Affordability

Affordability Has Improved in All 50 States

For the past few years, affordability has been what’s stopped a lot of buyers in their tracks. Maybe it stopped you, too.

At some point you probably did the math, looked at the monthly payment, and decided to pause your search and wait for things to get better. But here’s something you may have missed while you’ve been sitting on the sidelines.

Over the last year, housing affordability has improved in all 50 states. Yes, you read that right. It’s gotten better in every single state.

That’s based on new research coming out of First American. And while housing is still fairly expensive compared to historical standards, the pressure buyers felt over the last few years is finally starting to ease.

Some Areas Are Seeing Bigger Improvements

The first thing you need to know is that this isn’t just happening in one region or in a small handful of cities. The trend is happening almost everywhere.

Sure, individual states, cities, and even neighborhoods are going to vary – sometimes by a lot. But overall, more buyers are able to buy again. And in 48 of the top 50 metros, affordability has improved over the past year.

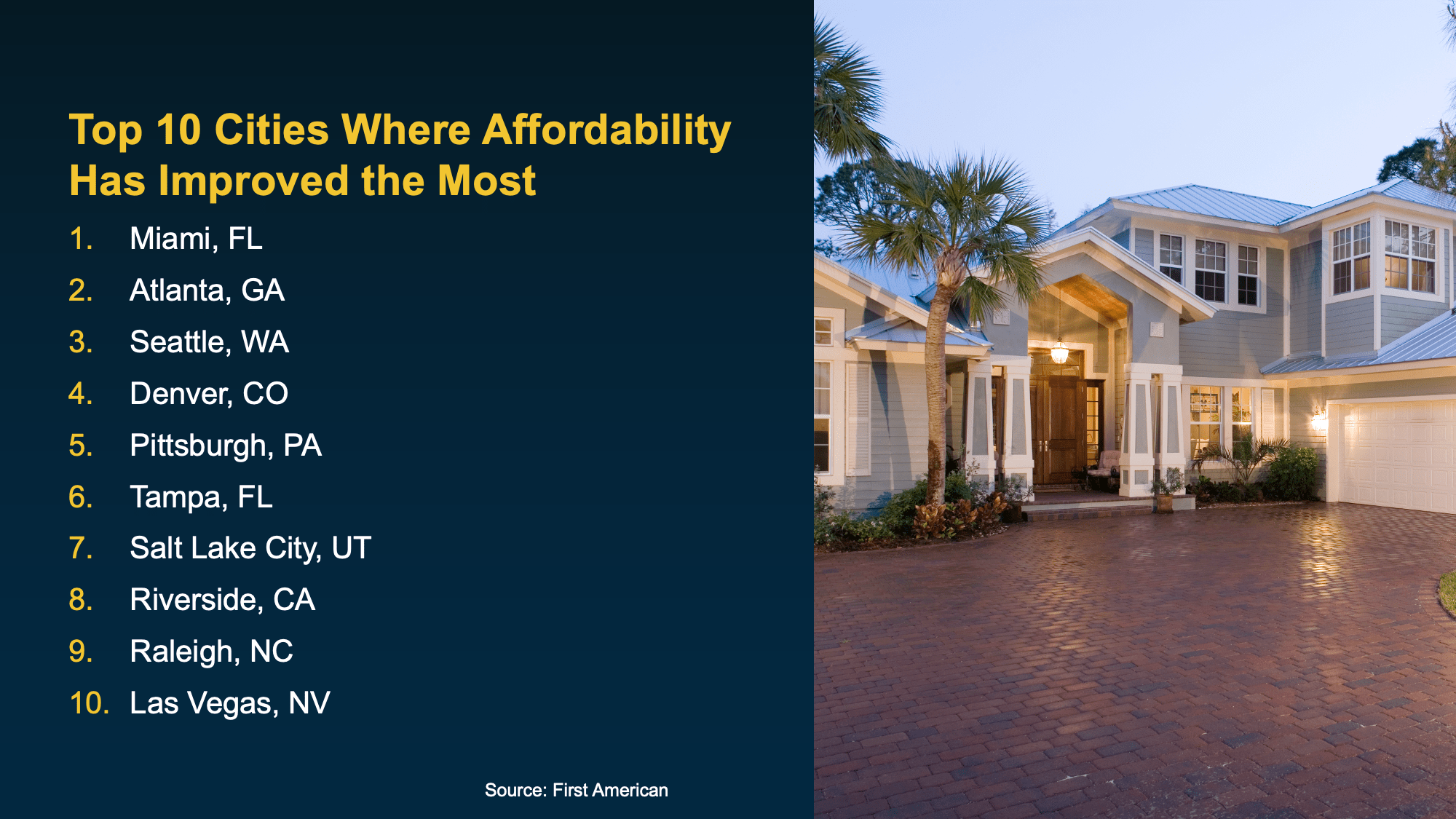

That same research breaks down which cities are seeing the biggest gains:

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

When buyers have more choices, it creates a healthier balance in the market and that can help bring affordability back within reach. With homes up for grabs, it opens the door a bit wider for buyers to negotiate with sellers for credits, price cuts, and more. And it gives you more chances to find a house that works for your needs and budget.

It may make more of a difference than you think.

None of this means affordability challenges have completely disappeared. Buying a home is still a big financial decision. But the trend is moving in a direction many buyers have been waiting for.

As Chen Zhao, Head of Economic Research at Redfin, puts it:

“The housing affordability crisis is showing signs of easing . . . opening the door for more Americans to make the jump to homeownership.”

Bottom Line

If you were holding off on buying, this could be exactly the signal you’ve been waiting so long for. To find out how much affordability’s improved in your area, connect with a local real estate agent.

Saving for a down payment can feel like the hardest part of buying a home. And with affordability as tight as it’s been lately, it’s fair to wonder how anyone manages it right now. Here’s something you may not have seen coming.

Some people are getting their foot in the door with a smaller down payment.

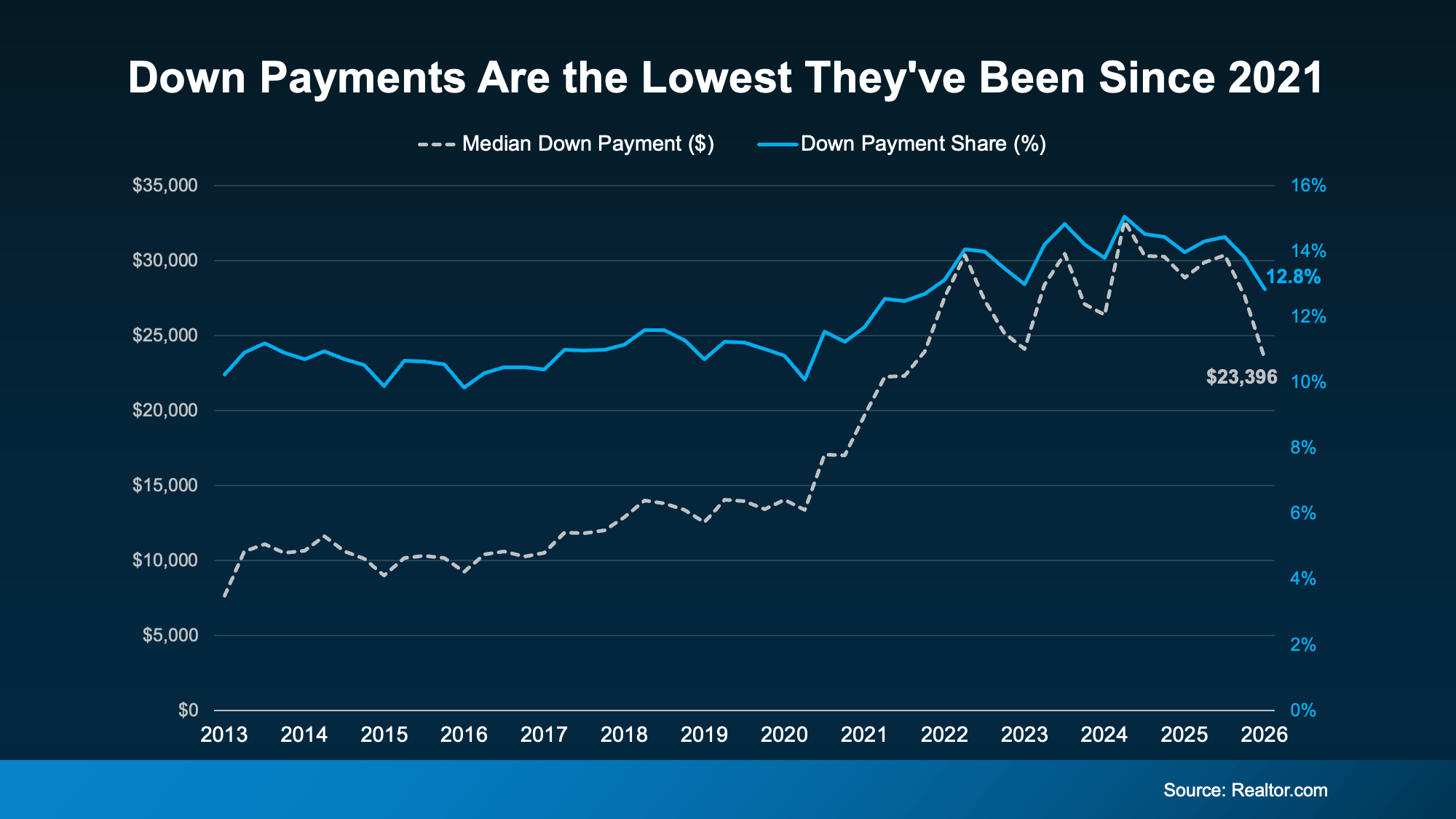

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that’s around $5,000 below what was typical the year before (a 19% drop year over year). That’s the lowest down payments have been since 2021 (see graph below):

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

There are a few things driving the trend:

-

Less competition between buyers. Part of it comes down to a more balanced market. With buyers facing less competition than they did a few years ago, there’s less pressure to put a big sum down just to stand out.

-

More moderate home prices. Your down payment is a percentage of the purchase price. So, as price growth cools, the amount you need to put down may change too. In a lot of markets, prices have slowed or leveled off, and some areas are even seeing slight dips. That can translate into smaller down payments.

-

Buyers opting for loans with lower down payments. More buyers are also turning to government-backed loans, like FHA and VA, which often need little or no money down. FHA loans have made up more than 24% of purchase mortgages for five straight quarters, and VA loans recently hit their highest share in over a decade, according to Mortgage Professional America.

But even a smaller down payment is still a significant chunk of cash, and saving it can be hard. So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

Help You May Not Know You Qualify For

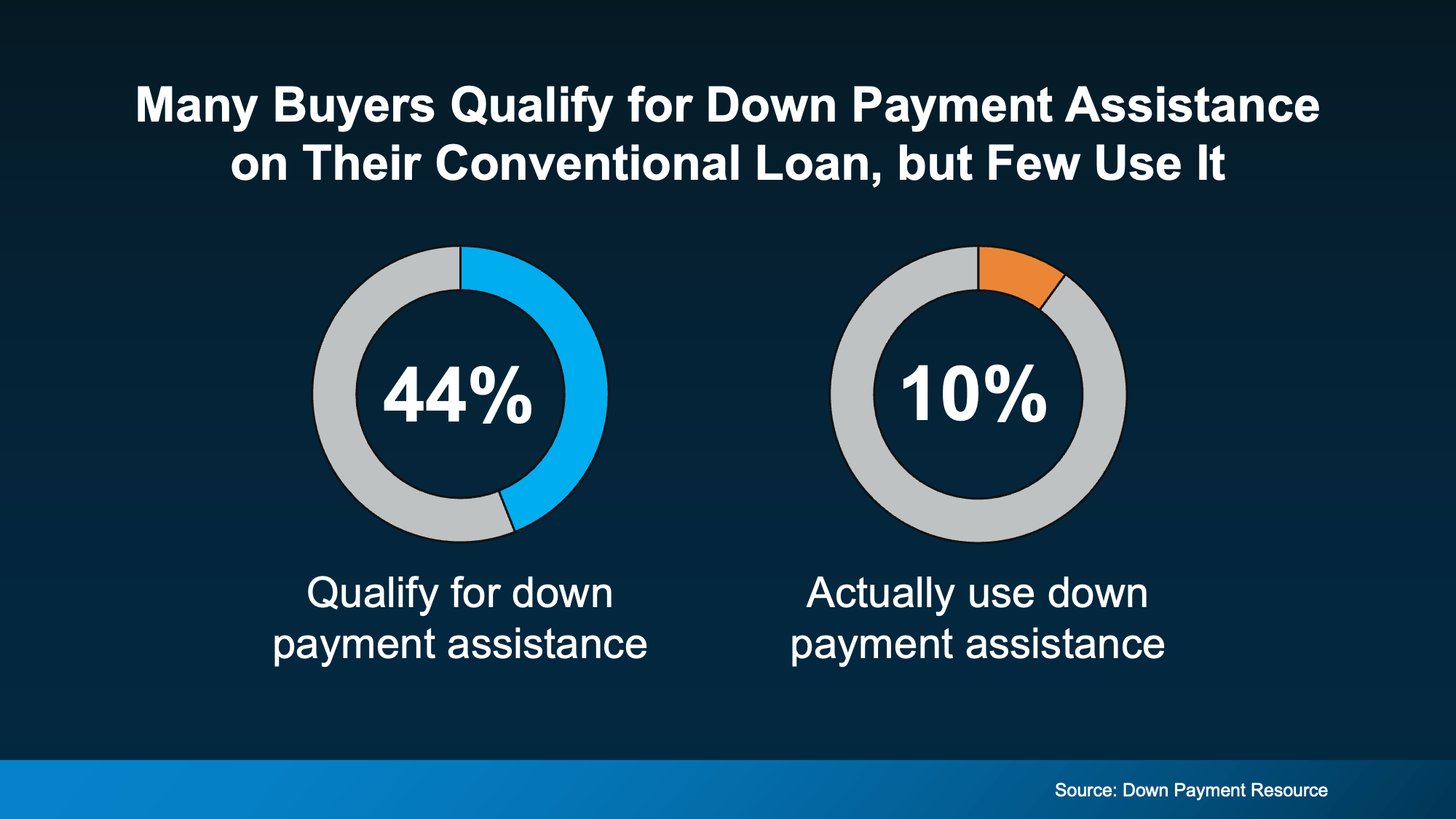

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

-

There are more than 2,600 down payment assistance programs available

-

More than half (62%) are designed to help first-time buyers

-

38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

-

62% are open to buyers earning $100,000 or more

A Boost from Loved Ones

For a growing number of buyers, help comes from closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support most often goes toward the down payment, followed by help qualifying for a mortgage and covering closing costs. Chris Birk, VP of Mortgage Insight at Veterans United, puts it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, it can make a real difference in how soon you can buy.

Bottom Line

Down payments are smaller than they’ve been in years, and that opens the door for more buyers.

And with added help from assistance programs and a little help from loved ones, you may have more ways forward than you realized. Connect with a trusted lender to talk through your options.

Open up a home search and you’ll see them. Listings that have been on the market for two months. Three. Some longer.

Most buyers scroll right past them, assuming something’s wrong with the house. But that instinct could be costing you, since the longer a home sits, the more motivated the seller usually gets.

Where Some Buyers Are Finding Better Deals

If affordability has been your #1 hurdle to buying, here’s a surprisingly simple strategy that could help you finally get your foot in the door. Start with the homes that have been sitting the longest. That’s often where the best deals are.

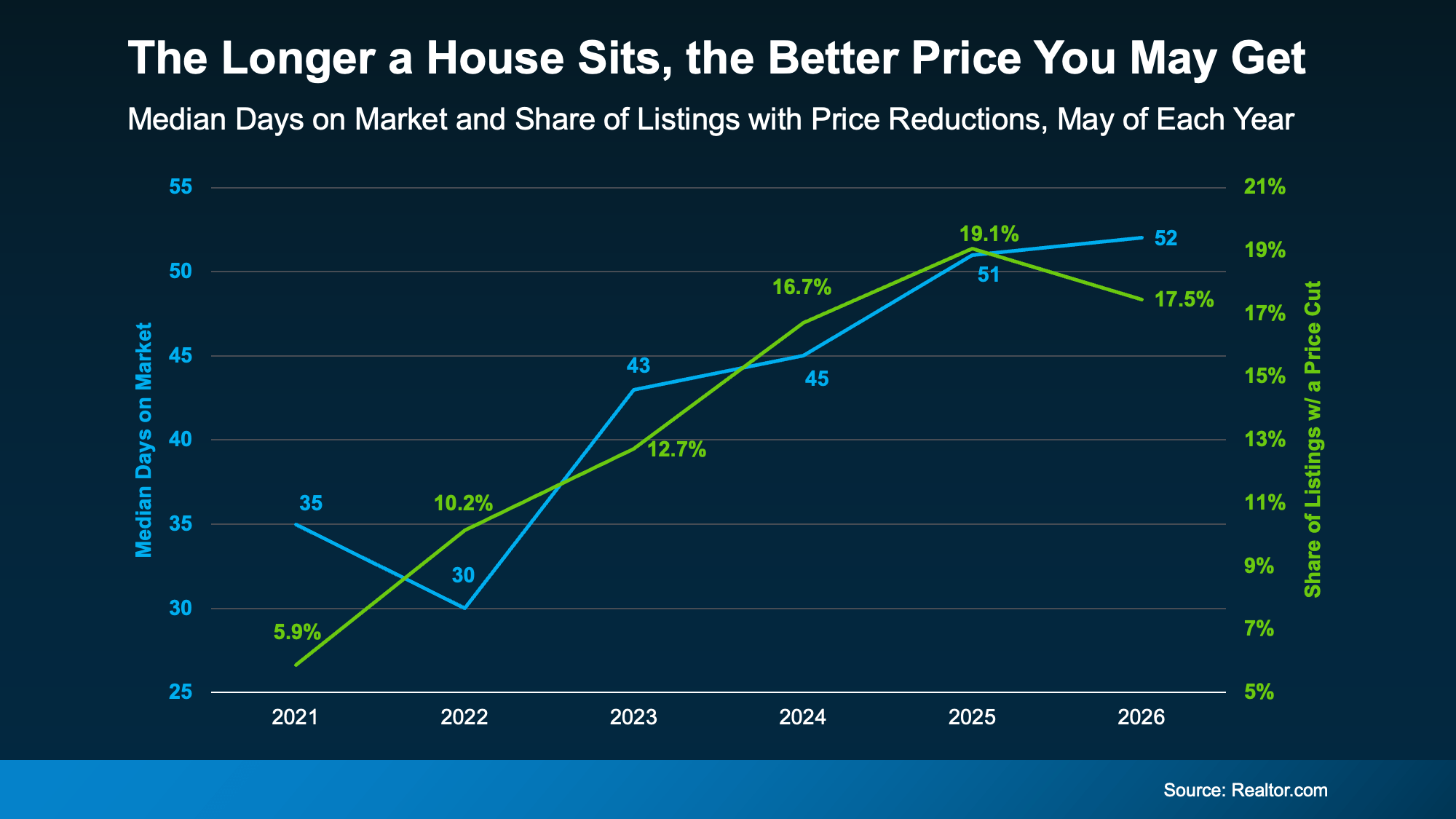

Here’s why. Data from Realtor.com shows there’s a connection between longer time on the market and lower sales prices. Basically, the longer a house sits, the more likely it is that the seller will reduce the price (see graph below):

The blue line tracks how long homes stay on the market, while the green line tracks the share of homes getting a price reduction. As one climbs, so does the other.

And if you focus on these homes that are just sitting and waiting, the opportunity for you is bigger than you may think right now.

Redfin data shows there’s $347 billion worth of stale listings on the market right now – more than ever before for this time of year. So, ask your agent to filter listings for you from oldest to newest. The home that fits your budget might already be there. Just further down the list than you thought.

Lingering Doesn’t Always Mean Something’s Wrong

Let’s say you do that and something catches your eye. Still, you might be questioning why the home has been sitting in the first place. Just remember, sometimes it has nothing to do with the home itself.

According to Redfin, common causes are:

-

The asking price was set too high to start

-

The home didn’t show well online

-

There are a lot of homes for sale in the area, so it just got buried

So, nothing that’s necessarily a dealbreaker, or even anything that’s wrong with the home itself. If there’s a real issue, a thorough inspection will surface it. And that’s information you can use to negotiate. Not a reason to assume it’s a house worth skipping over.

How To Turn a Lingering Listing into a Win

So how do you capitalize on a lingering listing? According to USA Today, you have two main levers to pull.

The first is price. Work with your agent to study what comparable homes recently sold for, then build an offer around that. Coming in below asking price is fair game when a home has been sitting.

The second is concessions. If a seller won’t budge much on price, they may still help in other ways, like covering some closing costs, repair credits, or even a mortgage rate buydown that lowers your monthly payment.

A local agent has the context to tell which homes are the real opportunities and which are skippable.

Bottom Line

A house sitting on the market isn’t always a glaring red flag. In today’s market, it may be your best opportunity yet.

For help deciding which lingering listings are actually worth a second look, connect with a local real estate agent.

If affordability has been the biggest thing standing between you and a home, there’s a little good news.

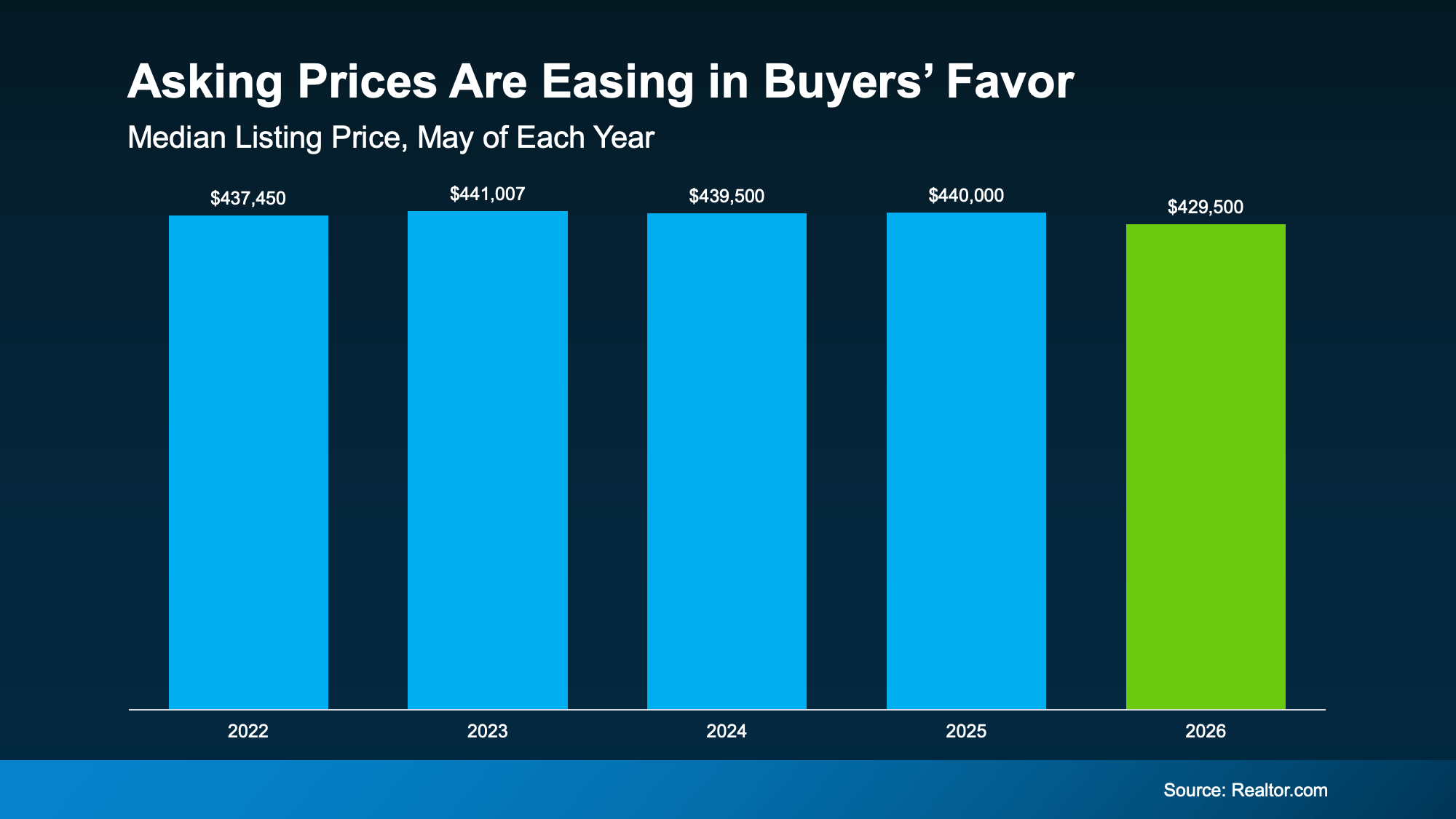

Asking prices have started to come down.

The typical seller listed their house for a median of $429,500 in May. That’s 2.4% lower than a year ago, according to Realtor.com. On its own, that won’t transform what you can afford, but in today’s market every little bit helps and it signals a broader shift taking place.

Buyers Are Finally Catching a Break

Check out this data from Realtor.com and you can see this is the first May in years where buyers have caught any sort of break price-wise.

Each May from 2022-2025, things held pretty steady. But this year? You can see that more noticeable shift in your favor (see graph below):

While the dip from $440,000 to $429,500 isn’t a big one, it gives you more breathing room. And that’s not a small thing when affordability has been this tough.

Now, lower asking prices don’t mean every home is suddenly within your range. But they do show buyers are gaining a little ground.

And in today’s market, a little ground can go a long way.

What That Means for the Housing Market

And just in case this crossed your mind, this is good news for your move, not bad news for the market as a whole.

The subtle dip from last May to this one shows prices are easing, but they’re not dropping off a cliff. What this is actually a sign of is that the market’s rebalancing now that the number of homes for sale has grown.

Buyers have a bit more power again, and sellers know they can’t name just any price and expect their house to sell. They either meet the market where it is, or face a price cut later. And in general, sellers would rather avoid a price cut. As the New York Post explains:

“Rather than swinging for the fences with pandemic-era price tags, sellers are increasingly coming to terms with a new reality. The share of listings featuring price cuts actually fell to 17.5% in May, suggesting homeowners are doing their homework before putting up a “For Sale” sign instead of chasing unrealistic numbers and cutting later.“

This signals a broader change in the market.

Seller expectations have been skewed a little high since the pandemic buying frenzy – you’ve probably felt that firsthand. But now, things are starting to normalize. It could mean less back-and-forth to land on a fair number. And homes should be priced a bit more realistically from the start.

Bottom Line

If affordability has been your top concern, the recent dip in prices is an opening. Connect with a local real estate agent to see what that looks like in your area.

Down Payments Are Smaller Than They’ve Been Since 2021

The Housing Market Is Stronger Than You Think

The 1 Factor That Explains Everything Happening with Home Prices Right Now

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoTwo Big Reasons To Move This Summer

-

Affordability4 weeks ago

Affordability4 weeks agoWhat Rising Inflation Means for Your Move

-

Affordability4 weeks ago

Affordability4 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Affordability3 weeks ago

Affordability3 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers3 weeks ago

For Sellers3 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers2 weeks ago

For Buyers2 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

-

Agent Value2 weeks ago

Agent Value2 weeks agoIs It Still a Seller’s Market? Here’s What the Data Says.

-

Affordability2 weeks ago

Affordability2 weeks agoThat House That’s Been Sitting Could Be Your Best Shot at a Deal

You must be logged in to post a comment Login