Mortgage Rates

Control the Controllables If You’re Worried About Mortgage Rates

If the first half of this year has left you feeling stuck, you’re not the only one. Mortgage rates stayed higher than people wanted. Affordability remained tight. And uncertainty overseas added another layer of pressure nobody saw coming.

That’s why so many people are asking the same question: Will the second half of the year be any better for the housing market?

While nobody has a crystal ball, there are a few encouraging signs things could start moving in a better direction. Here’s what to watch.

Mortgage Rates Could Be Near a Turning Point

One of the biggest reasons mortgage rates haven’t come down yet is inflation. And higher energy prices and uncertainty overseas are at least part of the reason inflation is still elevated. The encouraging news?

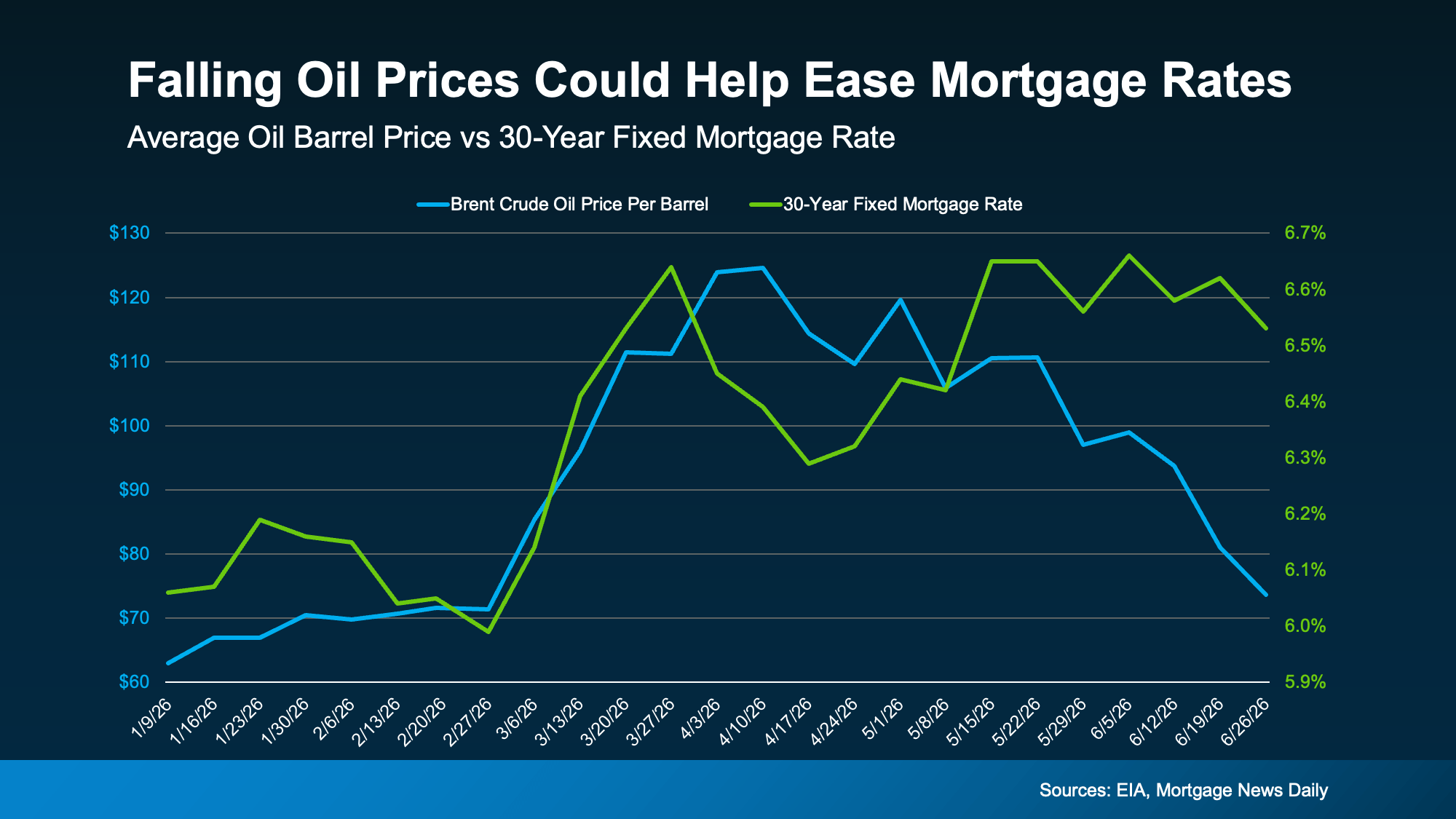

Oil prices have already started coming back down.

That may not sound like it has much to do with buying a home. But historically, mortgage rates and oil prices tend to move in the same direction.

Take a look at the graph below. Generally, they rise and fall together. Both went up in February when the conflict began. While there’s been some volatility lately, experts at the U.S. Energy Information Administration (EIA) say oil prices are forecast to come down. And since oil prices have been on an overall downward trend lately, mortgage rates could come down too:

It’s too soon to say exactly when that will happen (or by how much they’ll fall), but if energy prices go down, inflation cools off, and tensions overseas ease, mortgage rates could come down in the second half of the year.

And that’s good news for anyone thinking about moving. The first half of the year tested everyone’s patience. The second half may finally reward it.

Home Prices Could Pick Back Up

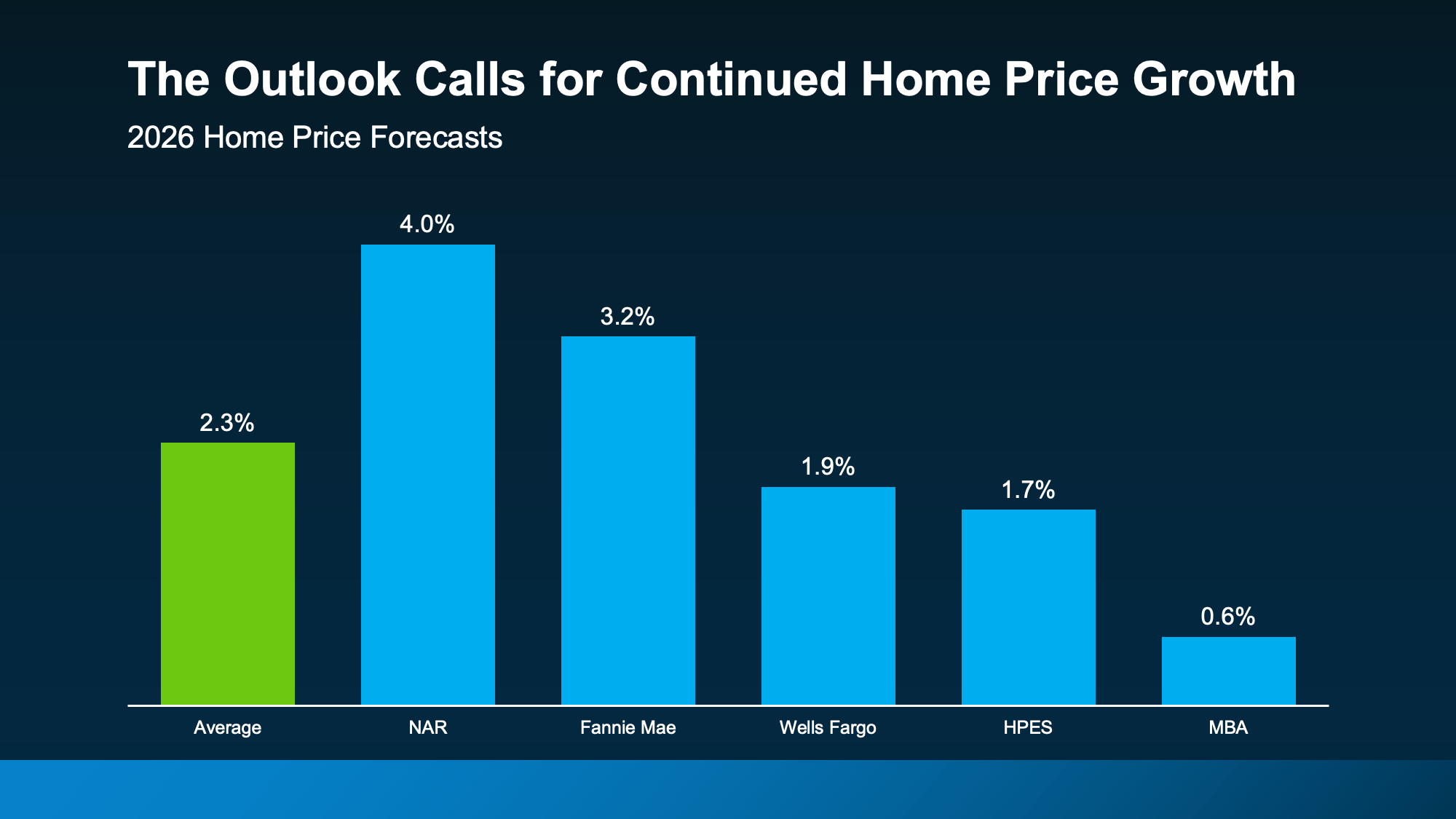

A lot of people want home prices to fall too. But that’s not what most forecasts show.

While price trends are going to vary by area, and some places are seeing mild declines, experts still expect home prices to net positive this year at the national level.

In fact, they’re projecting prices will rise by an average of 2.3% in 2026 (see graph below):

What does that mean for you? Right now, Federal Housing Finance Agency (FHFA)data shows prices are up about 1.7% nationally year-over-year. The average forecast for all of 2026? 2.3%.

Based on those projections, home price growth would have to pick up a bit during the second half of the year. Nothing dramatic, just enough to finish the year around that projected 2.3% gain.

Here’s why that’s possible.

The number of homes for sale has grown, but that growth may be starting to slow down. And if rates improve, more buyers could jump back into the market. More buyers competing could put modest upward pressure on prices, especially if inventory’s not growing as fast.

That’s why buyers shouldn’t assume waiting will guarantee a lower price later. And for sellers, that’s great news if you’ve been worried about your home’s value.

More Homes Are Expected To Sell

If you’ve been wondering why the housing market has felt quieter lately, you’re not imagining it. Home sales have been slower than many experts expected. But that doesn’t mean people have stopped wanting to move.

A lot of people still want or need to make a change. They’ve just been waiting for more certainty, better affordability, or a clearer read on where the market is headed. And early signs show that may be on the horizon.

If rates ease and confidence improves, more people may finally move. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Overall, we expect pent-up demand to continue emerging gradually. But the pace of recovery will vary significantly across markets and will depend on the path of rates, labor market conditions and inventory growth.”

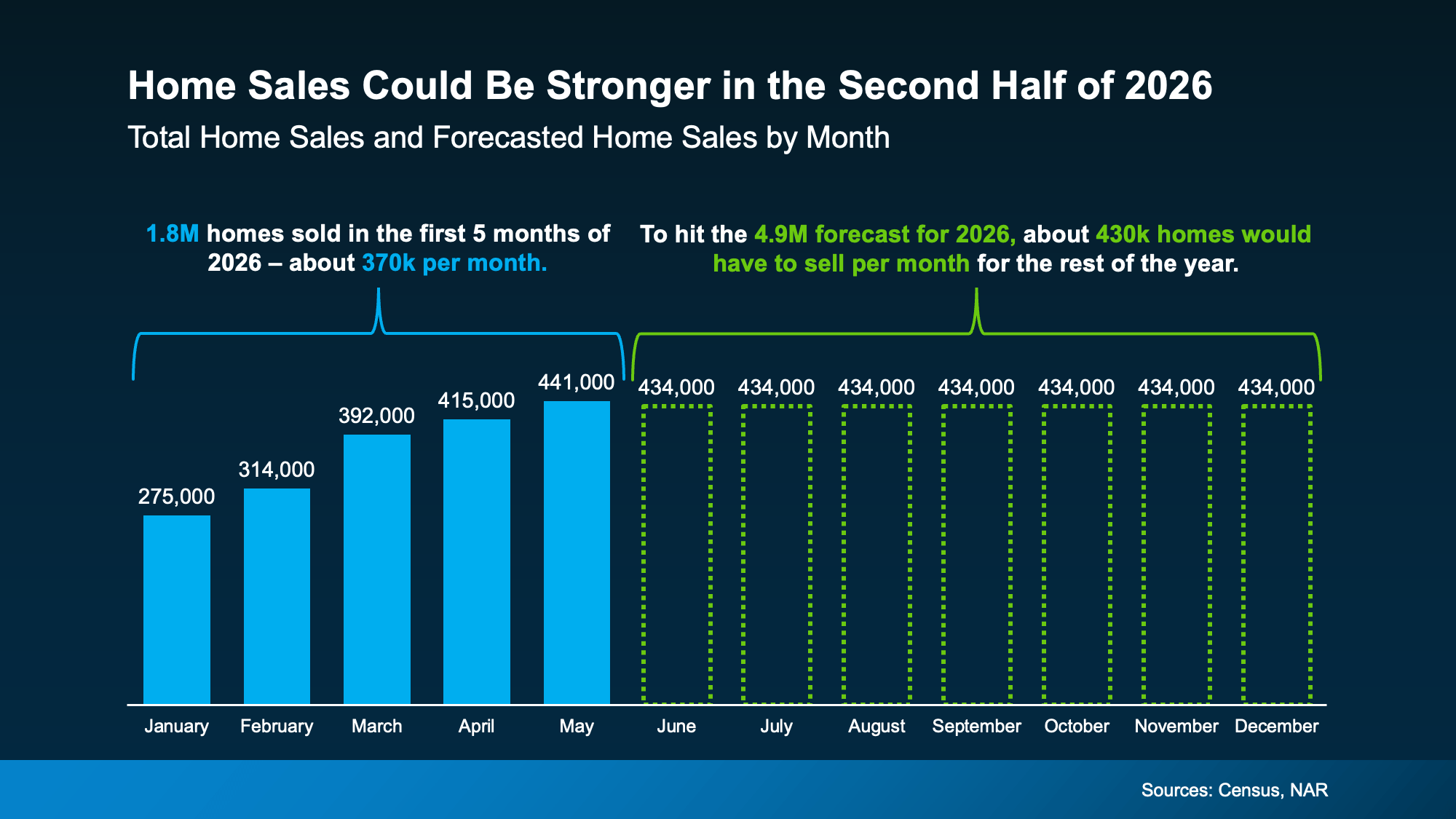

Based on the latest forecasts, to hit the number of sales expected this year, here’s what would have to happen. The second half of the year would need to outperform the first in sales (see graph below):

In fact, each month for the rest of 2026 would have to come close to matching the best month we’ve had so far this year (May). That’s a sign the experts are calling for more momentum headed into the second half.

More people will finally make their move happen – and you’ve got the chance to be one of them.

Bottom Line

The second half of the year probably won’t be perfect. But it could be better.

Mortgage rates may ease. Home sales could pick up. And prices are expected to continue rising at a healthier, more sustainable pace. If you’ve been waiting for signs of progress, this is it.

If you want to understand what these forecasts mean for your plans and what’s happening in your local market, connect with an agent.

You’ve probably heard plenty of doom and gloom about the housing market lately. High rates. Stretched budgets. Headlines that make buying or selling sound like a terrible idea. But the data tells a very different story.

This isn’t 2020 or 2021. It was never going to be. Those were the “unicorn years” – historic low mortgage rates, bidding wars on everything, homes flying off the market in days. That kind of market was a once-in-a-generation anomaly, not a baseline. So, when people compare today to that, of course it looks rough.

But compared to almost any other housing market in modern history? This one is holding up remarkably well.

Homeowners Are Sitting on a Mountain of Equity

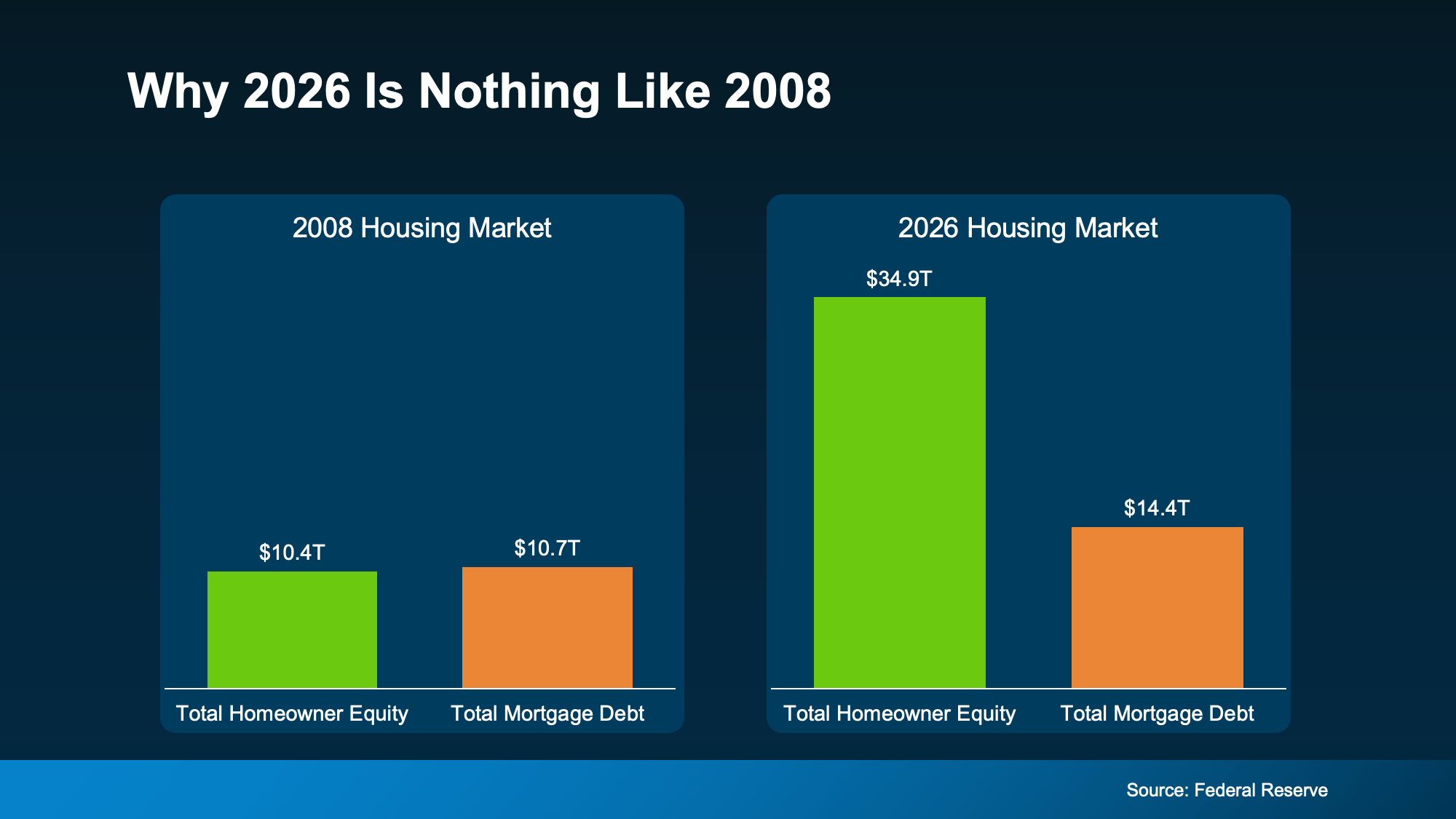

One of the biggest reasons this market hasn’t cracked is the financial strength of the American homeowner. According to Federal Reserve data, homeowner equity and mortgage debt were nearly identical in 2008. That means, if someone hit a rough patch, they had almost nothing to fall back on. That’s what made that crash so bad.

Today? Total homeowner equity across the country sits at $35 trillion – dwarfing total mortgage debt (see graph below):

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

-

Realtor.com found that homeowners who’ve been in their home just 5 years have built up around $180,000 in equity on average. Stick around 6-10 years, and that jumps to over $340,000.

-

Data from ATTOM and the Census shows two-thirds of homeowners either own their home outright or have more than 50% equity.

That’s not a fragile market. That’s a population of homeowners who are financially positioned to sell, to stay, or to make their next move from a place of strength rather than pressure.

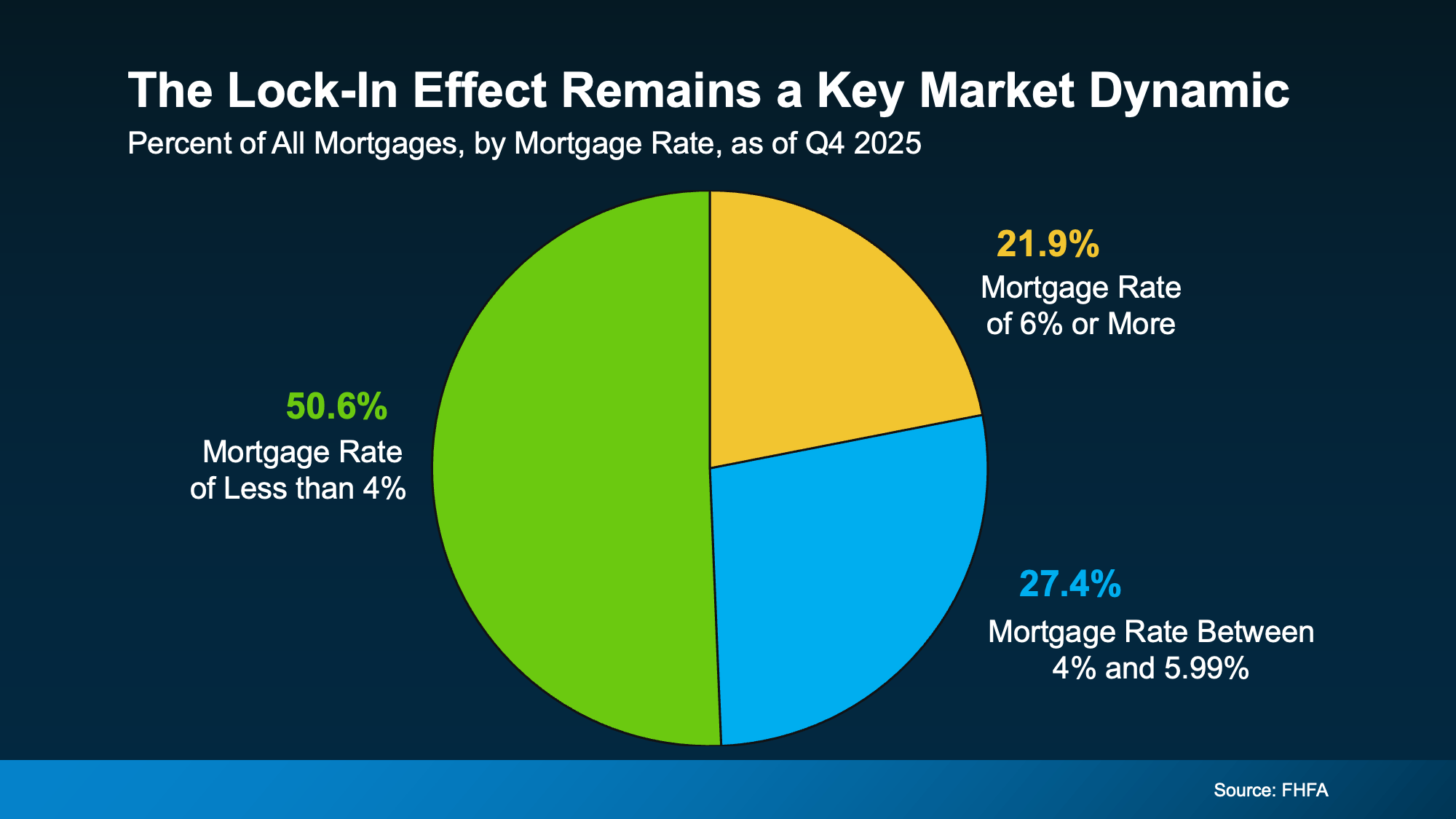

Low Rates and Low Foreclosures

At the same time, Federal Housing Finance Agency (FHFA) data shows more than half of all active mortgages still carry a rate below 4% (see graph below):

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That comfort shows up in the foreclosure numbers, too. Despite a slight recent uptick, foreclosure volumes remain dramatically below historical norms, according to ATTOM. Homeowners aren’t losing their homes in droves. They have equity, they have breathing room, and most have options that keep them out of financial distress.

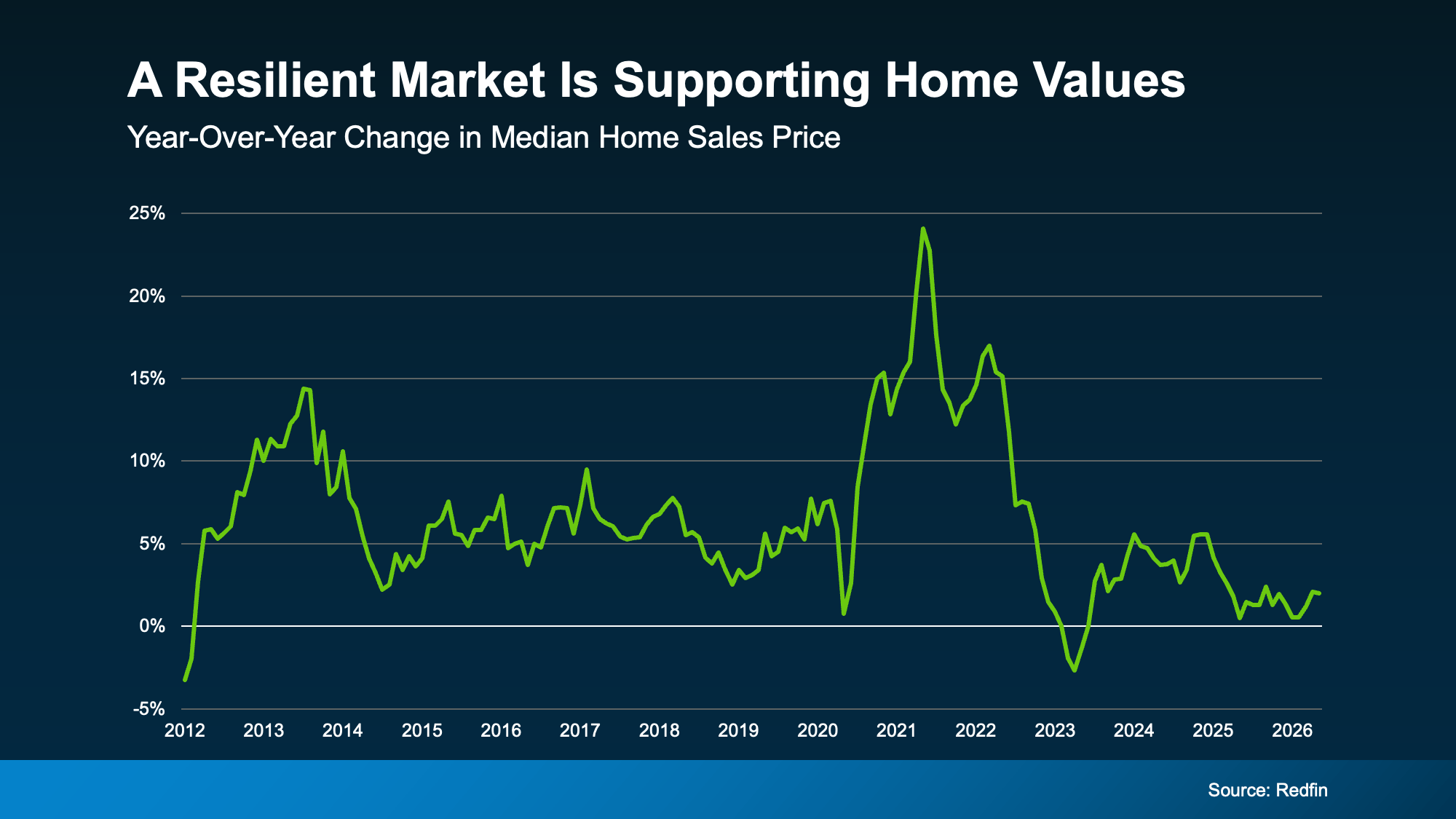

Prices Are Stabilizing, Not Crashing

Here’s another point on the resilience of the market. Redfin research shows home prices are still rising, but the pace has slowed, now closer to 2% year-over-year nationally (see graph below):

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

“We’re in the middle of a long-term housing market correction, not a housing market crash. After the pandemic-era frenzy sent prices soaring and inventory to historic lows, the market needed a reset.”

Bottom Line

This market isn’t broken, and waiting for a crash that isn’t coming has a cost. Every month spent on the sidelines is a month someone else is building equity, locking in a price, or getting ahead of what most experts expect to be a housing surge once broader economic conditions settle.

Whether you’re thinking about buying or selling, a local real estate agent can help you figure out what this market means for your specific situation and what your next move could look like.

Data shows inflation is moving in the wrong direction. But before the headlines send anyone into a panic, here’s what’s actually going on, why it matters for the housing market, and what it means if you’re thinking about buying or selling.

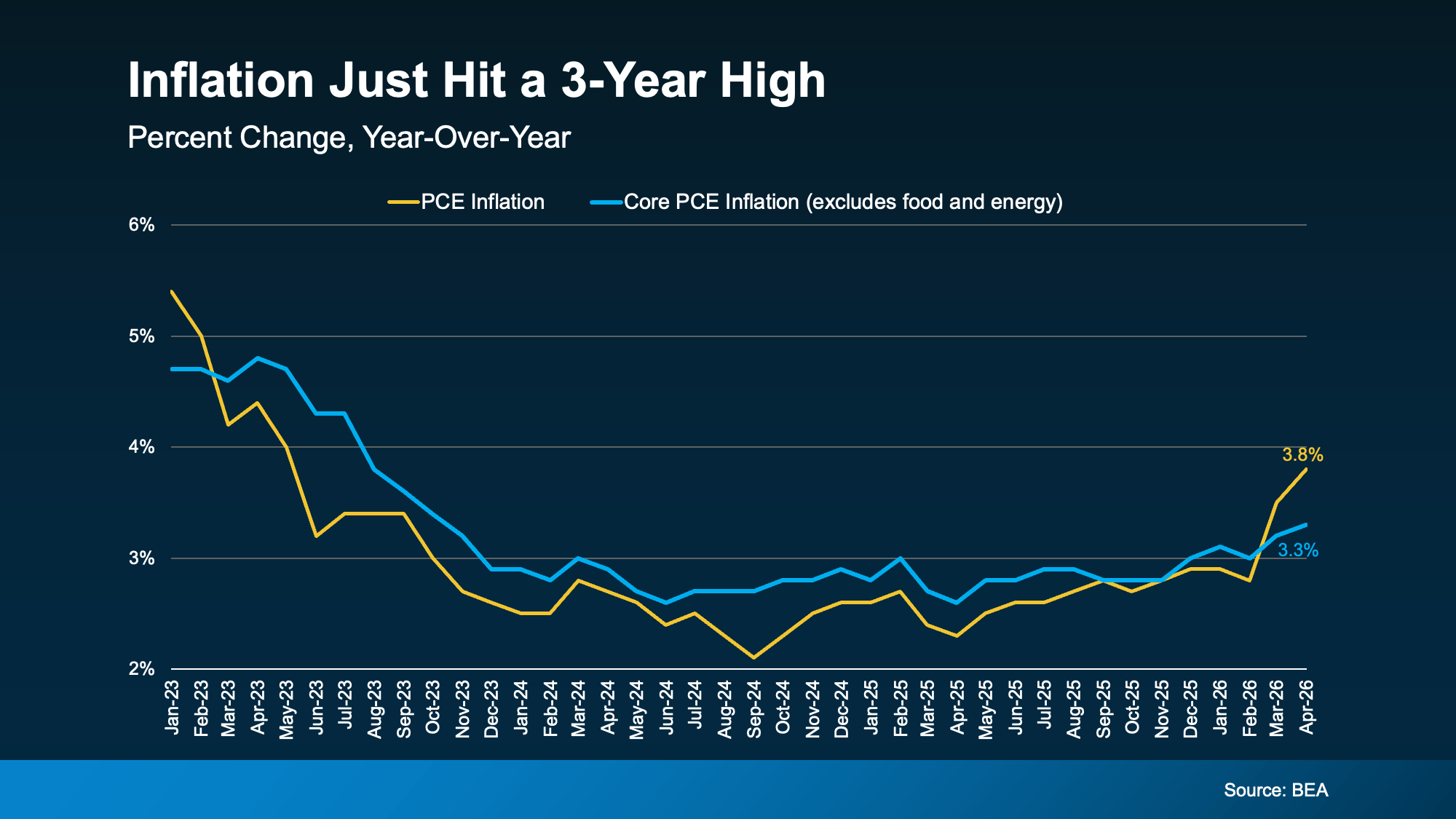

Inflation Went Up – Here’s What That Actually Means

The government tracks inflation in a variety of ways. One is something called PCE – the Personal Consumption Expenditures Price Index. It measures how much more (or less) people are paying for goods and services compared to a year ago. And just based on your own expenses, you can probably guess which way that’s trending.

That’s the one everyone is talking about right now. Check out the yellow line to see how that’s spiked since February (see graph below). A big driver of this jump is the ongoing conflict in the Middle East, which has pushed gas and energy prices significantly higher.

Now, you may have noticed there’s a second line. The blue line shows core PCE. That’s the same measure, but with gas and energy prices stripped out. The Federal Reserve (the Fed) actually watches this number most closely because energy prices swing around a lot and can be misleading.

And here’s the somewhat encouraging part.

Core PCE is rising, but not nearly as fast as the overall number. That suggests a good chunk of the inflation spike we’re seeing right now is tied directly to what’s happening overseas. So, when that situation settles down, inflation may settle a bit, too.

Why This Matters for Mortgage Rates

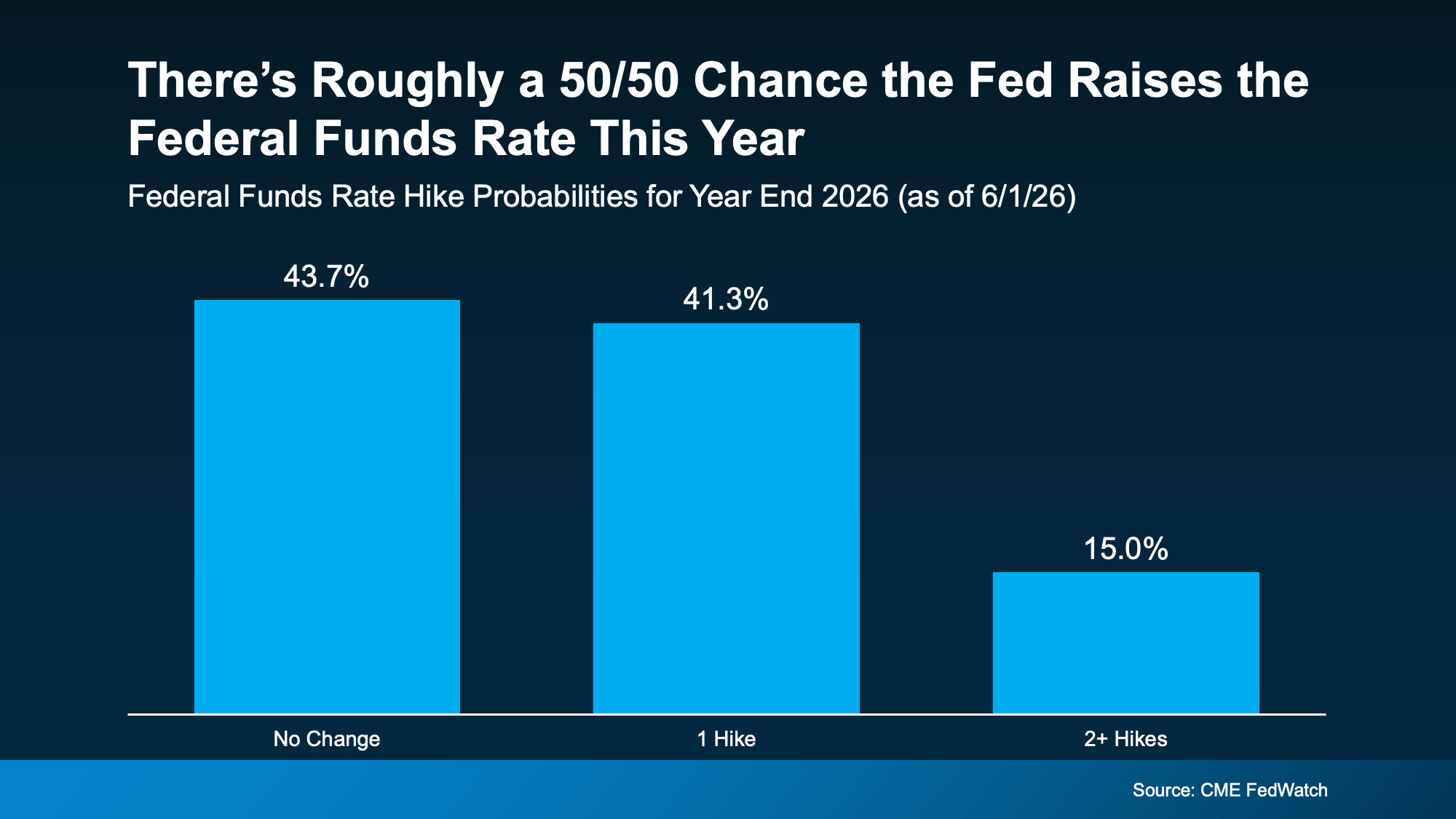

Here’s the housing connection. When inflation is high, the Fed tends to keep the Federal Funds Rate elevated or even raise it to try to taper spending and cool inflation back down. And while it’s not a one-for-one relationship, that Federal Funds Rate can have an impact on your mortgage rate when you buy.

Right now, based on the information we have, there’s roughly a 50/50 chance the Fed actually raises the Federal Funds Rate before the end of 2026, according to CME FedWatch (see graph below):

While it’s too soon to say where this goes for certain and if we’re headed for a rate hike, it does mean mortgage rates are probably not coming down as soon as most people were hoping.

If you’ve been waiting for rates to drop significantly before making a move, this report is a reminder that “higher for longer” is still very much on the table. It really all depends on where the economy goes from here. According to Bankrate:

“Oil prices and bond yields have dropped a bit . . . but they’re still way up compared to the start of spring. Until there’s a resolution to the war, look for both inflation and mortgage rates to stay high.”

But This Is Not 2008 – Not Even Close

Just remember, a tough economy does not equal a housing crash. The conditions today are very different from what led to the 2008 collapse. Here’s why:

-

Inventory is still relatively low. There’s no flood of homes hitting the market.

-

Most homeowners today have strong equity in their homes.

-

Lending standards are far stricter than they were before 2008.

-

Today’s challenge is affordability, not a wave of distressed underwater sellers.

Uncomfortable and unhealthy are not the same thing. The market feels hard right now, but “hard” and “crashing” are very different.

You Still Have Options. Here’s What To Do.

High rates don’t mean homeownership is out of reach. It just means the path looks a little different. There are real strategies that can help, depending on your situation:

-

Ask your lender about different loan options. Adjustable-rate mortgages (ARMs) or rate buydowns may help lower your monthly payment in the short term.

-

Explore first-time buyer programs, down payment assistance, or seller concessions that could help offset costs.

-

Stay in close touch with a trusted agent and lender. When rates shift, and they will, you’ll want to be ready to move fast.

The right strategy, tailored to your goals, matters a lot more than waiting for the perfect moment that may never come.

Bottom Line

Inflation is still above where the Fed wants it, and that means mortgage rates are likely to stay elevated for a while. But for people who need to move, strategy matters far more than trying to perfectly time the market.

Wondering what this means for your specific situation? Connect with a local agent or lender.

The House That Started It All Could Kickstart What’s Next

Priced Out? A Condo or Townhome Could Be Your Way In.

More Homes, Better Prices: A Buyer’s Summer

-

Equity4 weeks ago

Equity4 weeks agoThe Housing Market Is Stronger Than You Think

-

Economy3 weeks ago

Economy3 weeks agoWhat Buying or Selling a Home Gives Back to Your Community

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThe 1 Factor That Explains Everything Happening with Home Prices Right Now

-

Affordability4 weeks ago

Affordability4 weeks agoDown Payments Are Smaller Than They’ve Been Since 2021

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoStudent Loans Are Back in the News. Don’t Let It Put Your Homeownership Plans on Hold.

-

Affordability3 weeks ago

Affordability3 weeks agoWhat To Expect from the Housing Market in the Second Half of 2026

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

-

For Sellers2 weeks ago

For Sellers2 weeks agoThink Nobody’s Buying Homes Right Now? Think Again.

You must be logged in to post a comment Login