For Sellers

Think No One’s Buying Homes Right Now? Think Again.

That kitchen you’ve been mentally redesigning…

The bathroom that really needs a refresh…

Or the outdoor space you keep saying you’ll get to someday…

What if you already have what you need to finally make it happen? Because a growing number of homeowners are realizing just that.

Homeowners are expected to spend over $522 billion on home improvements by the end of 2026 – and they’re not draining their savings accounts to get it done. Many are using their home equity.

And if you’ve owned your home for 10+ years, there’s a chance you could use your equity to fund some home upgrades too. Let’s break down what you need to know first.

What Is Equity? And How Does It Help?

Equity is the difference between what your house is worth and what you owe on your mortgage.

And according to Cotality, the average homeowner has about $313,000 worth of equity today. That’s more than enough to finally knock some projects off your list. And more people are realizing they can use that to give their home a little TLC.

Research coming out of Meridian Link says home improvements are the top thing people are using their equity for today.

Top Motivations for Equity-Based Borrowing:

- Funding home improvements (45%)

- Using it to pay down other debts / debt consolidation (16%)

- Investing in other properties (16%)

Maybe it makes sense for you to do the same. But here’s what’s important. Just because you can use your equity doesn’t mean you have to. It also doesn’t mean every project makes sense.

What Projects Are Actually Worth It?

If you’re going to go this route, you’ll want to focus on upgrades that actually pay off. A good renovation should be something that improves the value of your home. Because, even if you’re not planning to sell soon, you want to make sure you’re setting yourself up for success when you do.

And an agent is the best resource as you weigh your options. They know what other homeowners are doing and what buyers in your area like. And that can be really helpful as you narrow down your project list. As the National Association of Realtors (NAR) puts it:

“Being able to help sellers prioritize home improvements and maximize their net on the sale is a key value real estate agents offer.”

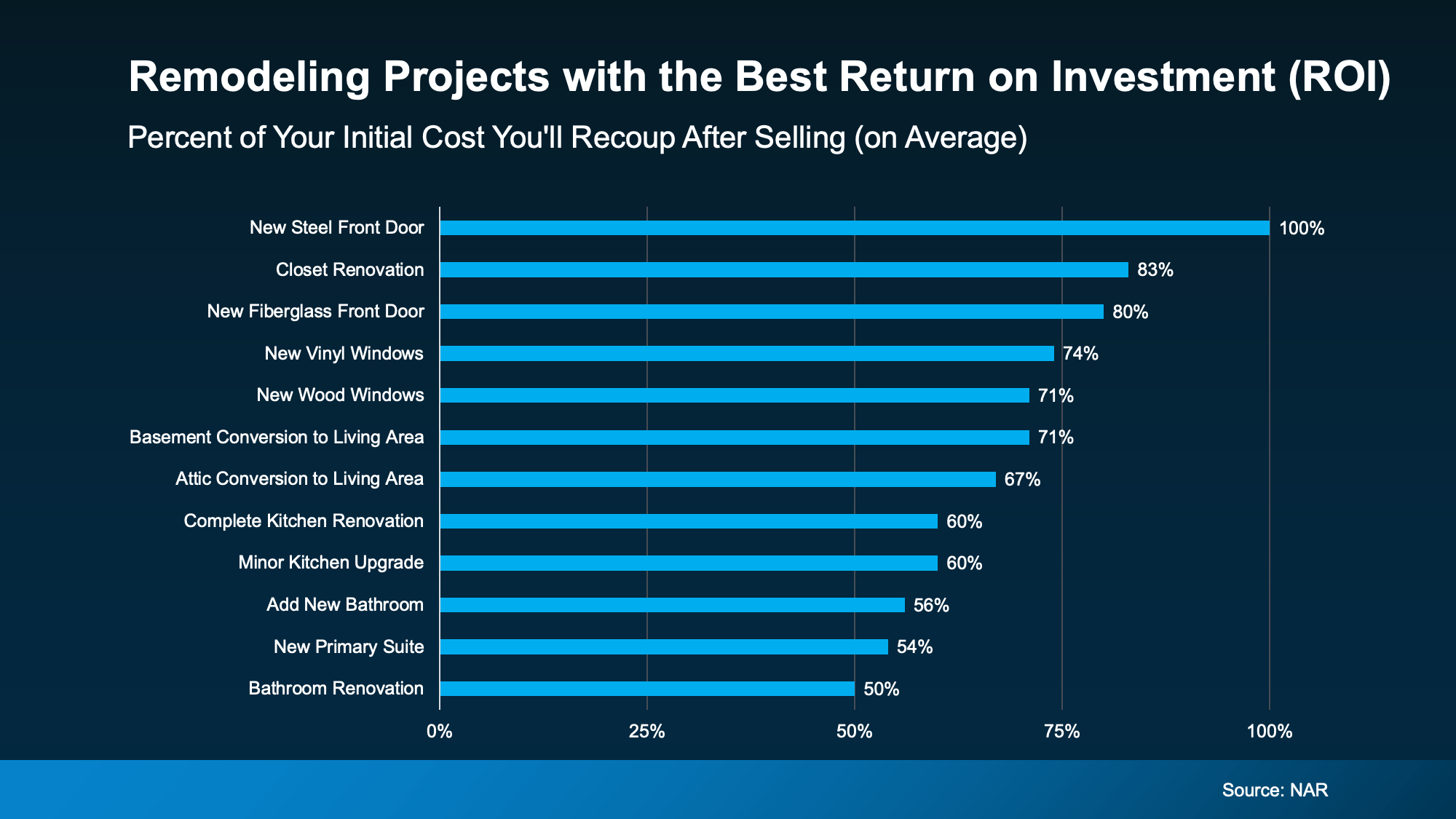

Here’s a quick rundown of the projects with the best potential to recoup your costs according to NAR (see graph below). While it’s a good starting point, just remember it can’t match the expertise an agent can provide.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

As you can see, there’s a wide range of projects on that list. Yes, some are bigger-ticket items, like kitchens or baths. But others are smaller updates with surprisingly strong ROI.

A new front door is a great project. But it’s not something to use your equity for. But revamping your kitchen? That’s where your equity can come in and lighten the load.

Where To Go from Here

Whether the project you’ve been thinking about is on this list or not, chat with an agent to make sure it’s worth the time, money, and effort before calling in any contractors.

Because the goal isn’t to do everything, it’s to invest where it counts.

And if you want to use your equity to get one of the bigger projects done, meet with a financial advisor too. Because you’ll want to make sure you’ll maintain a good loan-to-value (LTV) threshold even after using your equity. That way you have all the information you need to make your decision.

Bottom Line

Whether you’re selling next year or just giving your house some TLC, the right home improvements today can set you up for success tomorrow. And the best part? Your equity may be the key to making it happen.

What’s one upgrade you’ve been thinking about – and wondering if it’s worth it?

Have a quick conversation with an agent to find out if it’s the right decision for your home.

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

The Top Dealbreaker: Issues That Pop Up During the Inspection

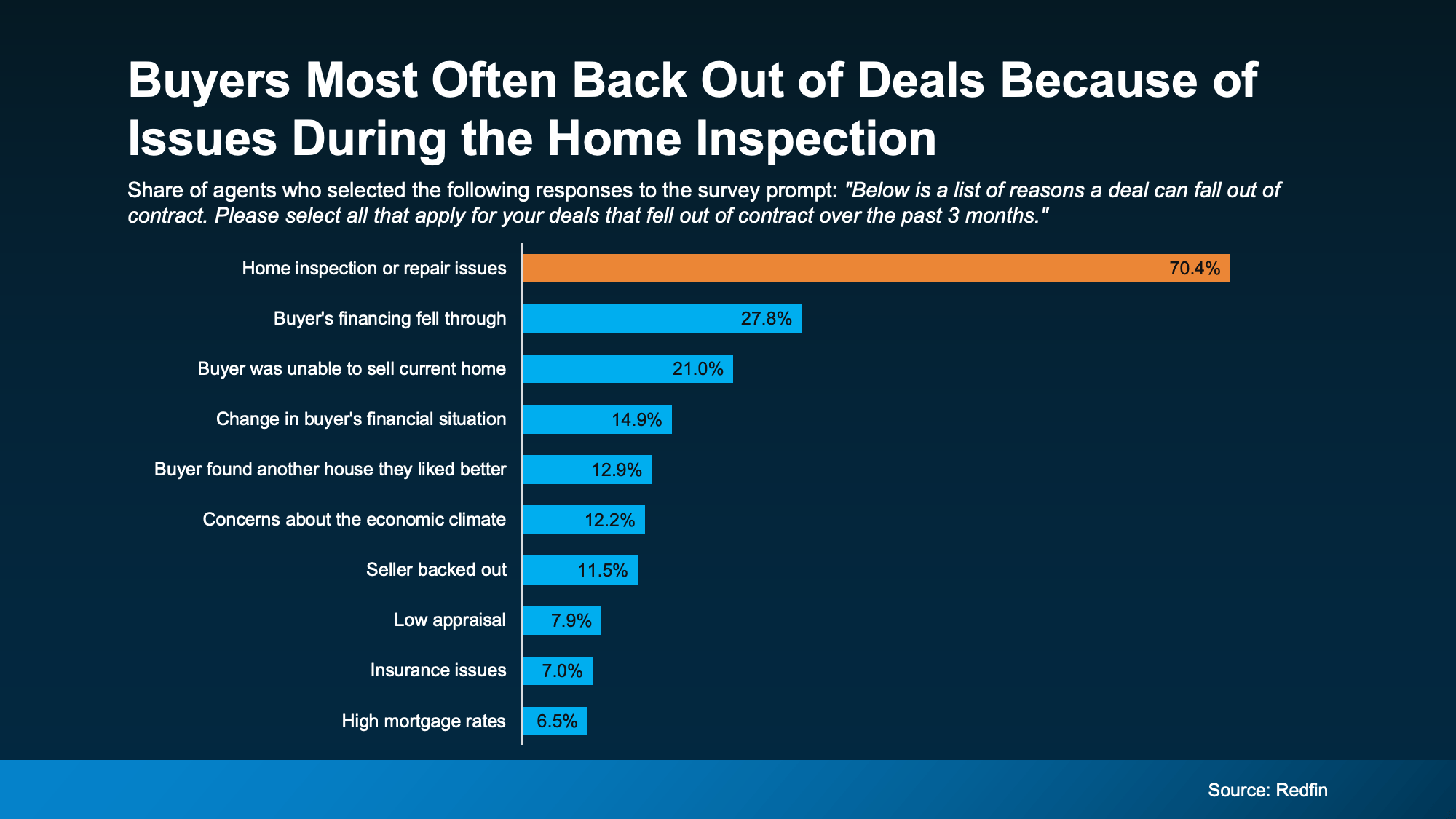

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

Why Fixing Things Before You List Matters More Today

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

How Your Agent Can Help Give You the Edge

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They’ll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

- Roof leaks or damage: sagging, leaking, etc.

- Plumbing problems: standing water, leaks, water damage, etc.

- Electrical concerns: outdated or exposed wiring, missing GFCI outlets, etc.

- HVAC issues: non-functioning units

- Pest or insect damage: termite colonies, etc.

- Hazardous materials: lead, mold, asbestos, etc.

- Safety/code violations: missing smoke detectors, windows stuck closed, etc.

- Structural problems: cracks in the foundation, sagging floors, etc.

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

The Benefits of a Pre-Listing Inspection

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

- Fix concerns before you list, or disclosue issues upfront

- Avoid having to respond or negotiate under pressure

- Stop scrambling to find contractors with availability before your closing date

But remember, you don’t have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

- Decide if a pre-listing inspection is worth it where you live

- Recommend a trusted inspector (if you decide to get one)

- Look at the results with you to identify true dealbreakers in your market

- Help you decide what to fix or what to credit

- Make sure you avoid over-spending or under-preparing

Bottom Line

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, connect with an agent.

Foreclosures are ticking up. And that may make your mind jump straight to thoughts of 2008 – specifically to what happened to the market during the housing crash. So, let’s do exactly what your brain already wants to do, and see if there’s any connection there.

The simple truth is foreclosure filings are rising. But they’re nowhere near crisis levels. And that’s not where they’re headed either. Here’s why.

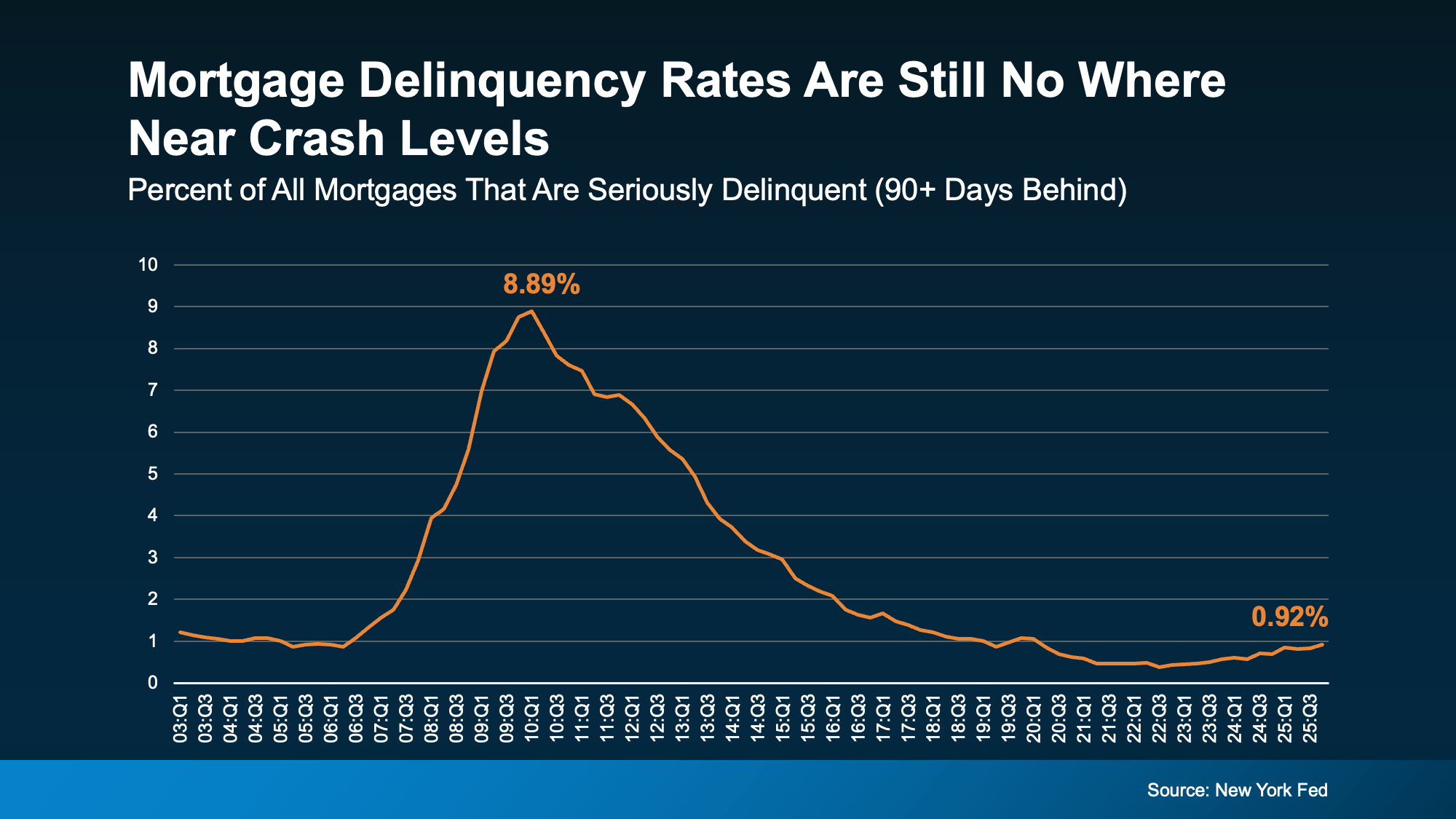

Take a look at serious delinquencies – loans where the homeowner is more than 90 days late on their mortgage payments.

While those have increased slightly, data from the New York Fed shows they still remain low. And they aren’t anywhere close to levels seen when the market crashed (see graph below):

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

In the years around the crash, they were up around 9%. That’s 1 in 11.

That’s a big difference.

And it’s important to remember not all delinquencies even become foreclosure filings. Some homeowners who are falling behind will work out repayment plans with their banks and lenders because banks don’t want to see a wave of foreclosures either.

That’s why foreclosure numbers are even lower than delinquencies. ATTOM shows only 0.3% of all homes are currently going through a foreclosure filing. And those won’t even all go to a full foreclosure. That’s not a wave. That’s a ripple at most.

If People Are Falling Behind on Payments, Why Aren’t There Even More Foreclosures?

And maybe you’re wondering, if people are struggling financially, why aren’t there more foreclosures? Here’s the easiest way to answer that.

When households feel financial pressure, they tend to prioritize their mortgage payment above almost everything else. Because the last thing they want to lose is their home.

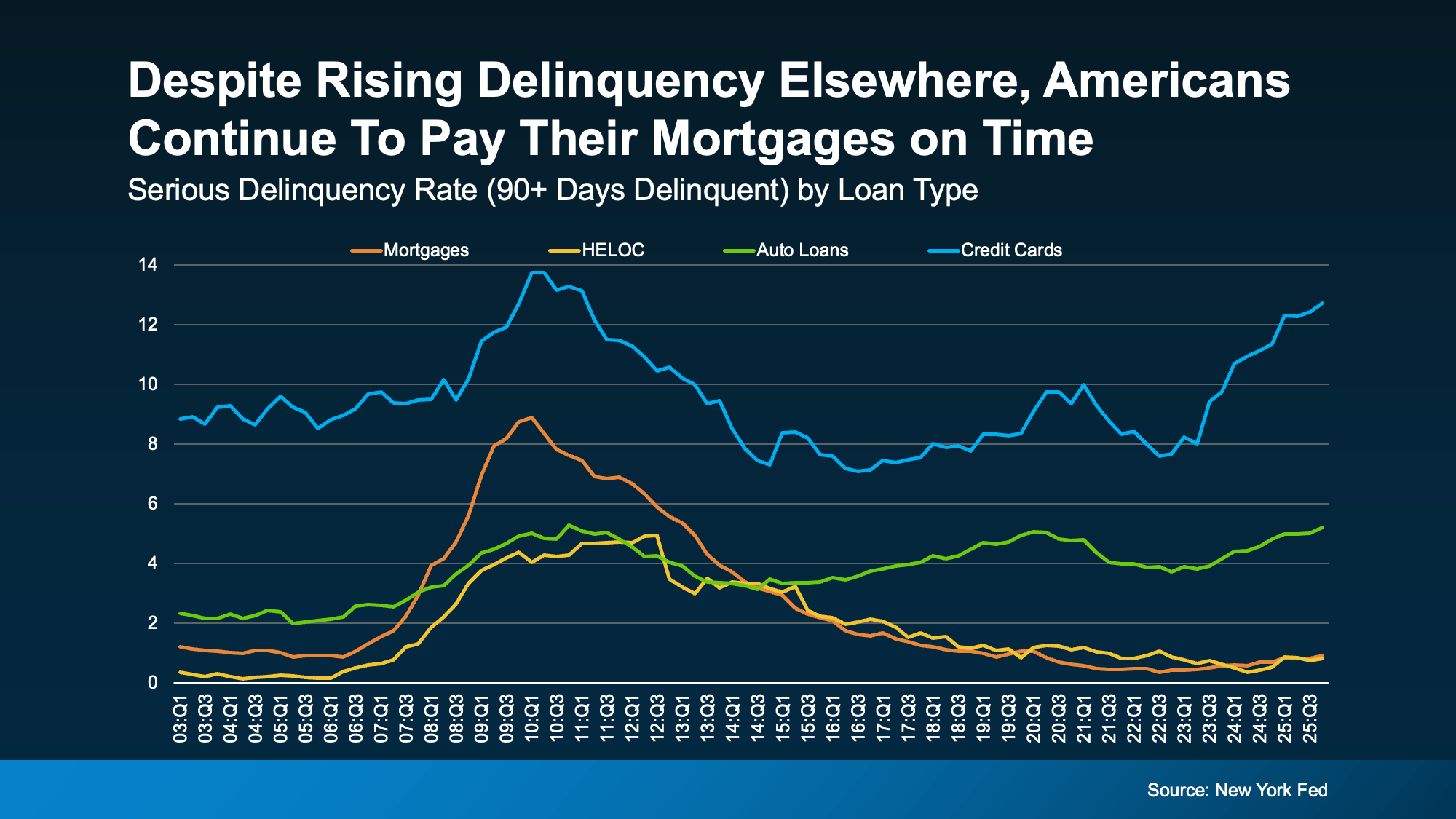

Data from the New York Fed shows serious delinquencies have risen more for credit cards and auto loans (the blue and green lines). But mortgage delinquencies and home equity lines of credit (borrowing against the value of your home) aren’t seeing the same big uptick (the yellow and orange lines). They’re a lot more stable overall.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

Home Equity Changes Everything

Many people have built significant equity over the past several years. And that creates options. As Daren Blomquist, VP of Market Economics at Auction.com, explains:

“Distressed homeowners… many times they still have equity in their homes. There’s an opportunity for them to sell that home, avoid foreclosure, and walk away with equity.”

That’s a major difference from 2008. Back then, many homeowners owed more than their homes were worth. And selling wasn’t an easy solution. Today, for many people, it is. And even in situations where equity isn’t enough, homeowners are encouraged to contact their loan servicer early to explore alternatives to foreclosure.

Bottom Line

Are foreclosure filings rising slightly? Yes. Are they anywhere near crash territory? No. And homeowners today have far more equity and flexibility than they did during the crash.

If you’re concerned about what you’re seeing in the headlines, the best move isn’t panic, it’s perspective. And the data right now says this isn’t 2008 all over again.

You Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

The Remodel You’ve Been Dreaming About May Be Closer Than You Think

Affordability Has Improved in All 50 States

-

Affordability4 weeks ago

Affordability4 weeks agoRenting vs. Buying: The Numbers Might Surprise You

-

For Sellers4 weeks ago

For Sellers4 weeks agoTop Mistakes Homeowners Are Making in 2026 (And How To Avoid Them)

-

For Sellers3 weeks ago

For Sellers3 weeks agoSpring Sellers Have an Edge. Here’s Why.

-

Downsize3 weeks ago

Downsize3 weeks agoThe Hidden Advantage Repeat Buyers Have Right Now

-

Equity3 weeks ago

Equity3 weeks agoAre Home Prices Dropping? Here’s the Real Story.

-

Agent Value2 weeks ago

Agent Value2 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability2 weeks ago

Affordability2 weeks agoShould You Wait for Lower Rates?

-

For Buyers2 weeks ago

For Buyers2 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

You must be logged in to post a comment Login