For Buyers

5 Simple Graphs Proving This Is NOT Like the Last Time

With all of the volatility in the stock market and uncertainty about the Coronavirus (COVID-19), some are concerned we may be headed for another housing crash like the one we experienced from 2006-2008. The feeling is understandable. Ali Wolf, Director of Economic Research at the real estate consulting firm Meyers Research, addressed this point in a recent interview:

“With people having PTSD from the last time, they’re still afraid of buying at the wrong time.”

There are many reasons, however, indicating this real estate market is nothing like 2008. Here are five visuals to show the dramatic differences.

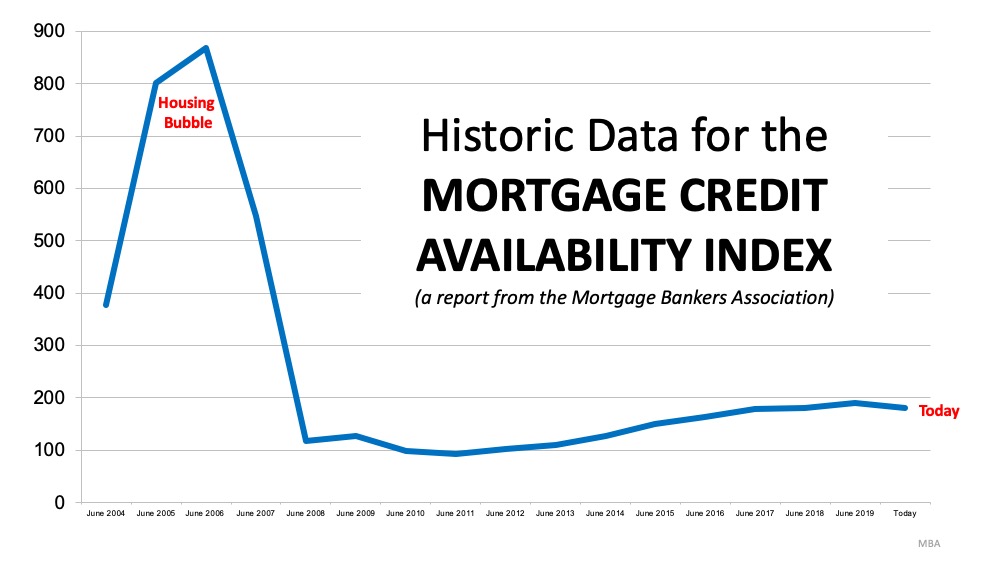

1. Mortgage standards are nothing like they were back then.

During the housing bubble, it was difficult NOT to get a mortgage. Today, it is tough to qualify. The Mortgage Bankers’ Association releases a Mortgage Credit Availability Index which is “a summary measure which indicates the availability of mortgage credit at a point in time.” The higher the index, the easier it is to get a mortgage. As shown below, during the housing bubble, the index skyrocketed. Currently, the index shows how getting a mortgage is even more difficult than it was before the bubble.

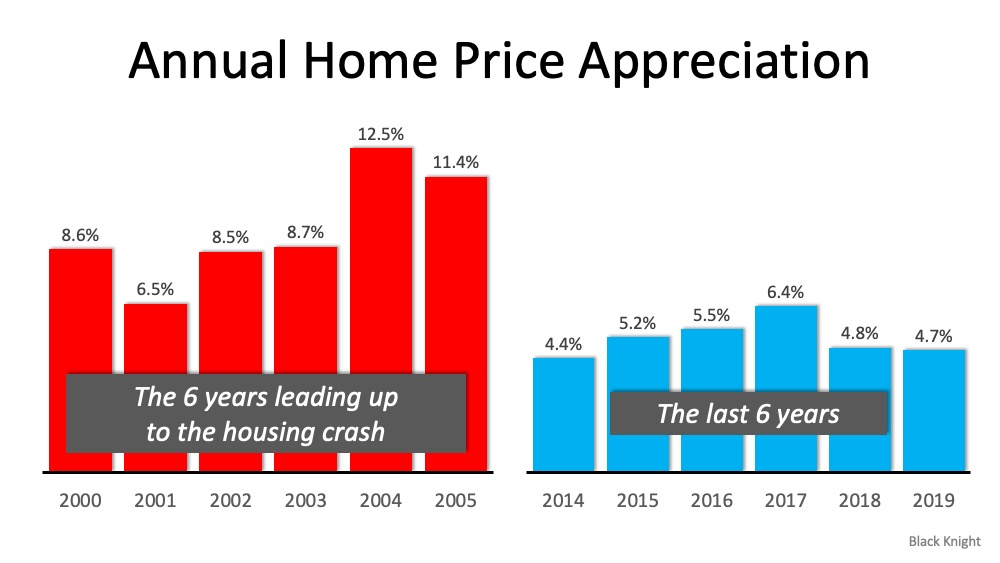

2. Prices are not soaring out of control.

Below is a graph showing annual house appreciation over the past six years, compared to the six years leading up to the height of the housing bubble. Though price appreciation has been quite strong recently, it is nowhere near the rise in prices that preceded the crash. There’s a stark difference between these two periods of time. Normal appreciation is 3.6%, so while current appreciation is higher than the historic norm, it’s certainly not accelerating beyond control as it did in the early 2000s.

There’s a stark difference between these two periods of time. Normal appreciation is 3.6%, so while current appreciation is higher than the historic norm, it’s certainly not accelerating beyond control as it did in the early 2000s.

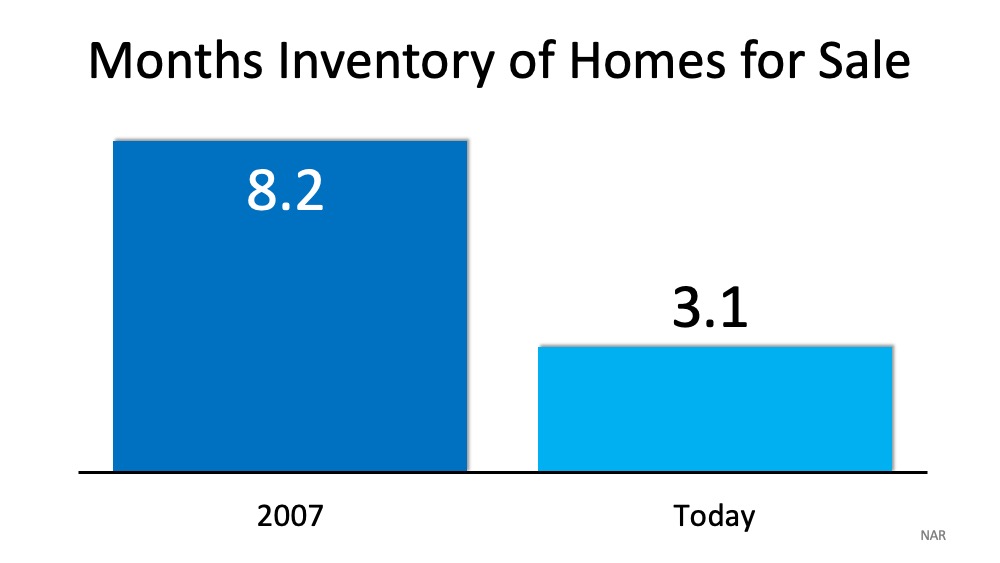

3. We don’t have a surplus of homes on the market. We have a shortage.

The months’ supply of inventory needed to sustain a normal real estate market is approximately six months. Anything more than that is an overabundance and will causes prices to depreciate. Anything less than that is a shortage and will lead to continued appreciation. As the next graph shows, there were too many homes for sale in 2007, and that caused prices to tumble. Today, there’s a shortage of inventory which is causing an acceleration in home values.

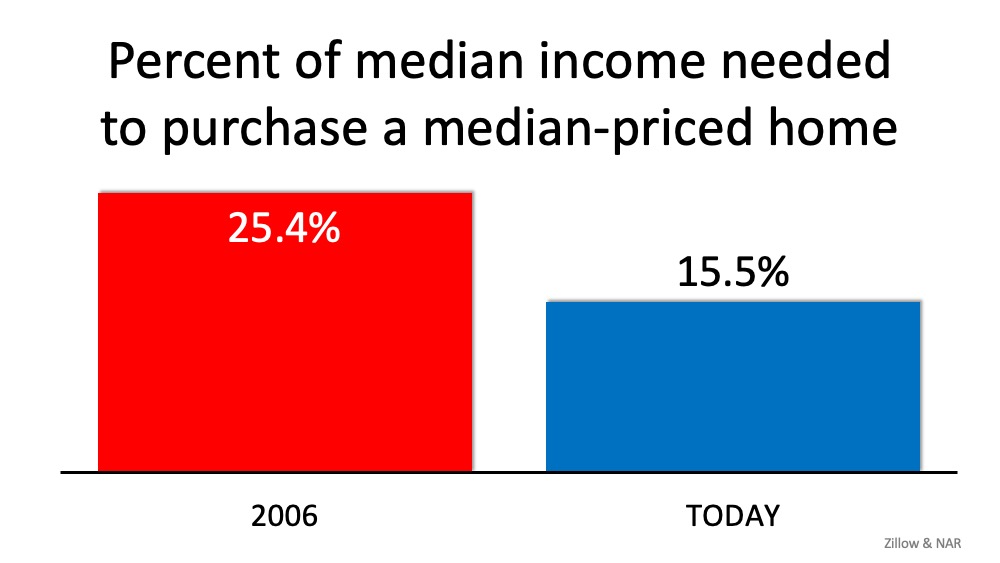

4. Houses became too expensive to buy.

The affordability formula has three components: the price of the home, the wages earned by the purchaser, and the mortgage rate available at the time. Fourteen years ago, prices were high, wages were low, and mortgage rates were over 6%. Today, prices are still high. Wages, however, have increased and the mortgage rate is about 3.5%. That means the average family pays less of their monthly income toward their mortgage payment than they did back then. Here’s a graph showing that difference:

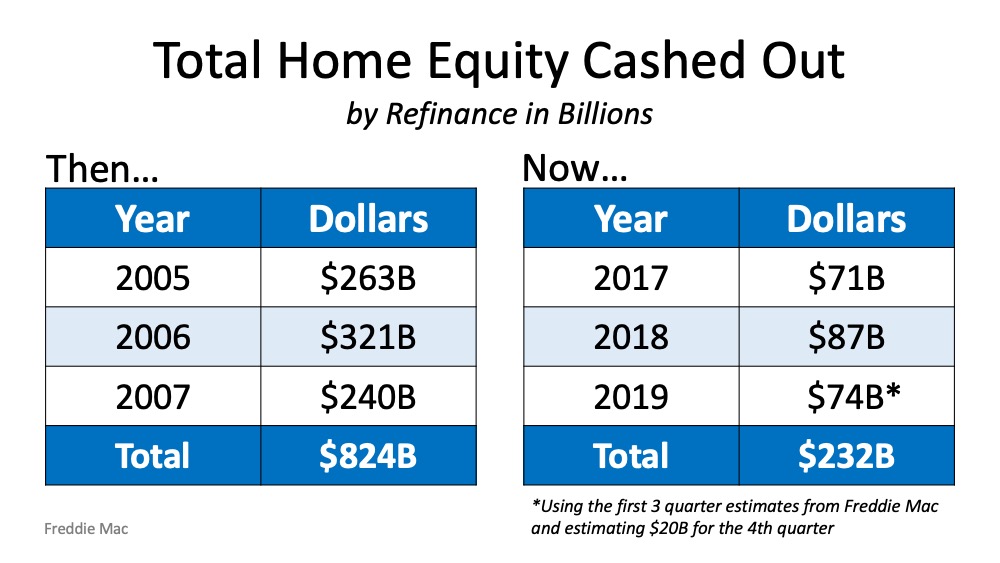

5. People are equity rich, not tapped out.

In the run-up to the housing bubble, homeowners were using their homes as a personal ATM machine. Many immediately withdrew their equity once it built up, and they learned their lesson in the process. Prices have risen nicely over the last few years, leading to over fifty percent of homes in the country having greater than 50% equity. But owners have not been tapping into it like the last time. Here is a table comparing the equity withdrawal over the last three years compared to 2005, 2006, and 2007. Homeowners have cashed out over $500 billion dollars less than before: During the crash, home values began to fall, and sellers found themselves in a negative equity situation (where the amount of the mortgage they owned was greater than the value of their home). Some decided to walk away from their homes, and that led to a rash of distressed property listings (foreclosures and short sales), which sold at huge discounts, thus lowering the value of other homes in the area. That can’t happen today.

During the crash, home values began to fall, and sellers found themselves in a negative equity situation (where the amount of the mortgage they owned was greater than the value of their home). Some decided to walk away from their homes, and that led to a rash of distressed property listings (foreclosures and short sales), which sold at huge discounts, thus lowering the value of other homes in the area. That can’t happen today.

Bottom Line

If you’re concerned we’re making the same mistakes that led to the housing crash, take a look at the charts and graphs above to help alleviate your fears.

Imagine waiting a year to buy a home, only to find mortgage rates haven’t changed much. That may sound frustrating.But it’s a real possibility.

A lot of people are putting their plans on hold because they believe much lower mortgage rates are right around the corner. But, based on today’s forecasts, that may not happen. And you should know that before you decide what to do.

Let’s look at why experts don’t expect a dramatic drop in rates – and the options that could help you buy anyway. Because even if rates don’t fall, you can still move. Here’s how.

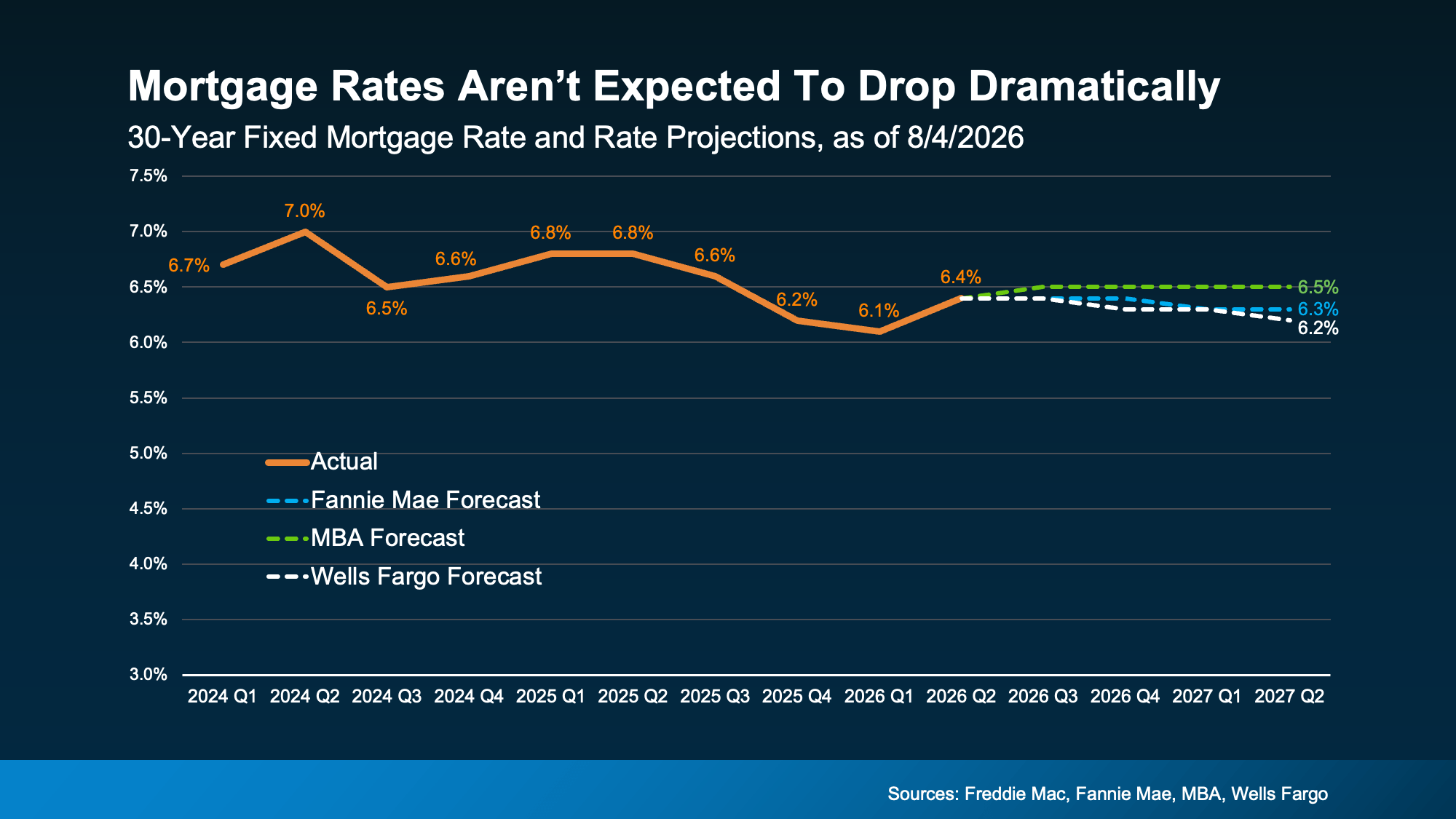

1. Mortgage Rates Aren’t Expected To Fall in a Meaningful Way

If you’re waiting for rates to fall, you’re not alone. A recent survey from Clever-Best Interest found 42% of people believe mortgage rates will drop below 5% this year.

The challenge is, that’s not what the experts who study mortgage rates every day are expecting.

Forecasts from Fannie Mae, the Mortgage Bankers Association, and Wells Fargo all show mortgage rates staying relatively steady in the low-to-mid 6% range through at least mid-2027 (see graph below):

Why? Rates are influenced by inflation, the overall economy, Treasury yields, Federal Reserve policy, global events, and a lot of other moving pieces. And right now, those factors simply aren’t pointing toward the kind of dramatic rate drop many buyers are waiting for.

Could rates move a little? Of course. But if you’re holding out for a bigger drop, today’s forecasts suggest you may be waiting a lot longer than you expect.

2. Inflation Is Still Elevated – And That’s Working Against Lower Rates

One reason experts aren’t expecting rates to fall much? Inflation. Generally speaking, high inflation is the enemy of lower mortgage rates.

And after a period of relative stability from mid 2023 to late 2025, recent data shows inflation has actually been trending higher lately (see graph below):

In other words, one of the biggest ingredients needed for much lower mortgage rates simply isn’t in place today. That helps explain why experts aren’t forecasting the kind of meaningful decline so many buyers are hoping for.

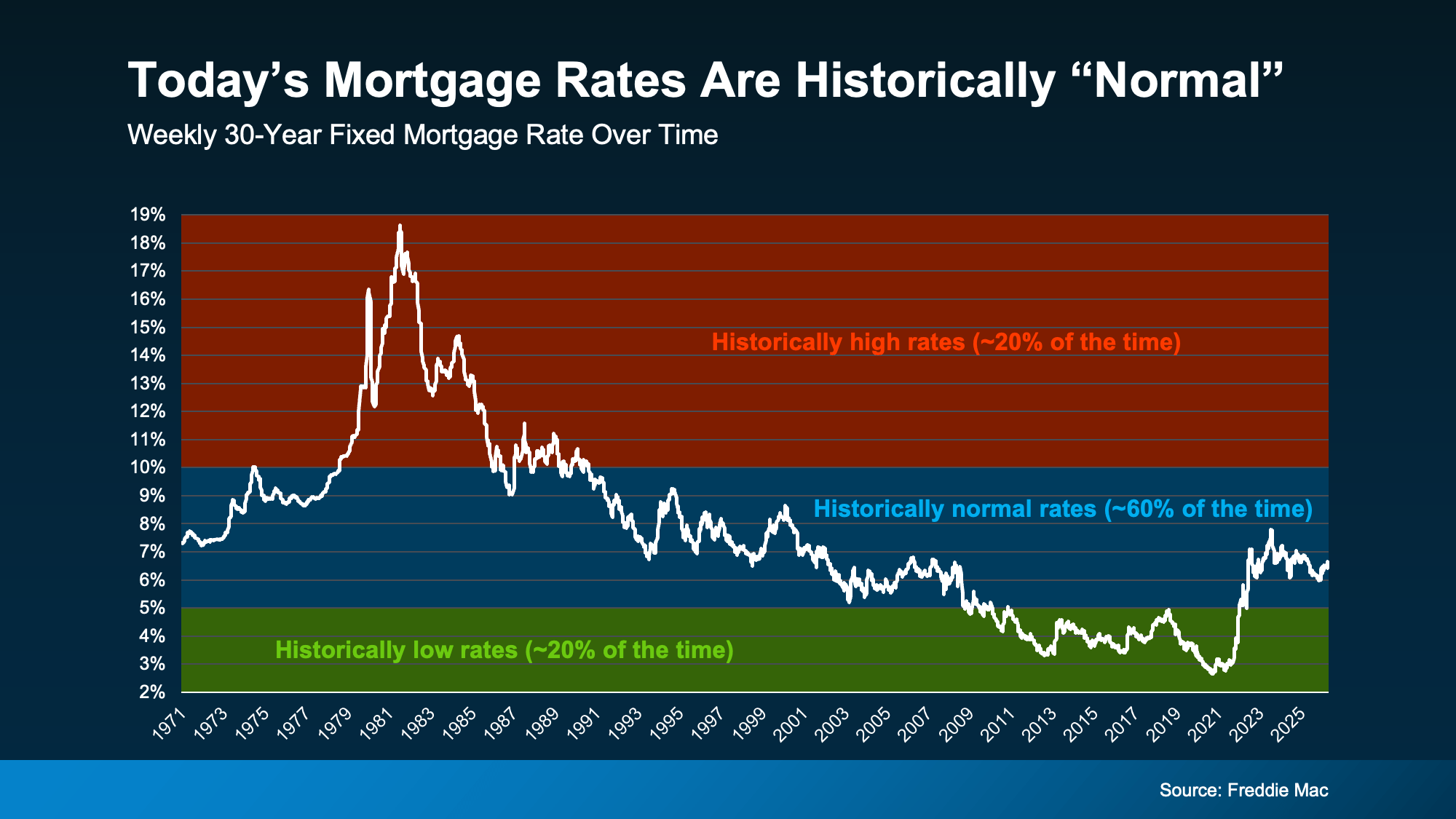

3. Today’s Rates Aren’t High, They’re “Normal”

And this may be the biggest mindset shift of all. The reality is, while today’s rates may feel high compared to a few years ago, they’re not high. They’re normal.

Historically, mortgage rates have spent the majority of their time somewhere between about 5% and 10%. And data from Freddie Mac shows we’re actually well in that range today. It just feels high because we all remember the ultra-low rates homeowners got during the pandemic (see graph below):

Now, this doesn’t suddenly make a 6% mortgage feel exciting. But it does remind us that waiting for super low rates again may not be a realistic strategy.

So… What Should You Do Instead?

None of this is meant to convince you that you have to buy today. You don’t. But if you need to because something in your life’s changed, there are still ways to find better affordability without waiting for mortgage rates to fall.

-

Check out newly built homes. Many builders are offering incentives to attract buyers, including price cuts, potentially lower rates, free upgrades, and more.

-

Ask about an adjustable-rate mortgage (ARM). If you don’t plan to stay in the home long-term, an ARM may offer a lower initial interest rate than a traditional 30-year fixed mortgage. It’s not the right choice for everyone, but it’s worth asking a lender if it fits your plans.

-

Look into mortgage rate buydowns. This is when you pay upfront to reduce your mortgage rate so you can get for a lower monthly payment without waiting for rates to fall.

-

Find out about assumable mortgages. An assumable mortgage allows you to take over the seller’s existing loan, including its lower mortgage rate.

The important thing is you shouldn’t assume waiting is your only option.

Talk with your real estate agent and lender about whether one of these strategies could be a good fit for you.

Bottom Line

If you’ve been putting your home search on hold because you’re convinced mortgage rates will be much lower soon, it may be worth taking another look at that strategy.

Connect with an agent or lender so you have an expert who can at least walk you through your options and decide whether waiting really puts you in a better position – or just keeps you on the sidelines a little longer.

For years, a lot of would-be homebuyers have worried about the same thing. How do you compete with big investors who can swoop in, pay cash, and snap up the houses you want?

Well, worry a little less. Because right now, those big investors aren’t buying up the market. They’re backing out of it.

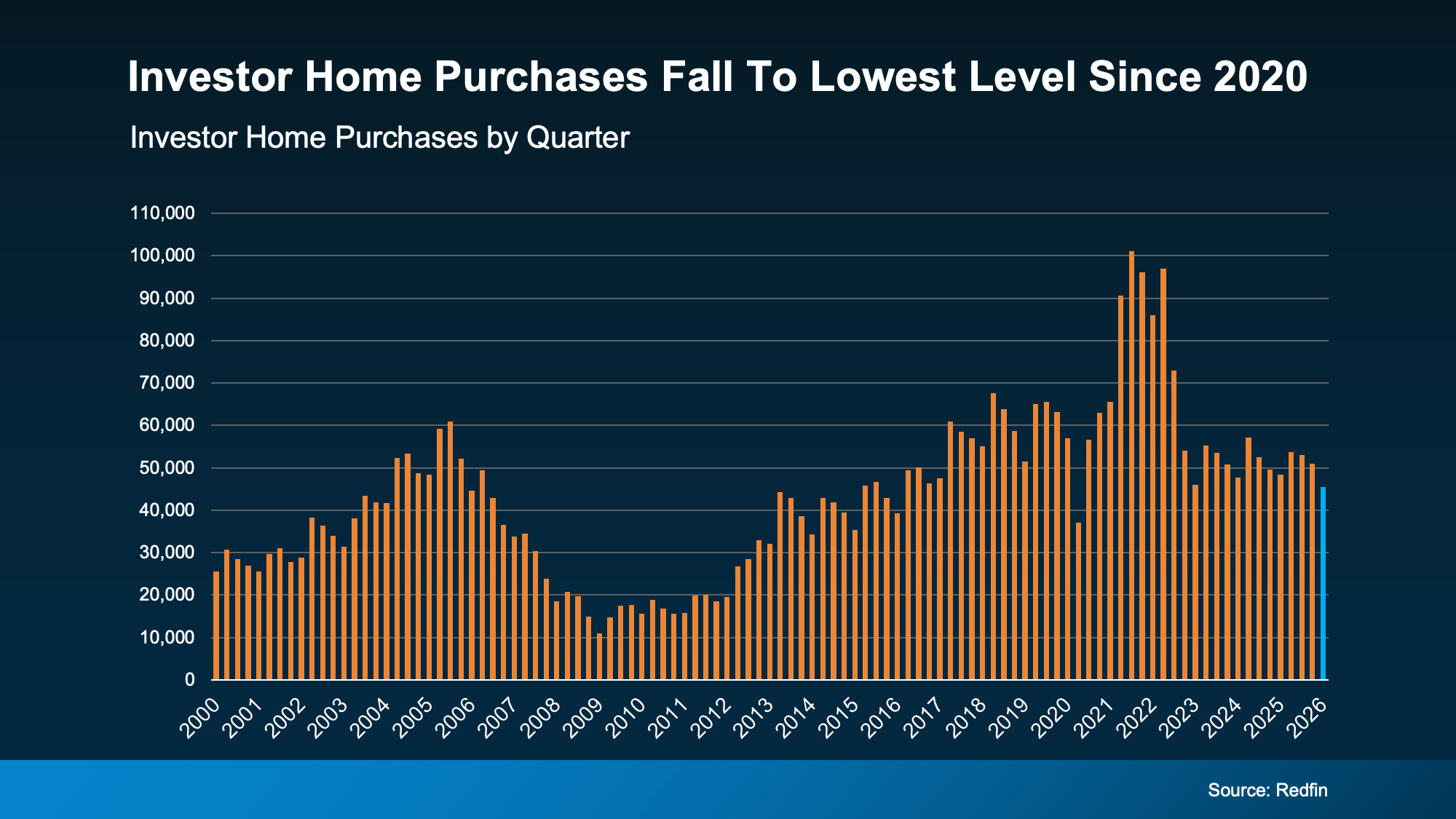

Investors Are Buying Fewer Homes Than They Have in Years

According to Redfin, investor home purchases just fell to their lowest level since 2020 – when the start of the pandemic temporarily caused pretty much all homebuying to pull way back. Before that, you’d have to go all the way back to 2016 to find a time when investors bought this few homes (see graph below):

Why the step back? Two big reasons.

First, Washington passed a housing law that takes aim at large institutional investors. To be clear, these mega investors were never as big a part of the market as the headlines made it sound. They’ve always made up a relatively small slice of housing pie. But the law still targeted the largest ones, and it worked fast. According to Thom Malone, Principal Economist at Cotality:

“When Washington announced its intention to curb institutional investors’ homebuying, the market reacted. . . Cotality data shows that investment by mega investors who own 1,000 or more properties retracted almost instantly.”

Second, the housing market has cooled. Price growth has slowed in much of the country, and in some markets, prices are dipping. That makes the math a lot less appealing for investors betting on quick gains. Lance Lambert, CEO of ResiClub, explains:

“Ever since rates spiked and the Pandemic Housing Boom fizzled out in spring 2022, institutional single-family rental (SFR) operators have pulled way back from buying up homes on the resale market—the math just isn’t as appealing right now. Home prices and rents are no longer ripping, holding costs (property taxes and insurance) have jumped, capital markets have shifted their attention elsewhere, and elevated materials prices make renovations expensive.”

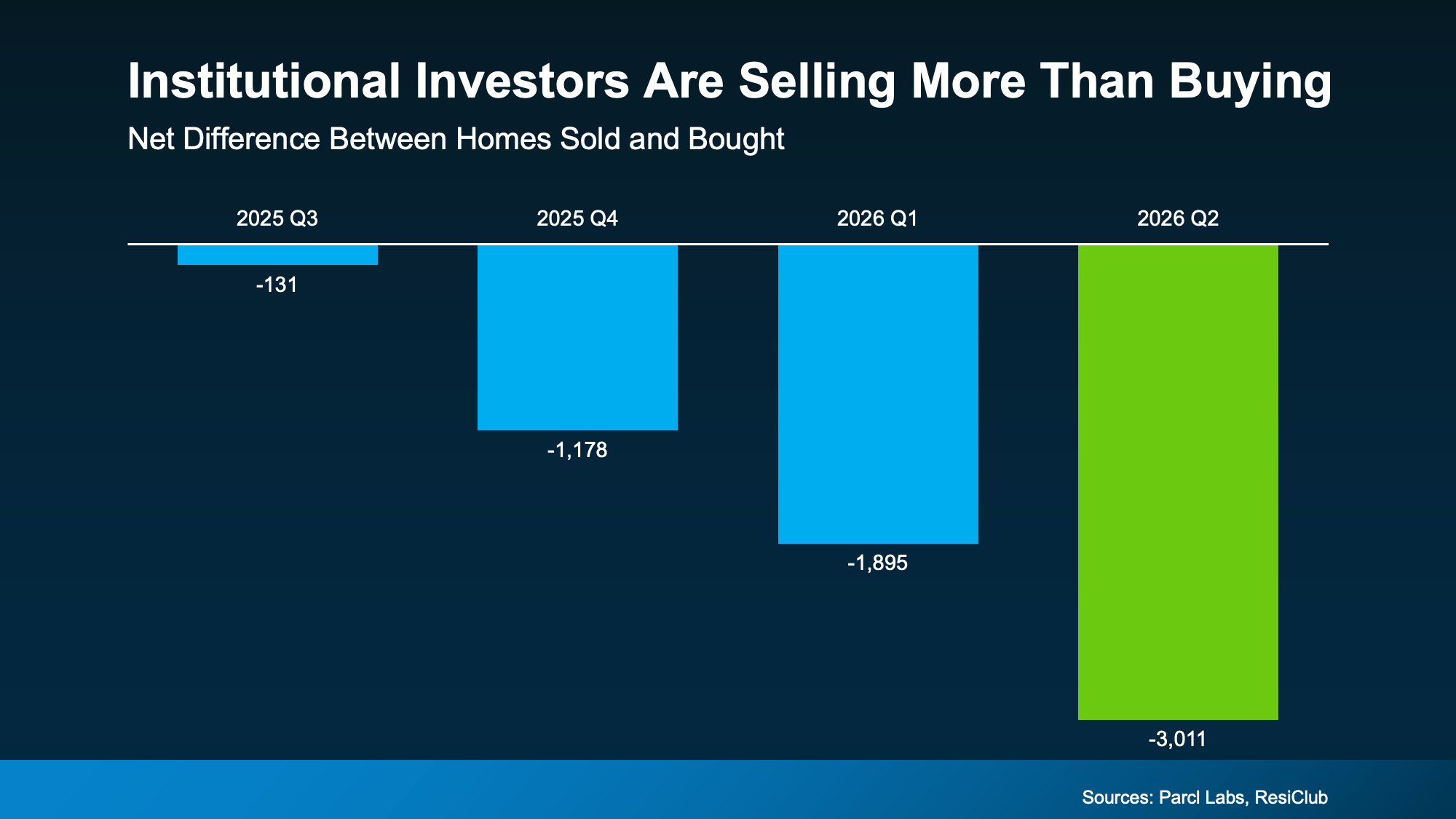

They’re Not Just Buying Less – They’re Selling More

This is the part most people miss. Big investors aren’t just slowing down their purchases. Data from Parcl Labs and ResiClub shows the largest institutional investors are now selling more homes than they’re buying – and that gap is growing these past 4 quarters (see graph below):

Every one of those homes goes right back into the market for buyers like you. And since big investors tend to own homes at the lower end of the price range, a lot of what they’re selling is exactly the kind of home first-time buyers are looking for. As Malone puts it:

“. . . this sudden dropoff in institutional investment is a signal to first-time homebuyers that there’s an opening.”

Less competition from deep-pocketed buyers. More homes hitting the market. And many of them at prices that work for a first purchase. That’s a shift that works in your favor.

Bottom Line

Big investors are stepping back, and they’re adding homes to the market as they go. If you’ve been waiting for a better shot at buying, this could be it. Connect with a local agent to find out what’s popping up in your area. You may have more options than you think.

If buying a home is on your radar, you’ve probably been keeping an eye on mortgage rates and home prices. But don’t forget about homeowners insurance.

Homeowners insurance has always been part of owning a home. But over the past few years, it’s become a larger expense for many homeowners – something that’s especially frustrating when affordability already feels tight.

The good news? While premiums are still rising, the latest data shows those increases are beginning to slow. Here’s what buyers should know.

Home Insurance Costs Have Gone Up

You’ve probably heard stories from friends or family about their premiums going up. And that’s not really a surprise when you consider data from the Pew Research Center shows 71% of homeowners say their insurance costs have gone up over the past few years.

While no one likes rising costs, knowing what to expect can help you plan ahead. Your first insurance payment is typically included in your closing costs, but after that it’ll become part of your monthly housing expenses.

Getting an insurance quote early can help you build a more realistic budget and avoid surprises later.

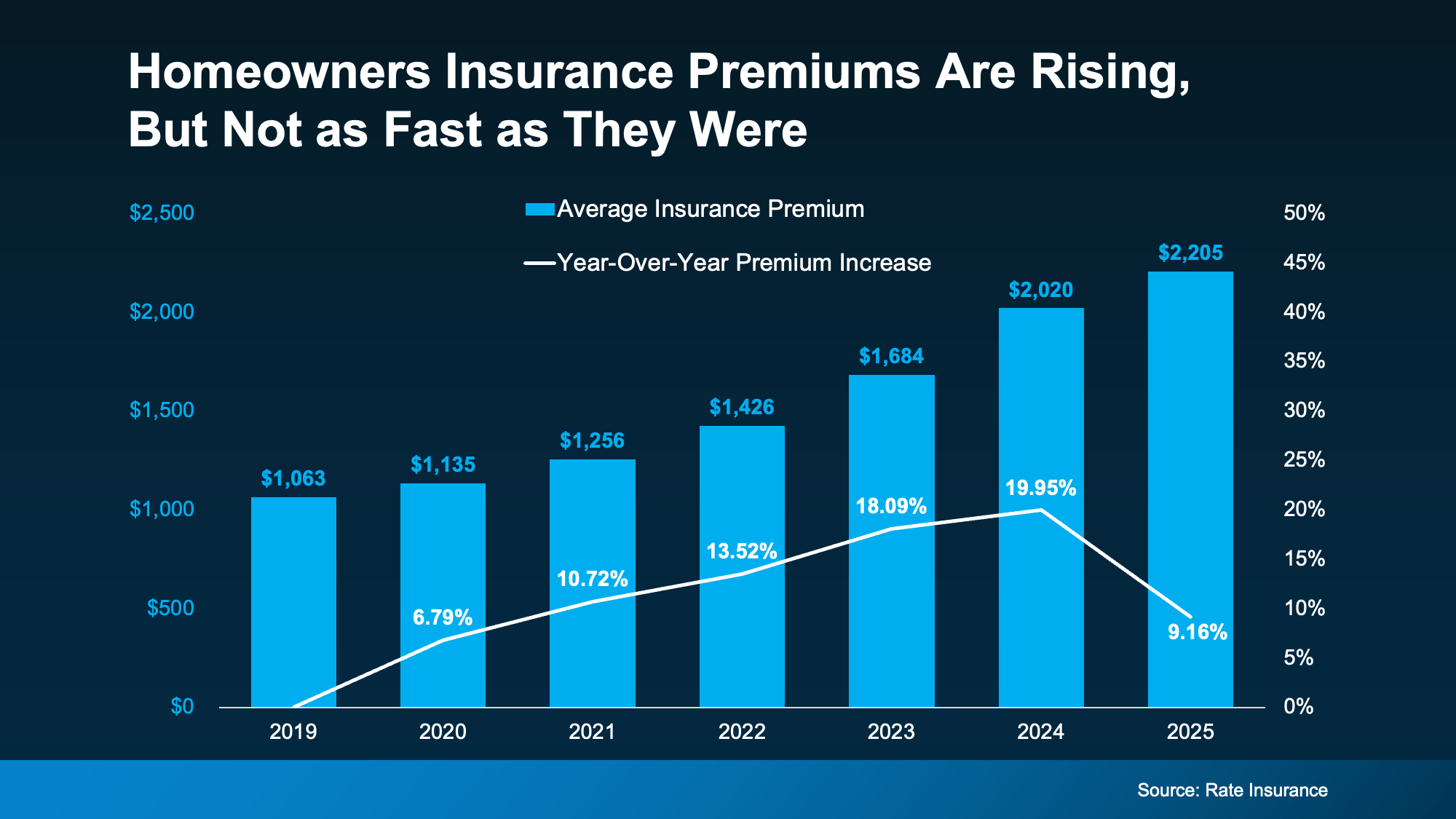

Premiums Are Rising, But Not as Fast as They Were

Most of the headlines focus on how home insurance is getting more expensive. And that’s true. But here’s the part that’s easy to miss.

Insurance premiums are still rising.

But they’re not rising as fast as they were.

According to the latest report from Rate Insurance, 2025 saw the first slowdown in annual premium increases since 2019 (see graph below):

That doesn’t mean premiums are getting cheaper. It simply means the rapid increases of the past several years may finally be starting to ease – a small but welcome step in the right direction.

But what you’ll pay in one part of the country can look very different from what someone pays somewhere else.

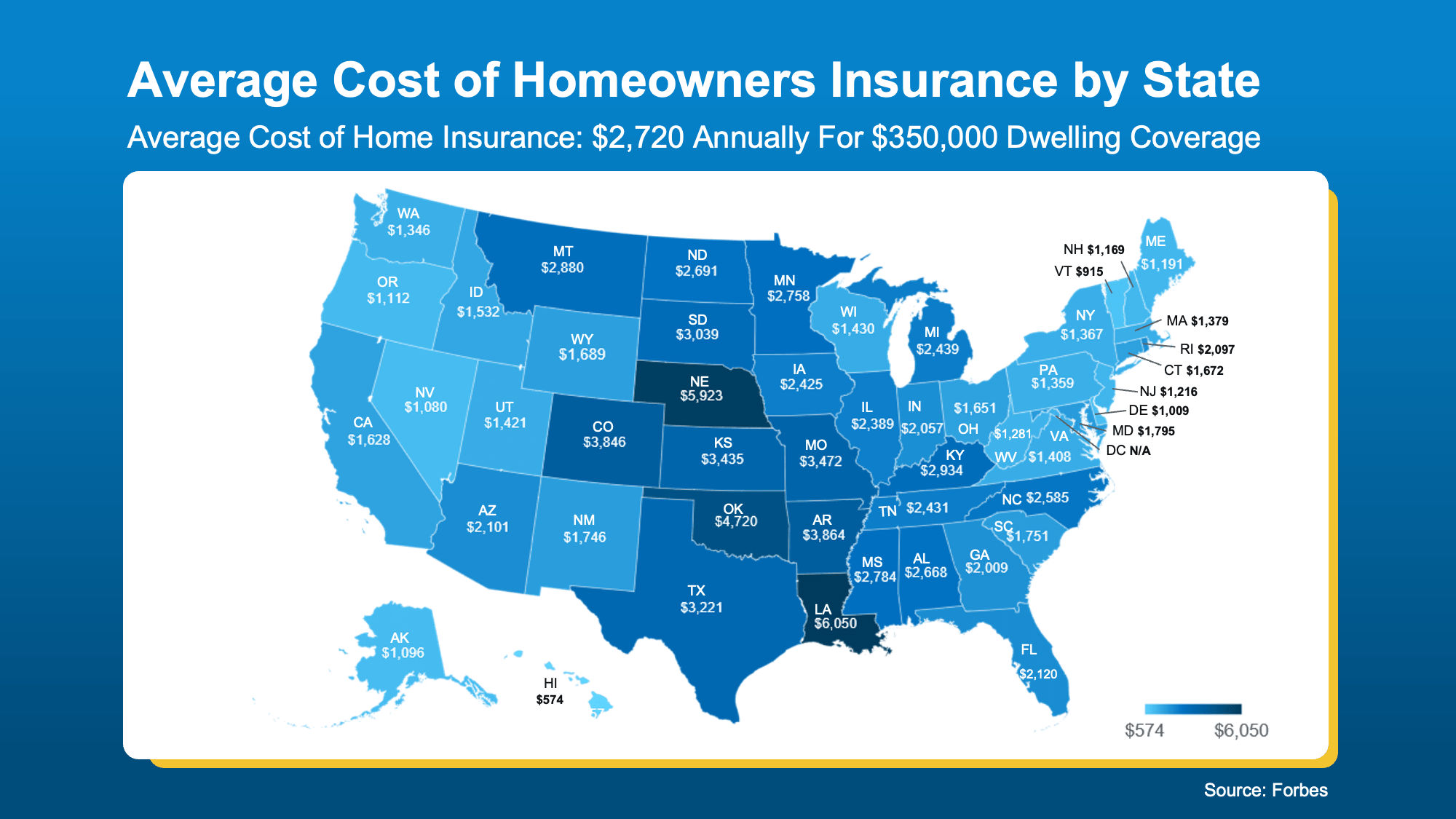

Where You Buy Can Make a Big Difference

Insurance costs vary because some parts of the country experience more claims than others. That’s why it’s important to look at what’s happening locally.

Your premium will depend on things like where you’re buying, the home itself, and the coverage you choose.

Forbes data can give a rough idea of your state’s typical premiums. Check out the map below – the darker the blue, the higher the costs tend to be in that state:

Ways To Lower Your Costs

While you can’t control every cost that comes with buying a home, you can control how prepared you are. If you’re crunching the numbers and trying to find ways to save, Insurify and NerdWallet offer these tips that can help you get the best insurance price possible:

-

Shop Around – Compare quotes from multiple companies.

-

Bundle Policies – Combine home and auto to see if a bundle price is cheaper.

-

Ask If There Are Discounts – Don’t miss out on savings you may qualify for.

-

Highlight Upgrades – Features like a new roof or storm windows can cut costs.

-

Improve Your Credit – A stronger credit score can mean better premiums.

One of the smartest things you can do is get an insurance quote before you make an offer. That way, you’ll know what your monthly housing costs are likely to be before you commit.

An insurance professional can walk you through your options and help you find coverage that fits both your needs and your budget.

Bottom Line

Homeowners insurance has become a bigger part of the homebuying conversation. But it doesn’t have to become a bigger source of stress.

The key is knowing what to expect before you buy. Get an insurance quote early, factor it into your budget, and lean on trusted local professionals to help you make the most informed decision possible.

Thinking About Waiting for Lower Mortgage Rates? Read This First.

Big Investors Are Backing Off and That’s Your Opening

Here’s Where To Start if You’re Selling and Buying at the Same Time

-

For Sellers4 weeks ago

For Sellers4 weeks agoThink Nobody’s Buying Homes Right Now? Think Again.

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

-

First-Time Buyers3 weeks ago

First-Time Buyers3 weeks ago14 Years Running: Why Real Estate Is Still America’s Favorite Investment

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoMore Homes, Better Prices: A Buyer’s Summer

-

Equity2 weeks ago

Equity2 weeks agoThe House That Started It All Could Kickstart What’s Next

-

Affordability3 weeks ago

Affordability3 weeks agoPriced Out? A Condo or Townhome Could Be Your Way In.

-

For Sellers2 weeks ago

For Sellers2 weeks agoSelling a Luxury House? Here’s Why Now Is a Good Time

-

Affordability1 week ago

Affordability1 week agoBuying a Home? Here’s What You Should Know About Home Insurance Costs.

You must be logged in to post a comment Login