For Buyers

A Tale of Two Housing Markets

For a long time, the housing market was all sunshine for sellers. Homes were flying off the shelves, and buyers had to compete like crazy. But lately, things are starting to shift. Some areas are still super competitive for buyers, while others are seeing more homes sit on the market, giving buyers a bit more breathing room.

In other words, it’s a tale of two markets, and knowing which one you’re in makes a huge difference when you move.

What Is a Buyer’s Market vs. a Seller’s Market?

In a buyer’s market, there are a lot of homes for sale, and not as many people buying. With fewer buyers competing for these homes, that means they generally sit on the market longer, they might not sell for as much as they would in a seller’s market, and buyers have more room to negotiate.

On the flip side, in a seller’s market, there aren’t enough homes for sale for the number of buyers who are trying to purchase them. Homes sell faster, sellers often get multiple offers, and prices shoot higher because buyers are willing to pay more to win the home.

The Market Is Starting To Balance Out

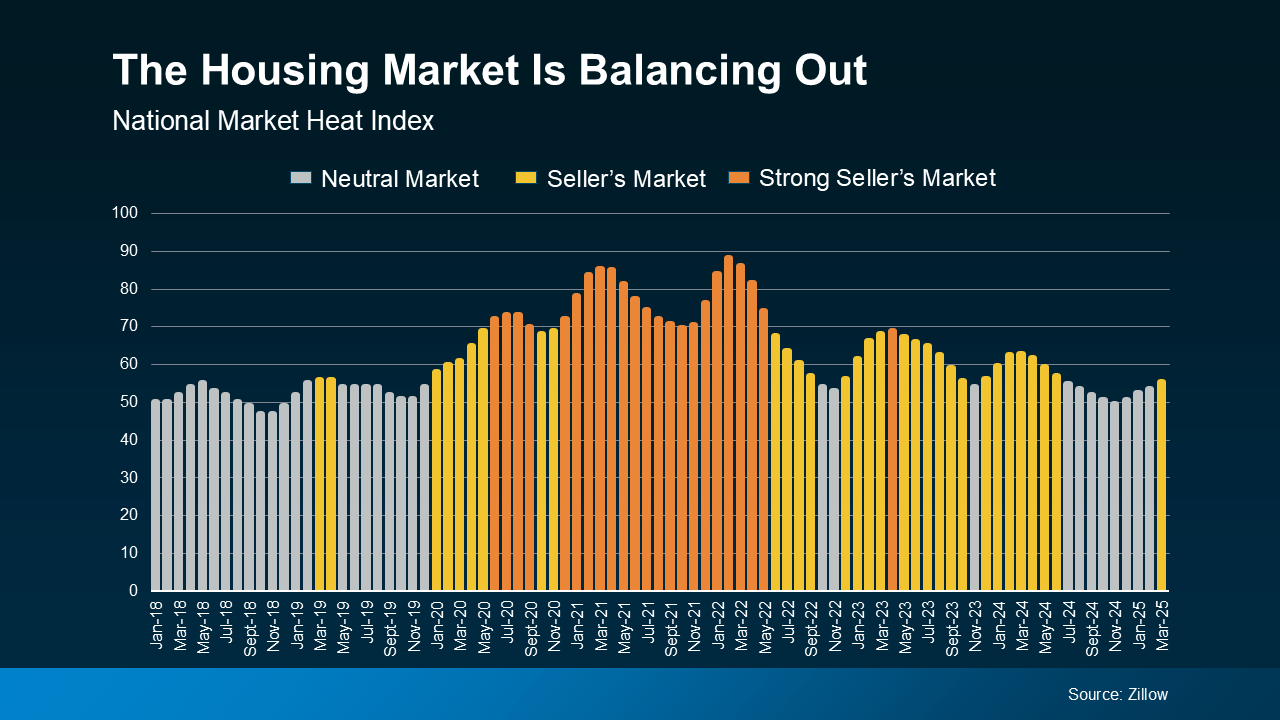

For years, almost every market in the country was a strong seller’s market. That made it tough for buyers – especially first-timers. But now, things are shifting. According to Zillow, the national housing market is balancing out (see graph below):

The index used in this graph measures whether the national housing market is more of a seller’s market, buyer’s market, or neutral market – basically, whether it favors buyers, sellers, or if it’s not really swinging either way. Each month, the market is measured between 0 and 100. The closer to 100, the bigger the advantage sellers have.

The index used in this graph measures whether the national housing market is more of a seller’s market, buyer’s market, or neutral market – basically, whether it favors buyers, sellers, or if it’s not really swinging either way. Each month, the market is measured between 0 and 100. The closer to 100, the bigger the advantage sellers have.

The orange bars in the middle of the graph show the years when sellers had their strongest advantage, from 2020 to early 2022. But, as time has gone on, the market has become more balanced. It shifted from a strong seller’s market to a less intense one. And lately, it’s been neutral more than anything else (that’s the gray bars on the right side of the graph). That means buyers are gaining some negotiating power again.

In a more balanced or neutral market, homes tend to stay on the market a little longer, bidding wars are less common, and sellers may need to make more concessions – like price reductions or helping with closing costs. That shift gives today’s buyers more opportunities and less competition than a couple of years ago.

Why Are Things Changing?

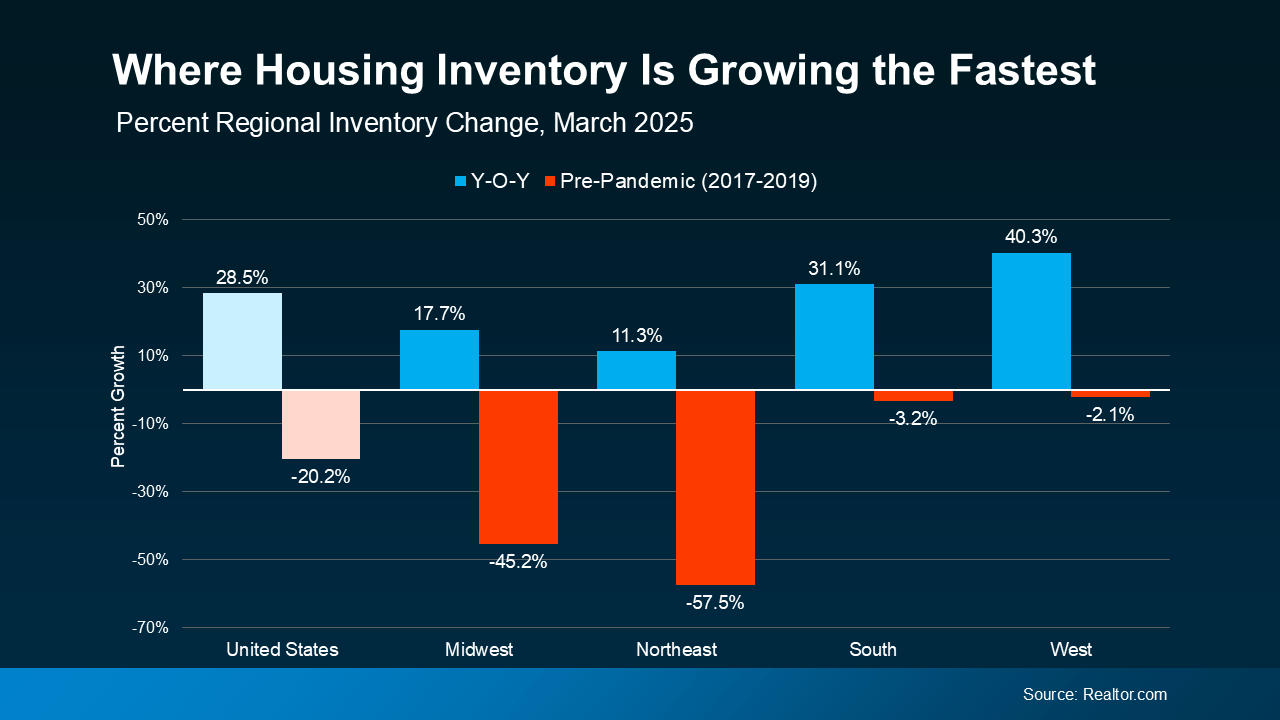

Inventory plays a big role. When there are more homes for sale, buyers have more options – and that cools down home price growth. As data from Realtor.com shows, the supply of available homes for sale isn’t growing at the same rate everywhere (see graph below):

This graph shows how inventory has changed compared to last year (blue bars) and compared to 2017–2019 (red bars) in different regions of the country.

This graph shows how inventory has changed compared to last year (blue bars) and compared to 2017–2019 (red bars) in different regions of the country.

The South and West regions of the U.S. have seen big jumps in housing inventory in the past year (that’s the blue on the right). Both are almost back to pre-pandemic levels. That’s why more buyer’s markets are popping up there.

But in the Northeast and Midwest, inventory is still very low compared to pre-pandemic (that’s why those red bars are so big). That means those areas are more likely to stay seller’s markets for now.

What This Means for You

Every local market is different. Even if the national headlines say one thing, your town (or even your neighborhood) could be telling a totally different story.

Knowing which type of market you’re in helps you make smarter decisions for your move. That’s why working with a local real estate agent is so important right now.

As Zillow says:

“Agents are experts on their local markets and can craft buying or selling strategies tailored to local market conditions.”

Agents understand the unique trends in your area and can help you make the best choices, whether you’re buying or selling. With their expert strategies, you can move no matter which way the market is leaning, because they know how to navigate various levels of buyer competition, how to find hidden gems locally, how to price a house right, how to negotiate based on who has more leverage, and more.

Bottom Line

If you’re ready to make a move, or even just thinking about it, connect with a local real estate agent. They’d love to help you understand your local market and create a game plan that works for you.

What’s one thing you’re curious about when it comes to the market in your area?

Remember a few years back when sellers held all the power and buyers were stuck offering way over asking or waiving inspections just to get a chance at the house? In many markets, those days are behind us.

While it’s going to vary by area, more metros are slowly shifting to favor buyers, and the market is starting to look a lot more like a two-way street again.

And that balance is something we haven’t had in a while.

Whether you’re buying or selling, here’s what you need to know about what’s changing and what it means for your move.

The Most Buyer-Friendly Market in Years

The national data tells an interesting story right now. According to Realtor.com:

“The national housing market is balanced but gradually loosening as the cycle moves in a more buyer-friendly direction . . .“

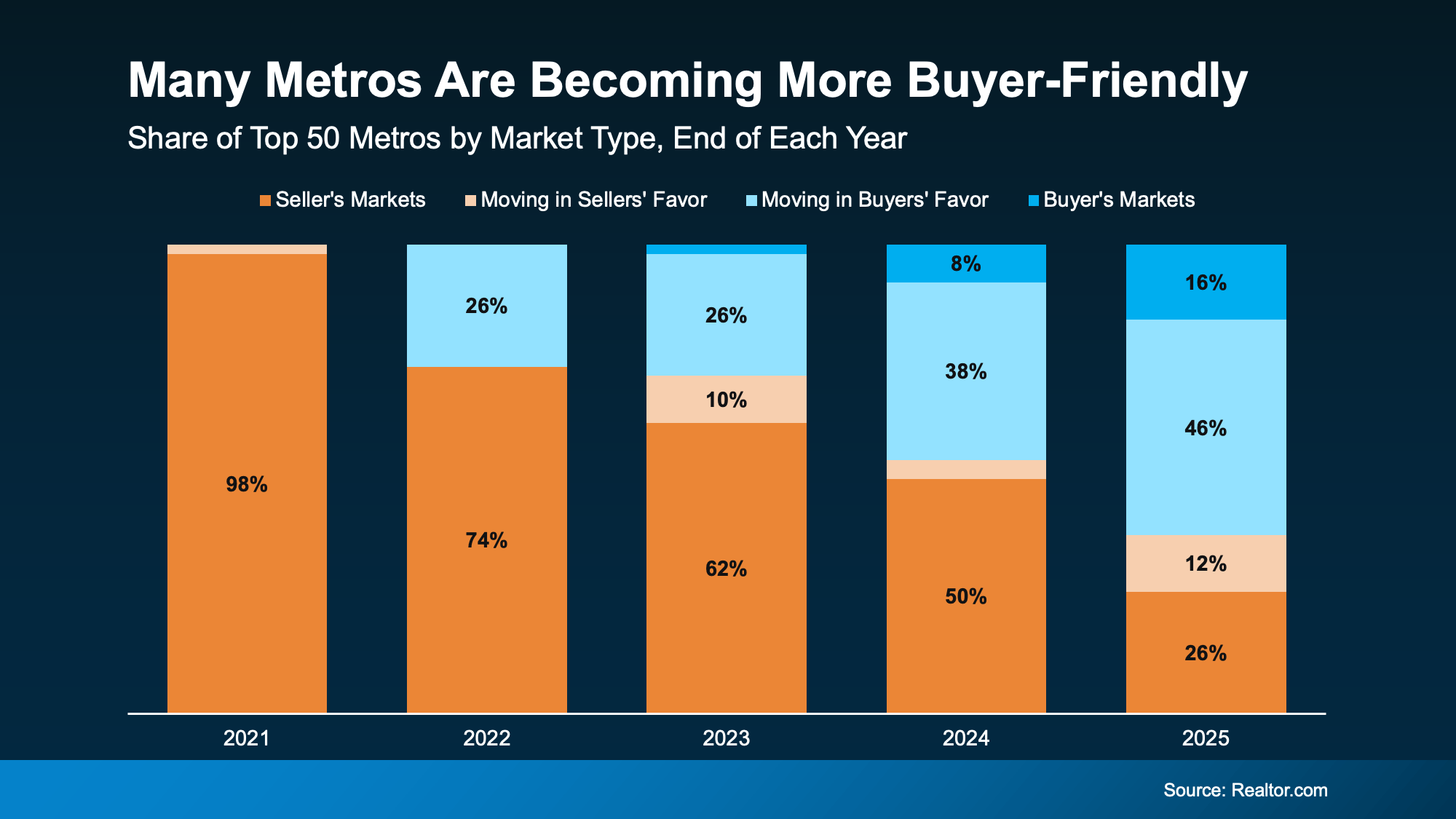

That’s because, over the past few years, more and more metros have been flipping back to more buyer-friendly terms as inventory’s grown. And when you zoom in on the latest Realtor.com data for the top 50 metro markets over time, the trend becomes really clear (see graph below).

Back in 2021, almost all major metros were seller’s markets. By the end of 2025, only 1 in 3 still favored sellers. That’s an obvious shift.

And that changes how the market is going to feel for everyone. Sellers shouldn’t still expect 2021 conditions, but neither should buyers. At least, not generally speaking.

It’s Not the Same Story Everywhere

That said, who has the power ultimately depends on where you live. While more metros are leaning buyer-friendly lately, there are still plenty of strong seller’s markets right now, too.

It really comes down to how much housing supply and demand there is in your area. And that varies enormously by region.

Sun Belt cities like Austin, Tampa, and San Antonio saw major building booms in recent years, giving buyers more options and more negotiating room. Meanwhile, cities in the Northeast and Midwest – think Rochester, Hartford, and Buffalo – didn’t see that same wave, so inventory stayed tight and competition stayed fierce. As Jeff Ostrowski, Housing Analyst at Bankrate, explains:

“The formerly hot Sun Belt markets have cooled, while the Northeast and Midwest have stayed hot. The big driver here is construction activity. The softest markets now [have] experienced big booms that spurred new building, and that has led to a large supply of new and existing homes on the market in those places.”

Practical Advice for Your Move

To find out who has the power in your local market, talk to an agent. Because knowing what’s happening locally is going to be the key to setting the right strategy for your move.

If the market is working in your favor, great. Lean in and use it to your benefit. But if it’s not, all hope isn’t lost. Your agent can help you figure out how to approach any market.

Here’s some practical advice if there’s a mismatch between your goal and local market conditions.

If you’re buying in a seller’s market:

-

Get pre-approved before you start shopping. It shows sellers you’re serious.

-

Be ready to act fast when the right home hits the market.

-

Consider offering a quick closing date or flexible terms.

-

Work closely with your agent to craft a competitive offer.

If you’re selling in a buyer’s market:

-

Price it right from day one. Overpricing will cost you time and money.

-

Focus on curb appeal and staging to stand out in areas with more inventory.

-

Be open to offering incentives, like covering closing costs or a home warranty.

-

Expect buyers to negotiate and be ready to be flexible.

Bottom Line

Right now, local markets are moving in very different directions. And your strategy as a buyer or seller should reflect your market.

Want to know which way your local market is leaning and what that means for your move? Talk to a local real estate agent.

One of the biggest reasons buyers are still sitting on the sidelines is because they think home prices are going to come down.

-

Some believe a crash is coming and they’ll get a better deal if they hold off.

-

Others worry they’ll buy now and watch their home’s value fall later.

And nobody wants to overpay or buy right before values drop. But here’s the question worth asking:

What if the crash you’re waiting for isn’t actually coming?

Because that’s what the latest data suggests.

Experts Are Not Calling for a Crash

If you’ve spent any time online lately, you’ve seen posts claiming home prices are about to come crashing down. And it’s true that some markets are seeing small price declines right now.

But that’s not the same thing as a nationwide crash.

While some places are going through a price adjustment, Realtor.com data shows home prices are still rising in 71% of housing markets across the country.

The trouble is, since negative news sells, you’re seeing more coverage about how a handful of markets are seeing declines, than how the majority are still seeing prices rise. And that’s unfortunate.

It’s exactly why a lot of buyers end up with the impression that prices are falling everywhere when they’re not. So how do you really know where prices are really headed from here?

That’s where the Home Price Expectations Survey (HPES) from Fannie Mae comes in.

Home Prices Will Rise for the Next 5 Years

Every quarter, more than 100 economists, housing experts, and market analysts are asked where they think home prices are headed based on the latest data available.

And despite all the uncertainty in today’s market, there’s one thing they largely agreed on:

They don’t think a crash is coming.

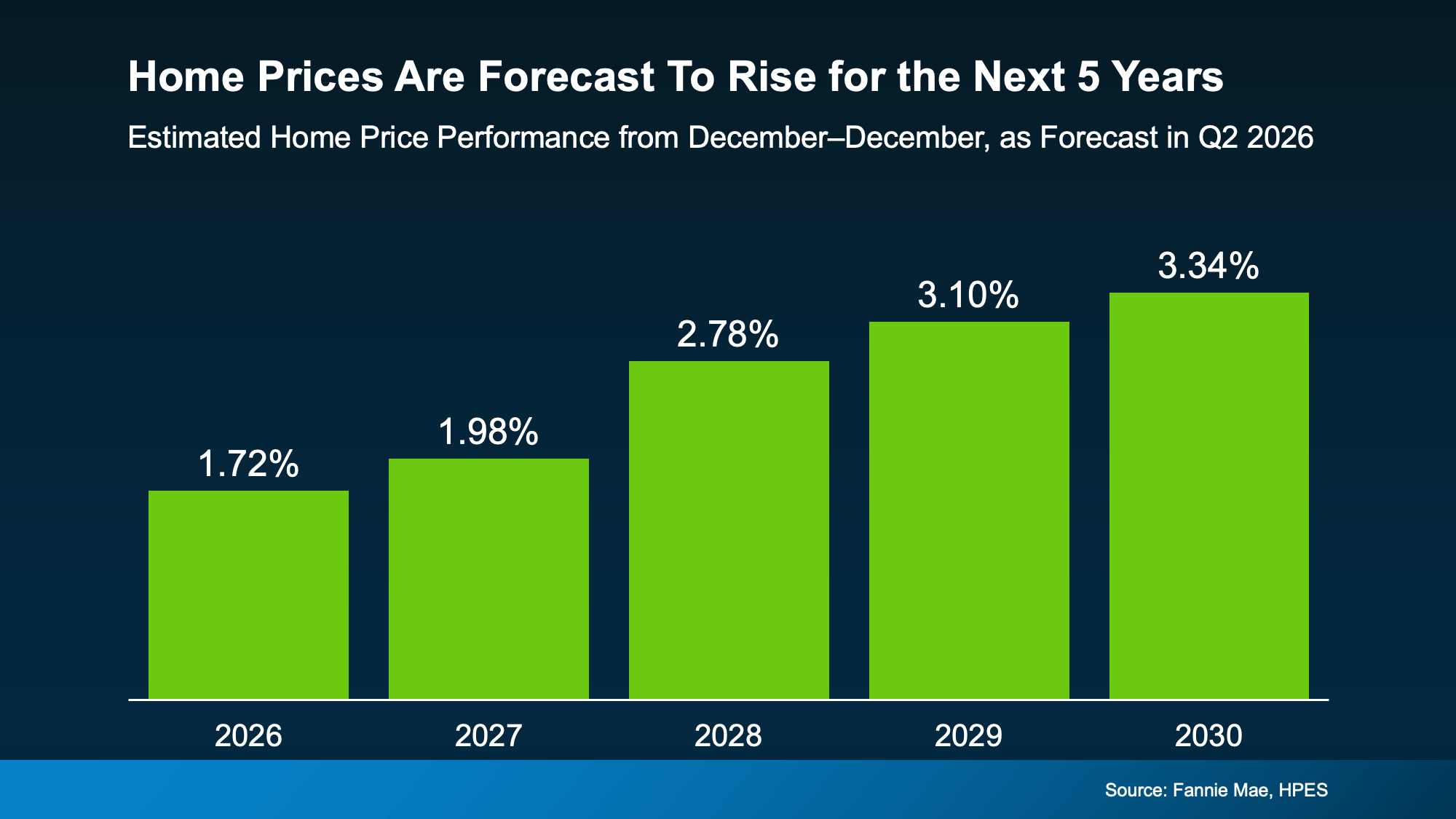

In fact, the average of all of their forecasts calls for home prices to rise every year for at least the next 5 years (see graph below):

The point is that the overwhelming expectation isn’t for prices to fall. It’s for prices to rise at a more normal pace. And just in case you’re looking at the forecasts and saying: “of course they’d say that” – know that this survey doesn’t just include optimists. It includes pessimists too.

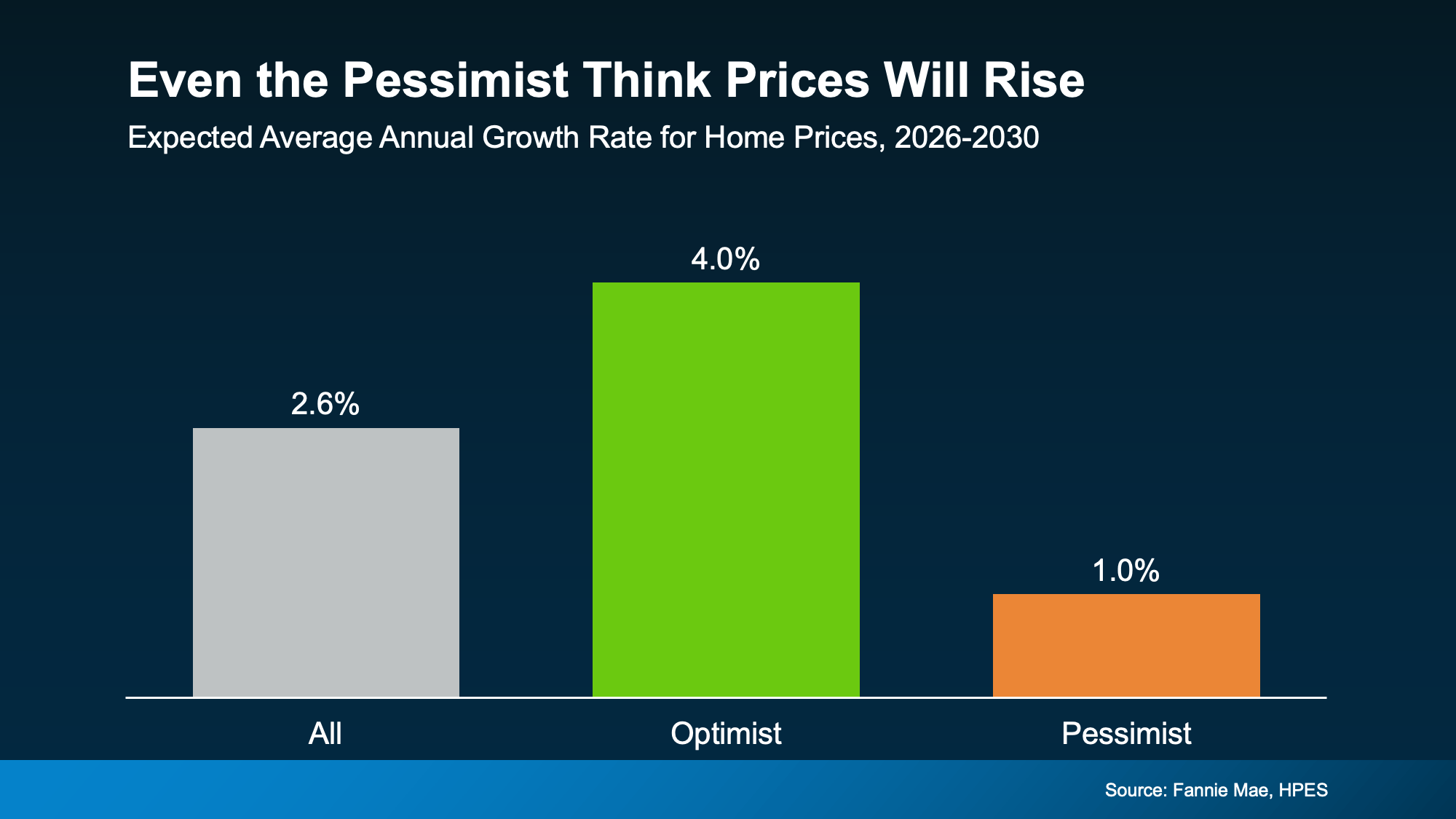

Even the Pessimists Aren’t Predicting a Crash

Researchers broke the panel into groups based on how bullish or bearish they were about housing. The result? Even the most pessimistic group still expects home prices to climb over the next five years.

Optimists think we’ll see prices go up roughly 4% a year. Pessimists say it’ll be closer to 1%. The reality may be somewhere in the middle.

Think about that for a second. The debate among experts isn’t whether prices will crash. It’s how much they’ll rise.

That’s a very different conversation than the one happening across social media.

This Means Waiting Could Actually Cost You

So, if you’re putting off your move until prices come down, you may be disappointed. According to the experts, a widespread crash isn’t in the cards.

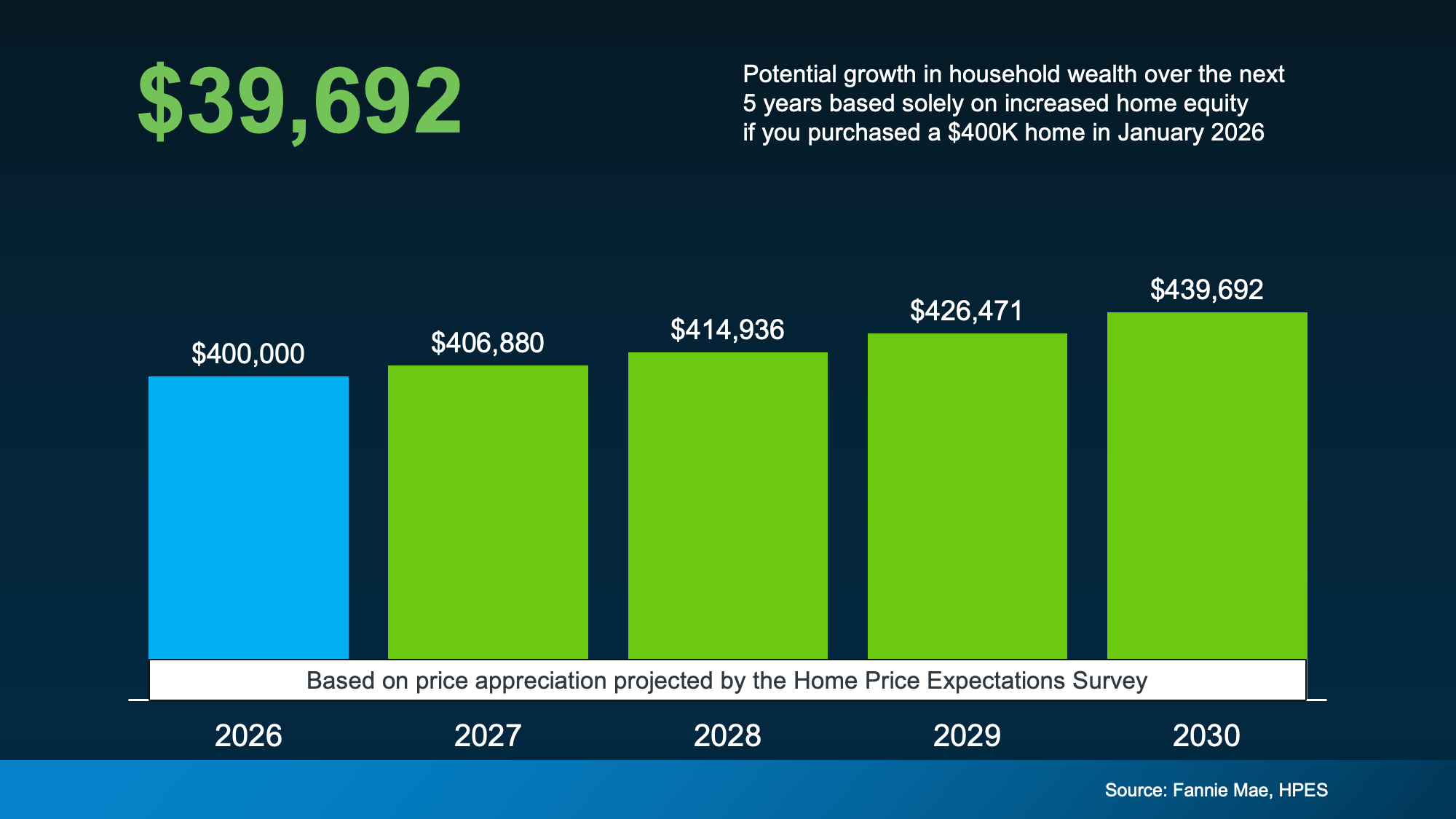

In fact, based on the HPES forecast, a buyer who purchased a $400,000 home this January would gain nearly $40,000 in equity over the next five years from appreciation alone, even in this more moderate market (see below):

Of course, this all depends on local market conditions. This forecast is a national average. But broadly speaking, if the experts are right, the bigger risk isn’t that prices will crash. It may be waiting for a crash that never comes.

Because depending on your market, if you wait, you could be missing out on $40k in equity or paying 40k more in 5 years for the same house.

Bottom Line

A lot of buyers are waiting because they think prices will fall, but that’s not what the experts are saying.

If you’re trying to decide whether waiting still makes sense, connect with a local agent. They’ll help you understand what’s happening in your local market and what it could mean for your plans.

A lot of people who want to move are telling themselves the same thing: “Maybe I’ll just wait until later this year once things calm down.”

While waiting sounds like a good plan, there’s something worth knowing before you decide. Rates aren’t expected to change much, so if that’s the #1 reason you’re waiting, it may not pay off. And there may be other things you miss out on in the meantime.

Historically, Summer is one of the strongest seasons of the year for both buyers and sellers. And if you delay your move until Fall or Winter, some of those opportunities may already be fading.

Buyers: Fresh Inventory Is Your Real Summer Advantage

One of the biggest frustrations buyers have faced over the past few years has been a lack of affordable options. Maybe you’ve run into that yourself:

-

You find a house you like, but it’s out of your budget.

-

You find something in your budget, but you don’t like it.

-

Or worse, nothing interesting hits the market for weeks.

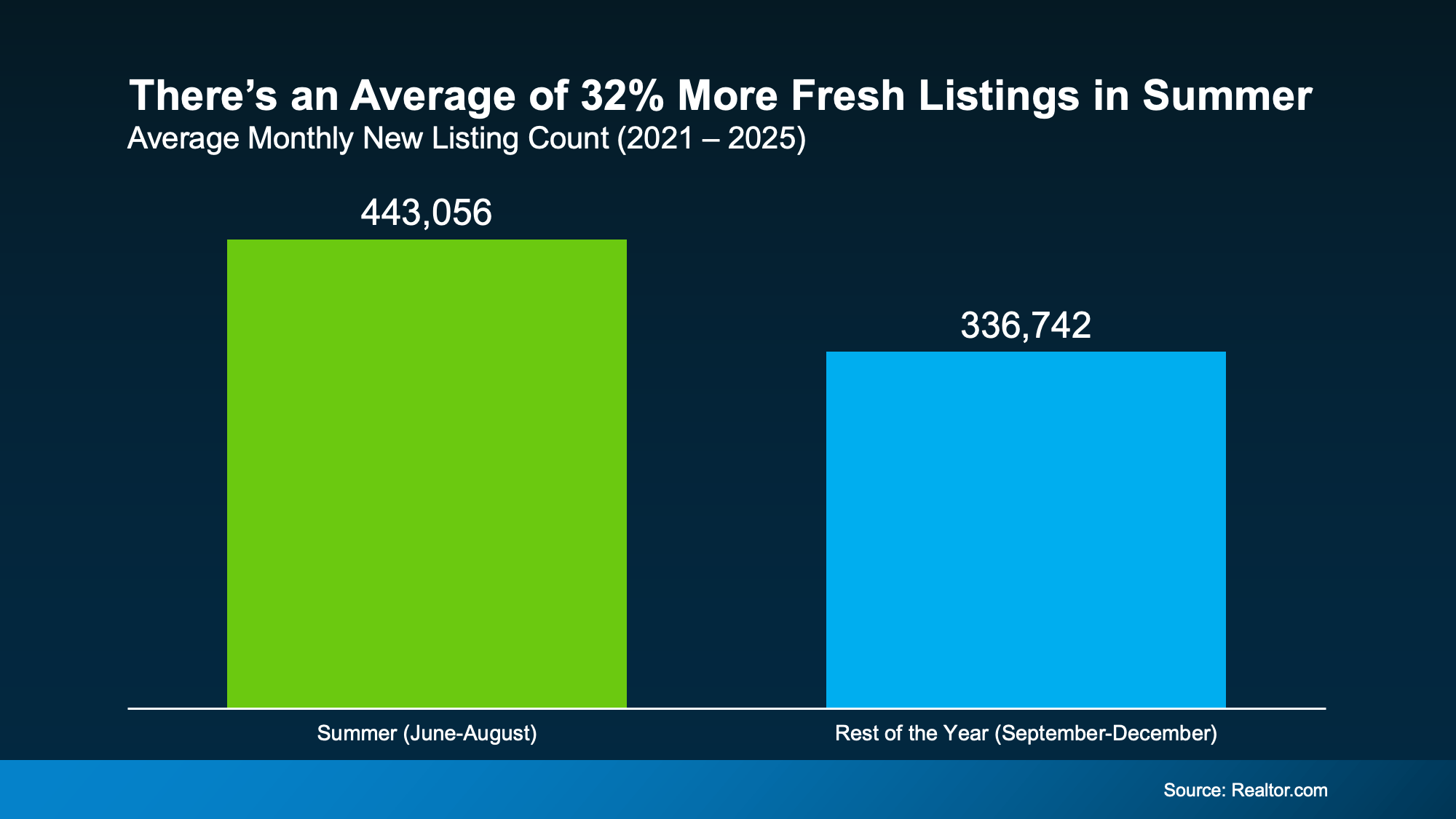

Historically, Summer helps with that.

Looking at data from the last few years, Summer months consistently bring more sellers into the market than later in the year. And that gives buyers a real window of fresh choices.

According to Realtor.com, any given Summer month typically sees about 32% more fresh options than the average month from September-December.

With more newly listed homes, there’s a better chance of finding one you like where the numbers actually work.

Because all it really takes is one home to completely change your search. And if you’ve got more popping onto the market to choose from, maybe one of those is exactly what you need.

But keep in mind, this seasonal window isn’t open forever. Fresh inventory tends to slow down once Summer ends.

Many homeowners who planned to sell this year have already listed by then. Families who wanted to move before school starts have often already gotten it done, or at least, set it into motion. So, new listing activity usually cools as we head into Fall and Winter.

Of course, every year is different. But if finding the right home at the right price has been your biggest challenge, waiting until later in the year may not necessarily give you more options. In fact, recent history suggests it may do just the opposite.

Sellers: Homes Usually Sell for More in the Summer

If you’re thinking of selling, you may be considering holding off because you’ve seen headlines about lower asking prices, price cuts, and softer conditions in some markets. But those headlines don’t tell the whole story or convey just how much it varies by area.

Here’s what you really need to know. Even though the market’s becoming more balanced and some pockets are experiencing price declines, that doesn’t mean you’ve missed your chance to sell.

Seasonality can still work in your favor no matter where you are. And this Summer could still give you the chance to sell for a good price.

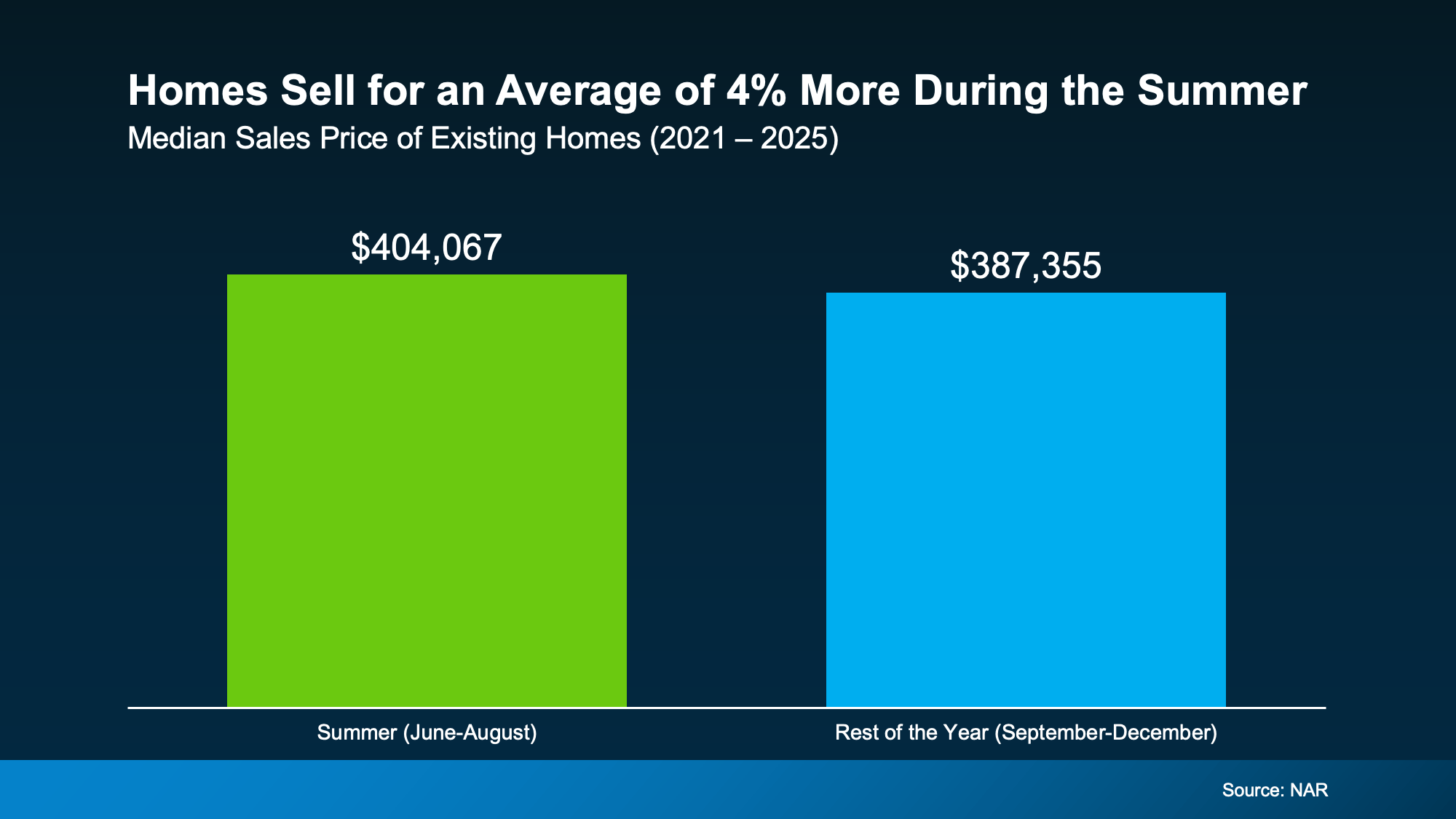

According to the National Association of Realtors (NAR), homes sold during a Summer month usually sell for about 4% more than homes sold during the typical month from September-December:

Why? Summer buyers are usually operating on a set timeframe. They’re trying to move before the next school year or when they have more PTO and warmer weather to tour houses. That urgency can translate into better offers.

Now, that doesn’t mean you should price your house 4% higher this Summer. That would actually be a mistake in today’s market.

It just means if you’re looking to get as much for your house as you reasonably can, a Summer move could be a smarter play than waiting until later this year.

Because based on typical seasonality, you may get more for your house than you would if you waited until the Fall or Winter (when there are typically fewer buyers active).

And if you’re considering a move anyway, that’s worth factoring in.

Bottom Line

Could waiting until later this year work out? Sure. But it’s important to understand what you may gain by moving now too – that way you have the full picture before you decide.

If a 2026 move is on your radar, talk to an agent about what matters most to you. Depending on your priorities, Summer could be your moment.

Is It Still a Seller’s Market? Here’s What the Data Says.

Think Home Prices Will Crash? Here’s What the Experts Actually Expect.

Should You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

Affordability4 weeks ago

Affordability4 weeks agoWhat Most Veterans Don’t Know About Their VA Home Loan Benefit

-

Affordability4 weeks ago

Affordability4 weeks agoThe Truth About Affordability Today

-

Affordability3 weeks ago

Affordability3 weeks agoWhat Rising Inflation Means for Your Move

-

For Sellers4 weeks ago

For Sellers4 weeks agoThe Real Reason Some People Are Still Moving Right Now

-

Economy3 weeks ago

Economy3 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability3 weeks ago

Affordability3 weeks agoLess House, More Home: Why Smaller Homes Are Paying Off for Today’s Buyers

-

Affordability2 weeks ago

Affordability2 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Affordability2 weeks ago

Affordability2 weeks agoLower Asking Prices Are a Win for Today’s Buyers

You must be logged in to post a comment Login