Housing Market Updates

Exploring the Future of Mortgage Rates: What Homebuyers Need to Know

For those embarking on the journey to buy a home this year, mortgage rates are likely a top-of-mind concern. It’s no surprise since these rates have a significant impact on what you can afford when securing a home loan. In a housing market where affordability is a pressing issue, it’s a good time to take a step back and analyze the broader historical context of mortgage rates in comparison to their present state. Furthermore, delving into their connection with inflation can provide valuable insights into the potential trajectory of mortgage rates in the near future.

Putting Sticker Shock into Perspective

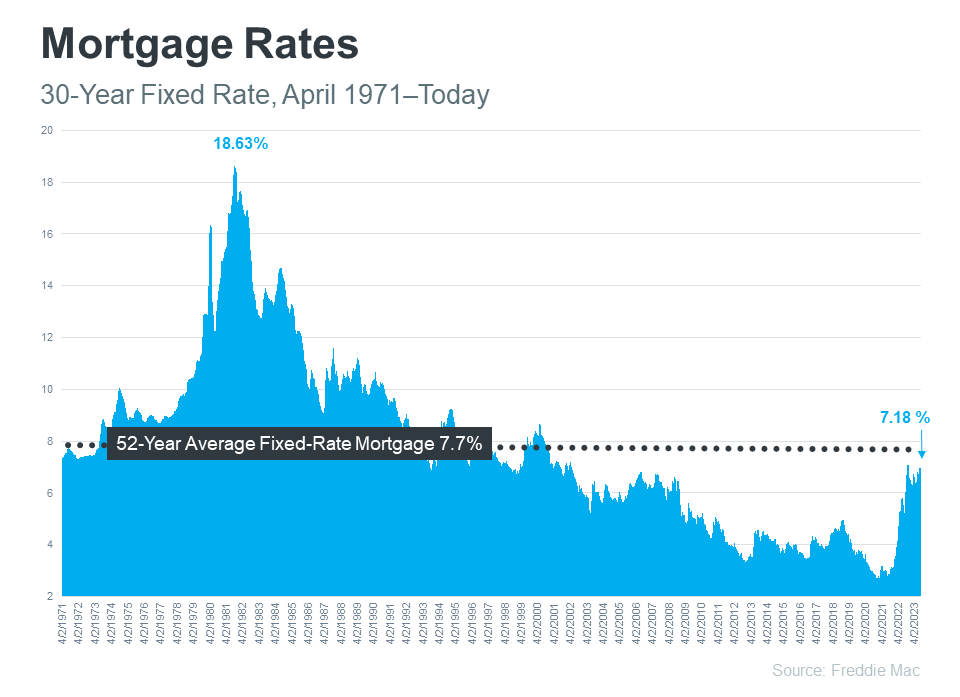

Freddie Mac has been diligently tracking the 30-year fixed mortgage rate since April of 1971. On a weekly basis, they publish the results of their Primary Mortgage Market Survey, which amalgamates mortgage application data from lenders across the nation (refer to the graph below):

Examining the right side of the graph, it becomes apparent that mortgage rates have seen a notable increase since the onset of the previous year. However, even with this upswing, today’s rates still linger below the 52-year average. While this historical context is informative, most homebuyers have grown accustomed to mortgage rates hovering between 3% and 5%—a range that has prevailed for the past 15 years.

This familiarity with lower rates elucidates why the recent surge might be causing sticker shock, even though rates are, by historical standards, near their long-term average. While many buyers have adapted to the higher rates that have persisted over the past year, a slight dip in rates would certainly be a welcome development. To ascertain the feasibility of this, it is crucial to factor in the variable of inflation.

Where Might Mortgage Rates Head in the Future?

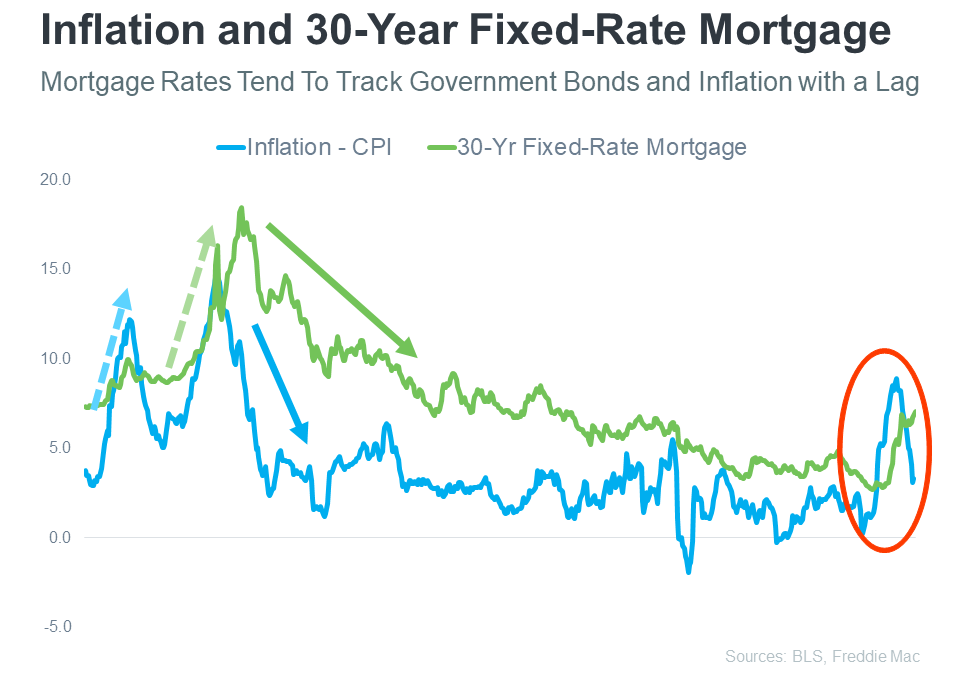

The Federal Reserve has been diligently engaged in efforts to quell inflation since the early part of 2022. This holds significance because, historically, there has been a discernible link between inflation and mortgage rates (refer to the graph below):

The graph vividly illustrates a fairly consistent relationship between inflation and mortgage rates. On the left side of the graph, each significant shift in inflation (highlighted in blue) is closely followed by a corresponding adjustment in mortgage rates (depicted in green).

The circled segment of the graph draws attention to the recent inflation surge, with mortgage rates showing a concurrent response. While inflation has shown signs of moderating somewhat this year, mortgage rates have not mirrored the same pattern.

Consequently, if history offers any guidance, it implies that the market is awaiting a scenario in which mortgage rates align with the trajectory of inflation and begin to recede. While it’s impossible to make precise predictions regarding mortgage rates, the evidence suggests that moderating inflation could portend a forthcoming dip in mortgage rates, consistent with a well-established trend.

In Conclusion

In order to gauge the potential path of mortgage rates, it is instructive to examine their historical journey. There exists a clear, proven correlation between inflation and mortgage rates, and if this historical link remains valid, the recent moderation in inflation might bode well for the future of mortgage rates and your aspirations of homeownership.

Have you heard the term “Silver Tsunami” getting tossed around recently? If so, here’s what you really need to know. That phrase refers to the idea that a lot of baby boomers are going to move or downsize all at once. And the fear is that a sudden influx of homes for sale would have a big impact on housing. That’s because it would create a whole lot more competition for smaller homes and would throw off the balance of supply and demand, which ultimately would impact home prices.

But here’s the thing. There are a couple of faults in that logic. Let’s break them down and put your mind at ease.

Not All Baby Boomers Plan To Move

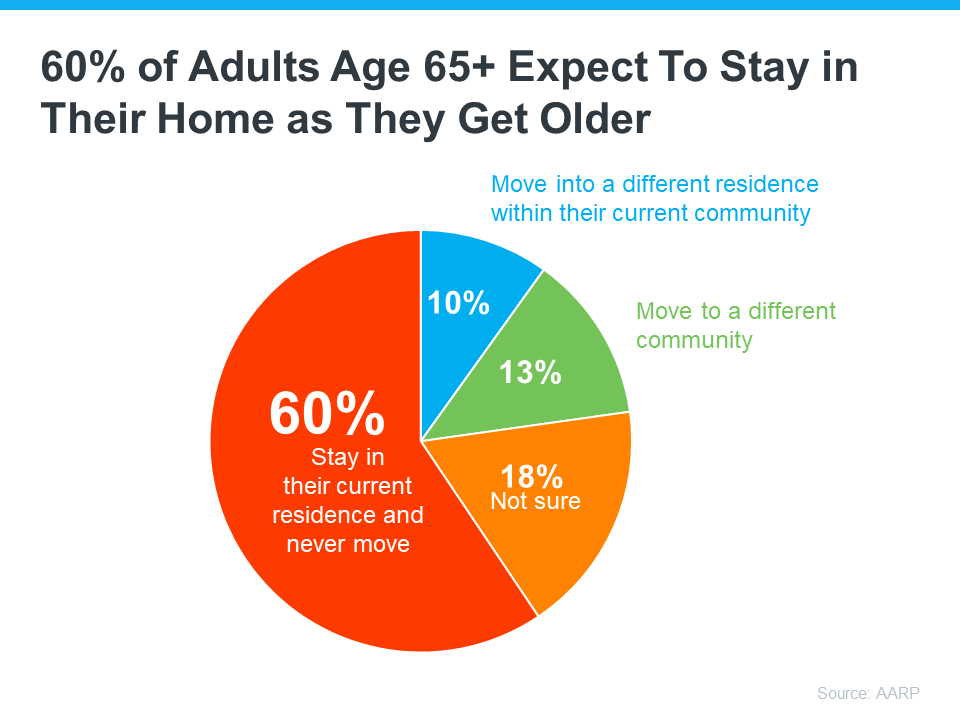

For starters, plenty of baby boomers don’t plan on moving at all. A study from the AARP says more than half of adults aged 65 and older want to stay in their homes and not move as they age (see graph below):

While it’s true circumstances may change and some people who don’t plan to move (the red in the chart above) may realize they need to down the road, the vast majority are counting on aging in place.

As for those who stay put, they’ll likely modify their homes as their needs change over time. And when updating their existing home won’t work, some will buy a second home and keep their original one as an investment to fuel generational wealth for their loved ones. As an article from Inman explains:

“Many boomers have no desire to retire fully and take up less space . . . Many will modify their current home, and the wealthiest will opt to have multiple homes.”

Even Those Who Do Move Won’t Do It All at Once

While not all baby boomers are looking to sell their homes and move – the ones who do won’t all do it at the same time. Instead, it’ll happen slowly over many years. As Freddie Mac says:

“We forecast the ‘tsunami’ will be more like a tide, bringing a gradual exit of 9.2 million Boomers by 2035 . . .”

As Mark Fleming, Chief Economist at First American, says:

“Demographics are never a tsunami. The baby boomer generation is almost two decades of births. That means they’re going to take about two decades to work their way through.”

Bottom Line

If you’re stressed about a Silver Tsunami shaking the housing market overnight, don’t be. Baby boomers will move slowly over a much longer period of time.

Some Highlights

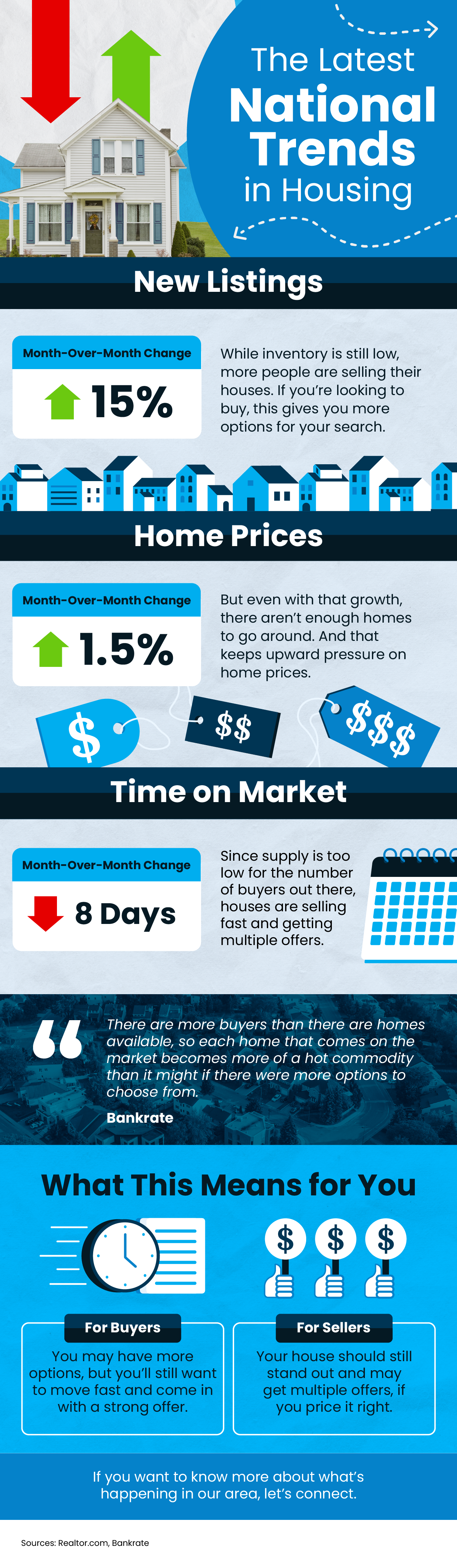

- With the number of new listings going up and average days on market going down, buyers may have more options, but will still want to move fast.

- For sellers, inventory is still low and houses are selling fast, meaning your house should stand out and may get multiple offers if you price it right.

- If you want to know more about what’s happening in your area, connect with a local real estate agent.

There’s been a lot of recession talk over the past couple of years. And that may leave you worried we’re headed for a repeat of what we saw back in 2008. Here’s a look at the latest expert projections to show you why that isn’t going to happen.

According to Jacob Channel, Senior Economist at LendingTree, the economy’s pretty strong:

“At least right now, the fundamentals of the economy, despite some hiccups, are doing pretty good. While things are far from perfect, the economy is probably doing better than people want to give it credit for.”

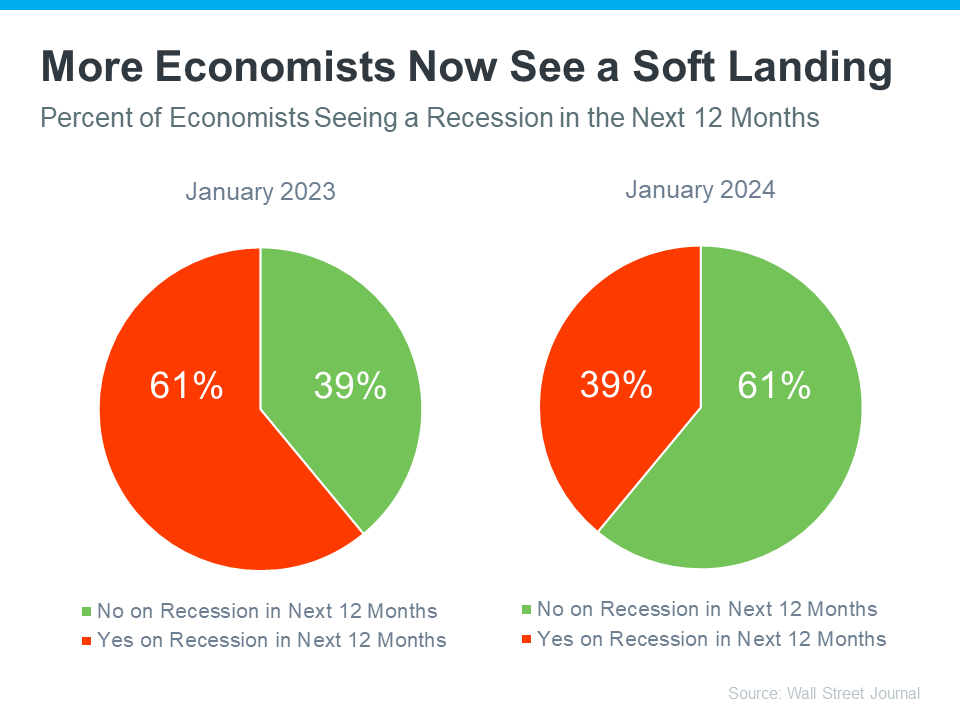

That might be why a recent survey from the Wall Street Journal shows only 39% of economists think there’ll be a recession in the next year. That’s way down from 61% projecting a recession just one year ago (see graph below):

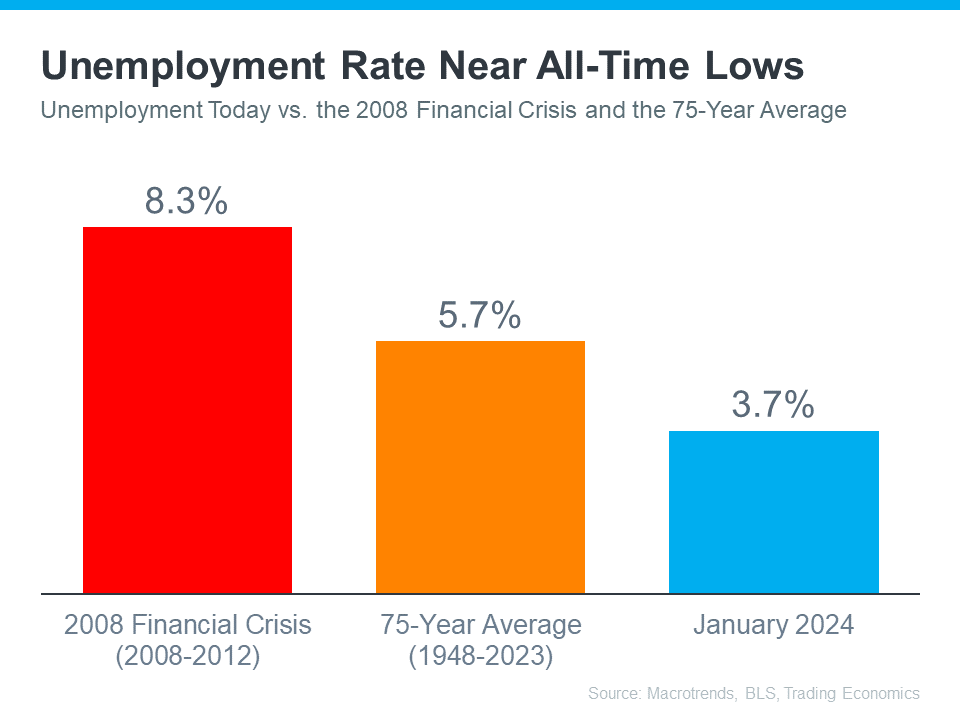

Most experts believe there won’t be a recession in the next 12 months. One reason why is the current unemployment rate. Let’s compare where we are now with historical data from Macrotrends, the Bureau of Labor Statistics (BLS), and Trading Economics. When we do, it’s clear the unemployment rate today is still very low (see graph below):

The orange bar shows the average unemployment rate since 1948 is about 5.7%. The red bar shows that right after the financial crisis in 2008, when the housing market crashed, the unemployment rate was up to 8.3%. Both of those numbers are much larger than the unemployment rate this January (shown in blue).

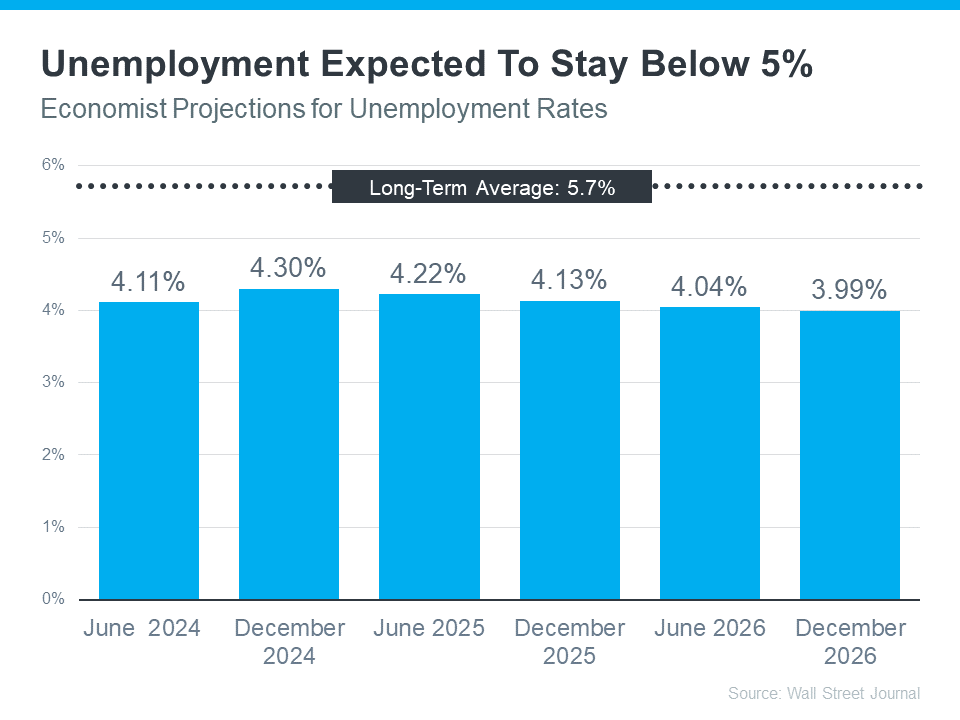

But will the unemployment rate go up? To answer that, look at the graph below. It uses data from that same Wall Street Journal survey to show what the experts are projecting for unemployment over the next three years compared to the long-term average (see graph below):

As you can see, economists don’t expect the unemployment rate to even come close to the long-term average over the next three years – much less the 8.3% we saw when the market last crashed.

Still, if these projections are correct, there will be people who lose their jobs next year. Anytime someone’s out of work, that’s a tough situation, not just for the individual, but also for their friends and loved ones. But the big question is: will enough people lose their jobs to create a flood of foreclosures that could crash the housing market?

Looking ahead, projections show the unemployment rate will likely stay below the 75-year average. That means you shouldn’t expect a wave of foreclosures that would impact the housing market in a big way.

Bottom Line

Most experts now think we won’t have a recession in the next year. They also don’t expect a big jump in the unemployment rate. That means you don’t need to fear a flood of foreclosures that would cause the housing market to crash.

The 1 Factor That Explains Everything Happening with Home Prices Right Now

Your House Didn’t Sell. Here’s How To Turn It Around.

More Sellers Are Taking Their Homes off the Market. Here’s What You Need To Know.

-

Affordability4 weeks ago

Affordability4 weeks agoWhat Rising Inflation Means for Your Move

-

Economy4 weeks ago

Economy4 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability4 weeks ago

Affordability4 weeks agoLess House, More Home: Why Smaller Homes Are Paying Off for Today’s Buyers

-

Affordability3 weeks ago

Affordability3 weeks agoCould Moving a Bit Further Out Change Everything About Your Budget?

-

Buying Tips3 weeks ago

Buying Tips3 weeks agoTwo Big Reasons To Move This Summer

-

Affordability3 weeks ago

Affordability3 weeks agoLower Asking Prices Are a Win for Today’s Buyers

-

For Sellers2 weeks ago

For Sellers2 weeks agoShould You Pay for Your Buyer’s Closing Costs? What Sellers Need To Know.

-

For Buyers2 weeks ago

For Buyers2 weeks agoThink Home Prices Will Crash? Here’s What the Experts Actually Expect.

You must be logged in to post a comment Login