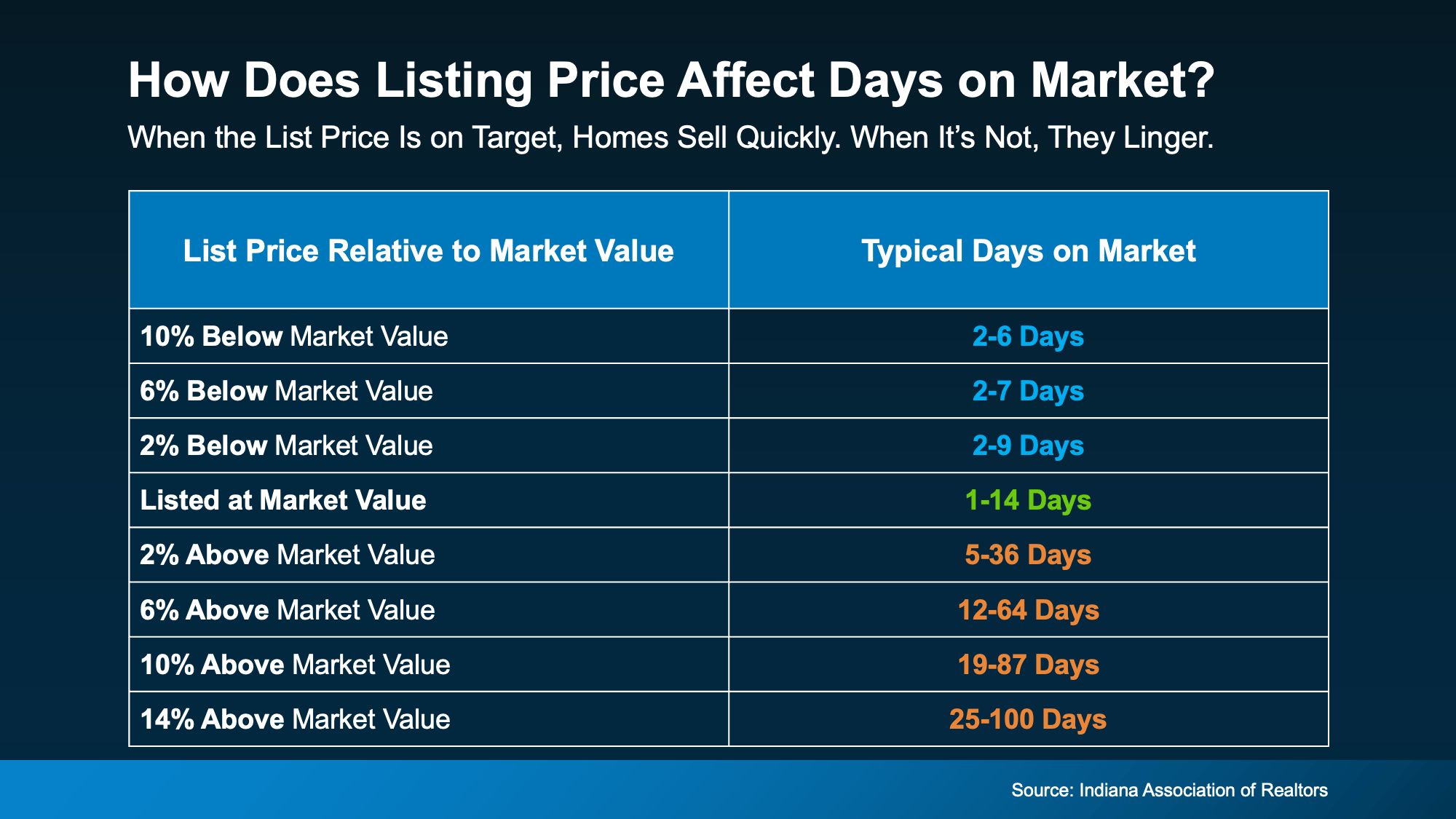

Take a look at this table from the Indiana Association of Realtors. While this data is from one state, the general trend is going to hold true across many markets in the country. It shows that homes listed at or under market value sell fast. But homes priced high? They linger. And that delay comes at a very real cost.

The Price Cut Trap (And How To Avoid It)

The Price Cut Trap (And How To Avoid It)

When a home sits that long without offers, a lot of sellers will do a price reduction. According to Realtor.com, 16.7% of sellers are going that route today.

But here’s the real problem. Even a price cut doesn’t guarantee a sale.

In fact, some buyers will see a reduction as a sign something’s wrong with the house – even when nothing is.

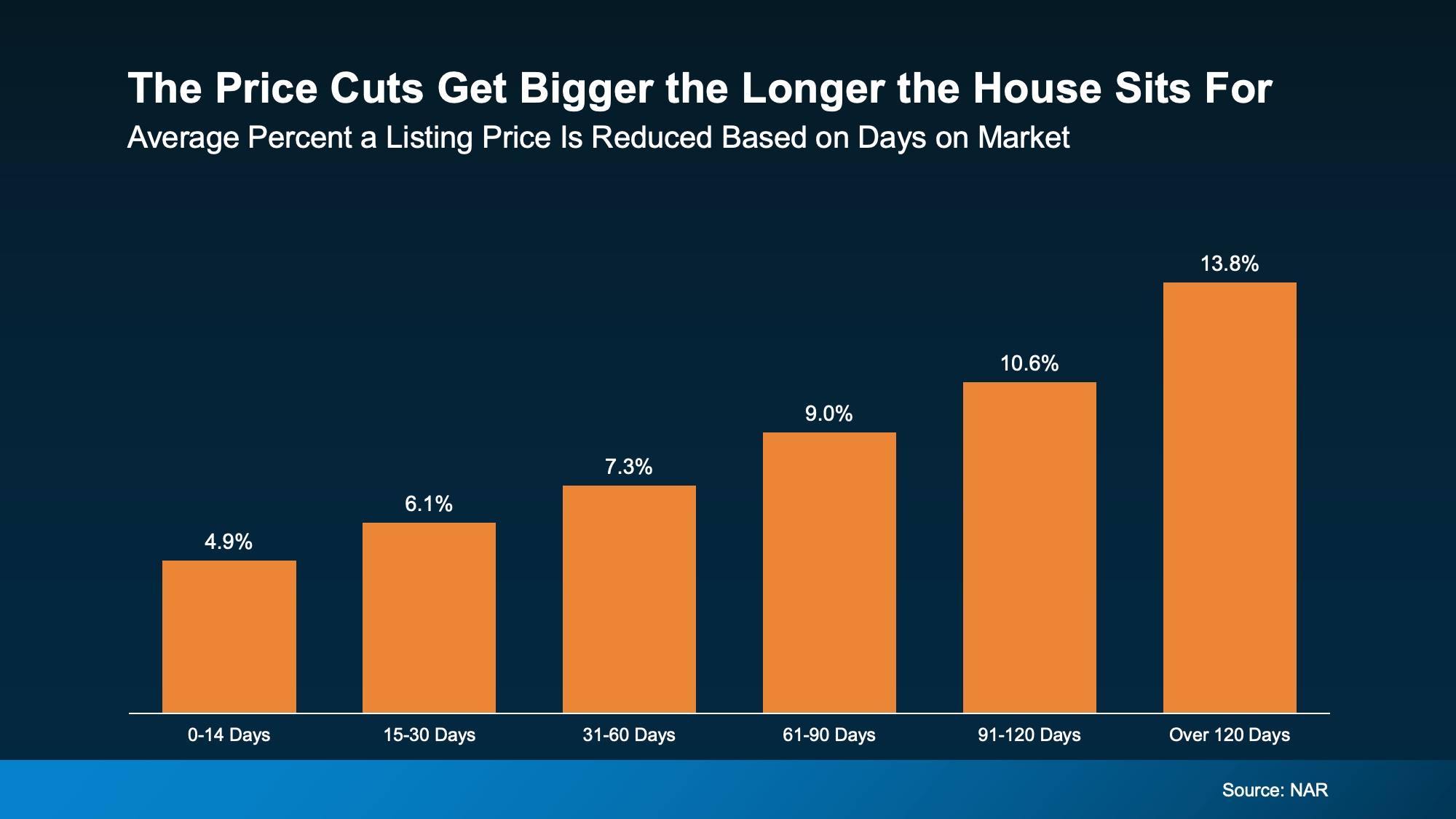

That’s why data from the National Association of Realtors (NAR) shows the longer a home sits, the bigger that price cut tends to be to attract buyers back:

So, what starts as a strategy to “leave room” for negotiate can end up costing you more in the long run.

So, what starts as a strategy to “leave room” for negotiate can end up costing you more in the long run.

Why Pricing Right from Day One Matters

Even though listing at or even just shy of market value may sound counter intuitive if you’re looking to get as much money for your house as possible, a lot of the time it really is the best strategy.

Because the goal isn’t just to list your house to see what price sticks. It’s to price it in a way that creates demand from day one.

NAR puts it best:

“While some sellers are pricing their homes higher than ever, a more ‘goldilocks’ frame of mind is a better approach to avoid price cuts and lingering time on the market.”

In other words, there’s a sweet spot. Too high, and buyers disappear. Too low, and they question the value.

But right in the middle? That’s where the magic happens.

And that’s where the right agent comes in.

They help you understand what buyers are actually paying right now, how your home compares, and how to price it so it stands out immediately. And in today’s market, that strategy is the difference between:

-

Listing high, watching it sit, and selling for less later.

-

Or, pricing it right, creating competition, and putting yourself in a position to win from the start.

Bottom Line

A lot of homeowners think they can list high now and negotiate later, but that’s a mistake that costs them. And it’s the reason only 4 out of every 10 sellers are getting their asking price or more.

If you want to be in that group, it starts with getting the price right from day one.

Connect with a local agent to make sure you are.

Selling your house this season? You’ve probably heard you should stage it before it hits the market. But what does that really mean – and is it worth the effort?

The short answer is “yes,” especially right now.

With more houses for sale this year, you’re likely wondering how to make the most money possible without your house sitting on the market. The answer is staging. It can help your house stand out, bring in stronger offers, and sell faster. As Nadia Evangelou, Principal Economist at the National Association of Realtors (NAR), puts it:

“Staging matters. Preparing the home to be ‘buyer-ready’ attracts more buyers, especially now that inventory has increased.”

Here’s what staging actually involves and what it could do for your sale.

What Is Home Staging?

Home staging is the process of preparing your house, so it appeals to as many buyers as possible. That usually means decluttering, deep cleaning, rearranging furniture, and adding simple touches that help each room feel bright, open, and welcoming.

The goal is to help buyers fall in love with the space and picture themselves living there, which makes them more likely to make an offer.

Why Staging Is Worth the Effort

Staged houses tend to perform better on almost every metric that matters when you sell. According to Redfin, staged homes have been shown to sell up to 73% faster than unstaged homes. And they often close in under a month, compared to anywhere from two to three months for vacant ones.

There’s also a strong return on the money you spend.

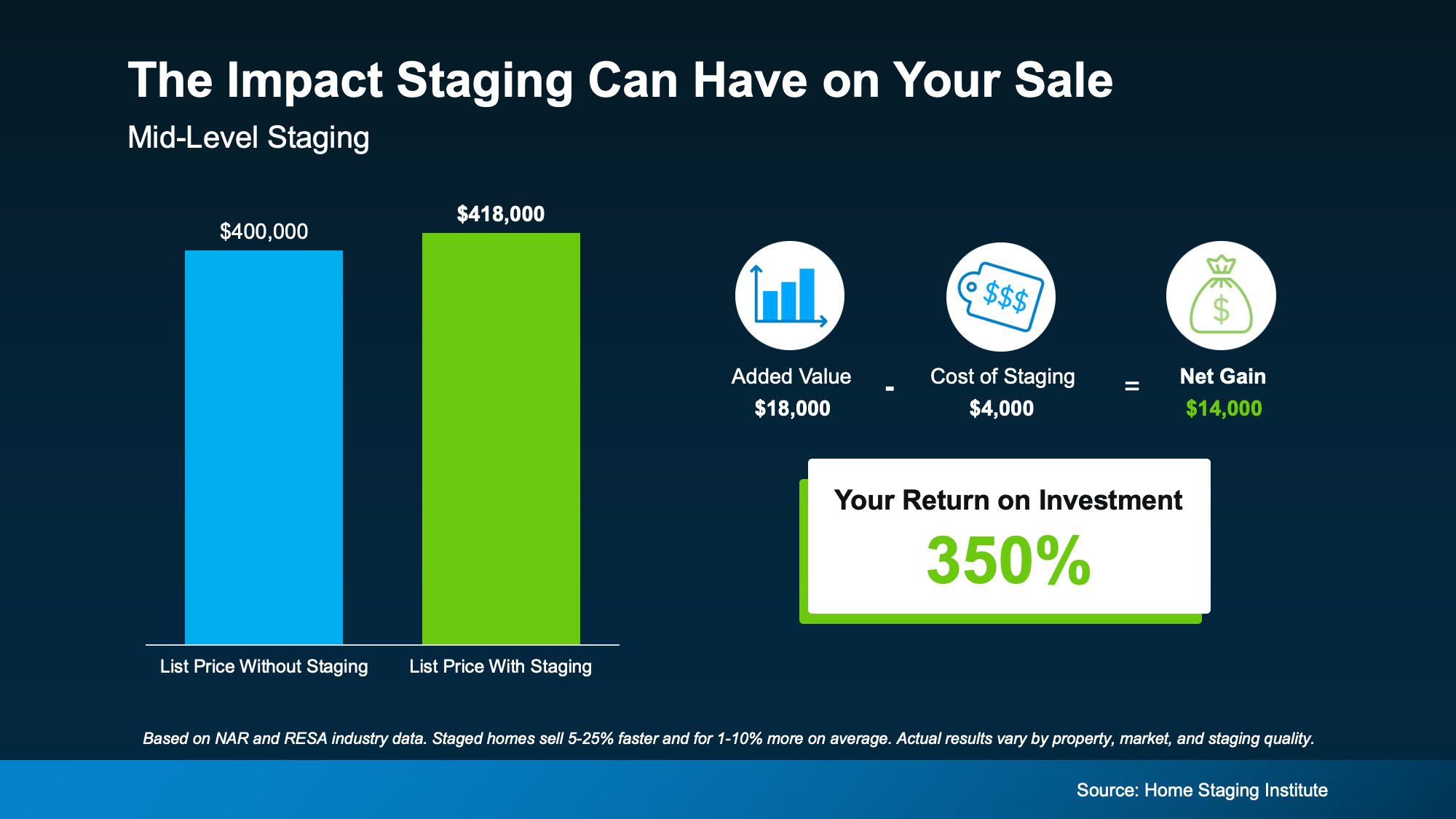

The Home Staging Institute says mid-level staging can deliver a 350% return on investment. On a $400k home, that turns the typical $4k cost into roughly $18k in added value when you sell (see graph below):

By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing.

By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing.

Your Staging Options

And just in case you’re seeing that $4k upfront investment above and thinking, “I’m not going to spend that,” here’s what you should know.

Staging doesn’t always have to mean hiring a full crew or filling your house with rented furniture. There are a few different paths you can take, depending on your budget and timeline. So, you could spend a lot less and still get a good return.

Here are a few options:

- Professional staging. A stager handles everything from layout to décor, often bringing in their own inventory. According to the Home Staging Institute, costs typically range from $500 to $5k or more, depending on the size of your house.

- Virtual staging. Digital furniture and styling are added to your listing photos, which can be a budget-friendly option for vacant houses.

- DIY staging. If your budget is tight and your home only needs minor updates, decluttering, deep cleaning, and arranging furniture for flow can still make a real difference.

Your agent can help you figure out which approach fits your house, your market, and your goals.

Agents see what buyers respond to in open houses and showings every week, so they can give you specific, personalized recommendations on what’s worth your time and money (and what isn’t).

That way you can get the most bang for your buck – no matter your budget.

Bottom Line

With more homes for sale right now, making a strong first impression matters. Staging can help your house sell faster and for more – and there’s an option for almost every budget.

If you’re getting ready to list, connect with a local real estate agent to talk through what level of staging makes the most sense for your house.

Two Big Reasons To Move This Summer

Lower Asking Prices Are a Win for Today’s Buyers

Could Moving a Bit Further Out Change Everything About Your Budget?

-

Equity3 weeks ago

Equity3 weeks agoRecord High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out.

-

Agent Value4 weeks ago

Agent Value4 weeks agoThe Pricing Mistake That Could Cost You Your Sale

-

Equity3 weeks ago

Equity3 weeks agoAre Home Prices Going To Fall?

-

Equity4 weeks ago

Equity4 weeks agoWhat the Foreclosure Headlines Aren’t Telling You

-

Affordability3 weeks ago

Affordability3 weeks agoNewly Built Home Prices Hit a 5-Year Low

-

Affordability2 weeks ago

Affordability2 weeks agoWhat Most Veterans Don’t Know About Their VA Home Loan Benefit

-

Affordability2 weeks ago

Affordability2 weeks agoThe Truth About Affordability Today

-

For Sellers2 weeks ago

For Sellers2 weeks agoThe Real Reason Some People Are Still Moving Right Now

You must be logged in to post a comment Login